|

시장보고서

상품코드

2043693

위조 방지 포장 시장 예측(-2031년) : 기술별, 최종 용도 산업별, 지역별Anti-Counterfeit Packaging Market by Technology (Mass Encoding, RFID, Hologram, Tamper Evidence, Forensic Markers), End-use Industry (Food & Beverage, Pharmaceutical, Personal Care, Apparel & Footwear, Luxury Goods), and Region - Global Forecast to 2031 |

||||||

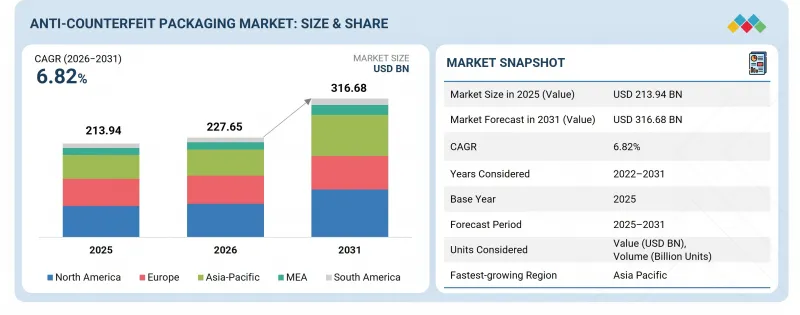

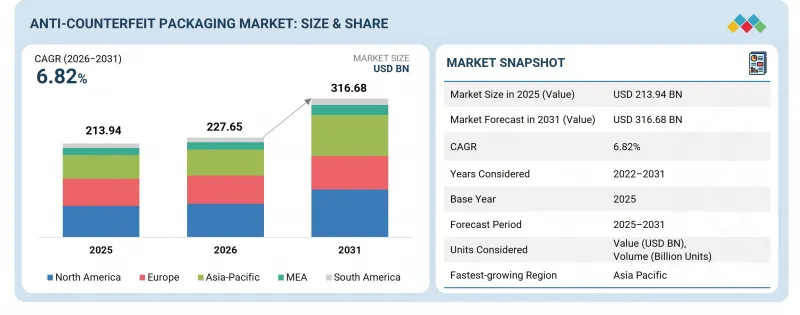

위조 방지 포장 시장 규모는 2026년 2,276억 5,000만 달러에서 2031년까지 3,166억 8,000만 달러로 성장하며, 예측 기간 중 CAGR은 6.82%에 달할 것으로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러)/수량(10억 단위) |

| 부문 | 기술별, 최종 용도 산업별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

위조 방지 포장에 대한 수요는 전 세계에서 증가하고 있는 의약품 관련 범죄, 소매업체들의 위조 방지 포장 채택 확대, 다양한 산업에서 시행되고 있는 엄격한 포장 관련 규제에 기인합니다.

"RFID 부문은 예측 기간 중 두 번째로 큰 시장 규모가 될 것으로 예상됩니다. "

무선 주파수 식별(RFID) 기술은 저비용의 대량 인코딩보다 우수한 자동화 및 실시간 모니터링 기능을 제공하므로 시장 점유율 2위를 차지하고 있습니다. RFID는 시야 내에서 스캔할 필요가 없고, 여러 개의 태그를 읽을 수 있으며, 실시간 추적이 가능하므로 소매, 물류, 제약 등의 산업에서 가치가 있습니다. Zebra Technologies와 Avery Dennison은 수년간 태그의 성능 향상과 비용 절감을 통해 RFID의 대중화를 주도해 왔습니다. 그러나 RFID는 여전히 전용 하드웨어(리더기, 안테나, 미들웨어)가 필요하고, 이익률이 낮고 대량 생산되는 시장에서는 인쇄된 코드에 비해 규모 확대가 어렵습니다. 하지만 위조 방지, 재고 관리, 옴니채널 대응 기능으로 인해 중고가 제품, 특히 의류 및 전자제품에서 선호되고 있습니다. IoT 및 분석 기능과의 통합이 진행됨에 따라 더 많은 부가가치가 창출되고 있습니다. 비용 하락과 규제 강화에 따라 RFID는 빠르게 성장하고 있습니다.

"식품 및 음료 부문은 예측 기간 중 두 번째로 큰 시장 규모가 될 것으로 예상됩니다. "

식품 및 음료 부문은 식품 안전, 브랜드 신뢰도 및 규제 요건에 대한 우려가 높아짐에 따라 위조 방지 포장에 대한 두 번째로 큰 수요처가 되었습니다. 인체의 건강에 미치는 영향은 심각하지만, 일반적으로 의약품만큼 긴급성은 높지 않습니다. 유럽식품안전청(EFSA), 미국 식품의약국(FDA) 등 규제 당국은 라벨링, 추적성 및 안전 규제를 의무화하고 있으며, 이는 위조 방지 솔루션의 필요성에 힘을 실어주고 있습니다. 이 산업은 위조, 허위 표시(예: 와인 및 올리브 오일의 원산지 사기) 및 위조 명품의 문제에 시달리고 있습니다. QR코드, 위변조 방지 실, 블록체인을 활용한 진위 확인 및 추적성이 도입되어 있습니다. 또한 국제 무역과 EC를 통한 식료품 소매업의 확대로 인해 업계는 사기의 위험에 노출되기 쉬워졌다. 그러나 이익률이 높지 않고, 의약품처럼 개별 제품 단위의 규제가 엄격하지 않기 때문에 RFID와 같은 첨단 기술이 모든 제품군에 도입되기에는 제약이 있습니다. 그럼에도 불구하고 프리미엄화와 투명성에 대한 니즈가 견고한 성장률을 견인하고 있으며, 이 시장은 세계 2위의 시장으로 자리매김하고 있습니다.

"예측 기간 중 유럽은 두 번째로 큰 시장이 될 것으로 예상됩니다. "

유럽은 탄탄한 규제 프레임워크, 소비자 의식, 제조 능력을 갖춘 위조방지 포장 시장에서 세계 2위의 규모를 자랑합니다. 유럽의약품청(EMA)이 관할하는 '위조 의약품 지침'을 비롯한 엄격한 규제가 확립되어 있으며, 의약품에 대한 시리얼라이제이션 및 변조 방지 조치가 의무화되어 있습니다. 마찬가지로 유럽식품안전청(EFSA)과 같은 기관도 식품의 진위 여부와 추적 가능성에 대한 엄격한 기준을 유지하고 있습니다. 또한 유럽에는(패션, 화장품, 와인 등) 대규모 고급품 시장이 존재하지만 위조 위험에 노출되어 있으며, RFID, 디지털 워터마크 등 첨단 포장 기술이 요구되고 있습니다. 또한 유럽에서는 지속가능하고 스마트한 포장의 적극적인 도입으로 혁신을 주도하고 있습니다. 이러한 규제 환경, 고부가가치 제품, 그리고 기술 혁신이 결합되어 유럽은 위조 방지 포장 시장 규모에서 2위를 차지하고 있습니다.

대상 기업 - CCL Industries Inc.(캐나다), 3M(미국), SATO Corporation(일본), Zebra Technologies Corporatio(미국), SICPA Holding SA(스위스), Intelligent Label Solutions(영국), SML Group(중국), Dover Corporation(미국), AlpVision SA(스위스), Authentix Inc.(미국) 등이 이 보고서의 대상입니다.

위조방지 포장 시장의 주요 기업에 대해 기업 개요, 최근 동향, 주요 시장 전략을 포함한 상세한 경쟁 분석을 실시했습니다.

조사 범위

위조방지 포장 시장을 기술(매스인코딩, RFID, 홀로그램, 변조방지, 감식용 마커, 기타 기술), 최종사용 산업(식품 및 음료, 제약, 퍼스널케어, 전자/전기, 자동차, 의류/신발, 럭셔리, 기타 최종사용 산업), 지역(아시아, 북미, 유럽, 아시아태평양, 중동, 아프리카, 유럽, 아시아태평양, 중동/아프리카) 등으로 분류하여 분석했습니다. 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)으로 분류하고 있습니다. 이 보고서의 조사 범위에는 위조 방지 포장 시장의 성장에 영향을 미치는 촉진요인, 제약 조건, 과제 및 기회에 대한 자세한 정보가 포함되어 있습니다. 주요 업계 플레이어에 대한 심층 분석을 통해 사업 개요, 제공 제품 및 위조 방지 포장 시장과 관련된 파트너십, 제휴, 제품 출시, 사업 확장, 인수와 같은 주요 전략에 대한 인사이트를 제공합니다. 이 보고서에서는 위조방지 포장 시장 생태계에서 떠오르고 있는 스타트업 기업의 경쟁 구도에 대한 인사이트도 다루고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 시장 리더와 신규 진입자에게 전체 위조 방지 포장 시장 및 각 하위 부문의 매출에 대한 가장 정확한 추정치를 제공합니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 비즈니스 포지셔닝을 위한 인사이트를 높이고, 적절한 시장 진입 전략을 수립하는 데 도움이 될 것입니다. 또한 시장 동향을 파악하고 주요 시장 촉진요인, 제약 조건, 과제 및 기회에 대한 정보를 제공합니다.

이 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다. :

주요 촉진요인(의약품 범죄 환경의 변화, 엄격한 규제 도입, 위조 방지에 대한 소매 체인의 적극적인 참여, 브랜드 보호에 대한 제조업체의 집중도 증가), 제약 요인(위조 활동의 복잡성, 막대한 초기 투자), 기회(기술의 지속적인 발전, 다양한 산업별 맞춤형 솔루션, 신흥 국가 수요 증가), 도전 과제(소비자 이해의 장벽, 높은 연구개발 투자, 지속되는 서방 분쟁의 영향)에 대한 분석. 솔루션, 신흥 시장의 수요 증가), 도전과제(소비자 이해의 장벽, 높은 R&D 투자, 지속되는 서아시아 분쟁의 영향)에 대한 분석.

- 제품 개발/혁신: 위조방지 포장 시장의 미래 기술, R&D 활동, 제품 및 서비스 출시에 대한 심층적인 인사이트

- 시장 개발: 수익성 높은 시장에 대한 포괄적인 정보 - 이 보고서는 다양한 지역의 위조 방지 포장 시장을 분석합니다.

시장 다각화: 위조방지 포장 시장의 신제품 및 서비스, 미개발 지역, 최근 동향 및 투자에 대한 포괄적인 정보

- 경쟁 분석 : 주요 기업 - CCL Industries Inc.(캐나다), 3M(미국), SATO Corporation(일본), Zebra Technologies Corporation(미국), SICPA Holding SA(스위스), Intelligent Label Solutions(영국), SML Group(중국), Dover Corporation(미국), AlpVision SA(스위스), Authentix Inc.(미국) 등 주요 기업의 시장 점유율, 성장 전략, 서비스 제공에 관한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 위조 방지 포장 시장(기술별)

제10장 위조 방지 포장 시장(최종 용도 산업별)

제11장 위조 방지 포장 시장(지역별)

제12장 경쟁 구도

제13장 기업 개요

제14장 조사 방법

제15장 부록

KSA 26.06.05The anti-counterfeit packaging market is projected to grow from USD 227.65 billion in 2026 to USD 316.68 billion by 2031, at a CAGR of 6.82% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) / Volume (Billion Units) |

| Segments | Technology, End-Use Industry and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

The demand for anti-counterfeit packaging is attributed to the evolving pharmaceutical crimes happening globally, the rising adoption of anti-counterfeit packaging by retailers, and the strict regulations being implemented for packaging in various industries.

"The RFID segment is projected to be the second-largest segment during the forecast period."

Radio frequency identification (RFID) technology has the second-highest market share as it provides better automation and real-time monitoring capabilities than low-cost mass encoding. RFID allows scanning without line-of-sight, reading multiple tags and real-time tracking - making it valuable for industries such as retail, logistics, and pharmaceuticals. Zebra Technologies and Avery Dennison have driven adoption through performance improvements and cost reduction of tags over time. But RFID still needs dedicated hardware (readers, antennas, middleware), making it harder to scale in low-margin/high volume markets than printed codes. However, its anti-counterfeiting, inventory management, and omnichannel capabilities have made it a favorite for mid-to-high value products, especially clothing and electronics. Greater integration with IoT and analytics adds value. RFID is rapidly growing as costs are reducing and legislation is increasing.

"The food & beverage segment is projected to be the second-largest segment during the forecast period."

The food & beverage sector is the second-largest consumer of anti-counterfeit packaging because of increasing concerns regarding food safety, brand integrity, and regulatory requirements. Though the impact on human health is severe, it's usually not as urgent as pharmaceuticals. Regulators such as the European Food Safety Authority and the U.S. Food and Drug Administration mandate labeling, traceability, and safety regulations, driving the need for anti-counterfeit solutions. The industry is plagued by adulteration, mislabeling (e.g., geographical fraud in wine and olive oil) and fake luxury products. Authentication and traceability through QR codes, tamper-proof seals, and blockchain are deployed. Moreover, global trade and e-commerce grocery retailing have further exposed the industry to fraud. But profit margins are not high, and unit-level enforcement is not as strict as with pharmaceuticals, restricting the adoption of high-end technologies such as RFID across all product segments. However, premiumization and the need for transparency are driving good growth rates, establishing its position as the second-biggest market.

"Europe is projected to be the second-largest market during the forecast period."

Europe is the second-largest market for anti-counterfeit packaging, with a robust regulatory framework, consumer awareness, and manufacturing capabilities. It has established stringent regulations, including the Falsified Medicines Directive, administered by the European Medicines Agency, requiring serialization and tamper-evident measures for medicines. Likewise, bodies such as the European Food Safety Authority maintain rigorous food authenticity and traceability standards. Europe is also home to a large luxury goods market (e.g., fashion, cosmetics, wines) that is at risk of counterfeiting and requires sophisticated packaging technologies such as the use of RFID and digital watermarking. Europe is further driving innovation with the robust adoption of sustainable and smart packaging. This regulatory, high-value product and technological innovation make Europe the second-largest market for anti-counterfeit packaging.

Break-up of primary participants for the report:

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: CCL Industries Inc. (Canada), 3M (US), SATO Corporation (Japan), Zebra Technologies Corporation (US), SICPA Holding SA (Switzerland), Intelligent Label Solutions (UK), SML Group (China), Dover Corporation (US), AlpVision SA (Switzerland), and Authentix Inc. (US), among others, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the anti-counterfeit packaging market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the anti-counterfeit packaging market based on technology (mass encoding, RFID, hologram, tamper evidence, forensic markers, other technologies), end-use industry (food & beverage, pharmaceutical, personal care, electronics & electrical, automotive, apparel & footwear, luxury goods, other end-use industries), and region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the anti-counterfeit packaging market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as partnerships, collaborations, product launches, expansions, and acquisitions, associated with the anti-counterfeit packaging market. This report covers a competitive analysis of upcoming startups in the anti-counterfeit packaging market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall anti-counterfeit packaging market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (Evolving pharmaceutical crime landscape, Implementation of stringent regulations, Proactive involvement of retail chains in combating counterfeiting, Increasing manufacturer focus on brand protection), restraints (Growing complexity of counterfeit operations, Significant initial investment), opportunities (Ongoing developments in technologies, customized solutions across various industries, Increasing demand from emerging markets), and challenges (Barriers to consumer understanding, High R&D investment, Ongoing West Asia war impact).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the anti-counterfeit packaging market

- Market Development: Comprehensive information about profitable markets - the report analyzes the anti-counterfeit packaging market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the anti-counterfeit packaging market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such CCL Industries Inc. (Canada), 3M (US), SATO Corporation (Japan), Zebra Technologies Corporation (US), SICPA Holding SA (Switzerland), Intelligent Label Solutions (UK), SML Group (China), Dover Corporation (US), AlpVision SA (Switzerland), and Authentix Inc. (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ANTI-COUNTERFEIT PACKAGING MARKET

- 3.2 NORTH AMERICA: ANTI-COUNTERFEIT PACKAGING MARKET, BY TECHNOLOGY AND COUNTRY

- 3.3 ANTI-COUNTERFEIT PACKAGING MARKET, BY TECHNOLOGY

- 3.4 ANTI-COUNTERFEIT PACKAGING MARKET, BY END-USE INDUSTRY

- 3.5 ANTI-COUNTERFEIT PACKAGING MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Evolving pharmaceutical crime landscape

- 4.2.1.2 Implementation of stringent regulations

- 4.2.1.3 Proactive involvement of retail chains in combating counterfeiting

- 4.2.1.4 Increasing manufacturer focus on brand protection

- 4.2.2 RESTRAINTS

- 4.2.2.1 Growing complexity of counterfeit operations

- 4.2.2.2 Significant initial investment

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Ongoing technological developments

- 4.2.3.2 Customized solutions across various industries

- 4.2.3.3 Increasing demand from emerging markets

- 4.2.4 CHALLENGES

- 4.2.4.1 Barriers to consumer understanding

- 4.2.4.2 High R&D investment

- 4.2.4.3 Ongoing West Asia war impact

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 INTELLIGENT AUTHENTICATION & CONSUMER ENGAGEMENT

- 4.3.2 INTEROPERABILITY & GLOBAL STANDARDIZATION

- 4.3.3 COST-EFFECTIVE & SCALABLE SECURITY SOLUTIONS

- 4.3.4 RESILIENCE AGAINST NEXT-GEN COUNTERFEITING

- 4.3.5 SUSTAINABLE & COMPLIANT SECURITY PACKAGING

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.4.2.1 Pharmaceuticals - Food & Beverage

- 4.4.2.2 Electronics - PHARMACEUTICALS

- 4.4.2.3 Luxury Goods - Personal Care

- 4.4.2.4 Automotive - Electronics

- 4.4.2.5 Luxury Goods - Apparel & Footwear

- 4.4.2.6 Electronics - Luxury Goods

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING CONSOLIDATION AND INNOVATION

- 4.5.1.1 CCL Industries, Inc. - "Acquisition of ALT Technologies"

- 4.5.1.2 SICPA (E7 Group) - "Strategic Partnership with 7i Holding"

- 4.5.2 TIER 2 PLAYERS: REGIONAL INNOVATORS AND NICHE LEADERS

- 4.5.2.1 Intelligent Label Solutions "START of Indonesian Operations"

- 4.5.2.2 SML Group - "RFID Partnership with Landmark Group"

- 4.5.3 TIER 3 PLAYERS: STRENGTHENING SUSTAINABILITYIN THE AMMONIA MARKET

- 4.5.3.1 Scantrust SA - "QR Code Anti-Counterfeiting for Marchesi Antinori"

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING CONSOLIDATION AND INNOVATION

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.4 THREAT OF NEW ENTRANTS

- 5.1.5 THREAT OF SUBSTITUTES

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 PRICING ANALYSIS

- 5.4.2 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY TECHNOLOGY

- 5.4.3 AVERAGE SELLING PRICE RANGE OF ANTI-COUNTERFEIT PACKAGING, BY REGION, 2022-2026

- 5.4.4 AVERAGE SELLING PRICE TREND OF ANTI-COUNTERFEIT PACKAGING, BY REGION

- 5.5 TRADE ANALYSIS

- 5.5.1 EXPORT SCENARIO (HS CODE 8523)

- 5.5.2 IMPORT SCENARIO (HS CODE 8523)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 CASE STUDY 1: ANTI-COUNTERFEITING WITH QR CODES FOR WINE PRODUCER MARCHESI ANTINORI

- 5.9.2 CASE STUDY 2: LAUNCHING A SUCCESSFUL RFID SOLUTION FOR SOUTHERN FRIED COTTON

- 5.9.3 CASE STUDY 3: IMPLEMENTING RFID FOR DECATHLON RETAIL OPERATIONS

- 5.10 IMPACT OF 2025 US TARIFF: ANTI-COUNTERFEIT PACKAGING MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 END-USE INDUSTRY IMPACT

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 SERIALIZATION

- 6.1.2 TAMPER-PROOF PACKAGING

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 NEUROTAGS

- 6.2.2 WATERMARKING

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2026-2028): INTEGRATION & COST OPTIMIZATION PHASE

- 6.3.2 MID-TERM (2028-2031): DIGITALIZATION & INTELLIGENT SYSTEMS PHASE

- 6.3.3 LONG-TERM (2031-2035+): AUTONOMOUS & INVISIBLE SECURITY PHASE

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 METHODOLOGY

- 6.4.3 ANTI-COUNTERFEIT PACKAGING MARKET, PATENT ANALYSIS, 2016-2025

- 6.5 FUTURE APPLICATIONS

- 6.5.1 AI-ENABLED SELF-RESPONSIVE ANTI-COUNTERFEIT PACKAGING

- 6.5.2 BLOCKCHAIN-LINKED DIGITAL IDENTITY PACKAGING

- 6.5.3 ENERGY-HARVESTING SMART PACKAGING SYSTEMS

- 6.6 IMPACT OF AI/GEN AI ON ANTI-COUNTERFEIT PACKAGING MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN ANTI-COUNTERFEIT PACKAGING MARKET

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN ANTI-COUNTERFEIT PACKAGING MARKET

- 6.6.3.1 Interconnected ecosystem and impact on market players

- 6.6.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ANTI-COUNTERFEIT PACKAGING MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 SHIFT TO ECO-FRIENDLY & RECYCLABLE MATERIALS (SMART LABELS)

- 7.2.2 COMPOSTABLE & BIODEGRADABLE SECURITY INKS

- 7.2.3 CIRCULAR ECONOMY & REUSABLE PACKAGING SYSTEMS

- 7.3 IMPACT OF REGULATORY POLICY ON SUSTAINABILITY INITIATIVES

- 7.3.1 REGULATORY MANDATES DRIVING MATERIAL INNOVATION

- 7.3.2 EXTENDED PRODUCER RESPONSIBILITY (EPR) EXPANDING LIFECYCLE ACCOUNTABILITY

- 7.3.3 DIGITALIZATION AS A LOW-CARBON COMPLIANCE STRATEGY

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES BY END-USE INDUSTRIES

9 ANTI-COUNTERFEIT PACKAGING MARKET, BY TECHNOLOGY

- 9.1 INTRODUCTION

- 9.2 MASS ENCODING

- 9.2.1 RISING DEMAND FOR TRACK AND TRACE TECHNOLOGIES IN PACKAGING TO PROPEL MARKET

- 9.2.2 BARCODES

- 9.2.3 DIGITAL MASS SERIALIZATION

- 9.2.4 DIGITAL MASS ENCRYPTION

- 9.3 RADIO FREQUENCY IDENTIFICATION (RFID)

- 9.3.1 TECHNOLOGICAL ADVANCEMENTS IN PACKAGING INDUSTRY TO BOOST MARKET

- 9.4 HOLOGRAMS

- 9.4.1 RISING DEMAND FOR THREE-DIMENSIONAL NON-IMITATIVE HOLOGRAMS TO PROPEL MARKET

- 9.5 FORENSIC MARKERS

- 9.5.1 INCORPORATION OF ADVANCED SCIENTIFIC TECHNIQUES IN ANTI-COUNTERFEIT PACKAGING TO BOOST MARKET

- 9.6 TAMPER EVIDENCE

- 9.6.1 RISING DEMAND FOR PACKAGING SOLUTIONS WITH VISUAL INDICATIONS TO PROPEL MARKET

- 9.7 OTHER TECHNOLOGIES

10 ANTI-COUNTERFEIT PACKAGING MARKET, BY END-USE INDUSTRY

- 10.1 INTRODUCTION

- 10.2 FOOD & BEVERAGE

- 10.2.1 RISING DEMAND FOR TRACK AND TRACE PACKAGING TO PROPEL MARKET

- 10.3 PHARMACEUTICAL

- 10.3.1 GOVERNMENT INITIATIVES TO COMBAT COUNTERFEITING TO PROPEL MARKET

- 10.4 APPAREL & FOOTWEAR

- 10.4.1 THREAT FROM COUNTERFEIT APPAREL & FOOTWEAR PRODUCTS AND BRAND IMITATIONS TO PROPEL MARKET

- 10.5 AUTOMOTIVE

- 10.5.1 ADOPTION OF ANTI-COUNTERFEIT PACKAGING SOLUTIONS BY AUTOMOTIVE MANUFACTURERS TO BOOST MARKET

- 10.6 PERSONAL CARE

- 10.6.1 RISING CONSUMER AWARENESS ABOUT FALSIFIED COSMETICS TO PROPEL MARKET

- 10.7 ELECTRONICS & ELECTRICAL

- 10.7.1 RISING DEMAND FOR AUTHENTIC AND RELIABLE ELECTRONIC GOODS TO BOOST MARKET

- 10.8 LUXURY GOODS

- 10.8.1 ADOPTION OF AUTHENTICATION TECHNOLOGIES BY LUXURY BRANDS TO BOOST MARKET

- 10.9 OTHER END-USE INDUSTRIES

11 ANTI-COUNTERFEIT PACKAGING MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 Growing need for effective traceability and tracking technologies to drive market

- 11.2.2 CANADA

- 11.2.2.1 Government initiatives to combat counterfeiting to drive market

- 11.2.3 MEXICO

- 11.2.3.1 Increasing prevalence of counterfeit goods to drive market

- 11.2.1 US

- 11.3 EUROPE

- 11.3.1 GERMANY

- 11.3.1.1 Growing demand for high-end and premium products to drive market

- 11.3.2 FRANCE

- 11.3.2.1 Increasing counterfeiting activities to drive market

- 11.3.3 UK

- 11.3.3.1 Increasing awareness of customers about counterfeiting to drive market

- 11.3.4 ITALY

- 11.3.4.1 Increasing falsification of luxury goods to drive market

- 11.3.5 RUSSIA

- 11.3.5.1 Government initiatives to combat counterfeiting to drive market

- 11.3.6 SPAIN

- 11.3.6.1 Increasing concerns about product authenticity and safety to drive market

- 11.3.7 REST OF EUROPE

- 11.3.1 GERMANY

- 11.4 ASIA PACIFIC

- 11.4.1 CHINA

- 11.4.1.1 Availability of low-cost labor and advanced manufacturing capabilities to drive market

- 11.4.2 INDIA

- 11.4.2.1 Expansion of pharmaceutical market to drive market

- 11.4.3 JAPAN

- 11.4.3.1 Government initiatives to combat counterfeiting to drive growth

- 11.4.4 AUSTRALIA

- 11.4.4.1 Growth of e-commerce and retail sectors to drive market

- 11.4.5 REST OF ASIA PACIFIC

- 11.4.1 CHINA

- 11.5 SOUTH AMERICA

- 11.5.1 BRAZIL

- 11.5.1.1 Growing need for effective traceability and tracking technologies to drive market

- 11.5.2 ARGENTINA

- 11.5.2.1 Government initiatives to combat counterfeiting to drive market

- 11.5.3 REST OF SOUTH AMERICA

- 11.5.1 BRAZIL

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 GCC COUNTRIES

- 11.6.1.1 Saudi Arabia

- 11.6.1.1.1 Increasing awareness among consumers about product authenticity to drive growth

- 11.6.1.2 UAE

- 11.6.1.2.1 Growing demand for secure packaging solutions to drive market

- 11.6.1.3 Rest of GCC Countries

- 11.6.1.1 Saudi Arabia

- 11.6.2 SOUTH AFRICA

- 11.6.2.1 Increasing prevalence of counterfeit products and demand for brand protection to drive market

- 11.6.3 TURKEY

- 11.6.3.1 Strategic geographical location between Europe and Asia for trading counterfeit goods to drive market

- 11.6.4 REST OF MIDDLE EAST & AFRICA

- 11.6.1 GCC COUNTRIES

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES

- 12.3 MARKET SHARE ANALYSIS

- 12.4 REVENUE ANALYSIS OF KEY PLAYERS

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS

- 12.6 BRAND COMPARISON

- 12.7 COMPANY EVALUATION QUADRANT, KEY PLAYERS

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.4.1 Company footprint

- 12.7.4.2 Regional footprint

- 12.7.4.3 Technology footprint

- 12.7.4.4 End-use industry footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.8.5.1.1 Competitive benchmarking of key startups/SMEs

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES/DEVELOPMENTS/ENHANCEMENT

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

- 12.9.4 OTHER DEVELOPMENTS

13 COMPANY PROFILE

- 13.1 KEY PLAYERS

- 13.1.1 AVERY DENNISON CORPORATION

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Expansion

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses & competitive threats

- 13.1.2 CCL INDUSTRIES INC

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Deals

- 13.1.2.3.2 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses & competitive threats

- 13.1.3 3M

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Expansions

- 13.1.3.3.3 Others

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses & competitive threats

- 13.1.4 SATO CORPORATION

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches

- 13.1.4.3.2 Deals

- 13.1.4.3.3 Expansions

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses & competitive threats

- 13.1.5 ZEBRA TECHNOLOGIES CORPORATION

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches

- 13.1.5.3.2 Deals

- 13.1.5.3.3 Expansions

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses & competitive threats

- 13.1.6 SICPA HOLDING SA

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Deals

- 13.1.6.4 MnM view

- 13.1.6.4.1 Right to Win

- 13.1.6.4.2 Strategic choices

- 13.1.6.4.3 Weaknesses & competitive threats

- 13.1.7 INTELLIGENT LABEL SOLUTIONS

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches

- 13.1.7.3.2 Expansions

- 13.1.7.3.3 Other Developments

- 13.1.7.4 MnM view

- 13.1.8 SML GROUP

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Product launches

- 13.1.8.3.2 Deals

- 13.1.8.4 MnM view

- 13.1.9 ALPVISION S.A.

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 MnM view

- 13.1.10 AUTHENTIX, INC.

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.10.2.1 Deals

- 13.1.10.3 MnM view

- 13.1.11 DOVER CORPORATION

- 13.1.11.1 Business overview

- 13.1.11.2 Products/Solutions/Services offered

- 13.1.11.2.1 Product launch

- 13.1.11.3 MnM view

- 13.1.1 AVERY DENNISON CORPORATION

- 13.2 OTHER PLAYERS

- 13.2.1 AMPACET CORPORATION

- 13.2.2 3D AG

- 13.2.3 TRACELINK INC.

- 13.2.4 ADVANCE TRACK & TRACE

- 13.2.5 ELUCEDA LTD.

- 13.2.6 IMPINJ, INC.

- 13.2.7 TRUTAG TECHNOLOGIES, INC.

- 13.2.8 EDGYN

- 13.2.9 MICROTAG TEMED LTD.

- 13.2.10 CERTILOGO SPA

- 13.2.11 TAGLET INC.

- 13.2.12 PROOFTAG

- 13.2.13 SELINKO

- 13.2.14 SCANTRUST SA

- 13.2.15 PIQR

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY DATA

- 14.1.1.1 Key data from secondary sources

- 14.1.2 PRIMARY DATA

- 14.1.2.1 Key data from primary sources

- 14.1.1 SECONDARY DATA

- 14.2 MARKET SIZE ESTIMATION

- 14.3 DATA TRIANGULATION

- 14.4 RESEARCH ASSUMPTIONS

- 14.5 RISK ASSESSMENT

- 14.6 GROWTH RATE ASSUMPTIONS

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS