|

시장보고서

상품코드

2043696

디지털 철도 시장 예측(-2031년) : 솔루션별, 서비스별, 용도별, 지역별Digital Railway Market By Solution (Remote Optimization & Scheduling, Remote Monitoring, Analytics, Network Management, Predictive Maintenance, Security), Application (Rail Operation Management, PIS, Asset Management) - Global Forecast to 2031 |

||||||

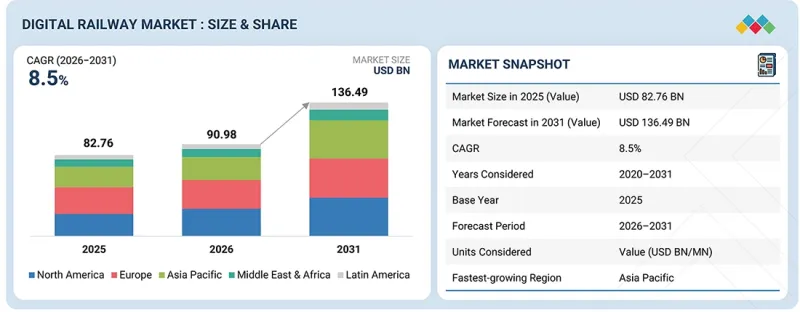

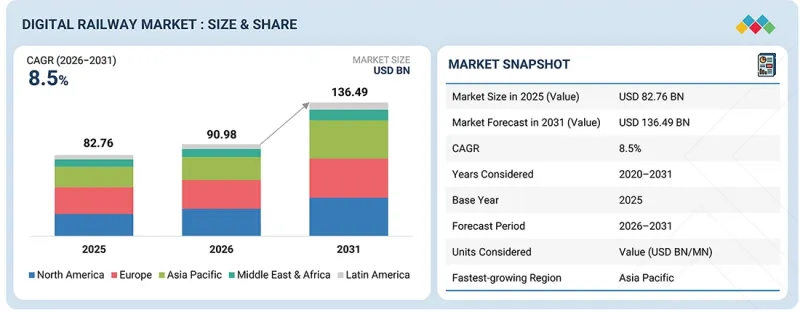

디지털 철도 시장 규모는 2026년 909억 8,000만 달러에서 2031년까지 1,364억 9,000만 달러에 달할 것으로 예측되고 있으며, CAGR은 8.5%에 달할 전망입니다.

변동하는 승객 수와 운행 스케줄의 수요에 맞춰 원활한 이동 경험을 제공해야 할 필요성이 이 분야를 주도하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(100만/10억 달러) |

| 부문 | 솔루션별, 서비스별, 용도별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

교통 당국은 경직되고 낡은 운영 체제에서 실시간 데이터를 활용하여 노선과 운행 스케줄을 최적화하는 민첩한 플랫폼으로 전환하고 있습니다. 이러한 변화는 클라우드 기반 철도 관리 시스템의 도입으로 더욱 가속화되고 있으며, 방대한 교통 네트워크 전반에 걸쳐 역동적인 업데이트와 자원 배분을 가능하게 하고 있습니다. 차량 성능을 모니터링하고 안전성을 향상시키기 위한 운영 분석에 대한 의존도가 높아지면서 인프라 투자에 큰 영향을 미치고 있습니다. 결국 이러한 요인들은 유연한 서비스 제공, 엄격한 성능 추적, 다양한 교통 환경에서의 견고한 구축을 보장하는 확장성이 뛰어난 디지털 철도 솔루션에 대한 수요를 가속화하고 있습니다.

예측 기간 중 승객 정보 시스템(PIS) 부문이 가장 높은 CAGR을 기록할 것으로 예상됩니다.

교통 당국이 통근자 경험 향상과 스마트 모빌리티를 우선시하는 가운데, 승객 정보 시스템(PIS)은 지속적으로 보급되고 있습니다. 철도 회사들은 시간표, 열차 위치 정보, 네트워크 장애에 대한 실시간 업데이트 정보를 제공하기 위해 동적 디지털 디스플레이와 모바일 애플리케이션의 도입을 확대하고 있습니다. 기존의 정적 안내 디스플레이와 비교하여 최신 PIS는 원활한 IoT 연결, 멀티모달 경로 계획, 스마트 장치와의 통합을 제공합니다. 이에 따라 지능형 인프라로 전환하는 역에서 PIS는 필수 불가결한 요소로 자리 잡고 있습니다. 신뢰할 수 있고 접근하기 쉬운 교통 데이터에 대한 수요 증가가 주요 촉진요인으로 작용하고 있으며, 혼잡한 도시 철도 네트워크 전체에서 대기 시간을 크게 단축하고 혼잡 관리를 효율화하여 승객의 만족도에 직접적인 영향을 미치고 있습니다.

2025년 디지털 철도 시장에서 원격 모니터링 부문이 가장 큰 점유율을 차지했습니다.

2025년 디지털 철도 시장에서 원격 모니터링이 가장 큰 점유율을 차지했습니다. 철도회사들은 시스템 장애를 줄이기 위한 모니터링 시스템 도입에 막대한 자금을 투자하고 있습니다. 철도 당국은 수작업 점검 대신 IoT 기반 센서와 분석 툴을 활용하여 선로 상태, 차량, 신호 시스템을 지속적으로 모니터링하는 방식으로 전환하고 있습니다. 이 기술의 도입으로 가동 중단 시간을 최소화하고, 승객의 안전을 향상시키며, 수명주기 비용을 절감할 수 있습니다. 전 세계에서 철도 시스템의 고도화가 진행됨에 따라 원격 모니터링 시스템에 대한 수요는 증가할 것입니다.

예측 기간 중 아시아태평양은 가장 빠르게 성장하는 시장이 될 것으로 예상됩니다.

급속한 도시화와 모빌리티 강화에 대한 절실한 수요에 힘입어 아시아태평양은 디지털 철도 시장에서 가장 빠른 성장세를 보이고 있습니다. 주요 경제국들은 네트워크 용량 최적화를 위해 첨단 CBTC 시스템 및 IoT에 적극적으로 투자하고 있으며, 철도 사업자들은 예지보전을 위해 AI를 우선순위에 두고 있습니다. 정부의 스마트 시티에 대한 대규모 자금 지원을 바탕으로, 이러한 디지털 솔루션은 장기적인 운영 강건성을 보장하고, 승객의 안전을 향상시키며, 고부가가치 인프라 자산을 보호할 수 있습니다. 특히 2025년 11월, 지멘스 모빌리티는 싱가포르 SBS 트랜짓(SBS Transit)과의 전략적 제휴를 확대하여 다운타운 라인의 첨단 신호 시스템의 IT 보안 및 디지털 수명주기를 현대화하기 위해 협력하기로 했습니다.

주요 시장 참여 기업으로는 Siemens(독일), Cisco(미국), Hitachi(일본), Wabtec(미국), Alstom(France), IBM(미국), ABB(Switzerland), Huawei(China), Fujitsu(일본), DXC(미국), Honeywell(미국), Indra(스페인), Nokia(핀란드), Atkins(영국), Toshiba(일본), Televic(벨기에), Advantech(대만), ZEDAS(독일), R2P(독일), Simpleway(체코), Tego(미국), Passio Technologies(미국), Delphisonic(미국), Konux(독일), Machines With Vision(영국), EKE-Electronics(핀란드), Aitek S.P.A.(이탈리아), CloudMoyo(미국), and RailTel(인도) 등이 있습니다.

조사 범위

이 시장조사는 다양한 부문에 걸친 디지털 철도 시장 규모를 포괄하고 있습니다. 솔루션, 서비스, 애플리케이션, 지역 등 다양한 부문 시장 규모와 성장 잠재력을 추정하는 것을 목표로 합니다. 주요 시장 진입업체에 대한 상세한 경쟁 분석, 기업 개요, 제품 및 사업 제공에 대한 주요 관찰 사항, 최근 동향, 시장 전략 등의 정보를 담고 있습니다.

이 보고서 구매의 주요 이점

이 보고서는 글로벌 디지털 철도 시장의 매출 및 하위 부문에 대한 가장 정확한 추정치에 대한 정보를 제공함으로써 시장 리더와 신규 진입자에게 도움이 될 것입니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 비즈니스 포지셔닝을 개선하고, 적절한 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악할 수 있는 인사이트를 제공하고, 주요 시장 촉진요인, 시장 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

이 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다. :

주요 촉진요인(지난 수년간 승객 수 급증, 철도 분야 IoT의 급속한 도입), 제약 요인(높은 초기 도입 비용, 개발도상국의 탄탄한 철도 인프라 부족), 기회 요인(첨단 교통 인프라의 필요성, 자율주행 열차의 부상), 도전 요인(철도 시스템 디지털화에 따른 사이버 공격 위협 증가, IT 인프라 부족, 숙련된 인력 부족)을 분석했습니다. 사이버 공격의 위협 증가, 불충분한 IT 인프라 및 숙련된 인력 부족)을 분석하고 있습니다.

제품 개발/혁신: 디지털 철도 시장의 미래 기술, 연구개발 활동, 제품 및 서비스 출시에 대한 심층적인 인사이트.

시장 개발: 수익성 높은 시장에 대한 포괄적인 정보 - 이 보고서는 각 지역의 디지털 철도 시장을 분석합니다.

시장 다각화: 디지털 철도 시장의 신제품 및 서비스, 미개발 지역, 최근 동향 및 투자에 대한 포괄적인 정보.

경쟁 분석 - Siemens(독일), Cisco(미국), Hitachi(일본), Wabtec(미국), Alstom(France), IBM(미국), ABB(Switzerland), Huawei(China), Fujitsu(일본), DXC(미국), Honeywell(미국), Indra(스페인), Nokia(핀란드), Atkins(영국), Toshiba(일본), Televic(벨기에), Advantech(대만), ZEDAS(독일), R2P(독일), Simpleway(체코), Tego(미국), Passio Technologies(미국), Delphisonic(미국), Konux(독일), Machines With Vision(영국), EKE-Electronics(핀란드), Aitek S.P.A.(이탈리아), CloudMoyo(미국), and RailTel(인도).

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요와 업계 동향

제5장 업계 동향

제6장 전략적 파괴 : 디지털과 AI의 도입

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 디지털 철도 시장(솔루션별)

제10장 디지털 철도 시장(서비스별)

제11장 디지털 철도 시장(용도별)

제12장 디지털 철도 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSA 26.06.05The digital railway market is projected to reach USD 136.49 billion by 2031, from USD 90.98 billion in 2026, with a CAGR of 8.5%. The need to deliver seamless journeys that adapt to fluctuating passenger volumes and scheduling demands is propelling this sector.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Solution, Service, Application |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

Transit authorities are moving away from rigid, legacy operations toward agile platforms utilizing real-time data to optimize routes and schedules. This shift is reinforced by the adoption of cloud-based rail management systems, enabling dynamic updates and resource allocation across vast transit networks. Increased reliance on operational analytics to monitor fleet performance and improve safety heavily influences infrastructure investments. Ultimately, these factors accelerate demand for scalable digital railway solutions that ensure flexible service delivery, rigorous performance tracking, and robust deployment across diverse transit environments.

The passenger information system segment is expected to register the highest CAGR during the forecast period.

Passenger information systems (PIS) continue to gain traction as transit authorities prioritize enhanced commuter experiences and smart mobility. Railways are increasingly deploying dynamic digital displays and mobile applications to deliver real-time updates on schedules, train locations, and network disruptions. Compared to traditional static signage, modern PIS offers seamless IoT connectivity, multimodal journey planning, and smart-device integration. This makes them crucial for stations transitioning toward intelligent infrastructure. The growing demand for reliable, accessible transit data acts as a primary driver, directly impacting passenger satisfaction by significantly reducing perceived wait times and streamlining crowd management across congested urban railway networks.

The remote monitoring segment contributed the largest share of the digital railway market in 2025.

Remote monitoring accounted for the largest share of the digital railway market in 2025. Railways are spending huge amounts of money on the installation of monitoring systems aimed at reducing system failures. Instead of carrying out inspections manually, railway authorities have resorted to using IoT-based sensors and analytics tools that provide continuous monitoring of the track conditions, rolling stock, and signaling systems. The application of this technology minimizes operational downtime, improves passenger safety, and increases the life cycle costs. As more railway systems become advanced globally, there will be an increased demand for remote monitoring systems.

Asia Pacific is expected to be the fastest-growing market during the forecast period.

Driven by rapid urbanization and the pressing demand for enhanced mobility, the Asia Pacific region is experiencing the fastest growth in the digital railway market. Major economies are aggressively investing in advanced CBTC systems and IoT to optimize network capacity, while operators prioritize AI for predictive maintenance. Supported by extensive government smart-city funding, these digital solutions ensure long-term operational resilience, improve passenger safety, and protect high-value infrastructure assets. Notably, in November 2025, Siemens Mobility extended its strategic collaboration with SBS Transit in Singapore to modernize the IT security and digital lifecycle of the Downtown Line's advanced signaling system.

Breakdown of Primaries

The study contains insights from various industry experts, from solution vendors to Tier 1 companies. The break-up of the primaries is as follows:

- By Company Type: Tier 1 - 30%, Tier 2 - 45%, and Tier 3 - 25%

- By Designation: C-level -35%, D-level - 30%, and Managers - 35%

- By Region: North America - 40%, Europe - 20%, Asia Pacific - 30%, Middle East & Africa- 5%, and Latin America- 5%.

Key market players include Siemens (Germany), Cisco (US), Hitachi (Japan), Wabtec (US), Alstom (France), IBM (US), ABB (Switzerland), Huawei (China), Fujitsu (Japan), DXC (US), Honeywell (US), Indra (Spain), Nokia (Finland), Atkins (UK), Toshiba (Japan), Televic (Belgium), Advantech (Taiwan), ZEDAS (Germany), R2P (Germany), Simpleway (Czech Republic), Tego (US), Passio Technologies (US), Delphisonic (US), Konux (Germany), Machines With Vision (UK), EKE-Electronics (Finland), Aitek S.P.A. (Italy), CloudMoyo (US), and RailTel (India).

Research Coverage

The market study covers the digital railway market size across different segments. It aims to estimate the market size and the growth potential across various segments, including solution, service, application, and region. The study includes an in-depth competitive analysis of the leading market players, their company profiles, key observations related to product and business offerings, recent developments, and market strategies.

Key Benefits of Buying the Report

The report will help the market leaders/new entrants with information on the closest approximations of the global digital railway market's revenue numbers and subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. Moreover, the report will provide insights for stakeholders to understand the market's pulse and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (Surge in passenger numbers over past few years, Rapid adoption of IoT in railways), restraints (High initial cost of deployment, Lack of strong railway infrastructure in underdeveloped countries), opportunities (Need for advanced transportation infrastructure, Rise of autonomous trains), and challenges (Increased threat of cyberattacks amid digitalization of railway system, Inadequate IT infrastructure and shortage of skilled personnel) influencing the growth of the digital railway market.

Product Development/Innovation: Detailed insights on upcoming technologies, R&D activities, and product and service launches in the digital railway market.

Market Development: Comprehensive information about lucrative markets - the report analyzes various regions' digital railway markets.

Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the digital railway market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Siemens (Germany), Cisco (US), Hitachi (Japan), Wabtec (US), Alstom (France), IBM (US), ABB (Switzerland), Huawei (China), Fujitsu (Japan), DXC (US), Honeywell (US), Indra (Spain), Nokia (Finland), Atkins (UK), Toshiba (Japan), Televic (Belgium), Advantech (Taiwan), ZEDAS (Germany), R2P (Germany), Simpleway (Czech Republic), Tego (US), Passio Technologies (US), Delphisonic (US), Konux (Germany), Machines With Vision (UK), EKE-Electronics (Finland), Aitek S.P.A. (Italy), CloudMoyo (US), and RailTel (India).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN DIGITAL RAILWAY MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DIGITAL RAILWAY MARKET

- 3.2 DIGITAL RAILWAY MARKET, BY OFFERING AND REGION

- 3.3 DIGITAL RAILWAY MARKET, BY SERVICE

- 3.4 DIGITAL RAILWAY MARKET, BY SOLUTION

- 3.5 DIGITAL RAILWAY MARKET, BY APPLICATION

4 MARKET OVERVIEW AND INDUSTRY TRENDS

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Global decarbonization goals fuel adoption of AI-driven energy optimization and smart power grids

- 4.2.1.2 Mandatory transitions to ERTMS/CBTC signaling propel market toward fully digitalized, fail-safe operations

- 4.2.1.3 Shift from reactive to IoT-based predictive maintenance accelerates demand for digital asset management

- 4.2.1.4 Deeper convergence of OT and IT networks to support real-time, data-driven rail operations

- 4.2.2 RESTRAINTS

- 4.2.2.1 Lack of strong railway infrastructure in underdeveloped countries

- 4.2.2.2 High initial cost of deployment

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Connecting rail to mobility-as-a-service apps offers opportunity to capture entire end-to-end digital passenger journey

- 4.2.3.2 Leveraging high-performance edge computing for AI-driven predictive maintenance on rolling stock

- 4.2.3.3 Industry-wide transition to 5G-enabled mission-critical broadband (FRMCS) for ultra-reliable connectivity

- 4.2.4 CHALLENGES

- 4.2.4.1 Increased threat of cyberattacks as railway system becomes digital

- 4.2.4.2 Ensuring "plug-and-play" compatibility between diverse hardware vendors poses a significant technical hurdle

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.3.1 SMART MOBILITY AND INTEGRATED URBAN TRANSPORT

- 4.3.2 SMART LOGISTICS AND CONNECTED SUPPLY CHAINS

- 4.3.3 TELECOM AND HIGH-SPEED 5G NETWORKS

- 4.3.4 GREEN ENERGY AND SMART GRIDS

- 4.3.5 RETAIL AND ENHANCED PASSENGER EXPERIENCE

- 4.3.6 REAL ESTATE AND TRANSIT-ORIENTED DEVELOPMENT

- 4.3.7 FINTECH AND DIGITAL PAYMENTS

- 4.3.8 TOURISM AND HOSPITALITY

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN DIGITAL RAILWAY INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICING ANALYSIS, BY SOLUTION, 2025

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 DEPLOYING PATHFINDER TECHNOLOGY TO ENABLE AUTONOMOUS RAIL OPERATIONS

- 5.9.2 COMMISSIONING FIRST ARGOS DIGITAL INTERLOCKING SYSTEM IN MONTBARD, FRANCE

- 5.9.3 SWISS FEDERAL RAILWAYS INCREASED CUSTOMER FLEXIBILITY ON ITS SERVICENOW PLATFORM WITH HELP FROM DXC

- 5.9.4 TRANSFORMING RAIL TRANSPORTATION WITH SMART ANALYTICS ACROSS UK RAILWAY NETWORK

- 5.9.5 NEW ZEALAND: INTEROPERABLE TICKETING SYSTEM FOR AUCKLAND

- 5.9.6 TRANSFORMING SMART RAIL STATIONS WITH ADVANTECH DS-330

- 5.10 IMPACT OF 2025 US TARIFF - DIGITAL RAILWAY MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 IMPACT ON END-USE INDUSTRIES

- 5.10.3.1 Price impact analysis

6 STRATEGIC DISRUPTIONS: DIGITAL AND AI ADOPTION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 INTERNET OF THINGS (IOT)

- 6.1.2 BIG DATA ANALYTICS AND CLOUD COMPUTING

- 6.1.3 ARTIFICIAL INTELLIGENCE (AI) & MACHINE LEARNING (ML)

- 6.1.4 ADVANCED SIGNALING SYSTEMS

- 6.1.5 COMMUNICATION-BASED TRAIN CONTROL (CBTC)

- 6.1.6 ADJACENT TECHNOLOGIES

- 6.1.6.1 Augmented reality (AR) & virtual reality (VR)

- 6.1.6.2 Blockchain

- 6.1.6.3 Drones

- 6.1.7 COMPLEMENTARY TECHNOLOGIES

- 6.1.7.1 Edge computing

- 6.1.7.2 Digital twin

- 6.1.7.3 Cybersecurity

- 6.1.7.4 5G and wireless communication networks

- 6.2 TECHNOLOGY/PRODUCT ROADMAP FOR DIGITAL RAILWAY MARKET

- 6.2.1 SHORT-TERM ROADMAP (2026-2027)

- 6.2.2 MID-TERM ROADMAP (2028-2029)

- 6.2.3 LONG-TERM ROADMAP (2030-2031)

- 6.3 PATENT ANALYSIS

- 6.4 IMPACT OF AI/GEN AI ON DIGITAL RAILWAY MARKET

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

- 6.4.2 CASE STUDIES OF AI IMPLEMENTATION IN DIGITAL RAILWAY MARKET

- 6.4.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.4.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN DIGITAL RAILWAY

7 REGULATORY LANDSCAPE

- 7.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2 INDUSTRY STANDARDS

- 7.3 SUSTAINABILITY INITIATIVES

- 7.4 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

8 CUSTOMER LANDSCAPE & BUYING BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.1.1 DEFINE BUSINESS OBJECTIVES AND SUCCESS CRITERIA

- 8.1.2 CURRENT-STATE ASSESSMENT AND GAP ANALYSIS

- 8.1.3 STAKEHOLDER ALIGNMENT AND REQUIREMENT PLANNING

- 8.1.4 VENDOR EVALUATION AND SOLUTION SELECTION

- 8.1.5 PILOT IMPLEMENTATION AND PERFORMANCE REVIEW

- 8.1.6 FULL-SCALE DEPLOYMENT AND CONTINUOUS IMPROVEMENT

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMEET NEEDS FROM VARIOUS END-USE INDUSTRIES

9 DIGITAL RAILWAY MARKET, BY SOLUTION

- 9.1 INTRODUCTION

- 9.1.1 SOLUTION: MARKET DRIVERS

- 9.2 REMOTE MONITORING

- 9.2.1 REMOTE MONITORING SOLUTIONS TO IMPROVE RELIABILITY OF RAILWAY INFRASTRUCTURE

- 9.3 ROUTE OPTIMIZATION & SCHEDULING

- 9.3.1 ROUTE OPTIMIZATION & SCHEDULING SOLUTIONS TO IMPROVE TRAIN PLANNING AND NETWORK CAPACITY

- 9.4 ANALYTICS

- 9.4.1 ANALYTICS SOLUTIONS TO ENABLE DATA-DRIVEN RAILWAY OPERATIONS

- 9.5 NETWORK MANAGEMENT

- 9.5.1 NETWORK MANAGEMENT SOLUTIONS TO SUPPORT CONNECTED AND RELIABLE RAILWAY OPERATIONS

- 9.6 PREDICTIVE MAINTENANCE

- 9.6.1 PREDICTIVE MAINTENANCE SOLUTIONS TO REDUCE FAILURES AND IMPROVE ASSET AVAILABILITY

- 9.7 SECURITY

- 9.7.1 SECURITY SOLUTIONS TO PROTECT CONNECTED RAILWAY SYSTEMS AND CRITICAL ASSETS

- 9.8 OTHER SOLUTIONS

10 DIGITAL RAILWAY MARKET, BY SERVICE

- 10.1 INTRODUCTION

- 10.1.1 SERVICE: MARKET DRIVERS

- 10.2 PROFESSIONAL SERVICES

- 10.2.1 CONSULTING

- 10.2.1.1 Consulting service providers to help railway operators define digital transformation roadmaps and upgrade priorities

- 10.2.2 SYSTEM INTEGRATION & DEPLOYMENT

- 10.2.2.1 System integration and deployment service providers to help integrate smart solutions with existing infrastructure

- 10.2.3 SUPPORT & MAINTENANCE

- 10.2.3.1 Support and maintenance service providers to help ensure continuous performance of digital railway systems

- 10.2.1 CONSULTING

- 10.3 MANAGED SERVICES

11 DIGITAL RAILWAY MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.1.1 APPLICATION: MARKET DRIVERS

- 11.2 RAIL OPERATIONS MANAGEMENT

- 11.2.1 RAIL AUTOMATION MANAGEMENT

- 11.2.2 RAIL CONTROL

- 11.2.2.1 Signaling Solutions

- 11.2.2.1.1 Signaling solutions to improve rail safety, capacity, and interoperability

- 11.2.2.2 Rail Traffic Management

- 11.2.2.2.1 Rail traffic management to offer flexible solutions to increase railway network capacity and efficiency

- 11.2.2.3 Freight Management

- 11.2.2.3.1 Freight management systems to help freight operators in infrastructure and planning decisions

- 11.2.2.1 Signaling Solutions

- 11.2.3 SMART TICKETING

- 11.2.3.1 Smart ticketing to help contribute to overall improvement of railway transport network

- 11.2.4 WORKFORCE MANAGEMENT

- 11.2.4.1 Workforce management to ensure significant cost reduction and effective employee engagement

- 11.3 PASSENGER INFORMATION SYSTEMS

- 11.3.1 PASSENGER INFORMATION SYSTEMS TO BE KEY COMMUNICATION LINK BETWEEN TRANSPORTATION OPERATORS AND PASSENGER CONNECTIVITY

- 11.4 ASSET MANAGEMENT

- 11.4.1 RAIL ASSET MANAGEMENT TO OPTIMIZE PERFORMANCE AND RAIL INFRASTRUCTURE

- 11.5 OTHER APPLICATIONS

12 DIGITAL RAILWAY MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 NORTH AMERICA: DIGITAL RAILWAY MARKET DRIVERS

- 12.2.2 US

- 12.2.2.1 PTC foundation and rail network upgrades to support digital railway adoption

- 12.2.3 CANADA

- 12.2.3.1 High-speed rail planning and CBTC expertise to drive demand for digital railway solutions

- 12.3 EUROPE

- 12.3.1 EUROPE: DIGITAL RAILWAY MARKET DRIVERS

- 12.3.2 UK

- 12.3.2.1 Signaling renewal and telecom modernization to support digital railway growth

- 12.3.3 GERMANY

- 12.3.3.1 Digital node projects and ETCS rollout to drive digital railway demand

- 12.3.4 FRANCE

- 12.3.4.1 ERTMS alignment and high-speed network modernization to drive digital railway solutions

- 12.3.5 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 ASIA PACIFIC: DIGITAL RAILWAY MARKET DRIVERS

- 12.4.2 CHINA

- 12.4.2.1 Intelligent high-speed rail and real-time monitoring to drive digital railway solutions

- 12.4.3 INDIA

- 12.4.3.1 Kavach rollout and telecom upgrades to drive demand for digital railway solutions

- 12.4.4 JAPAN

- 12.4.4.1 Strategic collaborations and digital railway advancements to drive market

- 12.4.5 REST OF ASIA PACIFIC

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 MIDDLE EAST & AFRICA: DIGITAL RAILWAY MARKET DRIVERS

- 12.5.2 UAE

- 12.5.2.1 Passenger rail launch and network integration to support digital railway solutions

- 12.5.3 NIGERIA

- 12.5.3.1 Government initiatives combined with cooperation with other countries to boost market in Nigeria

- 12.5.4 SOUTH AFRICA

- 12.5.4.1 Signaling renewal and fiber networks to support digital railway modernization

- 12.5.5 REST OF MIDDLE EAST & AFRICA

- 12.6 LATIN AMERICA

- 12.6.1 LATIN AMERICA: DIGITAL RAILWAY MARKET DRIVERS

- 12.6.2 BRAZIL

- 12.6.2.1 Freight growth and metro signaling upgrades to drive demand for digital railway solutions

- 12.6.3 MEXICO

- 12.6.3.1 Intercity rail modernization and ETCS deployment to support digital railway growth

- 12.6.4 REST OF LATIN AMERICA

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2026

- 13.3 MARKET SHARE ANALYSIS, 2025

- 13.4 REVENUE ANALYSIS OF LEADING PLAYERS, 2023-2025

- 13.5 BRAND/PRODUCT COMPARISON

- 13.6 COMPANY VALUATION AND FINANCIAL METRICS

- 13.7 COMPANY EVALUATION MATRIX, 2025

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.7.5.1 Company footprint

- 13.7.5.2 Region footprint

- 13.7.5.3 Offering footprint

- 13.7.5.4 Application footprint

- 13.8 STARTUP/SME EVALUATION MATRIX

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

14 COMPANY PROFILES

- 14.1 MAJOR PLAYERS

- 14.1.1 SIEMENS

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches

- 14.1.1.3.2 Deals

- 14.1.1.3.3 Other developments

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 CISCO

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 HITACHI

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches

- 14.1.3.3.2 Deals

- 14.1.3.3.3 Other developments

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 WABTEC

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Other developments

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths/Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 ALSTOM

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Other developments

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 IBM

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 MnM view

- 14.1.6.3.1 Right to win

- 14.1.6.3.2 Strategic choices

- 14.1.6.3.3 Weaknesses and competitive threats

- 14.1.7 ABB

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.8 HUAWEI

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches

- 14.1.8.3.2 Deals

- 14.1.8.3.3 Other developments

- 14.1.9 FUJITSU

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Other developments

- 14.1.10 DXC

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Other developments

- 14.1.11 HONEYWELL

- 14.1.11.1 Business overview

- 14.1.11.2 Products/Solutions/Services offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Deals

- 14.1.12 INDRA

- 14.1.13 NOKIA

- 14.1.14 ATKINS REALIS

- 14.1.15 TOSHIBA

- 14.1.16 TELEVIC

- 14.1.17 ADVANTECH

- 14.1.1 SIEMENS

- 14.2 STARTUPS/SMES

- 14.2.1 ZEDAS

- 14.2.2 R2P

- 14.2.3 SIMPLEWAY

- 14.2.4 TEGO

- 14.2.5 PASSIO TECHNOLOGIES

- 14.2.6 DELPHISONIC

- 14.2.7 KONUX

- 14.2.8 MACHINES WITH VISION

- 14.2.9 EKE-ELECTRONICS

- 14.2.10 AITEK S.P.A.

- 14.2.11 CLOUDMOYO

- 14.2.12 RAILTEL

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Primary interviews with experts

- 15.1.2.2 Breakdown of primary profiles

- 15.1.2.3 Key data from primary sources

- 15.1.2.4 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET BREAKUP AND DATA TRIANGULATION

- 15.3 MARKET SIZE ESTIMATION

- 15.3.1 TOP-DOWN APPROACH

- 15.3.2 BOTTOM-UP APPROACH

- 15.3.3 DIGITAL RAILWAY MARKET ESTIMATION: DEMAND-SIDE ANALYSIS

- 15.4 MARKET FORECAST

- 15.4.1 RISK ASSESSMENT

- 15.5 RESEARCH ASSUMPTIONS

- 15.6 LIMITATIONS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS