|

시장보고서

상품코드

2048958

비디오 감시 분야 AI 시장 : 제공별, 전개별, 기능별, 기술별, 업계별, 지역별 - 세계 예측(-2032년)AI in Video Surveillance Market by Offering, Function, Technology - Global Forecast to 2032 |

||||||

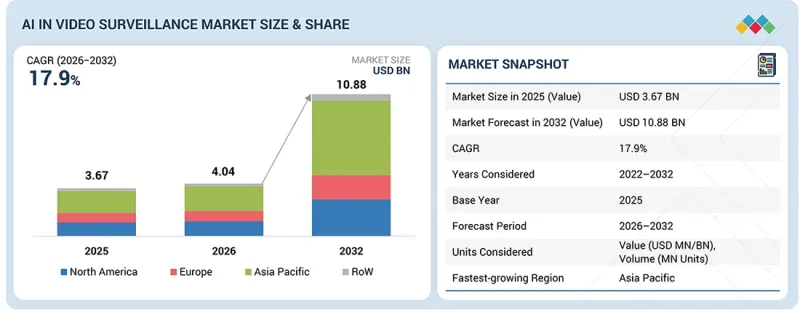

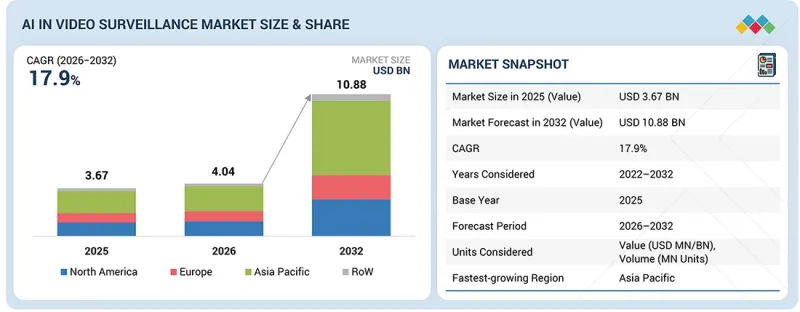

비디오 감시 분야 AI 시장 규모는 2026년 40억 4,000만 달러에서 2032년까지 108억 8,000만 달러로 성장하여 예측 기간 동안 CAGR은 17.9%에 달할 것으로 전망됩니다.

산업을 막론하고, 미래지향적인 자동화된 보안 솔루션에 대한 수요가 증가함에 따라 이 시장은 예측 기간 동안 강력한 성장세를 보일 것으로 예상됩니다. 조직은 안전성을 높이고, 인적 개입을 줄이며, 업무 효율성을 개선하기 위해 실시간 모니터링과 지능형 분석을 점점 더 우선순위로 삼고 있습니다. AI를 활용한 감시 시스템은 얼굴인식, 물체 감지, 행동 분석, 이상 감지 등의 기능을 구현하여 보다 신속하고 정확한 의사결정을 가능하게 합니다. 이러한 시스템은 오보를 크게 줄이고 예측적 위협 식별을 가능하게 합니다. 이는 스마트 시티, 교통, 유통, 소매, 중요 인프라 등의 분야에서 매우 중요합니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제공별, 전개별, 기능별, 기술별, 업계별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

또한, 엣지 컴퓨팅, 클라우드 통합, 딥러닝 알고리즘의 발전으로 시스템의 확장성과 성능이 향상되고 있습니다. 영상 데이터에서 실용적인 인사이트를 도출하는 능력과 더불어 운영 비용 절감 및 보안 효과 향상으로 인해 전 세계적으로 도입이 가속화되고 있습니다. 또한, 스마트 인프라, 도시 안전 대책 및 규제 준수 요건에 대한 투자 증가는 비디오 감시 시장에서 AI의 장기적인 성장 잠재력을 높이고 있습니다.

"제품별로는 소프트웨어 부문이 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예상됩니다."

지능형 분석 및 중앙 집중식 영상 관리 기능에 대한 수요가 증가함에 따라, 예측 기간 동안 비디오 감시 AI 시장에서 소프트웨어 부문이 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 조직은 보안 및 운영 인사이트를 강화하기 위해 영상 관리 시스템, 얼굴 인식, 물체 감지, 행동 분석과 같은 AI 기반 소프트웨어 솔루션을 빠르게 도입하고 있습니다. 클라우드 기반 플랫폼과 구독 모델로의 전환은 확장성과 비용 효율성을 더욱 높이고 있습니다. 딥러닝과 컴퓨터 비전의 지속적인 발전으로 정확성과 자동화가 향상되고 있으며, 소프트웨어는 전 세계 모든 산업에서 현대의 감시 생태계에서 필수적인 요소로 자리 잡고 있습니다.

"기능별로는 교육 분야가 2026년부터 2032년까지 가장 높은 CAGR로 성장할 것으로 예상됩니다."

예측 기간 동안 비디오 감시 AI 시장에서는 훈련 기능이 가장 높은 CAGR을 기록할 것으로 예상됩니다. 이는 복잡한 시각적 시나리오를 정확하게 감지, 분류, 대응할 수 있는 AI 모델 개발 및 개선에 대한 요구가 증가하고 있기 때문입니다. 모니터링 시스템이 점점 더 고도화됨에 따라, 정확도 향상, 오탐지 감소, 실시간 의사결정 능력 강화를 위해 방대한 데이터세트를 이용한 딥러닝 알고리즘의 지속적인 훈련이 필수적입니다. 각 업계의 조직들은 AI 감시 모델이 진화하는 위협과 환경에 계속 적응할 수 있도록 훈련 인프라에 많은 투자를 하고 있습니다. 또한, 엣지 컴퓨팅과 클라우드 기반 교육 플랫폼의 발전은 이러한 성장 궤도를 크게 가속화하고 있습니다.

"2026년부터 2032년까지 아시아태평양이 비디오 감시 AI 시장에서 가장 빠르게 성장하는 지역으로 부상할 전망"

아시아태평양은 급속한 도시화, 스마트 시티 프로젝트에 대한 투자 확대, 인구 밀집 국가의 보안 우려 증가로 인해 예측 기간 동안 비디오 감시 분야에서 가장 빠르게 성장하는 AI 시장으로 부상하고 있습니다. 정부와 기업은 공공안전과 교통 관리를 강화하기 위해 첨단 감시 인프라에 많은 투자를 하고 있습니다. 주요 제조 거점 및 기술 제공업체의 존재는 이 지역의 성장을 더욱 촉진하고 있습니다. 또한, 소매, 운송, 주요 인프라 등의 분야에서의 도입 확대와 더불어 정부의 우호적인 정책 및 디지털 전환 전략이 맞물리면서 지역 전체에서 시장 확대가 가속화되고 있습니다.

비디오 감시 AI 시장 분야에서 사업을 전개하고 있는 주요 기업으로는 Hangzhou Hikvision Digital Technology(중국), Dahua Technology(중국), Axis Communications AB(스웨덴), Motorola Solutions, Inc. Solutions, Inc.(미국), 한화 비전(한국), Milestone Systems A/S(덴마크), SenseTime(홍콩), Irisity(스웨덴), NEC Corporation(일본), Genetec Inc. MOBOTIX AG(독일), Teledyne Technologies Incorporated(미국), Honeywell International Inc(미국), VIVOTEK Inc(대만), 그리고 i-PRO(일본) 등이 있습니다. 이들 기업은 다양한 애플리케이션에서 물체 감지, 얼굴 인식, 행동 분석, 실시간 위협 식별정확도 향상에 초점을 맞추고, AI를 활용한 비디오 감시 기능을 지속적으로 강화하며 경쟁하고 있습니다. 확장성과 상호운용성을 갖춘 시스템 아키텍처, 클라우드 플랫폼, 엣지 컴퓨팅, IoT 생태계와의 통합, 스마트 시티, 소매, 교통, 의료, 중요 인프라 등의 분야를 위한 애플리케이션 특화 솔루션의 개발에 중점을 두고 있습니다. 개발에 중점을 두고 있습니다.

시장 진입 기업들은 기존 보안 및 IT 인프라와의 원활한 통합을 우선시하며 데이터 보안, 시스템 안정성 및 도입 용이성을 보장하고 있습니다. 또한, 오보 감소, 데이터 스토리지 최적화, 그리고 예측 분석을 통해 예측 가능한 의사결정을 가능하게 하는 데 중점을 두고 있습니다. 고도화된 AI 알고리즘, 사이버 보안 강화, 엣지 지원 디바이스에 대한 지속적인 투자, 시스템 통합업체, 정부, 기업과의 협력으로 세계 AI 비디오 감시 시장에서의 경쟁은 지속되고 도입이 가속화될 것으로 예상됩니다.

비디오 감시 분야 AI 시장 주요 기업에 대한 상세한 경쟁 분석을 실시했으며, 각 기업의 기업 프로파일, 최근 동향, 주요 시장 전략 등을 조사하여 전해드립니다.

조사 범위

본 비디오 감시용 AI 시장에 관한 보고서는 제공 형태, 도입 형태, 기능, 기술, 업종, 지역별로 상세한 분석을 제시하고 있습니다. 제공 형태별로는 AI 카메라와 소프트웨어로 분류됩니다. 도입 형태에 따라 엣지형과 클라우드형으로 구분됩니다. 기능별로는 트레이닝과 추론으로 분류됩니다. 기술별로는 컴퓨터 비전(ML/DL), 머신러닝(비시각 AI), 자연어 처리, 생성형 AI 등이 있습니다. 산업별로는 주거, 상업, 군사/방위, 정부/공공시설, 산업, 중요 인프라를 망라하고 있습니다. 지역별 분석에는 북미, 유럽, 아시아태평양, 기타 지역(RoW)이 포함되며, 세계 비디오 감시 AI 시장 전체의 수요 패턴, 성장 요인, 산업 동향을 평가할 수 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 전체 시장 및 하위 부문의 매출에 대한 가장 정확한 추정치에 대한 정보를 제공함으로써 이 시장의 리더와 신규 진입자에게 도움을 줄 수 있습니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 비즈니스 포지셔닝을 개선하고, 적절한 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 또한 이 보고서는 이해관계자들이 비디오 감시 분야 AI 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 제공하는 데 도움이 될 것입니다.

본 보고서 구매의 주요 이점

- 주요 촉진요인 분석(각 분야의 고도화 및 지능형 보안 솔루션에 대한 수요 증가, 딥러닝 및 컴퓨터 비전 기능의 급속한 발전, 범죄 발생률 증가에 따른 감시 시스템 도입 촉진, 스마트 시티 구상의 고도화된 감시 시스템 도입 확대, 스마트 시티 인프라 도입 확대), 제약요인(데이터 프라이버시 및 보안에 대한 우려, AI 기반 감시 시스템 도입의 높은 라이프사이클 비용) 인프라 도입 확대), 제약요인(AI 기반 감시 시스템의 데이터 프라이버시 및 보안 문제, 높은 도입 및 라이프사이클 비용), 기회 요인(IoT 지원 장치 및 생태계와의 AI 통합 발전, 전 세계 스마트홈 기술 보급 확대, 소매 및 교통 부문에서의 AI 기반 감시 채택 확대, 고급 머신러닝 기능을 갖춘 AI 카메라의 지속적인 진화, 특히 신흥 경제국에서 생성형 AI 기술 채택 확대), 도전 과제(지역별로 세분화되고 복잡한 데이터 보호 규제, 오탐지 발생, 사이버 보안 위협 및 시스템 취약성 노출 증가) 비디오 감시 분야 AI 시장 성장에 영향을 미치고 있습니다.

- 제품 개발 및 혁신 : 비디오 감시 AI 시장의 미래 기술, 연구 개발 활동, 신제품 출시에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 비디오 감시용 AI 시장을 분석합니다.

- 시장 다각화 : 비디오 감시 AI 시장의 신제품 및 서비스, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보

- 경쟁사 분석 : Hangzhou Hikvision Digital Technology(중국), Dahua Technology(중국), Axis Communications AB(스웨덴), Motorola Solutions, Inc. Vision(한국), Milestone Systems A/S(덴마크), SenseTime(홍콩), Irisity(스웨덴), NEC Corporation(일본), Genetec Inc. Technologies Incorporated(미국), Honeywell International Inc(미국), VIVOTEK Inc.(대만), i-PRO(일본) 등 주요 기업의 시장 점유율, 성장전략, 서비스 제공에 대한 상세한 평가

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 그리고 혁신

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 비디오 감시 분야 AI 응용

제10장 비디오 감시 분야 AI 시장(제공별)

제11장 비디오 감시 분야 AI 시장(전개별)

제12장 비디오 감시 분야 AI 시장(기능별)

제13장 비디오 감시 분야 AI 시장(기술별)

제14장 비디오 감시 분야 AI 시장(업계별)

제15장 비디오 감시 분야 AI 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSM 26.06.08According to Marketsand Markets, the AI in video surveillance market is projected to grow from USD 4.04 billion in 2026 to USD 10.88 billion by 2032, at a CAGR of 17.9% during the forecast period. The market is projected to witness strong growth during the forecast period, due to the rising need for proactive and automated security solutions across industries. Organizations are increasingly prioritizing real-time monitoring and intelligent analytics to enhance safety, reduce human intervention, and improve operational efficiency. AI-powered surveillance systems enable capabilities such as facial recognition, object detection, behavior analysis, and anomaly detection, allowing faster and more accurate decision-making. These systems significantly reduce false alarms and enable predictive threat identification, which is critical for sectors such as smart cities, transportation, retail, and critical infrastructure.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Offering, Function, Technology and Region |

| Regions covered | North America, Europe, APAC, RoW |

Additionally, advancements in edge computing, cloud integration, and deep learning algorithms are improving system scalability and performance. The ability to derive actionable insights from video data, combined with reduced operational costs and enhanced security outcomes, is accelerating adoption globally. Furthermore, increasing investments in smart infrastructure, urban safety initiatives, and regulatory compliance requirements are reinforcing the long-term growth potential of the AI in video surveillance market.

"By offering, the software segment to capture the largest market share during the forecast period"

The software segment is expected to capture the largest market share in the AI in video surveillance market during the forecast period due to the mounting demand for intelligent analytics and centralized video management capabilities. Organizations are rapidly adopting AI-powered software solutions, such as video management systems, facial recognition, object detection, and behavior analytics, to enhance security and operational insights. The shift toward cloud-based platforms and subscription models further supports scalability and cost efficiency. Continuous advancements in deep learning and computer vision are improving accuracy and automation, making software a critical component in modern surveillance ecosystems across industries globally.

"By function, the training segment to grow at the highest CAGR between 2026 and 2032"

The training function is anticipated to witness the highest CAGR in the AI in video surveillance market during the forecast, owing to the growing need for developing and refining AI models that can accurately detect, classify, and respond to complex visual scenarios. As surveillance systems become increasingly sophisticated, continuous training of deep learning algorithms using vast datasets is essential to improve accuracy, reduce false positives, and enhance real-time decision-making capabilities. Organizations across sectors are investing heavily in training infrastructure to ensure their AI surveillance models remain adaptive to evolving threats and environments. Furthermore, advancements in edge computing and cloud-based training platforms are significantly accelerating this growth trajectory.

"Asia Pacific to emerge as the fastest-growing region in the AI in video surveillance market from 2026 to 2032"

Asia Pacific is emerging as the fastest-growing region in the AI in video surveillance market during the forecast period due to the rapid urbanization, increasing investments in smart city projects, and rising security concerns across densely populated countries. Governments and enterprises are heavily investing in advanced surveillance infrastructure to enhance public safety and traffic management. The presence of major manufacturing hubs and technology providers further supports regional growth. Additionally, expanding adoption across sectors such as retail, transportation, and critical infrastructure, combined with favorable government initiatives and digital transformation strategies, is accelerating market expansion across the region.

Breakdown of primaries

A variety of executives from key organizations operating in the AI in video surveillance market were interviewed in-depth, including CEOs, marketing directors, and innovation and technology directors.

- By Company Type: Tier 1 - 38%, Tier 2 - 28%, and Tier 3 - 34%

- By Designation: C-level Executives - 40%, Directors - 30%, and Others - 30%

- By Region: North America - 35%, Europe - 35, Asia Pacific - 20%, and RoW - 10%

Note: RoW includes the Middle East, Africa, and South America.

Other designations include product, sales, and marketing managers.

Three tiers of companies have been defined based on their total revenues: tier 3: revenue less than USD 100 million; tier 2: revenue between USD 100 million and USD 1 billion; and tier 1: revenue more than USD 1 billion.

Major players are as follows: Major players operating in AI in video surveillance market include Hangzhou Hikvision Digital Technology Co., Ltd. (China), Dahua Technology Co., Ltd. (China), Axis Communications AB (Sweden), Motorola Solutions, Inc. (US), Hanwha Vision Co., Ltd. (South Korea), Milestone Systems A/S (Denmark), SenseTime (Hong Kong), Irisity (Sweden), NEC Corporation (Japan), Genetec Inc. (Canada), MOBOTIX AG (Germany), Teledyne Technologies Incorporated (US), Honeywell International Inc. (US), VIVOTEK Inc. (Taiwan), and i-PRO Co., Ltd. (Japan). These companies compete by continuously enhancing AI-powered video surveillance capabilities, focusing on improved accuracy in object detection, facial recognition, behavior analysis, and real-time threat identification across diverse applications. Strategic emphasis is placed on scalable and interoperable system architectures, integration with cloud platforms, edge computing, and IoT ecosystems, along with the development of application-specific solutions for sectors such as smart cities, retail, transportation, healthcare, and critical infrastructure.

Market participants prioritize seamless integration with existing security and IT infrastructure, ensuring data security, system reliability, and ease of deployment. Strong focus is also placed on reducing false alarms, optimizing data storage, and enabling predictive analytics for proactive decision-making. Continued investments in advanced AI algorithms, cybersecurity enhancements, edge-enabled devices, and collaborations with system integrators, governments, and enterprises are expected to sustain competition and accelerate adoption across the global AI in video surveillance market.

The study provides a detailed competitive analysis of these key players in the AI in video surveillance market, presenting their company profiles, most recent developments, and key market strategies.

Research Coverage

This report on the AI in video surveillance market presents a detailed analysis based on offering, deployment, function, technology, vertical, and region. By offering, it is segmented into AI cameras and software. By deployment, the market is segmented into edge-based and cloud-based. By function, it is segmented into training and inference. By technology, the market includes computer vision (ML/DL), machine learning (non-vision AI), natural language processing, and generative AI. By vertical, the market covers residential, commercial, military & defense, government & public facility, industrial, and critical infrastructure. The regional analysis includes North America, Europe, Asia Pacific, and RoW, enabling evaluation of demand patterns, growth drivers, and industry trends across the global AI in video surveillance market.

Reasons to buy the report

The report will help the leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall market and the sub-segments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the AI in video surveillance market and provides information on key market drivers, restraints, challenges, and opportunities.

Key Benefits of Buying the Report

- Analysis of key drivers (Growing demand for enhanced and intelligent security solutions across sectors, Rapid advancements in deep learning and computer vision capabilities, Increasing incidence of crime driving adoption of surveillance systems, Rising deployment of advanced surveillance infrastructure in smart city initiatives), Restraints (Concerns related to data privacy and security in AI-enabled surveillance systems, High implementation and lifecycle costs), Opportunities (Rising integration of AI with IoT-enabled devices and ecosystems, Increasing penetration of smart home technologies globally, Rising adoption of AI-driven surveillance across retail and transportation sectors, Continuous evolution of AI cameras with advanced machine learning capabilities, Growing adoption of generative AI technologies, particularly in emerging economies), Challenges (Fragmented and complex data protection regulations across regions, Occurrence of false negatives, Increasing exposure to cybersecurity threats and system vulnerabilities) influencing the growth of the AI in video surveillance market

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the AI in video surveillance market

- Market Development: Comprehensive information about lucrative markets-the report analyses the AI in video surveillance market across varied regions

- Market Diversification: Exhaustive information about new products/services, untapped geographies, recent developments, and investments in the AI in video surveillance market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Hangzhou Hikvision Digital Technology Co., Ltd. (China), Dahua Technology Co., Ltd. (China), Axis Communications AB (Sweden), Motorola Solutions, Inc. (US), Hanwha Vision Co., Ltd. (South Korea), Milestone Systems A/S (Denmark), SenseTime (Hong Kong), Irisity (Sweden), NEC Corporation (Japan), Genetec Inc. (Canada), MOBOTIX AG (Germany), Teledyne Technologies Incorporated (US), Honeywell International Inc. (US), VIVOTEK Inc. (Taiwan), and i-PRO Co., Ltd. (Japan)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN AI IN VIDEO SURVEILLANCE MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AI IN VIDEO SURVEILLANCE MARKET

- 3.2 AI IN VIDEO SURVEILLANCE MARKET, BY OFFERING

- 3.3 AI IN VIDEO SURVEILLANCE MARKET, BY DEPLOYMENT

- 3.4 AI IN VIDEO SURVEILLANCE MARKET, BY FUNCTION

- 3.5 AI IN VIDEO SURVEILLANCE MARKET, BY TECHNOLOGY

- 3.6 AI IN VIDEO SURVEILLANCE MARKET, BY VERTICAL

- 3.7 AI IN VIDEO SURVEILLANCE MARKET IN NORTH AMERICA, BY VERTICAL AND COUNTRY

- 3.8 AI IN VIDEO SURVEILLANCE MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing demand for advanced security solutions

- 4.2.1.2 Advancements in deep learning and computer vision technologies

- 4.2.1.3 Rising crime rate

- 4.2.1.4 Deployment of sophisticated surveillance systems in smart cities

- 4.2.2 RESTRAINTS

- 4.2.2.1 Privacy and security issues in AI-powered systems

- 4.2.2.2 High costs associated with implementing and maintaining AI-powered video surveillance systems

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration of AI with IoT

- 4.2.3.2 Growing adoption of smart home technologies

- 4.2.3.3 Deployment of AI in retail and transportation sectors

- 4.2.3.4 Integration of AI cameras with ML algorithms

- 4.2.3.5 Adoption of Gen AI technologies in developing countries

- 4.2.4 CHALLENGES

- 4.2.4.1 Complex and varied data protection laws across different regions

- 4.2.4.2 Occurrence of false negatives

- 4.2.4.3 Vulnerability to cyberattacks

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 THREAT OF NEW ENTRANTS

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN RESIDENTIAL VERTICAL

- 5.2.4 TRENDS IN COMMERCIAL VERTICAL

- 5.2.5 TRENDS IN MILITARY & DEFENSE VERTICAL

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICING OF AI CAMERA OFFERINGS, BY KEY PLAYER, 2025

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION, 2021-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 852580)

- 5.6.2 EXPORT SCENARIO (HS CODE 852580)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 IMPROVING PUBLIC PARK SAFETY USING AUTOMATED VIDEO MONITORING SYSTEMS

- 5.10.2 MOBOTIX AG CAMERAS SUPPORT CRIME PREVENTION FOR WESTCHESTER COUNTY RTC

- 5.10.3 BRIEFCAM ANALYTICS SUPPORTS SECURITY OPERATIONS AT HOSPITAL CAMPUS

- 5.10.4 MINISO ENHANCES LOSS PREVENTION USING HIKVISION DIGITAL TECHNOLOGY SYSTEMS

- 5.10.5 DAHUA TECHNOLOGY IMPLEMENTS HYBRID SURVEILLANCE FOR ECOISLAMIC BANK IN KYRGYZSTAN

- 5.10.6 LONG BEACH HOUSING AUTHORITY IMPLEMENTS AVIGILON VIDEO MANAGEMENT SYSTEM

- 5.11 IMPACT OF 2025 US TARIFF - AI IN VIDEO SURVEILLANCE MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Machine learning

- 6.1.1.2 Computer vision

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Internet of Things (IoT)

- 6.1.2.2 5G connectivity

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Smart city infrastructure

- 6.1.3.2 Smart home automation

- 6.1.1 KEY TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.3 PATENT ANALYSIS

- 6.4 IMPACT OF AI/GEN AI ON AI IN VIDEO SURVEILLANCE MARKET

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

- 6.4.1.1 AI-enabled real-time threat detection and public safety

- 6.4.1.2 Intelligent traffic monitoring and management

- 6.4.1.3 Retail analytics and customer behavior insights

- 6.4.1.4 Industrial safety and operational monitoring

- 6.4.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS IN AI IN VIDEO SURVEILLANCE MARKET

- 6.4.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN AI IN VIDEO SURVEILLANCE MARKET

- 6.4.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.4.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED VIDEO SURVEILLANCE

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 STANDARDS

- 7.1.3 REGULATIONS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.5 UNMET NEEDS OF VARIOUS END-USE INDUSTRIES

- 8.6 MARKET PROFITABILITY

- 8.6.1 REVENUE POTENTIAL

- 8.6.2 COST DYNAMICS

- 8.6.3 MARGIN OPPORTUNITIES, BY VERTICAL

9 APPLICATIONS OF AI IN VIDEO SURVEILLANCE

- 9.1 INTRODUCTION

- 9.2 SECURITY & PUBLIC SAFETY

- 9.3 TRAFFIC MONITORING & MANAGEMENT

- 9.4 INTELLIGENT TRANSPORTATION SYSTEMS

- 9.5 RETAIL MANAGEMENT

- 9.6 URBAN PLANNING & SMART CITIES

10 AI IN VIDEO SURVEILLANCE MARKET, BY OFFERING

- 10.1 INTRODUCTION

- 10.2 AI CAMERAS

- 10.2.1 BY CAMERA TYPE

- 10.2.1.1 Fixed cameras

- 10.2.1.1.1 Growing emphasis on perimeter security and asset protection to accelerate market growth

- 10.2.1.2 PTZ cameras

- 10.2.1.2.1 Growing demand for intelligent, adaptable surveillance solutions to drive adoption

- 10.2.1.3 Dome cameras

- 10.2.1.3.1 Evolving versatile tools that combine security with business intelligence to propel market growth

- 10.2.1.4 Bullet cameras

- 10.2.1.4.1 Increasing adoption of AI-powered bullet cameras for advanced perimeter and infrastructure security to drive market

- 10.2.1.5 Panoramic/Fisheye/Body-worn cameras

- 10.2.1.5.1 Increasing demand for accountability and transparency to drive adoption

- 10.2.1.1 Fixed cameras

- 10.2.1 BY CAMERA TYPE

- 10.3 SOFTWARE

- 10.3.1 AI-DRIVEN VIDEO MANAGEMENT SYSTEMS

- 10.3.1.1 Centralized control of multiple cameras provides efficient management of operations

- 10.3.2 AI-DRIVEN VIDEO ANALYTICS

- 10.3.2.1 Growing demand for real-time intelligence to drive adoption

- 10.3.2.2 By use case

- 10.3.2.2.1 Object detection & classification

- 10.3.2.2.2 Facial recognition

- 10.3.2.2.3 Behavior & anomaly detection

- 10.3.2.2.4 Crowd analytics & density estimation

- 10.3.2.2.5 License plate recognition (LPR/ANPR)

- 10.3.2.2.6 Intrusion detection & perimeter security

- 10.3.2.2.7 Weapon & threat detection

- 10.3.2.2.8 Retail & customer behavior analytics

- 10.3.1 AI-DRIVEN VIDEO MANAGEMENT SYSTEMS

11 AI IN VIDEO SURVEILLANCE MARKET, BY DEPLOYMENT

- 11.1 INTRODUCTION

- 11.2 EDGE-BASED

- 11.2.1 INCREASING DEMAND FOR HIGHLY CUSTOMIZABLE, AI-INTEGRATED SURVEILLANCE SOLUTIONS TO ACCELERATE SEGMENTAL GROWTH

- 11.3 CLOUD-BASED

- 11.3.1 RISING PREFERENCE FOR REMOTE ACCESSIBILITY AND REAL-TIME MONITORING TO BOOST SEGMENTAL GROWTH

12 AI IN VIDEO SURVEILLANCE MARKET, BY FUNCTION

- 12.1 INTRODUCTION

- 12.2 TRAINING

- 12.2.1 INCREASING COMPLEXITY OF SURVEILLANCE TASKS TO CONTRIBUTE TO SEGMENTAL GROWTH

- 12.3 INFERENCE

- 12.3.1 RISING DEMAND FOR REAL-TIME THREAT DETECTION TO AUGMENT SEGMENTAL GROWTH

13 AI IN VIDEO SURVEILLANCE MARKET, BY TECHNOLOGY

- 13.1 INTRODUCTION

- 13.2 COMPUTER VISION

- 13.2.1 NEED FOR ADVANCED PROCESSING CAPABILITIES TO BOOST SEGMENTAL GROWTH

- 13.2.2 DEEP LEARNING

- 13.2.3 CONVOLUTIONAL NEURAL NETWORKS

- 13.3 MACHINE LEARNING

- 13.3.1 ABILITY TO INTELLIGENTLY ANALYZE AND INTERPRET VIDEO DATA TO BOLSTER SEGMENTAL GROWTH

- 13.4 NATURAL LANGUAGE PROCESSING

- 13.4.1 ABILITY TO ENHANCE VIDEO SURVEILLANCE SYSTEMS TO EXPEDITE SEGMENTAL GROWTH

- 13.5 GENERATIVE AI

- 13.5.1 STRONG FOCUS ON ENHANCING TRAINING, SIMULATION, AND PREDICTIVE CAPABILITIES TO ACCELERATE SEGMENTAL GROWTH

- 13.5.2 RULE-BASED MODELS

- 13.5.3 STATISTICAL MODELS

14 AI IN VIDEO SURVEILLANCE MARKET, BY VERTICAL

- 14.1 INTRODUCTION

- 14.2 RESIDENTIAL

- 14.2.1 RISING ADOPTION OF SMART CITY INITIATIVES TO BOOST SEGMENTAL GROWTH

- 14.3 COMMERCIAL

- 14.3.1 RETAIL STORES & MALLS

- 14.3.1.1 Requirement for comprehensive surveillance across large areas using advanced tools to fuel segmental growth

- 14.3.2 BANKING & FINANCIAL BUILDINGS

- 14.3.2.1 Emphasis on safeguarding data and infrastructure to contribute to segmental growth

- 14.3.3 HOSPITALITY CENTERS

- 14.3.3.1 Increased demand for enhanced guest security solutions to stimulate segmental growth

- 14.3.1 RETAIL STORES & MALLS

- 14.4 MILITARY & DEFENSE

- 14.4.1 BORDER SURVEILLANCE

- 14.4.1.1 Rising focus on preventing smuggling and other illegal activities to drive segmental growth

- 14.4.2 COASTAL SURVEILLANCE

- 14.4.2.1 Growing intrusion and maritime threats to boost segmental growth

- 14.4.1 BORDER SURVEILLANCE

- 14.5 GOVERNMENT & PUBLIC FACILITIES

- 14.5.1 LAW ENFORCEMENT BUILDINGS

- 14.5.1.1 Increasing adoption of AI and ML in video surveillance systems to accelerate segmental growth

- 14.5.2 TRANSPORTATION FACILITIES

- 14.5.2.1 Rising integration of AI with real-time traffic monitoring solutions to foster segmental growth

- 14.5.3 SMART CITY SURVEILLANCE

- 14.5.3.1 Growing emphasis on enhancing public safety and law enforcement to foster market growth

- 14.5.4 HEALTHCARE FACILITIES

- 14.5.4.1 Increasing installation of intelligent video surveillance systems for threat detection to augment segmental growth

- 14.5.5 EDUCATIONAL FACILITIES

- 14.5.5.1 Growing investments in AI systems to enhance security to fuel segmental growth

- 14.5.6 RELIGIOUS FACILITIES

- 14.5.6.1 Rising need to safeguard artifacts and prevent firearm threats to contribute to segmental growth

- 14.5.1 LAW ENFORCEMENT BUILDINGS

- 14.6 INDUSTRIAL

- 14.6.1 MANUFACTURING

- 14.6.1.1 Rising integration of advanced technologies to optimize workflows and ensure safety compliance to drive market

- 14.6.2 ENERGY & UTILITIES

- 14.6.2.1 Escalating use of motion detection, automated alerts, and high-resolution cameras to accelerate segmental growth

- 14.6.3 CONSTRUCTION SITES

- 14.6.3.1 Increasing focus on meeting safety regulations to drive market

- 14.6.1 MANUFACTURING

- 14.7 CRITICAL INFRASTRUCTURE

- 14.7.1 DATA CENTERS

- 14.7.1.1 Growing adoption of surveillance cameras to safeguard critical assets to fuel segmental growth

- 14.7.2 TELECOMMUNICATIONS

- 14.7.2.1 Rising need for enhanced security and operational efficiency to augment segmental growth

- 14.7.1 DATA CENTERS

15 AI IN VIDEO SURVEILLANCE MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 15.2.2 US

- 15.2.2.1 Rising demand for smart surveillance systems to foster market growth

- 15.2.3 CANADA

- 15.2.3.1 Increasing break-and-enter cases to boost market growth

- 15.2.4 MEXICO

- 15.2.4.1 Growing affordability of AI CCTV technology to fuel market growth

- 15.3 EUROPE

- 15.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 15.3.2 UK

- 15.3.2.1 Rising public-private collaborations to offer lucrative growth opportunities

- 15.3.3 GERMANY

- 15.3.3.1 Growing demand for efficient and effective surveillance solutions to stimulate market growth

- 15.3.4 FRANCE

- 15.3.4.1 Growing emphasis on smart urban development to fuel market growth

- 15.3.5 ITALY

- 15.3.5.1 Rising integration of advanced AI-driven analytics into surveillance systems to drive market

- 15.3.6 SPAIN

- 15.3.6.1 Increasing deployment of 5G-enabled facial recognition surveillance systems to boost market growth

- 15.3.7 REST OF EUROPE

- 15.4 ASIA PACIFIC

- 15.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 15.4.2 CHINA

- 15.4.2.1 Surging need for real-time threat detection to foster market growth

- 15.4.3 JAPAN

- 15.4.3.1 Expanding commercial establishments to accelerate demand

- 15.4.4 SOUTH KOREA

- 15.4.4.1 Strong government-led smart city programs and nationwide digital transformation initiatives to propel market

- 15.4.5 INDIA

- 15.4.5.1 Rising emphasis on developing smart cities to fuel market growth

- 15.4.6 SOUTHEAST ASIA

- 15.4.6.1 Rapid urbanization and increasing investments in smart city projects to drive market

- 15.4.7 AUSTRALIA

- 15.4.7.1 Strong regulatory frameworks to support market growth

- 15.4.8 REST OF ASIA PACIFIC

- 15.5 ROW

- 15.5.1 MACROECONOMIC OUTLOOK FOR ROW

- 15.5.2 MIDDLE EAST

- 15.5.2.1 Bahrain

- 15.5.2.1.1 Digital transformation initiatives to propel market

- 15.5.2.2 Kuwait

- 15.5.2.2.1 Increasing focus on national security and infrastructure resilience to propel market

- 15.5.2.3 Oman

- 15.5.2.3.1 Government initiatives to drive market

- 15.5.2.4 Qatar

- 15.5.2.4.1 Rising government investments in AI-enabled smart city and digital infrastructure projects to accelerate market growth

- 15.5.2.5 Saudi Arabia

- 15.5.2.5.1 Rising investments in digital transformation and security infrastructure to drive adoption

- 15.5.2.6 UAE

- 15.5.2.6.1 Smart city initiatives to support market growth

- 15.5.2.7 Rest of Middle East

- 15.5.2.1 Bahrain

- 15.5.3 AFRICA

- 15.5.3.1 South Africa

- 15.5.3.1.1 Focus on smart city development and digital transformation systems to drive market

- 15.5.3.2 Rest of Africa

- 15.5.3.1 South Africa

- 15.5.4 SOUTH AMERICA

- 15.5.4.1 Brazil

- 15.5.4.1.1 Government initiatives on enhancing public safety through intelligent monitoring systems to propel growth

- 15.5.4.2 Argentina

- 15.5.4.2.1 Need to improve public safety and urban management to propel market

- 15.5.4.3 Rest of South America

- 15.5.4.1 Brazil

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 16.3 REVENUE ANALYSIS, 2020-2024

- 16.4 MARKET SHARE ANALYSIS, 2025

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS, 2025

- 16.6 BRAND COMPARISON

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Offering footprint

- 16.7.5.4 Deployment footprint

- 16.7.5.5 Function footprint

- 16.7.5.6 Vertical footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 16.8.5.1 Detailed list of key startups/SMEs

- 16.8.5.2 Competitive benchmarking of key startups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 HANGZHOU HIKVISION DIGITAL TECHNOLOGY CO., LTD.

- 17.1.1.1 Business overview

- 17.1.1.2 Products/Solutions/Services offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches

- 17.1.1.3.2 Deals

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths/Right to win

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses/Competitive threats

- 17.1.2 DAHUA TECHNOLOGY CO., LTD.

- 17.1.2.1 Business overview

- 17.1.2.2 Products/Solutions/Services offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths/Right to win

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses/Competitive threats

- 17.1.3 AXIS COMMUNICATIONS AB

- 17.1.3.1 Business overview

- 17.1.3.2 Products/Solutions/Services offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches

- 17.1.3.3.2 Deals

- 17.1.3.3.3 Other developments

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths/Right to win

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses/Competitive threats

- 17.1.4 MOTOROLA SOLUTIONS, INC. (AVIGILON CORPORATION)

- 17.1.4.1 Business overview

- 17.1.4.2 Products/Solutions/Services offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches

- 17.1.4.3.2 Deals

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths/Right to win

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses/Competitive threats

- 17.1.5 HANWHA VISION CO., LTD.

- 17.1.5.1 Business overview

- 17.1.5.2 Products/Solutions/Services offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product launches

- 17.1.5.3.2 Deals

- 17.1.5.4 MnM view

- 17.1.5.4.1 Key strengths/Right to win

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses/Competitive threats

- 17.1.6 MILESTONE SYSTEMS A/S

- 17.1.6.1 Business overview

- 17.1.6.2 Products/Solutions/Services offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches

- 17.1.6.3.2 Deals

- 17.1.7 SENSETIME

- 17.1.7.1 Business overview

- 17.1.7.2 Products/Solutions/Services offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches

- 17.1.7.3.2 Deals

- 17.1.8 IRISITY

- 17.1.8.1 Business overview

- 17.1.8.2 Products/Solutions/Services offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches

- 17.1.8.3.2 Deals

- 17.1.9 NEC CORPORATION

- 17.1.9.1 Business overview

- 17.1.9.2 Products/Solutions/Services offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Product launches

- 17.1.9.3.2 Deals

- 17.1.10 GENETEC INC.

- 17.1.10.1 Business overview

- 17.1.10.2 Products/Solutions/Services offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Product launches

- 17.1.10.3.2 Deals

- 17.1.11 MOBOTIX AG

- 17.1.11.1 Business overview

- 17.1.11.2 Products/Solutions/Services offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Product launches

- 17.1.11.3.2 Deals

- 17.1.12 TELEDYNE TECHNOLOGIES INCORPORATED

- 17.1.12.1 Business overview

- 17.1.12.2 Products/Solutions/Services offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Product launches

- 17.1.12.3.2 Other developments

- 17.1.13 HONEYWELL INTERNATIONAL INC.

- 17.1.13.1 Business overview

- 17.1.13.2 Products/Solutions/Services offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Deals

- 17.1.14 VIVOTEK INC.

- 17.1.14.1 Business overview

- 17.1.14.2 Products/Solutions/Services offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Product launches

- 17.1.14.3.2 Deals

- 17.1.15 I-PRO CO., LTD.

- 17.1.15.1 Business overview

- 17.1.15.2 Products/Solutions/Services offered

- 17.1.15.3 Recent developments

- 17.1.15.3.1 Product launches

- 17.1.15.3.2 Deals

- 17.1.1 HANGZHOU HIKVISION DIGITAL TECHNOLOGY CO., LTD.

- 17.2 OTHER PLAYERS

- 17.2.1 VERKAINCINC.

- 17.2.2 MORPHEAN SA

- 17.2.3 BOSCH SICHERHEITSSYSTEME GMBH

- 17.2.4 AXXONSOFT

- 17.2.5 CAMCLOUD

- 17.2.6 IVIDEON

- 17.2.7 HAKIMO, INC.

- 17.2.8 PROMISEQ GMBH

- 17.2.9 RHOMBUS SYSTEMS

- 17.2.10 UMBO COMPUTER VISION INC.

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 List of key secondary sources

- 18.1.1.2 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 List of primary interview participants

- 18.1.2.2 Breakdown of primaries

- 18.1.2.3 Key data from primary sources

- 18.1.2.4 Key industry insights

- 18.1.3 SECONDARY AND PRIMARY RESEARCH

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION

- 18.2.1 BOTTOM-UP APPROACH

- 18.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 18.2.2 TOP-DOWN APPROACH

- 18.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

- 18.2.3 DEMAND-SIDE ANALYSIS

- 18.2.4 SUPPLY-SIDE ANALYSIS

- 18.2.1 BOTTOM-UP APPROACH

- 18.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 18.4 RESEARCH ASSUMPTIONS

- 18.5 RISK ASSESSMENT

- 18.6 RESEARCH LIMITATIONS

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS