|

시장보고서

상품코드

2048959

테크니컬 세라믹 시장 : 소재별, 제품 유형별, 최종 이용 산업별, 지역별 - 세계 예측(-2031년)Technical Ceramics Market, By Material, Product Type, End-use Industry, and Region - Global Forecast To 2031 |

||||||

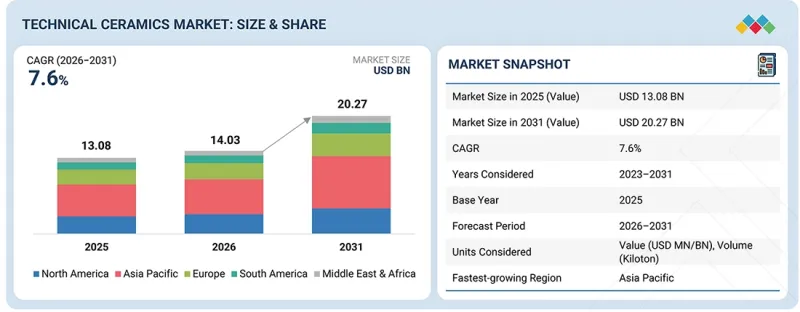

테크니컬 세라믹 시장 규모는 2026년에는 140억 3,000만 달러, 2031년까지 202억 7,000만 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR 7.6%를 기록할 것으로 전망됩니다.

극한의 기계적, 열적, 화학적 조건을 견딜 수 있는 재료에 대한 수요가 증가함에 따라 세계 테크니컬 세라믹 시장은 빠르게 성장하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2023-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(100만/10억 달러), 킬로톤 |

| 부문 | 소재별, 제품 유형별, 최종 이용 산업별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

세계 시장의 성장을 이끄는 요인으로는 빠르게 성장하는 반도체 제조 부문, 전기자동차 생산, 재생에너지 인프라 개발, 항공우주 분야의 지속적인 발전, 의료 기술 분야의 빠른 혁신 등이 있습니다. 또한, 에너지 효율에 대한 강한 집중, 재료 혁신, 성능 및 신뢰성에 대한 엄격한 규제 요건은 주요 산업 분야에서 첨단 기술 세라믹의 채택을 확대하는 데 기여할 것입니다.

"2026년부터 2031년까지 테크니컬 세라믹 시장에서 비산화물 부문이 가장 빠르게 성장하는 재료가 될 것으로 예상됩니다."

테크니컬 세라믹 시장에서 비산화물 세라믹은 고온 및 고응력 환경에서의 우수한 성능으로 인해 예측 기간 동안 두 번째로 높은 성장률을 보일 것으로 예상됩니다. 탄화규소 및 질화규소계 재료는 높은 기계적 강도, 높은 열전도율, 마모, 산화, 화학제품에 대한 높은 내성을 가지고 있습니다. 비산화물 세라믹의 높은 비용은 의료, 자동차, 에너지 및 전력, 그리고 다양한 산업 분야에서 고성능 응용 분야에서 이러한 재료의 역할에 의해 정당화됩니다.

"2026년 자동차 부문이 두 번째로 큰 시장 점유율을 차지할 것으로 예상"

자동차 산업은 자동차의 모든 시스템에서 고성능 소재를 사용하는 추세가 증가함에 따라 2026년 시장 점유율 2위를 차지할 것으로 예상됩니다. 자동차 산업에서 테크니컬 세라믹의 다른 응용 분야에는 열적 및 기계적 강도 특성으로 인해 센서, 브레이크, 전자 제어 시스템 등 다양한 부품이 포함됩니다. 전기자동차의 이용이 확대됨에 따라 테크니컬 세라믹의 채택이 빠르게 진행되고 있습니다. 또한, 자동차 부품에 적용 시 연비 향상, 배기가스 배출 감소, 내구성 향상 등 테크니컬 세라믹의 입증된 이점이 이 부문을 주도하고 있습니다.

"2031년 아시아태평양이 테크니컬 세라믹 시장에서 가장 큰 점유율을 차지할 것으로 예상"

2031년까지 테크니컬 세라믹 시장에서 아시아태평양이 가장 빠른 매출 성장을 보일 것으로 예상됩니다. 이러한 성장에 기여하는 요인으로는 급속한 산업화, 전자기기 및 반도체 제조 확대, 전기자동차 제조 거점의 급속한 확대, 재생에너지에 대한 인프라 투자 등을 들 수 있습니다. 경제 발전, 도시화, 첨단 제조 기술에 대한 지속적인 투자로 인해 하이테크 세라믹 재료에 대한 수요가 크게 증가할 것입니다. 세계 유수의 제조업체들이 이 지역에서 반도체, 소비자 전자제품, 자동차 제품을 생산하고 있기 때문에 이 지역은 기술용 세라믹 분야에서 가장 큰 고객 기반을 가질 수 있습니다. 중국, 일본, 한국, 인도는 자국의 제조 생태계를 활용하고 연방 정부의 이니셔티브와 연계하여 첨단 소재 연구개발 및 제조에 대한 투자를 통해 경제 발전을 도모하고 있습니다. 이러한 요인들이 전자, 자동차, 에너지, 의료 및 산업 응용 분야의 기술 세라믹 시장을 주도하고 있습니다.

대상 기업 : KYOCERA Corporation(일본), CoorsTek, Inc.(미국), CeramTec GmbH(독일), Morgan Advanced Materials plc(영국), Saint-Gobain Performance Ceramics & Co. Refractories(프랑스), 3M(미국), Niterra(일본), AGC Ceramics(일본), Paul Rauschert GmbH & Co. KG(독일), Elan Technology(미국), OC Oerlikon Management AG(스위스).가 본 보고서의 대상입니다.

테크니컬 세라믹 시장의 주요 기업들에 대해 기업 프로파일, 최근 동향, 주요 시장 전략을 포함한 상세한 경쟁 분석을 실시하였습니다.

조사 범위

본 보고서는 테크니컬 세라믹 시장을 소재(산화물 및 비산화물), 제품 유형(모놀리식 세라믹, 세라믹 매트릭스 복합재료, 세라믹 코팅 및 기타 제품), 최종 이용 산업(전자·반도체, 자동차, 에너지 및 전력, 산업, 의료, 군 및 방위, 기타 최종 이용 산업)에 따라 분류하고 있습니다. 이 보고서의 범위에는 테크니컬 세라믹 시장의 성장에 영향을 미치는 촉진요인, 제약 조건, 과제 및 기회에 대한 자세한 정보가 포함되어 있습니다. 주요 업계 플레이어에 대한 상세한 분석을 통해 사업 개요, 제공 제품 및 테크니컬 세라믹 시장과 관련된 인수합병, 제품 출시, 사업 확장 등 주요 전략에 대한 인사이트를 제공합니다. 또한, 본 보고서에서는 테크니컬 세라믹 시장 생태계에서 부상하고 있는 스타트업 기업들의 경쟁 분석도 함께 다루고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 시장 리더와 신규 진입자에게 전체 테크니컬 세라믹 시장과 각 하위 부문의 매출에 대한 가장 정확한 추정치를 제공합니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 비즈니스 포지셔닝을 위한 인사이트를 강화하며, 적절한 시장 진입 전략을 수립하는 데 도움이 될 것입니다. 또한, 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

본 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인 분석(열악한 환경에서의 테크니컬 세라믹 수요 증가, 의료 및 전자 기술 혁신에 대한 집중), 제약요인(맞춤형 테크니컬 세라믹에 따른 높은 비용과 시간적 제약, 섬유 생산 지연), 기회(열적, 전기적, 기계적 성능 향상을 위한 나노 엔지니어링 세라믹 의존, 테크니컬 세라믹 혁신), 도전 과제(비용 상승을 초래하는 리소스 제약, 다양한 용도의 테크니컬 세라믹 도입을 제한하는 복잡성 및 비용) 나노 엔지니어링 세라믹에 대한 의존도, 테크니컬 세라믹의 혁신), 그리고 도전과제(비용 상승을 초래하는 리소스 제약, 다양한 용도에 테크니컬 세라믹의 도입을 제한하는 복잡성과 비용)가 있습니다.

- 제품 개발/혁신 : 테크니컬 세라믹 시장의 미래 기술, R&D 활동, 제품 및 서비스 출시에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 테크니컬 세라믹 시장을 분석합니다.

- 시장 다각화 : 테크니컬 세라믹 시장의 신제품 및 서비스, 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁사 분석 : KYOCERA Corporation(일본),CoorsTek, Inc.(미국),CeramTec GmbH(독일),Morgan Advanced Materials plc(영국),Saint-Gobain Performance Ceramics & Refractories(프랑스),3 M(미국), Niterra(일본), AGC Ceramics(일본), Paul Rauschert GmbH & Co. KG(독일), Elan Technology(미국), OC Oerlikon Management AG(스위스) 등 주요 기업의 시장 점유율, 성장 전략 서비스 제공 내용에 대한 상세한 평가

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI의 도입에 의한 전략적 파괴

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 테크니컬 세라믹 시장(소재별)

제10장 테크니컬 세라믹 시장(제품 유형별)

제11장 테크니컬 세라믹 시장(최종 이용 산업별)

제12장 테크니컬 세라믹 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

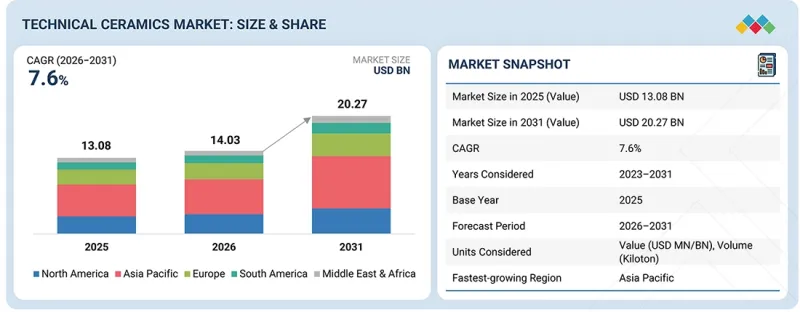

KSM 26.06.08The technical ceramics market is expected to be valued at USD 14.03 billion in 2026 and USD 20.27 billion by 2031, exhibiting a CAGR of 7.6% during the forecast period. The global market for technical ceramics is rapidly growing due to the increase in demand for materials that can endure extreme mechanical, thermal, and chemical conditions.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million/Billion), Volume (Kiloton) |

| Segments | Material, Product Type, End-use Industry, and Region |

| Regions covered | North America, Asia Pacific, Europe, the Middle East & Africa, and South America |

Factors that are driving global market growth include the rapidly expanding semiconductor manufacturing sector, the production of electric vehicles, the development of renewable energy infrastructure, ongoing aerospace advancements, and rapid innovations in the medical technology sector. In addition, the strong focus on energy efficiency, innovation in materials, and stringent regulatory requirements for performance and reliability will contribute to the greater adoption of advanced technical ceramics in critical industrial sectors.

"Non-oxide segment to be the fastest-growing material in the technical ceramics market from 2026 to 2031"

In the technical ceramics market, non-oxide ceramics in the material segment are expected to be the second-fastest-growing during the forecast period, owing to their superior performance in high-temperature and high-stress environments. Silicon carbide- and silicon nitride-based materials possess high mechanical strength, high thermal conductivity, and high resistance to wear, oxidation, and chemicals. The high cost of non-oxide ceramics is justified by the role these materials play in high-performance applications in the medical, automotive, energy & power, and various industries.

"Automotive segment to hold the second-largest market share in 2026"

The automotive industry ranks second in terms of market share in 2026, as there is an increasing trend to use high-performance materials on all types of systems in the automobile. Other applications for technical ceramics in the automotive industry include many components, including sensors, braking, and electronic control systems, due to the thermal and mechanical strength properties. The increase in the utilization of electric vehicles is resulting in the high acceptance of technical ceramics. Furthermore, the proven benefit of technical ceramics in the improvement of fuel economy, reduction of emissions, and increase in longevity by the utilization of these components in automobiles drives the segment.

"Asia Pacific to capture the largest share of the technical ceramics market in 2031"

It is anticipated that the technical ceramics market will see the fastest growth in revenue in the Asia Pacific region through 2031. Factors contributing to this growth will include the rapid industrialization, growth of manufacturing for electronics and semiconductors, the rapid expansion of the manufacturing base for electric vehicles, and infrastructure investments for renewable energy. Economic development, urbanization, and sustained investments in cutting-edge manufacturing will create a significant increase in demand for high-tech ceramic materials. Potentially, the region will have the largest customer base for technical ceramics, as many of the world's leading manufacturers produce semiconductors, consumer electronics, and automotive products in this area. China, Japan, South Korea, and India are leveraging their manufacturing ecosystems to couple with federal initiatives to create greater economic development through investment in research and manufacturing of advanced materials. These factors drive the technical ceramic market for electronics, automotive, energy, medical, and industrial applications.

By Company Type: Tier-1: 40%, Tier-2: 30%, and Tier-3: 30%

By Designation: Directors: 30%, Managers: 20%, and Others: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Others include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: KYOCERA Corporation(Japan), CoorsTek, Inc. (US), CeramTec GmbH (Germany), Morgan Advanced Materials plc (UK), Saint-Gobain Performance Ceramics & Refractories (France), 3M (US), Niterra Co., Ltd. (Japan), AGC Ceramics Co., Ltd. (Japan), Paul Rauschert GmbH & Co. KG. (Germany), Elan Technology (US), and OC Oerlikon Management AG (Switzerland) are covered in the report.

The study includes an in-depth competitive analysis of these key players in the technical ceramics market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the technical ceramics market based on Material (Oxide and Non-Oxide), Product Type (Monolithic Ceramics, Ceramic Matrix Composites, Ceramic Coatings, and Other Products), and End-use Industry (Electronics & Semiconductor, Automotive, Energy & Power, Industrial, Medical, Military & Defense, and Other End-use Industries). The report's scope covers detailed information regarding drivers, restraints, challenges, and opportunities influencing the growth of the technical ceramics market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as mergers, acquisitions, product launches, and expansions, associated with the technical ceramics market. This report covers a competitive analysis of upcoming startups in the technical ceramics market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall technical ceramics market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (Increased demand for technical ceramics in extreme environments, Focus on innovation in medical and electronic technologies), restraints (High costs and time associated with customized technical ceramics, Slow fiber production), opportunities (Reliance on nano-engineered ceramics to enhance thermal, electrical, and mechanical performance, Innovations of technical ceramics), and challenges (Limited resources driving up costs and Complexity and expenditure limiting entry of technical ceramics in diverse applications)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the technical ceramics market

- Market Development: Comprehensive information about profitable markets-the report analyzes the technical ceramics market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the technical ceramics market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as KYOCERA Corporation(Japan), CoorsTek, Inc. (US), CeramTec GmbH (Germany), Morgan Advanced Materials plc (UK), Saint-Gobain Performance Ceramics & Refractories (France), 3M (US), Niterra Co., Ltd. (Japan), AGC Ceramics Co., Ltd. (Japan), Paul Rauschert GmbH & Co. KG. (Germany), Elan Technology (US), and OC Oerlikon Management AG (Switzerland), among others

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN TECHNICAL CERAMICS MARKET

- 3.2 ASIA PACIFIC: TECHNICAL CERAMICS MARKET, BY MATERIAL AND COUNTRY

- 3.3 TECHNICAL CERAMICS MARKET, BY PRODUCT TYPE

- 3.4 TECHNICAL CERAMICS MARKET, BY END-USE INDUSTRY

- 3.5 TECHNICAL MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increased demand for technical ceramics in extreme environments

- 4.2.1.2 Technical ceramics drive innovation in medical and electronic technologies

- 4.2.2 RESTRAINTS

- 4.2.2.1 Higher costs and time associated with customized technical ceramics

- 4.2.2.2 High cost and slow fiber production restrict potential

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Nano-engineered ceramics enabling enhanced thermal, electrical, and mechanical performance

- 4.2.3.2 Innovations enhancing growth prospects of technical ceramics

- 4.2.4 CHALLENGES

- 4.2.4.1 Limited resources drive up costs

- 4.2.4.2 Complexity and high expenditure limit use in diverse applications

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN THE TECHNICAL CERAMICS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.4.2.1 Aerospace Industry -> Energy Industry

- 4.4.2.2 Medical Industry -> Dental Industry

- 4.4.2.3 Semiconductor Industry -> Automotive Electronics Industry

- 4.4.2.4 Industrial Ceramics Industry -> Oil & Gas Industry

- 4.4.2.5 Defense Ceramics Industry -> Law Enforcement & Personal Protection Industry

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING SCALE AND MATERIAL INNOVATION

- 4.5.1.1 Kyocera corporation: expansion of ceramic semiconductor components manufacturing

- 4.5.1.2 Coorstek inc.: strategic focus on bioceramics and medical ceramic expansion

- 4.5.2 TIER 2 PLAYERS: REGIONAL EXPANSION AND REGULATORY-LED INNOVATION

- 4.5.2.1 Ceramtec GMBH: expansion in medical and industrial ceramic segments

- 4.5.2.2 Morgan advanced materials: portfolio restructuring toward high-performance ceramics

- 4.5.3 TIER 3 PLAYERS: NICHE INNOVATORS AND TECHNOLOGY-DRIVEN EXPANSION

- 4.5.3.1 Precision ceramics USA: expansion of additive manufacturing ceramic capabilities

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING SCALE AND MATERIAL INNOVATION

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF SUBSTITUTES

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 THREAT OF NEW ENTRANTS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 PRICING ANALYSIS

- 5.4.1.1 Pricing analysis based on material type

- 5.4.1.2 Pricing analysis based on material

- 5.4.1.3 Pricing analysis based on region

- 5.4.1 PRICING ANALYSIS

- 5.5 TRADE ANALYSIS

- 5.5.1 EXPORT SCENARIO (HS CODE 690919)

- 5.5.2 IMPORT SCENARIO (HS CODE 690919)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 ADVANCING SATELLITE PROPULSION: ROLE OF AL300 ALUMINA IN HDLTFLOW

- 5.9.2 SHIFT FROM METAL TO CERAMIC IN WIRE PRODUCTION EFFICIENCY

- 5.9.3 ENHANCING ALUMINUM CASTING PROCESSES WITH SILICON NITRIDE

- 5.10 IMPACT OF 2025 US TARIFF: TECHNICAL CERAMICS MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 US

- 5.10.4.2 Canada

- 5.10.4.3 China

- 5.10.4.4 Europe

- 5.10.5 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ADVANCED CERAMIC SINTERING TECHNOLOGIES

- 6.1.2 PRECISION CERAMIC FORMING TECHNOLOGIES

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 CERAMIC ADDITIVE MANUFACTURING

- 6.2.2 ADVANCED CERAMIC COATING TECHNOLOGIES

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 METAL MATRIX COMPOSITE TECHNOLOGIES

- 6.3.2 HIGH-PERFORMANCE POLYMER TECHNOLOGIES

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | PROCESS OPTIMIZATION AND EARLY SMART INTEGRATION

- 6.4.2 MID-TERM (2027-2030) | ADVANCED MATERIAL INNOVATION AND SMART CERAMIC ECOSYSTEM INTEGRATION

- 6.4.3 LONG-TERM (2030-2035+) | AUTONOMOUS MANUFACTURING AND NET-ZERO CERAMIC SYSTEMS

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 METHODOLOGY

- 6.5.3 TECHNICAL CERAMICS MARKET, PATENT ANALYSIS, 2016-2025

- 6.6 FUTURE APPLICATIONS

- 6.6.1 SMART & SENSOR-EMBEDDED CERAMIC SYSTEMS FOR REAL-TIME STRUCTURAL MONITORING

- 6.6.2 CERAMIC MATRIX COMPOSITES (CMCS) FOR NEXT-GENERATION THERMAL & STRUCTURAL APPLICATIONS

- 6.6.3 WIDE-BANDGAP CERAMIC SUBSTRATES FOR POWER ELECTRONICS & SEMICONDUCTOR APPLICATIONS

- 6.6.4 BIOCERAMIC IMPLANTS & HERMETIC CERAMIC ENCLOSURES FOR ADVANCED MEDICAL DEVICES

- 6.7 IMPACT OF AI/GEN AI ON TECHNICAL CERAMICS MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN TECHNICAL CERAMICS - COMPANIES IMPLEMENTING USE CASES

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN TECHNICAL CERAMICS MARKET

- 6.7.3.1 Interconnected adjacent ecosystem and impact on market players

- 6.7.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN TECHNICAL CERAMICS MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 CERAMIC MATRIX COMPOSITES ENABLING NEXT-GENERATION JET ENGINE EFFICIENCY - GE AEROSPACE, USA

- 6.8.2 SILICON CARBIDE SUBSTRATES TRANSFORMING EV POWERTRAIN EFFICIENCY - WOLFSPEED & AUTOMOTIVE TIER-1S, USA/EUROPE

- 6.8.3 ADVANCED BIOCERAMIC IMPLANTS IMPROVING ORTHOPEDIC OUTCOMES - ZIMMER BIOMET, GLOBAL

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 LOW-CARBON MANUFACTURING AND ENERGY TRANSITION

- 7.2.2 SUSTAINABLE RAW MATERIAL SOURCING AND SUPPLY CHAIN RESPONSIBILITY

- 7.2.3 MATERIAL EFFICIENCY AND WASTE MINIMIZATION

- 7.2.4 EXTENDED SERVICE LIFE AND RESOURCE EFFICIENCY

- 7.2.5 SUSTAINABLE BIOCERAMICS AND MEDICAL APPLICATIONS

- 7.2.6 ADDITIVE MANUFACTURING AND DIGITAL PROCESS EFFICIENCY

- 7.2.7 END-OF-LIFE MANAGEMENT AND CERAMIC RECYCLING

- 7.3 IMPACT OF REGULATORY POLICY ON SUSTAINABILITY INITIATIVES

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES BY APPLICATION

9 TECHNICAL CERAMICS MARKET, BY MATERIAL

- 9.1 INTRODUCTION

- 9.2 OXIDE CERAMICS

- 9.2.1 HIGH FRACTURE TOUGHNESS AND HIGH WEAR, TEMPERATURE, AND CORROSION RESISTANCE PROPERTIES TO DRIVE MARKET

- 9.2.2 ALUMINA CERAMICS

- 9.2.2.1 Extreme hardness, thermal conductivity, chemical resistance, and compressive strength to drive market

- 9.2.3 TITANATE CERAMICS

- 9.2.3.1 Excellent resistance to chemicals and thermal shock to drive market

- 9.2.4 ZIRCONIA CERAMICS

- 9.2.4.1 Manufacturing of mechanical, automotive, and medical components to propel market

- 9.2.5 OTHER OXIDE MATERIALS

- 9.3 NON-OXIDE CERAMICS

- 9.3.1 HIGH STRENGTH, HARDNESS, ALONG WITH EXCELLENT RESISTANCE TO CORROSION AND WEAR, TO BOOST MARKET

- 9.3.2 ALUMINA NITRIDE

- 9.3.2.1 Extensive use in power and microelectronics applications to drive market

- 9.3.3 SILICON NITRIDE

- 9.3.3.1 Mechanical fatigue, creep resistance, and high fracture toughness at varied temperatures to propel market

- 9.3.4 SILICON CARBIDE

- 9.3.4.1 Increasing demand in nuclear energy, space technology, automobile, and marine engineering to drive market

- 9.3.5 OTHER NON-OXIDE MATERIALS

10 TECHNICAL CERAMICS MARKET, BY PRODUCT TYPE

- 10.1 INTRODUCTION

- 10.2 MONOLITHIC CERAMICS

- 10.2.1 RISING DEMAND FROM MEDICAL AND ELECTRICAL & ELECTRONICS INDUSTRIES TO DRIVE MARKET

- 10.3 CERAMIC MATRIX COMPOSITES

- 10.3.1 SUITABILITY FOR INTERNAL ENGINE COMPONENTS, EXHAUST SYSTEMS, AND OTHER HOT-ZONE STRUCTURES TO PROPEL MARKET

- 10.4 CERAMIC COATINGS

- 10.4.1 GROWING DEMAND FOR PLASMA-SPRAYED COATINGS IN SEMICONDUCTORS AND LCD EQUIPMENT TO DRIVE MARKET

- 10.5 OTHER PRODUCT TYPES

11 TECHNICAL CERAMICS MARKET, BY END-USE INDUSTRY

- 11.1 INTRODUCTION

- 11.2 ELECTRONICS & SEMICONDUCTOR

- 11.2.1 SURGE IN DEMAND IN CONSUMER ELECTRONICS, ROBOTICS, AUTOMOTIVE, SENSORS, AND INSTRUMENTATION TO DRIVE MARKET

- 11.2.2 ELECTRICAL INSULATORS

- 11.2.3 PASSIVE COMPONENTS

- 11.2.4 PIEZOELECTRIC CERAMICS

- 11.2.5 OTHER ELECTRONIC & SEMICONDUCTOR END-USE INDUSTRIES

- 11.3 AUTOMOTIVE

- 11.3.1 APPLICATION IN HIGH-PERFORMANCE VEHICLES, CERAMIC BRAKE COMPONENTS, AND ENGINE COMPONENTS TO BOOST MARKET

- 11.4 ENERGY & POWER

- 11.4.1 PRESSING NEED IN RENEWABLE ENERGY TECHNOLOGIES, SOLAR PANELS, AND FUEL CELLS TO DRIVE MARKET

- 11.5 INDUSTRIAL

- 11.5.1 RISING NEED FOR ABRASIVES IN MACHINERY AND CONSUMER GOODS INDUSTRIES TO DRIVE MARKET

- 11.6 MEDICAL

- 11.6.1 INCREASING DEMAND IN IMPLANTS, PROSTHETICS, AND SURGICAL INSTRUMENTS TO PROPEL MARKET

- 11.6.2 MEDICAL IMPLANTS

- 11.6.3 DENTAL CERAMICS

- 11.6.4 IMPLANTABLE ELECTRONIC DEVICES

- 11.6.5 OTHER MEDICAL APPLICATIONS

- 11.7 MILITARY & DEFENSE

- 11.7.1 RISE IN DEMAND FOR AIRCRAFT ENGINES, ARMOR PLATES, BODY ARMOR, AND DEFENSE-RELATED TECHNOLOGIES TO DRIVE MARKET

- 11.8 OTHER END-USE INDUSTRIES

12 TECHNICAL CERAMICS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Development of novel materials and sustainable use of technical ceramics to boost market

- 12.2.2 CANADA

- 12.2.2.1 Expanding applications in automotive and aerospace industries to drive market

- 12.2.3 MEXICO

- 12.2.3.1 Expansion of aerospace manufacturing, medical devices, and automotive production to drive market

- 12.2.1 US

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Advanced engineering excellence, automotive electrification, and industrial innovation to drive market

- 12.3.2 FRANCE

- 12.3.2.1 Expansion of healthcare, aerospace, and advanced electronics to drive market demand

- 12.3.3 SPAIN

- 12.3.3.1 Rising investments in electric mobility, chemicals, and medical technologies to propel market

- 12.3.4 UK

- 12.3.4.1 Significant demand for orthopedic implants and aircraft components to drive market

- 12.3.5 ITALY

- 12.3.5.1 Chemicals, renewable energy, and aerospace & defense sectors to boost demand

- 12.3.6 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 ASIA PACIFIC

- 12.4.1 CHINA

- 12.4.1.1 Strong manufacturing base, aerospace expansion, and medical innovation to drive market

- 12.4.2 JAPAN

- 12.4.2.1 Advanced electronics, aerospace leadership, and chemical industry strength to drive market

- 12.4.3 INDIA

- 12.4.3.1 Growth of aviation and electronics sectors to drive market

- 12.4.4 SOUTH KOREA

- 12.4.4.1 Strong semiconductor leadership, electronics exports, and aerospace manufacturing to drive market

- 12.4.5 REST OF ASIA PACIFIC

- 12.4.1 CHINA

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.5.1.1 Growing foreign investments and economic diversification to drive market

- 12.5.1.2 Saudi Arabia

- 12.5.1.2.1 Growth of aviation and medical sectors to drive market

- 12.5.1.3 UAE

- 12.5.1.3.1 Investments in aerospace infrastructure to propel market

- 12.5.1.4 Rest of GCC

- 12.5.2 SOUTH AFRICA

- 12.5.2.1 Healthcare & medical, mechanical equipment, chemical, and electronics industries to drive market

- 12.5.3 REST OF MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.6 SOUTH AMERICA

- 12.6.1 BRAZIL

- 12.6.1.1 Presence of major aerospace manufacturers and rapid growth of chemical industry to drive market

- 12.6.2 ARGENTINA

- 12.6.2.1 Rising consumer electronics and aviation industries to fuel market

- 12.6.3 REST OF SOUTH AMERICA

- 12.6.1 BRAZIL

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 13.3 MARKET SHARE ANALYSIS

- 13.4 REVENUE ANALYSIS OF KEY PLAYERS

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS

- 13.6 PRODUCT COMPARISON

- 13.7 COMPANY EVALUATION MATRIX

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.7.5.1 Company footprint

- 13.7.5.2 Company region footprint

- 13.7.5.3 Company material footprint

- 13.7.5.4 Company product type footprint

- 13.7.5.5 Company end-use industry footprint

- 13.8 STARTUP/SME EVALUATION MATRIX

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 COORSTEK, INC.

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Expansions

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 CERAMTEC GMBH

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches

- 14.1.2.3.2 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 KYOCERA CORPORATION

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Deals

- 14.1.3.3.2 Expansions

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 MORGAN ADVANCED MATERIALS PLC

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Deals

- 14.1.4.3.2 Expansions

- 14.1.4.4 MNM view

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 3M

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 MNM view

- 14.1.5.3.1 Right to win

- 14.1.5.3.2 Strategic choices

- 14.1.5.3.3 Weaknesses and competitive threats

- 14.1.6 SAINT-GOBAIN PERFORMANCE CERAMICS & REFRACTORIES

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 MNM view

- 14.1.7 NITERRA CO., LTD.

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Deals

- 14.1.7.4 MNM view

- 14.1.8 AGC CERAMICS CO., LTD.

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Deals

- 14.1.8.4 MNM view

- 14.1.9 PAUL RAUSCHERT GMBH & CO. KG.

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 MNM view

- 14.1.10 ELAN TECHNOLOGY

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 MNM view

- 14.1.11 OC OERLIKON MANAGEMENT AG

- 14.1.11.1 Business overview

- 14.1.11.2 Products/Solutions/Services offered

- 14.1.11.3 MNM view

- 14.1.1 COORSTEK, INC.

- 14.2 OTHER PLAYERS

- 14.2.1 JYOTI CERAMIC

- 14.2.2 TECHNOCERA

- 14.2.3 BCE SPECIAL CERAMICS GMBH

- 14.2.4 SUPERIOR TECHNICAL CERAMICS

- 14.2.5 DYSON TECHNICAL CERAMICS

- 14.2.6 ORTECH, INC.

- 14.2.7 INTERNATIONAL SYALONS (NEWCASTLE) LIMITED

- 14.2.8 BAKONY TECHNICAL CERAMICS LTD.

- 14.2.9 ADVANCED CERAMIC MATERIALS (ACM)

- 14.2.10 MCDANEL ADVANCED MATERIALS

- 14.2.11 ADVANCED CERAMICS MANUFACTURING

- 14.2.12 BLASCH PRECISION CERAMICS, INC.

- 14.2.13 PRECISION CERAMICS LIMITED

- 14.2.14 MANTEC TECHNICAL CERAMICS

- 14.2.15 K-TECH CERAMICS

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.3 BASE NUMBER CALCULATION

- 15.3.1 DEMAND-SIDE APPROACH

- 15.3.2 SUPPLY-SIDE APPROACH

- 15.4 MARKET FORECAST APPROACH

- 15.4.1 SUPPLY SIDE

- 15.4.2 DEMAND SIDE

- 15.5 DATA TRIANGULATION

- 15.6 FACTOR ANALYSIS

- 15.7 RESEARCH ASSUMPTIONS

- 15.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS