|

시장보고서

상품코드

2048960

의료 시뮬레이션 시장 : 제공별(해부 모델[환자용(고충실도), 외과용(복강경, 정형외과, 부인과), 트레이너, 초음파], 소프트웨어), 기술별(3D 프린팅, 가상 환자, 시술 리허설), 최종사용자별 - 세계 예측(-2030년)Medical Simulation Market by Offering (Anatomical Models [Patient (High Fidelity), Surgical (Laparoscopic, Ortho, Gynae), Trainers, Ultrasound], Software), Technology (3D Printing, Virtual Patient, Procedural Rehearsal), End User - Global Forecast 2030 |

||||||

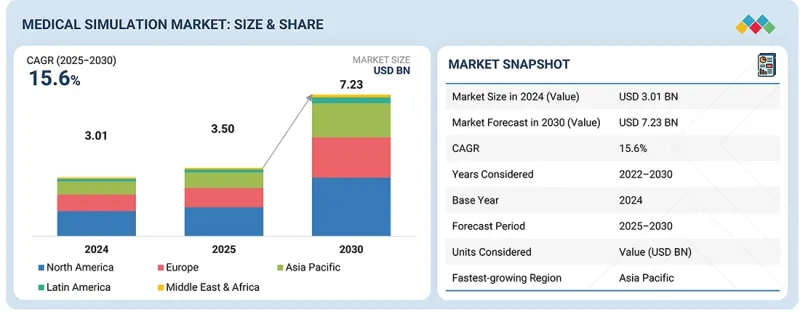

세계의 의료 시뮬레이션 시장 규모는 2025년 35억 달러에서 2030년에는 72억 3,000만 달러에 달할 것으로 예측되며, CAGR은 15.6%를 기록할 전망입니다.

의료 시뮬레이션 시장은 고급 임상 교육에 대한 수요 증가와 관련 인프라에 대한 투자 확대로 성장하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(달러) |

| 부문 | 제공, 기술, 최종사용자 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

University of Texas at Arlington은 2025년 3월에 Mobile Simulation Lab의 운영을 시작한다고 발표했습니다. 이는 텍사스주의 의료 서비스가 부족한 지역에 첨단 의학 교육을 제공하는 것을 목표로 하고 있으며, 시뮬레이션 기술이 기존의 학문적 기반을 넘어 실습 교육에 대한 접근성을 확대하고 있음을 보여줍니다.

"제공 부문별로는 해부학 모델이 가장 큰 점유율을 차지했습니다."

제공 부문별로는 해부 모형이 가장 큰 비중을 차지했습니다. 이는 기초 훈련 및 기술 연습에 널리 활용되고 있기 때문입니다. 이러한 물리적 모델은 학습자가 환자를 대면하기 전에 위험부담이 없는 환경에서 핵심 역량을 구축하는 데 도움이 됩니다. 예를 들어, Kyoto Kagaku는 초음파 검사 및 각종 시술 훈련을 위해 매우 정교한 해부학 팬텀을 제공하고 있습니다. 또한, Limbs & Things는 산부인과 및 응급의료 교육에 사용되는 사실적인 골반 모델과 신생아 모델을 제공하고 있습니다. 이러한 이유로 해부학 모델은 전 세계 의학 및 간호학 커리큘럼에서 없어서는 안 될 필수적인 요소로 자리 잡았습니다.

"기술별로는 2024년 수술 리허설 기술이 가장 큰 점유율을 차지했습니다."

이는 복잡한 의료 시술에 대한 실무적 실천에 대한 요구에 힘입은 것입니다. 이러한 기술을 통해 임상의는 정확도가 향상되고 수술 중 위험이 감소된 매우 사실적인 환자별 모델을 사용하여 수술을 시뮬레이션할 수 있습니다. 최소침습수술의 보급, 합병증 감소에 대한 관심 증가, 첨단 영상 진단 및 3D 모델링에 대한 투자 확대로 인해 도입이 더욱 가속화될 것입니다. 예를 들어, Surgical Science Sweden AB의 다양한 플랫폼은 외과 의사가 복강경 수술이나 내시경 수술을 가상 환경에서 미리 리허설할 수 있어 교육 및 수술 전 계획에서 이론과 실제의 간극을 효과적으로 메울 수 있습니다.

"예측 기간 동안 아시아태평양이 가장 빠른 성장률을 보이고 있습니다."

아시아태평양은 의료 인프라의 급속한 확장, 숙련된 임상 인력에 대한 수요 증가, 첨단 교육 솔루션의 도입 확대에 힘입어 의료 시뮬레이션 시장에서 가장 빠르게 성장하는 지역입니다. 예를 들어, 2025년 12월 인도 정부는 간호 교육을 위해 Bagalkot에 국내 두 번째 국립 시뮬레이션 센터(National Simulation Centre)를 개소했습니다. 이 센터에는 학생들의 임상 기술 향상을 돕기 위한 고충실도 시뮬레이터가 도입되어 이 지역 일반인들의 이 분야에 대한 지지를 보여주고 있습니다.

세계의 의료 시뮬레이션 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 및 AI의 도입에 의한 전략적 디스럽션

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 의료 시뮬레이션 시장 : 제공별

제10장 의료 시뮬레이션 시장 : 기술별

제11장 의료 시뮬레이션 시장 : 최종사용자별

제12장 의료 시뮬레이션 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

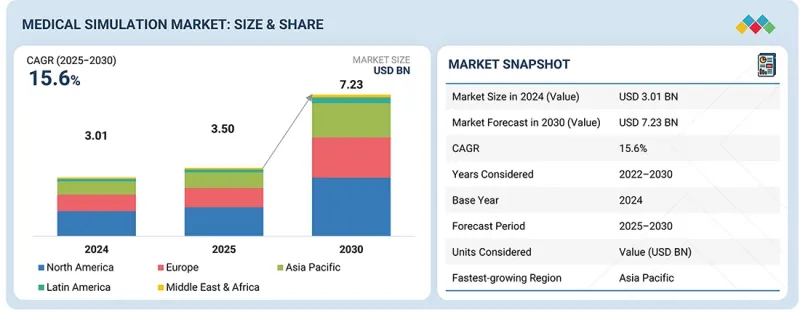

KSM 26.06.08The global medical simulation market is projected to reach USD 7.23 billion by 2030 from USD 3.50 billion in 2025, at a CAGR of 15.6%. The medical simulation market is growing due to increasing demand for advanced clinical training and investments in supporting infrastructure.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Offering, Technology, and End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

For example, the University of Texas at Arlington announced its Mobile Simulation Lab, launched in March 2025, aimed at delivering high-tech medical education in underserved parts of Texas, highlighting how simulation technologies are increasing access to hands-on education beyond traditional academic centers.

"Healthcare simulation anatomical models held the largest share of the medical simulation market."

Based on offering segment, healthcare simulation anatomical models held the largest share of the medical simulation market. This is because of their widespread use in foundational training and skills practice. These physical models help learners build core competencies in a risk-free environment before working with patients. For example, Kyoto Kagaku provides highly detailed anatomical phantoms for ultrasound and procedural skills training, and Limbs & Things offers realistic pelvic and neonatal models used in obstetrics and emergency care education, making anatomical models indispensable in medical and nursing curricula worldwide.

"Procedural rehearsal technology held the largest share of the medical simulation market in 2024."

The procedural rehearsal technology segment accounted for the largest share of the medical simulation market in 2024, driven by the need for hands-on practice of complex medical procedures. These technologies enable clinicians to simulate surgeries on highly realistic, often patient-specific models with improved accuracy and reduced intraoperative risk. Acceleration of adoption will be furthered by the rise of minimally invasive surgery, an increased focus on reducing complications, and greater investment in advanced imaging and 3D modeling. For example, various platforms from Surgical Science Sweden AB enable surgeons to rehearse laparoscopic and endoscopic procedures in virtual environments, effectively bridging the gap between theory and real-world execution in training and preoperative planning.

"Asia Pacific is growing at the fastest rate during the forecast period."

Asia Pacific is the fastest-growing region in the medical simulation market, driven by the rapid expansion of healthcare infrastructure, the growing need for skilled clinical resources, and the increasing adoption of state-of-the-art training solutions. For instance, in December 2025, the Indian government launched the second National Simulation Centre for nursing education in Bagalkot, equipped with high-fidelity simulators to help students improve their clinical skills, thereby indicating the general public's support for this sector in this region.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the authentication and brand protection marketplace.

The breakdown of primary participants is as mentioned below:

- By Company Type - Tier 1: 55%, Tier 2: 30%, and Tier 3: 15%

- By Designation - C-level Executives: 50%, Directors: 35%, and Others: 15%

- By Region - North America: 48%, Europe: 32%, Asia Pacific: 15%, Middle East & Africa: 3%, and Latin America: 2%

Note: Other designations include sales, marketing, and product managers.

Tiers are defined based on a company's total revenue as of 2024: Tier 1 = >USD 1 billion, Tier 2 = USD 500 million to USD 1 billion, and Tier 3 = <USD 500 million.

Key Players in the Medical Simulation Market

The key players functioning in the medical simulation market include CAE Inc. (Canada), Laerdal Medical (Norway), Gaumard Scientific Co. (US), Kyoto Kagaku (Japan), Limbs & Things (UK), Mentice AB (Sweden), Simulab Corporation (US), Simulaids (US), 3B Scientific (Germany), and Operative Experience Inc. (UK), among others.

Research Coverage:

The report analyzes the medical simulation market. It aims to estimate the market size and future growth potential of various market segments based on offering, technology, end user, and region. The report also provides a competitive analysis of the key players in this market, along with their company profiles, offerings, recent developments, and key market strategies.

Reasons to Buy the Report

This report will help established firms and new entrants/smaller firms gauge the market's pulse, which, in turn, would help them garner a larger market share. Firms purchasing the report could use one or more of the strategies listed below to strengthen their market positions.

This report provides insights into:

- Analysis of key drivers (rising demand for realistic and risk-free training environments in medical education, rapid technological advancements in medical education, surging demand for minimally invasive treatment, increasing focus on patient safety, growing adoption of AI-driven VR platforms to improve clinical decision-making), restraints (limited availability of funds to establish simulation training centers, poorly designed medical simulators), opportunities (widening workforce gaps creating demand for simulation-based training solutions, growing awareness about simulation training in emerging economies), and challenges (high cost of simulators, operational challenges) influencing the growth of the medical simulation market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the medical simulation market.

- Market Development: Comprehensive information on the lucrative emerging markets, products & services, technologies, end users, and regions.

- Market Diversification: Exhaustive information about the product portfolios, untapped geographies, recent developments, and investments in the medical simulation market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, and capabilities of the leading players in the medical simulation market such as CAE Inc. (Canada), Laerdal Medical (Norway), Gaumard Scientific Co. (US), Kyoto Kagaku (Japan), Limbs & Things (UK), Mentice AB (Sweden), Simulab Corporation (US), and Simulaids (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 STUDY SCOPE

- 1.2.2 INCLUSIONS & EXCLUSIONS

- 1.2.3 YEARS CONSIDERED

- 1.3 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET GROWTH

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR MEDICAL SIMULATION MARKET

- 3.2 NORTH AMERICA: MEDICAL SIMULATION MARKET, BY END USER AND COUNTRY

- 3.3 MEDICAL SIMULATION MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.3 MARKET DYNAMICS: IMPACT ANALYSIS

- 4.3.1 DRIVERS

- 4.3.1.1 Rising demand for realistic and risk-free training environments in medical education

- 4.3.1.2 Rapid technological advancements in medical education

- 4.3.1.3 Surging demand for minimally invasive treatments

- 4.3.1.4 Increasing focus on patient safety

- 4.3.1.5 Growing adoption of AI-driven VR platforms to improve clinical decision-making

- 4.3.2 RESTRAINTS

- 4.3.2.1 Limited availability of funds to establish simulation training centers

- 4.3.2.2 Poorly designed medical simulators

- 4.3.3 OPPORTUNITIES

- 4.3.3.1 Widening workforce gaps creating demand for simulation-based training solutions

- 4.3.3.2 Growing awareness about simulation training in emerging economies

- 4.3.4 CHALLENGES

- 4.3.4.1 High cost of simulators

- 4.3.4.2 Operational challenges

- 4.3.1 DRIVERS

- 4.4 UNMET NEEDS & WHITE SPACES

- 4.5 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 THREAT OF SUBSTITUTES

- 5.1.4 THREAT OF NEW ENTRANTS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 GDP TRENDS & FORECAST

- 5.2.2 TRENDS IN GLOBAL HEALTHCARE IT INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICING ANALYSIS OF MEDICAL SIMULATION PRODUCTS, BY KEY PLAYER, 2025

- 5.5.2 INDICATIVE PRICING ANALYSIS OF MEDICAL SIMULATION PRODUCTS, BY REGION, 2025

- 5.6 KEY CONFERENCES & EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.8 INVESTMENT & FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 CASE STUDY 1: ENHANCING CLINICAL READINESS: NORTHUMBRIA UNIVERSITY'S SCALABLE SIMULATION PROGRAM IN PARTNERSHIP WITH OMB

- 5.9.2 CASE STUDY 2: OPTIMIZING PATIENT FLOW AND INFRASTRUCTURE: MEMORIAL HEALTH SYSTEM'S SIMULATION-DRIVEN EFFICIENCY GAINS WITH SIMUL8

- 5.10 IMPACT OF 2025 US TARIFFS ON MEDICAL SIMULATION MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON END-USE INDUSTRIES

- 5.10.5.1 Academic institutes

- 5.10.5.2 Hospitals

- 5.10.5.3 Military organizations

6 STRATEGIC DISRUPTIONS THROUGH TECHNOLOGY, PATENTS, AND DIGITAL & AI ADOPTION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 COMPUTER-BASED SIMULATIONS

- 6.1.2 HAPTIC FEEDBACK DEVICES

- 6.1.3 ARTIFICIAL INTELLIGENCE & VIRTUAL REALITY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 BIG DATA & INTEROPERABILITY PLATFORMS

- 6.2.2 LEARNING MANAGEMENT SYSTEMS (LMS)

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 CLOUD COMPUTING

- 6.3.2 ROBOTICS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 PATENT PUBLICATION TRENDS FOR MEDICAL SIMULATION MARKET

- 6.5.2 INSIGHTS: JURISDICTION & TOP APPLICANT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-DRIVEN ADAPTIVE SIMULATION & PERFORMANCE ANALYTICS

- 6.6.2 DIGITAL TWIN-ENABLED PATIENT-SPECIFIC SIMULATION

- 6.6.3 IMMERSIVE XR-BASED COLLABORATIVE TRAINING ENVIRONMENTS

- 6.6.4 REMOTE, CLOUD-BASED SIMULATION, AND SCALABILITY

- 6.6.5 HAPTIC INNOVATION & HIGH-FIDELITY PHYSICAL-DIGITAL INTEGRATION

- 6.6.6 SIMULATION FOR CLINICAL DECISION SUPPORT & RISK REDUCTION

- 6.7 IMPACT OF AI/GEN AI ON MEDICAL SIMULATION MARKET

- 6.7.1 MARKET POTENTIAL OF AI/GEN AI

- 6.7.2 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION

- 6.7.2.1 AI-driven surgical simulation and performance analytics at Surgical Science Sweden AB

- 6.7.3 IMPACT OF AI/GEN AI ON INTERCONNECTED & ADJACENT ECOSYSTEMS

- 6.7.3.1 AI-driven adaptive simulation and training platforms

- 6.7.3.2 Virtual patients, digital twins, and simulation intelligence

- 6.7.3.3 Remote simulation, collaboration, and skill validation

- 6.7.4 USER READINESS & IMPACT ASSESSMENT

- 6.7.4.1 User readiness

- 6.7.4.1.1 User A: Academic institutes

- 6.7.4.1.2 User B: Hospitals

- 6.7.4.1.3 User C: Military organizations

- 6.7.4.2 Impact assessment

- 6.7.4.2.1 User A: Academic Institutes

- 6.7.4.2.2 User B: Hospitals

- 6.7.4.2.3 User C: Military organizations

- 6.7.4.1 User readiness

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS & THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM END-USE INDUSTRIES

- 8.4.1 UNMET NEEDS

- 8.4.2 END-USER EXPECTATIONS

- 8.5 MARKET PROFITABILITY

9 MEDICAL SIMULATION MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.2 HEALTHCARE SIMULATION ANATOMICAL MODELS

- 9.2.1 PATIENT SIMULATORS

- 9.2.1.1 Patient simulators market, by type

- 9.2.1.1.1 High-fidelity patient simulators

- 9.2.1.1.1.1 Growing adoption of high-fidelity patient simulators in educational training to drive growth

- 9.2.1.1.2 Medium-fidelity patient simulators

- 9.2.1.1.2.1 Cost benefits of medium-fidelity simulation to drive demand

- 9.2.1.1.3 Low-fidelity patient simulators

- 9.2.1.1.3.1 Budgetary constraints and ease of use to drive demand

- 9.2.1.1.1 High-fidelity patient simulators

- 9.2.1.2 Patient simulators market, by application

- 9.2.1.2.1 Laparoscopic surgical simulators

- 9.2.1.2.1.1 Increasing prevalence of minimally invasive surgeries to drive growth

- 9.2.1.2.2 Gynecology simulators

- 9.2.1.2.2.1 Increasing incidence of fibroids and polyps in women to drive demand

- 9.2.1.2.3 Cardiovascular simulators

- 9.2.1.2.3.1 Increasing prevalence of diabetes to boost demand

- 9.2.1.2.4 Orthopedic surgical simulators

- 9.2.1.2.4.1 Enhancement in surgeon skills by orthopedic simulation training to drive demand

- 9.2.1.2.5 Spine surgical simulators

- 9.2.1.2.5.1 Mastering spine surgeries through advanced simulation techniques to boost demand

- 9.2.1.2.6 Endovascular simulators

- 9.2.1.2.6.1 Reduced mortality rates associated with endovascular simulators to boost demand

- 9.2.1.2.7 Other patient simulators

- 9.2.1.2.1 Laparoscopic surgical simulators

- 9.2.1.1 Patient simulators market, by type

- 9.2.2 TASK TRAINERS

- 9.2.2.1 Inability to imitate emotional attributes of patients to restrain growth

- 9.2.3 INTERVENTIONAL/SURGICAL SIMULATORS

- 9.2.3.1 Laparoscopic surgical simulators

- 9.2.3.1.1 Increasing preference for minimally invasive surgeries to drive growth

- 9.2.3.2 Gynecology surgical simulators

- 9.2.3.2.1 Increasing incidence of fibroids and polyps in women to drive demand for gynecology simulators

- 9.2.3.3 Cardiovascular surgical simulators

- 9.2.3.3.1 Increasing prevalence of obesity and diabetes to boost demand

- 9.2.3.4 Orthopedic surgical simulators

- 9.2.3.4.1 Enhancement in surgeon skills by orthopedic simulation training to drive demand

- 9.2.3.5 Spine surgical simulators

- 9.2.3.5.1 Growing use of spine surgical simulators in training surgeons to boost demand

- 9.2.3.6 Endovascular surgical simulators

- 9.2.3.6.1 Ability to reduce mortality rates to drive demand for endovascular surgical simulators

- 9.2.3.7 Other interventional/surgical simulators

- 9.2.3.1 Laparoscopic surgical simulators

- 9.2.4 ULTRASOUND SIMULATORS

- 9.2.4.1 Inferior quality images due to low dynamics and spatial resolution to restrain growth

- 9.2.5 DENTAL SIMULATORS

- 9.2.5.1 Expanding dental tourism industry to drive growth

- 9.2.6 EYE SIMULATORS

- 9.2.6.1 Increasing incidence of eye disorders to drive growth

- 9.2.1 PATIENT SIMULATORS

- 9.3 WEB-BASED SIMULATION

- 9.3.1 RISING TECHNOLOGICAL ADVANCEMENTS TO DRIVE ADOPTION OF WEB-BASED SIMULATION

- 9.4 HEALTHCARE SIMULATION SOFTWARE

- 9.4.1 ABILITY TO REDUCE OVERALL SURGICAL PROCESS TRAINING TIME TO DRIVE ADOPTION

- 9.5 SIMULATION TRAINING SERVICES

- 9.5.1 VENDOR-BASED TRAINING

- 9.5.1.1 High focus on patient safety to drive demand

- 9.5.2 EDUCATIONAL SOCIETIES

- 9.5.2.1 Growing need for proper training and authenticity of knowledge to drive growth

- 9.5.3 CUSTOM CONSULTING SERVICES

- 9.5.3.1 Growing need to limit errors associated with traditional medical training systems to drive growth

- 9.5.1 VENDOR-BASED TRAINING

10 MEDICAL SIMULATION MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 VIRTUAL PATIENT SIMULATION

- 10.2.1 INCREASING FOCUS ON AUGMENTED REALITY/VIRTUAL REALITY TO DRIVE MARKET

- 10.3 3D PRINTING

- 10.3.1 INCREASING ADOPTION IN MEDICAL TRAINING TO DRIVE MARKET

- 10.4 PROCEDURAL REHEARSAL TECHNOLOGY

- 10.4.1 NEED FOR ADVANCING SURGICAL SKILLS WITH REHEARSAL TECH TO FUEL MARKET GROWTH

11 MEDICAL SIMULATION MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 ACADEMIC INSTITUTES

- 11.2.1 GROWING NEED FOR SKILLED MEDICAL PROFESSIONALS TO DRIVE DEMAND

- 11.3 HOSPITALS

- 11.3.1 RISING FOCUS ON MINIMIZING MEDICAL ERRORS TO DRIVE DEMAND

- 11.4 MILITARY ORGANIZATIONS

- 11.4.1 EXPLORATION OF NEW METHODS OF MEDICAL CARE DURING WARFARE TO DRIVE DEMAND

- 11.5 OTHER END USERS

12 MEDICAL SIMULATION MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 12.2.2 US

- 12.2.2.1 Increasing demand for virtual tutors and high healthcare spending to boost growth

- 12.2.3 CANADA

- 12.2.3.1 Clinical simulation and competency-based training in Canada to fuel market growth

- 12.3 EUROPE

- 12.3.1 EUROPE: MACROECONOMIC OUTLOOK

- 12.3.2 GERMANY

- 12.3.2.1 High healthcare spending to drive market growth

- 12.3.3 FRANCE

- 12.3.3.1 Growing focus on use of innovative methods in medical training to drive growth

- 12.3.4 UK

- 12.3.4.1 Rising number of healthcare simulation centers and hospitals to drive growth

- 12.3.5 ITALY

- 12.3.5.1 Shortage of trained healthcare personnel to drive growth

- 12.3.6 SPAIN

- 12.3.6.1 Increasing number of surgical procedures to boost growth

- 12.3.7 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 12.4.2 CHINA

- 12.4.2.1 Increasing demand for trained medical professionals to drive growth

- 12.4.3 JAPAN

- 12.4.3.1 Increasing demand for virtual tutors and technologically advanced simulators to drive growth

- 12.4.4 INDIA

- 12.4.4.1 Growing awareness regarding patient safety due to healthcare negligence to drive growth

- 12.4.5 AUSTRALIA

- 12.4.5.1 Accreditation-driven training and national workforce policies to fuel medical simulation adoption in Australia

- 12.4.6 SOUTH KOREA

- 12.4.6.1 Technology-driven innovation and national digital health initiatives to accelerate adoption of medical simulation in South Korea

- 12.4.7 REST OF ASIA PACIFIC

- 12.5 LATIN AMERICA

- 12.5.1 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 12.5.2 BRAZIL

- 12.5.2.1 High incidence of chronic diseases to drive market

- 12.5.3 MEXICO

- 12.5.3.1 Disruptive technologies and public-private partnerships to boost growth

- 12.5.4 REST OF LATIN AMERICA

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 12.6.2 GCC COUNTRIES

- 12.6.2.1 Focus on enhancing patient care to drive market

- 12.6.2.2 Saudi Arabia

- 12.6.2.2.1 Government-led digital transformation and strong investments in AI-driven healthcare to boost market

- 12.6.2.3 UAE

- 12.6.2.3.1 Quality-driven healthcare strategy and institutional investments to accelerate simulation demand in UAE

- 12.6.2.4 Rest of GCC Countries

- 12.6.3 SOUTH AFRICA

- 12.6.3.1 Evolving facility accreditation and workforce training needs to accelerate simulation adoption

- 12.6.4 REST OF MIDDLE EAST & AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2026

- 13.3 REVENUE ANALYSIS, 2021-2025

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.5 BRAND/PRODUCT COMPARISON

- 13.6 COMPANY VALUATION & FINANCIAL METRICS

- 13.6.1 FINANCIAL METRICS

- 13.6.2 COMPANY VALUATION

- 13.7 MARKET RANKING ANALYSIS, 2025

- 13.8 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.8.1 STARS

- 13.8.2 EMERGING LEADERS

- 13.8.3 PERVASIVE PLAYERS

- 13.8.4 PARTICIPANTS

- 13.8.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.8.5.1 Company footprint

- 13.8.5.2 Region footprint

- 13.8.5.3 Product & service footprint

- 13.8.5.4 Technology footprint

- 13.8.5.5 End-user footprint

- 13.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.9.1 PROGRESSIVE COMPANIES

- 13.9.2 RESPONSIVE COMPANIES

- 13.9.3 DYNAMIC COMPANIES

- 13.9.4 STARTING BLOCKS

- 13.9.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.9.5.1 Detailed list of key startups/SMEs

- 13.9.5.2 Competitive benchmarking of key startups/SMEs

- 13.10 COMPETITIVE SCENARIO

- 13.10.1 PRODUCT LAUNCHES & ENHANCEMENTS

- 13.10.2 DEALS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 SURGICAL SCIENCE SWEDEN AB

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product enhancements

- 14.1.1.3.2 Deals

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses & competitive threats

- 14.1.2 LAERDAL MEDICAL

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches

- 14.1.2.3.2 Deals

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses & competitive threats

- 14.1.3 GAUMARD SCIENTIFIC

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches

- 14.1.3.3.2 Deals

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses & competitive threats

- 14.1.4 KYOTO KAGAKU CO., LTD.

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 MnM view

- 14.1.4.3.1 Right to win

- 14.1.4.3.2 Strategic choices

- 14.1.4.3.3 Weaknesses & competitive threats

- 14.1.5 LIMBS & THINGS LTD.

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches

- 14.1.5.3.2 Deals

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses & competitive threats

- 14.1.6 MENTICE AB

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches & approvals

- 14.1.6.3.2 Deals

- 14.1.7 SIMULAB CORPORATION

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches & enhancements

- 14.1.8 SIMULAIDS

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches

- 14.1.9 OPERATIVE EXPERIENCE, INC.

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Other developments

- 14.1.10 ELEVATE HEALTHCARE

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.11 ANATOMAGE

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Product launches & enhancements

- 14.1.11.3.2 Other developments

- 14.1.12 3B SCIENTIFIC

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.13 VIRTAMED AG

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.13.3 Recent developments

- 14.1.13.3.1 Product enhancements

- 14.1.13.3.2 Deals

- 14.1.14 SYNBONE AG

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.15 ERLER-ZIMMER MEDICAL GMBH

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.16 MEDICAL-X

- 14.1.16.1 Business overview

- 14.1.16.2 Products offered

- 14.1.17 KAVO DENTAL

- 14.1.17.1 Business overview

- 14.1.17.2 Products offered

- 14.1.18 ALTAY SCIENTIFIC

- 14.1.18.1 Business overview

- 14.1.18.2 Products offered

- 14.1.19 TRUCORP LIMITED

- 14.1.19.1 Business overview

- 14.1.19.2 Products offered

- 14.1.19.3 Recent developments

- 14.1.19.3.1 Product launches

- 14.1.19.3.2 Deals

- 14.1.20 SIMENDO

- 14.1.20.1 Business overview

- 14.1.20.2 Products offered

- 14.1.1 SURGICAL SCIENCE SWEDEN AB

- 14.2 OTHER PLAYERS

- 14.2.1 HAAG-STREIT AG

- 14.2.2 SONOSIM

- 14.2.3 HRV SIMULATION

- 14.2.4 SYNAPTIVE MEDICAL

- 14.2.5 INOVUS LIMITED

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH APPROACH

- 15.1.1 SECONDARY RESEARCH

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY RESEARCH

- 15.1.2.1 Primary sources

- 15.1.2.2 Key data from primary sources

- 15.1.2.3 Breakdown of primary interviews

- 15.1.2.4 Insights from primary experts

- 15.1.1 SECONDARY RESEARCH

- 15.2 RESEARCH METHODOLOGY DESIGN

- 15.3 MARKET SIZE ESTIMATION

- 15.4 DATA TRIANGULATION

- 15.5 RESEARCH ASSUMPTIONS

- 15.6 RESEARCH LIMITATIONS

- 15.6.1 METHODOLOGY-RELATED

- 15.6.2 SCOPE-RELATED

- 15.7 RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS