|

시장보고서

상품코드

2048962

자동차용 납축배터리 시장 : 제품별(SLI 배터리, 마이크로 하이브리드, 보조용), 유형별(액식, VRLA), 고객별, 최종사용별(승용차, 소형 & 대형 상용차, 이륜차, 삼륜차), 지역별 - 세계 예측(-2033년)Automotive Lead-Acid Battery Market by Product (SLI Batteries, Micro Hybrid, Auxiliary), Type (Flooded, VRLA), Customer, End Use (Passenger Cars, Light & Heavy Commercial Vehicles, Two Wheelers, Three Wheelers), and Region - Global Forecast to 2033 |

||||||

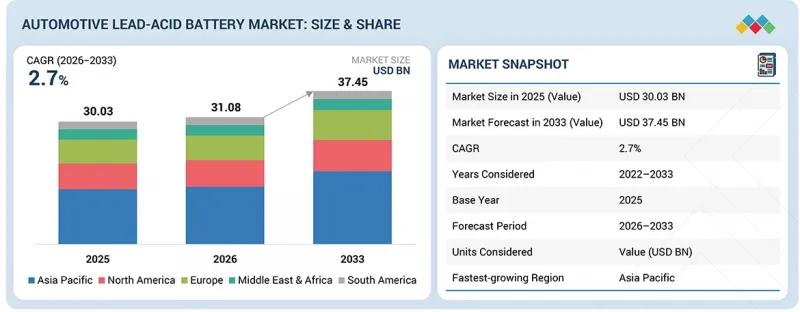

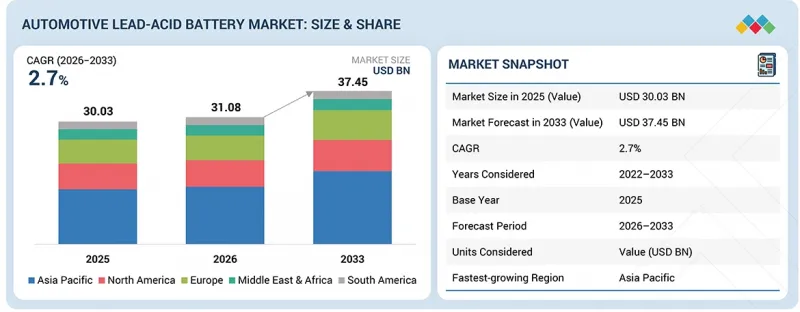

자동차용 납축배터리 시장 규모는 2026년 310억 8,000만 달러에서 2033년에는 374억 5,000만 달러에 달할 것으로 전망되고, 예측 기간 동안 CAGR은 2.7%를 기록할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2033년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2033년 |

| 단위 | 금액(달러)·수량(MWh) |

| 부문 | 유형, 제품, 고객, 최종사용, 지역 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 중동 및 아프리카, 남미 |

특히 인도, 중국, 동남아시아 등 신흥 경제국에서 자동차 산업이 지속적으로 성장함에 따라, 신뢰성과 비용 효율성이 높은 배터리 솔루션에 대한 수요가 증가하고 있습니다. 납축배터리는 저렴한 가격, 검증된 성능, 기존 내연기관(ICE) 차량과의 호환성으로 인해 대부분의 차량에서 선호되는 선택이 되고 있습니다.

"제품별로는 마이크로 하이브리드 배터리 부문이 시장 점유율 2위를 차지할 것으로 추정됩니다."

마이크로 하이브리드 배터리는 시장에서 두 번째로 큰 점유율을 차지하는 것으로 추정됩니다. 이는 스타트-스톱 시스템과의 호환성 및 연비 효율이 우수한 차량에 대한 수요 증가에 따른 것입니다. 강화된 배출가스 규제와 강화형 액체 배터리(EFB) 및 흡수성 유리 매트(AGM) 기술의 발전에 따라 이러한 기술의 채택이 증가하고 있습니다. 그 결과, 자동차 산업이 환경에 미치는 영향을 줄이고 보다 지속가능하고 효율적인 기술로 전환하면서 마이크로 하이브리드 배터리의 시장 점유율이 빠르게 확대되고 있습니다.

"유형별로는 액상 배터리 부문이 가장 큰 시장 점유율을 차지할 것으로 추정됩니다."

유형별로 보면 액체 배터리가 시장을 주도하고 있으며, AGM 배터리가 그 뒤를 잇고 있습니다. 설계가 구식임에도 불구하고 액체 배터리는 저렴한 가격과 표준 차량에서의 신뢰성으로 인해 여전히 인기를 끌고 있습니다. 그러나 AGM 및 강화 액체 배터리(EFB)와 같은 새로운 배터리 기술이 스타트-스톱 시스템을 포함한 현대 자동차의 요구를 충족하는 개선된 솔루션을 제공함에 따라 시장 점유율이 감소하고 있습니다. 예산이 중요한 소비자들이 시장의 대부분을 차지하는 지역에서 일상적으로 차량을 운전하는 운전자들에게는 여전히 액체 배터리가 가장 우선적인 선택이 되고 있습니다.

"용도별로는 소형 및 대형 상용차 부문이 시장 점유율 2위를 차지할 것으로 추정됩니다."

용도별로 보면 경/대형 상용차 부문은 시장에서 두 번째로 큰 점유율을 차지하는 것으로 추정됩니다. 상업용 차량은 시동, 조명, 점화(SLI) 기능의 전원으로 납축배터리에 의존하고 있습니다. 이러한 차량은 특히 가혹한 사용 조건에서도 저렴한 가격, 접근성, 신뢰할 수 있는 성능으로 인해 납축 배터리에 의존하고 있습니다. 승용차 시장이 여전히 가장 큰 시장이지만, 물류, 건설, 운송 산업의 확장을 배경으로 상용차에서 납축배터리의 사용은 증가하는 추세입니다.

"고객별로는 OEM 부문이 시장 점유율 2위를 차지하고 있는 것으로 추정됩니다."

자동차 제조업체는 신차 생산에 사용되는 납축배터리에 대한 일관된 요구사항을 가지고 있습니다. 그들은 시동, 조명, 점화(SLI) 기능을 지원하는 경제적이고 신뢰할 수 있는 배터리 시스템을 선택했습니다. 배터리는 자주 교체해야 하기 때문에 애프터마켓 부문이 시장을 주도하고 있습니다. 그러나 OEM 부문은 기존 차량의 지속적인 생산과 더불어 AGM 및 EFB와 같은 첨단 납축배터리 기술이 스타트-스톱 시스템을 장착한 신차에 적용됨에 따라 혜택을 누리고 있습니다. OEM 부문은 전체 시장 확대를 견인하는 데 있어 매우 중요한 역할을 하고 있습니다.

"예측 기간 동안 북미는 두 번째로 큰 시장 점유율을 차지할 것으로 추정됩니다."

북미는 자동차용 납축배터리 시장에서 두 번째로 큰 점유율을 차지하고 있는 것으로 추정됩니다. 이 지역의 시장 성장은 탄탄한 자동차 산업에 의해 주도되고 있습니다. 이 업계는 기존 차량을 제조하는 한편, 신차 모델에 스타트-스톱 시스템 기술 채택이 확대되고 있습니다. 북미의 납축배터리 수요는 승용차, 상용차, 교체용 시장에서 광범위하게 사용되고 있습니다. 이 지역에서 납축배터리는 탄탄한 자동차 제조 기반과 애프터마켓 수요로 인한 저렴한 가격과 신뢰성으로 인해 여전히 선호되는 전원공급장치로 남아 있습니다.

세계의 자동차용 납축배터리 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 자동차용 납축배터리 시장 : 제품별

제10장 자동차용 납축배터리 시장 : 유형별

제11장 자동차용 납축배터리 시장 : 최종사용별

제12장 자동차용 납축배터리 시장 : 용도별

제13장 자동차용 납축배터리 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSM 26.06.08The automotive lead-acid battery market is expected to reach USD 37.45 billion by 2033 from an estimated USD 31.08 billion in 2026, at a CAGR of 2.7% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | Value (USD Million/Billion) and Volume (MWh) |

| Segments | Type, Product, Customer, End Use, and Region |

| Regions covered | Asia Pacific, Europe, North America, Middle East & Africa, and South America |

As the automotive industry continues to grow, especially in emerging economies like India, China, and Southeast Asia, the need for reliable and cost-effective battery solutions intensifies. Lead-acid batteries are the preferred choice for most vehicles due to their affordability, proven performance, and compatibility with conventional internal combustion engine (ICE) vehicles.

"By product, the micro hybrid batteries segment is estimated to account for the second-largest market share."

Micro-hybrid batteries are estimated to account for the second-largest share of the automotive lead-acid battery market. This is due to their compatibility with start-stop systems and the growing demand for vehicles that offer better fuel economy. The adoption of these technologies has increased in response to stricter emission regulations and advancements in Enhanced Flooded Batteries (EFB) and Absorbent Glass Mat (AGM) technologies. As a result, micro-hybrid batteries are rapidly expanding their market share, driven by the automotive industry's shift toward more sustainable and efficient technologies that reduce environmental impact.

"By type, the flooded batteries segment is estimated to account for the largest market share."

By type, the automotive lead-acid battery market is led by flooded batteries, followed closely by Absorbent Glass Mat (AGM) batteries. Despite their outdated design, flooded batteries remain popular due to their affordability and reliability in standard vehicles. However, their market share has declined as newer battery technologies, such as AGM and Enhanced Flooded Batteries (EFB), offer improved solutions that meet the demands of modern automotive needs, including start-stop systems. Flooded batteries remain the top choice for drivers who regularly operate vehicles in areas where budget-conscious consumers make up the majority of the market.

"By end use, the light & heavy commercial vehicles segment is estimated to account for the second-largest market share."

By end use, the light & heavy commercial vehicles segment is estimated to account for the second-largest share of the automotive lead-acid battery market. Commercial vehicles rely on lead-acid batteries to power their starting, lighting, and ignition (SLI) functions. These vehicles depend on lead-acid batteries due to their affordability, accessibility, and reliable performance, especially in challenging operating conditions. While the market for passenger vehicles remains the largest, the use of lead-acid batteries in commercial vehicles is on the rise, driven by the expansion of the logistics, construction, and transportation industries.

"By customer, the OEM segment is estimated to account for the second-largest market share."

By customer, the OEM (original equipment manufacturer) segment is estimated to hold the second-largest share of the automotive lead-acid battery market. Vehicle manufacturers have consistent requirements for lead-acid batteries, which they utilize to build new vehicles. They select economical yet reliable battery systems that support starting, lighting, and ignition (SLI) functions. The aftermarket segment leads the market because batteries need to be replaced frequently. However, the OEM segment also benefits from the continued production of conventional vehicles and the use of advanced lead-acid battery technologies, such as Absorbent Glass Mat (AGM) and Enhanced Flooded Battery (EFB), in new vehicles equipped with start-stop systems. The OEM segment plays a crucial role in driving overall market expansion.

"North America is estimated to account for the second-largest market share during the forecast period."

North America is estimated to hold the second-largest share of the automotive lead-acid battery market. The market growth in this region is driven by its robust automotive sector, which manufactures traditional vehicles and increasingly incorporates start-stop system technology in new vehicle models. The demand for lead-acid batteries in North America is supported by their extensive use in light vehicles, commercial vehicles, and replacement markets. This region continues to favor lead-acid batteries as the preferred power source due to the affordability and reliability stemming from its strong automotive manufacturing base and aftermarket demand.

Break-up of primary participants for the report:

- By Company Type: Tier 1 - 20%, Tier 2 - 40%, and Tier 3 - 40%

- By Designation: C-Level Executives- 10%, Directors- 70%, and Others - 20%

- By Region: North America - 45%, Asia Pacific - 25%, Europe - 20%, Middle East & Africa - 5%, and South America - 5%

EnerSys (US), Clarios (US), Exide Industries Ltd. (India), GS Yuasa International Ltd. (Japan), and East Penn Manufacturing Company (US) are the key players in the automotive lead-acid battery market. These players have adopted various strategies, including agreements, joint ventures, and expansions, to increase their market share and business revenue.

Research Coverage:

The report defines, segments, and projects the size of the automotive lead-acid battery market by product, type, customer, end use, and region. It strategically profiles the key players and comprehensively analyzes their market share and core competencies. It also tracks and analyzes competitive developments, such as expansions, agreements, and acquisitions undertaken by them in the market.

Reasons to Buy the Report:

The report is expected to help market leaders/new entrants by providing the closest approximations of revenue for the automotive lead-acid battery market and its segments. This report is also expected to help stakeholders gain a deeper understanding of the market's competitive landscape, acquire valuable insights to enhance their business positions, and develop effective go-to-market strategies. It also enables stakeholders to understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of critical drivers (High demand for cost-effective and reliable batteries in automotive industry, Easy recyclability compared with lithium-ion batteries), restraints (Risk of battery explosion due to overcharging, Growing adoption of lithium-ion batteries), opportunities (Technological advancements to enhance durability of lead-acid batteries), and challenges (Limited capacity of lead-acid batteries) influencing the growth of the automotive lead-acid battery market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities in the automotive lead-acid battery market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the automotive lead-acid battery market across varied regions

- Market Diversification: Exhaustive information about new products, various types, untapped geographies, recent developments, and investments in the automotive lead-acid battery market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as EnerSys (US), Clarios (US), Exide Industries Ltd. (India), GS Yuasa International Ltd. (Japan), East Penn Manufacturing Company (US), and others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 RESEARCH LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTOMOTIVE LEAD-ACID BATTERY MARKET

- 3.2 AUTOMOTIVE LEAD-ACID BATTERY MARKET, BY REGION

- 3.3 AUTOMOTIVE LEAD-ACID BATTERY MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 High demand for cost-effective and reliable batteries in automotive industry and affordability

- 4.2.1.2 Easy recyclability compared with lithium-ion batteries

- 4.2.2 RESTRAINTS

- 4.2.2.1 Risk of battery explosion due to overcharging

- 4.2.2.2 Growing adoption of lithium-ion batteries

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Technological advancements to enhance durability of lead-acid batteries

- 4.2.4 CHALLENGES

- 4.2.4.1 Limited capacity of lead-acid batteries

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN AUTOMOTIVE LEAD-ACID BATTERY MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 THREAT OF NEW ENTRANTS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL AUTOMOTIVE LEAD-ACID BATTERY INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RESEARCH & DEVELOPMENT

- 5.3.2 RAW MATERIAL

- 5.3.3 MANUFACTURING

- 5.3.4 DISTRIBUTION NETWORK

- 5.3.5 END-USE INDUSTRIES

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF AUTOMOTIVE LEAD-ACID BATTERY, BY REGION

- 5.5.2 AVERAGE SELLING PRICE OF AUTOMOTIVE LEAD-ACID BATTERY (12V, 34 AH), BY KEY PLAYERS

- 5.6 TRADE DATA

- 5.6.1 IMPORT SCENARIO (HS CODE 850720)

- 5.6.2 EXPORT SCENARIO (HS CODE 850720)

- 5.7 KEY CONFERENCES AND EVENTS, 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 US TARIFF IMPACT ON AUTOMOTIVE LEAD-ACID BATTERY MARKET

- 5.10.1 KEY TARIFF RATES IMPACTING THE MARKET

- 5.10.2 PRICE IMPACT ANALYSIS

- 5.10.3 IMPACT ON KEY COUNTRIES/REGIONS

- 5.10.3.1 US

- 5.10.3.2 Europe

- 5.10.3.3 Asia Pacific

- 5.10.4 IMPACT ON END-USE INDUSTRIES OF AUTOMOTIVE LEAD-ACID BATTERY MARKET

- 5.10.4.1 Passenger cars

- 5.10.4.2 Light & heavy commercial vehicles

- 5.10.4.3 Two wheelers

- 5.10.4.4 Three wheelers

- 5.10.4.5 Aftermarket replacement industry

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ABSORBENT GLASS MAT (AGM) BATTERIES

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 BATTERY MANAGEMENT AND MONITORING SYSTEMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 ADVANCED LEAD-CARBON BATTERY TECHNOLOGY

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | PERFORMANCE OPTIMIZATION & START-STOP BATTERY EXPANSION

- 6.4.2 MID-TERM (2027-2030) | SMART BATTERY SYSTEMS & SUSTAINABLE MANUFACTURING

- 6.4.3 LONG-TERM (2030-2035+) | CIRCULARITY, LOW-EMISSION SOLVENT SYSTEMS

- 6.5 PATENT ANALYSIS

- 6.5.1 METHODOLOGY

- 6.6 FUTURE APPLICATIONS

- 6.6.1 PASSENGER CARS: START-STOP SYSTEMS & ADVANCED VEHICLE ELECTRIFICATION SUPPORT

- 6.6.2 LIGHT & HEAVY COMMERCIAL VEHICLES: HIGH-DURABILITY ENERGY STORAGE & FLEET RELIABILITY

- 6.6.3 TWO WHEELERS: AFFORDABLE MOBILITY & COMPACT POWER STORAGE

- 6.6.4 THREE WHEELERS: COST-EFFECTIVE URBAN TRANSPORTATION & ELECTRIFICATION SUPPORT

- 6.7 IMPACT OF GENERATIVE AI ON AUTOMOTIVE LEAD-ACID BATTERY MARKET

- 6.7.1 INTRODUCTION

- 6.7.1.1 Battery manufacturing & process optimization

- 6.7.1.2 Supply chain resilience & demand forecasting

- 6.7.1.3 Quality control & consistency

- 6.7.1.4 Innovation in product development & formulation

- 6.7.1.5 Cost, efficiency & competitive advantage

- 6.7.1.6 Challenges & regulatory considerations

- 6.7.1 INTRODUCTION

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 ENERSYS: ADVANCING HIGH-PERFORMANCE AGM BATTERY TECHNOLOGY FOR POWERSPORTS APPLICATIONS

- 6.8.2 CLARIOS: EXPANDING ADVANCED VARTA POWERSPORTS BATTERY SOLUTIONS

- 6.8.3 GS YUASA INTERNATIONAL: ENHANCING ECO-FRIENDLY AUTOMOTIVE BATTERY TECHNOLOGIES

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF AUTOMOTIVE LEAD ACID BATTERY

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF AUTOMOTIVE LEAD ACID BATTERY

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 AUTOMOTIVE LEAD-ACID BATTERY MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 SLI BATTERIES

- 9.2.1 CONTINUOUS GROWTH OF AUTOMOTIVE INDUSTRY IN DEVELOPING ECONOMIES TO FUEL DEMAND

- 9.3 MICRO HYBRID BATTERIES

- 9.3.1 RISING DEMAND FOR SUSTAINABLE MOBILITY SOLUTIONS AND FUEL-EFFICIENT VEHICLES TO PROPEL DEMAND

- 9.4 AUXILIARY BATTERIES

- 9.4.1 INCREASING ELECTRIFICATION OF AUTOMOBILES TO BOOST DEMAND

10 AUTOMOTIVE LEAD-ACID BATTERY MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 FLOODED BATTERIES

- 10.2.1 TRADITIONAL FLOODED BATTERIES

- 10.2.1.1 Relatively low initial cost and reliable performance under challenging circumstances to fuel market growth

- 10.2.2 ENHANCED FLOODED BATTERIES

- 10.2.2.1 Improved performance tailored for modern vehicles with start-stop systems to drive market

- 10.2.1 TRADITIONAL FLOODED BATTERIES

- 10.3 VRLA BATTERIES

- 10.3.1 ABSORBED GLASS MAT BATTERIES

- 10.3.1.1 Superior performance and durability to fuel market growth

- 10.3.2 OTHER VRLA BATTERIES

- 10.3.1 ABSORBED GLASS MAT BATTERIES

11 AUTOMOTIVE LEAD-ACID BATTERY MARKET, BY CUSTOMER

- 11.1 INTRODUCTION

- 11.2 OEM

- 11.2.1 INCREASING VEHICLE PRODUCTION TO FUEL MARKET GROWTH

- 11.3 AFTERMARKET

- 11.3.1 RISING BATTERY REPLACEMENTS AND SYSTEM UPGRADES BY VEHICLE OWNERS TO DRIVE MARKET

12 AUTOMOTIVE LEAD-ACID BATTERY MARKET, BY END USE

- 12.1 INTRODUCTION

- 12.2 PASSENGER CARS

- 12.2.1 RISING DISPOSABLE INCOME AND URBANIZATION TO DRIVE MARKET

- 12.3 LIGHT & HEAVY COMMERCIAL VEHICLES

- 12.3.1 HIGH STARTING POWER AND ELECTRICAL SUPPORT TO DRIVE MARKET

- 12.4 TWO WHEELERS

- 12.4.1 COST-EFFECTIVENESS TO SUPPORT MARKET GROWTH

- 12.5 THREE WHEELERS

- 12.5.1 AFFORDABILITY AND WIDESPREAD AVAILABILITY TO PROPEL MARKET

13 AUTOMOTIVE LEAD-ACID BATTERY MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Growing demand for vehicles to drive market growth

- 13.2.2 CANADA

- 13.2.2.1 Rise in commercial motor vehicle production to drive market

- 13.2.3 MEXICO

- 13.2.3.1 Increasing investments in automotive sector to fuel demand

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 UK

- 13.3.1.1 Increased production of commercial vehicles to drive market

- 13.3.2 GERMANY

- 13.3.2.1 Growth of transportation sector to drive market

- 13.3.3 ITALY

- 13.3.3.1 Rising demand for cars and commercial vehicles to propel market

- 13.3.4 FRANCE

- 13.3.4.1 Growing number of cars with start-stop systems to boost demand

- 13.3.5 REST OF EUROPE

- 13.3.1 UK

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Rising population and increasing demand for cars to propel market

- 13.4.2 JAPAN

- 13.4.2.1 Presence of leading automotive manufacturers to fuel market growth

- 13.4.3 INDIA

- 13.4.3.1 Increasing requirements for passenger cars and government initiatives to boost market growth

- 13.4.4 SOUTH KOREA

- 13.4.4.1 Increasing production of commercial vehicles with internal combustion engines to drive market

- 13.4.5 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.5.1.1 UAE

- 13.5.1.1.1 Growth of automotive aftermarket to drive market

- 13.5.1.2 Saudi Arabia

- 13.5.1.2.1 Government policies to boost market growth

- 13.5.1.3 Rest of GCC

- 13.5.1.3.1 Steady vehicle ownership levels, growing urban mobility, and consistent replacement demand to drive growth

- 13.5.1.1 UAE

- 13.5.2 SOUTH AFRICA

- 13.5.2.1 Government initiatives to support market growth

- 13.5.3 REST OF MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.6 SOUTH AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 Increased production of flexible-fuel vehicles to drive market

- 13.6.2 CHILE

- 13.6.2.1 Shift toward affordable, recyclable, and dependable energy storage options to drive adoption

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN (2021-2026)

- 14.3 REVENUE ANALYSIS

- 14.4 MARKET SHARE ANALYSIS

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 BRAND/PRODUCT COMPARISON

- 14.6.1 ENERSYS

- 14.6.2 CLARIOS

- 14.6.3 EXIDE INDUSTRIES LTD.

- 14.6.4 GS YUASA

- 14.6.5 EAST PENN

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Product footprint

- 14.7.5.4 Type footprint

- 14.7.5.5 End use footprint

- 14.7.5.6 Customer footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUP/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO AND TRENDS

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 ENERSYS

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Others

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 CLARIOS

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.3.3 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 EXIDE INDUSTRIES LTD.

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 GS YUASA INTERNATIONAL LTD.

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 EAST PENN MANUFACTURING COMPANY

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 MnM view

- 15.1.5.3.1 Key strengths

- 15.1.5.3.2 Strategic choices

- 15.1.5.3.3 Weaknesses & competitive threats

- 15.1.6 C&D TECHNOLOGIES, INC.

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.7 CAMEL GROUP CO., LTD.

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Expansions

- 15.1.8 TIANNENG RECHARGEABLE BATTERY MANUFACTURERS

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Expansions

- 15.1.9 LEOCH INTERNATIONAL TECHNOLOGY LIMITED

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Expansions

- 15.1.10 AMARA RAJA ENERGY & MOBILITY LIMITED

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Expansions

- 15.1.11 THE FURUKAWA BATTERY CO., LTD.

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.12 ROBERT BOSCH LLC

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.13 REEM BATTERIES

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.14 CENTURY BATTERIES INDONESIA

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.15 STRYTEN ENERGY

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Product launches

- 15.1.15.3.2 Deals

- 15.1.15.3.3 Expansions

- 15.1.16 EXIDE TECHNOLOGIES

- 15.1.16.1 Business overview

- 15.1.16.2 Products offered

- 15.1.16.3 Recent developments

- 15.1.16.3.1 Product launches

- 15.1.16.3.2 Deals

- 15.1.17 CROWN BATTERY

- 15.1.17.1 Business overview

- 15.1.17.2 Products offered

- 15.1.18 FIAMM ENERGY TECHNOLOGY S.P.A.

- 15.1.18.1 Business overview

- 15.1.18.2 Products offered

- 15.1.18.3 Recent developments

- 15.1.18.3.1 Product launches

- 15.1.18.3.2 Deals

- 15.1.19 CSB ENERGY TECHNOLOGY CO., LTD.

- 15.1.19.1 Business overview

- 15.1.19.2 Products offered

- 15.1.20 MOURA ACCUMULATORS SA

- 15.1.20.1 Business overview

- 15.1.20.2 Products offered

- 15.1.1 ENERSYS

- 15.2 OTHER PLAYERS

- 15.2.1 MEBCO

- 15.2.2 KOYOSONIC POWER CO., LTD.

- 15.2.3 RITAR INTERNATIONAL GROUP LIMITED

- 15.2.4 JYC BATTERY MANUFACTURER CO., LTD.

- 15.2.5 POWER SONIC CORPORATION

- 15.2.6 XINFU TECHNOLOGY (CHINA) CO., LIMITED

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 List of key secondary sources

- 16.1.1.2 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 List of primary interview participants (demand and supply sides)

- 16.1.2.3 Key industry insights

- 16.1.2.4 Breakdown of interviews with experts

- 16.1.1 SECONDARY DATA

- 16.2 DEMAND-SIDE ANALYSIS

- 16.3 SUPPLY-SIDE ANALYSIS

- 16.3.1 CALCULATIONS FOR SUPPLY-SIDE ANALYSIS

- 16.4 MARKET SIZE ESTIMATION

- 16.4.1 BOTTOM-UP APPROACH

- 16.4.2 TOP-DOWN APPROACH

- 16.5 GROWTH FORECAST

- 16.6 DATA TRIANGULATION

- 16.7 FACTOR ANALYSIS

- 16.8 RESEARCH ASSUMPTIONS

- 16.9 RESEARCH LIMITATIONS

- 16.10 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS