|

시장보고서

상품코드

2048963

이산화티타늄 시장 : 등급별, 프로세스별, 용도별, 지역별 - 세계 예측(-2031년)Titanium Dioxide Market by Grade (Rutile, Anatase), Process (Sulfate, Chloride), Application (Paints & Coatings, Plastics, Paper, Inks), & Region (North America, Europe, Asia Pacific, MEA, South America) - Global Forecast to 2031 |

||||||

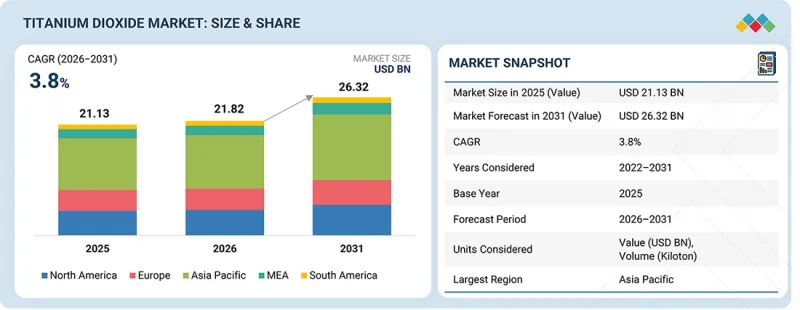

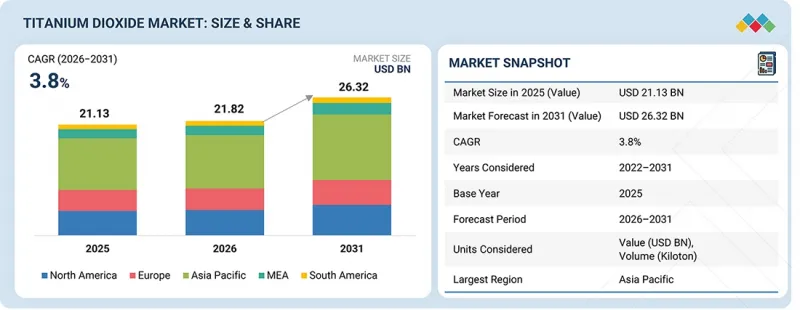

이산화티타늄 시장 규모는 2026년 218억 2,000만 달러에서 2031년까지 263억 2,000만 달러에 달할 것으로 예측되며, 2026년부터 2031년까지 CAGR은 3.8%를 기록할 전망입니다.

세계 이산화티타늄 시장의 확대는 주로 건설 부문의 호황에 힘입어 페인트, 코팅재, 건축자재에 대한 수요가 증가하고 있습니다. DIY 페인트 및 코팅 제품에 대한 소비자의 선호도 증가와 더불어 자동차 산업에서 경량화 차량 채택이 확대되면서 시장 수요를 더욱 촉진하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(100만 달러), 킬로톤 |

| 부문 | 등급별, 프로세스별, 용도별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

또한, 화장품 및 퍼스널케어 분야의 성장과 더불어 플라스틱 및 포장 응용 분야에서 이산화티타늄의 사용 확대는 시장 발전을 크게 촉진하고 있습니다.

"아나타제는 예측 기간 동안 두 번째로 큰 부문이 될 것으로 예상됩니다."

두 번째로 큰 시장은 아나타제계 이산화티타늄으로, 루틸계 이산화티타늄보다 가격이 저렴하고 밝기, 백색도 및 분산성이 우수한 제품입니다. 아나타제는 내후성이나 자외선 안정성이 루틸에 비해 떨어지지만, 실내용이나 내구성이 덜 요구되는 용도에 매우 적합합니다. 아나타제계 안료는 우수한 광학 특성, 높은 발색력, 높은 가성비로 인해 제지, 섬유, 잉크, 화장품, 고무 및 일부 플라스틱 제품 등 다양한 산업 분야에서 사용되고 있습니다. 이 등급은 가혹한 환경 조건에 대한 노출이 제한적인 응용 분야에서 특히 선호됩니다. 또한, 아나타제형 이산화티타늄은 연마성이 낮은 것으로 밝혀져 가공 시 제조 설비의 마모를 최소화할 수 있습니다. 제지 산업에서는 불투명도와 인쇄성 때문에 화장품 산업에서는 부드러움과 밝기 때문에 사용됩니다. 아나타제 생산에는 여전히 황산법이 사용되고 있으며, 생산비용이 낮기 때문에 개발도상국의 많은 제조업체들이 여전히 황산법을 선호하고 있습니다.

"염화법은 예측 기간 동안 2위의 시장 점유율을 유지할 것으로 예상됩니다."

염화법은 이산화티타늄 시장에서 두 번째로 큰 시장이며, 주로 고급 용도의 고순도 이산화티타늄 안료 생산에 사용됩니다. 이 공정은 티타늄 함유 원료를 사염화티타늄으로 전환하고, 이를 산화시켜 고휘도, 고순도, 고균일성을 자랑하는 이산화티타늄을 생산합니다. 선진 지역에서는 이 공정이 고품질 이산화티타늄 안료 생산에 적합하고 황산법에 비해 폐기물이 적게 발생하기 때문에 선호되고 있습니다. 이 안료는 특히 우수한 내후성과 내구성이 필수적인 자동차 및 산업용 페인트, 플라스틱 및 고성능 응용 분야에서 높은 평가를 받고 있습니다. 또한, 보다 깨끗한 생산 방식을 권장하는 환경 규제 역시 염화법 기술의 채택 확대를 부추기고 있으며, 이 분야에 대한 투자를 더욱 촉진하고 있습니다.

"예측 기간 동안 플라스틱 분야가 두 번째로 큰 시장 규모가 될 것으로 예상됩니다."

이산화티타늄은 플라스틱 제품의 외관, 내구성, 성능을 향상시키는 데 필수적이며, 플라스틱 산업은 이산화티타늄을 두 번째로 많이 사용하는 산업입니다. 이산화티타늄은 불투명도, 밝기, 자외선 차단 효과 및 색상 안정성으로 인해 포장, 소비재, 건축용 플라스틱, 자동차 부품, 가정용품에서 중요한 역할을 하고 있습니다. 가볍고 내구성이 뛰어나며 외관이 좋은 플라스틱에 대한 수요가 증가함에 따라 그 사용량이 증가하고 있습니다. 포장 분야에서는 백색도를 높이고 자외선에 의한 손상으로부터 제품을 보호합니다. 건설 분야에서는 PVC 파이프, 창문, 사이딩에 사용되어 내후성과 내구성을 향상시킵니다. 자동차용 플라스틱은 경량화를 추구하면서 매력적인 마무리를 실현하는 데 도움이 됩니다. 도시화의 진전과 엔지니어링 플라스틱에 대한 수요 증가는 이산화티타늄 사용량의 지속적인 성장을 주도하고 있습니다.

"금액 기준으로는 예측 기간 동안 북미가 두 번째로 큰 시장 규모가 될 것으로 예상됩니다."

북미는 이산화티타늄의 지역별 수요에서 두 번째로 큰 규모를 자랑하며, 탄탄한 산업 기반, 자동차 및 건설 산업의 높은 수요, 그리고 우수한 제조 노하우를 보유하고 있습니다. 미국과 캐나다가 이 지역에서 주도적인 역할을 하고 있습니다. 그 뒤를 이어 페인트 및 코팅 산업이 고도로 발달한 국가들이 그 뒤를 따르고 있으며, 이들 국가에서는 건축, 산업, 자동차 용도의 고품질 이산화티타늄 안료에 대한 의존도가 높아지고 있습니다. 주요 화학 제조업체의 존재와 첨단 염화법 생산 시설의 존재에 힘입어 시장은 계속 성장할 것으로 예상됩니다. 북미의 다른 이산화티타늄 소비 분야로는 플라스틱, 포장, 종이, 화장품 부문이 있습니다. 인프라 재건과 주택 건설이 계속되고 있어 코팅 분야의 수요는 견조하게 유지되고 있습니다. 또한, 업계에서 상당한 기술 혁신이 이루어지고, 지속가능한 노력이 도입되고, 고성능 응용 분야에 대한 투자가 이루어짐에 따라 북미가 세계 이산화티타늄 시장에서 강력한 입지를 유지할 수 있을 것으로 예상됩니다.

대상 기업 : The Chemours Company(미국), Tronox Holdings Plc(미국), LB Group(중국), Kronos Worldwide, Inc. 영국), Tinergy Chemical(중국), Cinkarna Celje d.d.(슬로베니아), Evonik Industries AG(독일), Tayca Corporation(일본) 등이 본 보고서에서 다루어지고 있습니다.

이산화티타늄 시장의 주요 기업들에 대해 기업 프로파일, 최근 동향, 주요 시장 전략을 포함한 상세한 경쟁 분석을 실시했습니다.

조사 범위

이 보고서는 이산화티타늄 시장을 등급별, 공정별, 용도별, 지역별로 분류하고 있습니다. 이 보고서의 연구 범위에는 이산화티타늄 시장의 성장에 영향을 미치는 촉진요인, 제약 조건, 과제 및 기회에 대한 자세한 정보가 포함되어 있습니다. 주요 업계 플레이어에 대한 상세한 분석을 통해 사업 개요, 제공 제품 및 이산화티타늄 시장과 관련된 파트너십, 제휴, 제품 출시, 사업 확장, 인수와 같은 주요 전략에 대한 인사이트를 제공합니다. 이 보고서는 이산화티타늄 시장 생태계에서 신생 스타트업 기업의 경쟁 분석도 다루고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 시장 리더와 신규 진입자에게 전체 이산화티타늄 시장과 각 하위 부문의 매출에 대한 가장 정확한 추정치를 제공합니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 비즈니스 포지셔닝을 위한 인사이트를 높이고, 적절한 시장 진입 전략을 수립하는 데 도움이 될 것입니다. 또한, 시장 동향을 파악하고 주요 시장 촉진요인, 제약 조건, 과제 및 기회에 대한 정보를 제공합니다.

본 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인(전 세계 건설 부문의 호황, DIY용 도료 및 코팅 솔루션에 대한 수요 확대, 경량 차량에 대한 수요 급증, 화장품 및 퍼스널 케어 산업의 급성장, 플라스틱 및 포장 산업에서의 이산화티타늄 사용 증가) 및 제약 요인(이산화티타늄 생산에 관한 정부의 엄격한 환경 정책)에 대한 분석, 기회(화장품 및 건설 업계에서의 이산화티타늄 초미세 입자 높은 채택률, 광촉매로서의 이산화티타늄 활용 확대, 지속 가능한 포장·인쇄 솔루션 추진에서의 잠재적 용도, 리튬이온 배터리 부품에서의 이산화티타늄 효율적 활용, 이산화티타늄을 이용한 수소 생성) 및 과제(이산화티타늄의 안전성에 대한 우려, 이산화티타늄의 비용 변동)에 대한 통찰력을 제공합니다.

- 제품 개발 및 혁신 : 이산화티타늄 시장의 미래 기술, 연구 개발 활동, 제품 및 서비스 출시에 대한 심층적인 인사이트.

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 이산화티타늄 시장을 분석합니다.

- 시장 다각화 : 이산화티타늄 시장의 신제품 및 서비스, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보를 제공합니다.

- 경쟁사 분석 : The Chemours Company(미국), Tronox Holdings Plc(미국), LB Group(중국), Kronos Worldwide, Inc. 영국), Tinergy Chemical(중국), Cinkarna Celje d.d.(슬로베니아), Evonik Industries AG(독일), Tayca Corporation(일본)과 같은 주요 기업의 시장 점유율, 성장 전략, 서비스 제공에 대한 상세 평가 평가.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 이산화티타늄 시장(등급별)

제10장 이산화티타늄 시장(프로세스별)

제11장 이산화티타늄 시장(용도별)

제12장 이산화티타늄 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSM 26.06.08The titanium dioxide market is projected to reach USD 26.32 billion by 2031 from USD 21.82 billion in 2026, at a CAGR of 3.8% from 2026 to 2031. The expansion of the global titanium dioxide market is primarily driven by a thriving construction sector, which increases demand for paints, coatings, and construction materials. The increasing consumer preference for do-it-yourself (DIY) paint and coating options, paired with the rising adoption of lightweight vehicles in the automotive industry, is further bolstering market demand.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million), Volume (Kilotons) |

| Segments | Grade, Process, Application, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

Furthermore, the growth of the cosmetics and personal care sector, along with the rising utilization of titanium dioxide in plastics and packaging applications, is significantly enhancing market development.

"Anatase is projected to be the second-largest segment during the forecast period."

The second-largest market is anatase-grade titanium dioxide, which is a lower-cost product than rutile-grade titanium dioxide and provides good brightness/whiteness and dispersibility. Anatase is less weather-resistant and less UV-stable, but it is very well suited for indoor and less durability-demanding applications. Anatase pigments are used in a wide variety of industries, including paper, textiles, inks, cosmetics, rubber, and some plastic products, due to their good optical characteristics, high color strength, and cost-effectiveness. The grade is especially desirable when the applications will have limited exposure to harsh environmental conditions. The anatase form of titanium dioxide is also found to have a lower abrasiveness, thereby minimizing wear on manufacturing equipment during processing. It is used in the paper industry for opacity and printability and in the cosmetic industry for smoothness and brightness. The sulfate process is still used to manufacture anatase, and many manufacturers in developing economies continue to prefer it because of its low production cost.

"Chloride is expected to hold the second-largest market share during the forecast period."

The chloride process is the second-largest segment in the titanium dioxide market, primarily used to produce high-purity titanium dioxide pigment for premium applications. It involves converting titanium-containing feedstock into titanium tetrachloride, which is then oxidized to produce titanium dioxide that boasts high brightness, purity, and consistency. In developed regions, this process is favored for manufacturing high-quality titanium dioxide pigments, producing less waste than the sulfate process. These pigments are particularly valued in automotive and industrial coatings, plastics, and high-performance applications where exceptional weather resistance and durability are essential. Growing adoption of chloride-based technologies is also encouraged by environmental regulations that favor cleaner production methods, further boosting investment in this area.

"Plastics segment projected to be the second-largest segment during the forecast period."

Titanium dioxide is essential for improving the look, durability, and performance of plastic products, making the plastics industry the second-largest user. Titanium dioxide is key in packaging, consumer goods, construction plastics, automotive parts, and household items because of its opacity, brightness, UV protection, and color stability. Growing demand for lightweight, durable, and attractive plastics has increased their use. In packaging, it enhances whiteness and shields products from UV damage. In construction, it is used in PVC pipes, windows, and siding to boost weather resistance and longevity. In automotive plastics, it helps achieve attractive finishes while keeping weight down. Rising urbanization and the growing need for engineered plastics are driving continued growth in titanium dioxide use.

"In terms of value, the North America region is projected to be the second-largest segment during the forecast period."

North America is the second-largest regional demand for titanium dioxide, with an established industrial base, high demand from the automotive and construction industries, and superior manufacturing expertise. The US and Canada are the leaders in this region. They are closely followed by other countries with well-developed paints and coatings industries, which are heavily reliant on high-quality titanium dioxide pigments for use in architectural, industrial, and automotive applications. The market will grow, supported by the presence of leading chemical manufacturers and advanced chloride-process production facilities. The plastics, packaging, paper, and cosmetics segments are other consumers of titanium dioxide in North America. Coatings demand remains steady due to ongoing infrastructure rebuilding and house-building. Furthermore, the industry has undergone significant innovation, adopted sustainable practices, and invested in high-performance applications, ensuring that North America maintains a strong presence in the global titanium dioxide market.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: The Chemours Company (US), Tronox Holdings Plc (US), LB Group (China), Kronos Worldwide, Inc. (US), Venator Materials PLC (UK), INEOS Group Limited (UK), Tinergy Chemical Co Ltd. (China), Cinkarna Celje d.d. (Slovenia), Evonik Industries AG (Germany), and Tayca Corporation (Japan), among others, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the titanium dioxide market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the titanium dioxide market based on grade (rutile, anatase), process (chloride, sulfate), application (paints & coatings, plastics, papers, inks, and other applications), and region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the titanium dioxide market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as partnerships, collaborations, product launches, expansions, and acquisitions, associated with the titanium dioxide market. This report covers a competitive analysis of upcoming startups in the titanium dioxide market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall titanium dioxide market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (thriving construction sector worldwide, growing demand for do-it-yourself paints and coating solutions, surging demand for lightweight vehicles, booming cosmetics and personal care industries, increasing use of titanium dioxide in plastics & packaging industry), restraints (stringent environmental policies of governments regarding production of titanium dioxide), opportunities (high adoption of ultrafine particles of titanium dioxide in cosmetics and construction industries, increased use of titanium dioxide as photocatalyst, potential use in advancing sustainable packaging and printing solutions, efficient use of titanium dioxide in lithium-ion battery components, hydrogen generation using titanium dioxide), and challenges (concerns about safety of titanium dioxide, volatility in cost of titanium dioxide).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the titanium dioxide market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the titanium dioxide market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the titanium dioxide market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as The Chemours Company (US), Tronox Holdings Plc (US), LB Group (China), Kronos Worldwide, Inc. (US), Venator Materials PLC (UK), INEOS Group Limited (UK), Tinergy Chemical Co Ltd. (China), Cinkarna Celje d.d. (Slovenia), Evonik Industries AG (Germany), and Tayca Corporation (Japan).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 RESEARCH LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN TITANIUM DIOXIDE MARKET

- 3.2 ASIA PACIFIC: TITANIUM DIOXIDE MARKET, BY GRADE AND COUNTRY

- 3.3 TITANIUM DIOXIDE MARKET, BY GRADE

- 3.4 TITANIUM DIOXIDE MARKET, BY PROCESS

- 3.5 TITANIUM DIOXIDE MARKET, BY APPLICATION

- 3.6 TITANIUM DIOXIDE MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Thriving construction sector worldwide

- 4.2.1.2 Growing demand for do-it-yourself paint & coating solutions

- 4.2.1.3 Surging demand for lightweight vehicles

- 4.2.1.4 Booming cosmetics and personal care industries

- 4.2.1.5 Increasing use of titanium dioxide in plastics and packaging industries

- 4.2.2 RESTRAINTS

- 4.2.2.1 Stringent environmental policies of governments regarding production of titanium dioxide

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Efficient use of titanium dioxide in lithium-ion battery components

- 4.2.3.2 Hydrogen generation using titanium dioxide (TiO2)

- 4.2.3.3 High adoption of ultrafine particles of titanium dioxide in cosmetics and construction industries

- 4.2.3.4 Increased use of titanium dioxide as photocatalyst

- 4.2.3.5 Potential use in advancing sustainable packaging and printing solutions

- 4.2.4 CHALLENGES

- 4.2.4.1 Concerns about safety of titanium dioxide

- 4.2.4.2 Volatility in cost of titanium dioxide

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN TITANIUM DIOXIDE MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.4.2.1 PAINTS & COATINGS - PAPER

- 4.4.2.2 PLASTICS - PAINTS & COATINGS

- 4.4.2.3 PAPER - INKS

- 4.4.2.4 PLASTICS - INKS

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING CONSOLIDATION AND INNOVATION

- 4.5.1.1 The Chemours Company Launches Ti-Pure TS-6706

- 4.5.2 INTRODUCTION OF BLUE-TONE TITANIUM DIOXIDE PIGMENT BY TRONOX HOLDINGS PLC

- 4.5.3 TIER 2 PLAYERS: REGIONAL INNOVATORS AND NICHE LEADERS

- 4.5.3.1 Ineos group acquires Eramet titanium & iron (ETI)

- 4.5.3.2 Tayca corporation expands micro titanium dioxide production

- 4.5.4 TIER 3 PLAYERS: STRENGTHENS ECO-EFFICIENCY WITH ZERO WASTE MILESTONE

- 4.5.4.1 GreenTidio Advances Sustainable Titanium Dioxide Technology

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING CONSOLIDATION AND INNOVATION

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF NEW ENTRANTS

- 5.1.5 THREAT OF SUBSTITUTES

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL SUPPLIERS

- 5.3.2 MANUFACTURERS

- 5.3.3 DISTRIBUTORS

- 5.3.4 END-USE SECTORS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 PRICING ANALYSIS

- 5.4.2 INDICATIVE PRICE TREND OF KEY PLAYERS, BY APPLICATION

- 5.4.3 AVERAGE SELLING PRICE TREND OF TITANIUM DIOXIDE, BY REGION, 2022-2026

- 5.4.4 AVERAGE SELLING PRICE TREND OF TITANIUM DIOXIDE, BY REGION

- 5.5 TRADE ANALYSIS

- 5.5.1 EXPORT SCENARIO (HS CODE 282300)

- 5.5.2 IMPORT SCENARIO (HS CODE 282300)

- 5.5.3 EXPORT SCENARIO (HS CODE 320611)

- 5.5.4 IMPORT SCENARIO (HS CODE 320611)

- 5.5.5 EXPORT SCENARIO (HS CODE 320619)

- 5.5.6 IMPORT SCENARIO (HS CODE 320619)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 UTILIZATION OF INNOVATIVE NANO TITANIUM PIGMENTS IN COSMETICS INDUSTRY

- 5.9.2 UTILIZATION OF SUSTAINABLE TI-PURE TITANIUM DIOXIDE PIGMENTS IN PLASTICS INDUSTRY

- 5.9.3 UTILIZATION OF REFORMULATED TIOXIDE TR81 TITANIUM DIOXIDE PIGMENTS IN COATINGS INDUSTRY

- 5.10 IMPACT OF 2025 US TARIFF: TITANIUM DIOXIDE MARKET

- 5.10.1 KEY TARIFF RATES

- 5.10.2 PRICE IMPACT ANALYSIS

- 5.10.3 IMPACT ON COUNTRY/REGION

- 5.10.3.1 US

- 5.10.3.2 Europe

- 5.10.3.3 Asia Pacific

- 5.10.4 END-USE INDUSTRY IMPACT

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 METHOD OF MANUFACTURING TITANIUM DIOXIDE USING CHLORIDE PROCESS

- 6.1.1.1 Method of manufacturing titanium dioxide using sulfate process

- 6.1.1.2 Surface treatment of titanium dioxide

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Dye-sensitized solar cells (DSSC)

- 6.1.2.2 Nanotechnology

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Use of titanium dioxide (TiO2) in green hydrogen production

- 6.1.1 METHOD OF MANUFACTURING TITANIUM DIOXIDE USING CHLORIDE PROCESS

- 6.2 TECHNOLOGY ROADMAP

- 6.2.1 SHORT-TERM (2026-2028) | EARLY TRANSITION TO SMART & LOW-IMPACT TITANIUM DIOXIDE SYSTEMS

- 6.2.2 MID-TERM (2028-2030) | FUNCTIONAL DIFFERENTIATION & CIRCULAR INTELLIGENCE

- 6.2.3 LONG-TERM (2030-2035+) | REGENERATIVE & INTELLIGENT TITANIUM MATERIAL ECOSYSTEMS

- 6.3 PATENT ANALYSIS

- 6.3.1 INTRODUCTION

- 6.3.2 METHODOLOGY

- 6.3.3 TITANIUM DIOXIDE MARKET, PATENT ANALYSIS, 2016-2025

- 6.4 FUTURE APPLICATIONS

- 6.4.1 SELF-HEALING TITANIUM DIOXIDE INFRASTRUCTURE MATERIALS

- 6.4.2 TITANIUM DIOXIDE-DRIVEN NEXT-GENERATION HYDROGEN PRODUCTION SYSTEMS

- 6.4.3 TITANIUM DIOXIDE MEMRISTORS FOR NEUROMORPHIC AI COMPUTING

- 6.4.4 TITANIUM DIOXIDE-ENHANCED QUANTUM MATERIALS AND COMPUTING

- 6.5 IMPACT OF AI/GEN AI ON TITANIUM DIOXIDE MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES IN TITANIUM DIOXIDE PROCESSING

- 6.5.3 CASE STUDIES OF AI IMPLEMENTATION IN TITANIUM DIOXIDE MARKET

- 6.5.3.1 Interconnected ecosystem and impact on market players

- 6.5.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN TITANIUM DIOXIDE MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 RESPONSIBLE CARE INITIATIVE

- 7.2.2 DECREASING CARBON FOOTPRINT

- 7.2.3 ECO-FRIENDLY TITANIUM DIOXIDE INNOVATION

- 7.3 IMPACT OF REGULATORY POLICY ON SUSTAINABILITY INITIATIVES

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS APPLICATIONS

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY APPLICATION

9 TITANIUM DIOXIDE MARKET, BY GRADE

- 9.1 INTRODUCTION

- 9.2 RUTILE

- 9.2.1 GROWING APPLICATION IN PAINTS & COATINGS FOR SCATTERING LIGHT IN PAINT FILMS

- 9.3 ANATASE

- 9.3.1 INCREASING UTILIZATION OF ANATASE-GRADE TITANIUM DIOXIDE IN PHOTOCATALYTIC APPLICATIONS

10 TITANIUM DIOXIDE MARKET, BY PROCESS

- 10.1 INTRODUCTION

- 10.2 CHLORIDE

- 10.2.1 REQUIREMENT OF HIGH-QUALITY TITANIUM DIOXIDE

- 10.3 SULFATE

- 10.3.1 COST-EFFECTIVE PROCESSING OF LOWER-GRADE ORES

11 TITANIUM DIOXIDE MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 PAINTS & COATINGS

- 11.2.1 INCREASING USE OF TITANIUM DIOXIDE IN PAINTS & COATINGS

- 11.3 PLASTICS

- 11.3.1 ENHANCED PERFORMANCE OF PLASTICS

- 11.4 PAPER

- 11.4.1 INCREASED DEMAND FOR DECORATIVE PAPERS

- 11.5 INK

- 11.5.1 CONSIDERABLE INCREASE IN DEMAND FROM ASIA PACIFIC

- 11.6 OTHER APPLICATIONS

12 TITANIUM DIOXIDE MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 Increase in demand from paints & coatings industry

- 12.2.2 INDIA

- 12.2.2.1 Make in India initiative to drive demand for titanium dioxide-infused coatings for industrial applications

- 12.2.3 JAPAN

- 12.2.3.1 Increased demand for titanium dioxide pigments for automotive coatings

- 12.2.4 SOUTH KOREA

- 12.2.4.1 Increasing applications in paints & coatings

- 12.2.5 AUSTRALIA

- 12.2.5.1 High feedstock availability for manufacturing titanium dioxide

- 12.2.6 REST OF ASIA PACIFIC

- 12.2.1 CHINA

- 12.3 NORTH AMERICA

- 12.3.1 US

- 12.3.1.1 Growing use in construction and automotive sectors

- 12.3.2 CANADA

- 12.3.2.1 Growth of construction sector driving demand

- 12.3.3 MEXICO

- 12.3.3.1 Rising demand for paints & coatings in residential segment

- 12.3.1 US

- 12.4 SOUTH AMERICA

- 12.4.1 BRAZIL

- 12.4.1.1 Growing paints & coatings sector

- 12.4.2 ARGENTINA

- 12.4.2.1 Investments in small-scale infrastructure projects

- 12.4.3 REST OF SOUTH AMERICA

- 12.4.1 BRAZIL

- 12.5 EUROPE

- 12.5.1 GERMANY

- 12.5.1.1 Growing construction industry

- 12.5.2 UK

- 12.5.2.1 Significant increase in use of decorative paints & coatings

- 12.5.3 FRANCE

- 12.5.3.1 Increasing use in paints & coatings

- 12.5.4 RUSSIA

- 12.5.4.1 Steady development of construction sector

- 12.5.5 ITALY

- 12.5.5.1 Rising investments in construction industry

- 12.5.6 REST OF EUROPE

- 12.5.1 GERMANY

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 GCC COUNTRIES

- 12.6.1.1 Saudi Arabia

- 12.6.1.1.1 Saudi Vision 2030 vital in driving market

- 12.6.1.2 UAE

- 12.6.1.2.1 Government initiatives to drive market

- 12.6.1.3 Rest of GCC countries

- 12.6.1.1 Saudi Arabia

- 12.6.2 SOUTH AFRICA

- 12.6.2.1 Demand for high titanium content feedstocks

- 12.6.3 REST OF MIDDLE EAST & AFRICA

- 12.6.1 GCC COUNTRIES

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER STRATEGIES

- 13.3 MARKET SHARE ANALYSIS

- 13.4 REVENUE ANALYSIS OF KEY PLAYERS

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS

- 13.6 BRAND COMPARISON

- 13.7 COMPANY EVALUATION QUADRANT

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2026

- 13.7.5.1 Company footprint

- 13.7.5.2 Regional footprint

- 13.7.5.3 Grade footprint

- 13.7.5.4 Process footprint

- 13.7.5.5 Application footprint

- 13.8 STARTUP/SME EVALUATION QUADRANT

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2026

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

- 13.9.4 OTHER DEVELOPMENTS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 THE CHEMOURS COMPANY

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches

- 14.1.1.3.2 Deals

- 14.1.1.3.3 Expansions

- 14.1.1.3.4 Other developments

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 TRONOX HOLDINGS PLC

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches

- 14.1.2.3.2 Other developments

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 LB GROUP

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches

- 14.1.3.3.2 Deals

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 KRONOS WORLDWIDE, INC.

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches

- 14.1.4.3.2 Deals

- 14.1.4.4 MnM view

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 VENATOR MATERIALS PLC

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches

- 14.1.5.3.2 Other developments

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 INEOS GROUP LIMITED

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Deals

- 14.1.6.4 MnM view

- 14.1.6.4.1 Right to win

- 14.1.6.4.2 Strategic choices

- 14.1.6.4.3 Weaknesses and competitive threats

- 14.1.7 TINERGY CHEMICAL CO., LTD.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Expansions

- 14.1.7.3.2 Other developments

- 14.1.7.4 MnM view

- 14.1.7.4.1 Right to win

- 14.1.7.4.2 Strategic choices

- 14.1.7.4.3 Weaknesses and competitive threats

- 14.1.8 CINKARNA CELJE D.D.

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches

- 14.1.8.4 MnM view

- 14.1.9 EVONIK INDUSTRIES AG

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 MnM view

- 14.1.10 TAYCA CORPORATION

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Expansions

- 14.1.10.4 MnM view

- 14.1.1 THE CHEMOURS COMPANY

- 14.2 OTHER PLAYERS

- 14.2.1 TITANOS GROUP

- 14.2.2 GREENTIDIO

- 14.2.3 GUANGDONG HUIYUN TITANIUM CO., LTD.

- 14.2.4 SHANDONG JINHAI TITANIUM RESOURCES TECHNOLOGY CO., LTD.

- 14.2.5 KUMYANG CO., LTD

- 14.2.6 TRAVANCORE TITANIUM PRODUCTS LTD.

- 14.2.7 PRECHEZA A.S.

- 14.2.8 THE KISH COMPANY, INC.

- 14.2.9 MEGHMANI ORGANICS LTD.

- 14.2.10 THE KERALA MINERALS & METALS LIMITED

- 14.2.11 TOR MINERALS

- 14.2.12 KUNCAI

- 14.2.13 DAWN GROUP

- 14.2.14 QIANJIANG FANGYUAN TITANIUM INDUSTRY CO., LTD.

- 14.2.15 GUANGXI JINMAO TITANIUM INDUSTRY

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.3 DATA TRIANGULATION

- 15.4 RESEARCH ASSUMPTIONS

- 15.5 RISK ASSESSMENT

- 15.6 GROWTH RATE ASSUMPTIONS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS