|

시장보고서

상품코드

2050383

오스토미용 드레싱 시장 예측(-2031년) : 제품, 용도(암, 크론병), 최종사용자(병원, 홈케어, ASC), 지역별Ostomy Dressing Market by Product, Application (Cancer, Crohn´s Disease), End User (Hospitals, Home Care, ASCs), and Region - Global Forecast to 2031 |

||||||

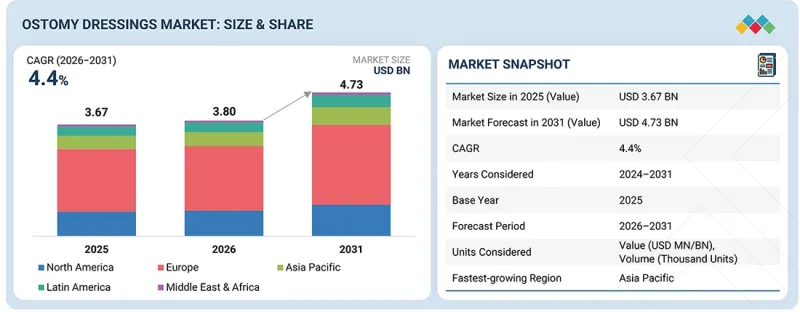

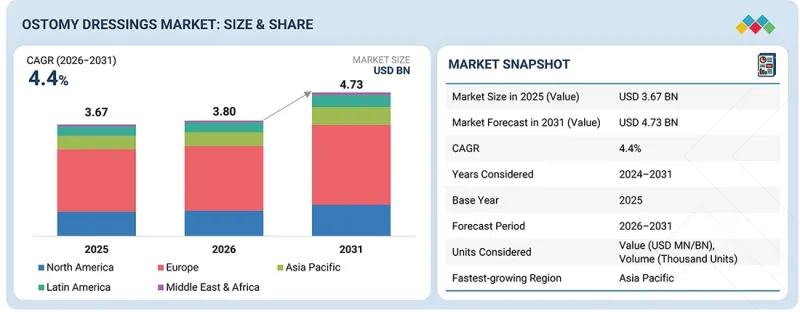

세계의 오스토미용 드레싱 시장 규모는 2026년 38억 달러에서 2031년에는 47억 3,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간 중 CAGR은 4.4%에 달할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(달러) |

| 부문 | 제품, 용도, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

장루용 드레싱 시장은 대장암과 염증성장질환의 증가, 지속적인 치료가 필요한 고령화 인구의 증가로 인해 성장이 예상됩니다. 장루 주변 피부질환에 대한 인식의 증가와 생존율 향상도 산업의 지속적인 성장에 기여하고 있습니다. 또한 개발도상국의 의료 인프라 개선, 유리한 상환 정책, 재택 간호 서비스의 보급으로 인해 장루 드레싱 제품에 대한 접근성이 향상되고 있습니다.

"제품별로는 피부 장벽 부문이 예측 기간 중 가장 높은 CAGR로 성장할 것으로 예상됩니다. "

이러한 성장은 장루 주변 피부 트러블에 대한 인식이 높아지고 효과적인 누출 방지에 대한 수요가 증가함에 따라 성장세를 보이고 있습니다. 피부 배리어링은 장루 주변에 사용되는 성형 가능한 접착 보조기구로, 피부와 장루 주머니 사이에 밀폐 층을 형성합니다. 환자들의 홈케어와 편의성에 대한 관심이 높아짐에 따라 사용하기 쉽고 개인에게 맞는 제품에 대한 수요가 증가하고 있습니다. 또한 피부 친화적인 소재의 발전과 예방적 스킨케어에 대한 관심이 높아진 것도 시장 확대에 기여하고 있습니다.

"최종사용자별로 보면 2025년 병원 부문이 두 번째로 큰 점유율을 차지했습니다. "

이는 주로 수술과 수술 후 관리 모두에서 병원이 중요한 역할을 하기 때문입니다. 인공항문(colostomy), 인공방광(ileostomy), 인공요도(urostomy)를 포함한 대부분의 인공항문 수술은 보통 병원에서 이루어지기 때문에 치료 기간 중 장루 드레싱에 대한 수요의 중요한 원천이 되고 있습니다. 또한 병원은 환자들에게 인공항문 관리에 대한 교육과 치료를 위한 다양한 제품 제공에 있으며, 중요한 역할을 담당하고 있습니다. 병원에서는 첨단 기술을 가진 직원들이 첨단 제품을 사용하므로 병원내 장루용 드레싱의 사용이 증가하고 있습니다.

"아시아태평양이 예측 기간 중 가장 높은 CAGR로 성장할 것으로 예상됩니다. "

아시아태평양 시장은 이 지역의 암 발병률 증가로 인해 절제술이 필요한 환자 수가 증가할 것으로 예상됨에 따라 가장 높은 CAGR을 기록할 것으로 예상됩니다. 2022년 인도에서 약 146만 건의 새로운 암 사례가 보고되었다(Indian Journal of Medical Research). 한편, 중국에서는 약 482만 건으로 추산되고 있다(GLOBOCAN 2022). 또한 공익재단법인 암연구진흥재단이 발표한 기사에 따르면 일본에서는 2024년까지 약 97만 9,300건에 달할 것으로 예측하고 있습니다. 이 수치는 특히 대장암과 방광암의 수술 수요가 매우 높다는 것을 보여줍니다.

또한 아시아태평양은 의료 인프라의 발전, 의료비 증가, 수술 시설에 대한 접근성 향상 등의 혜택을 누리고 있습니다. 장루 관리에 대한 의식의 향상, 지원적인 상환 정책, 재택 간호에 대한 노력도 장루 제품의 보급에 기여하고 있습니다.

세계의 장루용 드레싱(Ostomy Dressing) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 오스토미용 드레싱 시장 : 제품별

제10장 오스토미용 드레싱 시장 : 용도별

제11장 오스토미용 드레싱 시장 : 최종사용자별

제12장 오스토미용 드레싱 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSA 26.06.09The global ostomy dressings market is projected to reach USD 4.73 billion by 2031 from USD 3.80 billion in 2026, at a CAGR of 4.4% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Products, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

The ostomy dressings market is projected to grow due to a rise in cases of colorectal cancer, inflammatory bowel diseases, and an aging population that requires ongoing care. Increased awareness of peristomal skin disorders, along with higher survival rates, also contribute to sustained industry growth. Additionally, improvements in healthcare infrastructure in developing countries, favorable reimbursement policies, and the availability of home care services are enhancing access to ostomy dressing products.

"By product, the skin barrier rings segment is projected to grow at the highest CAGR in the ostomy dressings market during the forecast period."

The market for ostomy products is divided into several segments: ostomy bags/pouches, skin barrier sheets, skin barrier rings, film dressings, and other products. Among these, the skin barrier rings subsegment is expected to grow the fastest during the forecast period. This growth is driven by increasing awareness of peristomal skin issues and the rising demand for effective leakage protection. Skin barrier rings are moldable and adhesive aids used around the stoma site to create a seal between the skin and the ostomy bag. Patients' preference for home care and convenience is driving a growing demand for user-friendly, custom-fit products. Additionally, advancements in skin-friendly materials and a heightened focus on preventative skincare measures are contributing to the market's expansion.

"By end user, the hospitals segment held the second-largest share of the ostomy dressings market in 2025."

The ostomy dressings market is categorized by end users into hospitals, home care settings, ambulatory surgery centers, and other end users. In 2025, the hospitals segment is expected to hold the second-largest market share. This is primarily due to the crucial role hospitals play in both surgeries and post-surgery care. Most ostomy cases, including colostomy, ileostomy, and urostomy, typically occur in hospitals, making them a significant source of demand for ostomy dressings during treatment. Additionally, hospitals are important for educating patients about ostomy care and offering a variety of products for treatment. They employ highly skilled personnel who use advanced products, leading to an increased utilization of ostomy dressings within these facilities.

"The Asia Pacific regional segment is expected to grow at the highest CAGR in the ostomy dressings market during the forecast period."

The ostomy dressings market is divided into five major regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

The Asia Pacific market is expected to experience the highest CAGR due to the increasing burden of cancer in the region, which will lead to a rise in the number of patients requiring ostomy surgery. In 2022, India reported approximately 1.46 million newly diagnosed cancer cases (Indian Journal of Medical Research), while China estimated around 4.82 million cases (GLOBOCAN 2022). Moreover, Japan is projected to reach about 979,300 cases by 2024, according to an article published by the Foundation for the Promotion of Cancer Research. These figures highlight the significant need for surgeries, particularly for colorectal and bladder cancers.

Additionally, the Asia Pacific region is benefiting from advancements in healthcare infrastructure, increased healthcare spending, and improved access to surgical facilities. Growing awareness of ostomy care, supportive reimbursement policies, and home care initiatives are also contributing to the adoption of ostomy products.

A breakdown of the primary participants (supply side) for the ostomy dressings market referred to in this report is provided below:

- By Company Type: Tier 1 (35%), Tier 2 (40%), and Tier 3 (25%)

- By Designation: C-level Executives (45%), Directors (35%), and Others (20%)

- By Region: North America (27%), Europe (25%), Asia Pacific (30%), Latin America (8%), and the Middle East & Africa (10%)

Prominent players in the ostomy dressings market: Coloplast A/S (Denmark), ConvaTec Group Plc (UK), Hollister (US), Salts Healthcare (UK), B. Braun SE (Germany), Solventum (US), Welland Medical Limited (UK), ALCARE Co., Ltd. (Japan), Eakin Healthcare Group (Ireland), Marlen Manufacturing & Development (US), Advin Health Care (India), and Nu-Hope Laboratories, Inc. (US), among others

Research Coverage

The report analyzes the ostomy dressings market and estimates its size and future growth potential across segments such as product, application, end user, and region. The report also includes a competitive analysis of the key players in this market along with their company profiles, service offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will help market leaders/new entrants in this market by providing information on the closest approximations of revenue for the overall ostomy dressing market. This report will help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (rising colorectal and bladder cancer incidence and rising IBD prevalence), restraints (post-surgical complications and quality-of-life concerns), opportunities (rising reimbursement support and awareness initiatives), and challenges (limited awareness and education among patients and caregivers)

- Market Penetration: It includes extensive information on products offered by the major players in the global ostomy dressings market. The report includes various segments in products, applications, end users, and regions.

- Product Enhancement/Innovation: Comprehensive details about new product launches and anticipated trends in the global ostomy dressings market.

- Market Development: Thorough knowledge and analysis of the profitable rising markets by product, application, end user, and region.

- Market Diversification: Comprehensive information about newly launched products, expanding markets, current advancements, and investments in the global ostomy dressings market.

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings of products, and capacities of the major competitors in the global ostomy dressings market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED & REGIONAL SEGMENTATION

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND START DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 OSTOMY DRESSINGS MARKET OVERVIEW

- 3.2 NORTH AMERICA: OSTOMY DRESSINGS MARKET, BY END USER

- 3.3 OSTOMY DRESSINGS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.4 OSTOMY DRESSINGS MARKET: REGIONAL MIX

- 3.5 OSTOMY DRESSINGS MARKET: DEVELOPED COUNTRIES VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rise in colorectal and bladder cancer incidence accelerates long-term demand for ostomy dressing products

- 4.2.1.2 Rise in IBD prevalence driving sustained demand for ostomy dressings products

- 4.2.2 RESTRAINTS

- 4.2.2.1 Post-surgical complications and quality-of-life concerns are restraining ostomy dressing adoption

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increase in reimbursement support and awareness initiatives drive adoption in emerging markets

- 4.2.4 CHALLENGES

- 4.2.4.1 Limited awareness and education among patients and caregivers

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN OSTOMY DRESSINGS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN STOMA CARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL WOUND CARE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS FOR VARIOUS PRODUCTS

- 5.6.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 300691)

- 5.7.2 EXPORT DATA (HS CODE 300691)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 IMPACT OF 2025 US TARIFFS - OSTOMY DRESSINGS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 END-USE INDUSTRY IMPACT

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ADVANCED SKIN BARRIER TECHNOLOGIES

- 6.1.2 LEAK PREVENTION & FLEXIBLE ADHESIVE SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 DERMATOLOGY AND SKIN CARE TECHNOLOGIES

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.4 PATENT ANALYSIS

- 6.4.1 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 SMART OSTOMY SYSTEMS AND DIGITAL SUPPORT

- 6.5.2 SUSTAINABLE AND ECO-FRIENDLY OSTOMY PRODUCTS

- 6.6 IMPACT OF AI/GEN AI ON OSTOMY DRESSINGS MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7 BEST PRACTICES IN OSTOMY DRESSING PROCESSING

- 6.7.1 CASE STUDIES OF AI IMPLEMENTATION IN OSTOMY DRESSINGS MARKET

- 6.7.2 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.3 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN OSTOMY DRESSINGS MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF OSTOMY DRESSINGS MARKET

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF OSTOMY DRESSINGS MARKET

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

- 7.5 REIMBURSEMENT ANALYSIS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 OSTOMY DRESSINGS MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 BAGS/POUCHES

- 9.2.1 COLOSTOMY BAGS/POUCHES

- 9.2.1.1 Rise in colorectal cancer burden to drive sustained demand for colostomy bags

- 9.2.2 ILEOSTOMY BAGS/POUCHES

- 9.2.2.1 Rise in prevalence of inflammatory bowel diseases to fuel growth of ileostomy bags

- 9.2.3 UROSTOMY BAGS/POUCHES

- 9.2.3.1 Increase in bladder cancer incidence to support sustained demand for urostomy bags

- 9.2.1 COLOSTOMY BAGS/POUCHES

- 9.3 SKIN BARRIER SHEETS

- 9.3.1 INCREASE IN FOCUS ON PERISTOMAL SKIN PROTECTION AND COMPLICATION PREVENTION TO FUEL GROWTH OF SKIN BARRIER SHEETS

- 9.4 SKIN BARRIER RINGS

- 9.4.1 RISE IN FOCUS ON LEAKAGE PREVENTION AND SKIN PROTECTION DRIVING GROWTH OF OSTOMY SKIN BARRIER RINGS

- 9.5 FILM DRESSINGS

- 9.5.1 GROWTH IN EMPHASIS ON PREVENTIVE SKIN CARE AND ADHESION SUPPORT TO SUPPORT ADOPTION OF OSTOMY FILM DRESSINGS

- 9.6 OTHER PRODUCTS

10 OSTOMY DRESSINGS MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 CANCER (COLON, BLADDER)

- 10.2.1 CONTINUOUS USAGE OF RELIABLE, HIGH-PERFORMANCE PRODUCTS ACROSS EXTENDED CANCER SURVIVAL PERIODS TO DRIVE CONSUMPTION VOLUMES

- 10.3 CROHN'S DISEASE

- 10.3.1 LIFELONG MANAGEMENT OF CROHN'S DISEASE WITH POTENTIAL FOR MULTIPLE SURGERIES INCREASES DEPENDENCY ON OSTOMY CARE SOLUTIONS

- 10.4 TRAUMATIC INJURY

- 10.4.1 DEPENDENCY ON OSTOMY DRESSINGS FOR POST-SURGICAL MANAGEMENT DURING RECOVERY OR LONG-TERM CARE TO DRIVE CONSISTENT DEMAND

- 10.5 ULCERATIVE COLITIS

- 10.5.1 CHRONIC NATURE OF UC, COMBINED WITH INCREASING INCIDENCE AND LONG-TERM DISEASE MANAGEMENT, TO DRIVE SUSTAINED DEMAND

- 10.6 OTHER APPLICATIONS

11 OSTOMY DRESSINGS MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 HOME CARE SETTINGS

- 11.2.1 HOME CARE SETTINGS SEGMENT HELD MAJOR SHARE IN MARKET

- 11.3 HOSPITALS

- 11.3.1 HIGH VOLUME OF OSTOMY SURGERIES IN HOSPITALS TO DRIVE SIGNIFICANT DEMAND

- 11.4 AMBULATORY SURGICAL CENTERS

- 11.4.1 GROWTH IN COST-EFFICIENT OUTPATIENT COLORECTAL PROCEDURES TO DRIVE SEGMENTAL GROWTH

- 11.5 OTHER END USERS

12 OSTOMY DRESSINGS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 12.2.2 US

- 12.2.2.1 US: Largest country-level North American market

- 12.2.3 CANADA

- 12.2.3.1 Rise in cancer burden and aging population to drive demand

- 12.3 EUROPE

- 12.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 12.3.2 GERMANY

- 12.3.2.1 Germany: Largest share in European ostomy dressings market

- 12.3.3 UK

- 12.3.3.1 Established stoma patient base driving demand

- 12.3.4 FRANCE

- 12.3.4.1 High ostomy patient base and cancer incidence to fuel demand

- 12.3.5 ITALY

- 12.3.5.1 Rise in cancer incidence and established stoma patient base to drive ostomy dressing products demand

- 12.3.6 SPAIN

- 12.3.6.1 Increase in urostomy procedures to drive ostomy care demand in Spain

- 12.3.7 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 12.4.2 CHINA

- 12.4.2.1 China: Largest share in Asia Pacific ostomy dressings market

- 12.4.3 JAPAN

- 12.4.3.1 Rising disease burden, with advanced healthcare infrastructure, strong reimbursement systems, and high adoption of innovative medical products, in Japan

- 12.4.4 INDIA

- 12.4.4.1 Rise in cancer incidence and expanding access to surgical care to support demand

- 12.4.5 AUSTRALIA

- 12.4.5.1 Established patient base and strong healthcare infrastructure, reimbursement support through national programs to aid market growth

- 12.4.6 SOUTH KOREA

- 12.4.6.1 Increase in cancer incidence to aid growth of ostomy dressings market in South Korea

- 12.4.7 REST OF ASIA PACIFIC

- 12.5 LATIN AMERICA

- 12.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 12.5.2 BRAZIL

- 12.5.2.1 Brazil: Largest share in Latin American market

- 12.5.3 MEXICO

- 12.5.3.1 Population prone to cancer and gastrointestinal disorders and aging to contribute to market growth

- 12.5.4 REST OF LATIN AMERICA

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 12.6.2 GCC COUNTRIES

- 12.6.2.1 Rise in cancer incidence and strong healthcare infrastructure to aid market growth

- 12.6.3 REST OF MIDDLE EAST & AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN OSTOMY DRESSINGS MARKET

- 13.3 REVENUE ANALYSIS, 2021-2025

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.5.1 STARS

- 13.5.2 PERVASIVE PLAYERS

- 13.5.3 EMERGING LEADERS

- 13.5.4 PARTICIPANTS

- 13.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.5.5.1 Company footprint

- 13.5.5.2 Regional footprint

- 13.5.5.3 Product Footprint

- 13.5.5.4 Application footprint

- 13.5.5.5 End-user footprint

- 13.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 RESPONSIVE COMPANIES

- 13.6.3 DYNAMIC COMPANIES

- 13.6.4 STARTING BLOCKS

- 13.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.6.5.1 Detailed list of key startups/SMEs

- 13.6.5.2 Competitive benchmarking of key startups/SMEs

- 13.7 COMPANY VALUATION & FINANCIAL METRICS

- 13.7.1 FINANCIAL METRICS

- 13.7.2 COMPANY VALUATION

- 13.8 BRAND/PRODUCT COMPARISON

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES & APPROVALS

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 COLOPLAST A/S

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches & approvals

- 14.1.1.3.2 Deals

- 14.1.1.3.3 Expansions

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses & competitive threats

- 14.1.2 CONVATEC GROUP PLC

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches & approvals

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses & competitive threats

- 14.1.3 B BRAUN SE

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 MnM view

- 14.1.3.3.1 Right to win

- 14.1.3.3.2 Strategic choices

- 14.1.3.3.3 Weaknesses & competitive threats

- 14.1.4 HOLLISTER INCORPORATED

- 14.1.4.1 Business overview

- 14.1.4.2 Recent developments

- 14.1.4.2.1 Product launches & approvals

- 14.1.4.2.2 Expansions

- 14.1.4.2.3 Other developments

- 14.1.4.3 MnM view

- 14.1.4.3.1 Right to win

- 14.1.4.3.2 Strategic choices

- 14.1.4.3.3 Weaknesses & competitive threats

- 14.1.5 SOLVENTUM

- 14.1.5.1 Business overview

- 14.1.5.2 Recent developments

- 14.1.5.2.1 Other developments

- 14.1.5.3 MnM view

- 14.1.5.3.1 Right to win

- 14.1.5.3.2 Strategic choices

- 14.1.5.3.3 Weaknesses & competitive threats

- 14.1.6 ADVIN HEALTH CARE

- 14.1.6.1 Business overview

- 14.1.6.2 Recent developments

- 14.1.6.2.1 Expansions

- 14.1.7 SALTS HEALTHCARE

- 14.1.7.1 Business overview

- 14.1.8 WELLAND MEDICAL LIMITED

- 14.1.8.1 Business overview

- 14.1.8.2 Recent developments

- 14.1.8.2.1 Product launches & approvals

- 14.1.8.2.2 Deals

- 14.1.9 ALCARE CO., LTD.

- 14.1.9.1 Business overview

- 14.1.10 EAKIN

- 14.1.10.1 Business overview

- 14.1.10.1.1 Expansions

- 14.1.10.1 Business overview

- 14.1.11 MARLEN MANUFACTURING & DEVELOPMENT COMPANY

- 14.1.11.1 Business overview

- 14.1.1 COLOPLAST A/S

- 14.2 OTHER PLAYERS

- 14.2.1 CYMED

- 14.2.2 ADVACARE PHARMA

- 14.2.3 NU-HOPE LABORATORIES, INC.

- 14.2.4 SAFE N SIMPLE LLC

- 14.2.5 TORBOT, A DIVISION OF SAFETEC

- 14.2.6 FOR LIFE PRODUKTIONS

- 14.2.7 FORTIS MEDICAL PRODUCTS

- 14.2.8 ANGIPLAST PRIVATE LIMITED

- 14.2.9 PROWESS CARE

- 14.2.10 TRIO HEALTHCARE LTD

- 14.2.11 AVITR FARMICA PVT LTD.

- 14.2.12 CRIMSON HEALTHCARE PVT. LTD

- 14.2.13 WUJIANG EVERGREEN EX/IM CO., LTD.

- 14.2.14 OSTOFORM

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.3 DATA TRIANGULATION

- 15.4 MARKET RANKING ANALYSIS

- 15.5 STUDY ASSUMPTIONS

- 15.6 RESEARCH LIMITATIONS

- 15.6.1 METHODOLOGY-RELATED LIMITATIONS

- 15.6.2 SCOPE-RELATED LIMITATIONS

- 15.7 RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS