|

시장보고서

상품코드

2051995

실험실 자동화 시장 예측(-2031년) : 제품, 용도, 최종사용자별Lab Automation Market by Product, Application, End User Global Forecast to 2031 |

||||||

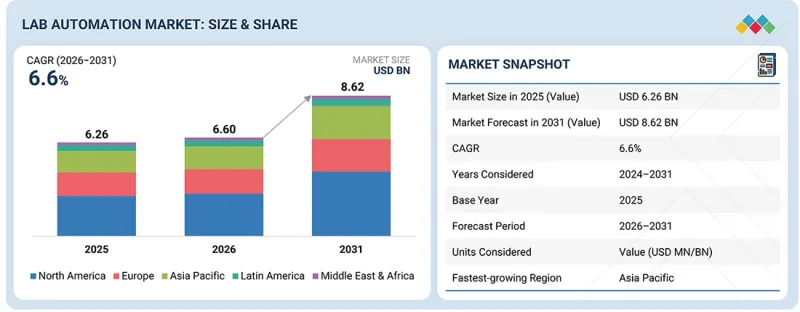

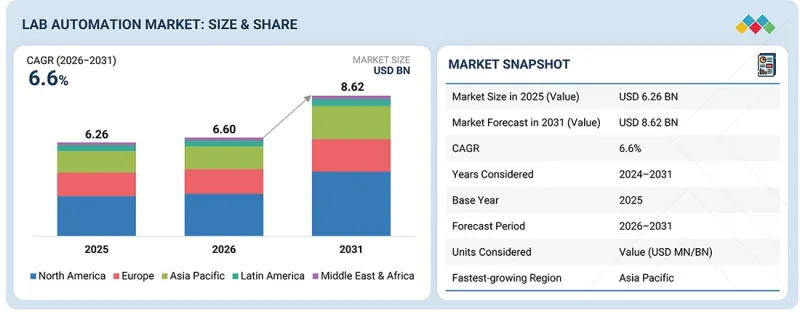

세계의 실험실 자동화 시장 규모는 2026년 66억 달러에서 2031년에는 86억 2,000만 달러로 성장하며, CAGR은 6.6%에 달할 것으로 예측됩니다.

실험실 자동화 도입을 촉진하는 주요 요인으로는 고처리량 검사에 대한 수요, 오믹스 연구의 확대, 실험실 업무에서 보다 정확하고 빠른 결과에 대한 요구 등이 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 제품, 용도, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

또한 만성질환의 증가와 함께 연구개발에 대한 투자가 확대되면서 보다 신속한 진단에 대한 수요가 증가하고 있으며, 이는 실험실의 자동화 도입을 더욱 가속화하고 있습니다.

"2025년에는 자동 워크스테이션 부문이 가장 큰 시장점유율을 차지할 것으로 예상됩니다. "

자동화 워크스테이션 부문은 예측 기간 중 실험실 자동화 시장을 주도할 것으로 예상됩니다. 이 제품군은 간소화된 워크스테이션, 향상된 정확도, 다양한 응용 분야에서 향상된 재현성을 제공하여 실험실 워크플로우를 강화합니다. 자동화 워크스테이션 제품 중 액체 취급 워크스테이션은 PCR, qPCR, 차세대 시퀀싱 등의 응용 분야에 필수적인 고정밀 시료 및 시약 이송에 일반적으로 사용됩니다. 또 다른 중요한 하위 부문은 마이크로플레이트 리더로, 하이스루풋 스크리닝 및 분석의 정량화를 가능하게 하여 신약 개발 및 생물학적 연구를 가속화할 수 있습니다. 또한 자동 ELISA 시스템은 면역측정에 따른 시간 소모적인 프로토콜을 효율화하므로 높은 수요가 있습니다. 이 시스템은 모든 면역측정 절차를 자동화하여 진단 및 임상 실험실에서 수작업을 최소화하면서 신속하고 신뢰할 수 있는 결과를 제공함으로써 시간을 크게 절약할 수 있도록 도와줍니다. 또한 자동 핵산 정제 시스템은 후속 응용을 위한 DNA 및 RNA 추출 및 정제를 신속하게 수행하므로 분자생물학 및 게놈 연구에 필수적입니다. 이러한 하위 부문의 성장은 제약, 진단 및 연구 분야에서 매우 중요한 요소인 효율성과 데이터 품질 향상에 대한 실험실 자동화 시장의 집중을 반영합니다.

"최종사용자별로는 병원 및 진단 연구소 부문이 2025년 가장 큰 점유율을 차지할 것으로 예상됩니다. "

이러한 성장은 주로 다양하고 복잡한 검사를 필요로 하는 더 많은 환자를 치료하는 데 필수적인 처리 능력, 정확성, 빠른 진단 솔루션에 대한 수요 증가에 의해 주도되고 있습니다. 이러한 환경에서 자동화 솔루션은 워크플로우 간소화, 검사 결과 반환 시간 단축, 정확도 향상에 기여할 것입니다.

"예측 기간 중 아시아태평양이 시장에서 가장 높은 성장률을 기록할 것으로 예상됩니다. "

아시아태평양은 실험실 자동화 시장의 성장을 주도하며 예측 기간 중 가장 높은 성장률을 보일 것으로 예상됩니다. 이러한 성장은 의료 인프라에 대한 투자 확대, 제약 및 생명공학 업계의 연구개발에 대한 집중, 인구 증가에 따른 효율적인 진단 솔루션에 대한 수요 증가로 인해 더욱 가속화될 것으로 예상됩니다. 또한 AI와 로봇공학의 발전으로 다양한 분야의 실험실에서 자동화가 진행되고 있습니다.

세계의 실험실 자동화(Lab Automation) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 지역의 규제와 컴플라이언스

제8장 실험실 자동화 시장 : 용도별

제9장 실험실 자동화 시장 : 제품별

제10장 실험실 자동화 시장 : 최종사용자별

제11장 실험실 자동화 시장 : 지역별

제12장 경쟁 구도

제13장 기업 개요

제14장 조사 방법

제15장 부록

KSA 26.06.09The global lab automation market is expected to grow from USD 6.60 billion in 2026 to USD 8.62 billion by 2031, at a CAGR of 6.6%. Key factors driving the adoption of lab automation include the demand for high-throughput testing, the rise in omics research, and the need for more accurate and faster results in laboratory procedures.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Additionally, the increasing prevalence of chronic diseases is driving greater investment in research and development and a demand for faster diagnoses, further accelerating the adoption of automation in laboratories.

"The automated workstations segment accounted for the largest market share in 2025."

The automated workstations segment is expected to lead the lab automation market during the forecast period. This product line enhances laboratory workflow by offering streamlined workstations, increased precision, and improved reproducibility across various applications. Among automated workstation products, liquid-handling workstations are commonly used for high-accuracy sample and reagent transfer, which is essential for applications such as PCR, qPCR, and next-generation sequencing. Another significant subsegment is microplate readers, which enable high-throughput screening and assay quantification, thereby accelerating drug discovery and biological research. Additionally, automated ELISA systems are in high demand because they streamline the time-consuming protocols involved in immunoassays. These systems enable diagnostics and clinical laboratories to save considerable time by automating all immunoassay procedures, delivering rapid, reliable results while minimizing manual intervention. Moreover, automated nucleic acid purification systems are essential for molecular biology and genomics research, as they expedite DNA and RNA extraction and purification for subsequent applications. The growth in these subsegments reflects the lab automation market's focus on increasing efficiency and data quality, which are crucial factors in pharmaceutical, diagnostic, and research settings.

"The hospitals & diagnostic laboratories segment held the largest share of the lab automation market in 2025."

The lab automation market is segmented by end user: hospitals & diagnostic laboratories, pharmaceutical & biotechnology companies, research & academic institutes, environmental testing laboratories, forensic laboratories, and the food & beverage industry. By 2025, hospitals & diagnostic laboratories are expected to hold the largest market share. This growth is primarily driven by increasing demand for throughput, accuracy, and high-speed diagnostic solutions necessary to treat more patients who require a variety of complex tests. Automation solutions in these settings will help simplify workflows, reduce turnaround times, and enhance accuracy.

"Asia Pacific is expected to register the highest growth rate in the market during the forecast period."

The Asia Pacific region is expected to lead the growth in the lab automation market, showing the highest growth rate during the forecast period. This growth will be fueled by increased investment in healthcare infrastructure, a strong emphasis on research and development from the pharmaceutical and biotechnology industries, and a rising demand for efficient diagnostic solutions to serve the region's growing population. Additionally, advancements in artificial intelligence and robotics are helping laboratories in various sectors become more automated.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1 (30%), Tier 2 (42%), and Tier 3 (28%)

- By Designation: C-level Executives (10%), Directors (15%), and Other Designations (75%)

- By Region: North America (40%), Europe (30%), Asia Pacific (22%), and the Rest of the World (8%)

Prominent players in the lab automation market include Thermo Fisher Scientific (US), Tecan Group (Switzerland), Danaher Corporation (US), Agilent Technologies (US), F. Hoffmann-La Roche Ltd. (Switzerland), Revvity (US), Eppendorf AG (Germany), Becton, Dickinson and Company (US), Waters Corporation (US), Siemens Healthineers (Germany), Abbott Laboratories (US), bioMerieux (France), Hamilton Company (US), and Hudson Robotics (US).

Research Coverage

The market is organized by product, application, end user, and region. The report also discusses various factors impacting the lab automation market, including drivers, constraints, opportunities, and challenges. It offers insights into the opportunities and challenges facing stakeholders and profiles the competitive landscape of leading players. Additionally, micromarkets are further divided by examining growth trends, prospects, and how these trends contribute to the lab automation market. Revenue generation across different market segments will be forecasted, with a focus on growth in five major geographic regions.

Key Benefits of Buying this Report

This report is designed to benefit both new and existing players in the lab automation market. It provides in-depth information that helps stakeholders identify potential investment opportunities. The report includes comprehensive details about both key and minor players in the market, supporting effective risk analysis and informed investment decisions. With accurate segmentation by end users and geographic regions, the report offers niche-level insights into specific market segments. Furthermore, it highlights critical trends, challenges, growth drivers, and opportunities, which contribute to a well-rounded strategic decision-making process.

Through this report, readers get insightful views into the following parameters:

Analysis of the key growth drivers, restraints, challenges, and opportunities influencing the market growth for the lab automation market.

Product Development/Innovation: Emerging technologies, ongoing R&D activities, and recent launches of products and services in the antimicrobial susceptibility testing market.

Market Development: The report segments the lab automation market by region.

Market Diversification: New product launches, unexploited markets, recent developments, and investments in the lab automation market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED

- 1.4 INCLUSIONS AND EXCLUSIONS

- 1.4.1 YEARS CONSIDERED

- 1.4.2 CURRENCY CONSIDERED

- 1.5 MARKET STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

- 1.7 ADDITION OF IMPACT OF GENERATIVE AI

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN LAB AUTOMATION MARKET

- 2.4 HIGH GROWTH SEGMENTS

3 PREMIUM INSIGHTS

- 3.1 LAB AUTOMATION MARKET OVERVIEW

- 3.2 LAB AUTOMATION MARKET, BY REGION

- 3.3 ASIA PACIFIC: LAB AUTOMATION MARKET, BY COUNTRY AND END USER

- 3.4 GEOGRAPHIC SNAPSHOT OF LAB AUTOMATION MARKET

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Need for automation in drug discovery

- 4.2.1.2 Advancements in Artificial Intelligence and Robotics

- 4.2.1.3 Growth in demand for process automation for food safety

- 4.2.1.4 Rise in demand for automation in forensics

- 4.2.2 RESTRAINTS

- 4.2.2.1 High initial investment costs

- 4.2.2.2 Slow adoption in developing regions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increased expenditure on healthcare

- 4.2.3.2 Growth in pharmaceutical and biotechnology industries

- 4.2.4 CHALLENGES

- 4.2.4.1 System integration issues

- 4.2.4.2 Availability of refurbished lab automation equipment

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 5.2.3 MACROECONOMIC OUTLOOK FOR EUROPE

- 5.2.4 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 5.2.5 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 5.2.6 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 5.2.7 TRENDS IN GLOBAL LIQUID HANDLING SYSTEM MARKET

- 5.2.8 TRENDS IN GLOBAL MICROPLATE SYSTEM MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RESEARCH & DEVELOPMENT

- 5.3.2 RAW MATERIAL PROCUREMENT & MANUFACTURING

- 5.3.3 DISTRIBUTION, MARKETING & SALES, AND POST-SALES SERVICES

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5.2 AVERAGE SELLING PRICE OF ROBOTIC ARMS, BY KEY PLAYER

- 5.6 TRADE DATA ANALYSIS

- 5.6.1 IMPORT DATA (HS CODE 8479)

- 5.6.2 EXPORT DATA (HS CODE 8479)

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 TOTAL LABORATORY AUTOMATION FOR ENHANCED WORKFORCE PRODUCTIVITY IN CLINICAL CHEMISTRY AND SEROLOGY

- 5.10.2 PRE-ANALYTICAL AUTOMATION AND LIMS INTEGRATION FOR LABORATORY DIGITAL TRANSFORMATION IN PHARMACEUTICAL MANUFACTURING

- 5.10.3 TOTAL LAB AUTOMATION AND LEAN PRINCIPLES FOR MICROBIOLOGY WORKFLOW OPTIMIZATION

- 5.11 IMPACT OF US TARIFFS

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USERS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 COBOTS

- 6.1.2 BIOBANKING

- 6.1.3 HIGH-THROUGHPUT SCREENING (HTS) TECHNOLOGIES

- 6.1.4 COMPLEMENTARY TECHNOLOGY

- 6.1.4.1 Cloud connectivity

- 6.1.4.2 Internet of Things (IoT)

- 6.1.4.3 Digital twins

- 6.1.5 ADJACENT TECHNOLOGY

- 6.1.5.1 Microfluidics technology

- 6.2 PATENT ANALYSIS

- 6.3 FUTURE APPLICATIONS

- 6.4 IMPACT OF AI/GEN AI ON LAB AUTOMATION MARKET

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

- 6.4.2 BEST PRACTICES FOLLOWED BY COMPANIES

- 6.4.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION

- 6.4.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.4.5 CLIENTS' READINESS TO ADOPT AI/GEN AI IN LAB AUTOMATION MARKET

- 6.5 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY STANDARDS AND APPROVALS

- 7.1.1.1 North America

- 7.1.1.1.1 US

- 7.1.1.1.2 Canada

- 7.1.1.2 Europe

- 7.1.1.3 Asia Pacific

- 7.1.1.3.1 Japan

- 7.1.1.3.2 China

- 7.1.1.3.3 India

- 7.1.1.1 North America

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.1 REGULATORY STANDARDS AND APPROVALS

- 7.2 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 7.2.1 DECISION-MAKING PROCESS

- 7.3 KEY STAKEHOLDERS IN BUYING PROCESS AND EVALUATION CRITERIA

- 7.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 7.3.2 KEY BUYING CRITERIA

- 7.4 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 7.5 UNMET NEEDS OF VARIOUS APPLICATIONS

8 LAB AUTOMATION MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 DRUG DISCOVERY

- 8.2.1 ACCELERATION OF DRUG DEVELOPMENT TIMELINE TO DRIVE MARKET

- 8.2.2 HIGH-THROUGHPUT SCREENING

- 8.2.2.1 Integration with automation technologies helps rapidly identify compounds

- 8.2.3 COMPOUND MANAGEMENT

- 8.2.3.1 Offerings by prominent players support growth

- 8.2.4 ADME SCREENING

- 8.2.4.1 Growing requirement for ADME screening in drug discovery to fuel segment

- 8.2.5 COMPOUND WEIGHING & DISSOLUTION

- 8.2.5.1 Potential to improve precision and operational efficiency without user intervention to boost growth

- 8.2.6 OTHER DRUG DISCOVERY APPLICATIONS

- 8.3 DIAGNOSTICS

- 8.3.1 NEED FOR AUTOMATED INSTRUMENTS FOR PRECISION AND EFFICIENCY IN DIAGNOSTICS

- 8.3.2 PRE-ANALYTICS/SAMPLE PREPARATION

- 8.3.2.1 Automation minimizes errors and cuts labor costs while enhancing precision and productivity

- 8.3.3 ENZYME IMMUNOASSAYS

- 8.3.3.1 Rising demand for automation of EIA processes

- 8.3.4 SAMPLE DISTRIBUTION, SPLITTING, AND ARCHIVING

- 8.3.4.1 Ease of monitoring interaction and need for reduced tube manipulation to drive segment

- 8.4 GENOMICS

- 8.4.1 INCREASING APPLICATION OF AUTOMATION IN GENOMICS TO FUEL GROWTH

- 8.5 PROTEOMICS

- 8.5.1 DEMAND FOR ROBOTICS TO REDUCE COMPLEXITY OF PROTEOME DATASETS

- 8.6 MICROBIOLOGY

- 8.6.1 INCREASING PRECISION AND EFFICIENCY SUPPORT DEMAND

- 8.7 OTHER APPLICATIONS

9 LAB AUTOMATION MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 AUTOMATED WORKSTATIONS

- 9.2.1 AUTOMATED LIQUID HANDLING SYSTEMS

- 9.2.1.1 Automated integrated workstations

- 9.2.1.1.1 Increase in applications of workstations

- 9.2.1.2 Pipetting systems

- 9.2.1.2.1 Application of automated pipetting systems across different sectors

- 9.2.1.3 Reagent dispensers

- 9.2.1.3.1 Adoption of advanced technologies by prominent players

- 9.2.1.4 Microplate washers

- 9.2.1.4.1 Multiple benefits provided by microplate washers

- 9.2.1.1 Automated integrated workstations

- 9.2.2 MICROPLATE READERS

- 9.2.2.1 Multi-mode microplate readers

- 9.2.2.1.1 Filter-based readers

- 9.2.2.1.1.1 High sensitivity and high specificity to enhance product demand

- 9.2.2.1.2 Monochromator-based readers

- 9.2.2.1.2.1 Presence of prominent players to support growth

- 9.2.2.1.3 Hybrid readers

- 9.2.2.1.3.1 High flexibility, sensitivity, and convenience to laboratories

- 9.2.2.1.1 Filter-based readers

- 9.2.2.2 Single-mode microplate readers

- 9.2.2.2.1 Fluorescence readers

- 9.2.2.2.1.1 Integration of AI and machine learning

- 9.2.2.2.2 Absorbance readers

- 9.2.2.2.2.1 Advanced products to propel growth

- 9.2.2.2.3 Luminescence readers

- 9.2.2.2.3.1 Greater sensitivity than absorbance and fluorescence readers

- 9.2.2.2.1 Fluorescence readers

- 9.2.2.1 Multi-mode microplate readers

- 9.2.3 AUTOMATED ELISA SYSTEMS

- 9.2.3.1 Integration of automation into ELISA system offers more benefits

- 9.2.4 AUTOMATED NUCLEIC ACID PURIFICATION SYSTEMS

- 9.2.4.1 Wide applications of automated nucleic acid extraction systems

- 9.2.1 AUTOMATED LIQUID HANDLING SYSTEMS

- 9.3 OFF-THE-SHELF AUTOMATED WORK CELLS

- 9.3.1 PRE-ANALYTICAL AUTOMATION

- 9.3.1.1 Enhanced efficiency through pre-analytical automation system

- 9.3.2 POST-ANALYTICAL AUTOMATION

- 9.3.2.1 Innovative automated product launches

- 9.3.3 TOTAL LAB AUTOMATION

- 9.3.3.1 Despite its advantages, total automation challenging to implement in most labs

- 9.3.1 PRE-ANALYTICAL AUTOMATION

- 9.4 SOFTWARE

- 9.4.1 LABORATORY INFORMATION MANAGEMENT SYSTEMS

- 9.4.1.1 Minimizing human errors and increasing efficacy

- 9.4.2 ELECTRONIC LABORATORY NOTEBOOKS

- 9.4.2.1 Data security and user-friendly interface of ELN

- 9.4.3 LABORATORY EXECUTION SYSTEMS

- 9.4.3.1 LES provides paperless, high-productivity environment

- 9.4.4 SCIENTIFIC DATA MANAGEMENT SYSTEMS

- 9.4.4.1 Increased application of SDMS in research

- 9.4.1 LABORATORY INFORMATION MANAGEMENT SYSTEMS

- 9.5 ROBOTIC SYSTEMS

- 9.5.1 ROBOTIC ARMS

- 9.5.1.1 Flexibility, accuracy, and enhanced to increase application of robotic arms

- 9.5.2 TRACK ROBOTS

- 9.5.2.1 Innovative products offered by key players

- 9.5.3 COLLABORATIVE ROBOTS

- 9.5.3.1 Rapidly expanding robotics technology with significant market potential

- 9.5.4 MOBILE ROBOTS

- 9.5.4.1 Significant Technological Trends and integration with software

- 9.5.1 ROBOTIC ARMS

- 9.6 AUTOMATED STORAGE & RETRIEVAL SYSTEMS

- 9.6.1 AUTOMATED STORAGE AND RETRIEVAL SYSTEMS PLAY AN IMPORTANT ROLE IN DRUG DISCOVERY

- 9.7 OTHER LAB AUTOMATION EQUIPMENT

10 LAB AUTOMATION MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 BIOTECHNOLOGY & PHARMACEUTICAL COMPANIES

- 10.2.1 NEED FOR ACCURACY DRIVES DEMAND FOR AUTOMATION

- 10.3 HOSPITAL & DIAGNOSTIC LABORATORIES

- 10.3.1 AUTOMATION MEETS DEMAND FOR FAST AND PRECISE RESULTS

- 10.4 RESEARCH & ACADEMIC INSTITUTES

- 10.4.1 INCREASE IN BIOTECHNOLOGY AND LIFE SCIENCE RESEARCH

- 10.5 ENVIRONMENTAL TESTING LABORATORIES

- 10.5.1 INTEGRATING AUTOMATION IN ENVIRONMENTAL TESTING LABS TO ENHANCE EFFICIENCY

- 10.6 FORENSIC LABORATORIES

- 10.6.1 PROMINENT COMPANIES TO ADOPT AUTOMATION IN FORENSICS FOR BETTER OUTCOME

- 10.7 FOOD & BEVERAGE INDUSTRY

- 10.7.1 INCREASING UTILIZATION OF ROBOTIC ARMS IN FOOD & BEVERAGE INDUSTRY

- 10.8 OTHER END USERS

11 LAB AUTOMATION MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 Strategies adopted by prominent players

- 11.2.2 CANADA

- 11.2.2.1 Innovative products related to automation to boost growth

- 11.2.1 US

- 11.3 EUROPE

- 11.3.1 GERMANY

- 11.3.1.1 Presence of public & private organizations

- 11.3.2 FRANCE

- 11.3.2.1 Rising expenditure by pharma and biotech companies

- 11.3.3 UK

- 11.3.3.1 Advanced automated solutions

- 11.3.4 ITALY

- 11.3.4.1 Expansion of Total Laboratory Automation in Clinical Diagnostics

- 11.3.5 SWITZERLAND

- 11.3.5.1 Recent developments in automation to propel growth

- 11.3.6 NETHERLANDS

- 11.3.6.1 Netherlands leads in R&D for lab automation solutions

- 11.3.7 REST OF EUROPE

- 11.3.1 GERMANY

- 11.4 ASIA PACIFIC

- 11.4.1 CHINA

- 11.4.1.1 Advanced automation solutions brought by key players

- 11.4.2 JAPAN

- 11.4.2.1 Strategic partnerships and expansions

- 11.4.3 INDIA

- 11.4.3.1 Automation technology gaining traction in Indian clinics and hospitals

- 11.4.4 AUSTRALIA

- 11.4.4.1 Advancements in Laboratory Automation and Analytical Workflows

- 11.4.5 SOUTH KOREA

- 11.4.5.1 Rising Investments in AI-Driven and Automated Laboratory Infrastructure

- 11.4.6 REST OF ASIA PACIFIC

- 11.4.1 CHINA

- 11.5 LATIN AMERICA

- 11.5.1 BRAZIL

- 11.5.1.1 Increased expenditure and expansions

- 11.5.2 MEXICO

- 11.5.2.1 Favorable business environment for market players

- 11.5.3 REST OF LATIN AMERICA

- 11.5.1 BRAZIL

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 MIDDLE EAST & AFRICA TO ACCOUNT FOR SMALLEST SHARE OF GLOBAL MARKET

- 11.6.2 GCC COUNTRIES

- 11.6.2.1 Growing Adoption of AI-Enabled and Automated Laboratory Infrastructure

- 11.6.3 REST OF MIDDLE EAST & AFRICA

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGY/RIGHT TO WIN

- 12.3 REVENUE ANALYSIS, 2021-2025

- 12.4 MARKET SHARE ANALYSIS, 2023

- 12.4.1 RANKING OF KEY MARKET PLAYERS

- 12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- 12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.5.5.1 Company footprint

- 12.5.5.2 Regional footprint

- 12.5.5.3 Application footprint

- 12.5.5.4 End user footprint

- 12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- 12.6.5 COMPANY BENCHMARKING: STARTUPS/SMES, 2024

- 12.6.5.1 Competitive benchmarking of emerging players/startups

- 12.6.5.2 Detailed list of key startups/SMEs

- 12.7 COMPANY VALUATION AND FINANCIAL METRICS

- 12.8 PRODUCT/BRAND COMPARISON

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES AND APPROVALS

- 12.9.2 DEALS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 THERMO FISHER SCIENTIFIC INC.

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches and approvals

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Expansions

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 TECAN TRADING AG

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.3.2 DEALS

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 DANAHER CORPORATION

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 DEALS

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 AGILENT TECHNOLOGIES

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches and approvals

- 13.1.4.3.2 Deals

- 13.1.4.3.3 Expansions

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 F. HOFFMANN-LA ROCHE LTD.

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches and approvals

- 13.1.5.3.2 Deals

- 13.1.5.3.3 Expansions

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 METTLER TOLEDO

- 13.1.6.1 Business overview

- 13.1.6.2 Products Offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches and approvals

- 13.1.6.3.2 Deals

- 13.1.7 REVVITY, INC.

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches and approvals

- 13.1.7.3.2 Deals

- 13.1.8 EPPENDORF SE

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Product launches

- 13.1.8.3.2 Deals

- 13.1.9 BECTON, DICKINSON AND COMPANY

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Product launches and approvals

- 13.1.9.3.2 Deals

- 13.1.9.3.3 Expansions

- 13.1.10 WATERS CORPORATION

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Product launches and approvals

- 13.1.10.4 Recent developments

- 13.1.10.4.1 Deals

- 13.1.10.4.2 Expansions

- 13.1.11 SIEMENS HEALTHINEERS

- 13.1.11.1 Business overview

- 13.1.11.2 Products offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Product launches and approvals

- 13.1.11.3.2 Expansions

- 13.1.12 ABBOTT LABORATORIES

- 13.1.12.1 Business overview

- 13.1.12.2 Products offered

- 13.1.13 BIOMERIEUX

- 13.1.13.1 Business overview

- 13.1.13.2 Products offered

- 13.1.14 HAMILTON COMPANY

- 13.1.14.1 Business overview

- 13.1.14.2 Products offered

- 13.1.14.3 Recent developments

- 13.1.14.3.1 Product launches

- 13.1.14.3.2 Deals

- 13.1.15 HUDSON LAB AUTOMATION

- 13.1.15.1 Business overview

- 13.1.15.2 Products offered

- 13.1.15.3 Recent developments

- 13.1.15.3.1 Deals

- 13.1.1 THERMO FISHER SCIENTIFIC INC.

- 13.2 OTHER COMPANIES

- 13.2.1 GILSON, INC.

- 13.2.2 BMG LABTECH

- 13.2.3 FESTO AG & CO. KG

- 13.2.4 AURORA BIOMED INC.

- 13.2.5 HIGHRES BIOSOLUTIONS

- 13.2.6 OPENTRONS LABWORKS INC.

- 13.2.7 PEAK ANALYSIS AND AUTOMATION

- 13.2.8 QIAGEN N.V.

- 13.2.9 LABVANTAGE SOLUTIONS, INC.

- 13.2.10 BIO-RAD LABORATORIES, INC.

- 13.2.11 LABWARE

- 13.2.12 SYSMEX CORPORATION

- 13.2.13 UNIVERSAL ROBOTS

- 13.2.14 AB CONTROLS, INC.

- 13.2.15 AUTOMATA

- 13.2.16 SPT LABTECH

- 13.2.17 BIOSERO, INC.

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.2 RESEARCH DESIGN

- 14.2.1 SECONDARY RESEARCH

- 14.2.1.1 Key data from secondary sources

- 14.2.2 PRIMARY RESEARCH

- 14.2.2.1 Primary sources

- 14.2.2.2 Key industry insights

- 14.2.1 SECONDARY RESEARCH

- 14.3 MARKET SIZE ESTIMATION

- 14.3.1 BOTTOM-UP APPROACH

- 14.3.1.1 Approach 1: Company revenue estimation approach

- 14.3.1.2 Approach 2: Customer-based market estimation

- 14.3.1.3 Approach 3: Top-down approach

- 14.3.1.4 Approach 4: Primary interviews

- 14.3.1 BOTTOM-UP APPROACH

- 14.4 GROWTH FORECAST

- 14.5 DATA TRIANGULATION

- 14.6 MARKET SHARE ASSESSMENT

- 14.7 RESEARCH ASSUMPTIONS

- 14.8 RESEARCH LIMITATIONS

- 14.8.1 RISK ASSESSMENT

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS