|

시장보고서

상품코드

2051997

생명과학 기기 시장 예측(-2031년) : 기술(분광법, 크로마토그래피, NGS, PCR, 현미경, 원심분리기, 액체 처리), 용도(진단, 연구), 최종사용자별(제약 및 바이오의약품, 식품, 병원, 학술기관, CRO)Life Science Instrumentation Market by Technology (Spectroscopy, Chromatography, NGS, PCR, Microscopy, Centrifuge, Liquid Handling), Application (Diagnostic, Research), End User (Pharma-Biopharma, Food, Hospital, Academia, CRO) - Global Forecast to 2031 |

||||||

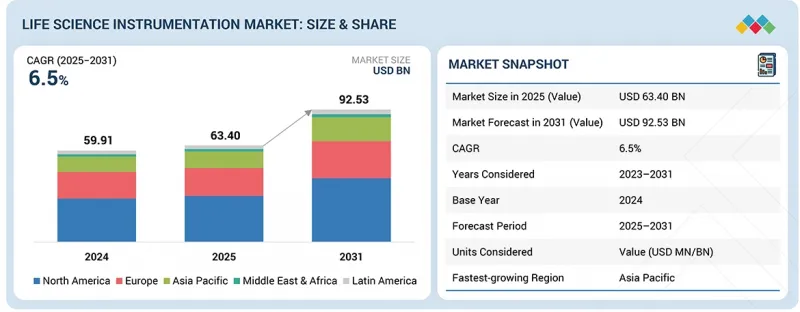

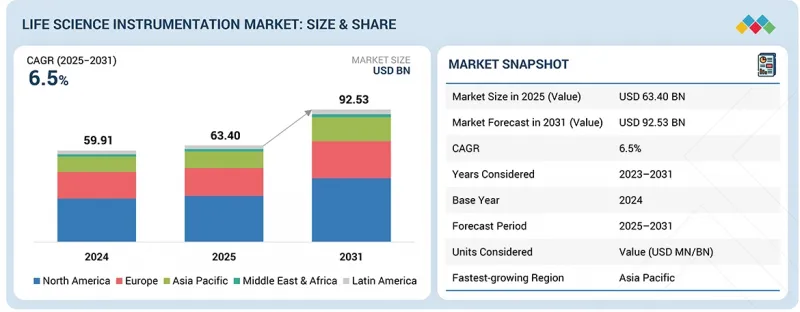

세계의 생명과학 기기 시장 규모는 2025년 634억 달러에서 2031년에는 925억 3,000만 달러에 달할 것으로 예측되고 있으며, 2025-2031년까지 CAGR은 6.5%에 달할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2025-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2025-2031년 |

| 단위 | 금액(달러) |

| 부문 | 기술, 용도, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

연구개발을 지원하는 자금 및 보조금 증가, 단백질체학 연구 활성화, 생명을 위협하는 질병의 유병률 증가 등의 요인이 이 시장의 성장을 주도하고 있습니다.

"2025년에는 분광학 부문이 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. "

분광법 시장은 제약 및 생명공학 연구, 임상 진단, 오믹스 연구 분야에서 첨단 분석 솔루션에 대한 수요 증가에 힘입어 성장하고 있습니다. 또한 정밀의료, 바이오마커 발굴, 신약개발에 대한 관심이 높아지면서 정확한 분자 분석을 위한 UV-Vis, IR, NMR, 질량분석법 등의 분광법 활용이 가속화되고 있습니다.

"2025년에는 연구용 분야가 가장 큰 점유율을 차지할 것으로 예상됩니다. "

연구 응용 분야는 주로 복잡한 생물학적 시스템, 분자 메커니즘, 질병 경로에 대한 이해에 대한 관심이 확대되면서 연구 중심 응용 분야의 급속한 성장에 힘입어 성장하고 있습니다. 학계, 정부 및 민간 기관이 유전체학, 단백질체학, 세포생물학에 대한 투자를 확대하면서 첨단 분석 및 이미징 기술에 대한 수요가 크게 증가하고 있습니다. 또한 맞춤의료, 신약개발, 바이오마커 식별에 대한 관심이 높아지면서 질량분석, 크로마토그래피, PCR, 차세대 시퀀싱 등 첨단 장비의 도입이 가속화되고 있으며, 향후 수년간 연구 부문이 시장 확대의 주요 원동력이 될 것으로 예상됩니다.

"아시아태평양 시장은 예측 기간 중 가장 높은 성장률을 보일 것으로 예상됩니다. "

아시아태평양에서는 생명공학 및 제약 연구에 대한 정부 자금 지원 증가, 학술 및 임상 연구 인프라 확충, 의료 및 진단 부문의 급속한 성장에 힘입어 생명과학 기기 시장이 크게 성장하고 있습니다. 중국, 인도, 일본, 한국 등의 국가에서 제조 및 R&D 시설 설립을 위한 글로벌 및 지역 기업의 투자가 증가하고 있으며, 이는 기술 도입을 촉진하고 있습니다. 만성질환의 유병률 증가와 더불어 첨단 진단 툴 및 정밀의료에 대한 수요 증가는 기기 활용을 더욱 촉진하고 있습니다. 또한 의약품 개발 수탁기관(CRO)의 부상, 규제 개혁의 진전, 품질 기준에 대한 인식이 높아지면서 시장 확대가 촉진되고 있습니다.

세계의 생명과학 기기(Life Science Devices) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI의 도입에 의한 전략적 디스럽션

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 생명과학 기기 시장 : 기술별

제10장 생명과학 기기 시장 : 용도별

제11장 생명과학 기기 시장 : 최종사용자별

제12장 생명과학 기기 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSA 26.06.09The global life science instrumentation market is projected to reach USD 92.53 billion by 2031 from USD 63.40 billion in 2025, at a CAGR of 6.5% from 2025 to 2031.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2025-2031 |

| Base Year | 2025 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD billion) |

| Segments | Technology, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Factors such as increased funding and grants supporting research and development, rising proteomics research, and the increasing prevalence of life-threatening diseases are driving the growth of this market.

"The spectroscopy segment held the largest share of the market in 2025."

Based on technology, the life science instrumentation market is segmented into spectroscopy, chromatography, PCR, immunoassays, lyophilization, liquid handling systems, clinical chemistry analyzers, microscopy, flow cytometry, NGS, centrifuges, electrophoresis, cell counting, and other technologies. The spectroscopy segment held the largest market share in 2025. The spectroscopy market is driven by the growing need for advanced analytical solutions across pharmaceutical and biotechnology research, clinical diagnostics, and omics-based studies. The increasing focus on precision medicine, biomarker discovery, and drug development is also accelerating the use of spectroscopic techniques, such as UV-Vis, IR, NMR, and mass spectrometry, for accurate molecular analysis.

"The research applications segment accounted for the largest share of the market in 2025."

Based on application, the life science instrumentation market is segmented into research applications, clinical & diagnostic applications, and other applications. The research applications segment accounted for the largest market share in 2025. The research applications segment of the life science instrumentation market is primarily driven by the rapid growth of research-focused applications, driven by the increasing emphasis on understanding complex biological systems, molecular mechanisms, and disease pathways. Expanding investments in genomics, proteomics, and cell biology by academic institutions, government bodies, and private organizations are significantly boosting demand for advanced analytical and imaging technologies. Additionally, the growing focus on personalized medicine, drug discovery, and biomarker identification is accelerating the adoption of sophisticated instruments, such as mass spectrometry, chromatography, PCR, and next-generation sequencing, positioning the research segment as a major driver of market expansion over the coming years.

"The market in the Asia Pacific region is expected to witness the highest growth during the forecast period."

The Asia Pacific region is witnessing significant growth in the life science instrumentation market, driven by increasing government funding for biotechnology and pharmaceutical research, expanding academic and clinical research infrastructure, and the rapid growth of the healthcare and diagnostics sectors. Rising investments by global and regional players to establish manufacturing and R&D facilities in countries such as China, India, Japan, and South Korea are fueling technology adoption. The growing prevalence of chronic diseases, coupled with increasing demand for advanced diagnostic tools and precision medicine, is further boosting instrument utilization. Additionally, the emergence of contract research organizations (CROs), favorable regulatory reforms, and growing awareness of quality standards are enhancing market expansion.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1 (20%), Tier 2 (45%), and Tier 3 (35%)

- By Designation: C-level (30%), Director-level (20%), and Others (50%)

- By Region: North America (36%), Europe (25%), Asia Pacific (27%), and the Rest of the World (12%)

The prominent players in the life science instrumentation market are Thermo Fisher Scientific Inc. (US), Danaher Corporation (US), Agilent Technologies, Inc. (US), Waters Corporation (US), Shimadzu Corporation (Japan), Becton, Dickinson and Company (US), PerkinElmer Inc. (US), Bio-Rad Laboratories, Inc. (US), Bruker (US), and Hitachi High-Technologies Corporation (Japan), among others.

Research Coverage

This report analyzes the life science instrumentation market by technology, application, end user, and region. It also covers the factors affecting market growth, analyzes the various opportunities and challenges in the market, and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micromarkets by growth trends and forecasts market segment revenue across five main regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will help market leaders/new entrants with information on the closest approximations of revenue for the overall life science instrumentation market and its subsegments. This report will help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides insights into key drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (rising investments in pharma), restraints (shortage of skilled professionals and high cost of instruments), opportunities (increasing demand for analytical tools in emerging countries, growing pharmaceutical and biotechnology industries, and rising opportunities in emerging countries), and challenges (inadequate infrastructure in emerging countries for research and ethical issues related to privacy of data generated from instruments/software) influencing the growth of the life science instrumentation market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the life science instrumentation market

- Market Development: Comprehensive information about lucrative markets; the report analyzes the life science instrumentation market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the life science instrumentation market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Thermo Fisher Scientific Inc. (US), Danaher Corporation (US), Agilent Technologies, Inc. (US), Waters Corporation (US), and Shimadzu Corporation (Japan), among others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN LIFE SCIENCE INSTRUMENTATION MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN LIFE SCIENCE INSTRUMENTATION MARKET

- 3.2 GROWING DEMAND FOR BIOBANKING, VACCINE STORAGE, AND BIOLOGICAL SAMPLE PRESERVATION

- 3.3 LIFE SCIENCE INSTRUMENTATION MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing investment in pharmaceutical R&D

- 4.2.1.2 Growing concerns regarding food contamination

- 4.2.1.3 Rising importance of biomolecular analysis in research and diagnostics

- 4.2.2 RESTRAINTS

- 4.2.2.1 Premium product pricing for instruments

- 4.2.2.2 Shortage of skilled professionals

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing opportunities from CRO, CDMO, and CTL expansion

- 4.2.3.2 Wide-ranging adoption of analytical instruments across multiple industries

- 4.2.4 CHALLENGES

- 4.2.4.1 Inadequate healthcare infrastructure in emerging economies

- 4.2.4.2 Data privacy concerns associated with NGS software

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN THE GLOBAL LIFE SCIENCE INSTRUMENTATION INDUSTRY

- 5.2.4 TRENDS IN THE GLOBAL HEALTHCARE INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RESEARCH & DEVELOPMENT

- 5.3.2 RAW MATERIAL PROCUREMENT AND MANUFACTURING

- 5.3.3 DISTRIBUTION AND MARKETING & SALES

- 5.3.4 POST-SALES SERVICES

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.4.1 RAW MATERIAL PROCUREMENT

- 5.4.2 MANUFACTURING

- 5.4.3 SALES & DISTRIBUTION

- 5.4.4 END USERS

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 ROLE IN ECOSYSTEM

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF LIFE SCIENCE INSTRUMENTS (PART 1), BY TECHNOLOGY, 2025

- 5.6.2 AVERAGE SELLING PRICE OF LIFE SCIENCE INSTRUMENTS (PART 1), BY REGION, 2025

- 5.6.3 AVERAGE SELLING PRICE OF LIFE SCIENCE INSTRUMENTS (PART 2), BY TECHNOLOGY, 2025

- 5.6.4 AVERAGE SELLING PRICE OF LIFE SCIENCE INSTRUMENTS (PART 2), BY REGION, 2025

- 5.6.5 AVERAGE SELLING PRICE OF LIFE SCIENCE INSTRUMENTS, BY KEY PLAYER, 2025

- 5.6.6 AVERAGE SELLING PRICE TREND OF PRODUCTS, BY REGION, 2023-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO FOR HS CODE 902730

- 5.7.2 EXPORT SCENARIO FOR HS CODE 902730

- 5.8 KEY CONFERENCES AND EVENTS IN 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 IMPACT OF 2025 US TARIFF ON LIFE SCIENCE INSTRUMENTATION MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 North America

- 5.11.4.1.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.4.1 North America

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Fourier transform infrared spectroscopy (FTIR)

- 6.1.1.2 Quadrupole mass analyzers

- 6.1.1.3 Real-time quantitative PCR

- 6.1.1.4 High-throughput screening HTS technologies

- 6.1.1.5 Optical microscope

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Laboratory robotics & automation systems

- 6.1.2.2 Laboratory information management systems (LIMS)

- 6.1.2.3 High-content screening (HCS) and cell imaging platforms

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Artificial intelligence (AI) and machine learning (ML)

- 6.1.3.2 Point-of-care testing (POCT) devices

- 6.1.1 KEY TECHNOLOGIES

- 6.2 PATENT ANALYSIS

- 6.3 IMPACT OF AI/GEN AI ON LIFE SCIENCE INSTRUMENTATION MARKET

- 6.3.1 TOP USE CASES AND MARKET POTENTIAL

- 6.3.2 BEST PRACTICES IN LIFE SCIENCE INSTRUMENTATION MARKET

- 6.3.3 CASE STUDIES ANALYSIS

- 6.3.4 INTERCONNECTED ADJACENT ECOSYSTEM & IMPACT ON MARKET PLAYERS

- 6.3.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN LIFE SCIENCE INSTRUMENTATION MARKET

- 6.4 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.2.1 North America

- 7.1.2.1.1 US

- 7.1.2.1.2 Canada

- 7.1.2.2 Europe

- 7.1.2.2.1 UK

- 7.1.2.2.2 France/ Germany

- 7.1.2.3 Asia Pacific

- 7.1.2.3.1 China

- 7.1.2.3.2 Japan

- 7.1.2.3.3 India

- 7.1.2.4 Latin America

- 7.1.2.4.1 Brazil

- 7.1.2.4.2 Mexico

- 7.1.2.5 Middle East & Africa

- 7.1.2.5.1 UAE

- 7.1.2.5.2 South Africa

- 7.1.2.1 North America

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESSES

- 8.2 KEY STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

9 LIFE SCIENCE INSTRUMENTATION MARKET, BY TECHNOLOGY

- 9.1 INTRODUCTION

- 9.2 SPECTROSCOPY

- 9.2.1 ACCELERATING DRUG DISCOVERY AND DIAGNOSTICS WITH MODERN SPECTROSCOPY SOLUTIONS

- 9.2.2 MASS SPECTROMETERS

- 9.2.2.1 Expanding analytical applications across laboratories to support strong segment growth

- 9.2.3 MOLECULAR SPECTROMETERS

- 9.2.3.1 Increasing use in pathology diagnostics and protein quantification to fuel segment growth

- 9.2.4 ATOMIC SPECTROMETERS

- 9.2.4.1 Increasing use in environmental analysis and industrial chemistry to drive segment growth

- 9.3 CHROMATOGRAPHY

- 9.3.1 ACCELERATING ADOPTION OF ADVANCED CHROMATOGRAPHY PLATFORMS TO DRIVE INNOVATION AND ANALYTICAL EXPANSION IN MARKET

- 9.3.2 LIQUID CHROMATOGRAPHY SYSTEMS

- 9.3.2.1 Increasing adoption of LC systems in pharmaceutical workflows to propel market

- 9.3.3 GAS CHROMATOGRAPHY SYSTEMS

- 9.3.3.1 Growing demand for efficient separation of volatile organic compounds in biopharmaceutical and food & beverage applications to support market expansion

- 9.3.4 SUPERCRITICAL FLUID CHROMATOGRAPHY SYSTEMS

- 9.3.4.1 Enhanced sample transfer efficiency and improved separation performance to fuel market expansion

- 9.3.5 THIN-LAYER CHROMATOGRAPHY SYSTEMS

- 9.3.5.1 Growing adoption of TLC for simultaneous multi-sample separation to accelerate market expansion

- 9.4 POLYMERASE CHAIN REACTION

- 9.4.1 INCREASING PREVALENCE OF INFECTIOUS AND GENETIC DISEASES TO ACCELERATE PCR ADOPTION

- 9.4.2 QUANTITATIVE PCR

- 9.4.2.1 Growing utilization of qPCR by researchers and healthcare providers to significantly accelerate segment expansion

- 9.4.3 DIGITAL PCR

- 9.4.3.1 Continuous advancements in technology to accelerate market expansion

- 9.4.4 OTHER PCR

- 9.5 IMMUNOASSAYS

- 9.5.1 RISING DEMAND FOR HIGHLY SENSITIVE AND ACCURATE IMMUNOASSAY TESTING TO FUEL MARKET

- 9.6 LYOPHILIZATION

- 9.6.1 RISING DEMAND FOR STABLE BIOLOGICS AND DIAGNOSTIC REAGENTS TO DRIVE LYOPHILIZATION ADOPTION IN LIFE SCIENCE INSTRUMENTATION

- 9.6.2 TRAY-STYLE FREEZE DRYERS

- 9.6.2.1 Increasing demand for freeze-dried food to propel segment growth

- 9.6.3 MANIFOLD FREEZE DRYERS

- 9.6.3.1 Increasing adoption in laboratories for storing bottles and vials to drive segment growth

- 9.6.4 SHELL (ROTARY) FREEZE DRYERS

- 9.6.4.1 Increasing research on food ingredients and biologic molecules development to drive segment growth

- 9.7 LIQUID HANDLING SYSTEMS

- 9.7.1 RISING DEMAND FOR HIGH-THROUGHPUT SCREENING, AUTOMATION, AND PRECISE FLUID HANDLING IN PHARMACEUTICAL, BIOTECHNOLOGY, AND LIFE SCIENCE RESEARCH TO DRIVE MARKET

- 9.7.2 ELECTRONIC LIQUID HANDLING SYSTEM

- 9.7.2.1 Increasing demand for freeze-dried food to propel segment growth

- 9.7.3 AUTOMATED LIQUID HANDLING SYSTEMS

- 9.7.3.1 Enhanced speed and operational efficiency over traditional electronic systems to drive market

- 9.7.4 MANUAL LIQUID HANDLING SYSTEMS

- 9.7.4.1 Increasing research on development of food ingredients and biologic molecules to drive segment growth

- 9.8 CLINICAL CHEMISTRY ANALYZERS

- 9.8.1 INCREASING VOLUME OF CLINICAL TESTING PROCEDURES TO FUEL MARKET

- 9.9 MICROSCOPY

- 9.9.1 RISING DEMAND FOR HIGH-THROUGHPUT SCREENING, AUTOMATION, AND PRECISE FLUID HANDLING IN PHARMACEUTICAL, BIOTECHNOLOGY, AND LIFE SCIENCE RESEARCH TO DRIVE MARKET

- 9.9.2 OPTICAL MICROSCOPES

- 9.9.2.1 Cost-effectiveness, user-friendly operation, and simplified particle screening to drive demand

- 9.9.3 ELECTRON MICROSCOPES

- 9.9.3.1 Enhanced speed and operational efficiency over traditional electronic systems to drive demand

- 9.9.4 SCANNING PROBE MICROSCOPES

- 9.9.4.1 Rising utilization in nanotechnology research to support market growth

- 9.9.5 OTHER MICROSCOPES

- 9.10 FLOW CYTOMETRY

- 9.10.1 RISING DEMAND FOR HIGH-THROUGHPUT SCREENING, AUTOMATION, AND PRECISE FLUID HANDLING IN PHARMACEUTICAL, BIOTECHNOLOGY, AND LIFE SCIENCE RESEARCH TO DRIVE MARKET

- 9.10.2 CELL ANALYZERS

- 9.10.2.1 Continuous technological advancements and introduction of innovative products to drive market

- 9.10.3 CELL SORTERS

- 9.10.3.1 Rising demand for high-precision, high-throughput cell separation in research, clinical applications, and personalized medicine to drive market

- 9.11 NEXT-GENERATION SEQUENCING

- 9.11.1 EXPANDING USE OF PERSONALIZED MEDICINE FOR CANCER AND GENETIC DISORDER TREATMENTS TO FUEL MARKET

- 9.12 CENTRIFUGES

- 9.12.1 GROWING NEED FOR PRECISE AND EFFICIENT SAMPLE SEPARATION TO DRIVE MARKET

- 9.12.2 MICROCENTRIFUGES

- 9.12.2.1 High precision and efficiency in small-volume sample processing to drive market

- 9.12.3 MULTIPURPOSE CENTRIFUGES

- 9.12.3.1 Broad laboratory applications and high versatility to drive demand

- 9.12.4 MINICENTRIFUGES

- 9.12.4.1 Compact design and quick, small-volume sample processing to drive demand

- 9.12.5 ULTRACENTRIFUGES

- 9.12.5.1 High-speed separation of macromolecules and subcellular components to drive demand

- 9.12.6 AUTOMATED CENTRIFUGES.

- 9.12.6.1 Rising Adoption of Laboratory Automation and High-Throughput Sample Processing

- 9.12.7 OTHER CENTRIFUGES.

- 9.13 ELECTROPHORESIS

- 9.13.1 GROWING NEED FOR PRECISE AND EFFICIENT SAMPLE SEPARATION TO DRIVE DEMAND

- 9.13.2 GEL ELECTROPHORESIS SYSTEMS

- 9.13.2.1 Growing emphasis on proteomics research and expanding adoption of personalized medicine to fuel market

- 9.13.3 CAPILLARY ELECTROPHORESIS SYSTEMS

- 9.13.3.1 Growing need for fast, high-resolution biomolecule separation to drive demand

- 9.14 CELL COUNTING

- 9.14.1 RISING DEMAND FOR ACCURATE, HIGH-THROUGHPUT CELL ANALYSIS IN DRUG DISCOVERY, CANCER RESEARCH, AND BIOPHARMACEUTICAL DEVELOPMENT TO DRIVE MARKET

- 9.14.2 AUTOMATED CELL COUNTERS

- 9.14.2.1 Increasing emphasis on research targeting life-threatening diseases to fuel market

- 9.14.3 HEMOCYTOMETERS & MANUAL CELL COUNTERS

- 9.14.3.1 Increasing adoption of manual cell counters alongside automated systems to drive market

- 9.15 OTHER TECHNOLOGIES

- 9.15.1 LABORATORY FREEZERS

- 9.15.1.1 Increasing demand for blood and blood components to fuel market

- 9.15.1.2 FREEZERS

- 9.15.1.2.1 Demand for ultra-low storage, biobanking, and safe, energy-efficient freezers to drive market

- 9.15.1.3 Refrigerators

- 9.15.1.3.1 Demand for reliable cold storage of samples and reagents to drive market

- 9.15.2 HEAT STERILIZATION

- 9.15.2.1 Rising need for infection control to drive heat sterilization demand

- 9.15.2.2 Moist Heat/Steam Sterilization Instruments.

- 9.15.2.2.1 Growing demand for reliable microbial sterilization to drive steam sterilization market

- 9.15.2.3 Dry Heat Sterilization Instrumentation

- 9.15.2.3.1 Demand for reliable cold storage of samples and reagents to drive market

- 9.15.3 MICROPLATE SYSTEMS

- 9.15.3.1 Extensive applications across various sectors to fuel market expansion

- 9.15.3.2 Microplate Readers

- 9.15.3.2.1 Ability to quickly and accurately analyze multiple samples for research, diagnostics, and drug discovery to drive market

- 9.15.3.3 Microplate Dispensers

- 9.15.3.3.1 Growing lab automation and demand for high-throughput screening in life-science research to drive market

- 9.15.3.4 Microplate Washers

- 9.15.3.4.1 Rising lab automation and high-throughput assay demand to drive market

- 9.15.4 LABORATORY BALANCES

- 9.15.4.1 Technical advantages and growing use to boost demand

- 9.15.5 COLORIMETERS

- 9.15.5.1 Affordable pricing and user-friendly operation to drive demand

- 9.15.6 INCUBATORS

- 9.15.6.1 Increasing use of instruments in microbiological applications to fuel market

- 9.15.7 FUME HOODS

- 9.15.7.1 Increasing focus on lab safety and hazardous fume containment to drive demand

- 9.15.8 ROBOTIC SYSTEMS

- 9.15.8.1 Advances in technology to drive market

- 9.15.8.2 Robotic Arms

- 9.15.8.2.1 Growing need to improve throughput, precision, and reproducibility in laboratory workflows to drive demand

- 9.15.8.3 Track Robot Systems

- 9.15.8.3.1 Growing demand for automated sample transport and high-throughput laboratory workflows to drive market

- 9.15.9 PH METERS

- 9.15.9.1 Increasing applications in pharmaceutical and food & beverage industries to drive demand

- 9.15.10 CONDUCTIVITY AND RESISTIVITY METERS

- 9.15.10.1 Efficient performance and cost-effective operation to drive demand

- 9.15.11 DISSOLVED CO2 AND O2 METERS

- 9.15.11.1 Increasing use in water quality testing to drive demand

- 9.15.12 TITRATORS

- 9.15.12.1 Increasing use in quality control testing for industrial chemical applications to drive demand

- 9.15.13 GAS ANALYZERS

- 9.15.13.1 Increasing use in iron and steel industry to drive demand

- 9.15.14 TOC ANALYZERS

- 9.15.14.1 Rising demand for contamination monitoring and quality control to drive market

- 9.15.15 THERMAL ANALYZERS

- 9.15.15.1 Increasing focus on contamination monitoring and quality control to drive demand

- 9.15.16 SHAKERS/ROTATORS & STIRRERS

- 9.15.16.1 Rising research activities in pharmaceutical and biotechnology sectors to demand

- 9.15.1 LABORATORY FREEZERS

10 LIFE SCIENCE INSTRUMENTATION MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 RESEARCH APPLICATIONS

- 10.2.1 RISING DEMAND FOR ADVANCED ANALYTICAL AND HIGH-THROUGHPUT TECHNOLOGIES TO ACCELERATE SCIENTIFIC RESEARCH

- 10.3 CLINICAL & DIAGNOSTIC APPLICATIONS

- 10.3.1 GROWING INCIDENCE OF INFECTIOUS AND CHRONIC TARGET DISEASES TO BOOST MARKET DEMAND

- 10.4 OTHER APPLICATIONS

11 LIFE SCIENCE INSTRUMENTATION MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 HOSPITALS & DIAGNOSTIC LABORATORIES

- 11.2.1 INCREASING NEED FOR RAPID, ACCURATE DISEASE DIAGNOSIS AND GROWING ADOPTION OF ADVANCED MOLECULAR TESTING TO DRIVE MARKET

- 11.3 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 11.3.1 INCREASING INVESTMENTS IN R&D TO STRENGTHEN THERAPEUTIC DRUG PIPELINES TO BOOST MARKET

- 11.4 ACADEMIC & RESEARCH INSTITUTES

- 11.4.1 INCREASING EMPHASIS ON INTERDISCIPLINARY RESEARCH AND RISING DEMAND FOR HIGH-QUALITY SCIENTIFIC EDUCATION TO BOOST MARKET

- 11.5 AGRICULTURE & FOOD INDUSTRIES

- 11.5.1 RISING EMPHASIS ON FOOD SAFETY AND QUALITY TO FUEL MARKET

- 11.6 ENVIRONMENTAL TESTING LABORATORIES

- 11.6.1 INCREASING ENVIRONMENTAL REGULATIONS AND RISING DEMAND FOR PRECISE DETECTION OF POLLUTANTS IN AIR, WATER, AND SOIL TO DRIVE ADOPTION OF ADVANCED INSTRUMENTATION

- 11.7 CLINICAL RESEARCH ORGANIZATIONS

- 11.7.1 RISING OUTSOURCING OF DRUG DEVELOPMENT TO DRIVE ADOPTION OF ADVANCED LIFE SCIENCE INSTRUMENTS

- 11.8 OTHER END USERS

12 LIFE SCIENCE INSTRUMENTATION MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 12.2.2 US

- 12.2.2.1 Rising diagnostic testing demand driven by strong laboratory infrastructure

- 12.2.3 CANADA

- 12.2.3.1 Growing burden of chronic diseases to accelerate demand for advanced life science instrumentation

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Strong biotech and pharma R&D activity to drive demand for life science instruments

- 12.3.2 UK

- 12.3.2.1 Increasing research initiatives and stronger academia-industry collaborations to drive market

- 12.3.3 FRANCE

- 12.3.3.1 Rising investments in infrastructure development for life science R&D to drive market

- 12.3.4 ITALY

- 12.3.4.1 Rising diagnostics demand and growing R&D activity to drive market

- 12.3.5 SPAIN

- 12.3.5.1 Growing biotechnology activity and rising investment in life science R&D to fuel market

- 12.3.6 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 ASIA PACIFIC

- 12.4.1 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 12.4.2 CHINA

- 12.4.2.1 Rising investments in biopharma and diagnostics to fuel market expansion

- 12.4.3 JAPAN

- 12.4.3.1 Rising diagnostic testing and biomedical research to support market growth

- 12.4.4 INDIA

- 12.4.4.1 Increasing healthcare infrastructure and biopharma research to boost instrumentation demand

- 12.4.5 AUSTRALIA

- 12.4.5.1 Policy-driven phase-outs and sophisticated national monitoring (CSIRO and IMOS) to drive market

- 12.4.6 SOUTH KOREA

- 12.4.6.1 Local manufacturing and global partnerships to strengthen life science instrumentation ecosystem

- 12.4.7 REST OF ASIA PACIFIC

- 12.5 LATIN AMERICA

- 12.5.1 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 12.5.2 BRAZIL

- 12.5.2.1 Unparalleled scientific diagnosis (MICROMar) mandating high-fidelity morphological analytical methods to drive market

- 12.5.3 MEXICO

- 12.5.3.1 Healthcare expansion and laboratory modernization to support demand for life science instrumentation

- 12.5.4 REST OF LATIN AMERICA

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 12.6.2 GCC COUNTRIES

- 12.6.2.1 Rising healthcare investments and expanding diagnostic infrastructure to drive market

- 12.6.3 REST OF MIDDLE EAST & AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN 2022-2026

- 13.3 REVENUE ANALYSIS, 2023-2025

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.5 MARKET RANKING ANALYSIS, 2025

- 13.6 BRAND/PRODUCT COMPARISON

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.7.5.1 Company footprint

- 13.7.5.2 Region footprint

- 13.7.5.3 Technology footprint

- 13.7.5.4 Application footprint

- 13.7.5.5 End user footprint

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPANY VALUATION AND FINANCIAL METRICS

- 13.10 COMPETITIVE SCENARIO

- 13.10.1 PRODUCT LAUNCHES

- 13.10.2 DEALS

- 13.10.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 THERMO FISHER SCIENTIFIC INC.

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 PRODUCT LAUNCHES AND APPROVALS

- 14.1.1.3.2 DEALS

- 14.1.1.3.3 Expansions

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 AGILENT TECHNOLOGIES, INC.

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches and approvals

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 DANAHER CORPORATION

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.2.1 Product launches and approvals

- 14.1.3.2.2 Deals

- 14.1.3.2.3 Expansions

- 14.1.3.3 MnM view

- 14.1.3.3.1 Right to win

- 14.1.3.3.2 Strategic choices

- 14.1.3.3.3 Weaknesses and competitive threats

- 14.1.4 SHIMADZU CORPORATION

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches and approvals

- 14.1.4.3.2 Deals

- 14.1.4.3.3 Expansions

- 14.1.4.4 MnM view

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 WATERS CORPORATION

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches and approvals

- 14.1.5.3.2 Deals

- 14.1.5.3.3 Expansions

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 BRUKER CORPORATION

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 PRODUCT LAUNCHES AND APPROVALS

- 14.1.6.3.2 Deals

- 14.1.7 JEOL LTD.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches and approvals

- 14.1.7.3.2 Deals

- 14.1.8 MERCK KGAA

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Deals

- 14.1.8.3.2 Expansions

- 14.1.9 BECTON, DICKINSON AND COMPANY

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 PRODUCT LAUNCHES AND APPROVALS

- 14.1.9.3.2 Deals

- 14.1.9.3.3 Expansions

- 14.1.10 PERKINELMER

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Product launches and approvals

- 14.1.10.3.2 Deals

- 14.1.11 BIO-RAD LABORATORIES, INC.

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Deals

- 14.1.12 EPPENDORF SE

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.12.3 Recent developments

- 14.1.12.3.1 Product launches and approvals

- 14.1.12.3.2 Expansions

- 14.1.13 HORIBA LTD.

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.13.3 Recent developments

- 14.1.13.3.1 PRODUCT LAUNCHES AND APPROVALS

- 14.1.14 QIAGEN

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.14.3 Recent developments

- 14.1.14.3.1 PRODUCT LAUNCHES AND APPROVALS

- 14.1.14.3.2 Deals

- 14.1.15 HITACHI HIGH-TECH CORPORATION

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.15.3 Recent developments

- 14.1.15.3.1 Product launches and approvals

- 14.1.15.3.2 Expansions

- 14.1.1 THERMO FISHER SCIENTIFIC INC.

- 14.2 OTHER PLAYERS

- 14.2.1 BIOMERIEUX

- 14.2.2 TECAN TRADING AG

- 14.2.3 SIGMA LABORZENTRIFUGEN GMBH

- 14.2.4 ILLUMINA, INC

- 14.2.5 AVANTOR, INC

- 14.2.6 OLYMPUS CORPORATION

- 14.2.7 OXFORD INSTRUMENTS

- 14.2.8 GILSON INCORPORATED

- 14.2.9 GL SCIENCES INC

- 14.2.10 ACCU-SCOPE INC.

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH APPROACH

- 15.1.1 SECONDARY RESEARCH

- 15.1.2 PRIMARY RESEARCH

- 15.1.2.1 Primary sources

- 15.1.2.2 Key industry insights

- 15.1.2.3 Breakdown of primaries

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.1.1 Approach 1: Company revenue estimation approach

- 15.2.1.2 Approach 2: Customer-based market estimation

- 15.2.1.3 Growth forecast

- 15.2.1.4 CAGR projections: Supply-side analysis

- 15.2.1 BOTTOM-UP APPROACH

- 15.3 DATA TRIANGULATION APPROACH

- 15.4 MARKET SHARE ESTIMATION

- 15.5 RESEARCH ASSUMPTIONS

- 15.6 RISK ASSESSMENT

- 15.6.1 RISK ASSESSMENT: LIFE SCIENCE INSTRUMENTATION MARKET

- 15.7 GROWTH RATE ASSUMPTIONS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS