|

시장보고서

상품코드

2055589

데이터 다이오드 시장(-2031년) : 폼 팩터, 용도별Data Diode Market by Form Factor (DIN Rail, Embedded/OEM Modules & PCIe Systems), Application Area (Operational Process Visibility & Analytics, OT Security Monitoring & Compliance, Physical Security & Surveillance Monitoring) - Global Forecast to 2031 |

||||||

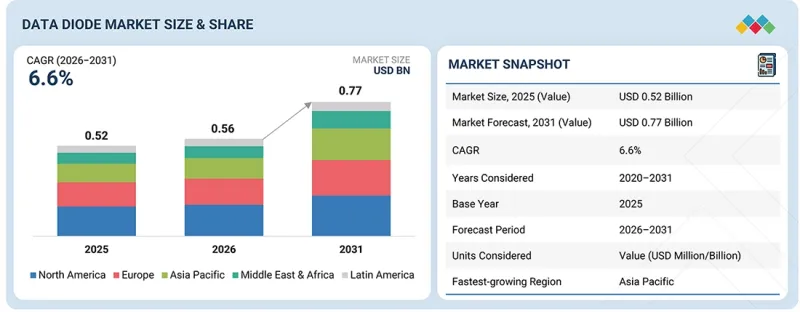

데이터 다이오드 시장 규모는 예측 기간 중에 CAGR 6.6%로 확대되어 2026년 5억 6,000만 달러에서 2031년에는 7억 7,000만 달러에 이를 전망입니다.

산업용 및 중요 인프라 환경을 겨냥한 랜섬웨어 공격이 증가함에 따라, 가동 중단, 생산 손실, 사업 중단에 대한 우려가 커지고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020년-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 제공 구분, 폼팩터, 유형, 조직 규모, 용도, 업종 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

기업들은 운영 시스템의 보안 확보, 부정 접근 방지, 산업 활동의 지속적 유지, 중요한 생산 및 인프라 환경에 영향을 미치는 사이버 위협의 위험을 줄이기 위해 데이터 다이오드 및 네트워크 분리 기술의 도입을 점점 더 확대되고 있습니다.

“업종별로는 정부 및 방위 부문이 2026년에 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. '

국방 및 정부 기관에서는 기밀성이 높은 군사 네트워크, 지휘통제 시스템, 정보 분석 플랫폼, 레이더 시스템, 위성 통신 인프라, 미션 크리티컬한 국방 환경을 사이버 스파이 활동이나 국가 지원형 공격으로부터 보호하기 위해 데이터 다이오드 솔루션의 도입이 확대되고 있습니다. 하드웨어를 통한 단방향 통신을 통해 운용 데이터 및 정보 데이터의 안전한 전송이 가능해지는 한편, 기밀성이 높은 방위 시스템에 대한 불법적인 인바운드 접근을 물리적으로 차단합니다. 사이버 전쟁 대비, 안전한 크로스 도메인 통신, 에어 갭이 적용된 군사 인프라 보호를 위한 투자 증가가 단방향 게이트웨이 기술의 도입을 가속화하고 있습니다. CISA와 NIST에 따르면, 국방 기관들은 계속해서 네트워크 세분화, 제로 트러스트 보안, 복원력 있는 운영 기술 보호 프레임워크를 우선순위로 삼고 있으며, 이는 국가 안보 및 국방 인프라 전반에 걸친 고도화된 데이터 다이오드 도입에 대한 강력한 수요를 뒷받침하고 있습니다.

“소프트웨어 부문은 예측 기간 동안 가장 높은 연평균 성장률(CAGR)을 보일 것으로 예측됩니다. '

산업 및 국방 분야 전반에서 유연성, 확장성, 통합 관리가 가능한 단방향 통신 솔루션에 대한 수요가 증가함에 따라, 소프트웨어 부문이 강력한 성장세를 보이고 있습니다. 기업들은 안전한 프로토콜 복제, 원격 모니터링, 도메인 간 통신, 클라우드, AI, 산업용 분석 시스템과의 통합을 지원하기 위해 소프트웨어 정의 데이터 다이오드 플랫폼의 도입을 점점 더 확대되고 있습니다. IT와 OT의 융합이 진전되고, 가상화된 산업 인프라가 확대되며, 비용 효율적인 사이버 보안 아키텍처에 대한 수요가 증가함에 따라 소프트웨어 기반의 단방향 보안 솔루션 도입이 더욱 가속화되고 있습니다. 또한, 중앙 집중식 OT 보안 관리, 안전한 데이터 시각화, 다중 벤더 산업 환경에서의 상호 운용성에 대한 관심이 높아지고 있는 점이 소프트웨어 부문의 급속한 성장을 뒷받침하고 있습니다.

본 보고서에서는 전 세계 데이터 다이오드 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류 및 지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 프로파일 등을 종합적으로 다루고 있습니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 소비자 상황과 구매 행동

제9장 데이터 다이오드 시장 : 제공 구분별

제10장 데이터 다이오드 시장 : 폼 팩터별

제11장 데이터 다이오드 시장 : 유형별

제12장 데이터 다이오드 시장 : 조직 규모별

제13장 데이터 다이오드 시장 : 용도별

제14장 데이터 다이오드 시장 : 산업별

제15장 데이터 다이오드 시장 : 지역별

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

LSH 26.06.19The data diode market is projected to grow from USD 0.56 billion in 2026 to USD 0.77 billion by 2031 at a compound annual growth rate (CAGR) of 6.6% during the forecast period. Growing ransomware attacks on industrial and critical infrastructure environments are increasing concerns regarding operational downtime, production losses, and business disruptions.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) |

| Segments | Offering, Form Factor, Type, Organization Size, Application Area, Vertical |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

Organizations are increasingly adopting data diodes and network isolation technologies to secure operational systems, prevent unauthorized access, maintain continuous industrial operations, and reduce the risk of cyber threats impacting critical production and infrastructure environments.

"By vertical, the government & defense segment is projected to hold the largest market share in 2026."

Defense and government organizations are increasingly deploying data diode solutions to secure classified military networks, command-and-control systems, intelligence platforms, radar systems, satellite communication infrastructure, and mission-critical defense environments from cyber espionage and state-sponsored attacks. Hardware-enforced one-way communication enables secure transfer of operational and intelligence data while physically preventing unauthorized inbound access into highly sensitive defense systems. Rising investments in cyber warfare preparedness, secure cross-domain communication, and protection of air-gapped military infrastructure are accelerating the adoption of unidirectional gateway technologies. According to CISA and NIST, defense agencies continue prioritizing network segmentation, zero-trust security, and resilient operational technology protection frameworks, supporting strong demand for advanced data diode deployments across national security and defense infrastructure.

"By offering, the software segment is expected to witness the highest CAGR during the forecast period."

The software segment is witnessing strong growth in the data diode Market due to increasing demand for flexible, scalable, and centrally managed unidirectional communication solutions across industrial and defense environments. Organizations are increasingly adopting software-defined data diode platforms to support secure protocol replication, remote monitoring, cross-domain communication, and integration with cloud, AI, and industrial analytics systems. Growing IT-OT convergence, expansion of virtualized industrial infrastructure, and rising demand for cost-effective cybersecurity architectures are further accelerating the adoption of software-based unidirectional security solutions. Additionally, increasing focus on centralized OT security management, secure data visibility, and interoperability across multi-vendor industrial environments is supporting the rapid growth of the software segment.

Breakdown of Primaries

The study draws insights from a range of industry experts, including component suppliers, tier 1 companies, and OEMs. The break-up of the primaries is as follows:

- By Company Type: Tier 1 - 20%, Tier 2 - 32%, and Tier 3 - 48%

- By Designation: C-level - 40%, Managerial & Other Levels - 60%

- By Region: North America - 40%, Europe - 25%, Asia Pacific - 20%, Middle East & Africa - 10%, Latin America - 5%

Major vendors in the data diode market include Forcepoint (US), Naonworks (South Korea), Waterfall Security Solutions (Israel), Infodas (Germany), Siemens (Germany), OPSWAT (US), Advenica (Sweden), Everfox (US), Garland Technology (US), Arbit Cyber Defence Systems (Denmark), Fibersystem (Sweden), VADO Security Technologies (Israel), Chipspirit (India), Sunhillo (US), Link22 (Sweden), 4Secure (UK), Stratign (UAE), Oakdoor (UK), BAE Systems (UK), ST Engineering (Singapore), Owl Cyber Defense (US), and Nexor (UK).

The study includes an in-depth competitive analysis of the key players in the data diode market, their company profiles, recent developments, and key market strategies.

Research Coverage

The report segments the data diode market and forecasts its size based on offering (hardware, software, services [consulting & design, deployment & integration, support & maintenance, education & training]), form factor (DIN rail, rack-mount, small/portable form, embedded/OEM modules & PCIE systems), type (ruggedized data diodes, non-ruggedized data diodes), organization size (SMEs, large enterprises), application area (operational process visibility & analytics, OT security monitoring & compliance, security domain & cross-classification information exchange, physical security & surveillance monitoring), vertical (government & defense, energy & utilities, manufacturing, aerospace & aviation, BFSI, telecom, transportation, others [healthcare, IT]), and region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America).

The study also includes an in-depth competitive analysis of the market's key players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report

The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall Data diode market and its subsegments. This report will help stakeholders understand the competitive landscape and gain valuable insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of drivers (rising cyberattacks targeting critical infrastructure and industrial control systems, increasing need for secure data transfer between isolated OT networks and enterprise IT environments, growing regulatory pressure for critical infrastructure and national security protection), restraints (high capital and deployment costs for industrial-grade unidirectional security infrastructure, Difficulty integrating data diodes into legacy OT systems and proprietary industrial environments), opportunities (emerging use cases for data diodes across smart manufacturing, renewable energy, transportation, and industrial IoT environments; growing demand for compact and embedded data diode solutions for edge and remote industrial operations) and challenges (shortage of OT cybersecurity expertise and industrial security awareness, maintaining interoperability across diverse industrial communication protocols and multi-vendor OT environments).

- Product Development/Innovation: Detailed insights on upcoming technologies, research development activities, new products, and service launches in the data diode market

- Market Development: Comprehensive information about lucrative markets - the report analyses the Data diode market across varied regions

- Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the data diode market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players Forcepoint (US), Naonworks (South Korea), Waterfall Security Solutions (Israel), Infodas (Germany), Siemens (Germany), OPSWAT (US), Advenica (Sweden), Everfox (US), Garland Technology (US), Arbit (Denmark), Fibersystem (Sweden), VADO Security Technologies (Israel), Chipspirit (India), Sunhillo (US), Link22 (Sweden), 4Secure (UK), Stratign (UAE), Oakdoor (UK), BAE Systems (UK), ST Engineering (Singapore), Owl Cyber Defense (US), and Nexor (UK), among others, in the data diode market strategies

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGION COVERAGE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DATA DIODE MARKET

- 3.2 DATA DIODE MARKET, BY OFFERING

- 3.3 DATA DIODE MARKET, BY SERVICE

- 3.4 DATA DIODE MARKET, BY FORM FACTOR

- 3.5 DATA DIODE MARKET, BY TYPE

- 3.6 DATA DIODE MARKET, BY ORGANIZATION SIZE

- 3.7 DATA DIODE MARKET, BY VERTICAL

- 3.8 DATA DIODE MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising cyberattacks targeting critical infrastructure and industrial control systems

- 4.2.1.2 Increasing need for secure data transfer between isolated OT networks and enterprise IT environments

- 4.2.1.3 Growing regulatory pressure for critical infrastructure and national security protection

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital and deployment costs for industrial-grade unidirectional security infrastructure

- 4.2.2.2 Difficulty integrating data diodes into legacy OT systems and proprietary industrial environments

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Emerging cases for data diodes in non-traditional critical infrastructure sectors

- 4.2.3.2 Growing demand for compact and embedded data diode solutions in edge and remote industrial environments

- 4.2.4 CHALLENGES

- 4.2.4.1 Shortage of OT cybersecurity expertise and industrial security awareness

- 4.2.4.2 Maintaining interoperability across diverse industrial communication protocols

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER -1/2/3 PLAYERS

- 4.5.1 CROSS-TIER STRATEGIC PATTERNS

- 4.5.2 STRATEGIC TRENDS

- 4.5.2.1 Expansion of Secure OT-to-IT Connectivity

- 4.5.2.2 Compact and Edge-Oriented Industrial Deployments

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL ICT INDUSTRY

- 5.2.4 TRENDS IN GLOBAL ICS SECURITY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 COMPONENT

- 5.3.2 PLANNING AND DESIGN

- 5.3.3 INFRASTRUCTURE DEVELOPMENT

- 5.3.4 SYSTEM INTEGRATION

- 5.3.5 CONSULTATION

- 5.3.6 VERTICALS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY FORM FACTOR, 2025

- 5.5.2 INDICATIVE PRICING ANALYSIS FOR KEY VENDORS, 2025

- 5.6 KEY CONFERENCES & EVENTS, 2026

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE: 8541)

- 5.7.2 EXPORT SCENARIO (HS CODE: 8541)

- 5.8 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 OWL CYBER DEFENSE SECURES ATM DATA COLLECTION OF NATIONAL BANK WITH OPDS-100 DATA DIODE SOLUTION

- 5.10.2 ADVENICA SECURES MAJOR ENERGY COMPANY WITH SECURICDS DATA DIODES AND ZONEGUARD SOLUTIONS

- 5.10.3 NEXOR ENABLED SECURE AND EFFICIENT FILE TRANSFERS FOR EUROPEAN MULTI-PARTNER ORGANIZATION WITH DATA GUARD SOLUTION

- 5.10.4 VADO SECURITY TECHNOLOGIES SECURES DETACHED NETWORKS AND CRITICAL INFRASTRUCTURE WITH OPTICAL ONE-WAY DATA DIODE SOLUTIONS

- 5.11 IMPACT OF 2025 US TARIFF - DATA DIODE MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Optical isolation

- 6.1.1.2 Protocol conversion

- 6.1.1.3 Traffic filtering and packet inspection

- 6.1.1.4 Encryption and data masking

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Data logging and audit systems

- 6.1.2.2 Data loss prevention (DLP)

- 6.1.2.3 Encryption key management

- 6.1.2.4 VPN and secure tunneling

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Industrial control systems (ICS) and SCADA

- 6.1.3.2 Firewall and network segmentation

- 6.1.3.3 Network monitoring and intrusion detection systems (IDS)

- 6.1.3.4 Secure file transfer protocol (SFTP)

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 SHORT-TERM (2026-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.2.2 MID-TERM (2027-2030) SCALING, INTELLIGENCE & ECOSYSTEM EXPANSION

- 6.2.3 LONG-TERM (2030-2035+) | AUTONOMOUS, PREDICTIVE & SELF-HEALING INDUSTRIAL SECURITY

- 6.3 PATENT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 SECURE OT-TO-IT TELEMETRY TRANSFER & REMOTE MONITORING

- 6.4.2 ZERO TRUST SEGMENTATION FOR CRITICAL INFRASTRUCTURE

- 6.4.3 EDGE & EMBEDDED DATA DIODE DEPLOYMENTS

- 6.4.4 SECURE CLOUD-CONNECTED INDUSTRIAL MONITORING

- 6.4.5 HIGH-ASSURANCE CROSS-DOMAIN COMMUNICATION FOR DEFENSE & GOVERNMENT

- 6.5 IMPACT OF AI/GEN AI ON DATA DIODE MARKET

- 6.5.1 BEST PRACTICES IN DATA DIODE MARKET

- 6.5.2 CASE STUDIES OF AI IMPLEMENTATION IN DATA DIODE MARKET

- 6.5.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN DATA DIODE MARKET

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 CERTIFICATIONS AND COMPLIANCES

- 7.1.2.1 Critical infrastructure compliance (NERC CIP, IEC 62443)

- 7.1.2.2 Critical infrastructure compliance (NERC CIP, IEC 62443)

- 7.1.2.3 Product assurance levels (Common Criteria, Eal Levels)

- 7.1.2.4 Regional Regulatory Alignment

8 CONSUMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

9 DATA DIODE MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.1.1 OFFERING: DATA DIODE MARKET DRIVERS

- 9.2 HARDWARE

- 9.2.1 HARDWARE ENABLES SECURE ONE-WAY DATA TRANSFER ACROSS SENSITIVE OPERATIONAL ENVIRONMENTS DRIVING MARKET GROWTH

- 9.3 SOFTWARE

- 9.3.1 SOFTWARE STRENGTHENS CENTRALIZED VISIBILITY AND SECURE DATA ORCHESTRATION

- 9.4 SERVICES

- 9.4.1 SERVICES SUPPORT SECURE DEPLOYMENT AND LONG-TERM OPERATIONAL RELIABILITY

- 9.4.2 CONSULTING AND DESIGN

- 9.4.3 DEPLOYMENT AND INTEGRATION

- 9.4.4 SUPPORT AND MAINTENANCE

- 9.4.5 EDUCATION AND TRAINING

10 DATA DIODE MARKET, BY FORM FACTOR

- 10.1 INTRODUCTION

- 10.1.1 FORM FACTOR: DATA DIODE MARKET DRIVERS

- 10.2 DIN RAIL

- 10.2.1 DIN RAIL FORM FACTORS SUPPORT INDUSTRIAL CONTROL AND AUTOMATION ENVIRONMENTS

- 10.3 RACK-MOUNT

- 10.3.1 RACK-MOUNT DEPLOYMENTS ENABLE CENTRALIZED MANAGEMENT OF HIGH-VOLUME OPERATIONAL DATA

- 10.4 SMALL/PORTABLE FORM

- 10.4.1 SMALL AND PORTABLE FORM FACTORS SUPPORT REMOTE AND SPACE-CONSTRAINED DEPLOYMENTS

- 10.5 EMBEDDED/OEM MODULES & PCIE SYSTEMS

- 10.5.1 EMBEDDED AND OEM DEPLOYMENTS SUPPORT INTEGRATED INDUSTRIAL SECURITY ARCHITECTURES

11 DATA DIODE MARKET, BY TYPE

- 11.1 INTRODUCTION

- 11.1.1 TYPE: DATA DIODE MARKET DRIVERS

- 11.2 RUGGEDIZED DATA DIODES

- 11.2.1 RUGGEDIZED DATA DIODES SUPPORT OPERATIONS IN HARSH INDUSTRIAL ENVIRONMENTS

- 11.3 NON-RUGGEDIZED DATA DIODES

- 11.3.1 NON-RUGGEDIZED DATA DIODES SUPPORT CONTROLLED OPERATIONAL AND ENTERPRISE ENVIRONMENTS

12 DATA DIODE MARKET, BY ORGANIZATION SIZE

- 12.1 INTRODUCTION

- 12.1.1 ORGANIZATION SIZE: DATA DIODE MARKET DRIVERS

- 12.2 SMES

- 12.2.1 SMES INCREASINGLY ADOPT SECURE COMMUNICATION ARCHITECTURES TO STRENGTHEN CYBER RESILIENCE

- 12.3 LARGE ENTERPRISES

- 12.3.1 LARGE ENTERPRISES DEPLOY SCALABLE ARCHITECTURES ACROSS DISTRIBUTED OT ECOSYSTEMS

13 DATA DIODE MARKET, BY APPLICATION AREA

- 13.1 INTRODUCTION

- 13.1.1 APPLICATION AREA: DATA DIODE MARKET DRIVERS

- 13.2 OPERATIONAL PROCESS VISIBILITY & ANALYTICS

- 13.2.1 DATA DIODES SUPPORT SECURE TELEMETRY TRANSFER FOR INDUSTRIAL VISIBILITY AND ANALYTICS

- 13.3 OT SECURITY MONITORING AND COMPLIANCE

- 13.3.1 DATA DIODES ENABLE SECURE LOG FORWARDING AND CENTRALIZED OT SECURITY MONITORING

- 13.4 SECURITY DOMAIN & CROSS-CLASSIFICATION INFORMATION EXCHANGE

- 13.4.1 DATA DIODES ENABLE SECURE LOG FORWARDING AND CENTRALIZED OT SECURITY MONITORING

- 13.5 PHYSICAL SECURITY AND SURVEILLANCE MONITORING

- 13.5.1 DATA DIODES ENABLE SECURE VIDEO AND SURVEILLANCE DATA TRANSFER ACROSS OPERATIONAL NETWORKS

14 DATA DIODE MARKET, BY VERTICAL

- 14.1 INTRODUCTION

- 14.1.1 VERTICAL: DATA DIODE MARKET DRIVERS

- 14.2 GOVERNMENT AND DEFENSE

- 14.2.1 GOVERNMENT AND DEFENSE ORGANIZATIONS PRIORITIZE AIR-GAPPED COMMUNICATION ARCHITECTURES

- 14.3 ENERGY & UTILITIES

- 14.3.1 ENERGY & UTILITIES OPERATORS DEPLOY DATA DIODES TO SECURE GRID AND PROCESS OPERATIONS

- 14.4 MANUFACTURING

- 14.4.1 MANUFACTURERS INTEGRATE DATA DIODES WITH INDUSTRIAL AUTOMATION AND PROCESS CONTROL SYSTEMS

- 14.5 AEROSPACE & AVIATION

- 14.5.1 AEROSPACE AND AVIATION SECTORS PRIORITIZE SECURE TELEMETRY AND SURVEILLANCE COMMUNICATION

- 14.6 BFSI

- 14.6.1 BFSI ORGANIZATIONS DEPLOY DATA DIODES TO STRENGTHEN NETWORK SEGMENTATION AND SECURE TRANSACTION ENVIRONMENTS

- 14.7 TELECOM

- 14.7.1 TELECOM OPERATORS USE DATA DIODES TO SECURE CORE NETWORK AND MONITORING INFRASTRUCTURE

- 14.8 TRANSPORTATION

- 14.8.1 TRANSPORTATION OPERATORS DEPLOY DATA DIODES TO SECURE SIGNALING AND OPERATIONAL CONTROL NETWORKS

- 14.9 OTHER VERTICALS

15 DATA DIODE MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 NORTH AMERICA: DATA DIODE MARKET DRIVERS

- 15.2.2 US

- 15.2.2.1 Rising OT cyber threats and utility modernization initiatives driving deployment across US

- 15.2.3 CANADA

- 15.2.3.1 Expansion of industrial cybersecurity and grid modernization initiatives supporting adoption in Canada

- 15.3 EUROPE

- 15.3.1 EUROPE: DATA DIODE MARKET DRIVERS

- 15.3.2 UK

- 15.3.2.1 Expansion of critical infrastructure cybersecurity initiatives supporting market growth in the UK

- 15.3.3 GERMANY

- 15.3.3.1 Industrial automation and smart manufacturing initiatives driving deployment across Germany

- 15.3.4 FRANCE

- 15.3.4.1 Increasing utility and transportation modernization initiatives driving adoption in France

- 15.3.5 ITALY

- 15.3.5.1 Increasing digital transformation initiatives and rising cyber threats driving data diode demand in Italy

- 15.3.6 REST OF EUROPE

- 15.4 ASIA PACIFIC

- 15.4.1 ASIA PACIFIC: DATA DIODE MARKET DRIVERS

- 15.4.2 CHINA

- 15.4.2.1 Industrial automation and smart infrastructure expansion driving deployment across China

- 15.4.3 JAPAN

- 15.4.3.1 Critical infrastructure modernization and industrial cybersecurity initiatives supporting adoption in Japan

- 15.4.4 INDIA

- 15.4.4.1 Smart grid modernization and industrial digitalization initiatives driving market growth in India

- 15.4.5 SOUTH KOREA

- 15.4.5.1 Semiconductor manufacturing and smart factory expansion accelerating deployment across South Korea

- 15.4.6 REST OF ASIA PACIFIC

- 15.5 MIDDLE EAST & AFRICA

- 15.5.1 MIDDLE EAST & AFRICA: DATA DIODE MARKET DRIVERS

- 15.5.2 GCC

- 15.5.2.1 Oil & gas digitization and smart infrastructure modernization driving deployment across GCC countries

- 15.5.2.2 UAE

- 15.5.2.3 KSA

- 15.5.2.4 Rest of GCC countries

- 15.5.3 SOUTH AFRICA

- 15.5.3.1 Expansion of industrial cybersecurity and utility modernization initiatives supporting market growth in South Africa

- 15.5.4 REST OF MIDDLE EAST & AFRICA

- 15.6 LATIN AMERICA

- 15.6.1 LATIN AMERICA: DATA DIODE MARKET DRIVERS

- 15.6.2 BRAZIL

- 15.6.2.1 Rapid fintech growth, regulatory enforcement, and rising cyber threats driving data diode demand in Brazil

- 15.6.3 MEXICO

- 15.6.3.1 Expanding digital economy, cross-border cloud adoption, and increasing cyber risks driving data diode growth in Mexico

- 15.6.4 REST OF LATIN AMERICA

16 COMPETITIVE LANDSCAPE

- 16.1 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2024-2026

- 16.2 REVENUE ANALYSIS, 2021-2025

- 16.3 MARKET SHARE ANALYSIS, 2025

- 16.4 BRAND COMPARISON

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS

- 16.5.1 COMPANY VALUATION, 2026

- 16.5.2 FINANCIAL METRICS USING EV/EBIDTA, 2026

- 16.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.6.1 STARS

- 16.6.2 EMERGING LEADERS

- 16.6.3 PERVASIVE PLAYERS

- 16.6.4 PARTICIPANTS

- 16.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.6.5.1 Company footprint

- 16.6.5.2 Regional footprint

- 16.6.5.3 Offering footprint

- 16.6.5.4 Type footprint

- 16.6.5.5 Vertical footprint

- 16.7 COMPANY EVALUATION MATRIX: RAILWAY DATA DIODE KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING: START-UPS/SMES, 2025

- 16.8.5.1 Detailed list of key startups/SMEs

- 16.8.5.2 Competitive benchmarking of key startups/SMEs

- 16.9 COMPETITIVE SCENARIO AND TRENDS

- 16.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 16.9.2 DEALS

17 COMPANY PROFILE

- 17.1 KEY PLAYERS

- 17.1.1 BAE SYSTEMS

- 17.1.1.1 Business overview

- 17.1.1.2 Products/Solutions/Services offered

- 17.1.1.2.1 Deals

- 17.1.1.3 MnM View

- 17.1.1.3.1 Key strengths

- 17.1.1.3.2 Strategic choices

- 17.1.1.3.3 Weaknesses and competitive threats

- 17.1.2 ST ENGINEERING

- 17.1.2.1 Business overview

- 17.1.2.2 Products/Solutions/Services offered

- 17.1.2.3 MnM View

- 17.1.2.3.1 Key strengths

- 17.1.2.3.2 Strategic choices

- 17.1.2.3.3 Weaknesses and competitive threats

- 17.1.3 EVERFOX

- 17.1.3.1 Business overview

- 17.1.3.2 Products/Solutions/Services offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Deals

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses and competitive threats

- 17.1.4 OWL CYBER DEFENSE

- 17.1.4.1 Business overview

- 17.1.4.2 Products/Solutions/Services offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches/enhancements

- 17.1.4.3.2 Deals

- 17.1.4.4 MnM View

- 17.1.4.4.1 Key strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 INFODAS

- 17.1.5.1 Business overview

- 17.1.5.2 Products/Solutions/Services offered

- 17.1.5.3 MnM view

- 17.1.5.3.1 Key strengths

- 17.1.5.3.2 Strategic choices

- 17.1.5.3.3 Weaknesses and competitive threats

- 17.1.6 OPSWAT

- 17.1.6.1 Business overview

- 17.1.6.2 Products/Solutions/Services offered

- 17.1.6.2.1 Deals

- 17.1.7 ADVENICA

- 17.1.7.1 Business overview

- 17.1.7.2 Products/Solutions/Services offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches/enhancements

- 17.1.7.3.2 Deals

- 17.1.8 NEXOR

- 17.1.8.1 Business overview

- 17.1.8.2 Products/Solutions/Services offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Deals

- 17.1.9 FORCEPOINT

- 17.1.9.1 Business overview

- 17.1.9.2 Products/Solutions/Services offered

- 17.1.10 NAONWORKS

- 17.1.10.1 Business overview

- 17.1.10.2 Products/Solutions/Services offered

- 17.1.11 WATERFALL SECURITY SOLUTIONS

- 17.1.11.1 Business overview

- 17.1.11.2 Products/Solutions/Services offered

- 17.1.12 SIEMENS

- 17.1.12.1 Business overview

- 17.1.12.2 Products/Solutions/Services offered

- 17.1.1 BAE SYSTEMS

- 17.2 OTHER PLAYERS

- 17.2.1 GARLAND TECHNOLOGY

- 17.2.2 ARBIT

- 17.2.3 FIBERSYSTEM

- 17.2.4 VADO SECURITY TECHNOLOGIES

- 17.2.5 CHIPSPIRIT

- 17.2.6 SUNHILLO

- 17.2.7 MISSING LINK ELECTRONICS (MLE)

- 17.2.8 EXELE INFORMATION SYSTEMS

- 17.2.9 LINK22

- 17.2.10 4SECURE

- 17.2.11 STRATIGN

- 17.2.12 OAKDOOR

- 17.2.13 FEND INCORPORATED

- 17.2.14 GENUA

- 17.2.15 LEORY AUTOMATION

- 17.2.16 PATTON ELECTRONICS

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Breakup of primary profiles

- 18.1.2.2 Key industry insights

- 18.2 MARKET SIZE ESTIMATION

- 18.2.1 TOP-DOWN APPROACH

- 18.2.2 BOTTOM-UP APPROACH

- 18.3 DATA TRIANGULATION

- 18.4 MARKET FORECAST

- 18.5 RESEARCH ASSUMPTIONS

- 18.6 RESEARCH LIMITATIONS

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS