|

시장보고서

상품코드

2055590

진료 정보 교환(HIE) 시장 : 용도별, 구성요소별, 운영 모델별, 설정 유형별, 솔루션별, 유형별, 지역별 - 예측(-2031년)Healthcare Information Exchange (HIE) Market by Type (Direct, Query), Mode (Centralized, Decentralized), Setup (Private, Public), Solution (Portal, Platform), Application (Workflow, Interfacing), End User (Hospital, ASC) - Global Forecast to 2031 |

||||||

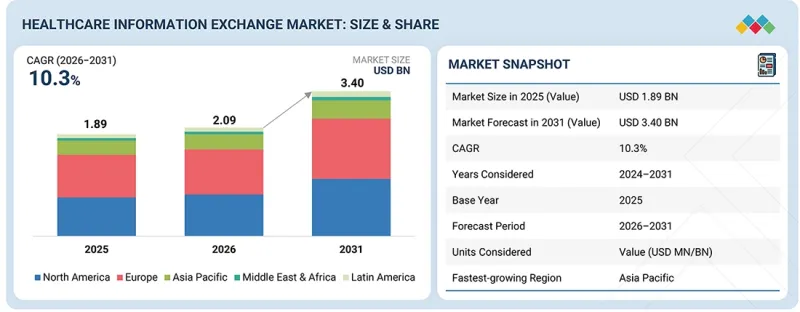

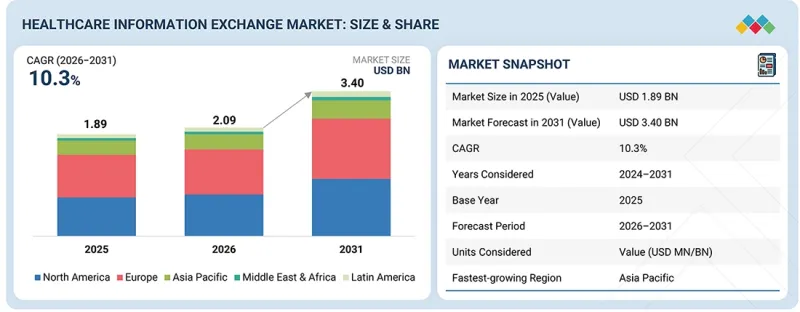

진료 정보 교환(HIE) 시장 규모는 2026년 20억 9,000만 달러에서 2031년까지 34억 달러에 이를 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 10.3%를 나타낼 전망입니다.

이 시장의 성장은 주로 의료 현장에서 환자의 건강 정보를 원활하게 공유하려는 수요에 힘입어 이루어지고 있습니다. 의료 서비스가 점점 더 세분화되고, 환자들이 여러 의료기관에서 진료를 받게 됨에 따라, 조율되고 일관성 있는 서비스에 대한 수요가 높아지고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 용도별, 구성요소별, 운영 모델별, 설정 유형별, 솔루션별, 유형별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

또한, 상호 운용성과 정보 교환을 촉진하기 위해 마련된 규제 정책, 정부의 이니셔티브 및 프로그램 역시 HIE 솔루션 도입에 기여하고 있습니다. 이러한 노력의 대표적인 사례로는 MACRA법이나 상호운용성 촉진 프로그램(구 명칭: Meaningful Use)을 들 수 있으며, 이들은 HIE 기능을 통합한 전자건강기록(EHR) 기술의 도입에 대해 인센티브를 제공합니다. 그러나 표준화된 데이터 형식의 부재와 호환되지 않는 시스템 간의 상호 운용성 문제로 인해 시장은 여러 과제에 직면해 있습니다.

“솔루션별로는 플랫폼 중심의 HIE 솔루션 부문이 예측 기간 동안 가장 높은 성장률을 보일 것으로 예측됩니다.” '

진료정보교환(HIE) 시장은 포털 중심형, 메시징 중심형, 플랫폼 중심형의 세 가지 부문으로 분류됩니다. 이 중 플랫폼 중심형 솔루션 부문이 가장 빠르게 성장할 것으로 예측됩니다. 이러한 성장은 의료 관계자들 사이에서 데이터 공유와 상호 운용성을 촉진하는 클라우드 기반 생태계에 대한 수요가 증가함에 따라 주도되고 있습니다. 플랫폼 중심형 솔루션은 데이터 교환, 분석, 용도를 통합한 플랫폼을 포함하며, 업무 효율과 의사 결정 능력을 모두 향상시킵니다. 이 분야의 기업으로 Veradigm을 예로 들 수 있습니다. 이 회사는 FHIR 표준을 활용해 상호 운용성을 촉진하고, 업계의 다양한 이해관계자간 실시간 데이터 교환을 가능하게 하는 데이터 플랫폼을 제공합니다.

“용도별로는 2025년에 웹 포털 개발 부문이 가장 큰 시장 점유율을 차지했습니다. '

진료 정보 교환 시장은 용도에 따라 웹 포털 개발, 워크플로 관리, 보안 메시징, 내부 인터페이스 및 기타 용도으로 분류됩니다. 웹 포털 개발 부문은 의료 종사자와 환자 모두에게 환자의 건강 데이터에 대한 편리한 접근성을 제공하는 데 중요한 역할을 수행하고 있어, 2025년에는 가장 큰 시장 점유율을 차지했습니다. 웹 포털은 검사 결과, 약물 프로파일 및 기타 건강 관련 정보를 포함한 본인의 건강 데이터에 접근하고, 공유하며, 정리할 수 있는 핵심 허브 역할을 합니다. 웹 포털 개발 분야의 성공에 기여하는 주요 요인은 모든 규모와 유형의 병원에서 널리 활용되고 있다는 점에 있습니다. 이러한 접근성을 통해 의사는 전자건강기록(EHR) 시스템, 검사 데이터, 영상진단 시스템 등 다양한 출처에서 환자의 건강 데이터를 신속하게 확보할 수 있게 됩니다.

“최종 사용자별로는 예측 기간 동안 의료 제공업체 부문이 진료 정보 교환 시장에서 가장 높은 성장률을 보일 것으로 예측됩니다. '

진료정보교환(HIE) 시장은 최종 사용자별로 의료 제공업체, 의료 보험자, 약국이라는 3가지 범주로 분류됩니다. 의료 제공업체 부문은 의료 서비스 제공 및 환자 의료 기록 관리에서 매우 중요한 역할을 담당하고 있어 가장 빠른 성장세를 보이고 있습니다. 미국에서는 의료 제공업체들이 진료 연계성을 강화하고 규정 준수를 확보하기 위해 HIE 솔루션 도입에 점점 더 주력하고 있습니다. 예를 들어, 2023년 6월, 저명한 의료 기관인 메이요 클리닉은 마이크로소프트와의 전략적 제휴를 발표하고 ‘Azure Health Data Services’ 플랫폼을 출시했습니다. 이 플랫폼에는 HIE 기능이 탑재되어 있어, 조직 내 시설 간 원활한 데이터 교환을 가능하게 합니다.

“아시아태평양은 예측 기간 동안 가장 높은 연평균 성장률(CAGR)을 보일 것으로 추정됩니다. '

본 보고서에서는 진료 정보 교환(HIE) 시장을 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카으로 분류하고 있습니다. 아시아태평양의 HIE 시장은 예측 기간 동안 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 이러한 성장은 주로 디지털화의 진전, 도시화, 의료비 증가 등의 특징을 보이는 APAC 지역의 의료 환경에서 일어난 큰 변화 덕분입니다. 서비스 향상을 위해 기술 혁신을 도입하는 의료 기관이 늘어남에 따라, 데이터 교환과 상호 운용성의 필요성이 점점 더 분명해지고 있습니다. 또한, 의료 분야의 IT 솔루션과 상호 운용성 활용을 촉진하기 위한 정부의 정책과 프로그램이 APAC 지역의 HIE 시장을 더욱 견인하고 있습니다. 중국, 일본, 한국, 호주 등의 국가들은 국가 차원의 의료 IT 전략 및 상호운용성 기준 수립을 통해 e-헬스 기술 도입을 촉진함으로써 이러한 흐름을 주도하고 있습니다. 이러한 노력은 의료기관 간 전자건강기록(EHR) 및 기타 중요한 의료 정보의 교환을 촉진합니다. 주목할 만한 사례로는 중국의 ‘건강중국 2030’ 이니셔티브나 호주의 ‘My Health Record’ 프로그램 등을 들 수 있습니다.

본 보고서에서 다룬 기업 프로파일 목록

- Epic Systems Corporation(미국)

- Oracle(미국)

- InterSystems Corporation(미국)

- Veradigm LLC(미국)

- Medical Information Technology, Inc.(미국)

- Health Catalyst(미국)

- Chetu Inc.(미국)

- Meditab(미국)

- 지멘스 헬시니어스(독일)

- Deloitte(영국)

- Dreamsoft4u(미국)

- NCrypted Technologies(인도)

- Glorium Technologies(미국)

- Daffodil Unthinkable Software Corporation(미국)

- eClinicalWorks(미국)

- NXGN Management, LLC(미국)

- Orion Health(뉴질랜드)

- Kellton(인도)

- Telstra Health(호주)

- CGI Inc.(캐나다)

- Excelicare(미국)

- Octal IT Solution(미국)

- Andersen(폴란드)

- SISGAIN(인도)

- Cleverdev Software(미국)

- OSP Labs(미국)

조사 범위

본 보고서에서는 유형, 도입 형태, 구현 모델, 솔루션, 구성 요소, 용도, 최종 사용자, 지역 등 다양한 요인을 바탕으로 진료 정보 교환 시장을 분석했습니다. 시장의 성장에 영향을 미치는 촉진요인, 기회 및 과제에 대해 분석했습니다. 또한, 이해관계자들에게 주어진 기회와 과제를 평가하고, 시장 선도 기업경쟁 구도에 대해 상세하게 설명하고 있습니다. 본 조사에서는 미시적 시장 또한 그 성장 동향, 전망 및 진료 정보 교환 시장 전체에 대한 기여도에 초점을 맞추어 분석했습니다. 또한, 5개 주요 지역 시장 세분화에 따른 매출 전망도 제공합니다.

이 보고서를 구매해야 하는 이유

본 보고서에는 다음 내용도 포함되어 있습니다.

- 주요 촉진요인(EHR/EMR 솔루션 도입 확대, 환자 중심 의료 제공에 대한 관심 증가, 급증하는 의료비 억제 필요성, 환자 치료 및 안전성 향상을 위한 정부의 이니셔티브 및 규제, 정부 및 민간 기관의 투자 증가), 제약 요인(인프라 개발에 대한 막대한 투자 필요성과 높은 도입 비용, 진정한 상호 운용성 솔루션의 부재, 구식 레거시 시스템의 사용), 기회(신흥 시장의 의료 인프라 개선, 실시간 데이터 교환을 위한 소프트웨어 기술의 발전), 과제(의료 업계의 환자 데이터 보안 및 개인정보 보호에 대한 우려, 일관성 없는 데이터로 인한 복잡성 증가, 숙련된 의료 IT 전문가 부족)가 진료 정보 교환 시장의 성장에 기여하고 있습니다.

- 제품 개발 및 혁신 : 진료 정보 교환 시장의 향후 동향, 연구 개발 활동, 그리고 신규 소프트웨어 출시에 대한 상세한 분석.

- 시장 개발: 수익성이 높은 신흥 시장, 구성 요소, 용도, 최종 사용자 및 지역에 대한 종합적인 정보.

- 시장의 다각화 : 진료 정보 교환 시장의 소프트웨어 포트폴리오, 성장 지역, 최근 동향 및 투자에 관한 종합적인 정보.

- 경쟁사 분석 : 전 세계 진료 정보 교환 시장의 주요 기업별 시장 점유율, 성장 전략, 제품 라인업, 기업 평가 쿼드런트 및 역량에 대한 상세한 분석.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황

제8장 고객 현황과 구매 행동

제9장 진료 정보 교환 시장(용도별)

제10장 진료 정보 교환 시장(구성요소별)

제11장 진료 정보 교환 시장(운영 모델별)

제12장 진료 정보 교환 시장(설정 유형별)

제13장 진료 정보 교환 시장(솔루션별)

제14장 진료 정보 교환 시장(유형별)

제15장 진료 정보 교환 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

LSH 26.06.19The healthcare information exchange (HIE) market is projected to reach USD 3.40 billion by 2031 from USD 2.09 billion in 2026, at a CAGR of 10.3% from 2026 to 2031. This market expansion is primarily driven by the need for seamless exchanges of patient health information within the healthcare environment. As healthcare delivery becomes increasingly fragmented, with patients seeking medical attention from multiple providers, there is a growing demand for coordinated and consistent services.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Type, Setup Type, Implementation Model, Solution, Component, Application, and End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Additionally, regulatory policies, government initiatives, and programs designed to promote interoperability and information exchange have contributed to the adoption of HIE solutions. Notable examples of these initiatives include the MACRA legislation and the Promoting Interoperability program (formerly known as Meaningful Use), which offer incentives for adopting electronic health record (EHR) technologies that incorporate HIE capabilities. However, the market faces challenges due to the lack of standardized data formats and interoperability between incompatible systems.

"By solution, the platform-centric HIE solutions segment is expected to witness the highest growth during the forecast period."

The health information exchange (HIE) market is divided into three segments: portal-centric, messaging-centric, and platform-centric. Among these, the platform-centric solutions segment is expected to grow the fastest. This growth is driven by an increasing need for cloud-enabled ecosystems that facilitate data sharing and interoperability among healthcare stakeholders. Platform-centric solutions encompass integrated platforms that combine data exchange, analytics, and applications, enhancing both operational efficiency and decision-making. One example of a company in this space is Veradigm, which offers data platforms that promote interoperability using FHIR standards and enable real-time data exchange among various industry stakeholders.

"By application, the web portal development segment held the largest market share in 2025."

The health information exchange market is segmented based on application into web portal development, workflow management, secure messaging, internal interfacing, and other applications. The web portal development segment held the largest market share in 2025 due to its crucial role in providing easy access to patient health data for both medical professionals and patients. Web portals serve as central hubs where users can access, share, and organize their health data, including test results, drug profiles, and other health-related information. A key factor contributing to the success of the web portal development category is its widespread use by hospitals of all sizes and types. This accessibility allows doctors to quickly obtain patient health data from various sources, including electronic health record (EHR) systems, lab data, and imaging systems.

"By end user, the healthcare providers segment is expected to register the highest growth in the health information exchange market during the forecast period."

The health information exchange (HIE) market is segmented by end user into three categories: healthcare providers, healthcare payers, and pharmacies. The healthcare providers segment is experiencing the fastest growth due to its vital role in delivering care and managing patient medical records. In the US, healthcare providers are increasingly focusing on implementing HIE solutions to enhance care coordination and ensure regulatory compliance. For example, in June 2023, the prominent healthcare provider, Mayo Clinic, announced a strategic alliance with Microsoft to launch the Azure Health Data Services platform. This platform is equipped with HIE functionality, enabling seamless data exchange across the organization's facilities.

"The APAC is estimated to register the highest CAGR during the forecast period."

This report segments the healthcare information exchange (HIE) market into several regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The HIE market in the Asia Pacific (APAC) region is projected to experience the highest compound annual growth rate (CAGR) during the forecast period. This growth is largely due to significant transformations in the APAC healthcare landscape, characterized by increased digitization, urbanization, and higher healthcare spending. As more healthcare organizations adopt technological innovations to enhance their services, the necessity for data exchange and interoperability is becoming more evident. Additionally, government policies and programs aimed at promoting the use of IT solutions and interoperability in the healthcare sector are further driving the HIE market in the APAC region. Countries such as China, Japan, South Korea, and Australia are leading the charge by encouraging the adoption of e-health technologies through the establishment of national health IT strategies and interoperability standards. These initiatives facilitate the exchange of electronic health records (EHRs) and other critical health information among healthcare institutions. Noteworthy examples include China's Healthy China 2030 initiative and Australia's My Health Record program.

Breakdown of Supply-side Primary Interviews, by Company Type, Designation, and Region:

- By Company Type: Tier 1 (40%), Tier 2 (35%), and Tier 3 (25%)

- By Designation: C-level Executives (35%), Directors (45%), and Others (20%)

- By Region: North America (55%), Europe (20%), Asia Pacific (15%), Latin America (5%), and the Middle East & Africa (5%)

List of Companies Profiled in the Report

- Epic Systems Corporation (US)

- Oracle (US)

- InterSystems Corporation (US)

- Veradigm LLC (US)

- Medical Information Technology, Inc. (US)

- Health Catalyst (US)

- Chetu Inc. (US)

- Meditab (US)

- Siemens Healthineers (Germany)

- Deloitte (UK)

- Dreamsoft4u (US)

- NCrypted Technologies. (India)

- Glorium Technologies (US)

- Daffodil Unthinkable Software Corporation (US)

- eClinicalWorks (US)

- NXGN Management, LLC (US)

- Orion Health (New Zealand)

- Kellton (India)

- Telstra Health (Australia)

- CGI Inc. (Canada)

- Excelicare (US)

- Octal IT Solution (US)

- Andersen (Poland)

- SISGAIN (India)

- Cleverdev Software (US)

- OSP Labs (US)

Research Coverage

This report analyzes the healthcare information exchange market based on various factors, including type, setup type, implementation model, solution, component, application, end user, and region. It examines the drivers, opportunities, and challenges that influence market growth. Additionally, the report assesses the opportunities and challenges for stakeholders and details the competitive landscape for market leaders. The study also explores micro markets, focusing on their growth trends, prospects, and contributions to the overall health information exchange market. Furthermore, it provides revenue forecasts for the market segments across five major regions.

Reasons to Buy the Report

This report also includes.

- Analysis of key drivers (rising adoption of EHR/EMR solutions, growing focus on patient-centric care delivery, need to curtail escalating healthcare costs, government initiatives and regulations to enhance patient care and safety, and rising investments from government and private institutions), restraints (need for significant investments in infrastructure development and high cost of deployment, lack of true interoperability solutions, and use of outdated legacy systems), opportunities (improving healthcare infrastructure in emerging markets and advancements in software technology for real-time data exchange), and challenges (patient data security and privacy concerns in the healthcare industry, increasing complexity due to lack of consistent data, and shortage of skilled healthcare IT professionals) are contributing the growth of the healthcare information exchange market.

- Product Development/Innovation: Detailed insights on upcoming trends, research & development activities, and new software launches in the healthcare information exchange market.

- Market Development: Comprehensive information on the lucrative emerging markets, components, applications, end users, and regions.

- Market Diversification: Exhaustive information about the software portfolios, growing geographies, recent developments, and investments in the healthcare information exchange market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, company evaluation quadrant, and capabilities of leading players in the global healthcare information exchange market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS OF STUDY

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING HEALTHCARE INFORMATION EXCHANGE MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR HEALTHCARE INFORMATION EXCHANGE MARKET

- 3.2 NORTH AMERICA HEALTH INFORMATION EXCHANGE MARKET, BY END USER AND COUNTRY

- 3.3 HEALTHCARE INFORMATION EXCHANGE MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising adoption of EHR/EMR solutions

- 4.2.1.2 Growing focus on patient-centric care delivery

- 4.2.1.3 Need to curtail escalating healthcare costs

- 4.2.1.4 Government initiatives and regulations to enhance patient care & safety

- 4.2.1.5 Rising investments from government & private institutes

- 4.2.2 RESTRAINTS

- 4.2.2.1 Need for significant investments in infrastructure development and high cost of deployment

- 4.2.2.2 Lack of true interoperability solutions

- 4.2.2.3 Use of outdated legacy systems

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Improving healthcare infrastructure in emerging markets

- 4.2.3.2 Advancements in software technology for real-time data exchange

- 4.2.4 CHALLENGES

- 4.2.4.1 Patient data security and privacy concerns in healthcare industry

- 4.2.4.2 Increasing complexity due to lack of consistent data

- 4.2.4.3 Shortage of skilled healthcare IT professionals

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS (MODERATE)

- 5.1.2 BARGAINING POWER OF BUYERS (HIGH)

- 5.1.3 THREAT OF SUBSTITUTES (LOW TO MODERATE)

- 5.1.4 THREAT OF NEW ENTRANTS (MODERATE)

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY (HIGH)

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 GDP TRENDS AND FORECAST

- 5.2.2 TRENDS IN GLOBAL HEALTHCARE IT INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICING ANALYSIS OF KEY PLAYERS, BY TYPE, 2025

- 5.5.2 INDICATIVE PRICING ANALYSIS, BY REGION, 2025

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 INTEROPERABILITY SOLUTIONS TO LEVERAGE CLINICAL WORKFLOWS

- 5.9.2 SHARING CLINICAL INFORMATION TO SET FOUNDATION OF EFFICIENT AND EFFECTIVE HEALTHCARE DELIVERY

- 5.9.3 SUPPORTING HEALTH INFORMATION EXCHANGE ACCESS

- 5.10 IMPACT OF 2025 US TARIFF

- 5.10.1 KEY TARIFF RATES

- 5.10.2 PRICE IMPACT ANALYSIS

- 5.10.3 IMPACT ON COUNTRY/REGION

- 5.10.3.1 US

- 5.10.3.2 Europe

- 5.10.3.3 Asia Pacific

- 5.10.4 IMPACT ON END-USE INDUSTRY

- 5.10.4.1 Healthcare Providers

- 5.10.4.2 Healthcare Payers

- 5.10.4.3 Pharmacies

- 5.10.4.4 Laboratories

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ARTIFICIAL INTELLIGENCE AND MACHINE LEARNING

- 6.1.2 BLOCKCHAIN

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 INTERNET OF THINGS

- 6.2.2 DATA ANALYTICS AND BUSINESS INTELLIGENCE TOOLS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 CLOUD COMPUTING

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 PATENT PUBLICATION TRENDS FOR THE HEALTHCARE INFORMATION EXCHANGE MARKET

- 6.5.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-DRIVEN PREDICTIVE CARE COORDINATION AND DECISION SUPPORT

- 6.6.2 UNIFIED LONGITUDINAL PATIENT RECORDS AND CONSUMER ACCESS

- 6.6.3 REAL-TIME PUBLIC HEALTH SURVEILLANCE AND EMERGENCY RESPONSE

- 6.6.4 BLOCKCHAIN-ENABLED TRUSTED DATA EXCHANGE

- 6.6.5 VALUE-BASED CARE, PAYER INTEGRATION, AND REVENUE OPTIMIZATION

- 6.6.6 INTEGRATION WITH REMOTE MONITORING, GENOMICS, AND PRECISION MEDICINE

- 6.7 IMPACT OF AI/GEN AI

- 6.7.1 MARKET POTENTIAL OF AI/GEN AI

- 6.7.2 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION

- 6.7.2.1 AI-Driven Clinical Summarization and Interoperability Intelligence at InterSystems HealthShare

- 6.7.3 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 6.7.3.1 Healthcare data analytics and AI-driven interoperability platforms

- 6.7.3.2 Digital health platforms, integration, and regulatory infrastructure

- 6.7.3.3 Clinical care, payer operations, and personalized healthcare delivery

- 6.7.4 USER READINESS AND IMPACT ASSESSMENT

- 6.7.4.1 User readiness

- 6.7.4.1.1 User A: Healthcare Providers (Hospitals, Clinics, Long-Term Care Centers, Other Providers)

- 6.7.4.1.2 User B: Healthcare Payers

- 6.7.4.2 Impact assessment

- 6.7.4.2.1 User A: Healthcare Providers

- 6.7.4.2.1.1 Implementation

- 6.7.4.2.1.2 Impact

- 6.7.4.2.2 User B: Healthcare Payers

- 6.7.4.2.2.1 Implementation

- 6.7.4.2.2.2 Impact

- 6.7.4.2.1 User A: Healthcare Providers

- 6.7.4.1 User readiness

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM END-USE INDUSTRIES

- 8.4.1 UNMET NEEDS

- 8.4.2 END-USER EXPECTATIONS

- 8.5 MARKET PROFITABILITY

9 HEALTH INFORMATION EXCHANGE MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 WEB PORTAL DEVELOPMENT

- 9.2.1 LARGE NUMBER OF PHYSICIANS OPTING FOR ELECTRONIC MEDICAL RECORDS TO DRIVE MARKET

- 9.3 WORKFLOW MANAGEMENT

- 9.3.1 BETTER DECISION-MAKING FOR ENHANCED PATIENT CARE TO PROPEL MARKET

- 9.4 SECURE MESSAGING

- 9.4.1 ABILITY TO PROVIDE SECURE COMMUNICATION WITHIN AND OUTSIDE CARE NETWORK TO SUPPORT MARKET GROWTH

- 9.5 INTERNAL INTERFACING

- 9.5.1 FASTEST-GROWING APPLICATION SEGMENT DURING FORECAST PERIOD

- 9.6 TRANSACTION MONITORING

- 9.6.1 SECURE, EFFICIENT, AND COMPLIANT EXCHANGE OF HEALTH DATA-KEY FACTORS DRIVING MARKET GROWTH

10 HEALTH INFORMATION EXCHANGE MARKET, BY COMPONENT

- 10.1 INTRODUCTION

- 10.2 CLINICAL DATA REPOSITORY

- 10.2.1 EASY ACCESS TO DATA ACROSS EMR DOMAIN TO SUPPORT MARKET GROWTH

- 10.3 ENTERPRISE MASTER PERSON INDEX

- 10.3.1 EMPI TO DOMINATE HIE MARKET DURING FORECAST PERIOD

- 10.4 RECORD LOCATOR SERVICE

- 10.4.1 RLS TO REGISTER HIGHEST GROWTH RATE

- 10.5 HEALTHCARE PROVIDER DIRECTORY

- 10.5.1 COMPREHENSIVE DATABASE AND RELIABILITY OF HPD TO DRIVE MARKET

11 HEALTH INFORMATION EXCHANGE MARKET, BY IMPLEMENTATION MODEL

- 11.1 INTRODUCTION

- 11.2 HYBRID MODEL

- 11.2.1 HYBRID HIE MODELS TO HOLD LARGEST MARKET SHARE

- 11.3 CENTRALIZED MODEL

- 11.3.1 PRIVACY AND SECURITY CONCERNS TO HINDER ADOPTION OF CENTRALIZED HIE

- 11.4 DECENTRALIZED/FEDERATED

- 11.4.1 REAL-TIME UPDATED DATA AVAILABILITY AND INCREASED SECURITY TO DRIVE ADOPTION

12 HEALTH INFORMATION EXCHANGE MARKET, BY SETUP TYPE

- 12.1 INTRODUCTION

- 12.2 PRIVATE

- 12.2.1 RISING MANDATES FOR INCENTIVE PROGRAMS TO DRIVE MARKET

- 12.3 PUBLIC

- 12.3.1 GROWING GOVERNMENT FUNDING TO SUPPORT MARKET GROWTH

13 HEALTH INFORMATION EXCHANGE MARKET, BY SOLUTION

- 13.1 INTRODUCTION

- 13.2 PORTAL-CENTRIC HIE SOLUTIONS

- 13.2.1 PORTAL-CENTRIC SOLUTIONS TO DOMINATE HEALTH INFORMATION EXCHANGE MARKET DURING FORECAST PERIOD

- 13.3 MESSAGING-CENTRIC HIE SOLUTIONS

- 13.3.1 HIGH PERFORMANCE AND RELIABILITY OF MESSAGING-CENTRIC SOLUTIONS TO DRIVE MARKET

- 13.4 PLATFORM-CENTRIC HIE SOLUTIONS

- 13.4.1 PLATFORM-CENTRIC SOLUTIONS TO REGISTER HIGHEST GROWTH RATE DURING FORECAST PERIOD

14 HEALTH INFORMATION EXCHANGE MARKET, BY TYPE

- 14.1 INTRODUCTION

- 14.2 DIRECTED EXCHANGE

- 14.2.1 DIRECTED EXCHANGE SEGMENT TO COMMAND LARGEST SHARE OF HEALTH INFORMATION EXCHANGE MARKET

- 14.3 QUERY-BASED EXCHANGE

- 14.3.1 QUERY-BASED EXCHANGE SEGMENT TO REGISTER HIGHEST GROWTH RATE DURING FORECAST PERIOD

- 14.4 CONSUMER-MEDIATED EXCHANGE

- 14.4.1 GROWING PATIENT-PHYSICIAN INTERACTION TO DRIVE POPULARITY OF CONSUMER-MEDIATED SOLUTIONS

15 HEALTH INFORMATION EXCHANGE MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 15.2.2 US

- 15.2.2.1 Layered interoperability and stringent certification requirements to drive market

- 15.2.3 CANADA

- 15.2.3.1 Government initiatives to support HIE adoption in Canada

- 15.3 EUROPE

- 15.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 15.3.2 GERMANY

- 15.3.2.1 Landmark Health Data Use Act and EHDS alignment catalyze research-grade HIE platforms

- 15.3.3 UK

- 15.3.3.1 Growing patient volumes to drive market

- 15.3.4 FRANCE

- 15.3.4.1 Favorable government initiatives to drive market

- 15.3.5 ITALY

- 15.3.5.1 PNRR-funded FSE 2.0 drives national interoperability and cross-regional HIE unification

- 15.3.6 SPAIN

- 15.3.6.1 Cross-regional HIE scale-up and national AI strategy cement digital health leadership

- 15.3.7 REST OF EUROPE

- 15.4 ASIA PACIFIC

- 15.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 15.4.2 JAPAN

- 15.4.2.1 Growing need to digitize patient records to drive market

- 15.4.3 CHINA

- 15.4.3.1 Large patient population and healthcare infrastructure improvements to drive market

- 15.4.4 INDIA

- 15.4.4.1 Rising need for cost-effective technologies to drive HCIT integration in India

- 15.4.5 REST OF ASIA PACIFIC

- 15.5 LATIN AMERICA

- 15.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 15.5.2 BRAZIL

- 15.5.2.1 RNDS formalized as national interoperability backbone with 2.8 billion clinical records

- 15.5.3 MEXICO

- 15.5.3.1 openEHR Adoption and IMSS digital health modernization drive national HIE platform investment

- 15.5.4 REST OF LATIN AMERICA

- 15.6 MIDDLE EAST & AFRICA

- 15.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 15.6.2 GCC COUNTRIES

- 15.6.2.1 Growing focus on implementing HCIT to drive market

- 15.6.3 REST OF MIDDLE EAST & AFRICA

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2026

- 16.3 REVENUE ANALYSIS, 2021-2025

- 16.4 MARKET SHARE ANALYSIS, 2025

- 16.5 BRAND/SOFTWARE COMPARISON

- 16.6 COMPANY VALUATION & FINANCIAL METRICS

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Setup type footprint

- 16.7.5.4 End user footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 EPIC SYSTEMS CORPORATION.

- 17.1.1.1 Business overview

- 17.1.1.2 Products and Services offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches and approvals

- 17.1.1.3.2 Deals

- 17.1.1.4 MnM view

- 17.1.1.4.1 Right to win

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 ORACLE

- 17.1.2.1 Business overview

- 17.1.2.2 Products and services offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches and approvals

- 17.1.2.3.2 Deals

- 17.1.2.4 MnM view

- 17.1.2.4.1 Right to win

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 INTERSYSTEMS CORPORATION

- 17.1.3.1 Business overview

- 17.1.3.2 Products and services offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches and approvals

- 17.1.3.3.2 Deals

- 17.1.3.4 MnM view

- 17.1.3.4.1 Right to win

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses and competitive threats

- 17.1.4 VERADIGM LLC

- 17.1.4.1 Business overview

- 17.1.4.2 Products and services offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches and approvals

- 17.1.4.3.2 Deals

- 17.1.4.4 MnM view

- 17.1.4.4.1 Right to win

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 MEDICAL INFORMATION TECHNOLOGY, INC.

- 17.1.5.1 Business overview

- 17.1.5.2 Products and services offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product launches and approvals

- 17.1.5.3.2 Deals

- 17.1.5.4 MnM view

- 17.1.5.4.1 Right to win

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses and competitive threats

- 17.1.6 HEALTH CATALYST

- 17.1.6.1 Business overview

- 17.1.6.2 Products and services offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Deals

- 17.1.7 KELLTON

- 17.1.7.1 Business overview

- 17.1.7.2 Products and services offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Deal

- 17.1.8 ECLINICALWORKS

- 17.1.8.1 Business overview

- 17.1.8.2 Products and services offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches and approvals

- 17.1.8.3.2 Deal

- 17.1.9 NXGN MANAGEMENT, LLC.

- 17.1.9.1 Business overview

- 17.1.9.2 Products and services offered

- 17.1.10 ORION HEALTH GROUP OF COMPANIES

- 17.1.10.1 Business overview

- 17.1.10.2 Products and services offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Deal

- 17.1.11 CHETU INC.

- 17.1.11.1 Business overview

- 17.1.11.2 Products and services offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Deal

- 17.1.12 TELSTRA HEALTH (A SUBSIDIARY OF TELSTRA CORPORATION LTD.)

- 17.1.12.1 Business overview

- 17.1.12.2 Products and services offered

- 17.1.12.2.1 Deal

- 17.1.13 CGI INC.

- 17.1.13.1 Business overview

- 17.1.13.2 Products and services offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Product launches and approvals

- 17.1.13.3.2 Deal

- 17.1.14 MEDITAB

- 17.1.14.1 Business overview

- 17.1.14.2 Products and services offered

- 17.1.15 DREAMSOFT4U

- 17.1.15.1 Business overview

- 17.1.15.2 Products and services offered

- 17.1.16 NCRYPTED TECHNOLOGIES

- 17.1.16.1 Business overview

- 17.1.16.2 Products and services offered

- 17.1.17 GLORIUM TECHNOLOGIES

- 17.1.17.1 Business overview

- 17.1.17.2 Products and services offered

- 17.1.18 DAFFODIL UNTHINKABLE SOFTWARE CORP.

- 17.1.18.1 Business overview

- 17.1.18.2 Products and services offered

- 17.1.19 SIEMENS HEALTHINEERS AG

- 17.1.19.1 Business overview

- 17.1.19.2 Products and services offered

- 17.1.19.2.1 Product launches and approvals

- 17.1.20 DELOITTE

- 17.1.20.1 Business overview

- 17.1.20.2 Products and services offered

- 17.1.20.3 Recent developments

- 17.1.20.3.1 Deals

- 17.1.21 EXCELICARE

- 17.1.21.1 Business overview

- 17.1.21.2 Products and services offered

- 17.1.1 EPIC SYSTEMS CORPORATION.

- 17.2 OTHER PLAYERS

- 17.2.1 OCTAL IT SOLUTION

- 17.2.2 ANDERSEN INC.

- 17.2.3 SISGAIN

- 17.2.4 CLEVERDEV SOFTWARE

- 17.2.5 OSP LABS

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Key data from primary sources

- 18.1.2.2 Breakdown of primaries

- 18.1.2.3 Insights from primary experts

- 18.1.1 SECONDARY DATA

- 18.2 RESEARCH METHODOLOGY DESIGN

- 18.3 MARKET SIZE ESTIMATION

- 18.4 MARKET BREAKDOWN DATA TRIANGULATION

- 18.5 MARKET SHARE ESTIMATION

- 18.6 STUDY ASSUMPTIONS

- 18.7 RESEARCH LIMITATIONS

- 18.7.1 METHODOLOGY-RELATED LIMITATIONS

- 18.8 RISK ASSESSMENT

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS