|

시장보고서

상품코드

2055591

감암성 접착제 시장(-2031년) : 기술, 화학 조성, 용도, 최종사용자 산업, 지역별Pressure Sensitive Adhesives Market by Technology (Water-based, Solvent-based), Chemistry (Acrylic PSA, Silicone PSA), Application (Tapes, Labels), End-use Industry (Packaging, Medical & Healthcare), and Region - Global Forecast to 2031 |

||||||

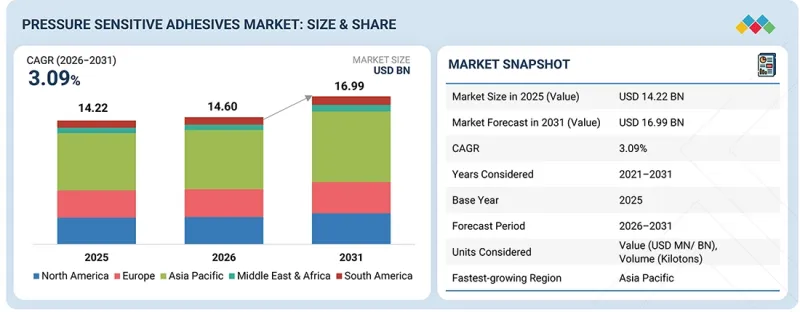

감암성 접착제 시장 규모는 2026년에 146억 달러로 추정되며, 2026-2031년 CAGR 3.09%로 성장을 지속하여, 2031년에는 169억 9,000만 달러에 이를 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러), 킬로톤 |

| 부문 | 기술, 화학 조성, 용도, 최종사용자 산업, 지역 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 중동 및 아프리카, 남미 |

“환경 규제 강화와 지속 가능한 포장 동향이 감암성 접착제 시장의 성장을 가속화할 것으로 전망됩니다.” '

세계 정부와 규제 기관의 환경 규제 및 지속가능성 노력에 대한 관심이 높아짐에 따라, 다양한 산업 분야에서 감암성 접착제(PSA)에 대한 수요가 증가하고 있습니다. 제조업체들은 휘발성 유기 화합물(VOC) 배출 감축, 재활용성 향상, 성능을 저하시키지 않으면서도 친환경적인 제품을 개발해야 한다는 압박을 점점 더 강하게 받고 있습니다. 이에 따라 환경에 미치는 영향이 적고 작업 안전성도 향상되는 특히 수성 및 무용제 방식의 첨단 PSA 기술 도입이 촉진되고 있습니다. 또한, 포장, 자동차, 의료, 전자 등 다양한 산업 분야에서는 장기적인 지속가능성 목표를 달성하기 위해 가볍고 지속가능하며 에너지 효율이 높은 소재가 점점 더 중요시되고 있습니다. 규제 준수 및 환경 친화적인 제조 관행의 중요성이 커짐에 따라, 전 세계적으로 감암성 접착제의 사용이 확대되고 있으며, 이에 따라 시장 성장이 가속화될 것으로 예측됩니다.

“수계 기술은 감암성 접착제 시장에서 수량 기준 두 번째로 높은 성장률을 보일 것으로 예측됩니다. '

기술별로 보면, 환경 의식의 고조와 용제 배출에 관한 규제 강화로 인해 수성 감암성 접착제 수요는 수량 기준으로 두 번째로 빠른 속도로 성장할 것으로 예측됩니다. 이러한 접착제는 VOC 배출량이 적어 작업장의 안전성을 높이고 비용 효율적인 가공이 가능하기 때문에 포장, 라벨, 종이, 위생용품 등의 용도에 매우 적합합니다. 포장 및 소비재 제조업체들의 지속 가능한 접착 기술에 대한 수요가 증가함에 따라, 해당 기술의 도입이 더욱 가속화되고 있습니다. 또한, 수성 접착제 배합 기술의 지속적인 발전으로 인해 다양한 산업 분야에서 접착 강도와 성능이 향상되고 있습니다.

“고무 PSA는 수량 기준으로 감암성 접착제 시장에서 2위를 차지하는 화학 부문입니다. '

화학 성분별로 보면, 고무 PSA 부문은 강력한 초기 접착력, 유연성, 높은 비용 효율성 덕분에 수량 기준 시장 점유율 2위를 차지할 것으로 추정됩니다. 고무 감암성 접착제는 마스킹 테이프, 포장용 테이프, 라벨 등 신속한 접착과 높은 신뢰성이 필수적인 범용 산업 분야에서 널리 사용되고 있습니다. 요철이 있는 표면에 접착하기에 적합하고 다양한 기질과의 호환성이 뛰어나다는 점은 포장 및 건설 분야 수요를 지속적으로 뒷받침하고 있습니다. 또한, 산업 활동의 활성화와 소비재 소비 확대가 전 세계적으로 고무 PSA의 용도를 꾸준히 확대시키는 요인이 되고 있습니다.

“전기 및 전자·통신 업계는 수량 기준으로 두 번째로 높은 성장률을 보일 것으로 전망됩니다. '

용도별로 보면, 전기 및 전자·통신 부문은 전자기기, 스마트 기술, 첨단 통신 인프라에 대한 수요 증가로 인해 수량 기준 두 번째로 높은 성장률을 보일 것으로 예측됩니다. PSA는 가벼운 무게와 뛰어난 성능 덕분에 전자기기 조립, 디스플레이 접착, 절연, 회로 보호, 와이어 하네스 등 다양한 분야에서 널리 사용되고 있습니다. 소비자용 전자기기 제조의 급속한 확대, 전기차의 보급 확대, 5G 인프라에 대한 투자 증가가 이 분야 전반에 걸친 고성능 감암성 접착제 솔루션에 대한 수요를 더욱 촉진하고 있습니다.

“중동 및 아프리카은 수량 기준으로 두 번째로 높은 성장률을 보일 것으로 전망됩니다. '

중동 및 아프리카은 신흥국의 산업화 진전, 인프라 개발, 포장 수요 증가에 힘입어 수량 기준 두 번째로 높은 성장률을 보일 것으로 예측됩니다. 건설 활동의 확대, 포장 소비재 소비 증가, 의료 인프라의 개선이 테이프, 라벨, 특수 용도 분야의 PSA 채택을 촉진하고 있습니다. 또한, 물류 및 소매 부문의 성장에 더해 제조업에 대한 투자 증가가 해당 지역 전체의 감암성 접착제 제품 소비 확대를 뒷받침하고 있습니다.

본 보고서에서는 전 세계 감암성 접착제 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류 및 지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 프로파일 등을 종합적으로 다루고 있습니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI 도입 전략적 파괴적 변화

제7장 지속가능성과 규제 상황

제8장 고객 현황과 구매 행동

제9장 감암성 접착제 시장 : 화학 조성별

제10장 감암성 접착제 시장 : 기술별

제11장 감암성 접착제 시장 : 용도별

제12장 감암성 접착제 시장 : 최종사용자 산업별

제13장 감암성 접착제 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

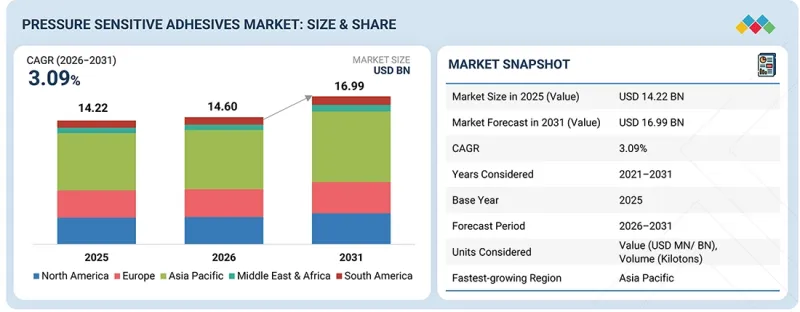

LSHThe pressure sensitive adhesives market is estimated to be USD 14.60 billion in 2026 and is projected to reach USD 16.99 billion by 2031, at a CAGR of 3.09% between 2026 and 2031.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million/Billion), Volume (Kilotons) |

| Segments | Technology, Chemistry, Application, End-use Industry, and Region |

| Regions covered | Asia Pacific, Europe, North America, Middle East & Africa, and South America |

"Increasing environmental regulations and sustainable packaging trends to accelerate the growth of the pressure sensitive adhesives market."

The demand for pressure-sensitive adhesives (PSAs) across multiple industries is being driven by the increasing focus on environmental regulations and sustainability initiatives implemented by governments and regulatory bodies worldwide. Manufacturers are under growing pressure to reduce volatile organic compound (VOC) emissions, improve recyclability, and develop environmentally friendly products without compromising performance. This has encouraged the adoption of advanced PSA technologies, particularly water-based and solvent-free formulations, which offer lower environmental impact and improved operational safety. In addition, industries such as packaging, automotive, healthcare, and electronics are increasingly emphasizing lightweight, sustainable, and energy-efficient materials to achieve their long-term sustainability goals. The rising importance of regulatory compliance and eco-friendly manufacturing practices is expected to strengthen the adoption of pressure-sensitive adhesives globally, thereby accelerating market growth.

"Water-based technology is projected to grow at the second-highest rate in the pressure sensitive adhesives market in terms of volume."

By technology, the demand for water-based pressure-sensitive adhesives is expected to grow at the second-fastest pace in terms of volume due to increasing environmental awareness and stricter regulations regarding solvent emissions. These adhesives offer low VOC emissions, improved workplace safety, and cost-effective processing, making them highly suitable for packaging, labeling, paper, and hygiene applications. Rising demand for sustainable adhesive technologies from packaging and consumer goods manufacturers is further accelerating adoption. In addition, continuous advancements in water-based adhesive formulations are improving their bonding strength and performance across diverse industrial applications.

"Rubber PSA is the second-largest chemistry segment in the pressure sensitive adhesives market in terms of volume."

By chemistry, the rubber PSA segment is estimated to account for the second-largest market share in terms of volume due to its strong initial tack, flexibility, and cost-effectiveness. Rubber-based pressure-sensitive adhesives are widely used in masking tapes, packaging tapes, labels, and general-purpose industrial applications where quick adhesion and reliable performance are essential. Their suitability for bonding on uneven surfaces and compatibility with various substrates continue to support demand across the packaging and construction sectors. Furthermore, increasing industrial activities and growing consumption of consumer goods are contributing to the steady expansion of rubber-based PSA applications globally.

"Graphics is projected to be the third-fastest growing application segment in the pressure sensitive adhesives market in terms of volume."

By application, the graphics segment is projected to grow at the third-highest rate in terms of volume, owing to increasing demand for advertising, promotional displays, vehicle wraps, and signage solutions. Pressure-sensitive adhesives are extensively used in graphic films due to their excellent adhesion, durability, and ease of application on multiple surfaces. Rapid urbanization, growth in retail branding activities, and increasing outdoor advertising expenditures are supporting market expansion. In addition, technological advancements in printable films and digital printing solutions are further enhancing the adoption of PSA-based graphics applications worldwide.

"Electrical, electronics, & telecommunications is projected to be the second-fastest growing end-use industry in the pressure sensitive adhesives market in terms of volume."

By end-use industry, the electrical, electronics, & telecommunications segment is expected to witness the second-fastest growth in the market in terms of volume due to increasing demand for electronic devices, smart technologies, and advanced communication infrastructure. PSAs are widely utilized in electronic assembly, display bonding, insulation, circuit protection, and wire harnessing applications because of their lightweight and high-performance properties. The rapid expansion of consumer electronics manufacturing, growing adoption of electric vehicles, and increasing investments in 5G infrastructure are further driving demand for advanced pressure-sensitive adhesive solutions across the sector.

"Middle East & Africa is projected to be the second-fastest growing region in the pressure sensitive adhesives market in terms of volume."

The Middle East & Africa region is expected to witness the second-fastest growth in the market in terms of volume due to increasing industrialization, infrastructure development, and expanding packaging demand across emerging economies. Growth in construction activities, rising consumption of packaged consumer goods, and improving healthcare infrastructure are driving PSA adoption in tapes, labels, and specialty applications. Additionally, the expansion of logistics and retail sectors, along with growing investments in manufacturing industries, is supporting higher consumption of pressure-sensitive adhesive products throughout the region.

- By Company Type: Tier 1 - 55%, Tier 2 - 25%, and Tier 3 - 20%

- By Designation: Directors - 50%, Managers - 30%, and Others - 20%

- By Region: North America - 40%, Europe - 35%, Asia Pacific - 20%, RoW- 5%

The key players profiled in the report include H.B. Fuller Company (US), Henkel AG & Co. KGaA (Germany), Dow Inc. (US), Arkema S.A. (France), Avery Dennison Corporation (US), 3M Company (US), Sika AG (Switzerland), Scapa Group PLC (UK), Wacker Chemie AG (Germany), and Illinois Tool Works Inc. (US).

Study Coverage

This report segments the market for pressure-sensitive adhesives based on technology, chemistry, application, end-use industry, and region, and provides estimations of value (in USD million) for the overall market size across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, services, and key strategies associated with the market.

Reasons to Buy this Report

This research report is focused on various levels of analysis-industry analysis (industry trends), market share analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the market, high-growth regions, and market drivers, restraints, and opportunities.

The report provides insights into the following points:

- Market Penetration: Comprehensive information on pressure-sensitive adhesives offered by top players in the global market

- Analysis of key drivers: (Rising Demand from Packaging and E-commerce Industries, Increasing Adoption in Automotive and Electric Vehicles), restraints (Volatility in Raw Material Prices, Stringent Environmental and VOC Regulations), opportunities (Expanding Opportunities in Electric Vehicles and Advanced Electronics, Rising Demand for Sustainable and Recyclable Packaging Solution) and challenges (Recycling Complexity of Adhesive-coated Materials, Performance Limitations in High-stress Applications) influencing the growth of pressure sensitive adhesives market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the market

- Market Development: Comprehensive information about lucrative emerging markets-the report analyzes the market for pressure-sensitive adhesives across regions.

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global pressure sensitive adhesives market

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS OF STUDY

- 1.3.3 MARKET DEFINITION AND INCLUSIONS, BY CHEMISTRY

- 1.3.4 MARKET DEFINITION AND INCLUSIONS, BY TECHNOLOGY

- 1.3.5 MARKET DEFINITION AND INCLUSIONS, BY APPLICATION

- 1.3.6 MARKET DEFINITION AND INCLUSIONS, BY END-USE INDUSTRY

- 1.3.7 YEARS CONSIDERED

- 1.3.8 CURRENCY CONSIDERED

- 1.3.9 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PRESSURE SENSITIVE ADHESIVES MARKET

- 3.2 PRESSURE SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY AND REGION

- 3.3 PRESSURE SENSITIVE ADHESIVES MARKET, BY APPLICATION

- 3.4 PRESSURE SENSITIVE ADHESIVES MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.1.1 DRIVERS

- 4.1.1.1 Rising demand from packaging and e-commerce industries

- 4.1.1.2 Increasing adoption in automotive and electric vehicles

- 4.1.1.3 Growing preference for sustainable and low-VOC adhesive technologies

- 4.1.2 RESTRAINTS

- 4.1.2.1 Volatility in raw material prices

- 4.1.2.2 Stringent environmental and VOC regulations

- 4.1.3 OPPORTUNITIES

- 4.1.3.1 Expanding opportunities in electric vehicles and advanced electronics

- 4.1.3.2 Rising demand for sustainable and recyclable packaging solutions

- 4.1.3.3 Increasing infrastructure development and construction activities

- 4.1.4 CHALLENGES

- 4.1.4.1 Recycling complexity of adhesive-coated materials

- 4.1.4.2 Performance limitations in high-stress applications

- 4.1.1 DRIVERS

- 4.2 UNMET NEEDS AND WHITE SPACES

- 4.2.1 UNMET NEEDS IN PRESSURE SENSITIVE ADHESIVES MARKET

- 4.2.1.1 Sustainable and recyclable adhesive solutions

- 4.2.1.2 High-temperature and chemical-resistant formulations

- 4.2.1.3 Low VOC and safer adhesive technologies

- 4.2.1.4 Advanced adhesives for electric vehicles and electronics

- 4.2.1.5 Improved adhesion on low surface energy substrates

- 4.2.2 WHITE SPACE OPPORTUNITIES

- 4.2.2.1 Smart and functional pressure-sensitive adhesives

- 4.2.2.2 Bio-based and renewable raw material integration

- 4.2.2.3 Wash off adhesives for packaging recycling

- 4.2.2.4 High growth opportunities in emerging economies

- 4.2.2.5 Specialty adhesives for medical and skin contact applications

- 4.2.1 UNMET NEEDS IN PRESSURE SENSITIVE ADHESIVES MARKET

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.3.1 INTERCONNECTED MARKETS

- 4.3.2 CROSS-SECTOR OPPORTUNITIES

- 4.4 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.4.1 EMERGING BUSINESS MODELS

- 4.4.2 ECOSYSTEM SHIFTS

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF SUBSTITUTES

- 5.1.2 THREAT OF NEW ENTRANTS

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST FOR MAJOR ECONOMIES

- 5.2.3 TRENDS IN GLOBAL PACKAGING INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF PRESSURE SENSITIVE ADHESIVES OFFERED BY KEY PLAYERS, BY END-USE INDUSTRY, 2025

- 5.5.2 AVERAGE SELLING PRICE TREND OF PRESSURE SENSITIVE ADHESIVES, BY REGION, 2022-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO (HS CODE-3506)

- 5.6.2 IMPORT SCENARIO (HS CODE-3506)

- 5.7 KEY CONFERENCES & EVENTS IN 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 SUSTAINABLE PACKAGING LABEL SOLUTIONS

- 5.10.2 LIGHTWEIGHT BONDING IN AUTOMOTIVE APPLICATIONS

- 5.10.3 ADVANCED PSA APPLICATIONS IN WEARABLE MEDICAL DEVICES

- 5.11 IMPACT OF 2025 US TARIFF - PRESSURE SENSITIVE ADHESIVES MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFFS

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.4.3.1 China

- 5.11.4.3.2 India

- 5.11.4.3.3 Vietnam

- 5.11.5 IMPACT ON END-USE INDUSTRIES

- 5.11.5.1 Packaging

- 5.11.5.2 Electrical, electronics & telecommunication

- 5.11.5.3 Automotive & transportation

- 5.11.5.4 Building & construction

- 5.11.5.5 Medical & healthcare

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 BIO-BASED AND SUSTAINABLE PRESSURE SENSITIVE ADHESIVES

- 6.1.2 UV-CURABLE AND SMART PRESSURE SENSITIVE ADHESIVES TECHNOLOGY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 RELEASE LINERS AND COATING TECHNOLOGIES

- 6.2.2 FLEXIBLE PACKAGING AND CONVERTING TECHNOLOGIES

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2026-2027)

- 6.3.2 MID-TERM (2028-2031)

- 6.3.3 LONG-TERM (2030-2035+)

- 6.4 PATENT ANALYSIS

- 6.4.1 APPROACH

- 6.4.2 DOCUMENT TYPE

- 6.4.3 TOP APPLICANTS

- 6.4.4 JURISDICTION ANALYSIS

- 6.5 IMPACT OF AI/GEN AI ON PRESSURE SENSITIVE ADHESIVES MARKET

- 6.5.1 ACCELERATED R&D AND ADHESIVE FORMULATION INNOVATION

- 6.5.2 ENHANCED PRODUCTION EFFICIENCY AND PROCESS CONTROL

- 6.5.3 PREDICTIVE MAINTENANCE AND OPERATIONAL CONTINUITY

- 6.5.4 OPTIMIZED SUPPLY CHAIN AND COST MANAGEMENT

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 REGULATORY POLICY INITIATIVES

- 7.2.1 SAFETY PROTOCOLS

- 7.2.2 SUSTAINABLE DEVELOPMENT

- 7.2.3 STANDARDIZATION

- 7.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

9 PRESSURE SENSITIVE ADHESIVES MARKET, BY CHEMISTRY

- 9.1 INTRODUCTION

- 9.2 ACRYLIC PSA

- 9.2.1 GROWING DEMAND FROM PACKAGING, AUTOMOTIVE, AND ELECTRONICS INDUSTRIES DRIVING MARKET GROWTH

- 9.3 RUBBER PSA

- 9.3.1 INCREASING DEMAND FOR COST-EFFECTIVE BONDING SOLUTIONS SUPPORTING GROWTH

- 9.4 SILICONE PSA

- 9.4.1 RISING DEMAND IN HIGH-TEMPERATURE AND SPECIALTY APPLICATIONS SUPPORTING MARKET GROWTH

- 9.5 OTHER CHEMISTRIES

- 9.5.1 INCREASING DEMAND FOR SPECIALIZED AND APPLICATION-SPECIFIC ADHESIVE SOLUTIONS DRIVING MARKET

10 PRESSURE SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 WATER-BASED

- 10.2.1 INCREASING DEMAND FOR ENVIRONMENTALLY FRIENDLY ADHESIVE SOLUTIONS DRIVING ADOPTION

- 10.3 SOLVENT-BASED

- 10.3.1 HIGH-PERFORMANCE BONDING REQUIREMENTS SUPPORTING DEMAND FOR SOLVENT-BASED PSA TECHNOLOGY

- 10.4 HOT-MELT

- 10.4.1 RAPID INDUSTRIALIZATION AND DEMAND FROM PACKAGING APPLICATIONS FUELING ADOPTION

- 10.5 RADIATION

- 10.5.1 GROWING DEMAND FOR ADVANCED CURING TECHNOLOGIES SUPPORTING ADOPTION

11 PRESSURE SENSITIVE ADHESIVES MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 TAPES

- 11.2.1 EXPANDING PACKAGING, AUTOMOTIVE, AND INDUSTRIAL APPLICATIONS DRIVING DEMAND

- 11.3 LABELS

- 11.3.1 RISING DEMAND FOR PACKAGING AND PRODUCT IDENTIFICATION SUPPORTING MARKET GROWTH

- 11.4 GRAPHICS

- 11.4.1 INCREASING DEMAND FOR ADVERTISING, DECORATIVE FILMS, AND VEHICLE WRAPS DRIVING SEGMENTAL GROWTH

- 11.5 OTHER APPLICATIONS

- 11.5.1 GROWING DEMAND FOR SPECIALTY BONDING AND DELAYED ADHESION SOLUTIONS SUPPORTING MARKET GROWTH

12 PRESSURE SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY

- 12.1 INTRODUCTION

- 12.2 PACKAGING

- 12.2.1 RAPID EXPANSION OF FLEXIBLE PACKAGING AND E-COMMERCE ACTIVITIES DRIVING DEMAND

- 12.3 ELECTRICAL, ELECTRONICS & TELECOMMUNICATION

- 12.3.1 INCREASING DEMAND FOR MINIATURIZED ELECTRONICS AND ADVANCED COMMUNICATION INFRASTRUCTURE DRIVING GROWTH

- 12.4 AUTOMOTIVE & TRANSPORTATION

- 12.4.1 RISING DEMAND FOR LIGHTWEIGHT BONDING AND VEHICLE PERFORMANCE ENHANCEMENT DRIVING ADOPTION

- 12.5 BUILDING & CONSTRUCTION

- 12.5.1 INCREASING INFRASTRUCTURE DEVELOPMENT AND URBAN CONSTRUCTION ACTIVITIES DRIVING DEMAND

- 12.6 MEDICAL & HEALTHCARE

- 12.6.1 GROWING DEMAND FOR ADVANCED MEDICAL DEVICES AND SKIN-FRIENDLY ADHESIVE SOLUTIONS DRIVING CONSUMPTION

- 12.7 OTHER END-USE INDUSTRIES

- 12.7.1 EXPANDING INDUSTRIAL APPLICATIONS AND CONSUMER PRODUCT DEMAND SUPPORTING MARKET GROWTH

13 PRESSURE SENSITIVE ADHESIVES MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 CHINA

- 13.2.1.1 Expanding consumer electronics and semiconductor production strengthening demand

- 13.2.2 INDIA

- 13.2.2.1 Rising flexible packaging consumption and rapid e-commerce expansion creating strong demand

- 13.2.3 JAPAN

- 13.2.3.1 Advanced electronics and high-performance material applications accelerating demand

- 13.2.4 SOUTH KOREA

- 13.2.4.1 Strong semiconductor and display manufacturing industry fueling demand

- 13.2.1 CHINA

- 13.3 NORTH AMERICA

- 13.3.1 US

- 13.3.1.1 Rapid growth in e-commerce and packaging industries driving market growth

- 13.3.2 CANADA

- 13.3.2.1 Expanding healthcare and medical device industries fueling demand

- 13.3.3 MEXICO

- 13.3.3.1 Expanding automotive manufacturing industry supporting market growth

- 13.3.1 US

- 13.4 EUROPE

- 13.4.1 GERMANY

- 13.4.1.1 Strong automotive manufacturing and electric vehicle production driving consumption

- 13.4.2 FRANCE

- 13.4.2.1 Rising healthcare and pharmaceutical packaging demand supporting market growth

- 13.4.3 UK

- 13.4.3.1 Expanding e-commerce and flexible packaging industries accelerating demand

- 13.4.4 ITALY

- 13.4.4.1 Growth in food packaging and labeling applications increasing demand

- 13.4.5 SPAIN

- 13.4.5.1 Expansion of food packaging industry accelerating demand

- 13.4.1 GERMANY

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.5.1.1 Rapid expansion of packaging industry driving market growth

- 13.5.2 SOUTH AFRICA

- 13.5.2.1 Growing healthcare industry driving demand for pressure sensitive adhesives

- 13.5.1 GCC COUNTRIES

- 13.6 SOUTH AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 Expanding packaging, healthcare, automotive, and electronics industries driving demand

- 13.6.2 ARGENTINA

- 13.6.2.1 Expanding packaging, automotive, and industrial activities fueling market growth

- 13.6.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN, JANUARY 2021-MAY 2026

- 14.2.1 STRATEGIES ADOPTED BY KEY PRESSURE SENSITIVE ADHESIVE MANUFACTURERS, JANUARY 2021-MAY 2026

- 14.3 MARKET SHARE ANALYSIS, 2025

- 14.4 REVENUE ANALYSIS, 2022-2025

- 14.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- 14.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.5.5.1 Company footprint

- 14.5.5.2 Region footprint

- 14.5.5.3 End-use industry footprint

- 14.5.5.4 Chemistry footprint

- 14.5.5.5 Technology footprint

- 14.5.5.6 Application footprint

- 14.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.6.1 PROGRESSIVE COMPANIES

- 14.6.2 RESPONSIVE COMPANIES

- 14.6.3 DYNAMIC COMPANIES

- 14.6.4 STARTING BLOCKS

- 14.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.6.5.1 Detailed list of key startups/SMES

- 14.6.5.2 Competitive benchmarking of key startups/SMEs

- 14.7 BRAND/PRODUCT COMPARISON ANALYSIS

- 14.8 COMPANY VALUATION AND FINANCIAL METRICS

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 HENKEL AG & CO. KGAA

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 DOW INC.

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 AVERY DENNISON CORPORATION

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Deals

- 15.1.3.3.3 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 H.B. FULLER COMPANY

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 3M COMPANY

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 ARKEMA SA

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches

- 15.1.6.3.2 Deals

- 15.1.7 SIKA AG

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.8 SCAPA GROUP PLC

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.9 WACKER CHEMIE AG

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.10 ILLINOIS TOOL WORKS INC.

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.1 HENKEL AG & CO. KGAA

- 15.2 OTHER KEY PLAYERS

- 15.2.1 TOYO INK AMERICA, LLC

- 15.2.2 PIDILITE INDUSTRIES

- 15.2.3 HELMITIN ADHESIVES

- 15.2.4 JOWAT SE

- 15.2.5 MAPEI S.P.A.

- 15.2.6 FRANKLIN ADHESIVES & POLYMERS

- 15.2.7 DRYTAC CORPORATION

- 15.2.8 JESONS INDUSTRIES LIMITED

- 15.2.9 ADHESIVES RESEARCH INC.

- 15.2.10 SHANGHAI JAOUR ADHESIVE PRODUCTS CO., LTD.

- 15.2.11 ESTER CHEMICAL INDUSTRIES PVT. LTD.

- 15.2.12 DYNA-TECH ADHESIVES, INC.

- 15.2.13 CATTIE ADHESIVES

- 15.2.14 ADVANCE POLYMER PRODUCTS

- 15.2.15 NANPAO RESINS CHEMICAL GROUP

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key primary interview participants

- 16.1.2.3 Breakdown of primary interviews

- 16.1.2.4 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.3 BASE NUMBER CALCULATION

- 16.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 16.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 16.4 MARKET FORECAST APPROACH

- 16.4.1 SUPPLY SIDE

- 16.4.2 DEMAND SIDE

- 16.5 DATA TRIANGULATION

- 16.6 RESEARCH ASSUMPTIONS

- 16.7 RESEARCH LIMITATIONS AND RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS