|

시장보고서

상품코드

2059328

군용 드론 시장 : 클래스별, 드론 유형별, 최대 이륙 중량별, 적재 능력별, 항속 시간별, 익형별, 자율성별, 발사 방식별, 추진 방식별, 지역별 - 예측(-2031년)Military Drones Market By Class (Small, Tactical, Strategic), Type (Combat, ISR, Delivery, Target), MTOW (Up to 150 Kg, 151-2000 Kg, >2000 Kg), Endurance, Payload Capacity, Wing Type, Autonomy, Launch Mode, Propulsion, Region - Global Forecast to 2031 |

||||||

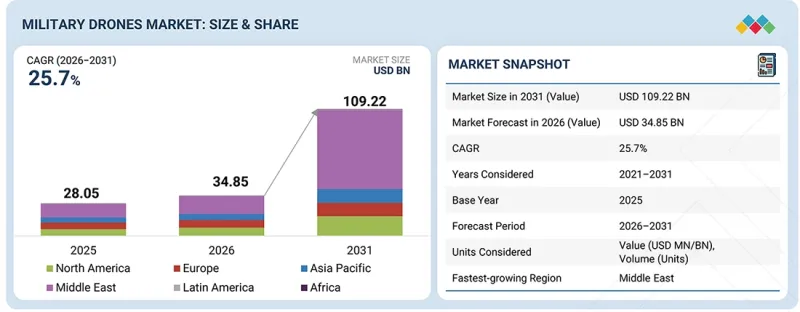

군용 드론 시장 규모는 2026년에 348억 5,000만 달러로 추정되며, 예측 기간 중에 CAGR 25.7%로 성장을 지속하여 2031년까지 1,092억 2,000만 달러에 이를 전망입니다.

현대 방위 작전에서의 무인 시스템 도입 확대에 힘입어, 해당 시장은 강력한 성장을 이루고 있습니다. 시장의 주요 동향 중 하나는 감시 임무에서 자율형 드론의 활용 확대입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 클래스별, 드론 유형별, 최대 이륙 중량별, 적재 능력별, 항속 시간별, 익형별, 자율성별, 발사 방식별, 추진 방식별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

방위 분야에서도 전투 지원 활동이 증가하고 있습니다. 국방 기관은 전장에서의 의사결정을 신속하게 하기 위해 인공지능(AI)을 활용한 드론 기술에 투자하고 있습니다. 첨단 페이로드 시스템을 탑재한 장거리 드론에 대한 수요가 증가하고 있습니다. 군용 드론 시장은 주요 경제국들의 국방비 증가에 힘입어 성장하고 있습니다.

“적재 용량별로는 5kg 미만 부문이 예측 기간 동안 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다.” '

5kg 미만의 적재 능력 부문이 군용 드론 시장에서 급속히 성장하고 있는 것은 국방 기관들이 감시 임무를 위해 경량 드론의 사용을 확대하고 있기 때문입니다. 이 드론들은 국경 지역이나 전투 지역에서의 실시간 감시를 지원합니다. 군사 기관은 전술 작전 중 신속한 전개를 위해 소형 드론을 선호하여 도입하고 있습니다. 휴대용 무인 시스템에 대한 수요 증가 역시 이 부문의 성장을 더욱 뒷받침하고 있습니다.

“비행 지속 시간별로는 21-40시간 구간이 예측 기간(SC3.1) 동안 가장 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 전망됩니다.” '

군용 드론 시장에서 21-40시간의 비행 지속 시간 구간이 성장하고 있는 것은 국방 기관들이 장시간 감시 임무를 수행하기 위해 드론을 필요로 하기 때문입니다. 국방 분야에서는 정보 수집 활동도 증가하고 있습니다. 이 드론들은 빈번한 착륙 없이도 국경 지역이나 분쟁 지역에서 지속적인 감시를 지원합니다. 군에서는 전투 지원 작전이나 해상 감시 작전에서 장시간 비행이 가능한 드론을 선호하여 도입하고 있습니다. 이 부문을 뒷받침하는 또 다른 요인은 지속적인 전투 감시에 대한 수요가 증가하고 있다는 점입니다.

“20(SC4.1)25년에는 중동이 가장 큰 시장 점유율을 차지했습니다. '

중동은 사우디아라비아, 이스라엘, UAE 등 여러 국가들의 국방 투자 증가에 힘입어 군용 드론 시장에서 큰 점유율을 차지하고 있습니다. 지역 방위 기관은 국경 감시 활동을 위해 감시용 드론의 활용을 확대되고 있습니다. 또한, 전투 임무 증가 역시 해당 지역에 드론을 배치하는 데 박차를 가하고 있습니다. 세계적 긴장이 고조됨에 따라 무인 방어 시스템의 활용이 확대되고 있습니다. 정보 수집 능력을 향상시키기 위해 각국 정부는 자율형 군사 기술에 주력하고 있습니다.

조사 범위

본 시장 조사에서는 군용 드론 시장을 다양한 부문 및 하위 부문에 걸쳐 분석했습니다. 본 조사는 각 지역 시장 규모와 성장 가능성을 추정하는 것을 목적으로 합니다. 또한, 주요 시장 진출기업에 대한 상세한 경쟁 분석도 제공하며, 여기에는 기업 프로파일, 제품 라인업, 최근 동향 및 전략적 시장 이니셔티브가 포함됩니다.

이 보고서를 구매해야 하는 이유

본 보고서는 시장 선도 기업 및 신규 진출기업을 대상으로 군용 드론 시장 전체의 매출 전망을 제시합니다. 또한, 이해관계자들이 경쟁 구도를 더 깊이 이해하고, 자사의 비즈니스를 보다 효과적으로 포지셔닝하며, 적절한 시장 진출 전략을 수립하기 위한 인사이트를 얻을 수 있게 해줍니다. 또한, 본 보고서는 이해관계자들이 시장 역학을 이해하는 데 도움을 주며, 주요 시장 성장 촉진요인, 제약 요인, 과제 및 기회에 대한 정보를 제공합니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 현황과 구매 행동

제7장 기술 진보, AI의 영향, 특허, 혁신, 그리고 향후 응용

제8장 지속가능성과 규제 상황

제9장 군용 드론 시장(클래스별)(시장 규모 및 2031년까지 예측, 100만 달러)

제10장 군용 드론 시장(드론 유형별)(시장 규모 및 2031년까지 예측, 100만 달러)

제11장 군용 드론 시장(최대 이륙 중량별)(시장 규모 및 2031년까지 예측, 100만 달러)

제12장 군용 드론 시장(적재 능력별)(시장 규모 및 2031년까지 예측, 100만 달러)

제13장 군용 드론 시장(항속 시간 별)(시장 규모 및 2031년까지 예측, 100만 달러)

제14장 군용 드론 시장(익형 별)(시장 규모 및 2031년까지 예측, 100만 달러)

제15장 군용 드론 시장(자율성 별)(시장 규모 및 2031년까지 예측, 100만 달러)

제16장 군용 드론 시장(발사 방식별)(시장 규모 및 2031년까지 예측, 100만 달러)

제17장 군용 드론 시장(추진 방식별)(시장 규모 및 2031년까지 예측, 100만 달러)

제18장 군용 드론 시장(지역별)(시장 규모 및 2031년까지 예측, 100만 달러)

제19장 경쟁 구도

제20장 기업 개요

제21장 조사 방법

제22장 지정학적 분쟁이 군용 드론 시장에 미치는 영향

제23장 부록

LSH 26.06.25The military drones market is estimated at USD 34.85 billion in 2026 and is projected to reach US[SC1.1]D 109.22 billion by 2031 at a CAGR of 25.7% during the forecast period. The market is witnessing strong growth from the increasing adoption of unmanned systems in modern defense operations. One major trend in the market is the rising use of autonomous drones for surveillance missions.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) |

| Segments | By Class, Payload Capacity, Propulsion and Region |

| Regions covered | North America, Europe, APAC, RoW |

Combat support activities are also increasing in the defense sector. Defense agencies are investing in artificial intelligence-based drone technologies for faster battlefield decision-making. Long-range drones with sophisticated payload systems are becoming increasingly popular. The market for military drones is also driven by increased defense spending in major economies.

"By payload capacity, the <5 Kg segment is projected to grow at the highest CAGR during the foreca[SC2.1]st period."

The <5 Kg payload capacity segment is growing rapidly in the military drones market because defense forces are increasing the use of lightweight drones for surveillance missions. These drones support real-time monitoring in border areas, plus combat zones. Military agencies prefer compact drones for faster deployment during tactical operations. Rising demand for portable unmanned systems is further supporting growth in this segment.

"By endurance, the 21-40 hours segment is projected to grow at the highest CAGR during the forecast [SC3.1]period."

The 21-40 Hours endurance segment is growing in the military drones market because defense agencies require drones for long-duration surveillance missions. Intelligence gathering operations are also increasing in the defense sector. These drones support continuous monitoring in border regions and conflict zones without frequent landing requirements. Military forces prefer long-endurance drones for combat support operations. maritime surveillance operations. Another factor boosting this segment is the growing need for ongoing combat surveillance.

"The Middle Eastern region captured the largest market share in 20[SC4.1]25."

The Middle Eastern region holds a major share in the military drones market because of increasing defense investments in countries such as Saudi Arabia, Israel, and the UAE. Regional defense agencies are expanding the use of surveillance drones for border monitoring operations. Combat missions are also increasing drone deployment in the region. The use of unmanned defense systems is growing as global tensions rise. To improve intelligence collecting capabilities, governments are concentrating on autonomous military technologies.

The breakdown of profiles for primary participants in the military drones market is provided below:

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C Level - 35%, Director Level - 25%, and Others - 40%

- By Region: North America - 25%, Europe - 15%, Asia Pacific - 45%, Middle East - 10%, and Rest of the World (RoW) - 5%

Research Coverage:

This market study examines the military drones market across various segments and subsegments. It aims to estimate the market's size and growth potential in different regions. The study also provides a detailed competitive analysis of key market players, including their company profiles, product offerings, recent developments, and strategic market initiatives.

Reasons to Buy This Report:

The report will assist market leaders and new entrants with estimates of the revenue figures for the overall military drones market. It will also enable stakeholders to understand the competitive landscape better and gain insights to position their businesses more effectively and develop appropriate go-to-market strategies. Additionally, the report will help stakeholders understand the market dynamics and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Market Drivers (increasing defense modernization programs and rising military expenditure), restraints (vulnerability to electronic warfare, cyberattacks, and communication disruptions), opportunities (expansion of military drone exports and international defense collaborations), challenges (supply chain disruptions and dependence on critical semiconductors and electronic components)

- Market Penetration: Comprehensive information on the military drones market offered by the top players in the market

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the military drones market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the military drones market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the military drones market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN MILITARY DRONES MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MILITARY DRONES MARKET

- 3.2 MILITARY DRONES MARKET, BY WING TYPE

- 3.3 MILITARY DRONES MARKET, BY LAUNCH MODE

- 3.4 MILITARY DRONES MARKET, BY END USER

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing defense modernization programs and rising military expenditure

- 4.2.1.2 Growing adoption of artificial intelligence and autonomous swarm technologies

- 4.2.1.3 Rising demand for border surveillance and counter-drone operations

- 4.2.2 RESTRAINTS

- 4.2.2.1 Vulnerability to electronic warfare, cyberattacks, and communication disruptions

- 4.2.2.2 High procurement, operational, and maintenance costs of advanced military drones

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of military drone exports and international defense collaborations

- 4.2.3.2 Growing integration of military drones with manned-unmanned teaming (MUM-T) operations

- 4.2.4 CHALLENGES

- 4.2.4.1 Supply chain disruptions and dependence on critical semiconductor and electronic components

- 4.2.4.2 Increasing regulatory and ethical concerns regarding autonomous combat drones

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 CONVERGENCE WITH DEFENSE ELECTRONICS, AUTONOMOUS SYSTEMS, AND MRO ECOSYSTEMS

- 4.4.2 INTEGRATION WITH ARTIFICIAL INTELLIGENCE, SWARM WARFARE, AND DIGITAL COMMAND NETWORKS

- 4.4.3 EXPANSION OF COUNTER-DRONE SYSTEMS AND ELECTRONIC WARFARE INTEGRATION

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 GDP TRENDS AND FORECAST

- 5.2.2 TRENDS IN GLOBAL UAV (DRONES) INDUSTRY

- 5.2.3 TRENDS IN GLOBAL MILITARY DRONE INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 R&D ENGINEERS (~30%)

- 5.3.2 RAW MATERIAL SUPPLIERS (10~%)

- 5.3.3 COMPONENT AND PRODUCT MANUFACTURERS (~10%)

- 5.3.4 ASSEMBLERS AND INTEGRATORS (~30%)

- 5.3.5 END USERS (~20%)

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 MANUFACTURERS

- 5.4.2 SOLUTION AND SERVICE PROVIDERS

- 5.4.3 END USERS

- 5.5 INVESTMENT AND FUNDING SCENARIO

- 5.6 PRICING ANALYSIS

- 5.6.1 INDICATIVE PRICING OF SMALL MILITARY DRONES, BY COUNTRY, 2024-2025 (USD MILLION)

- 5.6.2 INDICATIVE PRICING OF TACTICAL MILITARY DRONES, BY COUNTRY, 2024-2025 (USD MILLION)

- 5.6.3 INDICATIVE PRICING OF STRATEGIC MILITARY DRONES, BY COUNTRY, 2024-2025 (USD MILLION)

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 8806)

- 5.7.2 EXPORT SCENARIO (HS CODE 8806)

- 5.8 KEY CONFERENCE AND EVENTS, 2026-2027

- 5.9 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 GENERAL ATOMICS - LONG-ENDURANCE MILITARY SURVEILLANCE SOLUTIONS

- 5.10.2 BAYKAR - COST-EFFECTIVE COMBAT DRONE DEPLOYMENT

- 5.10.3 BOEING - COLLABORATIVE COMBAT AIRCRAFT PROGRAM

- 5.10.4 NORTHROP GRUMMAN - HIGH-ALTITUDE MARITIME SURVEILLANCE CAPABILITY

- 5.11 IMPACT OF 2025 US TARIFFS

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON DIFFERENT APPLICATIONS

- 5.11.5.1 Defense

- 5.11.5.2 Border security and surveillance

6 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 6.1 DECISION-MAKING PROCESS

- 6.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.2.2 BUYING CRITERIA

- 6.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 6.4 UNMET NEEDS OF END USERS

- 6.4.1 NEED FOR ADVANCED AUTONOMOUS AND LONG-ENDURANCE UAV SYSTEMS

- 6.4.2 NEED FOR ENHANCED SITUATIONAL AWARENESS AND MULTI-MISSION CAPABILITIES

- 6.4.3 NEED FOR RAPID DEPLOYMENT AND MODULAR UAV ARCHITECTURES

7 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 7.1 KEY EMERGING TECHNOLOGIES

- 7.1.1 AI IN MILITARY DRONES

- 7.1.2 MID-AIR REFUELING OF DRONES

- 7.1.3 SPY DRONES

- 7.1.4 UNMANNED COMBAT AERIAL VEHICLES

- 7.1.5 ANTI-UAV DEFENSE SYSTEMS

- 7.2 COMPLEMENTARY TECHNOLOGIES

- 7.2.1 SWARM TECHNOLOGY

- 7.2.2 AUTONOMOUS TAKE-OFF AND LANDING SYSTEMS

- 7.3 ADJACENT TECHNOLOGIES

- 7.3.1 5G & INTERNET OF THINGS (IOT)

- 7.3.2 ADDITIVE MANUFACTURING

- 7.4 TECHNOLOGY/PRODUCT ROADMAP

- 7.5 TECHNOLOGY TRENDS

- 7.5.1 SYNTHETIC APERTURE RADAR (SAR)

- 7.5.2 SIGNAL INTELLIGENCE (SIGINT) BY DRONES

- 7.5.3 ELECTRONIC WARFARE USING MILITARY DRONES

- 7.5.4 MANNED UNMANNED TEAMING (MUM-T)

- 7.5.5 TARGET DRONES

- 7.5.6 ENDURANCE

- 7.5.7 HYPERSONIC ARMED FORCES

- 7.6 PATENT ANALYSIS

- 7.7 FUTURE APPLICATIONS

- 7.8 IMPACT OF AI/GENERATIVE AI

- 7.8.1 TOP USE CASES AND POTENTIAL IN MILITARY DRONES MARKET

- 7.8.2 CASE STUDIES OF AI IMPLEMENTATION

- 7.8.3 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 7.8.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI

8 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 8.1 REGIONAL REGULATIONS AND COMPLIANCE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 INDUSTRY STANDARDS

- 8.2 SUSTAINABILITY INITIATIVES

- 8.2.1 ECO-APPLICATIONS

- 8.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 8.3.1 SUSTAINABILITY IMPACT ON MILITARY DRONES MARKET

- 8.3.2 REGULATORY POLICIES DRIVING MILITARY DRONES MARKET

- 8.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

9 MILITARY DRONES MARKET, BY CLASS (MARKET SIZE & FORECAST TO 2031, USD MILLION)

- 9.1 INTRODUCTION

- 9.2 SMALL

- 9.2.1 USE CASE: BLACK HORNET 4 NANO RECONNAISSANCE DRONE BY TELEDYNE FLIR DEFENSE

- 9.2.2 NANO (UP TO 250 GM)

- 9.2.2.1 Increasing demand for soldier-borne reconnaissance systems and covert battlefield intelligence to drive adoption

- 9.2.3 MICRO (251 GM - 2 KG)

- 9.2.3.1 Increasing requirement for portable tactical ISR platforms and enhanced battlefield awareness to drive adoption

- 9.2.4 MINI (2-25 KG)

- 9.2.4.1 Increasing demand for tactical multi-mission platforms and extended ISR capabilities to drive growth

- 9.3 TACTICAL

- 9.3.1 USE CASE: RQ-7 SHADOW TACTICAL UNMANNED AIRCRAFT SYSTEM BY TEXTRON SYSTEMS

- 9.3.2 SHORT RANGE (UP TO 50 KM)

- 9.3.2.1 Increasing demand for rapid tactical reconnaissance and frontline battlefield intelligence to drive growth

- 9.3.3 MEDIUM RANGE (51-200 KM)

- 9.3.3.1 Increasing demand for persistent ISR capabilities and expanded battlefield coverage to drive growth

- 9.3.4 EXTENDED RANGE (201-500 KM)

- 9.3.4.1 Increasing requirement for deep-area ISR missions and long-endurance battlefield surveillance to drive growth

- 9.4 STRATEGIC

- 9.4.1 USE CASE: MQ-9B SKYGUARDIAN BY GENERAL ATOMICS

- 9.4.2 MEDIUM-ALTITUDE LONG-ENDURANCE (MALE)

- 9.4.2.1 Increasing demand for persistent ISR missions and multi-role battlefield operations to drive growth

- 9.4.3 HIGH-ALTITUDE LONG-ENDURANCE (HALE)

- 9.4.3.1 Increasing requirement for persistent high-altitude surveillance and strategic intelligence collection to drive market expansion

10 MILITARY DRONES MARKET, BY DRONE TYPE (MARKET SIZE & FORECAST TO 2031, USD MILLION)

- 10.1 INTRODUCTION

- 10.2 COMBAT/STRIKE

- 10.2.1 USE CASE: MQ-9 REAPER COMBAT DRONE BY GENERAL ATOMICS

- 10.2.2 UNMANNED COMBAT AERIAL VEHICLE (UCAV)

- 10.2.2.1 Increasing demand for autonomous precision strike capability and high-risk mission execution to drive growth

- 10.2.3 LOITERING MUNITION

- 10.2.3.1 Increasing demand for precision strike capability and cost-effective tactical engagement systems to drive growth

- 10.3 INTELLIGENCE, SURVEILLANCE, AND RECONNAISSANCE (ISR)

- 10.3.1 INCREASING REQUIREMENT FOR PERSISTENT BATTLEFIELD AWARENESS AND REAL-TIME INTELLIGENCE COLLECTION TO DRIVE GROWTH

- 10.3.1.1 Use case: RQ-4 Global Hawk ISR platform by Northrop Grumman

- 10.3.1 INCREASING REQUIREMENT FOR PERSISTENT BATTLEFIELD AWARENESS AND REAL-TIME INTELLIGENCE COLLECTION TO DRIVE GROWTH

- 10.4 DELIVERY

- 10.4.1 INCREASING DEMAND FOR AUTONOMOUS LOGISTICS SUPPORT AND RAPID BATTLEFIELD RESUPPLY CAPABILITIES TO DRIVE GROWTH

- 10.4.1.1 Use case: K-MAX unmanned logistics platform by Lockheed Martin

- 10.4.1 INCREASING DEMAND FOR AUTONOMOUS LOGISTICS SUPPORT AND RAPID BATTLEFIELD RESUPPLY CAPABILITIES TO DRIVE GROWTH

- 10.5 TARGET

- 10.5.1 INCREASING DEMAND FOR REALISTIC COMBAT TRAINING ENVIRONMENTS AND ADVANCED WEAPON SYSTEM VALIDATION TO DRIVE GROWTH

- 10.5.1.1 Use case: BQM-177A subsonic aerial target system by Kratos Defense & Security Solutions

- 10.5.1 INCREASING DEMAND FOR REALISTIC COMBAT TRAINING ENVIRONMENTS AND ADVANCED WEAPON SYSTEM VALIDATION TO DRIVE GROWTH

11 MILITARY DRONES MARKET, BY MTOW (MARKET SIZE & FORECAST TO 2031, USD MILLION)

- 11.1 INTRODUCTION

- 11.2 UP TO 150 KG

- 11.2.1 INCREASING DEMAND FOR LIGHTWEIGHT TACTICAL PLATFORMS AND RAPID DEPLOYMENT CAPABILITIES TO DRIVE GROWTH

- 11.2.1.1 Use case: Puma 3 AE tactical drone by AeroVironment

- 11.2.1 INCREASING DEMAND FOR LIGHTWEIGHT TACTICAL PLATFORMS AND RAPID DEPLOYMENT CAPABILITIES TO DRIVE GROWTH

- 11.3 151-1,200 KG

- 11.3.1 INCREASING DEMAND FOR MULTI-MISSION TACTICAL PLATFORMS AND EXTENDED OPERATIONAL CAPABILITIES TO DRIVE GROWTH

- 11.3.1.1 Use case: Hermes 900 multi-mission platform by Israel Aerospace Industries Ltd.

- 11.3.1 INCREASING DEMAND FOR MULTI-MISSION TACTICAL PLATFORMS AND EXTENDED OPERATIONAL CAPABILITIES TO DRIVE GROWTH

- 11.4 >1,200 KG

- 11.4.1 INCREASING DEMAND FOR HIGH-PAYLOAD STRATEGIC PLATFORMS AND LONG-ENDURANCE MULTI-DOMAIN OPERATIONS TO DRIVE GROWTH

- 11.4.1.1 Use case: MQ-9B SkyGuardian by General Atomics

- 11.4.1 INCREASING DEMAND FOR HIGH-PAYLOAD STRATEGIC PLATFORMS AND LONG-ENDURANCE MULTI-DOMAIN OPERATIONS TO DRIVE GROWTH

12 MILITARY DRONES MARKET, BY PAYLOAD CAPACITY (MARKET SIZE & FORECAST TO 2031, USD MILLION)

- 12.1 INTRODUCTION

- 12.2 <5 KG

- 12.2.1 INCREASING DEMAND FOR LIGHTWEIGHT TACTICAL RECONNAISSANCE SYSTEMS AND SOLDIER-LEVEL BATTLEFIELD AWARENESS TO DRIVE GROWTH

- 12.2.1.1 Use case: Black Hornet 4 nano drone by Teledyne FLIR Defense

- 12.2.1 INCREASING DEMAND FOR LIGHTWEIGHT TACTICAL RECONNAISSANCE SYSTEMS AND SOLDIER-LEVEL BATTLEFIELD AWARENESS TO DRIVE GROWTH

- 12.3 5-50 KG

- 12.3.1 INCREASING DEMAND FOR TACTICAL MULTI-MISSION CAPABILITIES AND ENHANCED BATTLEFIELD OPERATIONAL FLEXIBILITY TO DRIVE GROWTH

- 12.3.1.1 Use case: R80D SkyRaider platform by Teledyne FLIR Defense

- 12.3.1 INCREASING DEMAND FOR TACTICAL MULTI-MISSION CAPABILITIES AND ENHANCED BATTLEFIELD OPERATIONAL FLEXIBILITY TO DRIVE GROWTH

- 12.4 51-250 KG

- 12.4.1 INCREASING DEMAND FOR MEDIUM-ALTITUDE LONG-ENDURANCE (MALE) SURVEILLANCE AND MULTI-MISSION TACTICAL OPERATIONS TO DRIVE GROWTH

- 12.4.1.1 Use case: MQ-9 Reaper by General Atomics Aeronautical Systems

- 12.4.1 INCREASING DEMAND FOR MEDIUM-ALTITUDE LONG-ENDURANCE (MALE) SURVEILLANCE AND MULTI-MISSION TACTICAL OPERATIONS TO DRIVE GROWTH

- 12.5 >250 KG

- 12.5.1 INCREASING DEMAND FOR HIGH-PAYLOAD STRATEGIC MISSIONS AND LONG-ENDURANCE MULTI-ROLE OPERATIONS TO DRIVE GROWTH

- 12.5.1.1 Use case: MQ-4C Triton platform by Northrop Grumman

- 12.5.1 INCREASING DEMAND FOR HIGH-PAYLOAD STRATEGIC MISSIONS AND LONG-ENDURANCE MULTI-ROLE OPERATIONS TO DRIVE GROWTH

13 MILITARY DRONES MARKET, BY ENDURANCE (MARKET SIZE & FORECAST TO 2031, USD MILLION)

- 13.1 INTRODUCTION

- 13.2 <5 HOURS

- 13.2.1 INCREASING DEMAND FOR RAPID DEPLOYMENT MISSIONS AND SHORT-DURATION TACTICAL SURVEILLANCE TO DRIVE GROWTH

- 13.2.1.1 Use case: Raven Tactical Unmanned Aircraft System by AeroVironment

- 13.2.1 INCREASING DEMAND FOR RAPID DEPLOYMENT MISSIONS AND SHORT-DURATION TACTICAL SURVEILLANCE TO DRIVE GROWTH

- 13.3 5-20 HOURS

- 13.3.1 INCREASING DEMAND FOR PERSISTENT TACTICAL ISR MISSIONS AND EXTENDED BATTLEFIELD COVERAGE TO DRIVE GROWTH

- 13.3.1.1 Use case: Hermes 450 tactical unmanned platform by Israel Aerospace Industries Ltd.

- 13.3.1 INCREASING DEMAND FOR PERSISTENT TACTICAL ISR MISSIONS AND EXTENDED BATTLEFIELD COVERAGE TO DRIVE GROWTH

- 13.4 21-40 HOURS

- 13.4.1 INCREASING DEMAND FOR LONG-DURATION ISR MISSIONS AND PERSISTENT OPERATIONAL SURVEILLANCE TO DRIVE GROWTH

- 13.4.1.1 Use case: Heron TP Platform by Israel Aerospace Industries Ltd.

- 13.4.1 INCREASING DEMAND FOR LONG-DURATION ISR MISSIONS AND PERSISTENT OPERATIONAL SURVEILLANCE TO DRIVE GROWTH

- 13.5 >40 HOURS

- 13.5.1 INCREASING DEMAND FOR ULTRA-LONG-ENDURANCE ISR MISSIONS AND PERSISTENT STRATEGIC SURVEILLANCE TO DRIVE GROWTH

- 13.5.1.1 Use case: RQ-4 Global Hawk platform by Northrop Grumman

- 13.5.1 INCREASING DEMAND FOR ULTRA-LONG-ENDURANCE ISR MISSIONS AND PERSISTENT STRATEGIC SURVEILLANCE TO DRIVE GROWTH

14 MILITARY DRONES MARKET, BY WING TYPE (MARKET SIZE & FORECAST TO 2031, USD MILLION)

- 14.1 INTRODUCTION

- 14.2 FIXED WING

- 14.2.1 INCREASING DEMAND FOR LONG-ENDURANCE MISSIONS AND WIDE-AREA SURVEILLANCE CAPABILITIES TO DRIVE GROWTH

- 14.2.1.1 Use case: Bayraktar Akinci platform by Baykar

- 14.2.1 INCREASING DEMAND FOR LONG-ENDURANCE MISSIONS AND WIDE-AREA SURVEILLANCE CAPABILITIES TO DRIVE GROWTH

- 14.3 ROTARY WING

- 14.3.1 INCREASING DEMAND FOR VERTICAL TAKEOFF CAPABILITY AND HIGH-MANEUVERABILITY TACTICAL OPERATIONS TO DRIVE GROWTH

- 14.3.1.1 Use case: Firebird 650 rotary-wing drone by Anduril Industries

- 14.3.1 INCREASING DEMAND FOR VERTICAL TAKEOFF CAPABILITY AND HIGH-MANEUVERABILITY TACTICAL OPERATIONS TO DRIVE GROWTH

- 14.4 HYBRID

- 14.4.1 INCREASING DEMAND FOR COMBINED VTOL FLEXIBILITY AND LONG-ENDURANCE MISSION PERFORMANCE TO DRIVE GROWTH

- 14.4.1.1 Use case: JUMP 20 platform by AeroVironment

- 14.4.1 INCREASING DEMAND FOR COMBINED VTOL FLEXIBILITY AND LONG-ENDURANCE MISSION PERFORMANCE TO DRIVE GROWTH

15 MILITARY DRONES MARKET, BY AUTONOMY LEVEL (MARKET SIZE & FORECAST TO 2031, USD MILLION)

- 15.1 INTRODUCTION

- 15.2 REMOTELY PILOTED

- 15.2.1 INCREASING DEMAND FOR REAL-TIME HUMAN-CONTROLLED OPERATIONS AND MISSION RELIABILITY TO DRIVE GROWTH

- 15.2.1.1 Use case: TB2 Platform by Baykar

- 15.2.1 INCREASING DEMAND FOR REAL-TIME HUMAN-CONTROLLED OPERATIONS AND MISSION RELIABILITY TO DRIVE GROWTH

- 15.3 SEMI-AUTONOMOUS

- 15.3.1 INCREASING DEMAND FOR REDUCED OPERATOR WORKLOAD AND ENHANCED MISSION AUTOMATION TO DRIVE GROWTH

- 15.3.1.1 Use case: Ghost Bat collaborative combat aircraft by Boeing

- 15.3.1 INCREASING DEMAND FOR REDUCED OPERATOR WORKLOAD AND ENHANCED MISSION AUTOMATION TO DRIVE GROWTH

- 15.4 FULLY AUTONOMOUS

- 15.4.1 INCREASING DEMAND FOR AI-DRIVEN MISSION EXECUTION AND NEXT-GENERATION UNMANNED WARFARE CAPABILITIES TO DRIVE GROWTH

- 15.4.1.1 Use case: Altius-600 autonomous drone by Anduril Industries

- 15.4.1 INCREASING DEMAND FOR AI-DRIVEN MISSION EXECUTION AND NEXT-GENERATION UNMANNED WARFARE CAPABILITIES TO DRIVE GROWTH

16 MILITARY DRONES MARKET, BY LAUNCH MODE (MARKET SIZE & FORECAST TO 2031, USD MILLION)

- 16.1 INTRODUCTION

- 16.2 VERTICAL TAKE-OFF & LANDING (VTOL)

- 16.2.1 WIDELY USED FOR ISR, BORDER MONITORING, TACTICAL LOGISTICS, URBAN WARFARE SUPPORT, MARITIME SURVEILLANCE, AND RAPID-RESPONSE MISSIONS

- 16.2.1.1 Use case: V-BAT platform by Shield AI

- 16.2.1 WIDELY USED FOR ISR, BORDER MONITORING, TACTICAL LOGISTICS, URBAN WARFARE SUPPORT, MARITIME SURVEILLANCE, AND RAPID-RESPONSE MISSIONS

- 16.3 RUNWAY DEPENDENT

- 16.3.1 SUPPORTS LARGER AIRFRAME ARCHITECTURES AND ADVANCED MISSION PAYLOADS

- 16.3.1.1 Use case: MQ-9B SkyGuardian platform by General Atomics

- 16.3.1 SUPPORTS LARGER AIRFRAME ARCHITECTURES AND ADVANCED MISSION PAYLOADS

- 16.4 CATAPULT LAUNCHED

- 16.4.1 ABILITY TO LAUNCH FROM COMPACT MOBILE SYSTEMS WHILE SUPPORTING EFFICIENT BATTLEFIELD DEPLOYMENT TO DRIVE GROWTH

- 16.4.1.1 Use case: Skylark I-LEX Platform by Elbit Systems

- 16.4.1 ABILITY TO LAUNCH FROM COMPACT MOBILE SYSTEMS WHILE SUPPORTING EFFICIENT BATTLEFIELD DEPLOYMENT TO DRIVE GROWTH

- 16.5 HAND LAUNCHED

- 16.5.1 INCREASING DEMAND FOR PORTABLE FRONTLINE ISR SYSTEMS AND RAPID TACTICAL DEPLOYMENT TO DRIVE GROWTH

- 16.5.1.1 Use case: Raven B tactical drone by AeroVironment

- 16.5.1 INCREASING DEMAND FOR PORTABLE FRONTLINE ISR SYSTEMS AND RAPID TACTICAL DEPLOYMENT TO DRIVE GROWTH

17 MILITARY DRONES MARKET, BY PROPULSION (MARKET SIZE & FORECAST TO 2031, USD MILLION)

- 17.1 INTRODUCTION

- 17.2 FUEL POWERED

- 17.2.1 USE CASE: MQ-4C TRITON PLATFORM BY NORTHROP GRUMMAN

- 17.2.2 TURBO ENGINES

- 17.2.2.1 Increasing demand for high-speed operations and long-endurance strategic missions to drive growth

- 17.2.3 PISTON ENGINES

- 17.2.3.1 Increasing demand for cost-efficient tactical operations and medium-endurance mission capability to drive growth

- 17.3 BATTERY POWERED

- 17.3.1 USE CASE: QUANTIX RECON PLATFORM BY AEROVIRONMENT

- 17.3.2 FULLY ELECTRIC

- 17.3.2.1 Increasing demand for low-noise tactical operations and lightweight autonomous mission capability to drive growth

- 17.3.3 HYBRID ELECTRIC

- 17.3.3.1 Increasing demand for extended endurance with low-signature operational capability to drive growth

- 17.4 FUEL CELL

- 17.4.1 INCREASING DEMAND FOR LONG-ENDURANCE LOW-SIGNATURE OPERATIONS AND NEXT-GENERATION ENERGY-EFFICIENT PROPULSION TO DRIVE GROWTH

- 17.4.1.1 Use case: Hydrogen fuel cell ISR drone by Doosan Mobility Innovation

- 17.4.1 INCREASING DEMAND FOR LONG-ENDURANCE LOW-SIGNATURE OPERATIONS AND NEXT-GENERATION ENERGY-EFFICIENT PROPULSION TO DRIVE GROWTH

18 MILITARY DRONES MARKET, BY REGION (MARKET SIZE & FORECAST TO 2031, USD MILLION)

- 18.1 INTRODUCTION

- 18.2 NORTH AMERICA

- 18.2.1 US

- 18.2.1.1 Overview

- 18.2.1.2 Key driver: AI-enabled autonomous warfare expansion

- 18.2.1.3 Use case: MQ-9B SkyGuardian expansion for multi-domain ISR

- 18.2.2 CANADA

- 18.2.2.1 Overview

- 18.2.2.2 Key driver: Arctic ISR & Northern Sovereignty Monitoring

- 18.2.2.3 Use case: MQ-9B SkyGuardian RPAS for Arctic Surveillance

- 18.2.1 US

- 18.3 EUROPE

- 18.3.1 UK

- 18.3.1.1 Overview

- 18.3.1.2 Key driver: Protector RG Mk1 strategic ISR deployment

- 18.3.1.3 Use case: Protector RG Mk1 Operational Integration Program

- 18.3.2 FRANCE

- 18.3.2.1 Overview

- 18.3.2.2 Key driver: Domestic tactical UAV ecosystem development

- 18.3.2.3 Use case: Safran Patroller tactical reconnaissance platform

- 18.3.3 GERMANY

- 18.3.3.1 Overview

- 18.3.3.2 Key driver: European battlefield intelligence modernization

- 18.3.3.3 Use case: German Heron TP for long-endurance reconnaissance

- 18.3.4 SWEDEN

- 18.3.4.1 Overview

- 18.3.4.2 Key driver: Nordic Security & NATO Readiness Programs

- 18.3.4.3 Use case: Saab-linked tactical ISR for Nordic reconnaissance

- 18.3.5 ITALY

- 18.3.5.1 Overview

- 18.3.5.2 Key driver: Mediterranean maritime ISR expansion

- 18.3.5.3 Use case: Leonardo Falco Xplorer for maritime surveillance

- 18.3.6 REST OF EUROPE

- 18.3.6.1 Overview

- 18.3.6.2 Key driver: Tactical battlefield ISR & loitering munition expansion

- 18.3.6.3 Use case: Warmate & FPV battlefield drone operations

- 18.3.1 UK

- 18.4 ASIA PACIFIC

- 18.4.1 CHINA

- 18.4.1.1 Overview

- 18.4.1.2 Key driver: Autonomous maritime surveillance expansion

- 18.4.1.3 Use case: Wing Loong Series for South China Sea monitoring

- 18.4.2 INDIA

- 18.4.2.1 Overview

- 18.4.2.2 Key driver: Indigenous drone manufacturing & border ISR

- 18.4.2.3 Use case: Nagastra-1R loitering munition for Indian Army operations

- 18.4.3 JAPAN

- 18.4.3.1 Overview

- 18.4.3.2 Key driver: East China Sea ISR & maritime monitoring

- 18.4.3.3 Use case: RQ-4B Global Hawk for wide-area maritime ISR

- 18.4.4 AUSTRALIA

- 18.4.4.1 Overview

- 18.4.4.2 Key driver: Indo-Pacific maritime drone coordination

- 18.4.4.3 Use case: MQ-4C Triton for Indo-Pacific maritime surveillance

- 18.4.5 SOUTH KOREA

- 18.4.5.1 Overview

- 18.4.5.2 Key driver: Counter-North Korea ISR readiness

- 18.4.5.3 Use case: KUS-FS MALE UAV for Korean Peninsula surveillance

- 18.4.6 REST OF ASIA PACIFIC

- 18.4.6.1 Overview

- 18.4.6.2 Key driver: Maritime ISR & asymmetric warfare modernization

- 18.4.6.3 Use case: Taiwan Albatross UAV & Southeast Asian maritime ISR operations

- 18.4.1 CHINA

- 18.5 MIDDLE EAST

- 18.5.1 SAUDI ARABIA

- 18.5.1.1 Overview

- 18.5.1.2 Key driver: Defense localization under Vision 2030

- 18.5.1.3 Use case: Saqr Tactical UAV for border and ISR missions

- 18.5.2 UAE

- 18.5.2.1 Overview

- 18.5.2.2 Key driver: Domestic combat UAV manufacturing expansion

- 18.5.2.3 Use case: ANAVIA HT-100 and HT-750 rotary-wing UAV procurement

- 18.5.3 ISRAEL

- 18.5.3.1 Overview

- 18.5.3.2 Key driver: Combat-proven ISR & loitering systems

- 18.5.3.3 Use case: Hermes 900 for persistent ISR and border surveillance

- 18.5.4 TURKEY

- 18.5.4.1 Overview

- 18.5.4.2 Key driver: Global export success of combat UAV platforms

- 18.5.4.3 Use case: Bayraktar Akinci for long-endurance strike and ISR

- 18.5.1 SAUDI ARABIA

- 18.6 LATIN AMERICA

- 18.6.1 BRAZIL

- 18.6.1.1 Overview

- 18.6.1.2 Key driver: Amazon Border ISR & anti-smuggling operations

- 18.6.1.3 Use case: Hermes 450 for Amazon Border monitoring

- 18.6.2 MEXICO

- 18.6.2.1 Overview

- 18.6.2.2 Key driver: Counter-cartel surveillance modernization

- 18.6.2.3 Use case: Tactical Quadrotor ISR for border and route monitoring

- 18.6.1 BRAZIL

- 18.7 AFRICA

- 18.7.1 SOUTH AFRICA

- 18.7.1.1 Overview

- 18.7.1.2 Key driver: ISR modernization for regional security operations

- 18.7.1.3 Use case: Milkor 380 MALE UAV for African ISR missions

- 18.7.2 NIGERIA

- 18.7.2.1 Overview

- 18.7.2.2 Key driver: Counter-insurgency UAV deployment expansion

- 18.7.2.3 Use case: Bayraktar TB2 for counter-insurgency ISR and strike support

- 18.7.1 SOUTH AFRICA

19 COMPETITIVE LANDSCAPE

- 19.1 INTRODUCTION

- 19.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2026

- 19.3 REVENUE ANALYSIS, 2021-2025

- 19.4 MARKET SHARE ANALYSIS, 2025

- 19.5 BRAND/PRODUCT COMPARISON

- 19.6 COMPANY VALUATION AND FINANCIAL METRICS, 2026

- 19.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 19.7.1 STARS

- 19.7.2 EMERGING LEADERS

- 19.7.3 PERVASIVE PLAYERS

- 19.7.4 PARTICIPANTS

- 19.7.5 COMPANY FOOTPRINT, KEY PLAYERS, 2025

- 19.7.5.1 Company footprint

- 19.7.5.2 Region footprint

- 19.7.5.3 Payload capacity footprint

- 19.7.5.4 Endurance footprint

- 19.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 19.8.1 PROGRESSIVE COMPANIES

- 19.8.2 RESPONSIVE COMPANIES

- 19.8.3 DYNAMIC COMPANIES

- 19.8.4 STARTING BLOCKS

- 19.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 19.8.5.1 List of startups/SMEs

- 19.8.5.2 Competitive benchmarking of startups/SMEs

- 19.9 COMPETITIVE SCENARIO

- 19.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 19.9.2 DEALS

- 19.9.3 OTHER DEVELOPMENTS

20 COMPANY PROFILES

- 20.1 KEY PLAYERS

- 20.1.1 NORTHROP GRUMMAN

- 20.1.1.1 Business overview

- 20.1.1.2 Products/Solutions offered

- 20.1.1.3 Recent developments

- 20.1.1.3.1 Product launches/developments

- 20.1.1.3.2 Deals

- 20.1.1.3.3 Other developments

- 20.1.1.4 MnM view

- 20.1.1.4.1 Key strengths

- 20.1.1.4.2 Strategic choices

- 20.1.1.4.3 Weaknesses and competitive threats

- 20.1.2 RTX

- 20.1.2.1 Business overview

- 20.1.2.2 Products/Solutions offered

- 20.1.2.3 Recent developments

- 20.1.2.3.1 Product launches/developments

- 20.1.2.3.2 Deals

- 20.1.2.3.3 Other developments

- 20.1.2.4 MnM view

- 20.1.2.4.1 Key strengths

- 20.1.2.4.2 Strategic choices

- 20.1.2.4.3 Weaknesses and competitive threats

- 20.1.3 ISRAEL AEROSPACE INDUSTRIES

- 20.1.3.1 Business overview

- 20.1.3.2 Products/Solutions offered

- 20.1.3.3 Recent developments

- 20.1.3.3.1 Product launches/developments

- 20.1.3.3.2 Deals

- 20.1.3.3.3 Other developments

- 20.1.3.4 MnM view

- 20.1.3.4.1 Key strengths

- 20.1.3.4.2 Strategic choices

- 20.1.3.4.3 Weaknesses and competitive threats

- 20.1.4 GENERAL ATOMICS

- 20.1.4.1 Business overview

- 20.1.4.2 Products/Solutions offered

- 20.1.4.3 Recent developments

- 20.1.4.3.1 Product launches/developments

- 20.1.4.3.2 Deals

- 20.1.4.3.3 Other developments

- 20.1.4.4 MnM view

- 20.1.4.4.1 Key strengths

- 20.1.4.4.2 Strategic choices

- 20.1.4.4.3 Weaknesses and competitive threats

- 20.1.5 TELEDYNE FLIR LLC

- 20.1.5.1 Business overview

- 20.1.5.2 Products/Solutions offered

- 20.1.5.3 Recent developments

- 20.1.5.3.1 Product launches/developments

- 20.1.5.3.2 Deals

- 20.1.5.3.3 Other developments

- 20.1.5.4 MnM view

- 20.1.5.4.1 Key strengths

- 20.1.5.4.2 Strategic choices

- 20.1.5.4.3 Weaknesses and competitive threats

- 20.1.6 AEROVIRONMENT, INC.

- 20.1.6.1 Business overview

- 20.1.6.2 Products/Solutions offered

- 20.1.6.3 Recent developments

- 20.1.6.3.1 Product launches/developments

- 20.1.6.3.2 Deals

- 20.1.6.3.3 Other developments

- 20.1.7 AIRBUS

- 20.1.7.1 Business overview

- 20.1.7.2 Products/Solutions offered

- 20.1.7.3 Recent developments

- 20.1.7.3.1 Product launches/developments

- 20.1.7.3.2 Deals

- 20.1.7.3.3 Other developments

- 20.1.8 TEXTRON INC.

- 20.1.8.1 Business overview

- 20.1.8.2 Products/Solutions offered

- 20.1.8.3 Recent developments

- 20.1.8.3.1 Product launches/developments

- 20.1.8.3.2 Deals

- 20.1.8.3.3 Other developments

- 20.1.9 LOCKHEED MARTIN CORPORATION

- 20.1.9.1 Business overview

- 20.1.9.2 Products/Solutions offered

- 20.1.9.3 Recent developments

- 20.1.9.3.1 Product launches/developments

- 20.1.9.3.2 Deals

- 20.1.9.3.3 Other developments

- 20.1.10 ELBIT SYSTEMS LTD.

- 20.1.10.1 Business overview

- 20.1.10.2 Products/Solutions offered

- 20.1.10.3 Recent developments

- 20.1.10.3.1 Product launches/developments

- 20.1.10.3.2 Deals

- 20.1.10.3.3 Other developments

- 20.1.11 BAE SYSTEMS

- 20.1.11.1 Business overview

- 20.1.11.2 Products/Solutions offered

- 20.1.11.3 Recent developments

- 20.1.11.3.1 Product launches/developments

- 20.1.11.3.2 Deals

- 20.1.11.3.3 Other developments

- 20.1.12 THALES

- 20.1.12.1 Business overview

- 20.1.12.2 Products/Solutions offered

- 20.1.12.3 Recent developments

- 20.1.12.3.1 Deals

- 20.1.12.3.2 Other developments

- 20.1.13 LEONARDO S.P.A.

- 20.1.13.1 Business overview

- 20.1.13.2 Products/Solutions offered

- 20.1.13.3 Recent developments

- 20.1.13.3.1 Product launches/developments

- 20.1.13.3.2 Deals

- 20.1.13.3.3 Other developments

- 20.1.14 KRATOS

- 20.1.14.1 Business overview

- 20.1.14.2 Products/Solutions offered

- 20.1.14.3 Recent developments

- 20.1.14.3.1 Product launches/developments

- 20.1.14.3.2 Deals

- 20.1.14.3.3 Other developments

- 20.1.15 BAYKAR TECH

- 20.1.15.1 Business overview

- 20.1.15.2 Products/Solutions offered

- 20.1.15.3 Recent developments

- 20.1.15.3.1 Product launches/developments

- 20.1.15.3.2 Deals

- 20.1.15.3.3 Other developments

- 20.1.1 NORTHROP GRUMMAN

- 20.2 OTHER PLAYERS

- 20.2.1 SHIELD AI

- 20.2.2 ANDURIL INDUSTRIES

- 20.2.3 SKYDIO, INC.

- 20.2.4 AUTERION LLC

- 20.2.5 GRIFFON AEROSPACE

- 20.2.6 XTEND

- 20.2.7 ROBOTICAN LTD.

- 20.2.8 BLUEBIRD

- 20.2.9 PERCEPTO LTD.

- 20.2.10 IDEAFORGE TECHNOLOGY LTD.

21 RESEARCH METHODOLOGY

- 21.1 RESEARCH DATA

- 21.1.1 SECONDARY DATA

- 21.1.1.1 Key data from secondary sources

- 21.1.2 PRIMARY DATA

- 21.1.2.1 Primary interview participants

- 21.1.2.2 Key data from primary sources

- 21.1.2.3 Breakdown of primary interviews

- 21.1.1 SECONDARY DATA

- 21.2 MARKET SIZE ESTIMATION

- 21.2.1 BOTTOM-UP APPROACH

- 21.2.2 TOP-DOWN APPROACH

- 21.2.3 BASE NUMBER CALCULATION

- 21.3 DATA TRIANGULATION

- 21.4 FACTOR ANALYSIS

- 21.4.1 SUPPLY-SIDE INDICATORS

- 21.4.2 DEMAND-SIDE INDICATORS

- 21.5 RESEARCH ASSUMPTIONS

- 21.6 RESEARCH LIMITATIONS

- 21.7 RISK ASSESSMENT

22 IMPACT OF GEOPOLITICAL CONFLICTS ON MILITARY DRONES MARKET

- 22.1 EVOLUTION OF MODERN WARFARE AND RISE OF DRONE-CENTRIC OPERATIONS

- 22.1.1 SHIFT FROM CONVENTIONAL TO ASYMMETRIC WARFARE

- 22.1.2 ROLE OF DRONES IN RECENT CONFLICTS (UKRAINE, MIDDLE EAST, AND OTHERS)

- 22.1.3 TACTICAL VS. STRATEGIC DRONE USAGE EVOLUTION

- 22.2 REGIONAL HOTSPOTS AND DEFENSE SPENDING REALIGNMENT

- 22.2.1 EUROPE (RUSSIA-UKRAINE IMPACT)

- 22.2.2 MIDDLE EAST (ISRAEL-IRAN DYNAMICS)

- 22.2.3 ASIA PACIFIC (CHINA-TAIWAN TENSIONS)

- 22.2.4 BUDGET SHIFTS TOWARD UAV PROCUREMENT

- 22.3 ACCELERATION OF PROCUREMENT, LOCALIZATION, AND SUPPLY CHAIN RECONFIGURATION

- 22.3.1 URGENT PROCUREMENT CYCLES

- 22.3.2 INDIGENOUS DRONE PROGRAMS (INDIA, TURKEY, AND OTHERS)

- 22.3.3 SUPPLY CHAIN DECOUPLING (CHINA VS. WEST)

- 22.4 EMERGENCE OF LOW-COST, HIGH-IMPACT DRONE STRATEGIES (LOITERING & SWARM SYSTEMS)

- 22.4.1 RISE OF LOITERING MUNITIONS

- 22.4.2 COST ASYMMETRY IN WARFARE

- 22.4.3 SWARM DRONE STRATEGIES

- 22.5 CONCLUSION

23 APPENDIX

- 23.1 DISCUSSION GUIDE

- 23.2 ANNEXURE

- 23.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 23.4 CUSTOMIZATION OPTIONS

- 23.5 RELATED REPORTS

- 23.6 AUTHOR DETAILS