|

시장보고서

상품코드

2059330

동물용 구충제 세계 시장 : 유형별, 동물 유형별, 최종사용자별, 지역별 - 예측(-2031년)Animal Parasiticides Market by Type (Ectoparasiticide, Endoparasiticide, Endectocide, Spray, Feed Additives), Animal Type (Dog, Cat, Horse, Cattle, Pig, Poultry), End user (Hospital, Animal farm, Home Care Setting) & Region - Global Forecast to 2031 |

||||||

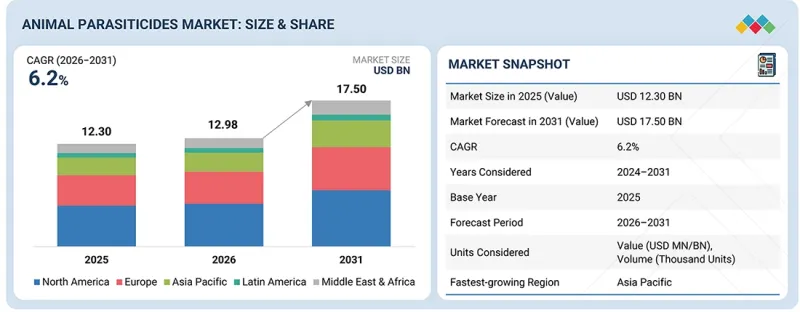

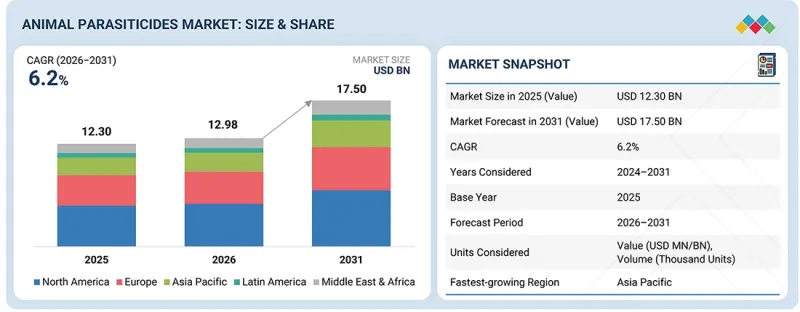

동물용 구충제 시장 규모는 2026년 129억 8,000만 달러에서 2031년까지 175억 달러로 성장하여 CAGR은 6.2%를 나타낼 것으로 예측됩니다.

이러한 성장은 장기 작용형 치료 솔루션과 수의학 분야의 정밀한 기생충 관리 등, 기생충 예방의 미래를 형성하는 몇 가지 주요 요인에 의해 주도되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 유형별, 동물 유형별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

동물용 구충제 시장에서 가장 중요한 성장 요인 중 하나는 수의학 전문가들이 기생충 구제의 정확성, 신속성 및 지속성을 높이기 위해 노력함에 따라, 보다 효과적이고 표적화된 예방적 기생충 구제 전략에 대한 수요가 증가하고 있다는 점입니다. 반려동물 헬스케어 업계 동향이 데이터 기반이자 위험 중심의 접근 방식을 통한 기생충 대책으로 지속적으로 진화함에 따라, 정밀한 투여, 내성 대책, 그리고 연중 보호를 지원할 수 있는 고품질 기생충 구제제에 대한 수요가 높아지고 있습니다. 이는 애널리틱스와 디지털 헬스 플랫폼의 활용에 힘입어 더욱 가속화되고 있으며, 혁신적이고 안전한 기생충 구제 제품에 대한 수요를 창출하고 있습니다.

기생충 감염, 매개성 질환, 그리고 노화에 따른 반려동물의 취약성이 계속해서 증가하고 있기 때문에 반려동물 주인들은 즉각적이고 효과적이며 장기적으로 지속되는 해결책을 시급히 찾고 있습니다. 수의사들은 첨단 경구제, 외용제 및 주사제를 사용하여 더 많은 환자를 치료하는 동시에, 환자의 추적 관찰 필요성을 줄임으로써 더 나은 치료 결과를 달성하고 있습니다. 심각해지는 기생충의 내성 문제와 환경 내 기생충 오염 문제로 인해, 과학자들은 연구 개발을 위해 새로운 유효 성분이나 복합 기생충 구제제의 개발을 서둘러야 하는 상황에 놓여 있습니다.

서방형 주사제, 장시간 작용형 경구 씹어 먹는 제제, 개선된 외용 제제 등의 제제 과학 및 투여 시스템의 발전은 효능, 사용 편의성 및 복약 순응도를 향상시키기 위해 시장을 주도하고 있습니다. 이러한 발전으로 인해 효과적인 예방 치료가 가능해졌고, 치료의 공백이 메워지며 실제 임상에서의 성과가 향상됨에 따라, 동물용 구충제 시장에서 혁신적인 솔루션의 지속적인 개발과 도입이 가속화되고 있습니다.

“동물 유형별로는 예측 기간 동안 반려동물 부문이 가축 부문보다 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다.” '

반려동물 부문은 반려동물 소유자 수 증가, 반려동물의 ‘인간화’ 추세, 그리고 예방 수의학에 대한 지출 확대에 힘입어 동물용 구충제 시장에서 높은 성장률을 보일 것으로 예측됩니다. 기생충 매개 질환에 대한 인식이 높아진 데 더해, 연중 내내 벼룩, 진드기, 심장사상충을 예방하고, 혁신적인 장시간 작용형 기생충 구제제 제품의 보급이 이 부문 수요를 더욱 부추기고 있습니다.

“최종 사용자별로는 2025년에 동물병원 및 진료소 부문이 가장 큰 시장 점유율을 차지했습니다.” '

2025년, 동물병원 및 진료소 부문이 동물용 구충제 시장을 독점한 것은 이러한 시설들이 진단 및 처방 능력을 바탕으로 기생충 구제 치료를 제공하는 주요 거점 역할을 했기 때문입니다. 반려동물 주인과 축산 농가들은 전문적인 제품 조언과 예방 관리 솔루션을 제공해 주는 수의사에 의존하고 있으며, 이로 인해 동물병원 및 클리닉에서의 기생충 구제제 판매가 증가하고 있습니다. 처방전이 필요한 제품과 첨단 지속형 제품의 조합은 물론, 정기 검진 및 예방 관리에 대한 수요가 증가함에 따라 동물병원 및 클리닉은 시장에서 주요 유통 및 치료 채널로서의 입지를 확고히 다졌습니다.

“라틴아메리카는 예측 기간 동안 가장 높은 성장률을 보일 것으로 예측됩니다. '

예측 기간 동안 라틴아메리카는 동물용 구충제 시장에서 가장 빠르게 성장하는 지역 시장이 될 것으로 전망됩니다. 이 지역의 높은 시장 성장률은 축산 규모의 확대, 반려동물 사육 마릿수 증가, 그리고 기생충 예방 및 동물 건강에 대한 인식 제고에서 기인한 것으로 보입니다. 해당 지역의 기후로 인해 일년내내 기생충 서식에 적합한 환경이 조성되고, 수의학 서비스 이용 기회가 확대되며, 최신 기생충 구제제 사용이 증가하는 것 등이 모두 라틴아메리카 시장 성장을 가속화하는 요인입니다.

조사 범위

본 시장 조사는 동물용 구충제 시장의 다양한 부문을 대상으로 하고 있습니다. 본 조사는 유형, 대상 동물, 최종 사용자 및 지역별로 이 시장 규모와 성장 잠재력을 추정하는 것을 목적으로 합니다. 또한, 시장 내 주요 기업에 대한 상세한 경쟁 분석 외에도 각 기업프로파일, 제품 유형, 사업 내용에 관한 주요 관찰 사항, 최근 동향, 주요 시장 전략에 대해서도 수록했습니다.

이 보고서를 구매해야 하는 이유

본 보고서는 기존 기업과 신생·중소기업이 시장 동향을 파악하고, 더 큰 시장 점유율을 확보하는 데 도움이 될 것입니다. 본 보고서를 입수한 기업은 아래에 개략적으로 설명된 5가지 전략 중 1가지 이상을 실행할 수 있습니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다.

- 주요 촉진요인(반려동물 사육 마릿수 증가, 예방적 동물 의료에 대한 관심 고조, 외부 기생충 및 내부 기생충의 확산), 제약 요인(식용 동물에 대한 살충제 잔류물에 대한 엄격한 규제, 프리미엄 제품 및 복합 살충제 제품의 높은 비용), 기회(장시간 작용형, 복합형 및 새로운 투여 경로의 구충제 개발, 신흥 시장에서의 구충제 보급 확대), 과제(기존 유효 성분에 대한 기생충의 내성 증가, 엄격한 규제 승인 절차, 지역별 규정 준수 요건의 차이)에 대해 분석하여, 동물용 구충제 시장의 성장에 영향을 미치는 요인을 밝히고 있습니다.

- 제품 개발/혁신 : 동물용 구충제 시장의 향후 기술 동향 및 신제품 출시에 관한 상세한 분석.

- 시장 개발: 수익성이 높은 신흥 시장에 대한 종합적인 정보. 본 보고서에서는 지역별, 제품 유형별 각종 동물용 구충제 시장 동향을 분석했습니다.

- 시장의 다양화: 동물용 구충제 시장의 제품, 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보.

- 경쟁 분석 : 동물용 구충제 시장에서 주요 기업의 시장 점유율, 전략, 제품, 유통망 및 생산 능력에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI 도입에 의한 전략적 파괴

제7장 고객 현황과 구매 행동

제8장 지속가능성과 규제 상황

제9장 동물용 구충제 시장(유형별)

제10장 동물용 구충제 시장(동물 유형별)

제11장 동물용 구충제 시장(최종사용자별)

제12장 동물 구충제 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

LSH 26.06.25The animal parasiticides market is expected to grow from USD 12.98 billion in 2026 to USD 17.50 billion by 2031, at a CAGR of 6.2%. This growth is driven by several key factors shaping the future of parasite prevention, including long-acting treatment solutions and precision-driven parasite management in veterinary care.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | By Type, Animal Type, End User, Region |

| Regions covered | North America, Europe, APAC, LATAM, MEA |

One of the most significant driving forces in the animal parasiticides market is the growing demand for more effective, targeted, and preventive parasite control strategies as veterinary healthcare professionals work to improve the accuracy, speed, and longevity of parasite control. As the trend in the companion animal healthcare industry continues to evolve to a data-driven and risk-based approach to parasite control, there is an increasing demand for high-quality parasiticides that can support precision dosing, resistance, and year-round protection. This has been further fueled by the use of analytics and digital health platforms, thus creating a demand for innovative and safe parasiticide products.

Pet owners face urgent demand for fast-acting, effective, and long-lasting solutions because parasite infestations, vector-borne diseases, and age-related pet vulnerability keep increasing in frequency. Veterinarians use advanced oral, topical, and injectable products to treat more patients while achieving better treatment results through reduced need for patient follow-ups. The rising parasite resistance problem and environmental parasite contamination issue compel scientists to develop new active ingredients and combination parasiticides for their research.

Formulation science and delivery system advancements, such as extended-release injectables, long-acting oral chewables, and enhanced topical formulations, are driving the market as they enhance efficacy, ease of use, and compliance. Such advancements enable effective preventive treatment, close treatment gaps, and improve real-world outcomes, thus accelerating the ongoing development and adoption of innovative solutions in the animal parasiticides market.

"By animal type, the companion animals segment is projected to exhibit a higher CAGR than the livestock segment during the forecast period."

The companion animals segment is expected to experience a high growth rate in the animal parasiticides market because of the rising number of pet owners, the increasing humanization of pets, and increased expenditures on preventive veterinary care. The growing awareness of parasite-borne diseases, combined with the strong adoption of year-round flea, tick, and heartworm prevention and innovative long-acting parasiticide products, has also fueled demand in this segment.

"By end user, the veterinary hospitals & clinics segment accounted for the largest market share in 2025."

In 2025, the veterinary hospitals & clinics segment dominated the animal parasiticides market because these facilities served as the main center for parasite control treatment delivery through their diagnostic and prescription capabilities. Pet owners and livestock producers depend on veterinarians to deliver expert product advice and preventive care solutions, which leads to increased sales of parasiticides at veterinary clinics. The combination of prescription-only products and advanced long-acting products, together with rising demand for routine check-ups and preventive care, has established veterinary hospitals and clinics as the primary distribution and treatment channel in the market.

"Latin America is expected to witness the highest growth rate during the forecast period."

Latin America is projected to be the fastest-growing regional market for animal parasiticides during the forecast period. The region's high market growth can be attributed to the expansion of livestock production, the increase in companion animal ownership, and a growing awareness of parasite prevention and animal health. Year-round favorable parasite living conditions due to the region's climate, enhanced availability of veterinary services, and increased use of modern parasiticide products are all factors that are speeding up the market growth in the Latin American region.

Breakdown of supply-side primary interviews:

- By Company Type: Tier 1 (60%), Tier 2 (30%), and Tier 3 (10%)

- By Designation: C-level Executives (30%), Directors (50%), and Other Designations (20%)

- By Region: North America (45%), Europe (15%), Asia Pacific (25%), Latin America (10%), and the Middle East & Africa (5%)

Breakdown of demand-side primary interviews:

- By End User: Veterinary Hospitals & Clinics (50%), Animal Farms (33%), and Home Care Settings (17%)

By Designation: Veterinarian/Chief Veterinary Officer (47%), Procurement/Purchasing Manager (22%), Head of Animal Health / Farm Manager (15%), and Others (16%)

- By Region: North America (25%), Europe (24%), Asia Pacific (25%), Latin America (11%), and the Middle East & Africa (15%)

Research Coverage

The market study covers the animal parasiticides market in various segments. It aims to estimate the size and growth potential of this market by type, animal type, end user, and region. The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report can assist established companies and newer or smaller firms in understanding market trends, enabling them to capture a larger market share. Firms that acquire the report can implement one or more of the five strategies outlined below.

This report provides insights into the following points:

- Analysis of key drivers (rising pet ownership and increased focus on preventive animal healthcare and growing prevalence of ecto- and endoparasites), restraints (strict regulations on parasiticide residues in food-producing animals and high cost of premium and combination parasiticide products), opportunities (development of long-acting, combination, and novel-delivery parasiticides and expansion of parasiticide adoption in emerging markets), and challenges (increasing parasite resistance to existing active ingredients and stringent regulatory approval processes and varying regional compliance requirements) influencing the growth of the animal parasiticides market.

- Product Development/Innovation: Detailed insights on upcoming technologies and product launches in the animal parasiticides market.

- Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of animal parasiticide products across regions.

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the animal parasiticides market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the animal parasiticides market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY

- 1.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN ANIMAL PARASITICIDES MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ANIMAL PARASITICIDES MARKET OVERVIEW

- 3.2 ASIA PACIFIC: ANIMAL PARASITICIDES MARKET, BY TYPE AND COUNTRY (2025)

- 3.3 ANIMAL PARASITICIDES MARKET: REGIONAL GROWTH OPPORTUNITIES

- 3.4 ANIMAL PARASITICIDES MARKET: REGION (2026-2031)

- 3.5 ANIMAL PARASITICIDES MARKET: DEVELOPED VS. DEVELOPING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing zoonotic & vector-borne disease burden, creating mandatory treatment

- 4.2.1.2 Expanding companion animal population and pet ownership

- 4.2.1.3 Increasing demand for animal-derived food products

- 4.2.2 RESTRAINTS

- 4.2.2.1 Growing resistance to parasiticides

- 4.2.2.2 Stringent regulatory approval processes for veterinary drugs

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 High growth potential of emerging economies

- 4.2.4 CHALLENGES

- 4.2.4.1 Uneven regulatory approval timelines across key markets, creating access inequalities

- 4.2.4.2 Balancing animal welfare, productivity, and compliance requirements

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKET AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCE ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 GDP, CURRENT PRICES (BILLIONS OF U.S. DOLLARS)

- 5.2.4 GDP: CURRENT PRICES (USD BILLION)

- 5.2.5 TRENDS IN GLOBAL ANIMAL HEALTHCARE INDUSTRY

- 5.2.6 TRENDS IN GLOBAL ANIMAL PARASITICIDES INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF ANIMAL PARASITICIDES, BY KEY PLAYER, 2023-2025

- 5.5.1.1 Average selling price trend of ectoparasiticides, by key player, 2023-2025

- 5.5.1.2 Average selling price trend of endoparasiticides, by key player, 2023-2025

- 5.5.1.3 Average selling price trend of endectocides, by key player, 2023-2025

- 5.5.2 AVERAGE SELLING PRICE TREND OF ANIMAL PARASITICIDES, BY REGION, 2023-2025

- 5.5.2.1 Average selling price trend of pour-on ectoparasiticides (USD per standard treatment unit), by region, 2023-2025

- 5.5.2.2 Average selling price trend of spray ectoparasiticides (USD per standard treatment unit), by region, 2023-2025

- 5.5.2.3 Average selling price trend of tablet ectoparasiticides (USD per standard treatment unit), by region, 2023-2025

- 5.5.2.4 Average selling price trend of endoparasiticide oral solids (USD per standard treatment unit), by region, 2023-2025

- 5.5.2.5 Average selling price trend of injectable endectocides (USD per standard treatment unit), by region, 2023-2025

- 5.5.1 AVERAGE SELLING PRICE TREND OF ANIMAL PARASITICIDES, BY KEY PLAYER, 2023-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT DATA FOR HS CODE 30, 2021-2025

- 5.6.2 IMPORT SCENARIO (HS CODE 30)

- 5.6.3 EXPORT DATA FOR HS CODE 30, 2021-2025

- 5.6.4 EXPORT SCENARIO (HS CODE 30)

- 5.7 KEY CONFERENCES AND EVENTS IN 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 CASE STUDY 1: BROAD-SPECTRUM COMBINATION ECTOPARASITICIDE + ENDOPARASITICIDE (ZOETIS - SIMPARICA TRIO)

- 5.10.2 CASE STUDY 2: FIRST BROAD-SPECTRUM FELINE TOPICAL ENDECTOCIDE (BOEHRINGER INGELHEIM - NEXGARD COMBO)

- 5.10.3 CASE STUDY 3: BROADEST-SPECTRUM CANINE ORAL PARASITICIDE WITH FOUR ACTIVE INGREDIENTS (ELANCO - CREDELIO QUATTRO)

- 5.11 ANIMAL PARASITICIDES MARKET: IMPACT OF 2025 US TARIFF

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.5 IMPACT ON END USERS

- 5.11.5.1 Veterinary hospitals & clinics

- 5.11.5.2 Home care settings

- 5.11.5.3 Animal farms

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Long-acting/Extended-release parasiticides

- 6.1.1.2 Novel multi-parasite combination therapies

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Immunomodulators for host-assisted parasitic control

- 6.1.2.2 Nanobiosensors and rapid diagnostics for parasitic detection

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Entomopathogenic Fungi (EPF) for ticks and ectoparasites

- 6.1.3.2 Precision livestock farming sensors and wearables

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.3 PATENT ANALYSIS

- 6.3.1 PUBLICATION TRENDS FOR ANIMAL PARASITICIDES

- 6.3.1.1 Insights on patent publication trends, top applicants and jurisdiction for animal parasiticides, january 2015-may 2026

- 6.3.2 LIST OF MAJOR PATENTS, 2023-2026

- 6.3.1 PUBLICATION TRENDS FOR ANIMAL PARASITICIDES

- 6.4 FUTURE APPLICATIONS

- 6.4.1 PRECISION LIVESTOCK HEALTH MANAGEMENT

- 6.4.2 ONCOLOGY AND CHRONIC DISEASE MANAGEMENT

- 6.4.3 REPRODUCTIVE AND FERTILITY ENHANCEMENT IN LIVESTOCK

- 6.4.4 INTEGRATED DISEASE SURVEILLANCE AND OUTBREAK CONTROL

- 6.5 IMPACT OF AI/GENERATIVE AI ON ANIMAL PARASITICIDES MARKET

- 6.5.1 INTRODUCTION

- 6.5.2 MARKET POTENTIAL IN ANIMAL PARASITICIDES ECOSYSTEM

- 6.5.3 AI USE CASES

- 6.5.4 KEY COMPANIES IMPLEMENTING AI IN ANIMAL PARASITICIDES MARKET

7 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 7.1 DECISION-MAKING PROCESS

- 7.2 KEY STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 7.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 7.2.2 BUYING CRITERIA

- 7.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 7.4 UNMET NEEDS IN VARIOUS END-USE SETTINGS

- 7.4.1 VETERINARY HOSPITALS & CLINICS

- 7.4.2 LIVESTOCK FARMS

- 7.4.3 HOME CARE SETTINGS

- 7.5 MARKET PROFITABILITY

- 7.5.1 PRODUCT INNOVATION AND DIFFERENTIATION

- 7.5.2 EXPANSION OF COMPANION ANIMAL HEALTHCARE SPENDING

- 7.5.3 OPERATIONAL SCALE AND DISTRIBUTION EFFICIENCY

8 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 8.1 REGULATORY LANDSCAPE

- 8.1.1 REGULATORY FRAMEWORK

- 8.1.1.1 North America

- 8.1.1.2 Europe

- 8.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.3 INDUSTRY STANDARDS

- 8.1.3.1 VICH Guidelines (International Cooperation on Harmonization of Technical Requirements for Registration of Veterinary Medicinal Products)

- 8.1.3.2 Good Manufacturing Practice (GMP) Standards - PIC/S Guide (PE 009 series)

- 8.1.3.3 Codex Alimentarius Standards for Veterinary Drug Residues (CXM 2 - Maximum Residue Limits)

- 8.1.1 REGULATORY FRAMEWORK

- 8.2 SUSTAINABILITY INITIATIVES

- 8.2.1 ENERGY-EFFICIENT MANUFACTURING & CARBON REDUCTION IN ANIMAL PARASITICIDES MARKET

- 8.2.2 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

- 8.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

9 ANIMAL PARASITICIDES MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 ECTOPARASITICIDES

- 9.2.1 POUR-ONS & SPOT-ONS

- 9.2.1.1 Ease of application and broad spectrum activity to drive continued adoption

- 9.2.1.2 Global volume analysis of pour-ons & spot-ons, 2024-2031 (Thousand Units)

- 9.2.2 ORAL TABLETS

- 9.2.2.1 High medication compliance and ease of administration to drive market

- 9.2.2.2 Global Volume Analysis of oral tablets, 2024-2031 (Thousand Units)

- 9.2.3 SPRAYS

- 9.2.3.1 Low price and convenience to drive market in emerging economies and livestock sector

- 9.2.3.2 Global Volume Analysis of sprays, 2024-2031 (Thousand Units)

- 9.2.4 DIPS

- 9.2.4.1 High popularity ensures sustained end-user demand

- 9.2.4.2 Global Volume Analysis of DIPS, 2024-2031 (Thousand Units)

- 9.2.5 EAR TAGS

- 9.2.5.1 High effectiveness in controlling flies around cattle drives market

- 9.2.5.2 Global Volume Analysis of ear tags, 2024-2031 (Thousand Units)

- 9.2.6 COLLARS

- 9.2.6.1 Growing prevalence of infections in companion animals to drive adoption

- 9.2.6.2 Global Volume Analysis of collars market, 2024-2031 (Thousand Units)

- 9.2.7 OTHER ECTOPARASITICIDES

- 9.2.1 POUR-ONS & SPOT-ONS

- 9.3 ENDOPARASITICIDES

- 9.3.1 ORAL LIQUIDS

- 9.3.1.1 Broad-spectrum activity to drive adoption across young animals and intensive livestock systems

- 9.3.1.2 Global volume analysis of oral liquids, 2024-2031 (Thousand Units)

- 9.3.2 ORAL SOLIDS

- 9.3.2.1 Emergence of internal parasitic infections in dogs to drive market

- 9.3.2.2 Global volume analysis of oral solids, 2024-2031 (Thousand Units)

- 9.3.3 INJECTABLES

- 9.3.3.1 Global volume analysis of injectables, 2024-2031 (Thousand Units)

- 9.3.3.2 Standard/Short-acting injectables

- 9.3.3.2.1 Veterinary preference for fast-acting injectable formulations in acute parasitic infections drives market growth

- 9.3.3.3 Long-acting/Extended-release injectables

- 9.3.3.3.1 Emergence of internal parasitic infections in dogs to drive market

- 9.3.4 FEED ADDITIVES

- 9.3.4.1 Can be administered to large number of animals at once

- 9.3.4.2 Global volume analysis of feed additives, 2024-2031 (Thousand Units)

- 9.3.5 OTHER ENDOPARASITICIDES

- 9.3.1 ORAL LIQUIDS

- 9.4 ENDECTOCIDES

- 9.4.1 ORAL ENDECTOCIDES

- 9.4.1.1 Growing pet owner preference for systemic all-in-one protection to accelerate oral endectocide demand

- 9.4.1.2 Global volume analysis of oral endectocides, 2024-2031 (Thousand Units)

- 9.4.2 INJECTABLE ENDECTOCIDES

- 9.4.2.1 Single-injection dual-action convenience underpins dominance in cattle and swine production systems

- 9.4.2.2 Global volume analysis of injectable endectocides, 2024-2031 (Thousand Units)

- 9.4.3 TOPICAL ENDECTOCIDES

- 9.4.3.1 Convenience, zero-injection compliance, and expanding multi-spectrum topical formulations sustain demand

- 9.4.3.2 Global volume analysis of topical endectocides, 2024-2031 (Thousand Units)

- 9.4.1 ORAL ENDECTOCIDES

10 ANIMAL PARASITICIDES MARKET, BY ANIMAL TYPE

- 10.1 INTRODUCTION

- 10.2 COMPANION ANIMALS

- 10.2.1 DOGS

- 10.2.1.1 Increasing adoption of dogs to drive market growth

- 10.2.2 CATS

- 10.2.2.1 Rising feline parasiticide adoption, low preventive compliance, and broad-spectrum product launches drive growth

- 10.2.3 HORSES

- 10.2.3.1 Higher risk of traumatic injuries in horses to drive demand

- 10.2.4 OTHER COMPANION ANIMALS

- 10.2.1 DOGS

- 10.3 LIVESTOCK ANIMALS

- 10.3.1 CATTLE

- 10.3.1.1 Gastrointestinal nematodes and tick-borne disease drive systemic endectocide and acaricide demand

- 10.3.2 PIG

- 10.3.2.1 Growing surgical volume for acute conditions in swine to drive market growth

- 10.3.3 POULTRY

- 10.3.3.1 Growing focus on infection prevention and flock health management propels growth

- 10.3.4 SHEEP & GOAT

- 10.3.4.1 Growth in consumption of sheep and goat meat to drive market

- 10.3.5 OTHER LIVESTOCK ANIMALS

- 10.3.1 CATTLE

11 ANIMAL PARASITICIDES MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 VETERINARY HOSPITALS & CLINICS

- 11.2.1 VETERINARY HOSPITALS & CLINICS TO DOMINATE MARKET DURING FORECAST PERIOD

- 11.3 ANIMAL FARMS

- 11.3.1 GROWING IMPORTANCE AND OPPORTUNITIES IN ON-FARM PARASITE MANAGEMENT

- 11.4 HOME CARE SETTINGS

- 11.4.1 RISING PET EXPENDITURE TO PROPEL MARKET GROWTH

12 ANIMAL PARASITICIDES MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 12.2.2 NORTH AMERICA: ANIMAL PARASITICIDES MARKET VOLUME ANALYSIS, BY PRODUCT TYPE, 2024-2031 (THOUSAND UNITS)

- 12.2.3 US

- 12.2.3.1 Surge in animal healthcare expenditure to boost market growth

- 12.2.4 CANADA

- 12.2.4.1 Growing pet ownership and increasing focus on preventive animal healthcare to drive market growth

- 12.3 EUROPE

- 12.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 12.3.2 EUROPE: ANIMAL PARASITICIDES MARKET VOLUME ANALYSIS, BY PRODUCT TYPE, 2024-2031 (THOUSAND UNITS)

- 12.3.3 GERMANY

- 12.3.3.1 Strong focus on animal welfare and advanced veterinary care to drive market growth

- 12.3.4 UK

- 12.3.4.1 Increasing pet ownership and rising animal healthcare spending to propel market growth

- 12.3.5 FRANCE

- 12.3.5.1 High standards of veterinary care and technological advancements to support market growth

- 12.3.6 ITALY

- 12.3.6.1 Growing pet ownership awareness and increasing livestock population to drive market growth

- 12.3.7 SPAIN

- 12.3.7.1 Increasing awareness regarding animal health to drive market growth

- 12.3.8 NETHERLANDS

- 12.3.8.1 Growing pet ownership and strong livestock sector to support market growth

- 12.3.9 SWEDEN

- 12.3.9.1 Growing companion animal care and advanced veterinary infrastructure supporting market growth

- 12.3.10 POLAND

- 12.3.10.1 Rapid expansion of poultry production and export-oriented farming increases demand

- 12.3.11 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 12.4.2 ASIA PACIFIC: ANIMAL PARASITICIDES MARKET VOLUME ANALYSIS, BY PRODUCT TYPE, 2024-2031 (THOUSAND UNITS)

- 12.4.3 CHINA

- 12.4.3.1 China to register highest growth rate during forecast period

- 12.4.4 JAPAN

- 12.4.4.1 Rising pet care expenditure and increasing adoption of companion animals to drive market growth

- 12.4.5 INDIA

- 12.4.5.1 Increasing livestock population to propel market growth

- 12.4.6 AUSTRALIA

- 12.4.6.1 Growing companion animal ownership and rise in animal health awareness to support market growth

- 12.4.7 SOUTH KOREA

- 12.4.7.1 Growing pet ownership to favor growth

- 12.4.8 THAILAND

- 12.4.8.1 Growing focus on livestock health and disease prevention to drive market growth

- 12.4.9 NEW ZEALAND

- 12.4.9.1 Growing pet ownership and focus on preventive animal healthcare to support market growth

- 12.4.10 REST OF ASIA PACIFIC

- 12.5 LATIN AMERICA

- 12.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 12.5.2 LATIN AMERICA: ANIMAL PARASITICIDES MARKET VOLUME ANALYSIS, BY PRODUCT TYPE, 2024-2031 (THOUSAND UNITS)

- 12.5.3 BRAZIL

- 12.5.3.1 Brazil to dominate Latin American market

- 12.5.4 MEXICO

- 12.5.4.1 Robust livestock base and growing companion animal care drive market

- 12.5.5 ARGENTINA

- 12.5.5.1 Expanding livestock production and increasing focus on disease prevention to drive market growth

- 12.5.6 REST OF LATIN AMERICA

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 12.6.2 MIDDLE EAST & AFRICA: ANIMAL PARASITICIDES MARKET VOLUME ANALYSIS, BY PRODUCT TYPE, 2024-2031 (THOUSAND UNITS)

- 12.7 GCC COUNTRIES

- 12.7.1 KINGDOM OF SAUDI ARABIA (KSA)

- 12.7.1.1 Market growth driven by Vision 2030 investments

- 12.7.2 UNITED ARAB EMIRATES (UAE)

- 12.7.2.1 Increasing focus on livestock health and companion animal care to support market growth

- 12.7.3 OTHER GCC COUNTRIES

- 12.7.4 REST OF MIDDLE EAST & AFRICA

- 12.7.1 KINGDOM OF SAUDI ARABIA (KSA)

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.1.1 KEY STRATEGIES ADOPTED BY PLAYERS IN ANIMAL PARASITICIDES MARKET

- 13.2 REVENUE ANALYSIS, 2023-2025

- 13.3 GLOBAL MARKET SHARE ANALYSIS, 2025

- 13.3.1 US ANIMAL PARASITICIDES MARKET SHARE ANALYSIS, 2025

- 13.3.2 EUROPE ANIMAL PARASITICIDES MARKET SHARE ANALYSIS, 2025

- 13.4 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.4.1 STARS

- 13.4.2 EMERGING LEADERS

- 13.4.3 PERVASIVE PLAYERS

- 13.4.4 PARTICIPANTS

- 13.4.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.4.5.1 Company footprint

- 13.4.5.2 Region footprint

- 13.4.5.3 Product type footprint

- 13.4.5.4 Animal type footprint

- 13.5 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.5.1 PROGRESSIVE COMPANIES

- 13.5.2 RESPONSIVE COMPANIES

- 13.5.3 DYNAMIC COMPANIES

- 13.5.4 STARTING BLOCKS

- 13.5.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.5.5.1 List of startups/SMEs

- 13.5.5.2 Competitive benchmarking of startups/SMEs

- 13.6 COMPANY VALUATION AND FINANCIAL METRICS

- 13.7 PRODUCT/BRAND COMPARISON

- 13.8 COMPETITIVE SITUATIONS & TRENDS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 ZOETIS INC.

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches & approvals

- 14.1.1.3.2 Expansions

- 14.1.1.3.3 Other developments

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 MERCK & CO., INC

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches & approvals

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 BOEHRINGER INGELHEIM INTERNATIONAL GMBH

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches & approvals

- 14.1.3.3.2 Deals

- 14.1.3.3.3 Expansions

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 ELANCO

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches & approvals

- 14.1.4.3.2 Expansions

- 14.1.4.3.3 Other developments

- 14.1.4.4 MnM view

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 VIRBAC

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches & approvals

- 14.1.5.3.2 Deal

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 CEVA

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Deals

- 14.1.6.3.2 Expansions

- 14.1.7 VETOQUINOL

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.8 NORBROOK

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches & approvals

- 14.1.8.3.2 Expansions

- 14.1.9 BIMEDA CORPORATE

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Product launches & approvals

- 14.1.9.3.2 Deals

- 14.1.9.3.3 Expansions

- 14.1.10 KYORITSU SEIYAKU CORPORATION

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.11 KRKA, D. D., NOVO MESTO

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.12 ECO - ANIMAL HEALTH LTD.

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.13 ALIVIRA ANIMAL HEALTH LIMITED

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.13.2.1 Recent developments

- 14.1.13.2.2 Deals

- 14.1.14 OUROFINO SAUDE ANIMAL

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.15 HEBEI VEYONG PHARMACEUTICAL CO., LTD.

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.1 ZOETIS INC.

- 14.2 OTHER PLAYERS

- 14.2.1 CHANELLE PHARMA

- 14.2.2 PETIQ LLC

- 14.2.3 HUVEPHARMA

- 14.2.4 CALIER

- 14.2.5 ABBEY LABS

- 14.2.6 BIOGENESIS BAGO

- 14.2.7 VETANCO SA

- 14.2.8 HESTER BIOSCIENCES LIMITED

- 14.2.9 BRILLIANT BIO PHARMA

- 14.2.10 ASHISH LIFE SCIENCE

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH APPROACH

- 15.2 RESEARCH METHODOLOGY DESIGN

- 15.2.1 SECONDARY RESEARCH

- 15.2.1.1 Key data from secondary sources

- 15.2.2 PRIMARY DATA

- 15.2.2.1 Key data from primary sources

- 15.2.2.2 Key industry insights

- 15.2.1 SECONDARY RESEARCH

- 15.3 MARKET SIZE ESTIMATION

- 15.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS (REVENUE SHARE ANALYSIS)

- 15.3.2 APPROACH 2: COMPANY PRESENTATIONS AND PRIMARY INTERVIEWS

- 15.3.3 APPROACH 3: DEMAND-SIDE ANALYSIS

- 15.3.4 APPROACH 4: TOP-DOWN APPROACH

- 15.3.5 APPROACH 5: BOTTOM-UP APPROACH

- 15.4 MARKET BREAKDOWN & DATA TRIANGULATION

- 15.5 MARKET SHARE ESTIMATION

- 15.6 RESEARCH ASSUMPTIONS

- 15.7 RISK ASSESSMENT

- 15.8 RESEARCH LIMITATIONS

- 15.8.1 METHODOLOGY-RELATED LIMITATIONS

- 15.8.2 SCOPE-RELATED LIMITATIONS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.3.1 PRODUCT ANALYSIS

- 16.3.2 COMPANY INFORMATION

- 16.3.3 GEOGRAPHIC ANALYSIS

- 16.3.4 COUNTRY-LEVEL VOLUME ANALYSIS BY PRODUCT

- 16.3.5 BY TYPE MARKET SHARE ANALYSIS (TOP 5 PLAYERS)

- 16.3.6 ANY CONSULT/CUSTOM REQUIREMENTS AS PER CLIENT REQUESTS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS