|

시장보고서

상품코드

2059333

정유 촉매 시장 예측(-2031년) : 유형(FCC 촉매, 수소화 처리 촉매, 수소화 분해 촉매, 접촉 개질 촉매), 성분(제올라이트, 금속, 화합물), 지역별Refinery Catalysts Market By Type (FCC Catalysts, Hydrotreating Catalysts, Hydrocracking Catalysts, Catalytic Reforming Catalysts), Ingredient (Zeolites, Metals, Chemical Compounds), and Region - Global Forecast to 2031 |

||||||

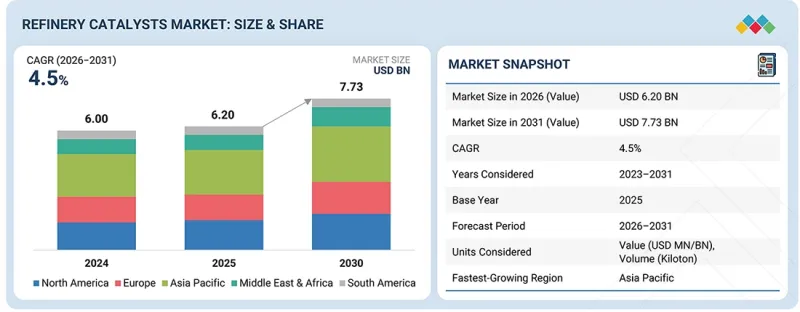

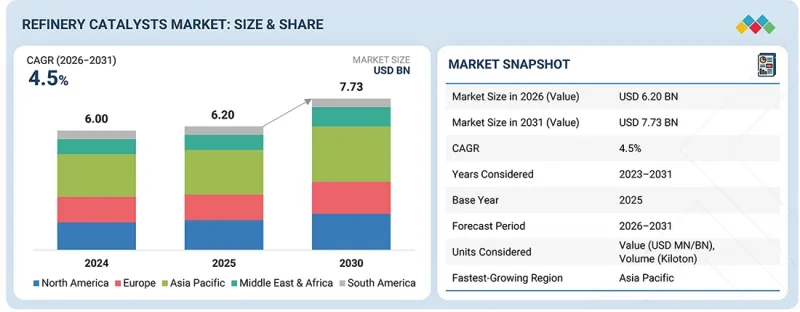

정유 촉매 시장 규모는 2026년 62억 달러에서 2031년에 77억 3,000만 달러로 성장하며, 예측 기간 중 CAGR은 4.5%에 달할 것으로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2023-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 유형, 성분, 지역 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미 |

제올라이트는 정유소용 촉매 분야에서 가장 빠르게 성장하고 있는 성분 중 하나입니다. 그 주요 이유는 높은 산도 및 규칙적인 다공성 구조에 있으며, 이러한 특성들이 탄화수소의 효율적인 전환을 촉진하기 때문입니다. 제올라이트의 높은 산도는 접촉 분해, 이성질화, 알킬화와 같은 주요 정유소 반응을 촉매하는 데 중요한 요소이며, 이러한 반응들은 정유소가 연료 품질 향상, 수율 효율 증대, 바람직하지 않은 부산물의 최소화를 도모하는 데 도움이 됩니다. 제올라이트의 분자 체 특성은 특히 고품질 연료나 석유화학 중간체의 제조 과정에서 선택적 반응에 매우 적합합니다.

또한 제올라이트는 뛰어난 열적 및 수열적 안정성을 갖추고 있으며, 고온이나 압력 변동과 같은 가혹한 산업 조건에서도 효과적으로 작동합니다. 이러한 안정성 덕분에 촉매 및 공정의 수명과 효율이 더욱 향상되며, 그 결과 산업 규모의 정유소 운영 비용을 최소화할 수 있습니다.

또한 제올라이트는 이온 교환이나 화학 처리를 통해 개질할 수 있으며, 특정 반응에 맞춰 기공 직경, 산도, 촉매 특성을 조절할 수 있습니다. 이러한 개질을 통해 보다 깨끗한 연료 생산 및 배기가스 제어 등 다양한 정유, 석유 및 환경 분야에서 제올라이트를 응용할 수 있게 됩니다.

"유형별로는 FCC 촉매가 예측 기간 중 금액 기준으로 가장 큰 시장 점유율을 차지할 것으로 보인다"

FCC(유동 접촉 분해) 촉매는 중질 탄화수소 분획을 분해하여 가솔린이나 분획 연료 등 더 가볍고 고부가가치인 제품을 생산하는 공정에서 중요한 역할을 수행하므로 시장에서 가장 큰 비중을 차지하고 있습니다. 이러한 촉매는 큰 탄화수소 분자를 더 작고 고부가가치가 높은 분자로 분해할 수 있게 하여 정유소의 효율을 높여줍니다.

또한 FCC 촉매는 정유소가 변화하는 연료 품질 규제 및 환경 규제를 준수하는 데에도 도움이 됩니다. 유황 불순물 저감, 옥탄가 향상, 질소산화물(NOx) 및 일산화탄소 배출 감축에 기여함으로써, 정유소가 변화하는 규제에 대응할 수 있도록 지원합니다. 이러한 촉매들이 가혹한 운전 조건에서도 전환 효율을 향상시키는 능력은 공정 성능의 최적화와 공정 안정성 유지에 기여합니다.

“지역별로는 북미가 예측 기간 중 금액 기준으로 정유소용 촉매 시장에서 2위를 차지할 것으로 보인다”

북미의 정유소에서는 효율 향상, 제품 생산량 극대화, 그리고 보다 깨끗한 연료에 관한 최신 환경 규제를 준수하기 위해 촉매 기술의 최신 발전을 점점 더 많이 도입하고 있습니다. 이 지역의 풍부한 석유 매장량과 확립된 정유 인프라는 정유소용 촉매 시장을 더욱 지원하고 있으며, 정유소가 환경 규제를 준수하면서도 고품질의 석유 제품을 효율적으로 생산할 수 있도록 하고 있습니다.

또한 운송용 연료 및 석유화학 원료에 대한 수요가 증가함에 따라 정유소는 공정 효율과 생산량을 극대화하기 위해 노력하고 있습니다. 촉매 기술의 발전은 정유소가 효율을 극대화하고, 황 함량을 최소화하며, 최신 환경 규제를 충족하는 데 있으며, 매우 중요한 역할을 하고 있습니다.

이 보고서에서는 전 세계 정유소용 촉매 시장을 조사하여, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 현황, 주요 기업 개요 등을 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 기술의 진보, AI의 영향, 특허, 혁신, 향후 응용

제6장 규제 상황과 지속가능성 구상

제7장 고객 상황과 구매 행동

제8장 정유 촉매 시장 : 유형별

제9장 정유 촉매 시장 : 원료별

제10장 정유 촉매 시장 : 지역별

제11장 경쟁 구도

제12장 기업 개요

제13장 조사 방법

제14장 부록

KSA 26.06.24The refinery catalysts market is projected to grow from USD 6.20 billion in 2026 to USD 7.73 billion by 2031, at a CAGR of 4.5% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Type, Ingredient, and Region |

| Regions covered | Europe, North America, Asia Pacific, the Middle East & Africa, and South America |

Zeolites are among the most rapidly expanding components in refinery catalysts, mainly because of their high acidity and ordered porous structure, which facilitates efficient hydrocarbon conversion. The high acidity of zeolites is a critical factor in catalyzing major refinery reactions such as catalytic cracking, isomerization, and alkylation, which help refiners enhance fuel quality, enhance yield efficiency, and minimize undesired by-products. The molecular sieve properties of zeolites make them highly suitable for selective reactions, especially in the production of premium fuels and petrochemical intermediates.

Moreover, zeolites have excellent thermal and hydrothermal stability, which enables them to function effectively under severe industrial conditions, such as high temperatures and pressure variations. This stability further improves the longevity and efficiency of the catalyst and the process, thereby minimizing costs in industrial-scale refinery operations.

Zeolites can also be modified by ion exchange and chemical treatments to adjust their pore size, acidity, and catalytic properties for specific reactions. This modification facilitates the application of zeolites in various petroleum refining, oil, and environmental applications, such as cleaner fuel production and emission control.

''Based on type, FCC catalysts is the largest market during the forecast period, in terms of value.''

FCC (Fluid Catalytic Cracking) catalysts are the largest segment in the refinery catalysts market, due to their importance in the cracking process of heavy hydrocarbon fractions to produce lighter and more valuable products such as gasoline and distillate fuels. These catalysts enable the cracking of large hydrocarbon molecules into smaller, more valuable ones, thereby improving refinery efficiency.

FCC catalysts also help refiners comply with changing fuel-quality and environmental regulations. They help reduce sulfur impurities, achieve higher octane numbers, and reduce nitrogen oxides (NOx) and carbon monoxide emissions, thus helping refineries comply with changing regulations. The ability of these catalysts to improve conversion efficiency under difficult operating conditions helps optimize process performance and maintain process stability.

"Based on region, North America is the second-largest market for refinery catalysts during the forecast period, in terms of value."

Refineries in North America are increasingly adopting the latest advances in catalyst technology to enhance efficiency, maximize product output, and meet the latest environmental regulations for cleaner fuels. The region's large oil reserves and established refining infrastructure further boost the market for refinery catalysts, enabling refineries to efficiently produce high-quality petroleum products while meeting environmental regulations.

Furthermore, the growing demand for transportation fuels and petrochemical feedstocks has led refineries to maximize process efficiency and output. Advances in catalyst technology are playing a crucial role in helping refineries maximize efficiency, minimize sulfur content, and meet the latest environmental regulations.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

- By Company Type- Tier 1- 60%, Tier 2- 20%, and Tier 3- 20%

- By Designation- C Level- 33%, Director Level- 33%, and Managers- 34%

- By Region- North America- 30%, Europe- 20%, Asia Pacific- 35%, Middle East & Africa- 5%, and South America- 10%

The report provides a comprehensive analysis of company profiles:

Prominent companies Albemarle Corporation (US), W. R. Grace (US), BASF (Germany), Haldor Topsoe (Denmark), Honeywell UOP (US), Clariant (Switzerland), Axens (France), Johnson Matthey (UK), China Petroleum and Chemical Corporation (Sinopec) (China), and Shell Catalyst & Technologies (Netherlands).

Research Coverage

This research report categorizes the refinery catalysts market by type (FCC, hydrotreating, hydrocracking, catalytic reforming), ingredient (zeolites, metals, chemical compounds), and region (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The scope of the report includes detailed information on the major factors influencing growth in the refinery catalysts market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted to provide insights into their business overviews, solutions, services, key strategies, contracts, partnerships, and agreements. Product launches, mergers and acquisitions, and recent developments in the refinery catalysts market are all covered. This report includes a competitive analysis of upcoming startups in the refinery catalysts market ecosystem.

Reasons to buy this report:

The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall refinery catalysts market and its subsegments. This report will help stakeholders understand the competitive landscape and gain insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Increasing demand for cleaner fuels, High octane number requirement, High refinery throughput and demand for fuel/petrochemicals), restraints (Energy transition reducing long term fuel demand, Precious group metal (PGM) price volatility), opportunities (Advanced catalyst innovation and customization, Backward integration by major refinery catalyst manufacturers), and challenges (Catalysts deactivation due to contaminants and coke formation, Feedstock variability and refinery complexity)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the refinery catalysts market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the refinery catalysts market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Albemarle Corporation (US), W. R. Grace (US), BASF (Germany), Haldor Topsoe (Denmark), Honeywell UOP (US), Clariant (Switzerland), Axens (France), Johnson Matthey (UK), China Petroleum and Chemical Corporation (Sinopec) (China), and Shell Catalyst & Technologies (Netherlands), among others in the refinery catalysts market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN REFINERY CATALYSTS MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN REFINERY CATALYSTS MARKET

- 3.2 REFINERY CATALYSTS MARKET, BY INGREDIENT, 2026 VS. 2031 (KILOTON)

- 3.3 REFINERY CATALYSTS MARKET, BY TYPE, 2026 VS. 2031 (KILOTON)

- 3.4 REFINERY CATALYSTS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing demand for cleaner fuels

- 4.2.1.2 High octane number requirement

- 4.2.1.3 High refinery throughput and demand for fuel/petrochemicals

- 4.2.2 RESTRAINTS

- 4.2.2.1 Energy transition reducing long-term fuel demand

- 4.2.2.2 Precious group metal (PGM) price volatility

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Advanced catalyst innovation and customization

- 4.2.3.2 Backward integration by major refinery catalyst manufacturers

- 4.2.4 CHALLENGES

- 4.2.4.1 Catalyst deactivation due to contaminants and coke formation

- 4.2.4.2 Feedstock variability and refinery complexity

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN REFINERY CATALYSTS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

- 4.7 PORTER'S FIVE FORCES ANALYSIS

- 4.7.1 THREAT OF SUBSTITUTES

- 4.7.2 BARGAINING POWER OF SUPPLIERS

- 4.7.3 THREAT OF NEW ENTRANTS

- 4.7.4 BARGAINING POWER OF BUYERS

- 4.7.5 INTENSITY OF COMPETITIVE RIVALRY

- 4.8 VALUE CHAIN ANALYSIS

- 4.8.1 RAW MATERIAL SUPPLIERS

- 4.8.2 MANUFACTURERS

- 4.8.3 DISTRIBUTORS

- 4.8.4 END USERS

- 4.9 ECOSYSTEM ANALYSIS

- 4.10 PRICING ANALYSIS

- 4.10.1 AVERAGE SELLING PRICE, BY REGION

- 4.10.2 AVERAGE SELLING PRICE, BY KEY PLAYER

- 4.10.3 AVERAGE SELLING PRICE

- 4.11 MACROECONOMIC INDICATORS

- 4.11.1 GLOBAL GDP TRENDS

- 4.11.2 GLOBAL OIL PRODUCTION

- 4.11.3 WORLD REFINERY CAPACITY

- 4.12 IMPACT OF 2025 US TARIFFS ON REFINERY CATALYSTS MARKET

- 4.12.1 INTRODUCTION

- 4.12.2 KEY TARIFF RATES

- 4.12.3 PRICE IMPACT ANALYSIS

- 4.12.4 IMPACT ON COUNTRIES/REGIONS

- 4.12.4.1 North America

- 4.12.4.2 Europe

- 4.12.4.3 Asia Pacific

- 4.12.5 IMPACT ON END-USE INDUSTRIES

- 4.13 TRADE ANALYSIS

- 4.13.1 IMPORT TRADE ANALYSIS: HS CODE 381511

- 4.13.2 EXPORT TRADE ANALYSIS: HS CODE 381511

- 4.13.3 IMPORT TRADE ANALYSIS: HS CODE 381512

- 4.13.4 EXPORT TRADE ANALYSIS: HS CODE 381512

- 4.13.5 IMPORT TRADE ANALYSIS: HS CODE 381519

- 4.13.6 EXPORT TRADE ANALYSIS: HS CODE 381519

- 4.14 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 4.15 INVESTMENT AND FUNDING SCENARIO

- 4.16 CASE STUDY

- 4.16.1 SELECTIVE CATALYTIC REDUCTION

- 4.16.2 BASF TECHNOLOGY CLEANS UP BOSTON'S BIG DIG PROJECT

- 4.17 KEY CONFERENCES & EVENTS

5 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 5.1 KEY EMERGING TECHNOLOGIES

- 5.1.1 FLUID CATALYTIC CRACKING CATALYSTS

- 5.1.2 HYDROPROCESSING CATALYSTS

- 5.2 COMPLEMENTARY TECHNOLOGIES

- 5.2.1 CATALYST REGENERATION TECHNOLOGIES

- 5.2.2 ADVANCED PROCESS CONTROL & DIGITAL OPTIMIZATION

- 5.3 ADJACENT TECHNOLOGIES

- 5.3.1 HYDROGEN PRODUCTION TECHNOLOGIES

- 5.3.2 EMISSIONS CONTROL TECHNOLOGIES

- 5.4 TECHNOLOGY/PRODUCT ROADMAP

- 5.4.1 SHORT-TERM (2026-2027)

- 5.4.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 5.4.3 LONG-TERM (2030-2035+)

- 5.5 PATENT ANALYSIS

- 5.5.1 INTRODUCTION

- 5.5.2 LEGAL STATUS OF PATENTS

- 5.5.3 JURISDICTION ANALYSIS

- 5.6 FUTURE APPLICATIONS

- 5.6.1 AI-DRIVEN CATALYST PERFORMANCE OPTIMIZATION SYSTEMS

- 5.6.2 ADVANCED CATALYST REGENERATION TECHNOLOGIES

- 5.6.3 NANOTECHNOLOGY-BASED CATALYST DEVELOPMENT

- 5.6.4 SMART REFINERY CATALYST MONITORING SYSTEMS

- 5.6.5 ADVANCED HYDROPROCESSING & CONVERSION TECHNOLOGIES

- 5.7 IMPACT OF AI/GEN AI ON REFINERY CATALYST MARKET

- 5.7.1 TOP USE CASES AND MARKET POTENTIAL

- 5.7.2 BEST PRACTICES IN REFINERY CATALYSTS MARKET

- 5.7.3 CASE STUDIES OF AI IMPLEMENTATION IN REFINERY CATALYSTS MARKET

- 5.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 5.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI REFINERY CATALYST MARKET

6 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 6.1 REGIONAL REGULATIONS AND COMPLIANCE

- 6.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.1.2 INDUSTRY STANDARDS

- 6.2 REGULATORY POLICY INITIATIVES

- 6.2.1 SAFETY PROTOCOLS

- 6.2.2 SUSTAINABLE DEVELOPMENT

- 6.2.3 STANDARDIZATION

- 6.2.4 CIRCULAR ECONOMY

- 6.3 SUSTAINABILITY INITIATIVES

- 6.3.1 MATERIAL PERFORMANCE, ENVIRONMENT, AND SAFETY INITIATIVES

- 6.3.1.1 Low-carbon materials and sustainable product strategies

- 6.3.1.2 Green refining & sustainable industrial applications

- 6.3.1 MATERIAL PERFORMANCE, ENVIRONMENT, AND SAFETY INITIATIVES

- 6.4 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

- 6.5 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

7 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 7.1 DECISION-MAKING PROCESS

- 7.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 7.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 7.2.2 BUYING CRITERIA

- 7.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 7.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 7.5 MARKET PROFITABILITY

- 7.5.1 REVENUE POTENTIAL

- 7.5.2 COST DYNAMICS

- 7.5.3 MARGIN OPPORTUNITIES IN KEY END-USE INDUSTRIES

8 REFINERY CATALYSTS MARKET, BY TYPE

- 8.1 INTRODUCTION

- 8.2 FCC CATALYSTS

- 8.2.1 USE OF FCCC DEPENDS ON QUALITY AND COMPOSITION OF CRUDE OIL

- 8.3 HYDROPROCESSING CATALYSTS

- 8.3.1 HYDROTREATING CATALYSTS

- 8.3.1.1 Essential in petroleum refining process

- 8.3.2 HYDROCRACKING CATALYSTS

- 8.3.2.1 Help convert heavy hydrocarbons into lighter, valuable products

- 8.3.1 HYDROTREATING CATALYSTS

- 8.4 CATALYTIC REFORMING CATALYSTS

- 8.4.1 DEMAND FOR HIGH OCTANE RATED PETROLEUM TO DRIVE MARKET

- 8.5 OTHER TYPES

- 8.5.1 ISOMERIZATION CATALYSTS

- 8.5.2 ALKYLATION CATALYSTS

- 8.5.3 HYDROGENATION CATALYSTS

- 8.5.4 DESULFURIZATION CATALYSTS

9 REFINERY CATALYSTS MARKET, BY INGREDIENT

- 9.1 INTRODUCTION

- 9.2 ZEOLITES

- 9.2.1 MOST COMMON INGREDIENT IN REFINING CATALYSTS

- 9.2.1.1 Natural zeolites

- 9.2.1.2 Synthetic zeolites

- 9.2.1 MOST COMMON INGREDIENT IN REFINING CATALYSTS

- 9.3 METALS

- 9.3.1 CRUCIAL ROLE IN PETROLEUM REFINING INDUSTRY

- 9.3.2 PRECIOUS METALS

- 9.3.2.1 Platinum

- 9.3.2.2 Palladium

- 9.3.2.3 Gold

- 9.3.3 RARE EARTH METALS

- 9.3.4 TRANSITION & BASE METALS

- 9.3.4.1 Molybdenum

- 9.3.4.2 Tungsten

- 9.3.4.3 Cobalt

- 9.3.4.4 Nickel

- 9.3.4.5 Iron

- 9.3.4.6 Zirconium

- 9.3.4.7 Manganese

- 9.3.4.8 Chromium

- 9.4 CHEMICAL COMPOUNDS

- 9.4.1 WIDELY USED IN ALKYLATION PROCESS

- 9.4.2 SULFURIC ACID & HYDROFLUORIC ACID

- 9.4.3 CALCIUM CARBONATE

- 9.4.4 ALUMINA

10 REFINERY CATALYSTS MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 US

- 10.2.1.1 FCC catalyst is essential for supply of transportation fuel

- 10.2.2 CANADA

- 10.2.2.1 Hydrocracking of heavy vacuum gas oils provides opportunity for market growth

- 10.2.3 MEXICO

- 10.2.3.1 Ultra-low sulfur fuel to drive market

- 10.2.1 US

- 10.3 ASIA PACIFIC

- 10.3.1 CHINA

- 10.3.1.1 Large FCC market to drive demand

- 10.3.2 JAPAN

- 10.3.2.1 High demand for high-quality jet fuels to drive market

- 10.3.3 INDIA

- 10.3.3.1 Massive oil refineries to drive market

- 10.3.4 SOUTH KOREA

- 10.3.4.1 Increased investments by major oil refining companies to drive market

- 10.3.5 REST OF ASIA PACIFIC

- 10.3.1 CHINA

- 10.4 EUROPE

- 10.4.1 RUSSIA

- 10.4.1.1 Government policies modernizing major refineries to drive market

- 10.4.2 GERMANY

- 10.4.2.1 Implementation of new government regulations to drive market

- 10.4.3 FRANCE

- 10.4.3.1 High demand for road transportation and aviation support market growth

- 10.4.4 UK

- 10.4.4.1 Rising demand for fuel to drive market

- 10.4.5 ITALY

- 10.4.5.1 Growth in bio-reactor sector to support market growth

- 10.4.6 SPAIN

- 10.4.6.1 Growth of oil refining industries to boost market growth

- 10.4.7 REST OF EUROPE

- 10.4.1 RUSSIA

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 GCC COUNTRIES

- 10.5.1.1 SAUDI ARABIA

- 10.5.1.1.1 High petroleum exports to drive market

- 10.5.1.2 Rest Of GCC Countries

- 10.5.1.1 SAUDI ARABIA

- 10.5.2 SOUTH AFRICA

- 10.5.2.1 Growth of petrochemical industry to drive market

- 10.5.3 REST OF MIDDLE EAST & AFRICA

- 10.5.1 GCC COUNTRIES

- 10.6 SOUTH AMERICA

- 10.6.1 BRAZIL

- 10.6.1.1 Adoption of advanced catalysts to enhance refinery efficiency to propel market

- 10.6.2 ARGENTINA

- 10.6.2.1 Requirement for high-octane gasoline to support market growth

- 10.6.3 REST OF SOUTH AMERICA

- 10.6.1 BRAZIL

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2026

- 11.3 REVENUE ANALYSIS, 2023-2025

- 11.4 MARKET SHARE ANALYSIS, 2025

- 11.5 COMPANY VALUATION AND FINANCIAL METRICS

- 11.6 BRAND/PRODUCT COMPARISON

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- 11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 11.7.5.1 Company footprint

- 11.7.5.2 Region footprint

- 11.7.5.3 Type footprint

- 11.7.5.4 Ingredient footprint

- 11.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2025

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- 11.8.5 COMPETITIVE BENCHMARKING, STARTUPS/SMES, 2025

- 11.8.5.1 Detailed list of key startups/SMEs

- 11.8.5.2 Competitive benchmarking of key startups/SMEs

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES

- 11.9.2 DEALS

- 11.9.3 EXPANSIONS

- 11.9.4 OTHER DEVELOPMENTS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 ALBEMARLE CORPORATION

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Solutions/Services offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches

- 12.1.1.3.2 Deals

- 12.1.1.3.3 Expansions

- 12.1.1.4 MnM view

- 12.1.1.4.1 Key strengths

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 W.R. GRACE & CO.

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Solutions/Services offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches

- 12.1.2.3.2 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Key strengths

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 BASF

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Solutions/Services offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and threats

- 12.1.4 TOPSOE

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Solutions/Services offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Expansions

- 12.1.4.4 MnM view

- 12.1.4.4.1 Key strengths

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses and competitive threats

- 12.1.5 HONEYWELL UOP

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Solutions/Services offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Deals

- 12.1.5.4 MnM view

- 12.1.5.4.1 Key strengths

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses and competitive threats

- 12.1.6 AXENS

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Solutions/Services offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches

- 12.1.6.3.2 Deals

- 12.1.6.3.3 Expansions

- 12.1.6.4 MnM view

- 12.1.7 CLARIANT

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Solutions/Services offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Product launches

- 12.1.7.3.2 Deals

- 12.1.7.3.3 Other developments

- 12.1.7.4 MnM view

- 12.1.8 JOHNSON MATTHEY

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Solutions/Services offered

- 12.1.8.3 MnM view

- 12.1.9 SHELL CATALYSTS & TECHNOLOGIES

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Solutions/Services offered

- 12.1.9.3 MnM view

- 12.1.10 CHINA PETROLEUM & CHEMICAL CORPORATION (SINOPEC)

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Solutions/Services offered

- 12.1.10.3 MnM view

- 12.1.11 ARKEMA

- 12.1.11.1 Business overview

- 12.1.11.2 Products/Solutions/Services offered

- 12.1.11.3 MnM view

- 12.1.12 CHEVRON CORPORATION

- 12.1.12.1 Business overview

- 12.1.12.2 Products/Solutions/Services offered

- 12.1.12.3 MnM view

- 12.1.13 EXXON MOBIL CORPORATION ARKEMA

- 12.1.13.1 Business overview

- 12.1.13.2 Products/Solutions/Services offered

- 12.1.13.3 MnM view

- 12.1.1 ALBEMARLE CORPORATION

- 12.2 OTHER PLAYERS

- 12.2.1 JGC CATALYSTS AND CHEMICALS LTD.

- 12.2.2 ANTENCHEM

- 12.2.3 DORF KETAL CHEMICALS (I) PVT. LTD.

- 12.2.4 REZEL CATALYSTS CORPORATION

- 12.2.5 KUWAIT CATALYST COMPANY

- 12.2.6 KNT GROUP

- 12.2.7 UNICAT CATALYST TECHNOLOGIES, LLC

- 12.2.8 N. E. CHEMCAT CORPORATION

- 12.2.9 GAZPROM

- 12.2.10 ZEOLYST INTERNATIONAL

- 12.2.11 QINGDAO HUICHENG ENVIRONMENTAL TECHNOLOGY CO., LTD

- 12.2.12 CHEMPACK

13 RESEARCH METHODOLOGY

- 13.1 RESEARCH DATA

- 13.1.1 SECONDARY DATA

- 13.1.1.1 Key data from secondary sources

- 13.1.2 PRIMARY DATA

- 13.1.2.1 Key data from primary sources

- 13.1.2.2 Primary interviews from demand and supply sides

- 13.1.2.3 Key industry insights

- 13.1.2.4 Breakdown of primary interviews

- 13.1.1 SECONDARY DATA

- 13.2 MARKET SIZE ESTIMATION

- 13.2.1 BOTTOM-UP APPROACH

- 13.2.2 TOP-DOWN APPROACH

- 13.3 FORECAST NUMBER CALCULATION

- 13.4 DATA TRIANGULATION

- 13.5 FACTOR ANALYSIS

- 13.6 ASSUMPTIONS

- 13.7 LIMITATIONS & RISKS ASSOCIATED WITH REFINERY CATALYSTS MARKET

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 RELATED REPORTS

- 14.4 AUTHOR DETAILS