|

시장보고서

상품코드

2059965

치과 임플란트 및 보철물 시장 예측(-2031년) : 제품(치과 임플란트(티타늄, 지르코늄), 치과보철물(브릿지, 크라운, 의치, 베니어, 인레이 및 온레이)), 최종사용자별(치과 병원 및 클리닉, 치과 기공소)Dental Implants and Prosthetics Market by Product [Dental Implants (Titanium, Zirconium), Dental Prosthetics (Bridges, Crowns, Dentures, Veneers, and Inlays & Onlays)], by End User (Dental Hospitals & Clinics, Dental Labs) - Global Forecast to 2031 |

||||||

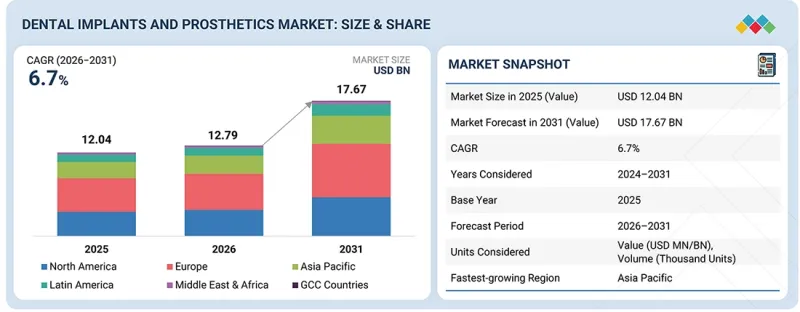

세계의 치과 임플란트 및 보철물 시장 규모는 2026년 127억 9,000만 달러에서 2031년에는 176억 7,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간 중 CAGR은 6.7%에 달할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 제품별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가 |

전 세계 치과 임플란트 및 보철물 시장은 예측 기간 중 상당한 성장이 예상됩니다. 이러한 성장은 주로 심미 치과에 대한 수요 증가와 치아 상실, 충치, 치주 질환 등 치과 질환의 유병률 상승에 힘입어 이루어지고 있습니다. 구강 미관에 대한 인식이 높아지고, 첨단 치과 치료에 대한 접근성이 개선되며, 가처분 소득이 증가함에 따라 점점 더 많은 환자들이 임플란트를 이용한 수복 치료를 선택하고 있습니다.

또한 고령 인구 증가와 디지털 치과 기술의 보급도 시장 확대를 지원하고 있습니다. CAD/CAM 시스템, 3D 프린팅, 최소 침습 임플란트 수술 등의 기술적 진보로 인해 치료 효율이 향상되고 환자의 치료 결과도 개선되면서, 이러한 제품들의 세계적 보급이 촉진되고 있습니다. 또한 신흥 국가내 치과 병원 및 숙련된 전문가의 증가, 치과 관광 활동의 확대 역시 시장 관계자들에게 더 큰 성장 기회를 제공하고 있습니다.

그러나 한편으로 시장은 예측 기간 중 몇 가지 과제에 직면할 가능성이 있습니다. 치과 임플란트, 보철 치료, 첨단 치과 의료 서비스와 관련된 고액의 비용은 인구의 상당 부분에게 경제적 부담이 되어, 이용을 제한하는 요인이 될 수 있습니다. 또한 특히 개발도상국에서는 치과 치료에 대한 미흡한 보상 정책과 제한적인 보험 적용 범위가 시장 성장을 어느 정도 저해할 것으로 예상됩니다.

제품 유형별로는 2025년에 치과 임플란트 부문이 시장에서 가장 큰 점유율을 차지했습니다.

치아 상실률의 증가, 지역을 불문하고 진행되는 고령화, 치과 기술의 발전에 따라 치과 임플란트에 대한 수요는 확대될 것으로 예상됩니다. 기술 혁신 덕분에 임플란트 수술은 훨씬 더 정확하고 효율적으로 변했으며, 환자에게 더욱 편리해졌습니다. 이러한 발전은 주로 3D 영상 진단, 구강내 스캐너, CAD/CAM 기술의 도입에 기인한 것으로, 이 기술들은 임플란트 식립 수술의 정확도와 성공률을 크게 향상시키고 있습니다. 또한 임플란트와 보철물을 같은 날 고정하는 즉시 하중 프로토콜은 보다 신속한 치료를 원하는 환자들을 중심으로 점점 더 널리 보급되고 있습니다. 치과 임플란트는 턱뼈에 단단히 고정되므로 기존의 틀니처럼 어긋나거나 헐거워지는 느낌이 들지 않습니다. 임플란트가 턱뼈와 일체화됨으로써, 인공 치아에 영구적이고 안정적인 지지력을 제공합니다. 이러한 일체형 구조 덕분에 자연스러운 씹기와 발음이 가능해질 뿐만 아니라, 탈부착식 틀니로 인한 불편함도 줄어듭니다. 또한 치과 임플란트는 뼈 조직을 자극하여 턱뼈의 건강을 유지하는 데 도움이 되며, 장기간 치아를 상실한 후 흔히 발생하는 뼈의 퇴화를 예방할 수 있습니다. 지르코니아나 티타늄 합금 등 신소재의 도입으로 임플란트의 내구성과 심미성도 향상되었습니다. 전반적으로 신소재와 기술의 지속적인 개발로 인해 임플란트의 효과, 내구성, 환자 만족도가 향상됨에 따라 치과 임플란트에 대한 수요는 더욱 증가할 것으로 예상됩니다.

최종사용자별로는 2025년에 치과 병원·클리닉 부문이 시장 점유율에서 가장 큰 비중을 차지했습니다.

이러한 우위는 임상 현장에서 이루어지는 치과 시술의 증가, 전문적인 치과 치료에 대한 환자의 선호도 상승, 그리고 치과의사들의 첨단 임플란트 및 수복 기술 도입 확대에 기인한 것으로 보입니다. 또한 민간 치과 병원의 확대, 숙련된 치과 전문가의 증가, 심미 치과 및 수복 치과 치료를 원하는 환자 방문 건수의 증가가 이 부문의 시장 입지를 더욱 공고히 하고 있습니다. 또한 이 부문은 의료 인프라의 개선, 구강 위생에 대한 의식의 향상, 환자 맞춤형 치료 솔루션 제공과 같은 요인들로부터도 혜택을 받고 있습니다. 또한 치과 병원 및 클리닉은 임플란트 수술, 보철물 장착, 경과 관찰, 디지털 치과 치료 절차에서 주요 진료 거점 역할을 수행하고 있으며, 이러한 요인들이 계속해서 이 부문의 성장을 주도하고 있습니다.

2025년, 유럽은 치과 임플란트 및 보철물 시장에서 가장 큰 점유율을 차지했습니다.

이 지역의 견고한 규제 체계, 고도로 발달한 의료 인프라, 고령화 인구가 치과 치료 시장의 성장에 기여하고 있습니다. 특히 서유럽은 가처분 소득이 높고 치과 의료 인프라가 잘 갖춰져 있으며, 시장 성장을 주도하고 있습니다. 치과 임플란트 및 보철물을 제조하는 많은 주요 기업이 이 지역에 거점을 두고 있습니다. 가처분 소득이 높은 인구가 많다는 점은 병원 및 치과에서 첨단 임플란트 솔루션의 도입을 촉진하며, 치과 임플란트 및 보철 분야에서 유럽의 선도적 지위를 더욱 공고히 하고 있습니다.

이 보고서에서는 전 세계 치과 임플란트 및 보철물 시장을 조사하여, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등을 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 상황 개요

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 치과 임플란트 및 보철물 시장 : 제품별

제10장 치과 임플란트 및 보철물 시장 : 최종사용자별

제11장 치과 임플란트 및 보철물 시장 : 지역별

제12장 경쟁 구도

제13장 기업 개요

제14장 조사 방법

제15장 부록

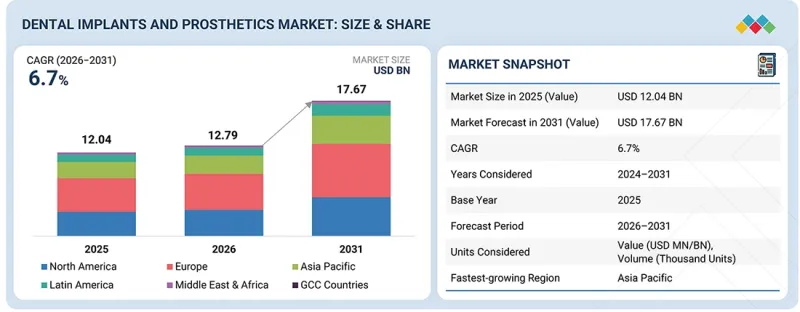

KSA 26.06.25The global dental implants and prosthetics market is projected to reach USD 17.67 billion by 2031 from USD 12.79 billion in 2026, at a CAGR of 6.7% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | By Product, End User, Region |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, the Middle East, and Africa, GCC Countries |

The global dental implants and prosthetics market is projected to grow significantly during the forecast period. This growth is primarily driven by the increasing demand for cosmetic dentistry and the rising prevalence of dental disorders, including tooth loss, dental caries, and periodontal diseases. Growing awareness of oral aesthetics, improved access to advanced dental treatments, and rising disposable incomes are encouraging more patients to choose implant-based restorative procedures.

Additionally, the expanding geriatric population and the increasing adoption of digital dentistry technologies are further supporting market expansion. Technological advancements, such as CAD/CAM systems, 3D printing, and minimally invasive implant procedures, are enhancing treatment efficiency and improving patient outcomes. This, in turn, is boosting the global adoption of these products. Furthermore, the growing number of dental clinics, skilled professionals, and dental tourism activities in emerging economies is creating additional growth opportunities for market players.

However, the market may encounter certain challenges during the forecast period. High costs associated with dental implants, prosthetic procedures, and advanced dental care services can limit affordability for a significant portion of the population. Additionally, inadequate reimbursement policies and limited insurance coverage for dental treatments-especially in developing regions-are expected to restrain market growth to some extent.

By product type, the dental implants segment accounted for the largest share of the market in 2025.

The market for dental implants and prosthetics is divided into two segments: dental implants and dental prosthetics. In 2025, the dental implants segment held the largest share of this market. The demand for dental implants is expected to grow due to rising tooth loss rates, an aging population across regions, and advancements in dental technology. Owing to technological innovations, implant procedures have become significantly more accurate, efficient, and user-friendly. This progress is primarily due to the introduction of 3D imaging, intraoral scanners, and CAD/CAM technology, which have greatly enhanced the precision and success rates of implant placement surgeries. Additionally, immediate loading protocols-where implants and restorations are fixed on the same day-are becoming increasingly popular, particularly among patients seeking quicker treatment options. Dental implants are anchored securely in the jawbone, ensuring they do not shift or feel loose like conventional dentures. As the implants fuse with the jawbone, they provide permanent and stable support for replacement teeth. This natural integration allows for seamless chewing and speaking, while also reducing the discomfort associated with removable dentures. Furthermore, dental implants help maintain jawbone health by stimulating bone tissue, which can prevent bone deterioration that often occurs after prolonged tooth loss. The introduction of new materials such as zirconia and titanium alloys has also made implants more durable and aesthetically pleasing. Overall, the ongoing development of new materials and technologies is expected to further increase the demand for dental implants, as they continue to improve in efficacy, longevity, and patient satisfaction.

By end user, the dental hospitals & clinics segment accounted for the largest share of the market in 2025.

The market for dental implants and prosthetics is categorized into three main end-user segments: dental hospitals & clinics, dental labs, and other end users. In 2025, dental hospitals & clinics held the largest share of the dental implants and prosthetics market. This dominance can be attributed to the increasing number of dental procedures performed in clinical settings, a rising patient preference for specialized dental care, and the growing adoption of advanced implant and restorative technologies by dental practitioners. Additionally, the expansion of private dental clinics, the increasing availability of skilled dental professionals, and a higher patient footfall for cosmetic and restorative dental treatments have further strengthened this segment's market position. The segment is also benefiting from improvements in healthcare infrastructure, increased awareness regarding oral health, and the availability of customized treatment solutions for patients. Moreover, dental hospitals & clinics serve as the primary point of care for implant surgeries, prosthetic fittings, follow-up consultations, and digital dentistry procedures, which continue to drive growth in this segment.

Europe held the largest share of the dental implants and prosthetics market in 2025.

Europe held the largest share of the market in 2025. The region's strong regulatory framework, highly developed healthcare infrastructure, and significant elderly population all contribute to the growth of dental treatments. Western Europe, in particular, leads market growth due to its higher disposable income and established dental infrastructure. Many leading companies that manufacture dental implants and prosthetics are based in this region. The large population with high disposable income encourages the adoption of advanced implant solutions in hospitals and dental clinics, further solidifying Europe's position as a leader in dental implants and prosthetics.

A breakdown of the primary participants (supply side) for the dental implants and prosthetics market referred to in this report is provided below:

- By Company Type: Tier 1 (30%), Tier 2 (35%), and Tier 3 (35%)

- By Designation: C-level Executives (20%), Directors (35%), and Others (45%)

- By Region: North America (30%), Europe (25%), Asia Pacific (20%), Latin America (20%), Middle East & Africa (2%), and GCC Countries (3%)

The prominent players in the global dental implants and prosthetics market are Institut Straumann AG (Switzerland), Envista (US), Dentsply Sirona (US), Henry Schein, Inc. (US), Osstem Implant Co., Ltd. (South Korea), Solventum (US), ZimVie Inc. (US), Glidewell (US), Ivoclar Vivadent (Liechtenstein), Avinent Science and Technology (Spain), Bicon (US), Adin Dental Implant Systems, Ltd. (Israel), Dio Implant Co., Ltd. (South Korea), Thommen Medical AG (Switzerland), Southern Implants (South Africa), Keystone Dental Inc. (US), BEGO GmbH & Co. KG (Germany), SDI Dental Implants (Germany), Dentium (South Korea), Bioline Dental Implants (Germany), DENTAURUM GmbH & Co. KG (Germany), MEGA'GEN IMPLANT CO., LTD. (South Korea), Sweden & Martina S.p.A. (Italy), Medigma Biomedical GmbH (Germany), and LYRA ETK (France).

Research Coverage:

The market study covers the dental implants and prosthetics market across various segments. It aims to estimate the market size and the growth potential of this market across different segments by product, dental implants market, dental prosthetics market and region. The study also includes an in-depth competitive analysis of the market's key players, along with their company profiles, key observations on their products and business offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will help market leaders/new entrants in this market by providing information on the closest approximations of revenue for the overall dental implants and prosthetics market and its subsegments. This report will help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (increasing patient pool for dental treatments, rising geriatric population and edentulism, rising demand for advanced cosmetic dental procedures, increasing demand for same-day dentistry, and growing consumer awareness and rising focus on aesthetics), restraints (high cost of dental implants and limited reimbursements and greater risk of tooth loss associated with dental bridges), opportunities (potential for growth in emerging countries and consolidation of dental practices and rising DSO activity), and challenges (dearth of trained dental practitioners and pricing pressure faced by prominent market players)

- Market Penetration: Comprehensive information on product portfolios offered by the top players in the global dental implants and prosthetics market. The report analyzes this market by product (dental implants and dental prosthetics), end user, and region.

- Product Enhancement/Innovation: Detailed insights on upcoming trends and product launches in the global dental implants and prosthetics market.

- Market Development: Comprehensive information on the lucrative emerging markets by product (dental implants and dental prosthetics), end user, and region.

- Market Diversification: Exhaustive information about new products and services, growing geographies, recent developments, and investments in the global dental implants and prosthetics market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product and service offerings, and capabilities of leading players in the global dental implants and prosthetics market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONS COVERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY MARKET PARTICIPANTS: INSIGHTS & DEVELOPMENTS

- 2.2 DISRUPTIVE TRENDS SHAPING MARKET GROWTH

- 2.3 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.4 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 DENTAL IMPLANTS AND PROSTHETICS MARKET OVERVIEW

- 3.2 ASIA PACIFIC: DENTAL IMPLANTS AND PROSTHETICS MARKET, BY PRODUCT AND COUNTRY, (2025)

- 3.3 DENTAL IMPLANTS AND PROSTHETICS MARKET, REGIONAL MIX, 2024-2031

- 3.4 DENTAL IMPLANTS AND PROSTHETICS MARKET: EMERGING VS. DEVELOPED ECONOMIES

- 3.5 DENTAL IMPLANTS AND PROSTHETICS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing patient pool for dental treatments

- 4.2.1.2 Increasing demand for advanced cosmetic dental procedures

- 4.2.1.3 Growing preference for same-day dentistry

- 4.2.1.4 Rising focus on aesthetics

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost of dental implants and limited reimbursements

- 4.2.2.2 Higher risk of tooth loss associated with dental bridges

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growth potential in emerging economies

- 4.2.3.2 Rapid growth of dental service organizations

- 4.2.4 CHALLENGES

- 4.2.4.1 Dearth of trained dental practitioners

- 4.2.4.2 Pricing pressure

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER- 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 THREAT OF NEW ENTRANTS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN DENTAL IMPLANTS AND PROSTHETICS MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF DENTAL IMPLANTS AND PROSTHETICS, BY KEY PLAYER, 2023-2025

- 5.6.2 AVERAGE SELLING PRICE TREND OF DENTAL IMPLANTS, BY REGION, 2023-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 TRADE ANALYSIS FOR DENTAL IMPLANT PRODUCTS

- 5.7.2 TRADE ANALYSIS FOR DENTAL PROSTHETIC PRODUCTS

- 5.8 KEY CONFERENCES & EVENTS, 2026-2027

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 CASE STUDY 1: SELF-DRILLING IMPLANTS FOR IMMEDIATE LOADING OF FULL-ARCH PROSTHESES

- 5.9.2 CASE STUDY 2: GUIDED SURGICAL APPROACH FOR PRECISE IMPLANT PLACEMENT

- 5.9.3 CASE STUDY 3: COMPLEX FULL-ARCH REHABILITATION USING MOLECULAR PRECISION IMPLANT SYSTEM

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 IMPACT OF 2025 US TARIFFS ON DENTAL IMPLANTS AND PROSTHETICS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON REGION

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USER INDUSTRIES

6 TECHNOLOGY LANDSCAPE

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 IMMEDIACY SOLUTIONS/IMMEDIATE LOADING

- 6.1.2 NOVEL BIOCOMPATIBLE MATERIALS

- 6.1.3 APICALLY TAPERED IMPLANTS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 IMPLANT COATINGS

- 6.2.1.1 Antibacterial coatings

- 6.2.1.2 Osseointegration-enhancing coatings

- 6.2.1.3 Combination coatings

- 6.2.2 OSSEOINTEGRATIVE SURFACE TECHNOLOGY

- 6.2.1 IMPLANT COATINGS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 CONE-BEAM COMPUTED TOMOGRAPHY

- 6.4 TECHNOLOGY/PRODUCT ROAD MAP

- 6.4.1 SHORT-TERM |RECENT TECHNOLOGIES| FOUNDATION & EARLY COMMERCIALIZATION

- 6.4.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.4.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.5 PATENT ANALYSIS

- 6.5.1 PATENT PUBLICATION TRENDS

- 6.5.2 JURISDICTION ANALYSIS

- 6.6 IMPACT OF AI/GEN AI ON DENTAL IMPLANTS AND PROSTHETICS MARKET

- 6.6.1 TOP USE CASES & MARKET POTENTIAL

- 6.6.2 INTERCONNECTED ADJACENT ECOSYSTEMS & IMPACT ON MARKET PLAYERS

- 6.6.3 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN DENTAL IMPLANTS AND PROSTHETICS MARKET

- 6.7 SUCCESS STORIES & REAL-WORLD APPLICATIONS

- 6.7.1 INSTITUT STRAUMANN: AI-DRIVEN DIGITAL WORKFLOW & SMILE DESIGN

- 6.7.2 DENTSPLY SIRONA: AI-POWERED CAD/CAM & SINGLE-VISIT DENTISTRY

7 REGULATORY LANDSCAPE

- 7.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2 INDUSTRY STANDARDS

- 7.2.1 NORTH AMERICA

- 7.2.1.1 US

- 7.2.1.2 Canada

- 7.2.2 EUROPE

- 7.2.3 ASIA PACIFIC

- 7.2.3.1 China

- 7.2.3.2 Japan

- 7.2.4 LATIN AMERICA

- 7.2.4.1 Brazil

- 7.2.4.2 Mexico

- 7.2.5 MIDDLE EAST

- 7.2.6 AFRICA

- 7.2.1 NORTH AMERICA

- 7.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS & BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

9 DENTAL IMPLANTS AND PROSTHETICS MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 DENTAL IMPLANTS

- 9.2.1 DENTAL IMPLANTS MARKET, BY MATERIAL

- 9.2.1.1 Titanium implants

- 9.2.1.1.1 Titanium implants, by procedure

- 9.2.1.1.1.1 Two-stage procedures

- 9.2.1.1.1.2 Single-stage procedures

- 9.2.1.1.2 Titanium implants, by connector

- 9.2.1.1.2.1 External hexagonal connectors

- 9.2.1.1.2.2 Internal hexagonal connectors

- 9.2.1.1.2.3 Internal octagonal connectors

- 9.2.1.1.1 Titanium implants, by procedure

- 9.2.1.2 Zirconium implants

- 9.2.1.2.1 Rising preference for aesthetic value to expedite growth

- 9.2.1.1 Titanium implants

- 9.2.2 DENTAL IMPLANTS MARKET, BY DESIGN

- 9.2.2.1 Tapered Implants

- 9.2.2.1.1 Increasing demand for bone-level tapered dental implants to aid growth

- 9.2.2.2 Parallel-walled implants

- 9.2.2.2.1 Increasing demand for long-term implant success and crestal bone preservation to drive growth

- 9.2.2.1 Tapered Implants

- 9.2.3 DENTAL IMPLANTS MARKET, BY TYPE

- 9.2.3.1 Root-form dental implants

- 9.2.3.1.1 Higher success rate and durability to support growth

- 9.2.3.2 Plate-form dental implants

- 9.2.3.2.1 Improved stability and bone preservation to support growth

- 9.2.3.1 Root-form dental implants

- 9.2.4 DENTAL IMPLANTS MARKET, BY PRICE

- 9.2.4.1 Premium implants

- 9.2.4.1.1 Increasing launches of technologically advanced implants to stimulate growth

- 9.2.4.2 Value implants

- 9.2.4.2.1 Rising number of manufacturers for value implants to support market growth

- 9.2.4.3 Discounted implants

- 9.2.4.3.1 Increasing cost-consciousness among patients to drive adoption

- 9.2.4.1 Premium implants

- 9.2.1 DENTAL IMPLANTS MARKET, BY MATERIAL

- 9.3 DENTAL PROSTHETICS

- 9.3.1 DENTAL PROSTHETICS MARKET, BY PRODUCT

- 9.3.1.1 Dental bridges

- 9.3.1.1.1 Dental bridges market, by type

- 9.3.1.1.1.1 3-unit bridges

- 9.3.1.1.1.2 4-unit bridges

- 9.3.1.1.1.3 Maryland bridges

- 9.3.1.1.1.4 Cantilever bridges

- 9.3.1.1.1 Dental bridges market, by type

- 9.3.1.2 Dental crowns

- 9.3.1.2.1 Rising popularity of modern dental crowns to propel growth

- 9.3.1.3 Dentures

- 9.3.1.3.1 Partial dentures

- 9.3.1.3.1.1 Booming geriatric population to propel market

- 9.3.1.3.2 Complete dentures

- 9.3.1.3.2.1 Growing advancements in 3D printing technology to fuel market

- 9.3.1.3.1 Partial dentures

- 9.3.1.4 Dental veneers

- 9.3.1.4.1 Increasing focus on dental aesthetics to contribute to growth

- 9.3.1.5 Dental inlays & onlays

- 9.3.1.5.1 Growing adoption of advanced technologies for fabrication to facilitate growth

- 9.3.1.1 Dental bridges

- 9.3.1 DENTAL PROSTHETICS MARKET, BY PRODUCT

10 DENTAL IMPLANTS AND PROSTHETICS MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 DENTAL HOSPITALS & CLINICS

- 10.2.1 RISING NUMBER OF DENTAL HOSPITALS & CLINICS IN EMERGING MARKETS TO DRIVE MARKET GROWTH

- 10.3 DENTAL LABS

- 10.3.1 INCREASING INTEREST IN COSMETIC DENTISTRY TO PROPEL MARKET GROWTH

- 10.4 OTHER END USERS

11 DENTAL IMPLANTS AND PROSTHETICS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 EUROPE

- 11.2.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 11.2.2 GERMANY

- 11.2.2.1 Export-oriented approach to contribute to growth

- 11.2.3 ITALY

- 11.2.3.1 Surging number of foreign patients to bolster growth

- 11.2.4 SPAIN

- 11.2.4.1 Growing dental tourism to propel market

- 11.2.5 FRANCE

- 11.2.5.1 Well-organized distribution network to expedite growth

- 11.2.6 UK

- 11.2.6.1 Rising awareness about dental health to favor growth

- 11.2.7 SWITZERLAND

- 11.2.7.1 Rising geriatric population to augment growth

- 11.2.8 REST OF EUROPE

- 11.3 NORTH AMERICA

- 11.3.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 11.3.2 US

- 11.3.2.1 Growing demand for technologically advanced dental implants and prosthetics to drive market

- 11.3.3 CANADA

- 11.3.3.1 Rising healthcare expenditure to spur growth

- 11.4 ASIA PACIFIC

- 11.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 11.4.2 SOUTH KOREA

- 11.4.2.1 High penetration of dental implants to support market

- 11.4.3 JAPAN

- 11.4.3.1 Rising geriatric population and favorable reimbursement scenario to support market growth

- 11.4.4 CHINA

- 11.4.4.1 Increasing number of specialized dental hospitals and clinics to sustain growth

- 11.4.5 INDIA

- 11.4.5.1 Growing dental tourism to support market

- 11.4.6 AUSTRALIA

- 11.4.6.1 Growing number of registered dental practitioners to sustain growth

- 11.4.7 REST OF ASIA PACIFIC

- 11.5 LATIN AMERICA

- 11.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 11.5.2 BRAZIL

- 11.5.2.1 High prevalence of partial edentulism to favor growth

- 11.5.3 ARGENTINA

- 11.5.3.1 Increasing demand for dental implants due to edentulism cases to drive market

- 11.5.4 MEXICO

- 11.5.4.1 Growing availability of skilled dentists to fuel market

- 11.5.5 REST OF LATIN AMERICA

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 EXPANDING NETWORK OF PRIVATE DENTAL CLINICS AND HOSPITALS TO AID GROWTH

- 11.6.2 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 11.7 GCC COUNTRIES

- 11.7.1 RISING NUMBER OF CONFERENCES, SYMPOSIA, SUMMITS, AND TRAINING COURSES TO SUPPORT MARKET GROWTH

- 11.7.2 MACROECONOMIC OUTLOOK FOR GCC COUNTRIES

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN DENTAL IMPLANTS AND PROSTHETICS MARKET

- 12.3 REVENUE ANALYSIS, 2021-2025

- 12.4 MARKET SHARE ANALYSIS, 2025

- 12.5 COMPANY VALUATION & FINANCIAL METRICS

- 12.5.1 COMPANY VALUATION

- 12.5.2 FINANCIAL METRICS

- 12.6 DENTAL IMPLANTS MARKET

- 12.6.1 BRAND/PRODUCT COMPARISON

- 12.7 DENTAL PROSTHETICS MARKET

- 12.7.1 BRAND/PRODUCT COMPARISON

- 12.8 COMPANY EVALUATION MATRIX (DENTAL IMPLANTS MARKET): KEY PLAYERS, 2025

- 12.8.1 STARS

- 12.8.2 EMERGING LEADERS

- 12.8.3 PERVASIVE PLAYERS

- 12.8.4 PARTICIPANTS

- 12.9 COMPANY EVALUATION MATRIX (DENTAL PROSTHETICS MARKET): KEY PLAYERS, 2025

- 12.9.1 STARS

- 12.9.2 EMERGING LEADERS

- 12.9.3 PERVASIVE PLAYERS

- 12.9.4 PARTICIPANTS

- 12.10 COMPANY EVALUATION MATRIX (DENTAL IMPLANTS MARKET): STARTUPS/SMES, 2025

- 12.10.1 PROGRESSIVE COMPANIES

- 12.10.2 RESPONSIVE COMPANIES

- 12.10.3 DYNAMIC COMPANIES

- 12.10.4 STARTING BLOCKS

- 12.10.5 COMPETITIVE BENCHMARKING

- 12.10.5.1 Detailed list of key startups/SMEs

- 12.10.5.2 Competitive benchmarking of key startups/SMEs

- 12.11 COMPANY EVALUATION MATRIX (DENTAL PROSTHETICS MARKET): STARTUPS/SMES 2025

- 12.11.1 PROGRESSIVE COMPANIES

- 12.11.2 RESPONSIVE COMPANIES

- 12.11.3 DYNAMIC COMPANIES

- 12.11.4 STARTING BLOCKS

- 12.11.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 12.11.5.1 Detailed list of key startups/SMEs

- 12.11.5.2 Competitive benchmarking of key startups/SMEs

- 12.11.6 DENTAL IMPLANTS AND PROSTHETICS MARKET: COMPANY FOOTPRINT

- 12.11.6.1 Company footprint

- 12.11.6.2 Region footprint

- 12.11.6.3 Product footprint

- 12.11.6.4 Material footprint

- 12.11.6.5 Type footprint

- 12.11.6.6 End-user footprint

- 12.12 DENTAL IMPLANTS AND PROSTHETICS MARKET: R&D EXPENDITURE

- 12.13 COMPETITIVE SCENARIO

- 12.13.1 PRODUCT LAUNCHES & APPROVALS

- 12.13.2 DEALS

- 12.13.3 EXPANSIONS

- 12.13.4 OTHER DEVELOPMENTS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 INSTITUT STRAUMANN AG

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Expansions

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses & competitive threats

- 13.1.2 ENVISTA

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches & approvals

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses & competitive threats

- 13.1.3 DENTSPLY SIRONA

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses & competitive threats

- 13.1.4 HENRY SCHEIN, INC.

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches

- 13.1.4.3.2 Deals

- 13.1.4.3.3 Expansions

- 13.1.4.3.4 Other developments

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses & competitive threats

- 13.1.5 OSSTEM IMPLANT CO., LTD.

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches & approvals

- 13.1.5.3.2 Deals

- 13.1.5.3.3 Expansions

- 13.1.5.3.4 Other developments

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses & competitive threats

- 13.1.6 SOLVENTUM

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Deals

- 13.1.7 ZIMVIE INC.

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches

- 13.1.7.3.2 Deals

- 13.1.7.3.3 Expansions

- 13.1.8 GLIDEWELL

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Product launches

- 13.1.8.3.2 Deals

- 13.1.9 LYRA ETK

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Product launches

- 13.1.9.3.2 Deals

- 13.1.10 MEDIGMA BIOMEDICAL GMBH

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.11 IVOCLAR VIVADENT

- 13.1.11.1 Business overview

- 13.1.11.2 Products offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Product launches

- 13.1.11.3.2 Deals

- 13.1.12 AVINENT SCIENCE AND TECHNOLOGY

- 13.1.12.1 Business overview

- 13.1.12.2 Products offered

- 13.1.13 BICON

- 13.1.13.1 Business overview

- 13.1.13.2 Products offered

- 13.1.14 ADIN DENTAL IMPLANT SYSTEMS LTD.

- 13.1.14.1 Business overview

- 13.1.14.2 Products offered

- 13.1.15 DIO IMPLANT CO., LTD.

- 13.1.15.1 Business overview

- 13.1.15.2 Products offered

- 13.1.1 INSTITUT STRAUMANN AG

- 13.2 OTHER PLAYERS

- 13.2.1 THOMMEN MEDICAL AG

- 13.2.2 SOUTHERN IMPLANTS

- 13.2.3 KEYSTONE DENTAL GROUP

- 13.2.4 BEGO GMBH & CO. KG

- 13.2.5 SWEDEN & MARTINA S.P.A

- 13.2.6 SDI DENTAL IMPLANTS

- 13.2.7 DENTIUM

- 13.2.8 MEGA'GEN IMPLANT CO., LTD.

- 13.2.9 BIOLINE DENTAL IMPLANTS

- 13.2.10 DENTAURUM GMBH & CO. KG

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY DATA

- 14.1.1.1 Key data from secondary sources

- 14.1.2 PRIMARY DATA

- 14.1.2.1 Key data from primary sources

- 14.1.2.2 Key industry insights

- 14.1.1 SECONDARY DATA

- 14.2 MARKET SIZE ESTIMATION

- 14.3 MARKET BREAKDOWN & DATA TRIANGULATION

- 14.4 MARKET SHARE ESTIMATION

- 14.5 RESEARCH ASSUMPTIONS

- 14.6 RESEARCH LIMITATIONS

- 14.6.1 SCOPE-RELATED LIMITATIONS

- 14.6.2 METHODOLOGY-RELATED LIMITATIONS

- 14.7 RISK ASSESSMENT

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS