|

시장보고서

상품코드

2059970

시험 및 계측 장비 시장 예측(-2032년) : 제품 유형별, 시스템 시험 레벨별, 시험 수명주기 스테이지별, 상용 모델별, 시험 유형별, 최종 용도 산업별, 지역별Test and Measurement Equipment Market by Product Type (Standalone Instruments, Modular Instrumentation, ATE), Testing Type, Commercial Model, End-Use Industry (Data Centers, Aerospace & Defense, Automotive) - Global Forecast to 2032 |

||||||

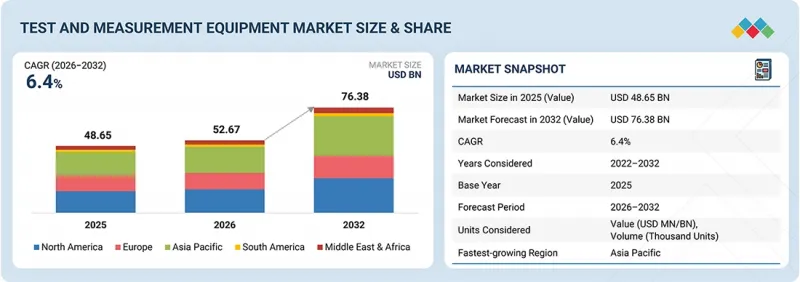

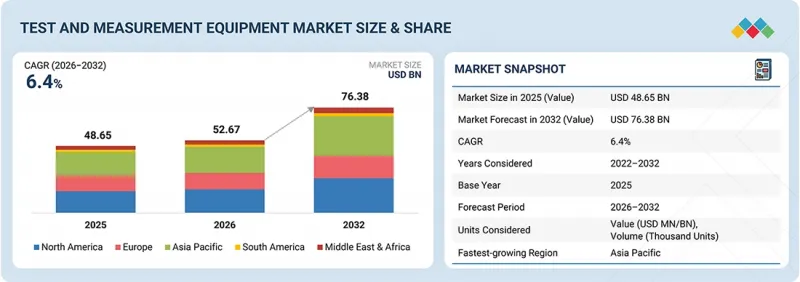

세계의 시험·계측 장비 시장 규모는 2026년 526억 7,000만 달러에서 2032년에는 763억 8,000만 달러로 확대하며, 예측 기간 중 CAGR 6.4%를 기록할 것으로 전망되고 있습니다.

이러한 성장은 반도체, 데이터센터, 전기자동차, 통신, 항공우주·방위, 그리고 산업 제조 등 각 분야에서 시험이 점점 더 복잡해짐에 따라 지원되고 있습니다. 자동 시험 장비, 모듈형 계측 기기, 소프트웨어 정의 시험 및 첨단 RF·마이크로파 검증 기술의 도입이 확대됨에 따라 시험의 속도, 정확도, 재현성 및 수명주기 커버리지가 향상되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품 유형별, 시스템 시험 레벨별, 시험 수명주기 스테이지별, 상용 모델별, 시험 유형별, 최종 용도 산업별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

그러나 첨단 시험 플랫폼의 높은 초기 비용, 긴 업데이트 주기, 통합의 복잡성, 그리고 장비의 노후화 위험이 여전히 시장의 주요 제약 요인으로 작용하고 있습니다.

"예측 기간 중 소프트웨어 테스트 부문이 가장 빠르게 성장할 것으로 예상된다"

시험 유형별로 살펴보면, 자동차, 통신, 데이터센터, 의료기기, 반도체, 산업용 자동화 등 각 분야의 제품이 점점 더 소프트웨어 주도형으로 전환됨에 따라 2026-2032년에 소프트웨어 테스트 부문은 놀라운 성장률을 보이고 있습니다. 임베디드 시스템, 커넥티드 디바이스, 클라우드 연동 인프라, 인공지능(AI) 워크로드, 첨단 운전자 지원 시스템(ADAS), 그리고 5G·6G 네트워크의 활용이 확대됨에 따라 성능, 신뢰성, 사이버 보안, 상호 운용성 및 시스템 동작에 대한 검증 수요가 증가하고 있습니다. 전기, RF, 기계 및 생산 검증 분야에서 물리적 계측기가 여전히 필수적이기 때문에 장비 시험은 여전히 더 큰 시장 점유율을 차지하고 있습니다. 그럼에도 불구하고 고객이 제품 수명 주기 전반에 걸친 하드웨어와 소프트웨어의 통합 검증을 요구함에 따라 소프트웨어 테스트는 더욱 탄력을 받고 있습니다.

“2032년에는 부품 시험 부문이 가장 큰 시장 점유율을 차지할 것으로 전망된다”

시스템 수준 시험 중에서는 구성 요소 시험 부문이 가장 큰 시장 점유율을 차지할 것으로 전망됩니다. 이는 개별 부품, 칩, 모듈, 센서, 회로, 커넥터, 배터리, RF 부품 및 기계적 요소가 더 큰 규모의 시스템에 통합되기 전에 검증되어야 하기 때문입니다. 이 시험 단계는 연구개발, 설계 검증, 생산, 현장 고장 분석 및 서비스 워크플로우를 통해 높은 재현성을 갖추고 있으며, T&M 장비에 대한 꾸준한 수요의 원동력이 되고 있습니다. 또한 자동차, 항공우주, 통신, 반도체, 의료 등의 업계에서는 시스템 전체의 인증에 앞서 기능 블록에 대한 검증을 수행하는 사례가 증가하고 있으므로, 하위 시스템 시험 역시 여전히 매우 중요합니다.

“2026년, 중국이 아시아·태평양 지역의 시험·측정 장비 시장에서 최대 점유율을 차지할 전망”

중국은 견고한 전자기기 제조 기반, 반도체 산업, 전기자동차 생산, 통신 인프라 및 산업 자동화 생태계에 힘입어 2026년에는 아시아태평양의 시험·측정 장비 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 이 국가의 주도적 지위는 국내 전자기기 생산 규모, 반도체 현지화, 전기자동차 및 배터리 제조, 5G 인프라, 산업 자동화 업그레이드를 통해 더욱 공고해지고 있습니다. 이러한 분야는 전기·전자 시험 장비, RF 및 마이크로파 시험, 자동 시험 장비, 생산 검증 시스템에 대한 지속적인 수요를 창출하고 있습니다. 또한 AI 데이터센터의 용량 확대와 고속 네트워크에 대한 요구 사항이 증가함에 따라 기술 및 제조 생태계 전반에 걸쳐 전력, 열, 광, 신호 무결성 테스트에 대한 필요성도 높아지고 있습니다.

1차 조사 내역

시험·계측(T&M) 장비 시장에서 사업을 운영하는 주요 조직의 임원(CEO, 마케팅 이사, 혁신·기술 이사 등)을 대상으로 심층 인터뷰를 시행했습니다.

계측기 시장은 Keysight Technologies(미국), Rohde & Schwarz(독일), Tektronix(미국), NI / Emerson Test & Measurement(미국), Anritsu Corporation(일본), Yokogawa Test & Measurement(일본), Advantest Corporation(일본), Teradyne Inc.(미국), Fluke Corporation(미국), EXFO Inc.(캐나다), VIAVI Solutions Inc.(미국), Chroma ATE Inc.(대만), Teledyne LeCroy(미국), AMETEK Inc.(미국), 그리고 Hioki E.E. Corporation(일본) 등이 있습니다. 본 조사에서는 시장의 이러한 주요 기업에 대해 기업 개요, 제품 포트폴리오, 최근 동향, 시장 순위, 핵심 경쟁력 및 주요 시장 전략을 포괄하는 상세한 경쟁 분석을 수행하고 있습니다.

조사 범위

이 보고서에서는 시험·계측 장비 시장을 세분화하고 있습니다. 제품 유형, 시험 유형, 상용 모델, 시스템 시험 수준, 시험 수명 주기 단계, 최종 용도 산업 및 지역별로 시장 규모를 예측하고 있습니다. 또한 이 보고서에서는 시장 성장에 영향을 미치는 촉진요인, 제약 요인, 기회 및 과제에 대해서도 다루고 있습니다. 북미, 유럽, 아시아·태평양, 남미, 중동 및 아프리카 등 5개 주요 지역에 걸친 시장에 대한 상세한 개요를 제공합니다. 또한 본 조사에서는 생태계 분석, 기술 동향, 사용 사례, 가격 분석, 구매 기준, 최근 동향은 물론, 주요 T&M 장비 공급업체, 임대 및 중고 장비 공급업체, 전문 시험 플랫폼 기업에 대한 경쟁 분석도 포괄적으로 다루고 있습니다.

이 보고서를 구매할 때의 주요 이점

- 주요 성장 동인(반도체, 전기자동차, 데이터센터, 통신, 항공우주 애플리케이션에서의 테스트 복잡성 증가, 자동 테스트 장비 및 모듈형 계측 장비의 도입 확대, 제품 수명 주기 전반에 걸친 더 빠르고 정확하며 추적 가능한 검증에 대한 수요 증가, RF 및 마이크로파 테스트, 반도체 테스트, 전기자동차 배터리 테스트, ADAS 검증, AI 데이터센터 테스트에 대한 높은 수요) , 제약 요인(고급 자동 시험 장비 및 모듈형 플랫폼의 높은 초기 비용, 빈번한 업그레이드를 제한하는 긴 갱신 주기, 하드웨어, 소프트웨어, 고정구 및 시험 데이터 워크플로우 간의 통합 복잡성), 기회(AI 지원, 소프트웨어 정의 및 자동화된 테스트의 속도, 정확도, 처리량 향상, 5G/6G, 전기자동차 배터리, ADAS, 치플릿 및 AI 데이터센터 인프라에서의 수요 증가), 그리고 과제(기술의 급속한 변화에 따른 장비 노후화 위험 증가, 하드웨어, 소프트웨어, 데이터 및 사이버 보안 테스트를 통합된 워크플로우로 통합할 필요성)가 테스트 및 계측 장비 시장의 성장에 영향을 미치고 있습니다.

- 제품 및 기술 개발: 이 보고서는 독립형 계측기, 모듈형 계측 장비, 자동 시험 장비, RF 및 마이크로파 시험, 반도체 시험, 전기자동차(EV) 시험, 데이터센터 검증, 그리고 소프트웨어 기반 시험 워크플로우에 걸친 신기술, 제품 출시, 연구개발 활동 및 혁신 동향에 대한 상세 인사이트를 제공합니다.

- 시장 동향: 이 보고서는 북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카의 고성장 시장 및 국가 차원의 비즈니스 기회에 대한 포괄적인 정보를 제공하며, 특히 반도체 제조, 통신 인프라 구축, 전기자동차(EV) 생산, AI 데이터센터 확장, 산업 현대화에 중점을 두고 있습니다.

- 시장의 다양화: 이 보고서에서는 신제품 카테고리, 비즈니스 모델, 최종 용도 및 미개발 기회에 대해 신품 장비 판매, 중고 장비 판매, 임대, 장비 시험, 소프트웨어 시험, 부품 시험, 서브시스템 시험, 시스템 시험은 물론, 연구개발부터 서비스 및 유지보수에 이르는 수명주기의 각 단계에 걸친 시험을 포괄적으로 다루고 있습니다.

- 경쟁사 분석: 이 보고서에는 키사이트 테크놀러지스, 로데 슈바르츠, 테크트로닉스, 내셔널 인스트루먼트, 안리쓰, 요코가와 계측, 어드반 테스트, 테라다인, 플루크, EXFO, VIAVI 솔루션즈, 크로마 ATE, 테레다인 루크로이, AMETEK, 히오키 등 주요 기업의 시장 순위, 제품 포트폴리오, 성장 전략, 최근 동향 및 경쟁 포지셔닝에 대한 상세한 평가가 포함되어 있습니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 시험·계측 장비 시장(제품 유형별)

제10장 시험·계측 장비 시장(시스템 시험 레벨별)

제11장 시험·계측 장비 시장(시험 수명주기 스테이지별)

제12장 시험·계측 장비 시장(상용 모델별)

제13장 시험·계측 장비 시장(시험 유형별)

제14장 시험·계측 장비 시장(최종 용도 산업)

제15장 시험·계측 장비 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSA 26.06.24The global test and measurement equipment market is anticipated to grow from USD 52.67 billion in 2026 to USD 76.38 billion by 2032, registering a CAGR of 6.4% during the forecast period. Growth is supported by the rising test complexity across semiconductors, data centers, electric vehicles, telecommunications, aerospace and defense, and industrial manufacturing. Increasing adoption of automated test equipment, modular instrumentation, software-defined testing, and advanced RF and microwave validation is improving test speed, accuracy, repeatability, and lifecycle coverage.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Product Type, Testing Type, End User and Region |

| Regions covered | North America, Europe, APAC, RoW |

However, high upfront costs of advanced test platforms, long replacement cycles, integration complexity, and risk of equipment obsolescence remain key restraints for the market.

"Software testing segment to be the fastest-growing testing type during forecast period"

By testing type, the software testing segment is growing at a significant rate from 2026 to 2032 as products across automotive, telecom, data centers, healthcare devices, semiconductors, and industrial automation become increasingly software-driven. Rising use of embedded systems, connected devices, cloud-linked infrastructure, artificial intelligence workloads, advanced driver assistance systems, and 5G and 6G networks is increasing the need to validate performance, reliability, cybersecurity, interoperability, and system behavior. Equipment testing remains the larger market as physical instruments are still essential for electrical, RF, mechanical, and production validation. Still, software testing is gaining stronger momentum as customers require integrated hardware-software validation across the full product lifecycle.

"Component testing segment to account for the largest market share in 2032"

By system level testing, the component testing segment is likely to hold the largest market share, as individual parts, chips, modules, sensors, circuits, connectors, batteries, RF components, and mechanical elements must be validated before being integrated into larger systems. This testing stage is highly repeatable across R&D, design validation, production, field failure analysis, and service workflows, making it a consistent demand driver for T&M equipment. Subsystem testing also remains crucial as industries such as automotive, aerospace, telecom, semiconductors, and healthcare increasingly validate functional blocks before full system-level qualification.

"China to hold largest share of the Asia Pacific test and measurement equipment market in 2026"

China is expected to hold the largest share of the Asia Pacific test and measurement equipment market in 2026, supported by its deep electronics manufacturing base, semiconductor activity, EV production, telecom infrastructure, and industrial automation ecosystem. The country's leadership is further reinforced by the scale of domestic electronics production, semiconductor localization, EV and battery manufacturing, 5G infrastructure, and industrial automation upgrades. These sectors create sustained demand for electrical and electronic test instruments, RF and microwave testing, automated test equipment, and production validation systems. Expanding AI data center capacity and high-speed networking requirements are also increasing the need for power, thermal, optical, and signal integrity testing across the technology and manufacturing ecosystem.

Breakdown of primaries

A variety of executives from key organizations operating in the test & measurement (T&M) equipment market were interviewed in-depth, including CEOs, marketing directors, and innovation and technology directors.

- By Company Type: Tier 1 - 30%, Tier 2 - 50%, and Tier 3 - 20%

- By Designation: C-level Executives - 25%, Directors - 35%, and Others - 40%

- By Region: North America - 35%, Europe - 25%, Asia Pacific - 30%, and RoW - 10%

The test and measurement equipment market is led by globally established players, such as Keysight Technologies (US), Rohde & Schwarz (Germany), Tektronix (US), NI / Emerson Test & Measurement (US), Anritsu Corporation (Japan), Yokogawa Test & Measurement (Japan), Advantest Corporation (Japan), Teradyne Inc. (US), Fluke Corporation (US), EXFO Inc. (Canada), VIAVI Solutions Inc. (US), Chroma ATE Inc. (Taiwan), Teledyne LeCroy (US), AMETEK Inc. (US), and Hioki E.E. Corporation (Japan). The study includes an in-depth competitive analysis of these key players in the market, covering their company profiles, product portfolios, recent developments, market rankings, core competencies, and key market strategies.

Study Coverage

The report segments the test and measurement equipment market. It forecasts its size by product type, testing type, commercial model, system testing level, testing lifecycle stage, end-use industry, and region. The report also discusses the drivers, restraints, opportunities, and challenges influencing market growth. It provides a detailed view of the market across five key regions, including North America, Europe, Asia Pacific, South America, and the Middle East & Africa. Ecosystem analysis, technology trends, use cases, pricing analysis, buying criteria, recent developments, and competitive analysis of key T&M equipment providers, rental and used equipment providers, and specialized testing platform companies have also been covered in the study.

Key Benefits of Buying the Report

- Analysis of key drivers (Rising test complexity for semiconductors, EVs, data centers, telecom, and aerospace applications, Increasing adoption of automated test equipment and modular instrumentation, Growing need for faster, accurate, and traceable validation across product lifecycles, High demand for RF and microwave testing, semiconductor testing, EV battery testing, ADAS validation, and AI data center testing), restraints (High upfront cost of advanced automated test equipment and modular platforms, Long replacement cycles limiting frequent upgrades, Integration complexity across hardware, software, fixtures, and test data workflows), opportunities (Improved speed, accuracy, and throughput of AI-enabled, software-defined, and automated testing, Mounting demand from 5G/6G, EV batteries, ADAS, chiplets, and AI data center infrastructure), and challenges (Rapid technology shifts increasing risk of equipment obsolescence, Need to integrate hardware, software, data, and cybersecurity testing into unified workflows) influencing the growth of the test and measurement equipment market.

- Product and Technology Development: The report offers detailed insights into emerging technologies, product launches, R&D activities, and innovation trends across standalone instruments, modular instrumentation, automated test equipment, RF and microwave testing, semiconductor testing, EV testing, data center validation, and software-enabled test workflows.

- Market Development: The report provides comprehensive information about high-growth regional markets and country-level opportunities across North America, Europe, Asia Pacific, South America, and the Middle East & Africa, with emphasis on semiconductor manufacturing, telecom deployment, EV production, AI data center expansion, and industrial modernization.

- Market Diversification: The report covers new product categories, commercial models, end-use applications, and untapped opportunities across new equipment sales, used equipment sales, rental, equipment testing, software testing, component testing, subsystem testing, system testing, and lifecycle-stage testing from R&D to service and maintenance.

- Competitive Assessment: The report includes an in-depth assessment of market rankings, product portfolios, growth strategies, recent developments, and competitive positioning of leading players such as Keysight Technologies, Rohde & Schwarz, Tektronix, National Instruments, Anritsu Corporation, Yokogawa Test & Measurement, Advantest, Teradyne, Fluke, EXFO, VIAVI Solutions, Chroma ATE, Teledyne LeCroy, AMETEK, and Hioki, among others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN TEST AND MEASUREMENT EQUIPMENT MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN TEST AND MEASUREMENT EQUIPMENT MARKET

- 3.2 TEST AND MEASUREMENT EQUIPMENT MARKET, BY STANDALONE INSTRUMENT TYPE

- 3.3 TEST AND MEASUREMENT EQUIPMENT MARKET, BY COMMERCIAL MODEL

- 3.4 TEST AND MEASUREMENT EQUIPMENT MARKET, BY TESTING TYPE

- 3.5 TEST AND MEASUREMENT EQUIPMENT MARKET FOR AEROSPACE & DEFENSE, BY TYPE

- 3.6 TEST AND MEASUREMENT EQUIPMENT MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing validation complexity across AI data centers and high-speed digital infrastructure

- 4.2.1.2 Rising semiconductor design, packaging, and production testing

- 4.2.1.3 Rapid expansion of 5G-advanced, RF, microwave, and future 6G-related testing

- 4.2.1.4 Shifting preference toward electric and software-defined architectures

- 4.2.2 RESTRAINTS

- 4.2.2.1 High upfront cost and long replacement cycles of precision instruments

- 4.2.2.2 Budget sensitivity among small- and mid-sized users

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Proliferation of rental, used equipment, leasing, and pay-per-use commercial models

- 4.2.3.2 Expansion of modular, software-defined, and automated test platforms

- 4.2.3.3 Localized calibration, service, and application support in emerging economies

- 4.2.4 CHALLENGES

- 4.2.4.1 Issues in maintaining technical accuracy of high frequencies and voltages, and mixed hardware-software architectures

- 4.2.4.2 Supply chain, component availability, and service turnaround pressure

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 THREAT OF NEW ENTRANTS

- 5.1.5 THREAT OF SUBSTITUTES

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL DATA CENTER INDUSTRY

- 5.2.4 TRENDS IN GLOBAL AEROSPACE & DEFENSE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF T&M EQUIPMENT OFFERED BY KEY PLAYERS, BY PRODUCT TYPE, 2022-2025

- 5.5.2 AVERAGE SELLING PRICE TREND OF T&M EQUIPMENT, BY REGION, 2022-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 9030)

- 5.6.2 EXPORT SCENARIO (HS CODE 9030)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 KEYSIGHT TECHNOLOGIES PROVIDES UXM 5G WIRELESS TEST SET TO ENABLE 5G DEVICE VALIDATION

- 5.10.2 TEKTRONIX DELIVERS MIXED-SIGNAL OSCILLOSCOPES TO SUPPORT AIRBUS FLIGHT TEST INSTRUMENTATION VALIDATION

- 5.10.3 ROHDE & SCHWARZ DEPLOYS QUALIPOC ANDROID PROBES TO ENABLE 24/7 MOBILE NETWORK MONITORING AT CERN

- 5.10.4 VIAVI SOLUTIONS DEPLOYS VIAVI TESTCENTER TO VALIDATE AND OPTIMIZE AI-DRIVEN INFRASTRUCTURE IN FINANCIAL INSTITUTION

- 5.10.5 CHROMA ATE PROVIDES BATTERY TEST SOLUTION FOR FORMULA 1 POWERTRAIN TEAM

- 5.11 IMPACT OF US TARIFFS - TEST AND MEASUREMENT EQUIPMENT MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 AUTOMATED TEST EQUIPMENT

- 6.1.2 RF & MICROWAVE TESTING SOLUTIONS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 AI-ENABLED TEST ANALYTICS

- 6.2.2 DIGITAL TWIN & SIMULATION PLATFORMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 CALIBRATION & METROLOGY SYSTEMS

- 6.3.2 INDUSTRIAL IOT & CONNECTED MONITORING SYSTEMS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.7 IMPACT OF AI/GEN AI ON TEST AND MEASUREMENT EQUIPMENT MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES FOLLOWED BY OEMS IN TEST AND MEASUREMENT EQUIPMENT MARKET

- 6.7.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION IN TEST AND MEASUREMENT EQUIPMENT MARKET

- 6.7.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT AI/GEN AI-INTEGRATED TEST AND MEASUREMENT EQUIPMENT

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 TEST AND MEASUREMENT EQUIPMENT MARKET, BY PRODUCT TYPE

- 9.1 INTRODUCTION

- 9.2 STANDALONE INSTRUMENTS

- 9.2.1 ELECTRICAL & ELECTRONIC TEST INSTRUMENTS

- 9.2.1.1 Ability to anchor circuit-level validation across design, production, and service workflows to fuel segmental growth

- 9.2.2 RF & MICROWAVE TEST INSTRUMENTS

- 9.2.2.1 Rapid expansion of 5G networks and satellite communications to contribute to segmental growth

- 9.2.3 MECHANICAL, PHYSICAL & INDUSTRIAL TEST INSTRUMENTS

- 9.2.3.1 Need to withstand mechanical stress and other industrial operating conditions to expedite segmental growth

- 9.2.4 OTHER SPECIALIZED STANDALONE INSTRUMENTS

- 9.2.1 ELECTRICAL & ELECTRONIC TEST INSTRUMENTS

- 9.3 MODULAR INSTRUMENTS

- 9.3.1 FOCUS ON REDUCING RACK SPACE AND IMPROVING TEST SPEED TO ACCELERATE SEGMENTAL GROWTH

- 9.4 AUTOMATED TEST EQUIPMENT

- 9.4.1 HIGH DEVICE COMPLEXITY AND STRICTER QUALITY EXPECTATIONS IN INDUSTRIES TO FOSTER SEGMENTAL GROWTH

10 TEST AND MEASUREMENT EQUIPMENT MARKET, BY SYSTEM TESTING LEVEL

- 10.1 INTRODUCTION

- 10.2 COMPONENT TESTING

- 10.2.1 RISING QUALITY EXPECTATION, ELECTRONIC CONTENT IN PRODUCTS, AND MINIATURIZATION TO BOOST SEGMENTAL GROWTH

- 10.3 SUBSYSTEM TESTING

- 10.3.1 INCREASING RELIANCE ON EMBEDDED ELECTRONICS AND SOFTWARE-DEFINED FUNCTIONALITY TO SPUR DEMAND

- 10.4 SYSTEM TESTING

- 10.4.1 MOUNTING ADOPTION OF CONNECTED, SOFTWARE-DEFINED, AND POWER-INTENSIVE PLATFORMS TO BOLSTER SEGMENTAL GROWTH

11 TEST AND MEASUREMENT EQUIPMENT MARKET, BY TESTING LIFECYCLE STAGE

- 11.1 INTRODUCTION

- 11.2 R&D TESTING

- 11.2.1 ABILITY TO SUPPORT NEW CHIP ARCHITECTURES, PACKAGING TECHNOLOGIES, AND HIGH-SPEED INTERFACES TO DRIVE MARKET

- 11.3 DESIGN VALIDATION TESTING

- 11.3.1 FOCUS ON MEETING INTERNAL SPECIFICATIONS AND EXTERNAL STANDARDS BEFORE ENTERING PRODUCTION TO BOOST SEGMENTAL GROWTH

- 11.4 PRODUCTION TESTING

- 11.4.1 REQUIREMENT FOR CONTINUOUS AND REPEATABLE TESTING AT SCALE TO AUGMENT SEGMENTAL GROWTH

- 11.5 FIELD TESTING

- 11.5.1 ADOPTION OF DISTRIBUTED, CONNECTED, AND INFRASTRUCTURE-DEPENDENT MODERN SYSTEMS TO FUEL SEGMENTAL GROWTH

- 11.6 SERVICE & MAINTENANCE TESTING

- 11.6.1 NEED TO MAINTAIN NETWORK UPTIME AND SIGNAL QUALITY TO CONTRIBUTE TO SEGMENTAL GROWTH

12 TEST AND MEASUREMENT EQUIPMENT MARKET, BY COMMERCIAL MODEL

- 12.1 INTRODUCTION

- 12.2 NEW EQUIPMENT SALES

- 12.2.1 REQUIREMENT FOR INSTRUMENTS THAT SUPPORT HIGH BANDWIDTH AND FASTER SAMPLING RATES TO EXPEDITE SEGMENTAL GROWTH

- 12.3 USED EQUIPMENT SALES

- 12.3.1 ABILITY TO EXPAND TEST CAPACITY TO CONTRIBUTE TO SEGMENTAL GROWTH

- 12.4 RENTAL

- 12.4.1 HIGH EMPHASIS ON BALANCING TECHNICAL REQUIREMENTS WITH CAPITAL EFFICIENCY TO BOLSTER SEGMENTAL GROWTH

13 TEST AND MEASUREMENT EQUIPMENT MARKET, BY TESTING TYPE

- 13.1 INTRODUCTION

- 13.2 EQUIPMENT TESTING

- 13.2.1 REGULATORY REQUIREMENTS AND RELIANCE ON AUTOMATED AND INTEGRATED VALIDATION ENVIRONMENTS TO DRIVE MARKET

- 13.3 SOFTWARE TESTING

- 13.3.1 INCREASING ELECTRIC VEHICLE SALES AND 5G CONNECTION TO BOLSTER SEGMENTAL GROWTH

14 TEST AND MEASUREMENT EQUIPMENT MARKET, BY END-USE INDUSTRY

- 14.1 INTRODUCTION

- 14.2 DATA CENTERS

- 14.2.1 INCREASING HYPERSCALE CLOUD PROVIDERS AND COLOCATION OPERATORS TO FUEL SEGMENTAL GROWTH

- 14.3 AEROSPACE & DEFENSE

- 14.3.1 COMMERCIAL AVIATION

- 14.3.1.1 Increasing electronic, software, and communication content in modern aircraft to augment segmental growth

- 14.3.2 SPACE

- 14.3.2.1 Rising satellite communication, earth observation, and security programs to expedite segmental growth

- 14.3.3 DEFENSE

- 14.3.3.1 Growing need to validate systems operating in mission-critical, harsh, and security-sensitive environments to drive market

- 14.3.1 COMMERCIAL AVIATION

- 14.4 AUTOMOTIVE

- 14.4.1 SHIFTING PREFERENCE TOWARD ELECTRIFIED, SENSOR-RICH, AND SOFTWARE-CONTROLLED SYSTEMS TO BOOST SEGMENTAL GROWTH

- 14.5 TELECOMMUNICATIONS

- 14.5.1 RISING ADOPTION OF HIGH BANDWIDTH, LOW LATENCY, AND SOFTWARE-DEFINED ARCHITECTURES TO FOSTER SEGMENTAL GROWTH

- 14.6 SEMICONDUCTORS

- 14.6.1 INCREASING SALES OF LOGIC AND MEMORY PRODUCTS TO ACCELERATE SEGMENTAL GROWTH

- 14.7 MANUFACTURING

- 14.7.1 RISING DEPLOYMENT OF AUTOMATION AND ROBOTICS TECHNOLOGIES TO FACILITATE SEGMENTAL GROWTH

- 14.8 HEALTHCARE & MEDICAL DEVICES

- 14.8.1 INCREASING NEED FOR DOCUMENTED DESIGN CONTROLS, INSPECTION READINESS, AND TRACEABLE VALIDATION TO DRIVE MARKET

- 14.9 OTHER END-USE INDUSTRIES

15 TEST AND MEASUREMENT EQUIPMENT MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 US

- 15.2.1.1 Rising semiconductor reshoring and artificial intelligence infrastructure development to augment market growth

- 15.2.2 CANADA

- 15.2.2.1 Thriving automotive and aerospace industries to boost market growth

- 15.2.3 MEXICO

- 15.2.3.1 Increasing light vehicle manufacturing and exports to accelerate market growth

- 15.2.1 US

- 15.3 EUROPE

- 15.3.1 GERMANY

- 15.3.1.1 Mounting demand for electric platforms, software-defined vehicles, battery systems, and power electronics to fuel market growth

- 15.3.2 UK

- 15.3.2.1 Booming defense and space industries to contribute to market growth

- 15.3.3 SPAIN

- 15.3.3.1 Escalating vehicle production and aerospace R&D to bolster market growth

- 15.3.4 NETHERLANDS

- 15.3.4.1 Rising development of digital and e-mobility infrastructure to expedite market growth

- 15.3.5 ITALY

- 15.3.5.1 Increasing electric vehicle charging base and energy transition projects to augment market growth

- 15.3.6 FRANCE

- 15.3.6.1 Rising electric vehicle production to support market growth

- 15.3.7 REST OF EUROPE

- 15.3.1 GERMANY

- 15.4 ASIA PACIFIC

- 15.4.1 CHINA

- 15.4.1.1 Growing emphasis on smart manufacturing and green development targets for data centers to drive market

- 15.4.2 JAPAN

- 15.4.2.1 Rising adoption of advanced semiconductors, precision automotive engineering, and robotics to foster market growth

- 15.4.3 SOUTH KOREA

- 15.4.3.1 Increasing semiconductor export and mega fabrication projects to expedite market growth

- 15.4.4 AUSTRALIA

- 15.4.4.1 Rising mining automation and defense modernization to accelerate market growth

- 15.4.5 SINGAPORE

- 15.4.5.1 Growing wafer fabrication capacity and semiconductor equipment production to support market growth

- 15.4.6 INDIA

- 15.4.6.1 Increasing electronics manufacturing and data center expansion to accelerate market growth

- 15.4.7 REST OF ASIA PACIFIC

- 15.4.1 CHINA

- 15.5 SOUTH AMERICA

- 15.5.1 BRAZIL

- 15.5.1.1 Rapid expansion of automotive and industrial bases to contribute to market growth

- 15.5.2 ARGENTINA

- 15.5.2.1 Mounting production of oil and gas and telecom modernization to boost market growth

- 15.5.3 REST OF SOUTH AMERICA

- 15.5.1 BRAZIL

- 15.6 MIDDLE EAST & AFRICA

- 15.6.1 ENERGY DIVERSIFICATION, TELECOM MODERNIZATION, AND DATA CENTER EXPANSION TO FACILITATE MARKET GROWTH

- 15.6.2 GCC COUNTRIES

- 15.6.3 REST OF MIDDLE EAST & AFRICA

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2023-2026

- 16.3 REVENUE ANALYSIS, 2021-2025

- 16.4 MARKET SHARE ANALYSIS, 2025

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS

- 16.6 PRODUCT COMPARISON

- 16.6.1 ADVANTEST CORPORATION (JAPAN)

- 16.6.2 KEYSIGHT TECHNOLOGIES, INC. (US)

- 16.6.3 TERADYNE, INC. (US)

- 16.6.4 AMETEK, INC. (US)

- 16.6.5 ROHDE & SCHWARZ (GERMANY)

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 PERVASIVE PLAYERS

- 16.7.3 EMERGING LEADERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 End-use industry footprint

- 16.7.5.4 Product type footprint

- 16.7.5.5 Testing type footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING, STARTUPS/SMES, 2025

- 16.8.5.1 Detailed list of startups/SMEs

- 16.8.5.2 Competitive benchmarking of key startups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

- 16.9.4 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 INTRODUCTION

- 17.2 KEY PLAYERS

- 17.2.1 ADVANTEST CORPORATION

- 17.2.1.1 Business overview

- 17.2.1.2 Products/Solutions/Services offered

- 17.2.1.3 Recent developments

- 17.2.1.3.1 Product launches

- 17.2.1.3.2 Deals

- 17.2.1.3.3 Expansions

- 17.2.1.3.4 Other developments

- 17.2.1.4 MnM view

- 17.2.1.4.1 Key strengths/Right to win

- 17.2.1.4.2 Strategic choices

- 17.2.1.4.3 Weaknesses/Competitive threats

- 17.2.2 KEYSIGHT TECHNOLOGIES

- 17.2.2.1 Business overview

- 17.2.2.2 Products/Solutions/Services offered

- 17.2.2.3 Recent developments

- 17.2.2.3.1 Product launches

- 17.2.2.3.2 Deals

- 17.2.2.3.3 Expansions

- 17.2.2.4 MnM view

- 17.2.2.4.1 Key strengths/Right to win

- 17.2.2.4.2 Strategic choices

- 17.2.2.4.3 Weaknesses/Competitive threats

- 17.2.3 TERADYNE INC.

- 17.2.3.1 Business overview

- 17.2.3.2 Products/Solutions/Services offered

- 17.2.3.3 Recent developments

- 17.2.3.3.1 Product launches

- 17.2.3.3.2 Deals

- 17.2.3.3.3 Other developments

- 17.2.3.4 MnM view

- 17.2.3.4.1 Key strengths/Right to win

- 17.2.3.4.2 Strategic choices

- 17.2.3.4.3 Weaknesses/Competitive threats

- 17.2.4 AMETEK, INC.

- 17.2.4.1 Business overview

- 17.2.4.2 Products/Solutions/Services offered

- 17.2.4.3 Recent developments

- 17.2.4.3.1 Product launches

- 17.2.4.3.2 Deals

- 17.2.4.3.3 Expansions

- 17.2.4.3.4 Other developments

- 17.2.4.4 MnM view

- 17.2.4.4.1 Key strengths/Right to win

- 17.2.4.4.2 Strategic choices

- 17.2.4.4.3 Weaknesses/Competitive threats

- 17.2.5 ROHDE & SCHWARZ

- 17.2.5.1 Business overview

- 17.2.5.2 Products/Solutions/Services offered

- 17.2.5.3 Recent developments

- 17.2.5.3.1 Product launches

- 17.2.5.3.2 Deals

- 17.2.5.3.3 Expansions

- 17.2.5.3.4 Other developments

- 17.2.5.4 MnM view

- 17.2.5.4.1 Key strengths/Right to win

- 17.2.5.4.2 Strategic choices

- 17.2.5.4.3 Weaknesses/Competitive threats

- 17.2.6 EMERSON ELECTRIC CO.

- 17.2.6.1 Business overview

- 17.2.6.2 Products/Solutions/Services offered

- 17.2.6.3 Recent developments

- 17.2.6.3.1 Product launches

- 17.2.6.3.2 Deals

- 17.2.7 RALLIANT

- 17.2.7.1 Business overview

- 17.2.7.2 Products/Solutions/Services offered

- 17.2.7.3 Recent developments

- 17.2.7.3.1 Product launches

- 17.2.7.3.2 Deals

- 17.2.7.3.3 Expansions

- 17.2.7.3.4 Other developments

- 17.2.8 ANRITSU

- 17.2.8.1 Business overview

- 17.2.8.2 Products/Solutions/Services offered

- 17.2.8.3 Recent developments

- 17.2.8.3.1 Product launches

- 17.2.8.3.2 Deals

- 17.2.8.3.3 Expansions

- 17.2.8.3.4 Other developments

- 17.2.9 YOKOGAWA ELECTRIC CORPORATION

- 17.2.9.1 Business overview

- 17.2.9.2 Products/Solutions/Services offered

- 17.2.9.3 Recent developments

- 17.2.9.3.1 Product launches

- 17.2.9.3.2 Deals

- 17.2.9.3.3 Other developments

- 17.2.10 CHROMA ATE INC.

- 17.2.10.1 Business overview

- 17.2.10.2 Products/Solutions/Services offered

- 17.2.10.3 Recent developments

- 17.2.10.3.1 Product launches

- 17.2.10.3.2 Deals

- 17.2.10.3.3 Expansions

- 17.2.10.3.4 Other developments

- 17.2.1 ADVANTEST CORPORATION

- 17.3 OTHER PLAYERS

- 17.3.1 TELEDYNE TECHNOLOGIES INCORPORATED

- 17.3.2 VIAVI SOLUTIONS INC.

- 17.3.3 HIOKI E.E. CORPORATION

- 17.3.4 COHU, INC.

- 17.3.5 FORMFACTOR

- 17.3.6 EXFO INC.

- 17.3.7 MEGGER

- 17.3.8 HOTTINGER BRUEL & KJAER

- 17.3.9 AVL

- 17.3.10 INSTRON

- 17.3.11 ASTRONICS CORPORATION

- 17.3.12 PICKERING

- 17.3.13 MARVIN TEST SOLUTIONS

- 17.3.14 DEWESOFT D.O.O

- 17.4 RENTAL & USED EQUIPMENT PROVIDERS

- 17.4.1 ELECTRORENT.COM, INC.

- 17.4.2 TRS-RENTELCO

- 17.4.3 TESTEQUITY LLC

- 17.4.4 TRANSCAT, INC.

- 17.4.5 AXIOM TEST

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 Key data from secondary sources

- 18.1.1.2 List of key secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Key data from primary sources

- 18.1.2.2 List of primary interview participants

- 18.1.2.3 Breakdown of primary interviews

- 18.1.2.4 Key industry insights

- 18.1.3 SECONDARY AND PRIMARY RESEARCH

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION

- 18.2.1 BOTTOM-UP APPROACH

- 18.2.1.1 Approach to arrive at market size using bottom-up analysis

- 18.2.2 TOP-DOWN APPROACH

- 18.2.2.1 Approach to arrive at market size using top-down analysis

- 18.2.1 BOTTOM-UP APPROACH

- 18.3 DATA TRIANGULATION

- 18.4 RISK ANALYSIS

- 18.5 RESEARCH ASSUMPTIONS

- 18.6 RESEARCH LIMITATIONS

19 APPENDIX

- 19.1 INSIGHTS FROM INDUSTRY EXPERTS

- 19.2 DISCUSSION GUIDE

- 19.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.4 CUSTOMIZATION OPTIONS

- 19.5 RELATED REPORTS

- 19.6 AUTHOR DETAILS