|

시장보고서

상품코드

2060321

이미지 센서 시장 예측(-2032년) : 유형, 처리 방식, 스펙트럼, 어레이, 해상도, 용도별Image Sensor Market by Type, Processing, Spectrum, Array, Resolution, Application - Global Forecast to 2032 |

||||||

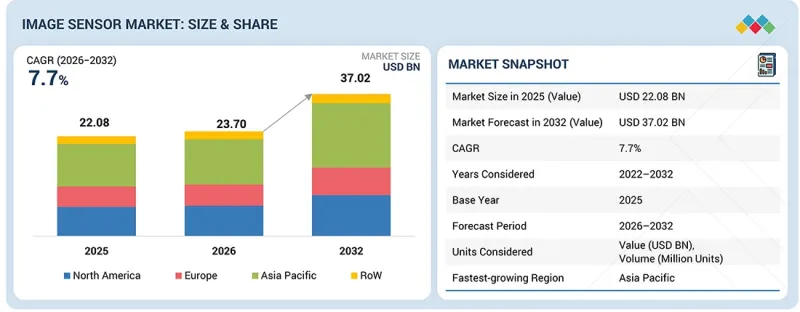

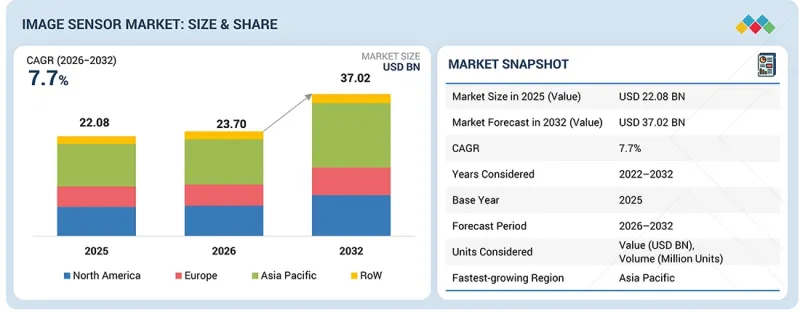

이미지 센서 시장 규모는 2026년 237억 달러에서 2032년에는 370억 2,000만 달러로 성장하며, CAGR은 7.7%에 달할 것으로 예측됩니다.

현대 시스템에서는 복잡한 환경에서 지속적인 시각 데이터 처리가 요구되므로 자동화 기술의 급속한 보급에 따라 이미지 센서에 대한 수요가 증가하고 있습니다. 첨단 운전자 보조 시스템(ADAS), 멀티 카메라 전자기기, 머신 비전의 보급으로 인해 데이터 수집 요구 사항이 대폭 증가했으며, 정확한 환경 인식에 대한 필요성이 높아지고 있습니다. 부정확한 시각 데이터는 시스템 알고리즘의 정확도를 떨어뜨리고, 처리 효율을 저하시키며, 운영상의 장애를 유발할 가능성이 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준연도 | 2025 |

| 예측 기간 | 2026-2032년 |

| 단위 | 금액(달러) |

| 부문 | 유형, 처리 방법, 최종사용자, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

따라서 제조사들은 특히 소형 고성능 전자 기기에서 데이터의 정확성을 확인하고, 시스템의 신뢰성을 유지하며, 안전 규정을 충족하기 위해 첨단 CMOS(상보형 금속 산화막 반도체) 및 3D 깊이 센서를 통합하고 있습니다.

"처리 기술별로는 3D 이미지 센서가 예측 기간 중 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 전망된다"

처리 기술별로는 전자 시스템 분야에서 정밀한 깊이 인식 및 공간 인식에 대한 수요가 증가함에 따라 3D 이미지 센서 부문이 가장 빠르게 성장할 것으로 전망됩니다. 3D 센서는 ToF(비행 시간 측정) 및 구조화된 빛 등의 기술을 활용하여 대상물까지의 거리를 정확하게 측정합니다. 이를 통해 얼굴 인식, 증강현실(AR), 자율주행 등의 분야에서 유용하게 활용될 수 있습니다. ADAS, 산업용 로봇, 스마트 기기에 힘입어 자동화 애플리케이션이 확대됨에 따라 정확한 체적 데이터의 확보가 필요해지고 있습니다. 또한 3D 이미징 기술은 측정 정밀도 향상, 높은 신뢰성을 갖춘 성능, 최신 생체 인증 아키텍처와의 손쉬운 통합을 실현합니다.

"파장대별로는 가시광선 이미지 센서가 예측 기간 내내 시장을 주도할 것으로 전망된다"

스펙트럼별로는 가시광 이미지 센서 부문이 소비자 및 상업용 기기에서 표준적인 광학 이미징에 대한 수요가 광범위하게 확산되고 있는 만큼, 예측 기간 중 시장을 주도할 것으로 예상됩니다. 전자 시스템에서는 인간의 가시광선 스펙트럼 범위에 속하는 빛을 지속적으로 포착해야 합니다. 이 기능은 일반적인 사진이나 고해상도 동영상을 생성하는 데 필수적입니다. 전자 제품에 여러 개의 카메라 모듈이 통합됨에 따라 표준 시각 데이터에 대한 수요가 크게 증가하고 있습니다. 가시광선 이미지 센서는 표준적인 적색, 녹색, 청색 색상 모델을 처리하여 디스플레이 및 기본적인 머신 비전 알고리즘에 필요한 영상 정보를 제공합니다. 이 기술은 스마트폰, 디지털 카메라, 보안 감시 시스템, ADAS 등 대량 생산되는 다양한 제품에 적용되고 있습니다. 이러한 용도에서 가시광선 스펙트럼 센서는 범용성이 높고 확장성이 뛰어나며 비용 효율이 뛰어난 하드웨어 솔루션을 제공합니다. 그 결과, 많은 제조업 분야에서 널리 채택되고 있습니다.

“22025년에는 중국이 아시아·태평양 지역의 이미지 센서 시장에서 최대 점유율을 차지할 것”

중국은 전자기기 제조 및 반도체 생산 분야의 생산 능력을 바탕으로 아시아태평양의 이미지 센서 시장에서 가장 큰 점유율을 차지할 것으로 추정됩니다. 이 국가는 CE 제품의 세계적 거점이며, 스마트폰, 디지털 카메라, 보안 장비 등을 대규모로 생산하고 있습니다. 이러한 장치에는 시각 데이터 처리를 위한 고정밀 이미지 센싱 부품이 필요합니다. 또한 스마트 시티 인프라 구축과 전기자동차 부문의 성장에 힘입어 이미징 하드웨어에 대한 수요는 더욱 증가하고 있습니다. 정부의 노력, 확립된 공급망, 주요 OEM의 존재 역시 현지 생산을 지원하고 있습니다. 이러한 요인들이 시장내 입지를 강화하여 중국이 지역내 점유율을 유지할 수 있게 하고 있습니다.

이 보고서에서는 전 세계 이미지 센서 시장을 조사하여, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 현황, 주요 기업 개요 등을 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 이미지 센서 출력

제10장 이미지 센서 기술

제11장 이미지 센서 시장 : 유형별

제12장 이미지 센서 시장 : 영상 처리 기술별

제13장 이미지 센서 시장 : 스펙트럼별

제14장 이미지 센서 시장 : 어레이 유형별

제15장 이미지 센서 시장 : 어레이 유형별

제16장 이미지 센서 시장 : 용도별

제17장 이미지 센서 시장 : 지역별

제18장 경쟁 구도

제19장 기업 개요

제20장 조사 방법

제21장 부록

KSA 26.06.25The image sensor market is projected to grow from USD 23.70 billion in 2026 to USD 37.02 billion by 2032, registering a CAGR of 7.7%. The demand for image sensors is increasing with the rapid proliferation of automated technologies because modern systems require continuous visual data processing in complex environments. The expansion of advanced driver assistance systems (ADAS), multi-camera electronics, and machine vision has significantly increased data capture requirements, leading to a greater need for accurate environmental perception. Inaccurate visual data can degrade system algorithms, reduce processing efficiency, and cause operational failures.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Type, Processing, End User and Region |

| Regions covered | North America, Europe, APAC, RoW |

As a result, manufacturers are integrating advanced complementary metal-oxide-semiconductor (CMOS) and 3D depth sensors to check data accuracy, maintain system reliability, and meet safety regulations, especially in compact and high-performance electronic equipment.

"3D image sensor, by processing technique, is expected to record the highest CAGR during the forecast period."

By processing technique, the 3D image sensor segment is likely to be the fastest-growing segment due to the increasing requirement for precise depth perception and spatial recognition in electronic systems. 3D sensors function by measuring the time of flight or utilizing structured light to calculate exact distances. This makes them effective for applications such as facial recognition, augmented reality, and autonomous navigation. With the expansion of automated applications driven by advanced driver assistance systems (ADAS), industrial robotics, and smart devices, capturing accurate volumetric data is necessary. Additionally, 3D imaging technologies offer improved measurement accuracy, reliable performance, and ease of integration into modern biometric architectures.

"Visible image sensor segment is expected to lead the image sensor market, by spectrum, throughout the forecast period."

By spectrum, the visible image sensor segment is expected to lead the market throughout the forecast period due to the widespread requirement for standard optical imaging in consumer and commercial devices. Electronic systems continuously require the capture of light within the human visible spectrum. This capability is necessary to produce standard photography and high-resolution video. As electronic products integrate multiple camera modules, the demand for standard visual data increases significantly. Visible image sensors process standard red, green, and blue color models. This processing provides the necessary visual input for displays and basic machine vision algorithms. The expansion of high-volume applications includes smartphones, digital cameras, security surveillance, and automotive driver assistance systems. In these specific applications, visible spectrum sensors offer a versatile, scalable, and cost-efficient hardware solution. These operational factors lead to their dominant adoption across multiple manufacturing industries.

"China secured the largest share of the Asia Pacific image sensor market in 2025."

China is estimated to account for the largest share of the Asia Pacific image sensor market due to its capacity in electronics manufacturing and semiconductor production. The country serves as a global hub for consumer electronics. This includes the large-scale production of smartphones, digital cameras, and security equipment. These devices require accurate image sensing components for visual data processing. Additionally, the deployment of smart city infrastructure and the growth of the electric vehicle sector further increase demand for imaging hardware. Government initiatives, established supply chains, and the presence of major OEMs support local manufacturing. These operational factors strengthen its market position and enable China to maintain its regional share.

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: Directors - 40%, C-level Executives - 30%, and Others - 30%

- By Region: North America - 25%, Europe - 20%, Asia Pacific - 45%, and RoW - 10%

Prominent players profiled in this report include Sony Corporation (Japan), Samsung (South Korea), OMNIVISION (US), STMicroelectronics (Switzerland), GalaxyCore Shanghai Limited Corporation (China), Semiconductor Components Industries, LLC (US), Hamamatsu Photonics K.K. (Japan), Infineon Technologies AG (Germany), Canon Inc. (Japan), and Teledyne Technologies Incorporated (US).

Research Coverage:

The report defines, describes, and forecasts the image sensor market based on type (COMS, CCD, and others), processing technique (2D Image Sensor and 3D Image Sensor), spectrum (Visible and Infrared), array type (Line Scan and Area Scan), resolution (VGA, 1.3MP to 3MP, 5MP to 10MP, 12MP to 16MP, and More than 16 MP), application (Consumer Electronics, Medical & Life Sciences, Industrial, Commercial, Security & Surveillance, and Aerospace & Defense), and region (North America, Europe, Asia Pacific, and RoW). It provides detailed information regarding drivers, restraints, opportunities, and challenges influencing the market's growth. It also analyzes competitive developments, including acquisitions, product launches, and expansions, adopted by key players to grow in the market.

Reasons to Buy This Report:

The report will help market leaders/new entrants with information on the closest approximations of the revenue for the overall image sensor market and its subsegments. The report will help stakeholders understand the competitive landscape and gain more insight to position their business better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market's pulse and provides information on key drivers, restraints, opportunities, and challenges.

The report will provide insights into the following points:

- Analysis of key drivers (Growing integration of ADAS technologies to enhance vehicle safety, comfort, and automation, Surging use of IoT devices in industrial, agriculture, and healthcare applications), restraints (Substantial costs associated with image sensor manufacturing, High power consumption by image sensors), opportunities (Emergence of newer applications of image sensors with technological advancements, Integration of image sensors with advanced technologies), and challenges (Balancing pixel size with optical performance during miniaturization, Supply chain disruptions due to geopolitical tensions) of the image sensor market

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the image sensor market

- Market Development: Comprehensive information about lucrative markets (The report analyzes the image sensor market across various regions.)

- Market Diversification: Exhaustive information about new products launched, untapped geographies, recent developments, and investments in the image sensor market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and offerings of leading players, including Sony Corporation (Japan), Samsung (South Korea), OMNIVISION (US), STMicroelectronics (Switzerland), and Semiconductor Components Industries, LLC (US), in the image sensor market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN IMAGE SENSORS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN IMAGE SENSORS MARKET

- 3.2 IMAGE SENSORS MARKET, BY TYPE

- 3.3 IMAGE SENSORS MARKET, BY PROCESSING TECHNIQUE

- 3.4 IMAGE SENSORS MARKET IN NORTH AMERICA, BY APPLICATION AND COUNTRY

- 3.5 IMAGE SENSORS MARKET, BY GEOGRAPHY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising integration of ADAS technologies to enhance vehicle safety, comfort, and automation

- 4.2.1.2 Surging adoption of IoT devices in industrial, agriculture, and healthcare sectors

- 4.2.1.3 Rapid advances in smartphone photography

- 4.2.1.4 Increasing use of CMOS image sensors in industrial applications

- 4.2.2 RESTRAINTS

- 4.2.2.1 Substantial costs associated with image sensor manufacturing

- 4.2.2.2 High power consumption by advanced image sensors

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing disposable income in emerging economies

- 4.2.3.2 Rising integration of image sensors with advanced technologies

- 4.2.3.3 Increasing image sensor applications with technological advancements

- 4.2.4 CHALLENGES

- 4.2.4.1 Balancing pixel size with optical performance during miniaturization

- 4.2.4.2 Shortage of essential materials and components

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL CONSUMER ELECTRONICS INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING RANGE OF IMAGE SENSORS OFFERED KEY PLAYERS, BY TYPE, 2025

- 5.5.2 AVERAGE SELLING PRICE TREND OF IMAGE SENSORS, BY TYPE, 2022-2025

- 5.5.3 AVERAGE SELLING PRICE TREND OF CMOS IMAGE SENSORS, BY REGION, 2022-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 854140)

- 5.6.2 EXPORT SCENARIO (HS CODE 854140)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 VIVAMOS OFFERS CMOS SENSOR TO CARRY OUT SURGERY AND CONE-BEAM COMPUTED TOMOGRAPHY IN MEDICAL FIELD

- 5.10.2 JRCS PROVIDES AI-BASED OBJECT RECOGNITION SYSTEM TO ENSURE RELIABLE OPERATIONS IN MARITIME ENVIRONMENTS

- 5.10.3 LILIN AND SONY UNITE TO OFFER TOF SENSOR-EQUIPPED MONITORING CAMERA TO IMPROVE SAFETY AND MAINTAIN PRIVACY OF NURSING HOME RESIDENTS

- 5.11 IMPACT OF US TARIFFS - IMAGE SENSORS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON APPLICATIONS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, AND INNOVATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 COPPER-COPPER CONNECTION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 THERMAL MANAGEMENT SYSTEMS

- 6.2.2 OPTICAL COATINGS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 BACK-ILLUMINATED CMOS SENSORS

- 6.3.2 ARTIFICIAL INTELLIGENCE/MACHINE LEARNING IMAGE ANALYTICS

- 6.4 TECHNOLOGY ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI ON IMAGE SENSORS MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIALS

- 6.6.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS IN IMAGE SENSORS MARKET

- 6.6.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN IMAGE SENSORS MARKET

- 6.6.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED IMAGE SENSORS

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS AND CERTIFICATIONS

- 7.1.3 REGULATIONS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.5 UNMET NEEDS OF VARIOUS APPLICATIONS

- 8.6 MARKET PROFITABILITY

9 OUTPUTS OF IMAGE SENSORS

- 9.1 INTRODUCTION

- 9.2 ANALOG

- 9.3 DIGITAL

10 TECHNOLOGIES OF IMAGE SENSORS

- 10.1 INTRODUCTION

- 10.2 ROLLING SHUTTER

- 10.3 GLOBAL RESET RELEASE

- 10.4 GLOBAL SHUTTER

- 10.5 POLARIZATION

- 10.6 ULTRAVIOLET

- 10.7 SHORT-WAVE INFRARED

- 10.8 TIME-OF-FLIGHT

- 10.9 EVENT-BASED VISION

- 10.10 MULTISPECTRAL

11 IMAGE SENSORS MARKET, BY TYPE

- 11.1 INTRODUCTION

- 11.2 CMOS

- 11.2.1 COST-EFFECTIVENESS, OPTIMIZED EFFICIENCY, AND RELIABLE PERFORMANCE ATTRIBUTES TO BOOST SEGMENTAL GROWTH

- 11.3 CCD

- 11.3.1 USE IN APPLICATIONS REQUIRING HIGH IMAGE QUALITY, LOW NOISE, AND PRECISE IMAGING TO FUEL SEGMENTAL GROWTH

- 11.4 OTHER TYPES

12 IMAGE SENSORS MARKET, BY PROCESSING TECHNIQUE

- 12.1 INTRODUCTION

- 12.2 2D

- 12.2.1 ABILITY TO OFFER HIGH-QUALITY IMAGE OUTPUT AND LOW POWER CONSUMPTION TO BOLSTER SEGMENTAL GROWTH

- 12.3 3D

- 12.3.1 HIGH ACCURACY AND IMPROVED RECOGNITION TO SUPPORT SEGMENTAL GROWTH

13 IMAGE SENSORS MARKET, BY SPECTRUM

- 13.1 INTRODUCTION

- 13.2 VISIBLE

- 13.2.1 SUITABILITY FOR SCIENTIFIC AND MEDICAL IMAGING, INDUSTRIAL INSPECTION, AND SURVEILLANCE TASKS TO DRIVE MARKET

- 13.2.2 MONOCHROME (MONO) IMAGE SENSORS

- 13.2.3 COLOR IMAGE SENSORS

- 13.3 INFRARED

- 13.3.1 ABILITY TO DETECT HEAT SIGNATURES AND FUNCTION EFFECTIVELY IN LOW-LIGHT CONDITIONS TO FOSTER SEGMENTAL GROWTH

- 13.3.2 NIR & SWIR IMAGE SENSORS

- 13.3.3 MWIR IMAGE SENSORS

- 13.3.4 LWIR IMAGE SENSORS

- 13.3.5 X-RAY IMAGE SENSORS

14 IMAGE SENSORS MARKET, BY ARRAY TYPE

- 14.1 INTRODUCTION

- 14.2 LINE SCAN

- 14.2.1 RISING EMPHASIS ON PRECISE INSPECTION OF MOVING OBJECTS TO BOOST SEGMENTAL GROWTH

- 14.3 AREA SCAN

- 14.3.1 INCREASING NEED FOR PRECISE AND RELIABLE VISUAL DATA TO CONTRIBUTE TO SEGMENTAL GROWTH

15 IMAGE SENSORS MARKET, BY RESOLUTION

- 15.1 INTRODUCTION

- 15.2 VGA

- 15.2.1 SIMPLICITY, EFFICIENCY, AND COMPACT DESIGN TO ACCELERATE SEGMENTAL GROWTH

- 15.3 1.3 TO 3 MP

- 15.3.1 HIGH DEMAND FOR COST-EFFECTIVE AND LOW-POWER SENSORS TO CONTRIBUTE TO SEGMENTAL GROWTH

- 15.4 5 TO 10 MP

- 15.4.1 INCREASED ADOPTION IN MACHINE VISION SYSTEMS AND ADAS APPLICATIONS TO FOSTER SEGMENTAL GROWTH

- 15.5 12 TO 16 MP

- 15.5.1 ABILITY TO PRODUCE SHARP IMAGES WITHOUT INCREASING FILE SIZE OR PROCESSING REQUIREMENTS TO SPUR DEMAND

- 15.6 ABOVE 16 MP

- 15.6.1 STRONG FOCUS ON HIGH-QUALITY IMAGING IN ELECTRONICS, AUTOMOTIVE, AND MANUFACTURING APPLICATIONS TO DRIVE MARKET

16 IMAGE SENSORS MARKET, BY APPLICATION

- 16.1 INTRODUCTION

- 16.2 AUTOMOTIVE

- 16.2.1 SHIFT TOWARD FULLY AUTONOMOUS VEHICLES AND COMPLIANCE WITH STRICT SAFETY STANDARDS TO EXPEDITE SEGMENTAL GROWTH

- 16.2.2 REAR & SIDE-VIEW CAMERAS

- 16.2.3 FORWARD-LOOKING ADAS

- 16.2.4 IN-CABIN ADAS

- 16.2.5 CAMERA MIRROR SYSTEMS

- 16.3 CONSUMER ELECTRONICS

- 16.3.1 ABILITY TO ENHANCE USER EXPERIENCE AND FUNCTIONALITY ACROSS DEVICES TO FACILITATE SEGMENTAL GROWTH

- 16.3.2 SMARTPHONES & TABLETS

- 16.3.3 DESKTOPS & LAPTOPS

- 16.3.4 COMMERCIAL COPIER MACHINES & SCANNERS

- 16.3.5 PHOTOGRAPHY & VIDEOGRAPHY CAMERAS

- 16.3.6 WEARABLES

- 16.3.7 COMMERCIAL DRONES

- 16.3.8 ROBOTS

- 16.3.9 SMART HOME DEVICES

- 16.4 MEDICAL & LIFE SCIENCES

- 16.4.1 FOCUS ON ENHANCING TREATMENT EFFECTIVENESS AND SCIENTIFIC ADVANCEMENTS TO BOOST SEGMENTAL GROWTH

- 16.4.2 X-RAY

- 16.4.3 ENDOSCOPY

- 16.5 INDUSTRIAL

- 16.5.1 HIGH EMPHASIS ON MEETING QUALITY AND SAFETY STANDARDS TO AUGMENT MARKET GROWTH

- 16.5.2 MACHINE VISION

- 16.5.3 ROBOTIC VISION

- 16.6 COMMERCIAL

- 16.6.1 RISING OMNICHANNEL RETAILING AND AUTOMATION TO CONTRIBUTE TO SEGMENTAL GROWTH

- 16.7 SECURITY & SURVEILLANCE

- 16.7.1 MOUNTING ADOPTION OF SMART HOME TECHNOLOGIES FOR SAFETY MEASURES TO EXPEDITE SEGMENTAL GROWTH

- 16.8 AEROSPACE & DEFENSE

- 16.8.1 INCREASING REQUIREMENT FOR SURVEILLANCE AND RECONNAISSANCE SOLUTIONS FOR SITUATIONAL AWARENESS TO DRIVE MARKET

17 IMAGE SENSORS MARKET, BY REGION

- 17.1 INTRODUCTION

- 17.2 NORTH AMERICA

- 17.2.1 US

- 17.2.1.1 Rising deployment of advanced technologies and infrastructure development to bolster market growth

- 17.2.2 CANADA

- 17.2.2.1 Increasing use of smartphones and investment in infrastructure development projects to drive market

- 17.2.3 MEXICO

- 17.2.3.1 Thriving automotive, manufacturing, and consumer electronics industries to fuel market growth

- 17.2.1 US

- 17.3 EUROPE

- 17.3.1 UK

- 17.3.1.1 Mounting demand for high-resolution cameras to accelerate market growth

- 17.3.2 GERMANY

- 17.3.2.1 Rising adoption of digital technologies and focus on Industry 4.0 to expedite market growth

- 17.3.3 FRANCE

- 17.3.3.1 Increasing development of smart city infrastructure and advanced safety systems to drive market

- 17.3.4 REST OF EUROPE

- 17.3.1 UK

- 17.4 ASIA PACIFIC

- 17.4.1 CHINA

- 17.4.1.1 Increasing investment in visual monitoring equipment to augment market growth

- 17.4.2 JAPAN

- 17.4.2.1 Rapid industrial automation and security-related projects to contribute to market growth

- 17.4.3 INDIA

- 17.4.3.1 Expanding consumer electronics manufacturing and emerging autonomous vehicle data collection to drive market

- 17.4.4 REST OF ASIA PACIFIC

- 17.4.1 CHINA

- 17.5 ROW

- 17.5.1 MIDDLE EAST

- 17.5.1.1 Saudi Arabia

- 17.5.1.1.1 Rising development of smart cities and industrial automation to expedite market growth

- 17.5.1.2 UAE

- 17.5.1.2.1 Growing emphasis on urban development and consumer electronics development to drive market

- 17.5.1.3 Rest of Middle East

- 17.5.1.1 Saudi Arabia

- 17.5.2 AFRICA

- 17.5.2.1 Increasing investment in public safety and urban video surveillance infrastructure to support market growth

- 17.5.3 SOUTH AMERICA

- 17.5.3.1 Growing consumption of surveillance cameras and consumer electronics to foster market growth

- 17.5.1 MIDDLE EAST

18 COMPETITIVE LANDSCAPE

- 18.1 OVERVIEW

- 18.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2021-2026

- 18.3 REVENUE ANALYSIS, 2021-2025

- 18.4 MARKET SHARE ANALYSIS, 2O25

- 18.5 COMPANY VALUATION AND FINANCIAL METRICS

- 18.6 BRAND COMPARISON

- 18.6.1 SONY SEMICONDUCTOR SOLUTIONS CORPORATION (JAPAN)

- 18.6.2 SAMSUNG (SOUTH KOREA)

- 18.6.3 OMNIVISION (US)

- 18.6.4 SEMICONDUCTOR COMPONENTS INDUSTRIES, LLC (US)

- 18.6.5 STMICROELECTRONICS (SWITZERLAND)

- 18.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 18.7.1 STARS

- 18.7.2 EMERGING LEADERS

- 18.7.3 PERVASIVE PLAYERS

- 18.7.4 PARTICIPANTS

- 18.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 18.7.5.1 Company footprint

- 18.7.5.2 Region footprint

- 18.7.5.3 Type footprint

- 18.7.5.4 Spectrum footprint

- 18.7.5.5 Application footprint

- 18.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 18.8.1 PROGRESSIVE COMPANIES

- 18.8.2 RESPONSIVE COMPANIES

- 18.8.3 DYNAMIC COMPANIES

- 18.8.4 STARTING BLOCKS

- 18.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 18.8.5.1 Detailed list of key startups/SMEs

- 18.8.5.2 Competitive benchmarking of key startups/SMEs

- 18.9 COMPETITIVE SCENARIO

- 18.9.1 PRODUCT LAUNCHES

- 18.9.2 DEALS

19 COMPANY PROFILES

- 19.1 KEY PLAYERS

- 19.1.1 SONY SEMICONDUCTOR SOLUTIONS CORPORATION

- 19.1.1.1 Business overview

- 19.1.1.2 Products/Solutions/Services offered

- 19.1.1.3 Recent developments

- 19.1.1.3.1 Product launches

- 19.1.1.3.2 Deals

- 19.1.1.4 MnM view

- 19.1.1.4.1 Key strengths/Right to win

- 19.1.1.4.2 Strategic choices

- 19.1.1.4.3 Weaknesses/Competitive threats

- 19.1.2 SAMSUNG

- 19.1.2.1 Business overview

- 19.1.2.2 Products/Solutions/Services offered

- 19.1.2.3 Recent developments

- 19.1.2.3.1 Product launches

- 19.1.2.3.2 Deals

- 19.1.2.4 MnM view

- 19.1.2.4.1 Key strengths/Right to win

- 19.1.2.4.2 Strategic choices

- 19.1.2.4.3 Weaknesses/Competitive threats

- 19.1.3 OMNIVISION

- 19.1.3.1 Business overview

- 19.1.3.2 Products/Solutions/Services offered

- 19.1.3.3 Recent developments

- 19.1.3.3.1 Product launches

- 19.1.3.3.2 Deals

- 19.1.3.4 MnM view

- 19.1.3.4.1 Key strengths/Right to win

- 19.1.3.4.2 Strategic choices

- 19.1.3.4.3 Weaknesses/Competitive threats

- 19.1.4 STMICROELECTRONICS

- 19.1.4.1 Business overview

- 19.1.4.2 Products/Solutions/Services offered

- 19.1.4.3 Recent developments

- 19.1.4.3.1 Product launches

- 19.1.4.3.2 Deals

- 19.1.4.4 MnM view

- 19.1.4.4.1 Key strengths/Right to win

- 19.1.4.4.2 Strategic choices

- 19.1.4.4.3 Weaknesses/Competitive threats

- 19.1.5 SEMICONDUCTOR COMPONENTS INDUSTRIES, LLC

- 19.1.5.1 Business overview

- 19.1.5.2 Products/Solutions/Services offered

- 19.1.5.3 Recent developments

- 19.1.5.3.1 Product launches

- 19.1.5.3.2 Deals

- 19.1.5.4 MnM view

- 19.1.5.4.1 Key strengths/Right to win

- 19.1.5.4.2 Strategic choices

- 19.1.5.4.3 Weaknesses/Competitive threats

- 19.1.6 GALAXYCORE SHANGHAI LIMITED CORPORATION

- 19.1.6.1 Business overview

- 19.1.6.2 Products/Solutions/Services offered

- 19.1.6.3 Recent developments

- 19.1.6.3.1 Product launches

- 19.1.6.3.2 Deals

- 19.1.6.4 MnM view

- 19.1.6.4.1 Key strengths/Right to win

- 19.1.6.4.2 Strategic choices

- 19.1.6.4.3 Weaknesses/Competitive threats

- 19.1.7 HAMAMATSU PHOTONICS K.K.

- 19.1.7.1 Business overview

- 19.1.7.2 Products/Solutions/Services offered

- 19.1.7.3 Recent developments

- 19.1.7.3.1 Deals

- 19.1.8 INFINEON TECHNOLOGIES AG

- 19.1.8.1 Business overview

- 19.1.8.2 Products/Solutions/Services offered

- 19.1.8.3 Recent developments

- 19.1.8.3.1 Deals

- 19.1.9 CANON INC.

- 19.1.9.1 Business overview

- 19.1.9.2 Products/Solutions/Services offered

- 19.1.9.3 Recent developments

- 19.1.9.3.1 Product launches

- 19.1.10 TELEDYNE TECHNOLOGIES INCORPORATED

- 19.1.10.1 Business overview

- 19.1.10.2 Products/Solutions/Services offered

- 19.1.10.3 Recent developments

- 19.1.10.3.1 Product launches

- 19.1.10.3.2 Deals

- 19.1.1 SONY SEMICONDUCTOR SOLUTIONS CORPORATION

- 19.2 OTHER PLAYERS

- 19.2.1 PIXART IMAGING INC.

- 19.2.2 PIXELPLUS

- 19.2.3 HIMAX TECHNOLOGIES, INC.

- 19.2.4 SHARP CORPORATION

- 19.2.5 GPIXEL MICROELECTRONICS INC.

- 19.2.6 NUVOTON TECHNOLOGY CORPORATION

- 19.2.7 DIODES INCORPORATED

- 19.2.8 ISDI LIMITED

- 19.2.9 ANDANTA GMBH

- 19.2.10 PHOTONFOCUS AG

- 19.2.11 NEW IMAGING TECHNOLOGIES (NIT)

- 19.2.12 BRIGATES ELECTRONICS CO., LTD.

- 19.2.13 AMS-OSRAM AG

- 19.2.14 IMASENIC ADVANCED IMAGING S.L.

- 19.2.15 VOXELSENSORS SRL/BV

- 19.2.16 IC-HAUS

- 19.2.17 FRAMOS GMBH

20 RESEARCH METHODOLOGY

- 20.1 RESEARCH DATA

- 20.1.1 SECONDARY DATA

- 20.1.1.1 List of key secondary sources

- 20.1.1.2 Key data from secondary sources

- 20.1.2 PRIMARY DATA

- 20.1.2.1 List of primary interview participants

- 20.1.2.2 Breakdown of primary interviews

- 20.1.2.3 Key data from primary sources

- 20.1.2.4 Key industry insights

- 20.1.3 SECONDARY AND PRIMARY RESEARCH

- 20.1.1 SECONDARY DATA

- 20.2 MARKET SIZE ESTIMATION

- 20.2.1 BOTTOM-UP APPROACH

- 20.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 20.2.2 TOP-DOWN APPROACH

- 20.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

- 20.2.1 BOTTOM-UP APPROACH

- 20.3 MARKET FORECAST APPROACH

- 20.3.1 DEMAND-SIDE

- 20.3.2 SUPPLY-SIDE

- 20.4 DATA TRIANGULATION

- 20.5 RESEARCH ASSUMPTIONS

- 20.6 RESEARCH LIMITATIONS

- 20.7 RISK ANALYSIS

21 APPENDIX

- 21.1 INSIGHTS FROM INDUSTRY EXPERTS

- 21.2 DISCUSSION GUIDE

- 21.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 21.4 CUSTOMIZATION OPTIONS

- 21.5 RELATED REPORTS

- 21.6 AUTHOR DETAILS