|

시장보고서

상품코드

2060323

대형 건설기계 시장 예측(-2033년) : 유형(굴착기, 로더, 불도저, 덤프트럭, 컴팩터, 크레인), 추진 방식, 출력, 엔진 배기량, 용도, 배터리 화학 조성, 지역별Heavy Construction Equipment Market By Equipment Type (Excavator, Loader, Dozer, Dump Truck, Compactor, Crane), Propulsion, Power Output, Engine Capacity, Application, Battery Chemistry, and Region - Global Forecast to 2033 |

||||||

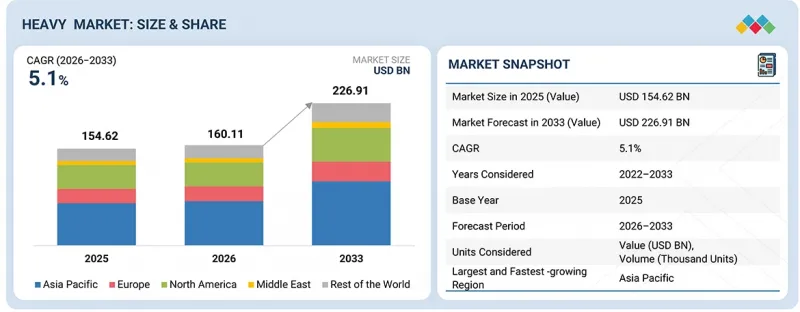

대형 건설기계 시장 규모는 2026년 1,601억 1,000만 달러에서 2033년에는 2,269억 1,000만 달러에 달하며, CAGR 5.1%로 성장할 것으로 예측됩니다.

시장 전반의 성장은 아시아 각국의 주거, 비주거, 상업 부문에 대한 인프라 투자가 지속적으로 증가하고 있는 데 힘입고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2033년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2033년 |

| 단위 | 달러 |

| 부문 | 기기 유형, 추진 방식, 출력, 엔진 배기량, 용도, 배터리 화학 조성, 지역 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동, 기타 지역 |

또한 유럽과 북미에서 건설 기계의 전기화 추세도 향후 수년간 건설 기계 수요를 끌어올릴 것으로 보입니다.

배터리 화학 성분별로는 인산철리튬(LFP) 부문이 예측 기간 중 가장 높은 성장률을 보일 것으로 전망된다

이러한 성장은 아시아태평양에서 가동률이 높은 건설 기계의 전기화가 진전되고 있는 데 힘입은 것입니다. 특히 전기 굴착기, 전기 휠로더, 전기 덤프트럭에 대한 수요가 광업 및 대규모 토목 공사 분야에서 확대되고 있습니다. 또한 LFP 배터리는 높은 열 안정성, 긴 사이클 수명, 고부하 환경에서도 안정적인 성능을 갖추고 있으며, 건설 기계 용도에 적합합니다.

Caterpillar, Komatsu, XCMG Group, SANY Group, Volvo Construction Equipment 등 주요 OEM 업체들은 로더, 굴착기, 광산 기계용 제품군에 LFP 배터리 시스템 도입을 적극적으로 추진하고 있습니다. 지역별로 보면 도입 현황은 기종에 따라 다릅니다. 중국에서는 강력한 정책 추진과 도시 지역의 배기가스 규제의 지원으로 전동 로더의 도입이 주도되고 있으며, 이는 로더 총판매량의 약 6-10%를 차지하는 것으로 추정됩니다. 이에 이어, 전동 광산용 굴착기나 보급이 막 시작된 전동 불도저의 도입도 진행되고 있습니다. 중국을 제외한 아시아 전역에서는 비용에 대한 민감성과 충전 인프라 부족으로 인해 도입이 여전히 초기 단계에 머물러 있으며, 소형 굴착기나 소형 로더의 시범 도입으로 한정되어 있습니다. 유럽에서는 소형 건설기계 분야에서 전동화가 진행되고 있으며, 전동 미니 굴착기와 소형 로더의 보급률이 가장 높습니다. 엄격한 배출 규제, 도시 지역 공사 현장의 요건, 건설업체의 조기 도입이 그 요인입니다. 전반적으로 중국은 대형 건설 기계의 전기화 규모 면에서 세계를 선도하고 있는 반면, 유럽은 소형 건설 기계의 조기 보급을 주도하고 있습니다. 다른 아시아 시장들도 시범 도입을 통해 서서히 뒤를 따르고 있습니다.

기계 카테고리별로는 토공 기계 부문이 예측 기간 중 가장 큰 규모와 가장 높은 성장률을 보일 것으로 전망된다

기기 카테고리별로 보면 토목·건설 기계 부문은 시장 전체의 60% 이상의 점유율을 차지할 것으로 예상됩니다. 이러한 성장은 광업, 표토 제거, 대규모 토공 작업 분야에서 크롤러 굴착기, 덤프트럭, 휠로더, 모터그레이더에 대한 강력한 수요에 힘입어 이루어지고 있습니다. 그중에서도 크롤러 굴착기는 연속 가동 및 고부하 용도에서의 높은 가동률에 힘입어 이 부문을 주도하고 있습니다. 아시아태평양은 광산 확장, 채석 작업, 재생에너지 발전소 부지 조성 분야의 활동 증가를 배경으로, 중국과 인도가 주도적인 역할을 맡아 50% 이상의 점유율로 토공 기계 시장을 이끌 것으로 추정됩니다.

각 OEM 업체들의 최근 동향도 이 부문을 더욱 강화하고 있습니다. 코마츠는 생산성 향상과 톤당 비용 절감에 중점을 둔 PC9000 등 차세대 대형 광산용 굴착기를 출시하는 한편, 지능형 기계 제어(IMC 3.0)가 탑재된 굴착기 라인업을 확대하고 있습니다. 볼보 건설기계(Volvo Construction Equipment)는 전 세계에서 증가하는 수요에 대응하기 위해 크롤러 굴착기의 생산 능력을 확대하고 있습니다. 또한 Caterpillar, Hitachi Construction Machinery, SANY, XCMG 등 각 OEM 업체들은 전동화 대응 플랫폼, AI 탑재 텔레매틱스, 저연비 유압 시스템의 개발을 추진하고 있습니다. 이러한 개발을 통해 기계의 효율, 가동률, 성능이 향상되어 토목·건설 기계 부문의 성장이 촉진되고 있습니다.

이 보고서에서는 전 세계 대형 건설기계 시장을 조사하여, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 현황, 주요 기업 개요 등을 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신, 향후 전략적 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 대형 건설기계 시장 : 기기 유형별

제10장 대형 건설기계 시장 : 기기 카테고리별

제11장 대형 건설기계 시장 : 용도별

제12장 대형 건설기계 시장 : 엔진 배기량별

제13장 대형 건설기계 시장 : 출력별

제14장 대형 건설기계 건설기계 시장 : 후처리 장비별

제15장 대형 건설기계 시장 : 추진 방식별

제16장 대형 건설기계 렌탈 시장 : 용도별

제17장 전기식 및 하이브리드식 대형 건설기계 시장 : 기기 유형별

제18장 전동 대형 건설기계 시장 : 배터리 화학 조성별

제19장 자율형 대형 건설기계 시장 : 지역별

제20장 대형 건설기계 시장 : 지역별

제21장 경쟁 구도

제22장 기업 개요

제23장 조사 방법

제24장 부록

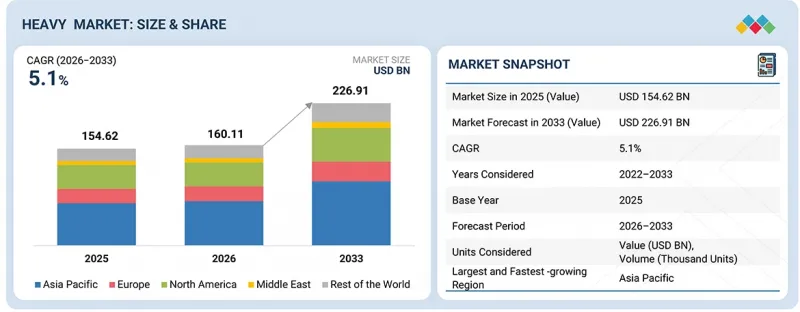

KSA 26.06.25The heavy construction equipment market is projected to grow from USD 160.11 billion in 2026 to USD 226.91 billion by 2033, at a CAGR of 5.1%. The overall market growth is propelled by the continuously increasing infrastructural investments in residential, non-residential, and commercial sectors in Asian countries.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | USD Billion |

| Segments | Equipment Type, Propulsion, Power Output, Engine Capacity, Application, Battery Chemistry, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East, and Rest of the World |

Additionally, the inclination toward the electrification of construction equipment in Europe and North America will boost the demand for construction equipment in the coming years.

The lithium iron phosphate (LFP) segment is expected to be the fastest-growing segment during the forecast period.

By battery chemistry, lithium iron phosphate (LFP) is expected to be the fastest-growing segment during the forecast period. This growth is driven by increasing electrification of high-utilization equipment in Asia Pacific, where demand for electric excavators, loaders, and dump trucks is rising across mining and large-scale earthmoving applications. Additionally, these batteries offer high thermal stability, long cycle life, and consistent performance under heavy-duty conditions, making them well-suited for construction equipment.

Major OEMs such as Caterpillar Inc., Komatsu Ltd., XCMG Group, SANY Group, and Volvo Construction Equipment are actively integrating LFP battery systems across loaders, excavators, and mining equipment portfolios. Regionally, adoption trends vary by equipment type. In China, electric loaders lead adoption, already accounting for an estimated ~6-10% of total loader sales, driven by strong policy push and urban emission controls, followed by electric mining excavators and gradually emerging electrified bulldozers. Across broader Asia (excluding China), adoption remains nascent, primarily focused on pilot deployments of compact excavators and small loaders due to cost sensitivity and limited charging infrastructure. In Europe, the transition is more advanced in compact equipment, with electric mini excavators and compact loaders seeing the highest penetration due to stringent emission norms, urban jobsite requirements, and early contractor adoption. Overall, while China is leading in heavy equipment electrification scale, Europe is driving early adoption in compact machinery, with other Asian markets gradually following through pilot-scale deployments.

The earthmoving equipment segment is expected to be the largest and fastest-growing equipment segment during the forecast period.

By equipment category, the earthmoving equipment segment is expected to account for more than 60% share of the heavy construction equipment market. This growth is driven by strong demand for crawler excavators, dump trucks, wheel loaders, and motor graders across mining, overburden removal, and large-scale earthmoving operations. Among these, crawler excavators dominate the segment, supported by their high utilization in continuous-duty and high-load applications. Asia Pacific is estimated to lead the earthmoving equipment market with more than 50% share, driven by China and India due to increasing activity in mining expansion, quarrying operations, and renewable energy site preparation.

Recent developments by OEMs are further strengthening this segment. Komatsu has launched next-generation large mining excavators, such as the PC9000, focusing on higher productivity and lower cost per ton, while also expanding its intelligent machine control (IMC 3.0) excavator range. Volvo Construction Equipment is increasing crawler excavator production capacity to meet rising global demand, and OEMs such as Caterpillar, Hitachi Construction Machinery, SANY, and XCMG are advancing electrification-ready platforms, AI-enabled telematics, and fuel-efficient hydraulic systems. These developments are enhancing machine efficiency, uptime, and performance, thereby driving the growth of the earthmoving equipment segment.

"North America is the world's second-largest heavy construction equipment market."

North America is the second-largest market for heavy construction equipment globally, with the US acting as the key demand driver. This trend is expected to continue into the forecast period. The market in the region is experiencing a slowdown in 2024-2025 due to inflationary pressures, high interest rates, and project financing constraints, impacting equipment demand in the short term. However, the market is expected to recover from late 2026 onwards, supported by renewed activity in mining operations, energy projects, and large-scale earthmoving applications.

Growth in the region is further driven by fleet modernization, replacement demand for high-capacity equipment, and rising adoption of advanced machinery with telematics and automation capabilities. Government-backed investments, particularly under infrastructure and energy transition programs, are supporting demand for high-horsepower equipment used in road rehabilitation, grid expansion, and industrial site development.

Additionally, the strong penetration of equipment rental models is enabling contractors to access advanced heavy machinery in a cost-efficient manner during uncertain economic cycles. The growing focus on low-emission and fuel-efficient equipment, including hybrid and electric platforms, is further influencing purchasing decisions in the region. Key players in the North American heavy construction equipment market include Caterpillar (US), Deere & Company (US), Terex Corporation (US), and Komatsu (Japan), all focusing on digitally integrated machines, electrification strategies, and productivity-enhancing technologies, thereby supporting long-term market growth.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and strategy directors, and executives from various key organizations operating in this market.

- By Company Type: Construction Equipment Manufacturers - 60%, and Rental Companies - 40%

- By Designation: CXOs - 40%, Directors - 40%, and Others - 20%

- By Region: Asia Pacific - 40%, North America - 20%, Europe - 15%, Middle East - 5%, and Rest of the World - 20%

The heavy construction equipment market is led by established players such as Caterpillar (US), Komatsu Ltd. (Japan), Xuzhou Construction Machinery Group (China), and Deere & Company (US).

Key Benefits of Buying the Report:

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall heavy construction equipment market and the sub-segments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (Growth in infrastructural development projects and adoption of advanced construction technologies), restraints (Stringent emission and regulatory standards), opportunities (Growth of electric and sustainable construction equipment, increasing equipment rental and leasing demand, digitalization and smart fleet management and accelerated replacement of aging fleets in developed markets), and challenges (Skilled labor shortage in equipment operations and economic and construction industry cyclicality) influencing the growth of heavy construction equipment market.

Product Development/Innovation: Detailed insights on upcoming technologies, research development activities, and new products & services of the heavy construction equipment market

Market Development: Comprehensive information about the lucrative market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the heavy construction equipment market

Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Caterpillar (US), Komatsu Ltd. (Japan), Hitachi Construction Machinery Co., Ltd. (Japan), Xuzhou Construction Machinery Group (China), and Deere & Company (US) in the heavy construction equipment market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN HEAVY CONSTRUCTION EQUIPMENT MARKET

- 2.4 HIGH-GROWTH SEGMENTS IN HEAVY CONSTRUCTION EQUIPMENT MARKET

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ELECTRIC HEAVY CONSTRUCTION EQUIPMENT MARKET

- 3.2 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY EQUIPMENT TYPE

- 3.3 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY APPLICATION

- 3.4 RENTAL HEAVY CONSTRUCTION EQUIPMENT MARKET, BY APPLICATION

- 3.5 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY EQUIPMENT CATEGORY

- 3.6 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY AFTER-TREATMENT DEVICE

- 3.7 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY PROPULSION

- 3.8 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY POWER OUTPUT

- 3.9 AUTONOMOUS HEAVY CONSTRUCTION EQUIPMENT MARKET, BY REGION

- 3.10 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY ENGINE CAPACITY

- 3.11 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY BATTERY CHEMISTRY

- 3.12 ELECTRIC & HYBRID HEAVY CONSTRUCTION EQUIPMENT MARKET, BY EQUIPMENT TYPE

- 3.13 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growth in infrastructural development projects

- 4.2.1.2 Adoption of advanced construction technologies

- 4.2.2 RESTRAINTS

- 4.2.2.1 Stringent emission and regulatory standards

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growth of electric and sustainable heavy construction equipment

- 4.2.3.2 Increasing rental equipment and leasing demand

- 4.2.3.3 Digitalization and smart fleet management

- 4.2.3.4 Accelerated replacement of aging fleets in developed markets

- 4.2.4 CHALLENGES

- 4.2.4.1 Shortage of skilled labor for equipment operations

- 4.2.4.2 Economic and construction industry cyclicality

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC OUTLOOK

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.3 TRENDS IN GLOBAL HEAVY CONSTRUCTION INDUSTRY

- 5.1.3.1 Regional GDP dynamics

- 5.1.3.2 Developed markets

- 5.1.3.3 Emerging markets

- 5.1.3.3.1 China

- 5.1.3.3.2 India

- 5.1.3.3.3 Brazil

- 5.1.3.3.4 Mexico

- 5.1.3.3.5 Indonesia

- 5.1.3.3.6 Thailand

- 5.1.3.3.7 Malaysia

- 5.1.3.4 Investment environment

- 5.2 PRICING ANALYSIS

- 5.3 ECOSYSTEM ANALYSIS

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 CASE STUDY ANALYSIS

- 5.5.1 KOMATSU SMART CONSTRUCTION ENHANCING DIGITAL INFRASTRUCTURE PROJECTS

- 5.5.2 SCALING PROVEN AUTONOMY SYSTEM TO SUPPORT NEW INDUSTRIES

- 5.5.3 PREDICTIVE MAINTENANCE

- 5.5.4 LOW-CARBON CONSTRUCTION MACHINERY

- 5.5.5 SMART HEAVY CONSTRUCTION EQUIPMENT BY SRI INTERNATIONAL RESEARCH INSTITUTE

- 5.6 PATENT ANALYSIS

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO OF HEAVY CONSTRUCTION EQUIPMENT

- 5.8 EXPORT SCENARIO OF HEAVY CONSTRUCTION EQUIPMENT

- 5.9 INVESTMENT SCENARIO

- 5.10 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.11 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.12 HEAVY CONSTRUCTION EQUIPMENT MARKET: OEM ANALYSIS

- 5.12.1 BATTERY CAPACITY OF ELECTRIC HEAVY CONSTRUCTION EQUIPMENT OFFERED BY OEMS

- 5.12.2 BACKHOE LOADER OFFERINGS BY OEMS, 2025

- 5.12.3 TRACK LOADER OFFERINGS BY OEMS, 2025

- 5.12.4 SKID STEER LOADER OFFERINGS BY OEMS, 2025

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE STRATEGIC APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Autonomous heavy construction equipment

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Monitoring and diagnosis via connected technologies

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Grade control systems

- 6.1.1 KEY TECHNOLOGIES

- 6.2 IMPACT OF AI/GENERATIVE AI

- 6.3 IMPACT OF EU-INDIA TRADE DEAL ON HEAVY CONSTRUCTION EQUIPMENT MARKET

- 6.4 IMPACT OF ISRAEL-IRAN CONFLICT ON AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 6.5 IMPACT OF ISRAEL-IRAN WAR ON HEAVY CONSTRUCTION EQUIPMENT MARKET

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 ELECTRIFICATION AND ALTERNATIVE POWERTRAINS

- 7.2.2 LOW-EMISSION AND FUEL-EFFICIENT TECHNOLOGIES

- 7.2.3 SMART TELEMATICS AND DIGITAL OPTIMIZATION

- 7.2.4 SUSTAINABLE MANUFACTURING PRACTICES

- 7.2.5 EQUIPMENT LIFECYCLE MANAGEMENT & CIRCULAR ECONOMY

- 7.2.6 NOISE AND URBAN IMPACT REDUCTION

- 7.2.7 SUSTAINABLE CONSTRUCTION PRACTICES INTEGRATION

- 7.2.8 REGULATORY ANALYSIS OF HEAVY CONSTRUCTION EQUIPMENT MARKET

- 7.2.9 NON-ROAD MOBILE MACHINERY REGULATIONS OUTLOOK, 2019-2033

- 7.2.9.1 North America

- 7.2.9.1.1 US

- 7.2.9.2 European Union

- 7.2.9.3 Asia Pacific

- 7.2.9.3.1 China

- 7.2.9.3.2 India

- 7.2.9.1 North America

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END USERS/END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY EQUIPMENT TYPE

- 9.1 INTRODUCTION

- 9.2 ARTICULATED DUMP TRUCKS

- 9.2.1 SMART, HIGH-PERFORMANCE HAULAGE DRIVING GROWTH

- 9.3 ASPHALT FINISHERS

- 9.3.1 EXPANSION OF ROAD INFRASTRUCTURE AND URBAN REPAIR PROJECTS TO SUSTAIN DEMAND

- 9.4 BACKHOE LOADERS

- 9.4.1 SMART CITY PROJECTS AND URBAN INFRA DEVELOPMENT DRIVING STEADY DEMAND

- 9.5 CRAWLER DOZERS

- 9.5.1 LARGE-SCALE INFRASTRUCTURE AND MINING PROJECTS TO DRIVE DEMAND

- 9.6 CRAWLER EXCAVATORS

- 9.6.1 SHIFT TOWARD HIGH-PERFORMANCE AND INTELLIGENT MACHINES DRIVING MARKET GROWTH

- 9.7 CRAWLER LOADERS

- 9.7.1 INTEGRATION OF SMART TECHNOLOGIES AND MULTI-FUNCTIONALITY TO SUPPORT DEMAND

- 9.8 MINI EXCAVATORS

- 9.8.1 URBANIZATION AND SPACE-CONSTRAINED PROJECTS DRIVING DEMAND

- 9.9 MOTOR GRADERS

- 9.9.1 ROAD INFRASTRUCTURE PROGRAMS AND MAINTENANCE SPENDING DRIVING DEMAND

- 9.10 MOTOR SCRAPERS

- 9.10.1 HIGH-VOLUME EARTHMOVING REQUIREMENTS IN LARGE PROJECTS DRIVING DEMAND

- 9.11 ROAD ROLLERS

- 9.11.1 ACCELERATION OF ROAD PROJECTS IN ASIA PACIFIC SUPPORTING DEMAND

- 9.12 RIGID DUMP TRUCKS

- 9.12.1 HIGH-PRODUCTIVITY HAULING AND AUTONOMOUS OPERATIONS DRIVING DEMAND

- 9.13 ROUGH TERRAIN LIFTING TRUCK (RTLT) MASTED

- 9.13.1 INCREASING DEMAND FOR MATERIAL HANDLING IN CHALLENGING SITE CONDITIONS DRIVING GROWTH

- 9.14 ROUGH TERRAIN LIFTING TRUCK (RTLT) TELESCOPIC

- 9.14.1 POWERTRAIN INNOVATION AND VERSATILITY DRIVING MARKET ADOPTION

- 9.15 SKID-STEER LOADERS

- 9.15.1 FOCUS ON ENERGY EFFICIENCY AND MULTI-ATTACHMENT CAPABILITY DRIVING DEMAND

- 9.16 WHEELED EXCAVATORS

- 9.16.1 MOBILITY AND OPERATIONAL FLEXIBILITY DRIVING MARKET ADOPTION

- 9.17 WHEELED LOADERS <80 HP

- 9.17.1 HIGH PRODUCTIVITY IN MATERIAL HANDLING AND LOADING OPERATIONS DRIVING DEMAND

- 9.18 WHEELED LOADERS >80 HP

- 9.18.1 DEPLOYMENT IN LARGE-SCALE INFRASTRUCTURE PROJECTS DRIVING MARKET GROWTH

- 9.19 COMPACTORS

- 9.19.1 GROWING ROLE IN WASTE MANAGEMENT AND INFRASTRUCTURE PROJECTS DRIVING DEMAND

- 9.20 PICK & CARRY CRANES

- 9.20.1 VERSATILITY IN MATERIAL HANDLING ACROSS CONSTRUCTION SITES DRIVING DEMAND

- 9.21 INDUSTRY INSIGHTS

10 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY EQUIPMENT CATEGORY

- 10.1 INTRODUCTION

- 10.2 EARTHMOVING EQUIPMENT

- 10.2.1 SURGE IN EXCAVATOR DEMAND ACROSS INFRASTRUCTURE AND MINING PROJECTS DRIVING OEM GROWTH

- 10.3 MATERIAL HANDLING EQUIPMENT

- 10.3.1 INDUSTRIAL AND LOGISTICS INFRASTRUCTURE EXPANSION DRIVING OEM-LED DEMAND

- 10.4 HEAVY-DUTY EQUIPMENT

- 10.4.1 SURGE IN ROAD, TUNNEL, AND MEGA TRANSPORT PROJECTS DRIVING OEM-LED DEMAND

- 10.5 OTHER EQUIPMENT

- 10.6 INDUSTRY INSIGHTS

11 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 INFRASTRUCTURE

- 11.2.1 RISING GLOBAL INFRASTRUCTURE SPENDING DRIVING OEM-LED EQUIPMENT DEMAND

- 11.3 COMMERCIAL

- 11.3.1 RAPID EXPANSION OF COMMERCIAL REAL ESTATE AND MIXED-USE PROJECTS DRIVING OEM DEMAND

- 11.4 RESIDENTIAL

- 11.4.1 SHIFT TOWARD PREMIUM HOUSING AND HIGH-DENSITY URBAN PROJECTS DRIVING OEM DEMAND

- 11.5 INDUSTRY INSIGHTS

12 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY ENGINE CAPACITY

- 12.1 INTRODUCTION

- 12.2 <5 L

- 12.2.1 RAPID URBAN INFRASTRUCTURE EXPANSION IN ASIA PACIFIC DRIVING DEMAND

- 12.3 5-10 L

- 12.3.1 HEAVY LOAD HANDLING AND MID-SCALE PROJECT EXECUTION DRIVING DEMAND

- 12.4 >10 L

- 12.4.1 DEPLOYMENT IN HIGH-INTENSITY MINING AND MEGA INFRA PROJECTS DRIVING DEMAND

- 12.5 INDUSTRY INSIGHTS

13 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY POWER OUTPUT

- 13.1 INTRODUCTION

- 13.2 <100 HP

- 13.2.1 ROAD MAINTENANCE AND URBAN PROJECTS DRIVING DEMAND

- 13.3 101-200 HP

- 13.3.1 OPTIMAL POWER AND COST BALANCE DRIVING ADOPTION IN CORE CONSTRUCTION SEGMENTS

- 13.4 201-400 HP

- 13.4.1 INFRASTRUCTURE EXECUTION PHASE DEMAND DRIVING SEGMENT GROWTH

- 13.5 >400 HP

- 13.5.1 MEGA TRANSPORT, MINING, AND INDUSTRIAL PROJECTS DRIVING HIGH-POWER EQUIPMENT DEMAND

- 13.6 INDUSTRY INSIGHTS

14 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY AFTER-TREATMENT DEVICE

- 14.1 INTRODUCTION

- 14.2 EXHAUST GAS RECIRCULATION (EGR)

- 14.2.1 INTEGRATION WITH ADVANCED AFTER-TREATMENT SYSTEMS TO MEET GLOBAL EMISSION NORMS

- 14.3 DIESEL OXIDATION CATALYST (DOC)

- 14.3.1 INTEGRATION WITH MULTI-STAGE AFTER-TREATMENT SYSTEMS TO MEET EVOLVING EMISSION NORMS

- 14.4 DIESEL PARTICULATE FILTER (DPF)

- 14.4.1 MANDATORY INTEGRATION UNDER STAGE V AND TIER 4 FINAL NORMS DRIVING OEM ADOPTION

- 14.5 SELECTIVE CATALYTIC REDUCTION (SCR)

- 14.5.1 CRITICAL ROLE IN NOX REDUCTION UNDER GLOBAL EMISSION NORMS DRIVING OEM ADOPTION

- 14.6 INDUSTRY INSIGHTS

15 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY PROPULSION

- 15.1 INTRODUCTION

- 15.2 DIESEL

- 15.2.1 HIGH TORQUE PERFORMANCE AND REGIONAL ADOPTION OF CLEANER BLENDS TO SUPPORT GROWTH

- 15.3 CNG/LNG/RNG

- 15.3.1 RISING ADOPTION OF ALTERNATIVE FUELS SUPPORTED BY EMISSION-FOCUSED TRANSITION

- 15.4 INDUSTRY INSIGHTS

16 HEAVY CONSTRUCTION EQUIPMENT RENTAL MARKET, BY APPLICATION

- 16.1 INTRODUCTION

- 16.2 INFRASTRUCTURE

- 16.2.1 INCREASE IN NUMBER OF PROJECTS THAT DO NOT REQUIRE LONG-TERM EQUIPMENT OWNERSHIP TO DRIVE MARKET

- 16.3 COMMERCIAL

- 16.3.1 ACCESS TO LATEST AND MOST EFFICIENT EQUIPMENT TO DRIVE DEMAND

- 16.4 RESIDENTIAL

- 16.4.1 LOW INITIAL INVESTMENT IN RESIDENTIAL CONSTRUCTION TO DRIVE GROWTH

- 16.5 INDUSTRY INSIGHTS

17 ELECTRIC & HYBRID HEAVY CONSTRUCTION EQUIPMENT MARKET, BY EQUIPMENT TYPE

- 17.1 INTRODUCTION

- 17.2 ELECTRIC DUMP TRUCKS

- 17.2.1 RISING DECARBONIZATION TARGETS AND SMART MINING PROJECTS TO ACCELERATE DEMAND

- 17.3 ELECTRIC DOZERS

- 17.3.1 DECARBONIZATION AND LOWER TCO TO DRIVE ADOPTION

- 17.4 ELECTRIC EXCAVATORS

- 17.4.1 RISING DEMAND FOR MINI EXCAVATORS AND ZERO-EMISSION JOBSITES TO DRIVE GROWTH

- 17.5 ELECTRIC MOTOR GRADERS

- 17.5.1 EARLY-STAGE ELECTRIFICATION AND ZERO-EMISSION MINING INITIATIVES TO DRIVE DEMAND

- 17.6 ELECTRIC LOADERS

- 17.6.1 COMPACT EQUIPMENT ELECTRIFICATION AND HYBRID INNOVATION TO ACCELERATE MARKET EXPANSION

- 17.7 ELECTRIC LOAD HAUL DUMP (LHD) LOADERS

- 17.7.1 URBAN CONSTRUCTION, TUNNELING, AND LOW-EMISSION PROJECTS TO DRIVE ADOPTION

- 17.8 INDUSTRY INSIGHTS

18 ELECTRIC HEAVY CONSTRUCTION EQUIPMENT MARKET, BY BATTERY CHEMISTRY

- 18.1 INTRODUCTION

- 18.2 LITHIUM IRON PHOSPHATE (LFP)

- 18.2.1 SAFETY, COST ADVANTAGE, AND SUPPLY CHAIN LOCALIZATION TO ACCELERATE ADOPTION

- 18.3 LITHIUM NICKEL MANGANESE COBALT (NMC)

- 18.3.1 HIGH ENERGY DENSITY TO SUPPORT PERFORMANCE-DRIVEN APPLICATIONS

- 18.4 OTHER BATTERY CHEMISTRIES

- 18.5 INDUSTRY INSIGHTS

19 AUTONOMOUS HEAVY CONSTRUCTION EQUIPMENT MARKET, BY REGION

- 19.1 INTRODUCTION

- 19.2 AUTONOMOUS HEAVY CONSTRUCTION EQUIPMENT PRODUCT/SERVICE OFFERINGS BY KEY OEMS

- 19.3 AI DEVELOPMENTS IN AUTONOMOUS HEAVY CONSTRUCTION EQUIPMENT MARKET

20 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY REGION

- 20.1 INTRODUCTION

- 20.2 ASIA PACIFIC

- 20.2.1 CHINA

- 20.2.1.1 Infrastructure stimulus and equipment modernization to drive market

- 20.2.2 INDIA

- 20.2.2.1 Government infrastructure initiatives and equipment localization to drive market

- 20.2.3 JAPAN

- 20.2.3.1 Infrastructure modernization and automation adoption to drive market

- 20.2.4 INDONESIA

- 20.2.4.1 Infrastructure expansion and capital relocation to drive market

- 20.2.5 REST OF ASIA PACIFIC

- 20.2.1 CHINA

- 20.3 EUROPE

- 20.3.1 GERMANY

- 20.3.1.1 Government infrastructure investments and demand for advanced equipment to drive market

- 20.3.2 UK

- 20.3.2.1 Government-led infrastructure and energy projects to drive market

- 20.3.3 FRANCE

- 20.3.3.1 Public infrastructure and energy transition investments to drive market

- 20.3.4 ITALY

- 20.3.4.1 Public infrastructure upgrades and energy transition investments to drive market

- 20.3.5 SPAIN

- 20.3.5.1 Transport modernization and renewable energy projects to drive market

- 20.3.6 REST OF EUROPE

- 20.3.1 GERMANY

- 20.4 NORTH AMERICA

- 20.4.1 US

- 20.4.1.1 Strong infrastructure pipeline and commercial expansion to drive demand

- 20.4.2 CANADA

- 20.4.2.1 Increasing investments in residential and non-residential construction to drive market

- 20.4.3 MEXICO

- 20.4.3.1 Increased private and public sector investments in construction activities to drive market

- 20.4.1 US

- 20.5 MIDDLE EAST

- 20.5.1 GULF COOPERATION COUNCIL (GCC)

- 20.5.1.1 Qatar

- 20.5.1.1.1 Development and maintenance activities for commercial events to drive market

- 20.5.1.1 Qatar

- 20.5.2 SAUDI ARABIA

- 20.5.2.1 Continued execution of state-backed infrastructure programs to drive market

- 20.5.3 UAE

- 20.5.3.1 Government-backed infrastructure spending to drive market

- 20.5.4 REST OF MIDDLE EAST

- 20.5.1 GULF COOPERATION COUNCIL (GCC)

- 20.6 REST OF THE WORLD

- 20.6.1 RUSSIA

- 20.6.1.1 Strategic infrastructure investments driving heavy construction equipment demand

- 20.6.2 SOUTH AFRICA

- 20.6.2.1 Infrastructure development driving heavy construction equipment demand

- 20.6.3 BRAZIL

- 20.6.3.1 Rising Infrastructure Investments Supporting heavy construction equipment Demand

- 20.6.4 OTHERS

- 20.6.5 INDUSTRY INSIGHTS

- 20.6.1 RUSSIA

21 COMPETITIVE LANDSCAPE

- 21.1 OVERVIEW

- 21.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, JANUARY 2022-MAY 2026

- 21.3 MARKET SHARE ANALYSIS, 2025

- 21.4 REVENUE ANALYSIS OF TOP 5 PLAYERS, 2021-2025

- 21.5 COMPANY EVALUATION MATRIX: HEAVY CONSTRUCTION EQUIPMENT MANUFACTURERS, 2025

- 21.5.1 STARS

- 21.5.2 EMERGING LEADERS

- 21.5.3 PERVASIVE PLAYERS

- 21.5.4 PARTICIPANTS

- 21.5.5 COMPANY FOOTPRINT: HEAVY CONSTRUCTION EQUIPMENT MANUFACTURERS, 2025

- 21.5.6 REGION FOOTPRINT, 2025

- 21.5.7 APPLICATION FOOTPRINT, 2025

- 21.5.8 PROPULSION FOOTPRINT, 2025

- 21.6 MAJOR COMPACT CONSTRUCTION EQUIPMENT MANUFACTURERS, BY EQUIPMENT TYPE

- 21.7 COMPANY EVALUATION MATRIX: COMPACT CONSTRUCTION EQUIPMENT MARKET, 2025

- 21.7.1 STARS

- 21.7.2 EMERGING LEADERS

- 21.7.3 PERVASIVE PLAYERS

- 21.7.4 PARTICIPANTS

- 21.7.5 COMPANY FOOTPRINT: COMPACT CONSTRUCTION EQUIPMENT MANUFACTURERS, 2025

- 21.8 COMPACT CONSTRUCTION EQUIPMENT MARKET: REGION FOOTPRINT, 2025

- 21.9 COMPACT HEAVY CONSTRUCTION EQUIPMENT MARKET: PRODUCT FOOTPRINT, 2025

- 21.10 COMPACT CONSTRUCTION EQUIPMENT MARKET: PROPULSION FOOTPRINT, 2025

- 21.11 COMPANY VALUATION

- 21.12 BRAND/PRODUCT COMPARISON

- 21.13 COMPETITIVE SCENARIO

- 21.13.1 PRODUCT LAUNCHES/DEVELOPMENTS/ENHANCEMENTS, JANUARY 2022-MAY 2026

- 21.13.2 DEALS, JANUARY 2022-MAY 2026

- 21.13.3 EXPANSIONS, JANUARY 2022-MAY 2026

- 21.13.4 OTHERS, JANUARY 2022-MAY 2026

22 COMPANY PROFILES

- 22.1 KEY PLAYERS

- 22.1.1 CATERPILLAR INC.

- 22.1.1.1 Business overview

- 22.1.1.2 Products offered

- 22.1.1.3 Recent developments

- 22.1.1.3.1 Product launches/enhancements

- 22.1.1.3.2 Deals

- 22.1.1.3.3 Expansions

- 22.1.1.3.4 Others

- 22.1.1.4 MnM view

- 22.1.1.4.1 Key strengths

- 22.1.1.4.2 Strategic choices

- 22.1.1.4.3 Weaknesses and competitive threats

- 22.1.2 KOMATSU

- 22.1.2.1 Business overview

- 22.1.2.2 Products offered

- 22.1.2.3 Recent developments

- 22.1.2.3.1 Product developments/enhancements/upgrades

- 22.1.2.3.2 Deals

- 22.1.2.3.3 Expansions

- 22.1.2.3.4 Others

- 22.1.2.4 MnM view

- 22.1.2.4.1 Key strengths

- 22.1.2.4.2 Strategic choices

- 22.1.2.4.3 Weaknesses and competitive threats

- 22.1.3 DEERE & COMPANY

- 22.1.3.1 Business overview

- 22.1.3.2 Products offered

- 22.1.3.3 Recent developments

- 22.1.3.3.1 Product launches/developments/enhancements

- 22.1.3.3.2 Deals

- 22.1.3.3.3 Expansions

- 22.1.3.3.4 Others

- 22.1.3.4 MnM view

- 22.1.3.4.1 Key strengths

- 22.1.3.4.2 Strategic choices

- 22.1.3.4.3 Weaknesses and competitive threats

- 22.1.4 HITACHI CONSTRUCTION MACHINERY CO., LTD.

- 22.1.4.1 Business overview

- 22.1.4.2 Products offered

- 22.1.4.3 Recent developments

- 22.1.4.3.1 Product launches/enhancements

- 22.1.4.3.2 Deals

- 22.1.4.3.3 Expansions

- 22.1.4.3.4 Others

- 22.1.4.4 MnM view

- 22.1.4.4.1 Key strengths

- 22.1.4.4.2 Strategic choices

- 22.1.4.4.3 Weaknesses and competitive threats

- 22.1.5 VOLVO CE

- 22.1.5.1 Business overview

- 22.1.5.2 Products offered

- 22.1.5.3 Recent developments

- 22.1.5.3.1 Product launches/enhancements/developments

- 22.1.5.3.2 Deals

- 22.1.5.3.3 Expansions

- 22.1.5.3.4 Others

- 22.1.5.4 MnM view

- 22.1.5.4.1 Key strengths

- 22.1.5.4.2 Strategic choices

- 22.1.5.4.3 Weaknesses and competitive threats

- 22.1.6 CNH INDUSTRIAL N.V.

- 22.1.6.1 Business overview

- 22.1.6.2 Products offered

- 22.1.6.3 Recent developments

- 22.1.6.3.1 Product launches/enhancements

- 22.1.6.3.2 Deals

- 22.1.6.3.3 Expansions

- 22.1.6.3.4 Others

- 22.1.7 LIEBHERR

- 22.1.7.1 Business overview

- 22.1.7.2 Products offered

- 22.1.7.3 Recent developments

- 22.1.7.3.1 Product launches/developments/enhancements/upgrades

- 22.1.7.3.2 Deals

- 22.1.7.3.3 Expansions

- 22.1.7.3.4 Others

- 22.1.8 SANY GROUP

- 22.1.8.1 Business overview

- 22.1.8.2 Products offered

- 22.1.8.3 Recent developments

- 22.1.8.3.1 Product launches/developments/enhancements

- 22.1.8.3.2 Deals

- 22.1.8.3.3 Expansions

- 22.1.8.3.4 Others

- 22.1.9 J C BAMFORD EXCAVATORS LTD.

- 22.1.9.1 Business overview

- 22.1.9.2 Products offered

- 22.1.9.3 Recent developments

- 22.1.9.3.1 Product launches/developments

- 22.1.9.3.2 Deals

- 22.1.9.3.3 Expansions

- 22.1.9.3.4 Others

- 22.1.10 XCMG GROUP

- 22.1.10.1 Business overview

- 22.1.10.2 Products offered

- 22.1.10.3 Recent developments

- 22.1.10.3.1 Product launches

- 22.1.10.3.2 Deals

- 22.1.10.3.3 Expansions

- 22.1.10.3.4 Others

- 22.1.11 TEREX CORPORATION

- 22.1.11.1 Business overview

- 22.1.11.2 Products offered

- 22.1.11.3 Recent developments

- 22.1.11.3.1 Product launches/enhancements/developments

- 22.1.11.3.2 Deals

- 22.1.11.3.3 Others

- 22.1.12 ZOOMLION HEAVY INDUSTRY SCIENCE & TECHNOLOGY CO., LTD.

- 22.1.12.1 Business overview

- 22.1.12.2 Products offered

- 22.1.12.3 Recent developments

- 22.1.12.3.1 Product launches

- 22.1.12.3.2 Expansions

- 22.1.12.3.3 Others

- 22.1.13 HD HYUNDAI CONSTRUCTION EQUIPMENT CO., LTD.

- 22.1.13.1 Business overview

- 22.1.13.2 Products offered

- 22.1.13.3 Recent developments

- 22.1.13.3.1 Product launches/developments/enhancements

- 22.1.13.3.2 Deals

- 22.1.13.3.3 Expansions

- 22.1.13.3.4 Others

- 22.1.14 KUBOTA CORPORATION

- 22.1.14.1 Business overview

- 22.1.14.2 Products offered

- 22.1.14.3 Recent developments

- 22.1.14.3.1 Product launches/developments/enhancements

- 22.1.14.3.2 Expansions

- 22.1.14.3.3 Others

- 22.1.15 YANMAR HOLDINGS CO., LTD.

- 22.1.15.1 Business overview

- 22.1.15.2 Products offered

- 22.1.15.3 Recent developments

- 22.1.15.3.1 Product launches/developments/enhancements

- 22.1.15.3.2 Deals

- 22.1.15.3.3 Expansions

- 22.1.15.3.4 Others

- 22.1.1 CATERPILLAR INC.

- 22.2 OTHER PLAYERS

- 22.2.1 SANDVIK

- 22.2.2 THE MANITOWOC COMPANY, INC.

- 22.2.3 ASTEC INDUSTRIES, INC.

- 22.2.4 WACKER NEUSON SE

- 22.2.5 ESCORTS KUBOTA LIMITED.

- 22.2.6 AMMANN GROUP

- 22.2.7 LIUGONG MACHINERY CO., LTD.

- 22.2.8 MANITOU GROUP

- 22.2.9 SHANTUI CONSTRUCTION MACHINERY CO., LTD.

- 22.2.10 DINGSHENG TIANGONG CONSTRUCTION MACHINERY CO., LTD.

23 RESEARCH METHODOLOGY

- 23.1 RESEARCH DATA

- 23.1.1 SECONDARY DATA

- 23.1.1.1 Secondary sources

- 23.1.1.2 Key data from secondary sources

- 23.1.2 PRIMARY DATA

- 23.1.2.1 Primary participants

- 23.1.3 SAMPLING TECHNIQUES AND DATA COLLECTION METHODS

- 23.1.1 SECONDARY DATA

- 23.2 MARKET SIZE ESTIMATION

- 23.2.1 BOTTOM-UP APPROACH

- 23.2.2 TOP-DOWN APPROACH

- 23.3 DATA TRIANGULATION

- 23.4 FACTOR ANALYSIS

- 23.5 RESEARCH ASSUMPTIONS AND RISK ASSESSMENT

- 23.6 RESEARCH LIMITATIONS

24 APPENDIX

- 24.1 INSIGHTS FROM INDUSTRY EXPERTS

- 24.2 DISCUSSION GUIDE

- 24.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 24.4 CUSTOMIZATION OPTIONS

- 24.4.1 HEAVY CONSTRUCTION EQUIPMENT MARKET, BY END-USE INDUSTRY

- 24.4.2 HEAVY ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY BATTERY CAPACITY

- 24.4.3 HEAVY ELECTRIC HEAVY CONSTRUCTION EQUIPMENT MARKET, BY COUNTRY

- 24.5 RELATED REPORTS

- 24.6 AUTHOR DETAILS