|

시장보고서

상품코드

2060326

폴리비닐 알코올 필름 시장 예측(-2031년) : 용도별, 소재 등급별, 제품 유형별, 지역별Polyvinyl Alcohol Films Market by Material Grade (Fully Hydrolyzed, Partially Hydrolyzed), By Product Type (Water Soluble, Biodegradable, Specialty Functional), By Application (Household Detergents, Agrochemicals) and Region - Global Forecast to 2031 |

||||||

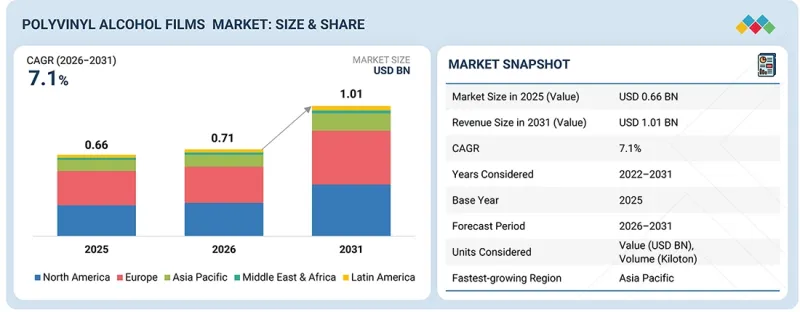

세계의 폴리비닐 알코올 필름 시장 규모는 2026년 7억 1,000만 달러에서 2031년까지 10억 1,000만 달러로 성장하며, 예측 기간 중 CAGR 7.1%를 기록할 것으로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(100만 달러), 킬로톤 |

| 부문 | 용도별, 소재 등급별, 제품 유형별, 지역별 |

| 대상 지역 | 아시아태평양, 북미, 유럽, 중동 및 아프리카, 남미 |

폴리비닐알코올(PVA) 필름 시장은 가정용 세제, 농약, 의약품, 식품 포장 및 특수 산업 용도를 포함한 일상적으로 사용되는 친환경적이고 수용성이며 지속가능한 포장 제품에 대한 수요 증가에 힘입어 성장하고 있습니다. 1회용 세탁용 포드나 수용성 농약 포장의 보급으로 인해 사용 편의성, 투여 정확도, 그리고 화학 물질 취급 시의 안전성이 크게 향상되고 있습니다. 또한 정부의 규제로 인해 기존 플라스틱 제품의 사용이 제한됨에 따라 생분해성 및 퇴비화 가능한 폴리비닐알코올 필름의 사용이 더욱 확대되고 있습니다. 또한 전자기기 및 의료용 특수 필름의 개발이 진행되고 있으며, 고부가가치 비즈니스 기회가 새롭게 확대되고 있습니다. 폴리비닐알코올 필름 시장의 성장이 직면한 과제로는 폴리비닐알코올 수지의 가격 변동, 폴리비닐알코올 필름의 높은 가공 및 제조 비용, 폴리비닐알코올 필름의 습기에 대한 민감성, 그리고 많은 지역에서 미흡한 퇴비화 인프라 등을 들 수 있습니다. 마지막으로 대체 가능한 생분해성 소재와의 경쟁과 제품이 환경에서 어떻게 분해되는지에 대한 규제 당국의 감시는 세계 시장의 제조업체들에게 중대한 우려 사항이 되고 있습니다.

“원료 등급별로 보면 예측 기간 중 부분 가수분해 필름 부문이 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. ” '

폴리비닐알코올 필름 시장에서 가장 큰 비중을 차지하는 소재 등급 부문은 부분 가수분해 필름입니다. 이 필름은 뛰어난 수용성, 낮은 가공 비용, 그리고 대량 생산되는 소비재 용도에 대한 폭넓은 적합성을 갖추고 있습니다. 부분 가수분해 필름은 완전 가수분해 필름보다 빠르게 용해되므로 1회용 세제 포드, 농약 포장재 및 기타 소비자용 수용성 제품에서 선호되는 선택지가 되고 있습니다. 이러한 뛰어난 성막성, 유연성 및 가공 용이성은 상용 제품의 대규모 생산을 지원하고 있습니다. 또한 부분 가수분해 필름은 성능과 비용 효율성 사이에서 최적의 균형을 제공하며, 가격 경쟁이 치열하고 빠른 용해가 제조사와 소비자의 구매 결정에 중요한 요소가 되는 대량 시장에서 큰 판매 포인트가 되고 있습니다.

제품 등급별로는 예측 기간 중 수용성 필름 부문이 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.

폴리비닐알코올 필름 시장에서 가장 큰 제품 유형 부문은 수용성 필름입니다. 이러한 필름은 가정용 세제 포드, 농약 포장, 세탁용 봉투 및 산업용 화학물질의 정량 공급 용도로 널리 사용되고 있습니다. 수용성 필름은 제어된 용해(즉, 물 속에서 용해되는 능력), 정확한 제품 공급(화학 물질을 직접 취급할 필요성을 줄이기 위함), 그리고 소비자의 편의성 향상을 제공합니다. 이 모든 것은 대량 포장 용도에서 수용성 필름을 탁월한 선택지로 만드는 특성입니다. 북미, 유럽, 아시아·태평양 지역에서 1회용 세제를 도입하는 기업이 늘어남에 따라 수용성 폴리비닐알코올 필름의 수요가 확대되고 있습니다. 또한 기업은 기존의 플라스틱 폐기물을 줄이고 지속가능성 노력을 강화하기 위해 수용성 포장 솔루션으로의 전환을 추진하고 있습니다. 수용성 필름은 자동 포장 시스템과의 높은 호환성을 갖추고 있으며, 뛰어난 강도와 다양한 용도에 대한 적응성을 겸비하고 있으며, 세계 시장에서 그 주도적인 위상은 앞으로도 유지될 것입니다.

“아시아·태평양 지역은 예측 기간 중 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.

아시아태평양은 세제, 전자기기, 섬유, 농약 등의 제조 산업이 집중되어 있으며, 폴리비닐알코올 필름의 최대 시장으로 자리 잡고 있습니다. 폴리비닐알코올 수지 및 필름의 주요 생산·가공 거점은 아시아태평양에 위치해 있으며, 중국, 일본, 인도, 한국 등이 포함됩니다. 이 모든 국가들이 폴리비닐알코올을 대량으로 생산하고 있으며, 이 지역은 폴리비닐알코올 수지 및 필름의 세계 주요 생산지가 되었습니다. 해당 지역에서 수용성 필름 소비 증가를 지원하는 요인으로는 급속한 도시화, 소비재에 대한 수요 증가, 그리고 1회용 세제 포장재의 사용 확대 등을 들 수 있습니다. 또한 아시아태평양에서는 낮은 제조 비용, 풍부한 원자재 공급, 그리고 제품을 수출하는 포장재 제조업체의 성장 덕분에 생산된 대량의 폴리비닐알코올을 고객에게 공급할 수 있습니다. 또한 지속가능한 포장 기술에 대한 투자 확대와 생분해성 소재 개발이 진행되고 있는 만큼, 폴리비닐알코올 필름 세계 시장에서 아시아태평양의 우위는 계속해서 공고해지고 있습니다.

폴리비닐알코올 필름 시장에는 KURARAY(일본), AICELLO CORPORATION(일본), MITSUBISHI CHEMICAL GROUP CORPORATION(일본), 세키스이 케미컬(일본), 애로우 그린테크(인도), 창춘 그룹(대만), 아쿠아팩 폴리머스(영국), 조이포스(중국), 에코폴(이탈리아), 암트렉스 네이처 케어(인도) 등의 주요 기업으로 구성되어 있습니다. 본 조사에서는 폴리비닐알코올 필름 시장의 주요 기업에 대해 기업 개요, 최근 동향 및 주요 시장 전략을 포함한 상세한 경쟁 분석을 수행하고 있습니다.

조사 범위

이 보고서에서는 폴리비닐알코올 필름 시장을 소재 등급, 용도, 제품 유형, 지역별로 세분화하여 각 지역의 전체 시장 규모를 추산하고 있습니다. 주요 업계 업체에 대한 상세한 분석을 통해, 폴리비닐알코올 필름 시장과 관련된 사업 개요, 제품 및 서비스, 주요 전략, 그리고 사업 확장에 대한 인사이트를 제공합니다.

이 보고서를 구매할 때의 주요 이점

본 조사 보고서는 업계 분석(업계 동향), 주요 기업의 시장 순위 분석, 그리고 기업 개요 등 여러 분석 수준에 초점을 맞추고 있으며, 이를 종합함으로써 경쟁 구도의 전체적인 모습, 폴리비닐알코올 필름 시장의 새로운 성장 분야 및 고성장 부문, 고성장 지역, 그리고 시장 촉진요인, 억제요인, 기회, 과제를 명확히 밝힙니다.

이 보고서에서는 다음 사항에 대한 인사이트를 제공합니다. :

- 촉진요인 분석:(지속가능하고 폐기물이 적은 포장재를 장려하는 규제 압력의 증가) , 제약 요인(높은 생산 비용 및 변동성이 큰 비닐아세테이트 단량체 가격에 대한 의존), 기회(아시아 및 라틴아메리카의 신흥 소비자 시장의 성장 기회), 그리고 과제(다양한 기후 조건 하에서 습기에 대한 민감성과 성능 안정성 관리)가 폴리비닐알코올 필름 시장의 성장에 미치는 영향

- 시장 침투: 전 세계 폴리비닐알코올 필름 시장의 주요 기업이 제공하는 제품에 대한 포괄적인 정보

- 제품 개발 및 혁신: 폴리비닐알코올 필름 시장의 향후 기술 동향, 신제품 출시, 사업 확장 및 M&A에 대한 상세한 분석

- 시장 개발: 수익성이 높은 신흥 시장에 대한 포괄적인 정보. 이 보고서에서는 지역별 폴리비닐알코올 필름 시장을 분석하고 있습니다.

- 시장 규모: 입수 가능한 범위 내에서 각 기업의 생산 능력을 제시하고, 폴리비닐알코올 필름 시장의 향후 생산 능력에 대해서도 기술하고 있습니다.

- 경쟁 분석: 폴리비닐알코올 필름 시장 주요 기업의 시장 점유율, 전략, 제품 및 생산 능력에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황과 지속가능성 구상

제8장 고객 상황과 구매 행동

제9장 폴리비닐 알코올 필름 시장(용도별)

제10장 폴리비닐 알코올 필름 시장(소재 등급별)

제11장 폴리비닐 알코올 필름 시장(제품 유형별)

제12장 폴리비닐 알코올 필름 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

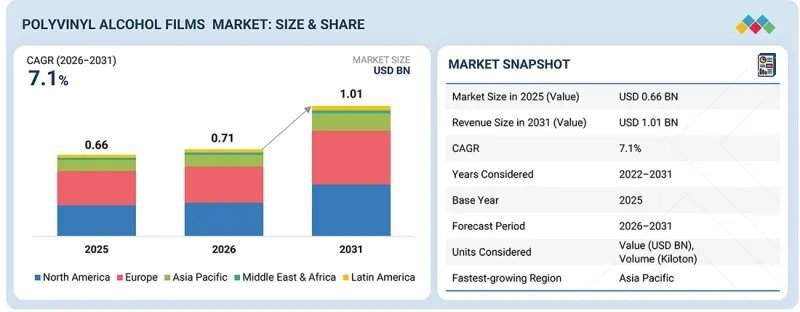

KSA 26.06.24The global polyvinyl alcohol films market is projected to grow from USD 0.71 billion in 2026 to USD 1.01 billion by 2031, registering a CAGR of 7.1% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million), Volume (Kilotons) |

| Segments | Material Grade, Application, Product Type, and Region |

| Regions covered | Asia Pacific, North America, Europe, Middle East & Africa, South America |

The polyvinyl alcohol film market is growing, driven by the increasing need for environmentally friendly, water-soluble, and sustainable packaging products for everyday use, including household cleaning items, agrochemical products, pharmaceuticals, food packaging, and specialty industrial applications. The acceptance of unit-dose laundry cleaning pods and water-soluble agrochemical packages is significantly improving ease of use, dosing accuracy, and the safety of chemical handling. Government regulations have also recently limited the use of traditional plastic products, further increasing the use of biodegradable and compostable polyvinyl alcohol films. The recent development of specialty films for electronic and medical applications also offers a new and growing source of high-value opportunities. Challenges facing the growth of the polyvinyl alcohol film market include fluctuations in the price of polyvinyl alcohol resin, high processing and production costs of polyvinyl alcohol films, moisture sensitivity of polyvinyl alcohol films, and insufficient composting infrastructure in many geographical areas. Lastly, competition from alternative biodegradable materials and regulatory scrutiny regarding how the products degrade in the environment are significant concerns for manufacturers in the global market.

"By material grade, partially hydrolyzed films segment is anticipated to account for the largest market share during the forecast period."

The polyvinyl alcohol films market's largest materials-grade segment comprises partially hydrolyzed films, which offer superior water solubility, lower processing costs, and broad suitability for high-volume consumer packaged goods applications. Partially hydrolyzed films dissolve more rapidly than fully hydrolyzed films, making them the preferred choice for unit-dose detergent pods, agrochemical packages, and other consumer water-soluble products. Their strong film-forming properties, flexibility, and ease of processing support large-scale manufacturing of commercial products. Moreover, partially hydrolyzed films offer an optimal balance between performance and cost efficiency, a major selling point in mass markets where pricing is competitive and rapid dissolution is a key factor in purchase decisions by manufacturers and consumers.

By product grade, the water-soluble films segment is anticipated to account for the largest market share during the forecast period.

The largest product type segment in the polyvinyl alcohol films market is water-soluble films. These films are used extensively for household detergent pods, agrochemical packaging, laundry bags, and industrial chemical dosing applications. Water-soluble films provide controlled dissolution (i.e., the ability to dissolve in water), precise product delivery (to reduce the need to handle chemicals directly), and greater convenience for consumers, all attributes that make them an excellent choice for high-volume packaging applications. As more companies adopt unit-dose detergents across North America, Europe, and Asia Pacific, demand for water-soluble polyvinyl alcohol films has grown. In addition, companies are moving toward soluble packaging solutions to reduce conventional plastic waste and improve their sustainability efforts. The strong compatibility of water-soluble films with automated packaging systems, along with their excellent strength and versatility across a variety of applications, will continue to support their leading position in the global market.

"Asia Pacific is anticipated to account for the largest market share during the forecast period.

The Asia Pacific region has the largest market for polyvinyl alcohol films due to the high concentration of industries manufacturing detergents, electronics, textiles, and agrochemicals. Major producers of polyvinyl alcohol resin and film conversion are located in Asia Pacific, including China, Japan, India, and South Korea, all of which manufacture polyvinyl alcohol in large volumes, making the region a key global manufacturer of polyvinyl alcohol resins and films. Factors supporting increased consumption of water-soluble films in the region include rapid urbanization, rising demand for consumer goods, and growing use of unit-dose detergent packaging. Additionally, large volumes of polyvinyl alcohol manufactured in Asia Pacific can be supplied to customers due to lower manufacturing costs, an abundant supply of raw materials, and the growth of packaged goods manufacturers that export their products. Furthermore, increasing investment in sustainable packaging technologies and the development of biodegradable materials continue to solidify the dominant position of the Asia Pacific region in the global market for polyvinyl alcohol films.

In-depth interviews were conducted with chief executive officers (CEOs), marketing directors, other innovation and technology directors, and executives from key organizations operating in the polyvinyl alcohol films market. Information was also gathered from secondary research to determine and verify the market size of several segments. Q4R56TY78

- By Company Type: Tier 1 - 50%, Tier 2 - 30%, and Tier 3 - 20%

- By Designation: Managers - 15%, Directors - 20%, and Others - 65%

- By Region: North America - 30%, Europe - 25%, Asia Pacific - 25%, Middle East & Africa - 15%, South America- 5%

The polyvinyl alcohol films market comprises major companies, such as KURARAY CO., LTD. (Japan), AICELLO CORPORATION (Japan), MITSUBISHI CHEMICAL GROUP CORPORATION (Japan), SEKISUI CHEMICAL CO., LTD. (Japan), Arrow GreenTech Ltd. (India), Chang Chun Group (Taiwan), Aquapak Polymers Limited (UK), Joyforce (China), ECOPOL S.p.A. (Italy), Amtrex Nature Care Pvt. Ltd. (India). The study includes in-depth competitive analysis of these key players in the polyvinyl alcohol films market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This report segments the polyvinyl alcohol films market by material grade, application, product type, and region, and provides estimates of the market's overall value across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products and services, key strategies, and expansions associated with the polyvinyl alcohol films market.

Key benefits of buying this report

This research report focuses on multiple levels of analysis-industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape; emerging and high-growth segments of the polyvinyl alcohol films market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights into the following points:

- Analysis of Drivers: (Increasing Regulatory Pressure Supporting Sustainable and Low-Waste Packaging Materials), restraints (High Production Costs and Dependence on Volatile Vinyl Acetate Monomer Pricing), opportunities (Expansion Opportunities in Emerging Asian and Latin American Consumer Markets), and challenges (Managing Moisture Sensitivity and Performance Stability Across Diverse Climatic Conditions) influencing the growth of polyvinyl alcohol films market

- Market Penetration: Comprehensive information on the polyvinyl alcohol films offered by top players in the global polyvinyl alcohol films market

- Product Development/Innovation: Detailed insights on upcoming technologies, product launches, expansions, and acquisitions in the polyvinyl alcohol films market

- Market Development: Comprehensive information about lucrative emerging markets, the report analyzes the markets for polyvinyl alcohol films across regions.

- Market Capacity: Production capacity of the companies is provided wherever available, with upcoming capacities for the polyvinyl alcohol films market

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the polyvinyl alcohol films market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN POLYVINYL ALCOHOL FILMS MARKET

- 3.2 POLYVINYL ALCOHOL FILMS MARKET, BY MATERIAL GRADE AND REGION

- 3.3 POLYVINYL ALCOHOL FILMS MARKET, BY PRODUCT TYPE

- 3.4 POLYVINYL ALCOHOL FILMS MARKET, BY APPLICATION

- 3.5 POLYVINYL ALCOHOL FILMS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising adoption of water-soluble packaging solutions across detergent and institutional cleaning industry

- 4.2.1.2 Increasing regulatory pressure supporting sustainable and low-waste packaging materials

- 4.2.1.3 Expanding utilization in agrochemical, medical, and healthcare packaging applications

- 4.2.1.4 Technological advancements in high-performance and specialty PVA film formulations

- 4.2.2 RESTRAINTS

- 4.2.2.1 High production costs and dependence on volatile vinyl acetate monomer pricing

- 4.2.2.2 Environmental scrutiny regarding biodegradability and wastewater decomposition performance

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing development of high-barrier, specialty, and pharmaceutical-grade PVA films

- 4.2.3.2 Increasing strategic investments, capacity expansion, and vertical integration across the value chain

- 4.2.3.3 Expansion opportunities in emerging Asian and Latin American consumer markets

- 4.2.4 CHALLENGES

- 4.2.4.1 Managing moisture sensitivity and performance stability across diverse climatic conditions

- 4.2.4.2 Intensifying competitive pressure and technological differentiation requirements

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN POLYVINYL ALCOHOL FILMS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL PACKAGING INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE, BY REGION (2022-2025)

- 5.4.2 AVERAGE SELLING PRICE, BY MATERIAL GRADE (2022-2025)

- 5.4.3 AVERAGE SELLING PRICE, BY APPLICATION (2022-2025)

- 5.4.4 AVERAGE SELLING PRICE, BY PRODUCT TYPE (2022-2025)

- 5.4.5 AVERAGE SELLING PRICE AMONG KEY PLAYERS, BY MATERIAL GRADE, 2025

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 390520)

- 5.6.2 EXPORT SCENARIO (HS CODE 390520)

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 KURARAY CO., LTD. & DETERGENT MANUFACTURERS COLLABORATION FOR WATER-SOLUBLE UNIT-DOSE PACKAGING

- 5.10.2 MONOSOL & HEALTHCARE INSTITUTIONS FOR INFECTION-CONTROL LAUNDRY BAGS

- 5.10.3 AICELLO CORPORATION & AGROCHEMICAL PRODUCERS FOR WATER-SOLUBLE PESTICIDE PACKAGING

- 5.11 IMPACT OF 2025 US TARIFF ON POLYVINYL ALCOHOL FILMS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END USERS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 POLYVINYL ALCOHOL RESIN HYDROLYSIS AND POLYMERIZATION TECHNOLOGY

- 6.1.2 FILM EXTRUSION AND CASTING TECHNOLOGY

- 6.1.3 WATER-SOLUBLE FILM FORMULATION TECHNOLOGY

- 6.1.4 HUMIDITY-CONTROLLED PROCESSING TECHNOLOGY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 AUTOMATED UNIT-DOSE PACKAGING SYSTEMS

- 6.2.2 BIODEGRADABILITY TESTING AND CERTIFICATION TECHNOLOGY

- 6.2.3 COATING AND SURFACE TREATMENT TECHNOLOGY

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 BIODEGRADABLE BIOPOLYMER FILMS

- 6.3.2 SMART SOLUBLE DELIVERY FILMS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 TRANSITION FROM CONVENTIONAL SOLUBLE FILMS TO HIGH-PERFORMANCE MULTI-FUNCTIONAL FILMS

- 6.4.2 EXPANSION TOWARD COLD-WATER AND CONTROLLED-DISSOLUTION PRODUCT PLATFORMS

- 6.4.3 DEVELOPMENT OF SUSTAINABLE AND REGULATORY-COMPLIANT FILM PLATFORMS

- 6.4.4 INTEGRATION INTO ADVANCED SPECIALTY APPLICATIONS

- 6.5 PATENT ANALYSIS

- 6.5.1 METHODOLOGY

- 6.5.2 GRANTED PATENTS, 2016-2025

- 6.5.2.1 Publication trends for last ten years

- 6.5.3 INSIGHTS

- 6.5.4 LEGAL STATUS

- 6.5.5 JURISDICTION ANALYSIS

- 6.5.6 TOP APPLICANTS

- 6.5.7 LIST OF MAJOR PATENTS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 SMART DISSOLVABLE PHARMACEUTICAL DELIVERY FILMS

- 6.6.2 WATER-SOLUBLE AGRICULTURAL INPUT DELIVERY FILMS

- 6.6.3 SUPPORT FILMS FOR 3D PRINTING AND ADVANCED MANUFACTURING

- 6.6.4 OPTICAL AND FLEXIBLE ELECTRONICS FILMS

- 6.7 IMPACT OF AI/GEN AI ON POLYVINYL ALCOHOL FILMS MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN POLYVINYL ALCOHOL FILMS PROCESSING

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN POLYVINYL ALCOHOL FILMS MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN POLYVINYL ALCOHOL FILMS MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 KURARAY CO., LTD.: DIGITAL INNOVATION IN WATER-SOLUBLE DETERGENT PACKAGING

- 6.8.2 MONOSOL: SUSTAINABLE HEALTHCARE AND SPECIALTY PACKAGING EXPANSION

- 6.8.3 AICELLO CORPORATION: SPECIALTY FILM CUSTOMIZATION FOR AGROCHEMICAL AND ELECTRONICS APPLICATIONS

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 DEVELOPMENT OF BIODEGRADABILITY-VALIDATED FILM GRADES

- 7.2.2 LOW-CARBON MANUFACTURING AND ENERGY EFFICIENCY

- 7.2.3 REPLACEMENT OF CONVENTIONAL SINGLE-USE PLASTIC PACKAGING

- 7.2.4 CIRCULAR ECONOMY AND WASTEWATER COMPATIBILITY RESEARCH

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, & ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 PREMIUM SPECIALTY APPLICATIONS DRIVE HIGHER MARGINS

- 8.5.2 DETERGENT PACKAGING IS HIGH VOLUME BUT PRICE COMPETITIVE

- 8.5.3 RAW MATERIAL VOLATILITY DIRECTLY AFFECTS PROFITABILITY

- 8.5.4 REGIONAL MANUFACTURING AND COMPLIANCE COSTS SHAPE RETURNS

9 POLYVINYL ALCOHOL FILMS MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 HOUSEHOLD DETERGENTS

- 9.2.1 RAPID EXPANSION OF UNIT-DOSE CLEANING PRODUCT CONSUMPTION

- 9.3 AGROCHEMICALS

- 9.3.1 RISING NEED FOR SAFE HANDLING AND PRECISION DOSING SYSTEMS

- 9.4 FOOD PACKAGING

- 9.4.1 HIGH DEMAND FOR SUSTAINABLE SINGLE-USE AND PORTION-CONTROL PACKAGING

- 9.5 PHARMACEUTICALS & HEALTHCARE

- 9.5.1 RISING NEED FOR HYGIENIC DISSOLVABLE PACKAGING SOLUTIONS

- 9.6 TEXTILE

- 9.6.1 GROWING USE OF WATER-SOLUBLE SUPPORT FILMS IN ADVANCED GARMENT MANUFACTURING

- 9.7 ELECTRONICS

- 9.7.1 GROWING DEMAND FOR HIGH-PURITY OPTICAL AND FUNCTIONAL FILM MATERIALS

- 9.8 OTHER APPLICATIONS

10 POLYVINYL ALCOHOL FILMS MARKET, BY MATERIAL GRADE

- 10.1 INTRODUCTION

- 10.2 FULLY HYDROLYZED FILMS

- 10.2.1 HIGH-PERFORMANCE PACKAGING AND SPECIALTY INDUSTRIAL APPLICATIONS

- 10.3 PARTIALLY HYDROLYZED FILMS

- 10.3.1 WIDESPREAD USE IN CONSUMER AND HOUSEHOLD PACKAGING

11 POLYVINYL ALCOHOL FILMS MARKET, BY PRODUCT TYPE

- 11.1 INTRODUCTION

- 11.2 WATER-SOLUBLE FILMS

- 11.2.1 GROWING ADOPTION IN UNIT-DOSE PACKAGING AND SUSTAINABLE DISSOLVABLE APPLICATIONS

- 11.3 BIODEGRADABLE/COMPOSTABLE FILMS

- 11.3.1 REGULATORY PRESSURE TO REPLACE CONVENTIONAL PLASTIC PACKAGING

- 11.4 POLARIZER FILMS

- 11.4.1 INCREASING DEMAND FROM HIGH-PERFORMANCE DISPLAY AND ELECTRONICS APPLICATIONS

- 11.5 EMBROIDERY/TEXTILE SUPPORT FILMS

- 11.5.1 RISING TEXTILE AUTOMATION AND DECORATIVE APPAREL MANUFACTURING

- 11.6 SPECIALTY FUNCTIONAL FILMS

- 11.6.1 DIVERSIFICATION INTO HIGH-PERFORMANCE INDUSTRIAL AND MEDICAL APPLICATIONS

12 POLYVINYL ALCOHOL FILMS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 Strong detergent packaging and chemical manufacturing bases

- 12.2.2 JAPAN

- 12.2.2.1 High-value market growth through advanced specialty film technologies

- 12.2.3 INDIA

- 12.2.3.1 Rising water-soluble packaging applications across consumer and agricultural sectors

- 12.2.4 SOUTH KOREA

- 12.2.4.1 Electronics and premium consumer packaging applications

- 12.2.5 REST OF ASIA PACIFIC

- 12.2.1 CHINA

- 12.3 NORTH AMERICA

- 12.3.1 US

- 12.3.1.1 Strong unit-dose detergent adoption and advanced specialty packaging consumption

- 12.3.2 CANADA

- 12.3.2.1 Sustainable packaging adoption and industrial chemical applications

- 12.3.3 MEXICO

- 12.3.3.1 Manufacturing expansion and cross-border packaging supply chains

- 12.3.1 US

- 12.4 EUROPE

- 12.4.1 GERMANY

- 12.4.1.1 Advanced sustainable packaging and industrial manufacturing

- 12.4.2 ITALY

- 12.4.2.1 Demand driven by textile processing and flexible packaging conversion

- 12.4.3 FRANCE

- 12.4.3.1 Agrochemical packaging and sustainability-driven consumer packaging

- 12.4.4 UK

- 12.4.4.1 Consumer convenience packaging and healthcare applications

- 12.4.5 SPAIN

- 12.4.5.1 Agrochemical and consumer packaging expansion

- 12.4.6 REST OF EUROPE

- 12.4.1 GERMANY

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.5.1.1 Saudi Arabia

- 12.5.1.1.1 Industrial diversification and specialty packaging adoption

- 12.5.1.2 UAE

- 12.5.1.2.1 Healthcare and consumer packaging imports

- 12.5.1.3 Rest of GCC countries

- 12.5.1.1 Saudi Arabia

- 12.5.2 SOUTH AFRICA

- 12.5.2.1 Agrochemical and institutional packaging applications

- 12.5.3 REST OF MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.6 SOUTH AMERICA

- 12.6.1 ARGENTINA

- 12.6.1.1 Agricultural inputs and specialty packaging demand

- 12.6.2 BRAZIL

- 12.6.2.1 Strong agrochemical packaging and expanding consumer goods applications

- 12.6.3 REST OF SOUTH AMERICA

- 12.6.1 ARGENTINA

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.3 MARKET SHARE ANALYSIS, 2025

- 13.4 REVENUE ANALYSIS

- 13.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- 13.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2026

- 13.5.5.1 Company footprint

- 13.5.5.2 By region footprint

- 13.5.5.3 By material grade footprint

- 13.5.5.4 By product type footprint

- 13.5.5.5 By application footprint

- 13.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 RESPONSIVE COMPANIES

- 13.6.3 DYNAMIC COMPANIES

- 13.6.4 STARTING BLOCKS

- 13.6.5 COMPETITIVE BENCHMARKING

- 13.6.5.1 Detailed list of key startups/SMEs

- 13.6.5.2 Competitive benchmarking of key startups/SMEs

- 13.7 BRAND COMPARISON

- 13.8 COMPANY VALUATION AND FINANCIAL METRICS

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 DEALS

- 13.9.2 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 KURARAY CO., LTD.

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Expansions

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 AICELLO CORPORATION

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 MnM view

- 14.1.2.3.1 Right to win

- 14.1.2.3.2 Strategic choices

- 14.1.2.3.3 Weaknesses and competitive threats

- 14.1.3 MITSUBISHI CHEMICAL GROUP CORPORATION

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Expansions

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 SEKISUI CHEMICAL CO., LTD.

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 MnM view

- 14.1.4.3.1 Right to win

- 14.1.4.3.2 Strategic choices

- 14.1.4.3.3 Weaknesses and competitive threats

- 14.1.5 ARROW GREENTECH LTD.

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Deals

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 CHANG CHUN GROUP

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 MnM view

- 14.1.6.3.1 Right to Win

- 14.1.6.3.2 Strategic choices

- 14.1.6.3.3 Weaknesses and competitive threats

- 14.1.7 AQUAPAK POLYMERS LIMITED

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Deals

- 14.1.7.4 MnM view

- 14.1.7.4.1 Right to Win

- 14.1.7.4.2 Strategic choices

- 14.1.7.4.3 Weaknesses and competitive threats

- 14.1.8 JOYFORCE

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 MnM view

- 14.1.8.3.1 Right to Win

- 14.1.8.3.2 Strategic choices

- 14.1.8.3.3 Weaknesses and competitive threats

- 14.1.9 ECOPOL S.P.A

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 Recent Developments

- 14.1.9.3.1 Deals

- 14.1.9.3.2 Expansions

- 14.1.9.4 MnM view

- 14.1.9.4.1 Right to Win

- 14.1.9.4.2 Strategic choices

- 14.1.9.4.3 Weaknesses and competitive threats

- 14.1.10 AMTREX NATURE CARE PVT. LTD.

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 MnM View

- 14.1.10.3.1 Right to Win

- 14.1.10.3.2 Strategic Choices

- 14.1.10.3.3 Weaknesses and competitive threats

- 14.1.1 KURARAY CO., LTD.

- 14.2 OTHER PLAYERS

- 14.2.1 NOBLE INDUSTRIES

- 14.2.2 KK NONWOVENS

- 14.2.3 FOSHAN POLYVA MATERIALS CO., LTD

- 14.2.4 GUANGZHOU PIONEER TECH CO., LTD.

- 14.2.5 SIBOTE FILM

- 14.2.6 CHANGZHOU WATER SOLUBLE CO., LTD.

- 14.2.7 JIANGMEN CINCH PACKAGING MATERIALS CO., LTD.

- 14.2.8 GUANGDONG PROUDLY NEW MATERIAL TECHNOLOGY CORP.

- 14.2.9 FUJIAN ZHONGSU BIODEGRADABLE FILMS CO., LTD

- 14.2.10 SOLTEC DEVELOPMENT

- 14.2.11 YONG'AN SANYUANFENG WATER SOLUBLE FILM CO., LTD.

- 14.2.12 GREEN TECH BIO PRODUCTS

- 14.2.13 ZHAOQING FANGXING PACKING MATERIAL CO., LTD.

- 14.2.14 ACEDAG LIMITED

- 14.2.15 SENGONG NEW MATERIALS TECHNOLOGY CO., LTD.

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key primary interview participants

- 15.1.2.3 Breakdown of primary interviews

- 15.1.2.4 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.2 TOP-DOWN APPROACH

- 15.3 BASE NUMBER CALCULATION

- 15.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 15.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 15.4 MARKET FORECAST APPROACH

- 15.4.1 SUPPLY SIDE

- 15.4.2 DEMAND SIDE

- 15.5 DATA TRIANGULATION

- 15.6 FACTOR ANALYSIS

- 15.7 RESEARCH ASSUMPTIONS

- 15.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS