|

시장보고서

상품코드

2061163

이력관리 솔루션 시장 예측(-2031년) : 용도별, 컴포넌트별, 배포 모델별, 최종사용자별, 기술별, 지역별Track and Trace Solutions Market by Component (Software, Hardware), Application [Serialization (Carton, Bottle, Blister), Aggregation (Bundle, Case, Pallet)], Technology (Barcode, RFID, NFC), End User (Pharma, Food, Cosmetic) - Global Forecast to 2031 |

||||||

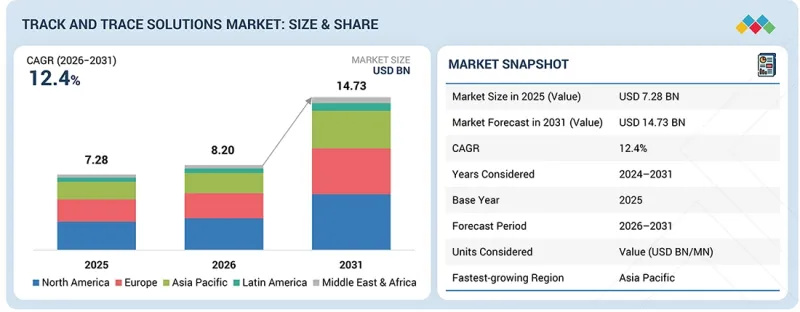

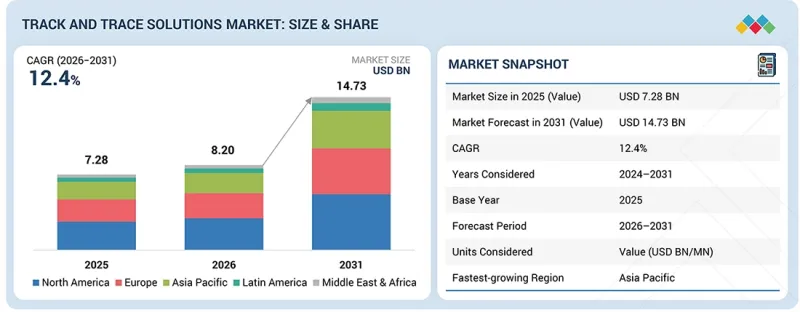

이력관리 솔루션 시장 규모는 2026년 82억 달러에서 2031년까지 147억 3,000만 달러로 성장하며, CAGR은 12.4%에 달할 것으로 예측됩니다.

이러한 성장은 주로 의약품, 식품, 의료기기, 화장품 분야의 제품 인증, 공급망 가시화, 그리고 규제 요건에 대한 수요 증가에 기인한 것입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 용도별, 컴포넌트별, 배포 모델별, 최종사용자별, 기술별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

생산 라인, 창고, 유통업체에서 최종사용자에 이르기까지 제품을 추적하기 위해 일련번호 부여, 집계, 바코드, RFID, NFC, 육안 검사 및 클라우드 기반 추적 기술에 대한 투자가 증가하고 있습니다. 또한 제조업체들 사이에서 단순한 규정 준수에 그치지 않고, 신속한 리콜 관리, 위조 방지 대책, 파트너와의 소통, 그리고 프로세스 관리를 위해 추적 및 트레이서빌리티 기술을 활용하는 추세가 높아짐에 따라 시장은 더욱 성장하고 있습니다.

“2025년에는 바코드 기반 추적성 부문이 가장 큰 시장 점유율을 차지했습니다. ” '

기술적 측면에서, 추적 및 트레이서빌리티 솔루션 시장은 바코드를 통한 트레이서빌리티, RFID를 통한 트레이서빌리티, 그리고 NFC를 통한 트레이서빌리티로 분류됩니다. 바코드를 활용한 추적성 부문은 의약품, 식품, 의료기기, 화장품, 물류 업계에서 광범위하게 활용됨에 따라 2025년에 시장을 장악했습니다. 바코드는 식별, 일련번호 부여, 집계, 보고를 지원하는 가장 효율적이고 경제적인 기술로 자리매김하고 있습니다. 특히 2D 바코드나 데이터 매트릭스 코드는 제품 코드, 일련번호, 로트 정보, 유효기간을 아주 작은 공간에 기록할 수 있으므로 의약품 포장에 널리 사용되고 있습니다. 포장 기계, 스캔 장치, 창고, 규제 플랫폼과의 손쉬운 통합 덕분에 바코드 기반 시스템은 다른 기술보다 더 널리 채택되고 있습니다. 또한 제품 인증을 위해 소비자들이 QR코드를 채택하는 사례가 증가하고 있는 점도 추적 및 트레이서빌리티 솔루션 시장에서 바코드의 중요성을 더욱 높이고 있습니다.

“예측 기간 중 소프트웨어 부문이 가장 높은 성장률을 기록할 것으로 예상됩니다. ” '

구성 요소별로 보면 추적 및 트레이서빌리티 솔루션 시장은 소프트웨어, 하드웨어, 서비스로 분류됩니다. 독립형 시리얼화 시스템에서 벗어나 통합형 기업 추적성 솔루션을 도입하는 추세가 강해지고 있으며, 이 중 소프트웨어가 가장 빠르게 성장하고 있는 부문입니다. 시리얼화 데이터 관리, 집계 구조, EPCIS 데이터 교환, 규제 당국에 대한 제출, 감사 로그, 창고 관리 점검 및 예외 관리 분야에서 소프트웨어의 중요성이 점점 더 커지고 있습니다. 기업은 여러 공장이나 CMO(위탁 제조업체)에 걸쳐 사업을 운영하고, 국가별 규정 준수 요건을 충족해야 하므로 확장성과 설정 유연성을 갖춘 소프트웨어 플랫폼에 대한 수요가 높아지고 있습니다. 또한 클라우드 기반 추적성 소프트웨어에 대한 수요도 증가하고 있습니다. 이는 도입을 신속하게 진행하고, 파트너와의 협력을 강화하며, 실시간 가시성을 높일 수 있을 뿐만 아니라, 동시에 사내 IT 인프라에 대한 의존도를 낮출 수 있기 때문입니다.

“아시아·태평양 지역은 예측 기간 중 가장 빠르게 성장할 지역 시장이 될 것으로 예상됩니다. '

아시아태평양의 급속한 성장은 제조 활동의 확대, 수출 증가, 그리고 아시아 주요 경제권에서 시리얼화 및 추적성 규제의 도입 확대에 힘입어 이루어지고 있습니다. 특히 중국, 인도, 일본, 한국, 호주에서는 의약품, 의료기기, 식품, 소비재 등 각 산업 분야에서 추적 시스템이 도입되어 있으며, 일련번호 부여 및 바코드 시스템, 집적기, 비전 검사, 클라우드 기반 추적성 솔루션에 대한 수요가 크게 증가하고 있습니다. 인도와 중국은 의약품 생산 규모, 수탁제조의 증가, 그리고 미국 및 유럽 등으로의 수출을 위해 글로벌 규제 기준을 충족해야 하는 높은 수요에 힘입어, 아시아태평양의 중요한 성장 시장으로 부상하고 있습니다. 한편, 일본, 한국, 호주는 우수한 의료 인프라, 식품 안전을 확보하기 위한 노력, 그리고 제조 및 물류 분야의 자동화를 통해 성장에 기여하고 있습니다. 또한 E-Commerce, 국경 간 무역, 제품 위조 문제 등도 이 지역의 수요를 더욱 부추기고 있습니다.

Antares Vision S.p.A(이탈리아), Axway(프랑스), OPTEL GROUP(캐나다) 및 TraceLink Inc.(미국)는 추적 및 트레이서빌리티 솔루션 시장의 주요 기업 중 일부입니다.

- 본 조사에서는 추적 및 트레이서빌리티 솔루션 시장의 주요 기업에 대해 기업 개요, 최근 동향 및 주요 시장 전략을 포함한 상세한 경쟁 분석을 수행하고 있습니다.

조사 범위

본 조사 보고서에서는 추적 및 트레이서빌리티 솔루션 시장을 구성 요소별, 배포 모델별, 기술별, 최종사용자별, 지역별로 분석하고 있습니다. 이 보고서의 범위는 추적 및 트레이서빌리티 솔루션 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 제약 요인, 과제, 기회 등)에 대한 상세한 정보를 포괄하고 있습니다. 주요 업계 참여자에 대한 상세한 분석을 통해, 해당 기업의 사업 개요, 솔루션, 서비스, 주요 전략, 계약, 파트너십, 합의, 제품 및 서비스 출시, 합병 및 인수, 그리고 추적 및 트레이서빌리티 솔루션 시장과 관련된 최근 동향에 대한 인사이트를 제공합니다.

이 보고서를 구매해야 하는 이유

이 보고서는 추적 및 트레이서빌리티 솔루션 시장과 그 하위 부문의 매출에 관한 가장 정확한 추정치를 제공함으로써, 이 시장의 선도 기업과 신규 진입 기업을 지원합니다. 이 보고서는 이해관계자들이 경쟁 구도를 이해하고, 자사의 비즈니스를 더 유리한 위치에 놓으며, 적절한 시장 진입 전략을 수립하는 데 필요한 추가적인 인사이트를 얻는 데 도움이 됩니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움을 주며, 주요 시장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

이 보고서에서는 다음 사항에 대한 인사이트를 제공합니다. :

- 주요 촉진요인(시리얼화에 관한 엄격한 규제 및 기준, 제조사별 브랜드 보호에 대한 집중도 강화, 포장 관련 제품의 리콜 증가, 제네릭 의약품 및 OTC 시장의 급성장, 의료기기 산업의 성장) , 제약 요인(시리얼화 및 애그리게이션 도입 기간의 길이와 기술 도입에 소요되는 막대한 초기 비용), 기회(해외 의약품 제조 증가, 제품의 원격 인증, 연구개발 분야의 현저한 기술적 진보, 식품 이력추적 시장의 성장), 그리고 과제(일련번호 부여 및 집계와 관련된 공통 기준의 부재, 위조자 억제 기술의 가용성)에 대해 분석하여, 이러한 요인들이 이력관리 솔루션 시장의 성장에 미치는 영향을 밝히고 있습니다.

- 제품 개발 및 혁신: 이력관리 솔루션 시장에서 향후 기술, 연구개발 활동, 그리고 제품 및 서비스 출시에 관한 상세 인사이트.

- 시장 개발: 수익성이 높은 시장에 대한 포괄적인 정보. 이 보고서에서는 다양한 지역에 걸친 추적 및 트레이서빌리티 솔루션 시장을 분석하고 있습니다.

- 시장의 다양화: 추적 및 트레이서빌리티 솔루션 시장의 신제품·서비스, 미개발 지역, 최근 동향 및 투자에 관한 포괄적인 정보.

- 경쟁사 분석: Antares Vision S.p.A(이탈리아), Axway(프랑스), OPTEL GROUP(캐나다), TraceLink Inc.(미국), Syntegon Technology GmbH(독일), ACG(인도), Marchesini Group S.p.A.(이탈리아), Markem-Imaje(Dover 자회사)(스위스) 등 주요 기업의 시장 점유율, 성장 전략, 서비스 제공에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 테크놀러지, 특허, 디지털 기술, AI의 도입에 의한 전략적 파괴

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 이력관리 솔루션 시장(용도별)

제10장 이력관리 솔루션 시장(컴포넌트별)

제11장 이력관리 솔루션 시장(배포 모델별)

제12장 이력관리 솔루션 시장(최종사용자별)

제13장 이력관리 솔루션 시장(기술별)

제14장 이력관리 솔루션 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSA 26.06.25The track and trace solutions market is expected to grow from USD 8.20 billion in 2026 to USD 14.73 billion by 2031, with a CAGR of 12.4%. This growth is mainly attributed to the rising demand for product authentication, supply chain visibility, and regulatory requirements in pharmaceuticals, foods, medical devices, and cosmetics.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Component, Deployment Model, Application, Technology, End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

There is increasing investment in serialization, aggregation, barcode, RFID, NFC, vision inspection, and cloud-based traceability technologies to trace products from production lines, warehouses, distributors, to end users. The market is further witnessing a boost due to the growing trend amongst manufacturers of going beyond compliance and using track and trace technology for quick recall management, anti-counterfeit measures, partner communication, and process control.

"The barcode-based traceability segment accounted for the largest market share in 2025."

In terms of technology, the track and trace solutions market is divided into barcode traceability, RFID traceability, and NFC traceability. The barcode traceability segment dominated the market in 2025 due to its extensive usage in pharmaceuticals, foods, medical devices, cosmetics, and logistics industry. Barcodes continue to be the most efficient and economical technologies that help identify, serialize, aggregate, and report. Especially, 2D barcodes and Data Matrix codes have become popular for pharmaceutical packing since they can record product codes, serial numbers, batch information, and expiration dates within a tiny space. Their easy integration with packaging machinery, scanning devices, warehouses, and regulation platforms make barcodes-based systems more popular than other technologies. Moreover, increasing adoption of QR codes by consumers for product authentication further enhances their importance in track and trace solutions market.

"The software segment is expected to record the highest growth rate during the forecast period."

Based [VP2.1]on component, the track and trace solutions market is segmented into software, hardware, and services. Software is the fastest-growing segment among these due to the growing tendency to move away from standalone serialization systems and adopt integrated enterprise traceability solutions. The software becomes increasingly important when it comes to managing serialization data, aggregation structures, exchange of EPCIS data, regulatory submissions, audit logs, warehousing checks, and exceptions management. Given that businesses function within several plants and/or CMOs as well as work within country-specific compliance requirements, there is an increased need for scalable and configurable software platforms. There is also a rising demand for cloud-based traceability software since it allows for quicker implementation, partner connections, and better real-time visibility while reducing reliance on in-house IT facilities.

"Asia Pacific is expected to be the fastest-growing regional market during the forecast period."

Asia Pacific's rapid growth is driven by expanding manufacturing activity, rising exports, and the growing implementation of serialization and traceability regulations in key Asian economies. Notably, China, India, Japan, South Korea, and Australia are implementing tracking mechanisms across the pharmaceutical, medical device, food, and consumer goods industries, creating strong demand for serialization and barcode systems, aggregation machines, vision inspection, and cloud-based traceability solutions. India and China have emerged as significant growth markets in the Asia Pacific region, driven by the scale of pharmaceutical production, increased contract manufacturing, and high demand to meet global regulatory standards for exports to countries like the US and Europe. Meanwhile, Japan, South Korea, and Australia are contributing to growth through superior healthcare infrastructure, initiatives to ensure food safety, and automation in manufacturing and logistics. E-commerce, cross-border trade, and product counterfeiting have further driven demand in this region.

The breakdown of primary participants is as follows:

- By Company Type - Tier 1: 60%, Tier 2: 30%, and Tier 3: 10%

- By Designation - C-level: 30%, Director-level: 50%, and Others: 20%

- By Region - North America: 45%, Europe: 20%, Asia Pacific: 25%, Rest of the world: 10%

Antares Vision S.p.A (Italy), Axway (France), OPTEL GROUP (Canada), and TraceLink Inc. (US) are some of the key players in the track and trace solutions market.

- The study includes an in-depth competitive analysis of these key players in the track and trace solutions market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the track and trace solutions market by Component [Software (Modular Track & Trace Solutions, End-to-End Traceability Platforms), Hardware (Printing & Coding Systems, Vision Inspection & Verification Systems, Barcode Scanners & RFID Infrastructure, Packaging Line Controllers & Automation Systems, Others), Services (Integration & Deployment Services, Validation & Consulting Services, Managed & Support Services, Others)] | Deployment Model (On-premises, Cloud-based, Hybrid) | Application [Serialization (Carton Serialization, Bottle Serialization, Blister Serialization, Others), Aggregation (Bundle Aggregation, Case Aggregation, Pallet Aggregation), Warehouse & Distribution Traceability (Warehouse Verification, Shipment Traceability, Distribution Monitoring, Others), Compliance & Reporting (Regulatory Reporting, EPCIS Data Exchange, Audit Trail Management, Others), Authentication & Brand Protection (Product Authentication, Consumer Verification, Others)] | Technology [Barcode-based Traceability (Linear/1D Barcodes, 2D Barcodes & Data Matrix Codes, QR Codes), RFID-Based Traceability, NFC-Based Traceability] | End User (Pharmaceutical and Biopharmaceutical Companies, Food Industry, Medical Device Companies, Cosmetic Industry, Others) | Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the track and trace solutions market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements, product & service launches, mergers & acquisitions, and recent developments associated with the track and trace solutions market.

Reasons to buy this report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the track and trace solutions market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and to plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Stringent regulations and standards for serialization, increasing focus of manufacturers on brand protection, growth in packaging-related product recalls, high growth in generic and OTC markets, and growth of the medical device industry), restraints (Long implementation timeframe of serialization and aggregation and huge setup costs of technologies), opportunities (Increase in offshore pharmaceutical manufacturing, remote authentication of products, significant technological advancements in R&D, and growth in the food traceability market), and challenges (Lack of common standards for serialization and aggregation and availability of technologies to deter counterfeiters) influencing the growth of the track and trace solutions market.

- Product Development/Innovation: Detailed insights on upcoming technologies, R&D activities, and product & service launches in the track and trace solutions market.

- Market Development: Comprehensive information about lucrative markets; the report analyses the track and trace solutions market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the track and trace solutions market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Antares Vision S.p.A (Italy), Axway (France), OPTEL GROUP (Canada), TraceLink Inc. (US), Syntegon Technology GmbH (Germany), ACG (India), Marchesini Group S.p.A. (Italy), Markem-Imaje, a Dover Company. (Switzerland), among others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 TRACK AND TRACE SOLUTIONS MARKET OVERVIEW

- 3.2 TRACK & TRACE SOLUTIONS MARKET, BY APPLICATION & REGION

- 3.3 TRACK & TRACE SOLUTIONS MARKET: GEOGRAPHIC SNAPSHOT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Stringent regulations and standards for serialization

- 4.2.1.2 Increase in focus of manufacturers on brand protection

- 4.2.1.3 Growth in packaging-related product recalls

- 4.2.1.4 High growth in generic and OTC markets

- 4.2.1.5 Growth of medical device industry

- 4.2.2 RESTRAINTS

- 4.2.2.1 Huge setup costs for technologies

- 4.2.2.2 Long implementation timeframe of serialization and aggregation

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increase in offshore pharmaceutical manufacturing

- 4.2.3.2 Remote authentication of products

- 4.2.3.3 Significant technological advancements in R&D

- 4.2.3.4 Growth of food traceability market

- 4.2.4 CHALLENGES

- 4.2.4.1 Lack of common standards for serialization and aggregation

- 4.2.4.2 Existence of technologies to deter counterfeiters

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 THREAT OF NEW ENTRANTS

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN THE GLOBAL HEALTHCARE IT AND SUPPLY CHAIN INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICE FOR TRACK AND TRACE SOLUTIONS, BY PRODUCT (2025)

- 5.5.2 INDICATIVE PRICE FOR TRACK AND TRACE SOLUTIONS, BY REGION (2025)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 MARKET OPPORTUNITY ANALYSIS OF TRACK AND TRACE SOLUTIONS

- 5.9.2 TO SIMPLIFY PRODUCT TRACEABILITY FROM SEED TO STORE SHELF

- 5.9.3 TO FULFILL TRACK AND TRACE REGULATORY REQUIREMENTS ACROSS SEVERAL COUNTRIES WITH THE HELP OF VISIOTT TPS

- 5.10 IMPACT OF 2025 US TARIFF - OVERVIEW

- 5.10.1 INTRODUCTION

- 5.11 KEY TARIFF RATES

- 5.12 PRICE IMPACT ANALYSIS

- 5.13 IMPACT ON COUNTRY/REGION

- 5.13.1 US

- 5.13.2 EUROPE

- 5.13.3 ASIA PACIFIC

- 5.14 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 BLOCKCHAIN AND DISTRIBUTED LEDGER TECHNOLOGY (DLT)

- 6.1.2 RFID AND NEAR-FIELD COMMUNICATION (NFC)

- 6.1.3 INTERNET OF THINGS (IOT) FOR COLD-CHAIN AND ENVIRONMENTAL MONITORING

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ARTIFICIAL INTELLIGENCE (AI) & MACHINE LEARNING (ML)

- 6.2.2 CLOUD COMPUTING AND SAAS PLATFORMS

- 6.2.3 EDGE COMPUTING

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.4 PATENT ANALYSIS

- 6.4.1 PATENT PUBLICATION TRENDS FOR TRACK AND TRACE SOLUTIONS

- 6.4.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 DIGITAL PRODUCT PASSPORTS AND SUSTAINABILITY TRACEABILITY

- 6.5.2 ADVANCED THERAPY MEDICINAL PRODUCT (ATMP) AND CELL AND GENE THERAPY TRACEABILITY

- 6.5.3 CONSUMER-FACING AUTHENTICATION AND ENGAGEMENT VIA GS1 DIGITAL LINK

- 6.6 IMPACT OF AI/GEN AI ON TRACK & TRACE SOLUTIONS MARKET

- 6.6.1 INTRODUCTION

- 6.6.2 MARKET POTENTIAL OF AI/GEN AI IN TRACK & TRACE SOLUTIONS MARKET

- 6.6.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION

- 6.6.3.1 AI-driven serialization analytics & compliance risk detection

- 6.6.4 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 6.6.4.1 Serialization, Aggregation, and Packaging Line Systems

- 6.6.4.2 Supply Chain Visibility, Warehouse, and Distribution Platforms

- 6.6.4.3 Regulatory Compliance, Authentication, and Brand Protection

- 6.6.5 USER READINESS AND IMPACT ASSESSMENT

- 6.6.5.1 User readiness

- 6.6.5.1.1 User A: Pharmaceutical & Biopharmaceutical Companies

- 6.6.5.1.2 User B: Distributors, Logistics Providers, and Supply Chain Partners

- 6.6.5.2 Impact assessment

- 6.6.5.2.1 User A: Pharmaceutical & Biopharmaceutical Companies

- 6.6.5.2.2 User B: Distributors, Logistics Providers, and Supply Chain Partners

- 6.6.5.1 User readiness

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY ANALYSIS

- 7.1.3 NORTH AMERICA

- 7.1.4 EUROPE

- 7.1.5 ASIA PACIFIC

- 7.1.6 LATIN AMERICA AND MIDDLE EAST & AFRICA

- 7.1.7 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN THE BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.5 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5.1 UNMET NEEDS

- 8.5.2 END-USER EXPECTATIONS

- 8.6 MARKET PROFITABILITY

9 TRACK AND TRACE SOLUTIONS MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 SERIALIZATION APPLICATIONS

- 9.2.1 CARTON SERIALIZATION

- 9.2.1.1 Carton-level code application mandated as primary traceability data point across every major market

- 9.2.2 BOTTLE SERIALIZATION

- 9.2.2.1 Injectable and liquid pharmaceutical formats driving specialized bottle-level traceability investment

- 9.2.3 BLISTER SERIALIZATION

- 9.2.3.1 High-volume solid oral dose markets drive investment in compact blister serialization infrastructure

- 9.2.4 OTHERS

- 9.2.4.1 Non-standard packaging formats extending serialization technology into flexible and unit-dose applications

- 9.2.1 CARTON SERIALIZATION

- 9.3 AGGREGATION APPLICATIONS

- 9.3.1 BUNDLE AGGREGATION

- 9.3.1.1 Bundle-level grouping creates intermediate traceability tier for efficient pharmacy distribution

- 9.3.2 CASE AGGREGATION

- 9.3.2.1 Case-level SSCC aggregation serves as primary logistics traceability unit in pharmaceutical distribution

- 9.3.3 PALLET AGGREGATION

- 9.3.3.1 Pallet-level traceability linking full manufacturing output to first distribution touchpoint

- 9.3.1 BUNDLE AGGREGATION

- 9.4 WAREHOUSE & DISTRIBUTION TRACEABILITY APPLICATIONS

- 9.4.1 WAREHOUSE VERIFICATION

- 9.4.1.1 Automated serialized verification at receipt blocking counterfeit entry into legitimate supply chain

- 9.4.2 SHIPMENT TRACEABILITY

- 9.4.2.1 Electronic shipment records replacing paper documentation across pharmaceutical logistics handoffs

- 9.4.3 DISTRIBUTION MONITORING

- 9.4.3.1 Real-time distribution monitoring enabling proactive recall management and product diversion detection

- 9.4.4 OTHERS

- 9.4.4.1 Last-mile and cold-chain traceability extending distribution monitoring to every pharmaceutical touchpoint

- 9.4.1 WAREHOUSE VERIFICATION

- 9.5 COMPLIANCE & REPORTING APPLICATIONS

- 9.5.1 REGULATORY REPORTING

- 9.5.1.1 Country-specific repository submissions becoming most complex track and trace operational requirement

- 9.5.2 EPCIS DATA EXCHANGE

- 9.5.2.1 EPCIS 2.0 standard creating universal language for cross-industry supply chain traceability data

- 9.5.3 AUDIT TRAIL MANAGEMENT

- 9.5.3.1 Immutable transaction records enabling rapid regulatory response, recall execution, and investigation

- 9.5.4 OTHERS

- 9.5.4.1 AI-powered exception management and digital product passports expanding compliance application scope

- 9.5.1 REGULATORY REPORTING

- 9.6 AUTHENTICATION & BRAND PROTECTION APPLICATIONS

- 9.6.1 PRODUCT AUTHENTICATION

- 9.6.1.1 Serialized digital identities enabling real-time product legitimacy verification across global supply chains

- 9.6.2 CONSUMER VERIFICATION

- 9.6.2.1 QR and NFC scanning empowering direct-to-consumer product authenticity and transparency engagement

- 9.6.3 OTHERS

- 9.6.3.1 Investigative authentication and gray market monitoring extending brand protection into supply chain enforcement

- 9.6.1 PRODUCT AUTHENTICATION

10 TRACK AND TRACE SOLUTIONS MARKET, BY COMPONENT

- 10.1 INTRODUCTION

- 10.2 SOFTWARE

- 10.2.1 MODULAR TRACK & TRACE SOLUTIONS

- 10.2.1.1 Phased regulatory deadlines driving scalable module-by-module compliance deployment

- 10.2.2 END-TO-END TRACEABILITY PLATFORMS

- 10.2.2.1 Multi-jurisdiction compliance complexity accelerating adoption of unified network platforms

- 10.2.1 MODULAR TRACK & TRACE SOLUTIONS

- 10.3 HARDWARE

- 10.3.1 HIGH INVESTMENT IN SEGMENT TO BOOST GROWTH

- 10.3.2 PRINTING & CODING SYSTEMS

- 10.3.2.1 Mandatory high-speed serialized code application at pharmaceutical packaging lines to drive market

- 10.3.3 VISION INSPECTION & VERIFICATION SYSTEMS

- 10.3.3.1 Automated code verification eliminating serialization errors before market release at line speed

- 10.3.4 BARCODE SCANNERS & RFID INFRASTRUCTURE

- 10.3.4.1 RFID technology establishing complementary role alongside barcode in pharmaceutical traceability networks

- 10.3.5 PACKAGING LINE CONTROLLERS & AUTOMATION SYSTEMS

- 10.3.5.1 Smart line controllers synchronizing serialization data across high-speed integrated packaging operations

- 10.3.6 OTHERS

- 10.3.6.1 Peripheral traceability hardware expanding coverage across cold-chain and last-mile distribution points

- 10.4 SERVICES

- 10.4.1 INTEGRATION & DEPLOYMENT SERVICES

- 10.4.1.1 ERP-serialization integration complexity driving sustained demand for technical deployment expertise

- 10.4.2 VALIDATION & CONSULTING SERVICES

- 10.4.2.1 GxP validation and regulatory audit readiness sustaining specialized consulting demand globally

- 10.4.3 MANAGED & SUPPORT SERVICES

- 10.4.3.1 Continuous compliance obligations converting serialization deployments into long-term managed engagements

- 10.4.4 OTHERS

- 10.4.4.1 Specialized ancillary services addressing credentialing, security, and regulatory intelligence complexity

- 10.4.1 INTEGRATION & DEPLOYMENT SERVICES

11 TRACK AND TRACE SOLUTIONS MARKET, BY DEPLOYMENT MODEL

- 11.1 INTRODUCTION

- 11.2 ON-PREMISES

- 11.2.1 DATA SOVEREIGNTY REQUIREMENTS SUSTAINING ON-PREMISES DEPLOYMENT IN HIGHLY REGULATED NATIONAL MARKETS

- 11.3 CLOUD-BASED

- 11.3.1 SAAS SERIALIZATION NETWORKS DELIVERING INTEROPERABILITY SCALE THAT ON-PREMISES CANNOT REPLICATE

- 11.4 HYBRID

- 11.4.1 HYBRID ARCHITECTURES BALANCING DATA SOVEREIGNTY REQUIREMENTS WITH CLOUD SCALABILITY

12 TRACK AND TRACE SOLUTIONS MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 PHARMACEUTICAL & BIOPHARMACEUTICAL COMPANIES

- 12.2.1 GLOBAL SERIALIZATION WAVE CREATING SUSTAINED TECHNOLOGY INVESTMENT ACROSS PHARMACEUTICAL VALUE CHAIN

- 12.3 FOOD INDUSTRY

- 12.3.1 FSMA 204 FOOD TRACEABILITY RULE CATALYZING SUSTAINED TECHNOLOGY INVESTMENT ACROSS FOOD SUPPLY CHAIN

- 12.4 MEDICAL DEVICE COMPANIES

- 12.4.1 UDI REGULATIONS AND EXPANDING EUDAMED REQUIREMENTS DRIVE INVESTMENT IN MEDICAL DEVICE TRACEABILITY

- 12.5 COSMETIC INDUSTRY

- 12.5.1 ANTI-COUNTERFEITING IMPERATIVES AND DIGITAL PRODUCT PASSPORT REGULATIONS ACCELERATING TRACEABILITY ADOPTION

- 12.6 OTHER END USERS

- 12.6.1 VARYING REGULATORY FRAMEWORKS EXPAND TRACEABILITY ADOPTION ACROSS AGRICULTURE, TOBACCO, AND VETERINARY SECTORS

13 TRACK AND TRACE SOLUTIONS MARKET, BY TECHNOLOGY

- 13.1 INTRODUCTION

- 13.2 BARCODE-BASED TRACEABILITY

- 13.2.1 LINEAR (1D) BARCODES

- 13.2.1.1 Legacy linear barcodes transitioning as 2D mandates drive universal packaging code upgrade programs

- 13.2.2 2D BARCODES & DATA MATRIX CODES

- 13.2.2.1 DataMatrix codes mandated across all major regulatory frameworks as universal pharmaceutical serialization standard

- 13.2.3 QR CODES

- 13.2.3.1 QR codes expanding traceability value beyond compliance into consumer engagement and digital authentication

- 13.2.1 LINEAR (1D) BARCODES

- 13.3 RFID-BASED TRACEABILITY

- 13.3.1 RFID TECHNOLOGY MATURING AS VALIDATED COMPLEMENTARY STANDARD FOR HIGH-VALUE AUTOMATED PHARMACEUTICAL TRACEABILITY

- 13.4 NFC-BASED TRACEABILITY

- 13.4.1 SMARTPHONE-READABLE NFC TECHNOLOGY BRIDGING SUPPLY CHAIN TRACEABILITY WITH DIRECT CONSUMER AUTHENTICATION

14 TRACK AND TRACE SOLUTIONS MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 14.2.2 US

- 14.2.2.1 Full DSCSA enforcement reshaping pharma supply chain digitalization

- 14.2.3 CANADA

- 14.2.3.1 Voluntary-to-mandatory barcoding roadmap activating manufacturer investment

- 14.3 EUROPE

- 14.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 14.3.2 GERMANY

- 14.3.2.1 Advanced FMD alert management and AI-driven verification expanding platform demand

- 14.3.3 FRANCE

- 14.3.3.1 FMD maturity driving pharmaceutical export serialization and cloud platform growth

- 14.3.4 UK

- 14.3.4.1 Post-Brexit MHRA framework and Northern Ireland alignment accelerating platform reinvestment

- 14.3.5 ITALY

- 14.3.5.1 Bollino-to-EU-FMD transition creating high-value technology replacement cycle

- 14.3.6 SPAIN

- 14.3.6.1 Mature FMD compliance and parallel import complexity sustaining platform demand

- 14.3.7 REST OF EUROPE

- 14.4 ASIA PACIFIC

- 14.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 14.4.2 CHINA

- 14.4.2.1 Insurance reimbursement linkage accelerating nationwide point-of-dispensing traceability

- 14.4.3 JAPAN

- 14.4.3.1 Electronic package insert mandate embedding GS1 barcodes across national drug supply

- 14.4.4 INDIA

- 14.4.4.1 QR code mandate for top drug brands catalyzing domestic serialization industry

- 14.4.5 AUSTRALIA

- 14.4.5.1 TGA serialization standard creating phased mandatory compliance pipeline

- 14.4.6 SOUTH KOREA

- 14.4.6.1 EDMS real-time reporting enhances track and trace integration across pharmacy networks

- 14.4.7 REST OF ASIA PACIFIC

- 14.5 LATIN AMERICA

- 14.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 14.5.2 BRAZIL

- 14.5.2.1 SNCM full-chain compliance driving distributor and dispenser system upgrades

- 14.5.3 MEXICO

- 14.5.3.1 COFEPRIS regulatory modernization expanding serialization and anti-counterfeit investment

- 14.5.4 REST OF LATIN AMERICA

- 14.6 MIDDLE EAST & AFRICA

- 14.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 14.6.2 GCC

- 14.6.3 SAUDI ARABIA

- 14.6.3.1 SFDA mandates strengthen serialization compliance across pharmaceuticals

- 14.6.4 UAE

- 14.6.4.1 Tatmeen mandates drive serialization-led regulatory compliance

- 14.6.5 REST OF GCC

- 14.6.6 SOUTH AFRICA

- 14.6.6.1 SAHPRA regulatory reform and counterfeit threat accelerating traceability investment

- 14.6.7 REST OF MIDDLE EAST & AFRICA

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 15.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN TRACK AND TRACE SOLUTIONS MARKET

- 15.3 REVENUE SHARE ANALYSIS, 2021-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.5.1 STARS

- 15.5.2 PERVASIVE PLAYERS

- 15.5.3 EMERGING LEADERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.5.5.1 Company footprint

- 15.5.5.2 Region footprint

- 15.5.5.3 Component footprint

- 15.5.5.4 Application footprint

- 15.5.5.5 End User footprint

- 15.6 COMPANY EVALUATION MATRIX: STARTUPS /SMES, 2025

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 DYNAMIC COMPANIES

- 15.6.3 STARTING BLOCKS

- 15.6.4 RESPONSIVE COMPANIES

- 15.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.7 COMPANY VALUATION & FINANCIAL METRICS

- 15.7.1 FINANCIAL METRICS

- 15.7.2 COMPANY VALUATION

- 15.8 BRAND/SOFTWARE COMPARISON ANALYSIS

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES & APPROVALS

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

16 COMPANY PROFILES

- 16.1 OTHER PLAYERS

- 16.1.1 ANTARES VISION S.P.A.

- 16.1.1.1 Business overview

- 16.1.1.2 Products & services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches & approvals

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM View

- 16.1.1.4.1 Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 AXWAY

- 16.1.2.1 Business overview

- 16.1.2.2 Products & services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches

- 16.1.2.3.2 Deals

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths/Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 OPTEL GROUP

- 16.1.3.1 Business overview

- 16.1.3.2 Products & services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Deals

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths/Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 TRACELINK INC.

- 16.1.4.1 Business overview

- 16.1.4.2 Products & services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches

- 16.1.4.3.2 Deals

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths/Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 SYNTEGON TECHNOLOGY GMBH

- 16.1.5.1 Business overview

- 16.1.5.2 Products & services offered

- 16.1.5.3 MnM view

- 16.1.5.3.1 Key strengths/Right to win

- 16.1.5.3.2 Strategic choices

- 16.1.5.3.3 Weaknesses and competitive threats

- 16.1.6 ACG

- 16.1.6.1 Business overview

- 16.1.6.2 Products & services offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product launches

- 16.1.6.3.2 Deals

- 16.1.6.3.3 Expansions

- 16.1.7 MARCHESINI GROUP S.P.A.

- 16.1.7.1 Business overview

- 16.1.7.2 Products & services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Deals

- 16.1.8 MARKEM-IMAJE, A DOVER COMPANY

- 16.1.8.1 Business overview

- 16.1.8.2 Products & services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches

- 16.1.9 UHLMANN

- 16.1.9.1 Business overview

- 16.1.9.2 Products & services offered

- 16.1.10 SIEMENS

- 16.1.10.1 Business overview

- 16.1.10.2 Products & services offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Deals

- 16.1.11 SAP SE

- 16.1.11.1 Business overview

- 16.1.11.2 Products & services offered

- 16.1.12 ZEBRA TECHNOLOGIES CORP.

- 16.1.12.1 Business overview

- 16.1.12.2 Products & services offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Product launches

- 16.1.12.3.2 Deals

- 16.1.12.3.3 Expansions

- 16.1.13 METTLER-TOLEDO

- 16.1.13.1 Business overview

- 16.1.13.2 Products & services offered

- 16.1.14 IBM

- 16.1.14.1 Business overview

- 16.1.14.2 Products & services offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Product launches

- 16.1.14.3.2 Deals

- 16.1.15 WIPOTEC

- 16.1.15.1 Business overview

- 16.1.15.2 Products & services offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Expansions

- 16.1.16 VISIOTT TECHNOLOGIE GMBH

- 16.1.16.1 Business overview

- 16.1.16.2 Products & services offered

- 16.1.17 JEKSON VISION

- 16.1.17.1 Business overview

- 16.1.17.2 Products & services offered

- 16.1.18 KEVISION

- 16.1.18.1 Business overview

- 16.1.18.2 Products & services offered

- 16.1.18.3 Recent developments

- 16.1.18.3.1 Product launches & approvals

- 16.1.1 ANTARES VISION S.P.A.

- 16.2 OTHER PLAYERS

- 16.2.1 TRACKTRACERX INC.

- 16.2.2 ARVATO SYSTEMS

- 16.2.3 3KEYS

- 16.2.4 RN MARK INC

- 16.2.5 KEZZLER

- 16.2.6 SHUBHAM AUTOMATION PVT. LTD.

- 16.2.7 BAR CODE INDIA LIMITED

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 Insights from primary experts

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.3 DATA TRIANGULATION

- 17.4 STUDY ASSUMPTIONS

- 17.5 LIMITATIONS

- 17.5.1 METHODOLOGY-RELATED LIMITATIONS

- 17.5.2 SCOPE-RELATED LIMITATIONS

- 17.6 RISK ASSESSMENT

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS:

- 18.5 AUTHOR DETAILS