|

시장보고서

상품코드

2064084

산업용 로봇 시장 예측(-2032년) : 로봇 유형별, 가반중량별, 오퍼링별, 용도별, 최종 용도 산업별, 지역별Industrial Robotics Market by Robot (Articulated, SCARA, Cartesian, Parallel, Cylindrical, Collaborative), Payload (up to 16 kg, >16 to 60 kg, >60 to 225 kg, >225 kg), Offering (End Effectors, Controllers, Drive Units, Sensors) - Global Forecast to 2032 |

||||||

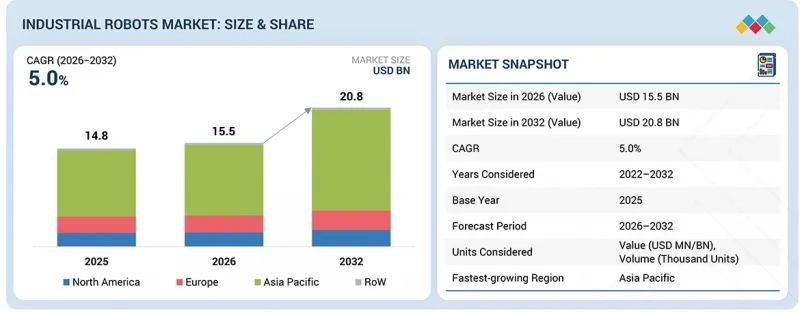

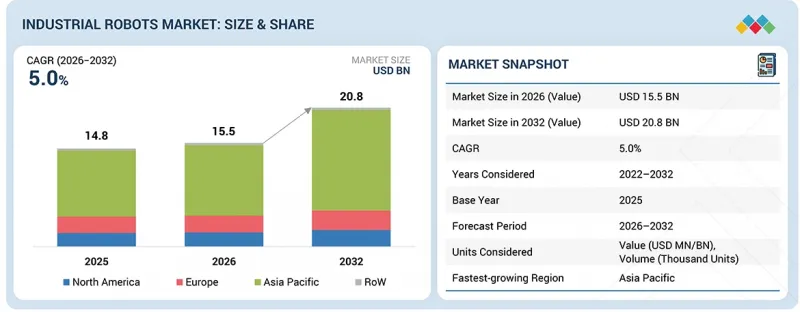

산업용 로봇 시장 규모는 2026년 155억 달러에서 2032년까지 208억 달러로 성장하며, 같은 기간의 CAGR은 5.0%에 달할 것으로 예측됩니다.

산업용 로봇 시장은 자동화 생산 시스템에 대한 수요 증가, 제조 효율 향상, 그리고 각 산업 분야의 조작 정밀도 향상에 힘입어 예측 기간 중 강력한 성장을 이룰 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 산정 단위 | 금액(10억 달러) |

| 부문 | 로봇 유형별, 가반중량별, 오퍼링별, 용도별, 최종 용도 산업별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

기업은 제조 환경에서 지속적인 생산을 유지하고, 운영 비용을 절감하며, 제품의 품질 안정성을 높이기 위해 산업용 로봇 솔루션에 대한 투자를 점점 더 늘리고 있습니다. 또한 스마트 팩토리의 확대, 노동력 부족의 심화, 그리고 인공지능(AI)을 탑재한 로봇 시스템의 도입 확대에 따라 각 업계는 첨단 자동화 기술을 활용하여 생산 설비의 현대화를 추진하고 있습니다. 유연한 제조, 직장 안전, 그리고 생산 주기 단축에 대한 관심이 높아지고 있는 점도 전 세계 산업용 로봇 시장의 장기적인 성장을 더욱 지원하고 있습니다.

“2026년에는 기존형 로봇이 가장 큰 시장 점유율을 차지할 것으로 추정됩니다. '

기존의 로봇 유형 부문은 자동차, 전자기기, 금속 가공, 중장비 등 대규모 제조업 분야에서 널리 채택되고 있으며, 산업용 로봇 시장에서 가장 큰 점유율을 차지하고 있습니다. 기존의 산업용 로봇은 용접, 조립, 도장, 자재 취급 작업 등 고속이며 반복적이고 높은 정밀도가 요구되는 작업에 널리 활용되고 있습니다. 이러한 높은 적재 중량, 운영 효율성, 그리고 연속 생산 공정을 지원하는 능력이 전 세계 시장 수요를 주도하고 있습니다. 또한 공장 자동화 및 스마트 제조 기술에 대한 투자 확대가 산업 환경 전반에 걸쳐 기존 산업용 로봇 시스템의 대규모 도입을 촉진하고 있습니다.

“소프트웨어 및 프로그래밍 분야는 예측 기간 중 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 추정됩니다. '

소프트웨어 및 프로그래밍 분야는 업종을 불문하고 지능형 자동화, 실시간 모니터링, 유연한 로봇 조작에 대한 수요 증가에 힘입어 산업용 로봇 시장에서 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 예상됩니다. 기업은 업무 효율과 생산 정밀도를 높이기 위해 첨단 로봇 프로그래밍 플랫폼, 시뮬레이션 소프트웨어, AI 기반 제어 시스템에 대한 투자를 점점 더 늘리고 있습니다. 스마트 팩토리, IIoT, 디지털 제조 기술의 도입 확대는 산업용 로봇 소프트웨어 솔루션에 대한 전 세계적 수요를 더욱 가속화하고 있습니다. 또한 소프트웨어 플랫폼을 통해 로봇 통합, 예측 유지보수, 원격 감시가 용이해지고, 생산 라인의 최적화도 신속해짐에 따라 시장의 급속한 성장을 지원하고 있습니다.

“아시아·태평양 지역은 예측 기간 중 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 전망됩니다. '

아시아태평양은 중국, 인도, 한국, 동남아시아 국가 등에서 제조업의 급속한 확대와 공장 자동화에 대한 투자 증가로 인해 산업용 로봇 시장에서 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 예상됩니다. 스마트 제조 기술의 도입 확대, 산업화의 진전, 그리고 대량 생산에 대한 수요 증가가 해당 지역 전체에서 산업용 로봇 시스템의 도입을 가속화하고 있습니다. 또한 자동차, 전자, 반도체 및 E-Commerce(e-커머스) 산업의 확장이 첨단 로봇 자동화 솔루션에 대한 강력한 수요를 창출하고 있습니다. 산업 현대화를 지원하는 정부의 노력에 더해, 인더스트리 4.0 및 디지털 제조 인프라에 대한 투자 증가도 아시아태평양의 산업용 로봇 시장의 급속한 성장에 더욱 기여하고 있습니다.

2차 조사를 통해 수집된 각종 부문 및 하위 부문 시장 규모를 파악하고 검증하기 위해, 산업용 로봇 솔루션 분야의 주요 업계 전문가들을 대상으로 광범위한 1차 인터뷰가 실시되었습니다. 이 보고서의 1차 인터뷰 대상자 구성은 다음과 같습니다. :

이 보고서에서는 산업용 로봇 시장의 주요 기업을 각각의 시장 순위 분석과 함께 소개하고 있습니다. 이 보고서에서 다루고 있는 주요 기업은 ABB(스위스), YASKAWA ELECTRIC CORPORATION(일본), FANUC Corporation(일본), KUKA SE &Co. KGaA(독일), 그리고 Mitsubishi Electric Corporation(일본)입니다.

이 밖에도 Kawasaki Heavy Industries, Ltd.(일본), DENSO CORPORATION(일본), NACHI Robotics(일본), Seiko Epson Corporation(일본), Durr Group(독일) 등이 산업용 로봇 시장의 주요 기업으로 꼽힙니다.

조사 범위:

본 조사 보고서에서는 산업용 로봇 시장을 로봇의 유형, 적재 중량, 제공 서비스, 용도, 최종 용도 산업 및 지역별로 분류하고 있습니다. 이 보고서에서는 산업용 로봇 시장의 주요 성장 동인, 제약 요인, 과제 및 기회에 대해 설명하고, 2032년까지의 전망을 제시하고 있습니다. 이 외에도 이 보고서에는 산업용 로봇 시장의 생태계에 속한 모든 기업에 대한 리더십 매핑 및 분석도 포함되어 있습니다.

이 보고서를 구매할 때의 주요 이점

이 보고서는 시장을 선도하는 기업 및 신규 진입 기업을 대상으로, 산업용 로봇 시장 전체 및 그 하위 부문에 관한 가장 정확한 수치 추정 정보를 제공합니다. 이 보고서는 이해관계자들이 경쟁 구도를 이해하고, 더 심층 인사이트를 얻어, 자사의 비즈니스를 최적의 위치에 자리매김하며, 적절한 시장 진입 전략을 수립하는 데 도움이 됩니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움이 되며, 주요 시장 촉진요인, 제약 요인, 과제 및 기회에 대한 정보를 제공합니다.

이 보고서에서는 다음 사항에 대한 인사이트를 제공합니다. :

- 주요 촉진요인(제조 업무 최적화를 위한 자동화 솔루션 도입 확대, AI 및 디지털 자동화 기술의 급속한 발전), 제약 요인(협동 로봇의 높은 비용), 기회(인더스트리 5.0의 부상, 전자기기 제조 분야의 자동화 진전) 및 과제(다양한 워크스테이션에 협동 로봇을 통합함에 따른 복잡성, 표준화 부족 및 상호 운용성 문제)에 대한 분석

- 제품 개발/혁신: 산업용 로봇 시장의 향후 기술, 연구개발 활동 및 신제품·서비스 출시에 관한 상세 인사이트

- 시장 개발: 수익성이 높은 시장에 대한 포괄적인 정보 -- 이 보고서에서는 다양한 지역에 걸친 산업용 로봇 시장을 분석하고 있습니다.

- 시장의 다양화: 산업용 로봇 시장의 신제품·서비스, 미개발 지역, 최근 동향 및 투자에 관한 포괄적인 정보

- 경쟁사 분석: 산업용 로봇 시장의 주요 기업, ABB(스위스), YASKAWA ELECTRIC CORPORATION(일본), FANUC Corporation(일본), KUKA SE &Co. KGaA(독일), Mitsubishi Electric Corporation(일본)의 시장 점유율, 성장 전략 및 서비스 제공에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 산업용 로봇 재생(정성 적)

제10장 산업용 로봇 시장(로봇 유형별)

제11장 산업용 로봇 시장(가반중량별)

제12장 산업용 로봇 시장(오퍼링별)

제13장 산업용 로봇 시장(용도별)

제14장 산업용 로봇 시장(최종 용도 산업별)

제15장 산업용 로봇 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSAThe industrial robots market is projected to grow from USD 15.50 billion in 2026 to USD 20.80 billion by 2032, registering a CAGR of 5.0% during the same period. The industrial robotics market is expected to grow strongly during the forecast period, driven by rising demand for automated production systems, higher manufacturing efficiency, and improved operational precision across industries.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Robot, Payload, Offering and Region |

| Regions covered | North America, Europe, APAC, RoW |

Companies are increasingly investing in industrial robotic solutions to support continuous production, reduce operational costs, and improve product consistency in manufacturing environments. In addition, the growing expansion of smart factories, increasing labor shortages, and rising adoption of Artificial Intelligence (AI)-enabled robotic systems are encouraging industries to modernize production facilities with advanced automation technologies. The increasing focus on flexible manufacturing, workplace safety, and faster production cycles is further supporting the long-term expansion of the global industrial robotics market.

"Traditional robot type is estimated to hold the largest market share in 2026."

The traditional robot type segment holds the largest share in the industrial robots market due to its widespread adoption across large-scale manufacturing industries such as automotive, electronics, metal processing, and heavy machinery. Traditional industrial robots are widely used for high-speed, repetitive, and precision-based tasks, including welding, assembly, painting, and material handling operations. Their high payload capacity, operational efficiency, and ability to support continuous production processes are driving strong global market demand. In addition, increasing investments in factory automation and smart manufacturing technologies are further supporting the large-scale deployment of traditional industrial robotic systems across industrial environments.

"Software & programming offering is estimated to record the highest CAGR during the forecast period."

The software & programming offering segment is expected to register the highest CAGR in the industrial robotics market, driven by increasing demand for intelligent automation, real-time monitoring, and flexible robotic operations across industries. Companies are increasingly investing in advanced robot programming platforms, simulation software, and AI-based control systems to improve operational efficiency and production accuracy. The growing adoption of smart factories, IIoT, and digital manufacturing technologies is further accelerating global demand for industrial robotics software solutions. In addition, software platforms enable easier robot integration, predictive maintenance, remote monitoring, and faster production line optimization, which supports rapid market growth.

"Asia Pacific is projected to grow at the highest CAGR during the forecast period."

Asia Pacific is expected to register the highest CAGR in the industrial robotics market due to the rapid expansion of manufacturing industries and increasing investments in factory automation across countries such as China, India, South Korea, and Southeast Asian nations. The growing adoption of smart manufacturing technologies, rising industrialization, and increasing demand for high-volume production are accelerating the deployment of industrial robotic systems across the region. In addition, the expansion of automotive, electronics, semiconductor, and e-commerce industries is creating strong demand for advanced robotic automation solutions. Government initiatives supporting industrial modernization, along with increasing investments in Industry 4.0 and digital manufacturing infrastructure, are further contributing to the rapid growth of the industrial robotics market in Asia Pacific.

Extensive primary interviews were conducted with key industry experts on industrial robotics solutions to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is provided below:

The study contains insights from various industry experts, including component suppliers, Tier 1 companies, and OEMs. The break-up of the primaries is as follows:

- By Company Type: Tier 1-35%, Tier 2-40%, and Tier 3-25%

- By Designation: C-level-23%, Directors-30%, and Others-47%

- By Region: North America-22%, Europe-22%, Asia Pacific-45%, and RoW-11%

The report profiles key players in the industrial robotics market with their respective market ranking analysis. Prominent players profiled in this report are ABB (Switzerland), YASKAWA ELECTRIC CORPORATION (Japan), FANUC Corporation (Japan), KUKA SE & Co. KGaA (Germany), and Mitsubishi Electric Corporation (Japan).

Apart from this, Kawasaki Heavy Industries, Ltd. (Japan), DENSO CORPORATION (Japan), NACHI Robotics (Japan), Seiko Epson Corporation (Japan), and Durr Group (Germany), among others, are the few other companies in the industrial robotics market.

Research Coverage:

This research report categorizes the industrial robotics market based on robot type, payload, offering, application, end-use industry, and region. The report describes the major drivers, restraints, challenges, and opportunities in the industrial robotics market and forecasts them through 2032. Apart from this, the report also includes leadership mapping and analysis of all the companies in the industrial robotics market ecosystem.

Key Benefits of Buying the Report

The report will help market leaders and new entrants with information on the closest approximations of numbers for the overall industrial robotics market and its subsegments. This report will help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (mounting adoption of automation solutions to optimize manufacturing operations, rapid advances in AI and digital automation technologies), restraints (high costs of collaborative robots), opportunities (emergence of industry 5.0, rise in automation in electronics manufacturing), and challenges (complexities associated with integrating cobots into diverse workstations, lack of standardization and interoperability issues)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and new product & service launches in the industrial robotics market

- Market Development: Comprehensive information about lucrative markets-the report analyzes the industrial robotics market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the industrial robotics market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, ABB (Switzerland), YASKAWA ELECTRIC CORPORATION (Japan), FANUC Corporation (Japan), KUKA SE & Co. KGaA (Germany), and Mitsubishi Electric Corporation (Japan) in the industrial robotics market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING INDUSTRIAL ROBOTICS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INDUSTRIAL ROBOTS MARKET

- 3.2 INDUSTRIAL ROBOTS MARKET, BY APPLICATION

- 3.3 INDUSTRIAL ROBOTS, BY END-USE INDUSTRY

- 3.4 INDUSTRIAL ROBOTS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing adoption of collaborative robots across industries

- 4.2.1.2 Shortage of skilled workforce in manufacturing sector

- 4.2.1.3 Rising deployment of Industry 4.0 technologies

- 4.2.1.4 Mounting adoption of automation solutions to optimize manufacturing operations

- 4.2.1.5 Rapid advances in AI and digital automation technologies

- 4.2.2 RESTRAINTS

- 4.2.2.1 High costs of collaborative robots

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rise in automation in electronics manufacturing

- 4.2.3.2 Emergence of Industry 5.0

- 4.2.4 CHALLENGES

- 4.2.4.1 Requirement for extensive training and expertise in setting up high-end robots

- 4.2.4.2 Lack of standardization and interoperability issues

- 4.2.4.3 Complexities associated with integrating cobots into diverse workstations

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.2.2 BARGAINING POWER OF SUPPLIERS

- 5.2.3 BARGAINING POWER OF BUYERS

- 5.2.4 THREAT OF SUBSTITUTES

- 5.2.5 THREAT OF NEW ENTRANTS

- 5.3 MACROECONOMIC INDICATORS

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- 5.3.4 TRENDS IN GLOBAL ELECTRICAL & ELECTRONICS INDUSTRY

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICING TREND OF KEY PLAYERS, BY ROBOT TYPE

- 5.5.2 AVERAGE SELLING PRICE, BY TYPE

- 5.5.3 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 847950)

- 5.6.2 EXPORT SCENARIO (HS CODE 847950)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT AND FUNDING SCENARIO, 2022-2026

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 QISDA ADOPTED TOUCHE SOLUTIONS' HUMAN-ROBOT COLLABORATION SAFETY SOLUTION TO MINIMIZE COLLISIONS

- 5.10.2 GREAT PLAINS MANUFACTURING IMPLEMENTED GENESIS' VIRTUAL SOLUTION FOR ROBOT WELDING TO INCREASE PRODUCTION SPEED

- 5.10.3 TTI, INC. USED DRIVERLESS ROBOTS TO AUTOMATE CART PICKING AND DELIVERY PROCESSES

- 5.10.4 SCHOTT AG IMPLEMENTED AUTOMATION SOLUTION USING ONROBOT'S RG2-FT GRIPPER TO MITIGATE MANUAL LOADING

- 5.10.5 EMERSON PROFESSIONAL TOOLS ADOPTED FANUC COBOT CRX-10IA/L TO MEET SAFETY REQUIREMENTS

- 5.10.6 GRUPO FORTEC LEVERAGED MITSUBISHI ELECTRIC'S ROBOTICS TECHNOLOGY TO FACILITATE BULK PALLETIZING

- 5.11 IMPACT OF 2025 US TARIFF -INDUSTRIAL ROBOTICS MARKET

- 5.11.1 INTRODUCTION

- 5.11.1.1 Key tariff rates

- 5.11.2 PRICE IMPACT ANALYSIS

- 5.11.3 IMPACT OF COUNTRIES/REGIONS

- 5.11.3.1 US

- 5.11.3.2 Europe

- 5.11.3.3 Asia Pacific

- 5.11.4 IMPACT ON INDUSTRIES

- 5.11.1 INTRODUCTION

6 TECHNOLOGICAL ADVANCEMENTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 INDUSTRIAL ROBOTS AND VISION SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 INDUSTRIAL INTERNET OF THINGS AND ARTIFICIAL INTELLIGENCE

- 6.2.2 SAFETY SENSORS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 5G

- 6.4 TECHNOLOGY ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.7 IMPACT OF AI ON INDUSTRIAL ROBOTICS

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN INDUSTRIAL ROBOTICS MARKET

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN INDUSTRIAL ROBOTICS MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT AI IN INDUSTRIAL ROBOTICS MARKET

7 REGULATORY LANDSCAPE

- 7.1 INTRODUCTION

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END USERS

9 REFURBISHMENT OF INDUSTRIAL ROBOTS (QUALITATIVE)

- 9.1 INTRODUCTION

- 9.2 KEY PARAMETERS

- 9.2.1 CYCLE TIME

- 9.2.2 PERFORMANCE & ACCURACY

- 9.2.3 WEAR & TEAR

- 9.3 REFURBISHMENT TRENDS FOR VARIOUS INDUSTRIAL ROBOTS

- 9.4 TOP FIVE INDUSTRIES ADOPTING REFURBISHED ROBOTS

- 9.4.1 AUTOMOTIVE

- 9.4.2 METALS & MACHINERY

- 9.4.3 ELECTRICAL & ELECTRONICS

- 9.4.4 SMALL WORKSHOPS

- 9.4.5 FOOD & BEVERAGES

- 9.4.6 PHARMACEUTICALS & HEALTHCARE

- 9.4.7 LOGISTICS & WAREHOUSING

- 9.5 KEY PRACTICES OF INDUSTRIAL ROBOT OEMS

- 9.5.1 FOCUS ON NEW ROBOTS

- 9.5.2 POST-SALES SERVICE

- 9.5.3 RESEARCH & DEVELOPMENT

- 9.5.4 CUSTOMIZATION & FLEXIBILITY

- 9.5.5 INTEGRATION & CONNECTIVITY

- 9.5.6 SAFETY STANDARDS AND COMPLIANCE

- 9.5.7 USE CASE: JACOBS DOUWE EGBERTS ENHANCES PERFORMANCE WITH ABB IRB640 REFURBISHED ROBOT

- 9.5.8 USE CASE: OSSID MACHINERY BOOSTS RELIABILITY PERFORMANCE WITH AND MITSUBISHI ELECTRIC AUTOMATION PORTFOLIO

10 INDUSTRIAL ROBOTICS MARKET, BY ROBOT TYPE

- 10.1 INTRODUCTION

- 10.2 TRADITIONAL ROBOTS

- 10.2.1 ARTICULATED ROBOTS

- 10.2.1.1 Flexibility, accuracy, and cost-effectiveness to boost segmental growth

- 10.2.2 SCARA ROBOTS

- 10.2.2.1 Precision in material handling to contribute to segmental growth

- 10.2.3 PARALLEL ROBOTS

- 10.2.3.1 Enhanced stiffness, accuracy, and dynamic performance to augment segmental growth

- 10.2.4 CARTESIAN ROBOTS

- 10.2.4.1 Capability to handle heavy loads to accelerate segmental growth

- 10.2.5 CYLINDRICAL ROBOTS

- 10.2.5.1 Compact and space-saving structures to expedite segmental growth

- 10.2.6 OTHER TRADITIONAL ROBOTS

- 10.2.1 ARTICULATED ROBOTS

- 10.3 COLLABORATIVE ROBOTS

- 10.3.1 EASE OF USE AND LOW-COST DEPLOYMENT TO DRIVE MARKET

11 INDUSTRIAL ROBOTICS MARKET, BY PAYLOAD

- 11.1 INTRODUCTION

- 11.2 UP TO 16.00 KG

- 11.2.1 HIGH ACCURACY AND FLEXIBILITY TO STRENGTHEN MARKET

- 11.3 16.01-60.00 KG

- 11.3.1 AUTOMOTIVE INDUSTRY TO OFFER LUCRATIVE OPPORTUNITIES

- 11.4 60.01-225.00 KG

- 11.4.1 ENSURED SAFETY IN INDUSTRIES WITH HEAVY AND CUMBERSOME MATERIALS TO BOOST DEMAND

- 11.5 MORE THAN 225.00 KG

- 11.5.1 REDUCED RISK OF HUMAN INJURY AND IMPROVED PRODUCTIVITY TO AUGMENT MARKET SIZE

12 INDUSTRIAL ROBOTICS MARKET, BY OFFERING

- 12.1 INTRODUCTION

- 12.2 TRADITIONAL INDUSTRIAL ROBOTS

- 12.2.1 PHARMACEUTICAL AND FOOD AND BEVERAGE SECTORS TO GENERATE SIGNIFICANT DEMAND

- 12.3 ROBOT ACCESSORIES

- 12.3.1 GROWING INVESTMENT IN RESEARCH AND DEVELOPMENT TO DRIVE MARKET

- 12.3.2 END EFFECTORS

- 12.3.2.1 Growth in welding and painting applications to boost demand

- 12.3.2.2 Welding guns

- 12.3.2.2.1 Suitable for high-volume production applications

- 12.3.2.3 Grippers

- 12.3.2.3.1 Growing need to handle sensitive objects cautiously to boost demand

- 12.3.2.3.2 Mechanical

- 12.3.2.3.2.1 Cost-effective nature to drive market

- 12.3.2.3.3 Electric

- 12.3.2.3.3.1 Programmability and seamless integration with other robotic systems to boost demand

- 12.3.2.3.4 Magnetic

- 12.3.2.3.4.1 Capability to function during blackout to drive market

- 12.3.2.4 Tool changers

- 12.3.2.4.1 Increasing need to use robotic tool changers for multiple functioning of robot arms

- 12.3.2.5 Clamps

- 12.3.2.5.1 Space-saving benefits and enhanced safety to strengthen market

- 12.3.2.6 Suction cup

- 12.3.2.6.1 Inexpensive and versatility to benefit market growth

- 12.3.2.7 Others

- 12.3.2.7.1 Deburring tools

- 12.3.2.7.2 Milling tools

- 12.3.2.7.3 Soldering tools

- 12.3.2.7.4 Painting tools

- 12.3.2.7.5 Screwdrivers

- 12.3.3 CONTROLLERS

- 12.3.3.1 Ease of programming and minimizing compatibility issues to drive demand

- 12.3.4 DRIVE UNITS

- 12.3.4.1 Ability to enhance capacity of robot to boost demand

- 12.3.4.2 Hydraulic drive

- 12.3.4.2.1 Ability to be used around highly explosive materials t o boost demand

- 12.3.4.3 Electric drives

- 12.3.4.3.1 Low maintenance requirements to augment market size

- 12.3.4.4 Pneumatic drives

- 12.3.4.4.1 Ease of installation to benefit market

- 12.3.5 VISION SYSTEMS

- 12.3.5.1 Reduced human involvement and operational benefits to strengthen market

- 12.3.6 SENSORS

- 12.3.6.1 Incorporation of sensors in industrial robots to gather information about environment to strengthen market

- 12.3.7 POWER SUPPLY

- 12.3.7.1 Incorporation of safety features like voltage regulation to drive market

- 12.3.8 OTHERS

- 12.4 ADDITIONAL HARDWARE

- 12.4.1 SAFETY FENCING

- 12.4.1.1 Addresses safety concerns by machine perimeter guarding, among others

- 12.4.2 FIXTURES

- 12.4.2.1 Enhanced flexibility in manufacturing to expand segment growth

- 12.4.3 CONVEYORS

- 12.4.3.1 High efficiency in manufacturing processes to augment market size

- 12.4.1 SAFETY FENCING

- 12.5 SYSTEM ENGINEERING

- 12.5.1 FACILITATES INSTALLATION OF ROBOTIC SYSTEM IN INDUSTRIAL ENVIRONMENT

- 12.6 SOFTWARE & PROGRAMMING

- 12.6.1 EASE OF MAINTENANCE AND OPERATIONS OF INDUSTRIAL ROBOTS TO BOOST DEMAND

13 INDUSTRIAL ROBOTS MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- 13.2 HANDLING

- 13.2.1 INCREASING DEMAND FOR PALLETIZING ROBOTS TO MOVE HEAVY OBJECTS TO BOOST SEGMENTAL GROWTH

- 13.2.2 PICK & PLACE

- 13.2.3 MATERIAL HANDLING

- 13.2.4 PACKAGING & PALLETIZING

- 13.3 ASSEMBLING & DISASSEMBLING

- 13.3.1 RISING EMPHASIS ON MAINTAINING MANUFACTURING QUALITY AND CONSISTENCY TO FOSTER SEGMENTAL GROWTH

- 13.4 WELDING & SOLDERING

- 13.4.1 GROWING FOCUS ON IMPROVING WELD QUALITY AND JOINT INTEGRITY TO DRIVE MARKET

- 13.5 DISPENSING

- 13.5.1 RAPID ADVANCES IN MOTION CONTROL AND SENSING TECHNOLOGIES TO BOLSTER SEGMENTAL GROWTH

- 13.5.2 GLUING

- 13.5.3 PAINTING

- 13.5.4 FOOD DISPENSING

- 13.6 PROCESSING

- 13.6.1 RISING DEPLOYMENT OF ROBOTIC GRINDERS IN AUTOMOTIVE SECTOR TO FUEL SEGMENTAL GROWTH

- 13.6.2 GRINDING & POLISHING

- 13.6.3 MILLING

- 13.6.4 CUTTING

- 13.7 CLEANROOM

- 13.7.1 INCREASING NEED TO MINIMIZE PARTICLE GENERATION AND COMPLY WITH REGULATIONS TO AUGMENT SEGMENTAL GROWTH

- 13.8 OTHER APPLICATIONS

14 INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY

- 14.1 INTRODUCTION

- 14.2 AUTOMOTIVE

- 14.2.1 INCREASING NEED FOR AUTOMATED SPOT WELDING AND PAINTING TO DRIVE MARKET

- 14.3 ELECTRICAL & ELECTRONICS

- 14.3.1 RISING ADOPTION OF SCARA ROBOTS IN CLEANROOM APPLICATIONS TO BOLSTER SEGMENTAL GROWTH

- 14.4 METALS & MACHINERY

- 14.4.1 INCREASING USE OF END EFFECTORS TO AUTOMATE HAZARDOUS TASKS TO FUEL SEGMENTAL GROWTH

- 14.5 PLASTICS, RUBBER & CHEMICALS

- 14.5.1 MOUNTING DEMAND FOR ROBOTS TO ENSURE HIGH-SPEED TASK EXECUTION TO ACCELERATE SEGMENTAL GROWTH

- 14.6 FOOD & BEVERAGES

- 14.6.1 INCREASING REQUIREMENT FOR WATER-RESISTANT ROBOTS TO FOSTER SEGMENTAL GROWTH

- 14.7 PRECISION ENGINEERING & OPTICS

- 14.7.1 RISING EMPHASIS ON REDUCING MANUAL LABOR AND AUTOMATING COMPLEX TASKS TO CONTRIBUTE TO SEGMENTAL GROWTH

- 14.8 PHARMACEUTICALS & COSMETICS

- 14.8.1 ESCALATING ADOPTION OF AUTOMATED SYSTEMS TO MINIMIZE CONTAMINATION AND HUMAN ERROR TO DRIVE MARKET

- 14.9 OIL & GAS

- 14.9.1 GROWING FOCUS ON INCREASING ACCURACY OF DRILLING OPERATIONS TO BOOST SEGMENTAL GROWTH

- 14.10 OTHER END-USE INDUSTRIES

15 INDUSTRIAL ROBOTS MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 US

- 15.2.1.1 Increased emphasis on automating manufacturing operations to contribute to market growth

- 15.2.2 CANADA

- 15.2.2.1 Implementation of policies and grants to encourage adoption of robots to drive market

- 15.2.3 MEXICO

- 15.2.3.1 Expansion of manufacturing facilities to boost market growth

- 15.2.1 US

- 15.3 EUROPE

- 15.3.1 GERMANY

- 15.3.1.1 Mounting investment in electric and hybrid vehicles to fuel market growth

- 15.3.2 ITALY

- 15.3.2.1 Escalating adoption of robots in automobile manufacturing facilities to augment market growth

- 15.3.3 FRANCE

- 15.3.3.1 Rising adoption of electric and hybrid vehicles to drive demand for robots

- 15.3.4 SPAIN

- 15.3.4.1 Increasing adoption of robots in surgical applications to accelerate market growth

- 15.3.5 UK

- 15.3.5.1 Rising deployment of advanced technologies in industrial sectors to foster market growth

- 15.3.6 REST OF EUROPE

- 15.3.1 GERMANY

- 15.4 ASIA PACIFIC

- 15.4.1 CHINA

- 15.4.1.1 Mounting adoption of automation solutions due to labor shortage to drive market

- 15.4.2 SOUTH KOREA

- 15.4.2.1 Rising implementation of initiatives to support automated machine training to boost market growth

- 15.4.3 JAPAN

- 15.4.3.1 Increasing aging population and automation trends to contribute to market growth

- 15.4.4 TAIWAN

- 15.4.4.1 Rising implementation of government policies to promote research of automation technologies to drive market

- 15.4.5 INDIA

- 15.4.5.1 Mounting demand for cobots in industries to expedite market growth

- 15.4.6 THAILAND

- 15.4.6.1 Rising emphasis on automating manufacturing operations to fuel market growth

- 15.4.7 REST OF ASIA PACIFIC

- 15.4.1 CHINA

- 15.5 ROW

- 15.5.1 MIDDLE EAST

- 15.5.1.1 Burgeoning demand for automated material handling systems to drive market

- 15.5.1.2 GCC

- 15.5.1.3 Rest of Middle East

- 15.5.2 AFRICA

- 15.5.2.1 Increasing shipment of robots for industrial operations to augment market growth

- 15.5.3 SOUTH AMERICA

- 15.5.3.1 Rapid urbanization and industrial development to fuel market growth

- 15.5.1 MIDDLE EAST

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 16.3 REVENUE ANALYSIS, 2022-2025

- 16.4 MARKET SHARE ANALYSIS, 2025

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS

- 16.6 BRAND/PRODUCT COMPARISON

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Payload footprint

- 16.7.5.4 End-use industry footprint

- 16.7.5.5 Robot type footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 16.8.5.1 Detailed list of key startups/SMEs

- 16.8.5.2 Competitive benchmarking of key startups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 ABB

- 17.1.1.1 Business overview

- 17.1.1.2 Products/Solutions/Services offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches

- 17.1.1.3.2 Deals

- 17.1.1.3.3 Expansions

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths/Right to win

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses/Competitive threats

- 17.1.2 YASKAWA ELECTRIC CORPORATION

- 17.1.2.1 Business overview

- 17.1.2.2 Products/Solutions/Services offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.3.2 Deals

- 17.1.2.3.3 Expansions

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths/Right to win

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses/Competitive threats

- 17.1.3 FANUC CORPORATION

- 17.1.3.1 Business overview

- 17.1.3.2 Products/Solutions/Services offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches

- 17.1.3.3.2 Deals

- 17.1.3.3.3 Expansions

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths/Right to win

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses/Competitive threats

- 17.1.4 KUKA SE & CO. KGAA

- 17.1.4.1 Business overview

- 17.1.4.2 Products/Solutions/Services offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches

- 17.1.4.3.2 Deals

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths/Right to win

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses/Competitive threats

- 17.1.5 MITSUBISHI ELECTRIC CORPORATION

- 17.1.5.1 Business overview

- 17.1.5.2 Products/Solutions/Services offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product launches

- 17.1.5.3.2 Deals

- 17.1.5.3.3 Expansions

- 17.1.5.4 MnM view

- 17.1.5.4.1 Key strengths/Right to win

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses/Competitive threats

- 17.1.6 KAWASAKI HEAVY INDUSTRIES, LTD.

- 17.1.6.1 Business overview

- 17.1.6.2 Products/Solutions/Services offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches

- 17.1.6.3.2 Deals

- 17.1.7 DENSO CORPORATION

- 17.1.7.1 Business overview

- 17.1.7.2 Products/Solutions/Services offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Deals

- 17.1.8 NACHI-FUJIKOSHI CORP.

- 17.1.8.1 Business overview

- 17.1.8.2 Products/Solutions/Services offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches

- 17.1.9 SEIKO EPSON CORPORATION

- 17.1.9.1 Business overview

- 17.1.9.2 Products/Solutions/Services offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Product launches

- 17.1.9.3.2 Deals

- 17.1.10 DURR GROUP

- 17.1.10.1 Business overview

- 17.1.10.2 Products/Solutions/Services offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Product launches

- 17.1.10.3.2 Deals

- 17.1.1 ABB

- 17.2 OTHER PLAYERS

- 17.2.1 YAMAHA MOTOR CO., LTD.

- 17.2.2 ESTUN AUTOMATION CO., LTD

- 17.2.3 SHIBAURA MACHINE

- 17.2.4 DOVER CORPORATION

- 17.2.5 AUROTEK CORPORATION

- 17.2.6 HIRATA CORPORATION

- 17.2.7 RETHINK ROBOTICS

- 17.2.8 FRANKA ROBOTICS GMBH

- 17.2.9 TECHMAN ROBOT INC.

- 17.2.10 BOSCH REXROTH AG

- 17.2.11 UNIVERSAL ROBOTS A/S

- 17.2.12 OMRON CORPORATION

- 17.2.13 STAUBLI INTERNATIONAL AG

- 17.2.14 COMAU

- 17.2.15 B+M SURFACE SYSTEMS GMBH

- 17.2.16 ICR SERVICES

- 17.2.17 IRS ROBOTICS

- 17.2.18 HD HYUNDAI ROBOTICS

- 17.2.19 SIASUN ROBOT & AUTOMATION CO., LTD

- 17.2.20 ROBOTWORX

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 List of key secondary sources

- 18.1.1.2 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 List of primary interview participants

- 18.1.2.2 Key data from primary sources

- 18.1.2.3 Breakdown of primaries

- 18.1.2.4 Key industry insights

- 18.1.3 SECONDARY AND PRIMARY RESEARCH

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION METHODOLOGY

- 18.2.1 BOTTOM-UP APPROACH

- 18.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 18.2.2 TOP-DOWN APPROACH

- 18.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

- 18.2.1 BOTTOM-UP APPROACH

- 18.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 18.4 RESEARCH ASSUMPTIONS

- 18.5 RISK ANALYSIS

- 18.6 RESEARCH LIMITATIONS

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS