|

시장보고서

상품코드

2064089

액체 도포형 방수막 시장 예측(-2031년) : 용도별, 최종 용도 산업별, 유형별, 사용법별, 지역별Liquid-applied Membrane Market by Type (Bituminous, Elastomeric, Cementitious), Application (Roofing, Walls, Roadways), Usage (New Construction, Refurbishment), End-use Industry (Commercial, Residential), and Region - Global Forecast to 2031 |

||||||

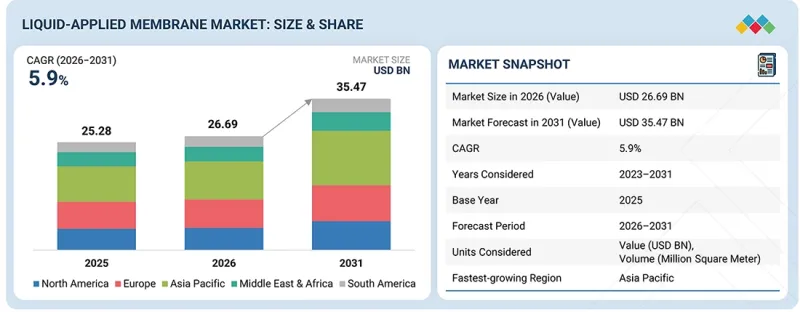

액체 도포형 방수막 시장 규모는 2026년 266억 9,000만 달러에서 2031년까지 354억 7,000만 달러에 달할 것으로 예상되고 있으며, 예측 기간 중 CAGR은 5.9%에 달할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2023-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(100만/10억 달러), 수량(백만 평방미터) |

| 부문 | 유형, 용도, 이용 형태, 최종 용도 산업 및 지역 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

효율적이고 이음매 없는 방수 솔루션에 대한 수요가 증가함에 따라 액상 도포형 방수막(LAM) 세계 시장은 점차 확대되고 있습니다. 시장 성장의 주요 촉진요인은 주택, 상업, 산업을 포함한 각 부문에서의 도시화와 인프라 개발입니다. 또한 엄격한 건축 기준과 에너지 효율이 뛰어나며 환경을 고려한 건물 건설에 대한 관심이 높아짐에 따라 최신 액상 도포형 방수 시스템의 도입이 촉진되고 있습니다. 리모델링 및 개조 프로젝트 역시 LAM 시장의 성장에 기여하는 요인 중 하나입니다.

“예측 기간 중 액체 도포형 방수막 시장에서 엘라스토머계 방수막이 가장 큰 점유율을 차지할 것으로 예상됩니다.”

엘라스토머 막은 주로 주택 및 상업용 건물의 방수 용도로의 사용이 확대됨에 따라 액상 도포형 방수 시트 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 이러한 성장은 해당 소재의 유연성, 뛰어난 균열 연결 능력, 높은 탄력성, 그리고 강력한 접착력에 힘입은 것으로, 이러한 특성들 덕분에 동적 건축 구조에 매우 적합하기 때문입니다. 또한 엘라스토머 막은 자외선, 습기, 온도 변화는 물론 지붕, 테라스, 지하실 및 기타 노출된 표면에서 흔히 볼 수 있는 그 밖의 가혹한 환경 요인에 대해서도 뛰어난 내성을 갖추고 있습니다. 이러한 특징 외에도, 엘라스토머 막은 이음매 없이 시공할 수 있고 내구성이 뛰어나며 구조물의 움직임에 대응할 수 있으므로 장기적으로는 성능 향상과 유지보수 부담 경감으로 이어집니다. 또한 시공이 용이하고 비용 대비 효과가 뛰어나며, 다양한 표면재와도 잘 어울립니다. 이러한 요인들은 신축 및 리모델링 프로젝트 모두에서 그 사용이 증가하고 있는 이유를 더욱 지원하고 있습니다.

“예측 기간 중 지붕 공사는 액체 도포형 방수막 시장에서 가장 큰 용도로 자리매김할 것으로 전망됩니다.”

지붕 공사는 주택 및 상업용 건축 분야에서 이 재료가 가장 유력한 선택지 중 하나이기 때문에 액상 도포형 필름 시장에서 가장 큰 용도 분야가 될 것으로 예상됩니다. 이 부문의 성장은 물의 침투, 자외선 및 기타 가혹한 기상 조건으로부터 장기간 보호해 주는 견고하고 누수 방지 성능이 뛰어나며 내후성이 뛰어난 지붕에 대한 수요가 증가함에 기인합니다. 액체 막은 복잡한 지붕 형태라도 시공이 간편하고, 균열을 효과적으로 덮어주는 능력이 뛰어나며, 이음매 없는 연속적인 방수층을 형성할 수 있다는 점에서 지붕 공사에서 널리 사용되는 대표적인 솔루션으로 자리 잡았습니다. 또한 건설 활동의 활성화, 에너지 절약 및 환경 친화형 건축물의 보급 확대, 그리고 유지보수 부담이 적은 지붕 시스템에 대한 수요가 증가하고 있는 점도 시장 성장을 지원하고 있습니다. 뛰어난 비용 대비 효과, 다양한 기질에 대한 강력한 접착력, 그리고 신축 및 리모델링 프로젝트 모두에 대한 적응성 덕분에, 지붕 공사는 앞으로도 액상 도포형 필름 업계에서 가장 큰 용도 분야로 자리매김할 것으로 확실시되고 있습니다.

“예측 기간 중 상업용 건축물은 액상 도포형 방수막 시장에서 두 번째로 큰 규모를 차지하는 최종 사용 산업이 될 것으로 전망됩니다.”

상업용 건축물은 사무실, 쇼핑몰, 병원, 학교 및 기타 비주거용 건축물에서 신뢰할 수 있는 방수 솔루션에 대한 강력한 수요에 힘입어, 액상 도포형 방수막 시장에서 두 번째로 큰 점유율을 차지하고 있습니다. 상업 인프라 개발에 더해, 개보수 및 리모델링 활동이 급증함에 따라 건물의 수명과 내구성을 연장하기 위한 LAM 시스템의 도입이 촉진되고 있습니다. 에너지 효율, 친환경 주택, 그리고 물의 침투 및 환경적 스트레스로부터의 보호에 대한 관심이 높아지고 있는 것이 시장 성장의 주요 촉진요인으로 작용하고 있습니다. 또한 이러한 막은 이음매 없이 시공할 수 있고 밀착성이 뛰어나며, 장기간 사용해도 높은 내구성을 유지하므로 대규모 상업 건축 프로젝트에 가장 적합합니다.

“예측 기간 중 유럽은 액상 도포형 필름 시장에서 2위의 규모를 차지할 것으로 전망됩니다.”

유럽은 강력한 성장 모멘텀, 건물 개보수에 대한 높은 수요, 엄격한 에너지 효율 기준, 그리고 친환경 건설 기법의 도입에 힘입어, 액상 도포형 방수막 시장에서 아시아태평양에 이어 2위를 차지할 것으로 예상됩니다. 유럽은 이산화탄소 배출량 감축과 기온 상승에 대한 대책 마련에 주력하고 있으며, 이는 주택, 상업 시설, 인프라 등 각 분야에서 최첨단 방수 솔루션의 활용을 촉진하게 될 것입니다. 내구성이 뛰어나고 수명이 긴 건축자재에 대한 관심이 높아지고 있는 점도 유럽 주요 국가 전반의 시장 성장을 더욱 지원할 것입니다.

대상 기업: Sika AG(스위스), MAPEI S.p.A.(이탈리아), SOPREMA(프랑스), Saint-Gobain(프랑스), H.B. Fuller(미국), Wacker Chemie AG(독일), Johns Manville(미국), Bostik(프랑스), GCP Applied Technologies Inc(미국) 및 Ardex(독일)가 이 보고서의 대상입니다.

본 조사에서는 액체 도포형 방수막 시장의 주요 기업에 대해 기업 개요, 최근 동향 및 주요 시장 전략을 포함한 상세한 경쟁 분석을 수행하고 있습니다.

조사 범위

본 조사 보고서에서는 액상 도포형 방수막 시장을 유형(아스팔트계 방수막, 엘라스토머계 방수막, 시멘트계 방수막), 용도(지붕, 벽, 건축 구조물, 도로), 사용 목적(신축, 개보수), 그리고 최종 용도 산업(주택 건설, 상업용 건설, 공공 인프라)별로 분류하고 있습니다. 이 보고서의 범위에는 액상 도포형 필름 시장의 성장에 영향을 미치는 촉진요인, 제약 요인, 과제 및 성장 기회에 관한 상세한 정보가 포함되어 있습니다. 주요 업계 참여 기업에 대한 상세한 분석을 통해 각 기업의 사업 개요, 제품 포트폴리오, 그리고 액상 도포형 필름 시장과 관련된 인수합병, 신제품 출시, 사업 확장 등의 주요 전략에 대한 인사이트를 제공합니다. 또한 이 보고서에서는 액상 도포형 필름 시장의 생태계에서 두각을 보이고 있는 신생 기업에 대한 경쟁 분석도 다루고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 시장을 선도하는 기업 및 신규 진입 기업을 대상으로, 액체 도포형 필름 시장 전체 및 그 하위 부문의 매출에 대한 가장 정확한 추정치를 제공합니다. 이를 통해 이해관계자들은 경쟁 구도를 파악하고, 자사의 비즈니스를 보다 효과적으로 포지셔닝하기 위한 심층적인 인사이트를 얻어, 적절한 시장 진입 전략을 수립할 수 있게 됩니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움이 되며, 주요 시장 촉진요인 및 과제에 관한 정보를 제공합니다.

이 보고서에서는 다음 사항에 대한 인사이트를 제공합니다. :

- 주요 촉진요인(인프라 및 상업 건축 활동의 증가, 그리고 구조적 안전성과 방습 기준을 지원하는 엄격한 건축 규제) 및 제약 요인(기존 방수 시스템에 비해 높은 시공·자재 비용, 적절한 시공과 안정적인 성능을 확보하기 위한 숙련된 인력의 필요성)에 대한 분석, 기회(신흥 경제국에서의 스마트 시티 및 인프라 확대, 그리고 에너지 절약형 건축물 및 그린 루프에서 친환경 방수막에 대한 수요 증가), 그리고 과제(시트 막 등 대체 방수 시스템과의 치열한 경쟁, 극한 기상 조건 및 복잡한 현장 조건 하에서의 성능 편차)에 대한 분석.

- 제품 개발/혁신: 액체 도포형 방수막 시장의 향후 기술, 연구개발 활동 및 제품·서비스 출시에 관한 상세 인사이트

- 시장 개발: 수익성이 높은 시장에 대한 포괄적인 정보 - 이 보고서에서는 다양한 지역의 액상 도포형 방수막 시장을 분석하고 있습니다.

- 시장의 다각화: 액상 도포형 방수막 시장의 신제품·서비스, 미개발 지역, 최근 동향 및 투자에 관한 포괄적인 정보

- 경쟁사 분석: Sika AG(스위스), MAPEI S.p.A.(이탈리아), SOPREMA(프랑스), Saint-Gobain(프랑스), H.B. Fuller(미국), Wacker Chemie AG(독일), Johns Manville(미국), Bostik(프랑스), GCP Applied Technologies Inc(미국), Ardex(독일) 등 주요 기업의 시장 점유율, 성장 전략, 서비스 제공에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 그리고 혁신

제7장 규제 상황과 지속가능성 구상

제8장 고객 상황과 구매 행동

제9장 액체 도포형 방수막 시장(용도별)

제10장 액상 도포 형막 시장(최종 용도 산업별)

제11장 액상 도포 형막 시장(유형별)

제12장 액상 도포 형막 시장(사용법별)

제13장 액상 도포 형막 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

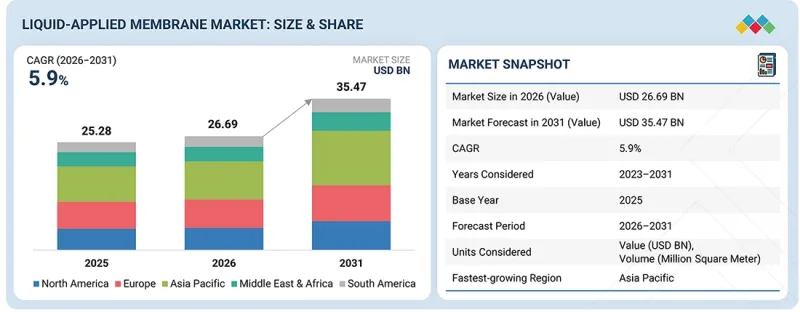

KSAThe liquid-applied membrane market is expected to reach USD 35.47 billion by 2031 from USD 26.69 billion in 2026, at a CAGR of 5.9% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million/Billion), Volume (Million Square Meters) |

| Segments | Type, Application, Usage, End-use Industry, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

The global market for liquid-applied membranes is gradually expanding due to the growing need for efficient, seamless waterproofing solutions. The main drivers of market growth are urbanization and infrastructure development across sectors, including residential, commercial, and industrial. In addition, strict building codes and a growing focus on constructing energy-efficient, environmentally friendly buildings are driving the installation of modern liquid-applied waterproofing systems. Renovation and refurbishment projects are other factors that help the LAM market grow.

"Elastomeric membrane is expected to be the largest membrane type in the liquid-applied membrane market during the forecast period."

Elastomeric membranes are expected to hold the largest share of the liquid-applied membrane market, primarily due to their growing use in waterproofing applications for residential and commercial buildings. This growth is driven by the material's flexibility, excellent crack-bridging capability, high elasticity, and strong adhesion, which make it well suited for dynamic building structures. Elastomeric membranes are also highly resistant to UV radiation, moisture, temperature fluctuations, and other harsh environmental factors common on roofs, terraces, basements, and other exposed surfaces. In addition to these qualities, elastomeric membranes offer seamless application, durability, and the ability to accommodate structural movements, which ultimately lead to enhanced performance and less maintenance over the long term. They are also easy to install, cost-effective, and compatible with many surfaces. These factors further explain their increasing use in both new construction and renovation projects.

"Roofing is expected to be the largest application in the liquid-applied membrane market during the forecast period."

Roofing is expected to be the largest application in the liquid-applied membrane market, as the material is among the top choices for residential and commercial construction. The main reason behind the growth of this segment is the increasing demand for robust, leak-resistant, weatherproof roofs that provide long-term protection against water infiltration, UV rays, and other harsh weather conditions. Liquid membranes are the go-to solution for roofing due to their simple application, even on complex roof shapes, their remarkable ability to cover cracks, and their capability to create a continuous, joint-free waterproof layer. In addition, rising construction activity, increased use of energy-efficient and green buildings, and the requirement for low-maintenance roofing systems are driving market growth. Their cost-effectiveness, strong bond with various substrates, and suitability for both new and renovation projects also ensure that roofing remains the top application segment of the liquid-applied membrane industry.

"Commercial construction is projected to be the second largest end-use industry in the liquid-applied membrane market during the forecast period."

Commercial construction accounts for the second-largest share of the liquid-applied membrane market, driven by strong demand for reliable waterproofing solutions in offices, shopping malls, hospitals, schools, and other non-residential buildings. The development of commercial infrastructure, along with a surge in renovation and refurbishment activities, is encouraging the use of LAM systems to extend the life and durability of buildings. Increasingly, the emphasis on energy efficiency, environmentally friendly housing, and protection against water penetration and environmental stresses is a key driver of market growth. In addition, these membranes can be applied seamlessly, adhere well, and remain highly durable over long-term use, making them ideal for large-scale commercial construction projects.

"Europe is projected to be the second largest region in the liquid-applied membrane market during the forecast period."

Europe is expected to be the second-largest market after Asia Pacific in the liquid-applied membrane market, driven by strong growth momentum, high demand for building renovations, stringent energy-efficiency norms, and the adoption of environmentally friendly construction practices. Europe is committed to reducing carbon emissions and increasing ambient temperatures, which will benefit the use of highly advanced waterproofing solutions across residential, commercial, and infrastructure applications. A growing focus on durable, long-life building materials will further enhance market growth across all major European nations.

By Company Type: Tier 1: 40%, Tier 2: 30%, and Tier 3: 30%

By Designation: Directors: 30%, Managers: 20%, and Others: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Others include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: Sika AG (Switzerland), MAPEI S.p.A. (Italy), SOPREMA (France), Saint-Gobain (France), H.B. Fuller (US), Wacker Chemie AG (Germany), Johns Manville (US), Bostik (France), GCP Applied Technologies Inc (US), and Ardex (Germany) are covered in the report.

The study includes an in-depth competitive analysis of these key players in the liquid-applied membrane market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the liquid-applied membrane market by type (bituminous membrane, elastomeric membrane, cementitious membrane), application (roofing, walls, building structures, roadways), usage (new construction, refurbishment), and end-use industry (residential construction, commercial construction, public infrastructure). The report's scope includes detailed information on drivers, restraints, challenges, and opportunities that influence the growth of the liquid-applied membrane market. A detailed analysis of key industry players provides insights into their business overviews, product portfolios, and key strategies, such as mergers, acquisitions, product launches, and expansions, associated with the liquid-applied membrane market. This report also covers a competitive analysis of upcoming startups in the liquid-applied membrane market ecosystem.

Reasons to Buy the Report

The report will provide market leaders and new entrants with the closest approximations of revenue figures for the overall liquid-applied membrane market and its subsegments. It will help stakeholders understand the competitive landscape, gain deeper insights into positioning their businesses more effectively, and plan suitable go-to-market strategies. The report will also help stakeholders gauge the pulse of the market and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (rising infrastructure and commercial construction activities and stringent building regulations supporting structural safety and moisture protection standards), restraints (high installation and material costs compared to conventional waterproofing systems and requirement of skilled labor for proper installation and consistent performance), opportunities (expansion of smart cities and infrastructure in emerging economies and rising demand for eco-friendly membranes in energy-efficient buildings and green roofs), and challenges (strong competition from alternative waterproofing systems like sheet membranes and performance variability under extreme weather and complex site conditions).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the liquid-applied membrane market

- Market Development: Comprehensive information about profitable markets - the report analyzes the liquid-applied membrane market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the liquid-applied membrane market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and service offerings of leading players such as Sika AG (Switzerland), MAPEI S.p.A. (Italy), SOPREMA (France), Saint-Gobain (France), H.B. Fuller (US), Wacker Chemie AG (Germany), Johns Manville (US), Bostik (France), GCP Applied Technologies Inc (US), and Ardex (Germany), among others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 UNITS CONSIDERED

- 1.3.4.1 Currency/Value unit

- 1.3.4.2 Volume unit

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING LIQUID-APPLIED MEMBRANE MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR LIQUID-APPLIED MEMBRANE MARKET PLAYERS

- 3.2 LIQUID-APPLIED MEMBRANE MARKET, BY TYPE

- 3.3 LIQUID-APPLIED MEMBRANE MARKET, BY APPLICATION

- 3.4 LIQUID-APPLIED MEMBRANE MARKET, BY USAGE

- 3.5 LIQUID-APPLIED MEMBRANE MARKET, BY END-USE INDUSTRY

- 3.6 LIQUID-APPLIED MEMBRANE MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising infrastructure and commercial construction activities

- 4.2.1.2 Increasing renovation and refurbishment activities

- 4.2.1.3 Stringent building regulations supporting structural safety and moisture protection standards

- 4.2.2 RESTRAINTS

- 4.2.2.1 High installation and material costs compared to conventional waterproofing

- 4.2.2.2 Requirement of skilled labor for proper installation and consistent performance

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of smart cities and infrastructure in emerging economies

- 4.2.3.2 Rising demand for eco-friendly membranes in energy-efficient buildings and green roofs

- 4.2.4 CHALLENGES

- 4.2.4.1 Strong competition from alternative waterproofing systems such as sheet membranes

- 4.2.4.2 Performance variability under extreme weather and complex site conditions

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN LIQUID-APPLIED MEMBRANE MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 GLOBAL GDP TRENDS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5.2 AVERAGE SELLING PRICE TREND, BY TYPE

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 391990)

- 5.6.2 EXPORT SCENARIO (HS CODE 391990)

- 5.7 KEY CONFERENCES AND EVENTS

- 5.8 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 LIQUID-APPLIED MEMBRANE IN BASEMENT WATERPROOFING

- 5.10.2 LIQUID-APPLIED MEMBRANE IN TUNNEL WATERPROOFING

- 5.11 IMPACT OF 2025 US TARIFF - LIQUID-APPLIED MEMBRANE MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON REGIONS

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 DEVELOPMENT OF ADVANCED POLYMERIC LIQUID-APPLIED MEMBRANE SYSTEMS

- 6.1.2 SMART FUNCTIONAL AND SELF-RESPONSIVE MEMBRANE MATERIALS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 RAPID CURING & HIGH-EFFICIENCY APPLICATION TECHNOLOGIES

- 6.2.2 REINFORCED AND MULTI-LAYER MEMBRANE SYSTEMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 HYBRID SURFACE PROTECTION AND COATING SYSTEMS

- 6.3.2 DIGITAL APPLICATION, MONITORING, AND SMART CONSTRUCTION TECHNOLOGIES

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2026-2027)

- 6.4.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.4.3 LONG-TERM (2030-2035+)

- 6.5 PATENT ANALYSIS

- 6.5.1 LEGAL STATUS OF PATENTS

- 6.5.2 JURISDICTION ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-DRIVEN DEFECT DETECTION & SURFACE EVALUATION SYSTEMS

- 6.6.2 AUTOMATED APPLICATION & SPRAY-CONTROL TECHNOLOGIES

- 6.6.3 SENSOR-BASED STRUCTURAL HEALTH MONITORING SYSTEMS

- 6.6.4 SMART CONSTRUCTION & DIGITAL INTEGRATION PLATFORMS

- 6.6.5 ADVANCED SELF-HEALING & ADAPTIVE MEMBRANE TECHNOLOGIES

- 6.7 IMPACT OF AI/GEN AI ON LIQUID-APPLIED MEMBRANE MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN LIQUID-APPLIED MEMBRANE MARKET

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN LIQUID-APPLIED MEMBRANE MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN LIQUID-APPLIED MEMBRANE MARKET

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 REGULATORY POLICY INITIATIVES

- 7.2.1 SAFETY PROTOCOLS

- 7.2.2 SUSTAINABLE DEVELOPMENT

- 7.2.3 STANDARDIZATION

- 7.2.4 CIRCULAR ECONOMY

- 7.3 SUSTAINABILITY INITIATIVES

- 7.3.1 MATERIAL PERFORMANCE, ENVIRONMENT, AND SAFETY INITIATIVES

- 7.3.1.1 Low-carbon materials and sustainable product strategies

- 7.3.1.2 Green buildings & eco applications

- 7.3.1 MATERIAL PERFORMANCE, ENVIRONMENT, AND SAFETY INITIATIVES

- 7.4 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

- 7.5 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY END-USE INDUSTRIES

9 LIQUID-APPLIED MEMBRANE MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 ROOFING

- 9.2.1 RISING DEMAND FOR GREEN ROOF SYSTEMS TO DRIVE MARKET

- 9.3 WALLS

- 9.3.1 HIGH EXPOSURE TO MOISTURE, TEMPERATURE FLUCTUATIONS, UV RADIATION, AND AIR POLLUTANTS TO DRIVE DEMAND

- 9.4 BUILDING STRUCTURES

- 9.4.1 STRUCTURAL CRACKING AND BIOLOGICAL DEGRADATION TO FUEL DEMAND FOR POLYURETHANE AND BITUMINOUS MEMBRANES

- 9.5 ROADWAYS

- 9.5.1 RISING INFRASTRUCTURE PROJECTS TO FUEL MARKET

- 9.6 OTHER APPLICATIONS

10 LIQUID-APPLIED MEMBRANE MARKET, BY END-USE INDUSTRY

- 10.1 INTRODUCTION

- 10.2 RESIDENTIAL CONSTRUCTION

- 10.2.1 STRONG GROWTH IN RESIDENTIAL SECTOR TO FUEL DEMAND

- 10.3 COMMERCIAL CONSTRUCTION

- 10.3.1 INCREASING DEMAND FOR COMMERCIAL INFRASTRUCTURE TO BOOST MARKET

- 10.4 PUBLIC INFRASTRUCTURE

- 10.4.1 RAPID URBANIZATION AND INDUSTRIALIZATION TO DRIVE MARKET

11 LIQUID-APPLIED MEMBRANE MARKET, BY TYPE

- 11.1 INTRODUCTION

- 11.2 ELASTOMERIC MEMBRANES

- 11.2.1 NEED FOR ROBUST PERFORMANCE IN SENSITIVE ENVIRONMENTS TO DRIVE MARKET

- 11.2.2 ACRYLIC MEMBRANES

- 11.2.3 POLYURETHANE WATERPROOFING MEMBRANES

- 11.2.4 PMMA MEMBRANES

- 11.3 BITUMINOUS MEMBRANES

- 11.3.1 RESISTANCE TO UV AND TEMPERATURE FLUCTUATIONS TO DRIVE DEMAND

- 11.3.2 SOLVENT-BASED

- 11.3.3 WATER-BASED

- 11.4 CEMENTITIOUS MEMBRANES

- 11.4.1 WIDE APPLICATIONS IN ROOFS AND TUNNELS TO DRIVE MARKET

- 11.4.2 ONE-COMPONENT (1K)

- 11.4.3 TWO-COMPONENT (2K)

12 LIQUID-APPLIED MEMBRANE MARKET, BY USAGE

- 12.1 INTRODUCTION

- 12.2 NEW CONSTRUCTION

- 12.2.1 STRONG GROWTH IN NEW CONSTRUCTION ACTIVITIES TO DRIVE MARKET

- 12.3 REFURBISHMENT

- 12.3.1 RISE IN INFRASTRUCTURAL DEVELOPMENTS TO BOOST MARKET

13 LIQUID-APPLIED MEMBRANE MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Strong building & construction industry to drive market

- 13.2.2 CANADA

- 13.2.2.1 Increase in demand due to government measures to drive market

- 13.2.3 MEXICO

- 13.2.3.1 Increased public and private investments in infrastructure projects to drive market

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Steady economic growth and rapid urbanization to boost market

- 13.3.2 FRANCE

- 13.3.2.1 Investments in public infrastructure and digitalization to boost market

- 13.3.3 SPAIN

- 13.3.3.1 Growth of construction industry to propel market

- 13.3.4 UK

- 13.3.4.1 Various government activities to drive market

- 13.3.5 ITALY

- 13.3.5.1 Rise in renovation and refurbishment projects to boost market

- 13.3.6 RUSSIA

- 13.3.6.1 Increase in residential construction activities to fuel market

- 13.3.7 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Surge in transportation projects to drive market

- 13.4.2 INDIA

- 13.4.2.1 Government initiatives and increased infrastructure spending to drive market

- 13.4.3 JAPAN

- 13.4.3.1 Surge in redevelopment activities to boost market

- 13.4.4 SOUTH KOREA

- 13.4.4.1 Strong construction industry to fuel market

- 13.4.5 AUSTRALIA

- 13.4.5.1 Rising need for durable waterproofing solutions to boost market

- 13.4.6 THAILAND

- 13.4.6.1 Growth of real estate and tourism industries to drive market

- 13.4.7 INDONESIA

- 13.4.7.1 Rapid urbanization and population growth to drive market

- 13.4.8 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.5.1.1 Saudi Arabia

- 13.5.1.1.1 Development of Jeddah Economic City to drive market

- 13.5.1.2 UAE

- 13.5.1.2.1 Growing emphasis on eco-friendly construction solutions to boost market

- 13.5.1.3 Rest of GCC

- 13.5.1.1 Saudi Arabia

- 13.5.2 SOUTH AFRICA

- 13.5.2.1 Growing investment in construction sector to boost market

- 13.5.3 REST OF MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.6 SOUTH AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 Upcoming international sports events to boost market

- 13.6.2 ARGENTINA

- 13.6.2.1 Growth of construction industry to drive market

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS, 2021-2025

- 14.4 MARKET SHARE ANALYSIS, 2024

- 14.5 PRODUCT COMPARISON

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.6.5.1 Company footprint

- 14.6.5.2 Region footprint

- 14.6.5.3 Type footprint

- 14.6.5.4 Application footprint

- 14.6.5.5 Usage footprint

- 14.6.5.6 End-use industry footprint

- 14.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- 14.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.7.5.1 Detailed list of key startups/SMEs

- 14.7.5.2 Competitive benchmarking of key startups/SMEs

- 14.8 COMPANY VALUATION & FINANCIAL METRICS

- 14.8.1 FINANCIAL METRICS

- 14.8.2 COMPANY VALUATION

- 14.8.3 ENTERPRISE VALUATION

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 SIKA AG

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.3.2 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 MAPEI S.P.A.

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.3.2 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 SOPREMA

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 SAINT-GOBAIN

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 H.B. FULLER

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 WACKER CHEMIE AG

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Expansions

- 15.1.6.4 MnM view

- 15.1.7 JOHNS MANVILLE

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.4 MnM view

- 15.1.8 BOSTIK

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 MnM view

- 15.1.9 GCP APPLIED TECHNOLOGIES INC.

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 MnM view

- 15.1.10 ARDEX GROUP

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.4 MnM view

- 15.1.1 SIKA AG

- 15.2 OTHER PLAYERS

- 15.2.1 RENOLIT SE

- 15.2.2 PAUL BAUDER GMBH CO. KG

- 15.2.3 GAF, INC.

- 15.2.4 CARLISLE COMPANIES INC.

- 15.2.5 PIDILITE INDUSTRIES LTD

- 15.2.6 TREMCO INCORPORATED

- 15.2.7 KEMPER SYSTEM

- 15.2.8 ALCHIMICA

- 15.2.9 AMES RESEARCH LABORATORIES, INC.

- 15.2.10 CHASE CORPORATION

- 15.2.11 CHEMBOND CHEMICALS LIMITED

- 15.2.12 CHEM LINK

- 15.2.13 CONCRETE SEALANTS, INC.

- 15.2.14 CROMMELIN WATERPROOFING & SEALING

- 15.2.15 ESKOLA LLC

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key industry insights

- 16.1.2.3 Breakdown of primary interviews

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.3 DATA TRIANGULATION

- 16.4 STUDY ASSUMPTIONS

- 16.5 RESEARCH LIMITATIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS