|

시장보고서

상품코드

2070221

배기 후처리 시스템 시장 : 제품 유형별(DOC, DPF, LNT, SCR, GPF), 차종별(승용차, 소형 상용차, 트럭, 버스), 연료 유형별(디젤, 가솔린), 판매 채널별(OEM, 애프터마켓), 지역별 - 세계 예측(-2033년)Exhaust Aftertreatment System Market by Product Type (DOC, DPF, LNT, SCR, GPF), Vehicle Type (Passenger Cars, LCVs, Trucks, Buses), Fuel Type (Diesel, Gasoline), Sales Channel (OEM, Aftermarket), and Region - Global Forecast to 2033 |

||||||

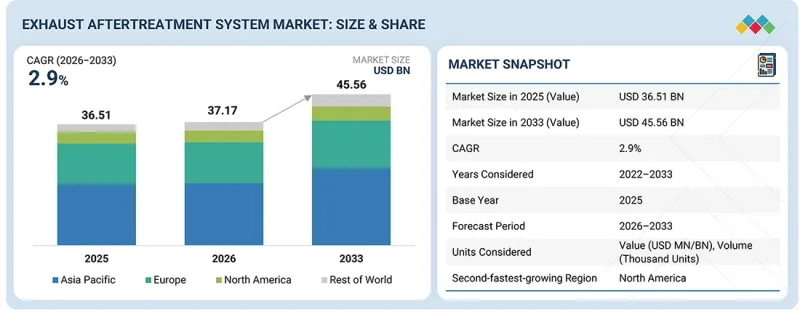

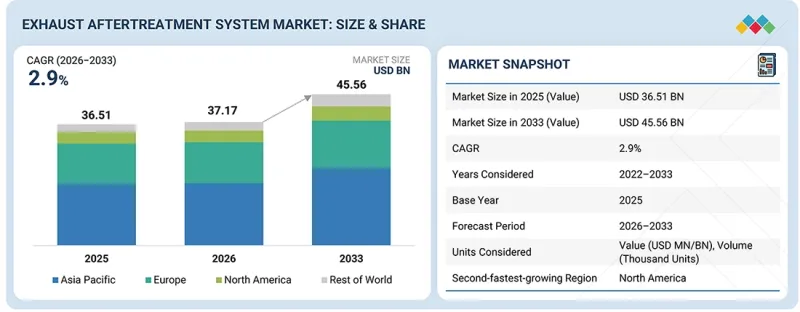

배기 후처리 시스템 시장 규모는 2026년에는 371억 7,000만 달러, 2033년에는 455억 6,000만 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR 2.9%를 기록할 것으로 전망됩니다.

각 OEM 업체들은 차량 성능 향상을 위해 소형 다단식 후처리 아키텍처, 첨단 촉매 소재, 지능형 요소수 분사 시스템, 센서가 통합된 배기가스 제어 시스템을 도입하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2033년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2033년 |

| 단위 | 달러 |

| 부문 | 제품 유형, 차종, 연료 유형, 판매 채널, 지역별 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 기타 지역 |

화물 운송량 증가, 차량의 현대화, 대형 디젤 트럭의 이용 확대에 따라, 더 대용량의 촉매와 높은 NOx 전환 효율을 갖춘 SCR 및 DPF 시스템에 대한 수요가 더욱 가속화되고 있습니다. 전 세계적으로 배기가스 규제가 강화되는 가운데, 각 OEM 업체들이 규제 준수, 연비, 내구성, 엔진 성능 간의 균형을 맞추기 위해서는 첨단 배기 후처리 기술이 필수적입니다.

“가솔린 미립자 필터 부문이 2026년부터 2033년까지 가장 빠르게 성장할 후처리 장치가 될 전망”

가솔린 미립자 필터(GPF) 부문은 승용차 및 소형 상용차에 가솔린 직접 분사(GDI) 엔진의 채택이 확대됨에 따라, 예측 기간 동안 배기 후처리 시스템 시장에서 가장 빠른 성장세를 보일 것으로 예상됩니다. 특히 소형 SUV, 크로스오버 차량, 고급 승용차의 경우, 터보차저가 장착된 가솔린 차량의 보급이 확대됨에 따라 가솔린 미립자 필터(GPF)의 채택도 증가하고 있습니다. 각 자동차 제조사들은 엔진의 반응성과 연비를 저해하지 않으면서도, 냉시동 시 배기가스 제어, 촉매의 라이트오프 효율, 미세먼지 여과 성능을 향상시키기 위해 GPF 시스템과 삼원 촉매, 클로즈 커플링 배기 레이아웃을 결합하는 경향이 강해지고 있습니다. Forvia, Tenneco, Sango 등의 기업들은 차세대 가솔린 차량을 위해 여과 효율, 내열성, 패키징 유연성을 향상시키기 위해 저배압 기판 기술, 소형 필터 통합, 첨단 코팅 소재에 대한 투자를 추진하고 있습니다. 전 세계적으로 가솔린 직접분사 승용차의 생산이 계속 확대되는 가운데, 배기 후처리 기술 중에서도 GPF 시스템은 급속한 성장이 예상됩니다.

“애프터마켓 판매 채널 부문은 예측 기간 동안 주요 시장 점유율을 확보할 것으로 전망”

예측 기간 동안 애프터마켓 부문은 유럽, 아시아태평양, 북미의 디젤차 도입 대수가 막대함에 따라 상당한 시장 점유율을 차지할 것으로 전망됩니다. 유럽에서는 Euro IV, V, VI 규정에 따라 DPF 및 SCR 시스템을 탑재한 디젤 승용차 및 상용차에 대한 교체 수요가 증가하고 있습니다. 마찬가지로, 중국과 인도에서도 China VI 및 BS VI 규제에 따라 SCR 및 DPF 시스템이 대규모로 도입됨에 따라 교체 수요가 증가하고 있습니다. 북미는 EPA 배출 기준에 따라 운행되는 대배기량 대형 디젤 트럭의 보급률이 높기 때문에 여전히 중요한 애프터마켓으로 자리 잡고 있습니다. 화물 운송, 광업, 건설 분야의 차량 평균 사용 연한이 늘어나고 주행 거리가 증가함에 따라, DPF, SCR, DOC, 센서, DEF 관련 부품의 교체 주기가 빨라지고 있습니다. 또한, 유럽, 중국, 인도, 캘리포니아주에서 시행되는 중고차 배기가스 적합성 프로그램, 개조 규제, 정기 검사 요건, 차량 함대 현대화 노력의 강화로 인해, 인증된 애프터마켓용 후처리 시스템에 대한 수요가 증가하고 있습니다.

“유럽은 2026년에 배기 후처리 시스템 분야에서 2위 시장이 될 전망”

유럽은 첨단 배기가스 기술의 조기 도입은 물론, 엄격한 유로 6 규제와 향후 도입될 유로 7 규제로 인해 2026년에는 배기 후처리 시스템 시장에서 2위를 차지할 것으로 전망됩니다. 해당 지역에서는 메르세데스-벤츠, BMW, 폭스바겐 그룹, 스텔란티스, 르노 등의 OEM을 중심으로 프리미엄 승용차, 멀티밴, 소형 상용차, 버스, 대형 트럭 분야에서 디젤 후처리 시스템의 보급률이 높게 나타나고 있습니다. 유럽에서는 대형 상용차, 버스, 대형 밴 분야에서 디젤 파워트레인이 여전히 주류를 이루고 있으며, 저NOx 규제 및 실제 주행 배출 요건을 충족하기 위해 첨단 SCR, DPF, DOC, 암모니아 슬립 촉매 시스템이 요구되고 있습니다. 프리미엄 SUV, 고급 세단, 장거리 트럭, 다목적 밴에서도 높은 토크 요구 사항, 연비 효율, 장거리 운행 시의 이점 등으로 인해 디젤 엔진의 채택이 여전히 두드러집니다. 향후 유로 7 규제로 인해 콜드 스타트, 저온 주행, 브레이크 먼지, 실제 주행 시 배기가스에 대한 제한이 더욱 강화됨에 따라, 후처리 시스템의 복잡성이 더욱 커질 것으로 예상됩니다. 이에 따라 OEM을 통한 통합형 클로즈 커플링 배기 아키텍처, 듀얼 도징 SCR 시스템, 첨단 차량 진단 시스템, 열효율이 뛰어난 촉매 기술에 대한 투자가 가속화되고 있습니다. 또한, 유럽은 세계 최대 규모의 유로 VI 디젤차 보유 대수를 자랑하며, OEM 시장과 애프터마켓 시장 양쪽 모두에서 고부가가치 후처리 시스템에 대한 지속적인 수요를 창출하고 있습니다. 특히 장거리 화물 운송 및 상용차 차량단 분야에서 이러한 경향이 두드러집니다.

본 보고서에서는 전 세계 배기 후처리 시스템 시장을 조사하여, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규 환경, 사례 연구, 시장 규모 추정 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 현황, 주요 기업 개요 등을 정리하고 있습니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 OE 배기 후처리 시스템 시장 : 후처리 장비별

제10장 OE 배기 후처리 시스템 시장 : 차종별

제11장 OE 배기 후처리 시스템 시장 : 연료 유형별

제12장 애프터마켓 배기 후처리 시스템 시장 : 후처리 장비별

제13장 배기 후처리 시스템 시장 : 판매 채널별

제14장 배기 후처리 시스템 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSM 26.07.02The exhaust aftertreatment system market is projected to be valued at USD 37.17 billion in 2026 and USD 45.56 billion by 2033, exhibiting a CAGR of at 2.9% during the forecast period. OEMs are deploying compact multi-stage aftertreatment architectures, advanced catalyst materials, intelligent urea dosing systems, and sensor-integrated emission control systems to improve vehicle performance.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | USD Billion |

| Segments | by Product Type, Vehicle Type, Fuel Type, Sales Channel, and Region |

| Regions covered | Asia Pacific, Europe, North America and RoW |

Rising freight transportation activity, fleet modernization, and higher utilization of heavy-duty diesel trucks are further accelerating the demand for SCR and DPF systems with larger catalyst volumes and higher NOx conversion efficiency. As emission norms tighten globally, advanced exhaust aftertreatment technologies are becoming essential for OEMs to balance regulatory compliance, fuel economy, durability, and engine performance.

"Gasoline particulate filters segment to be the fastest-growing aftertreatment device from 2026 to 2033"

The gasoline particulate filters segment is expected to witness the fastest growth in the exhaust aftertreatment system market during the forecast period due to the adoption of gasoline direct injection (GDI) engines across passenger cars and light commercial vehicles. Gasoline particulate filter (GPF) adoption is increasing with the rising penetration of turbocharged gasoline vehicles, particularly in compact SUVs, crossover vehicles, and premium passenger cars. Automakers are increasingly combining GPF systems with three-way catalysts and close-coupled exhaust layouts to improve cold-start emission control, catalyst light-off efficiency, and particulate filtration without compromising engine responsiveness or fuel economy. Companies such as Forvia, Tenneco, and Sango are investing in low-backpressure substrate technologies, compact filter integration, and advanced coating materials to improve filtration efficiency, thermal durability, and packaging flexibility for next-generation gasoline vehicles. As gasoline direct injection passenger vehicle production continues expanding globally, GPF systems are expected to witness rapid growth among exhaust aftertreatment technologies.

"Aftermarket sales channel segment to capture a major market share during the forecast period"

The aftermarket segment accounts for a commendable market share during the forecast period due to the large installed base of diesel vehicles across Europe, Asia Pacific, and North America. Europe has a high replacement demand from diesel passenger cars and commercial vehicles equipped with DPF and SCR systems under Euro IV, V, and VI regulations. Similarly, China and India are witnessing rising replacement demand following large-scale adoption of SCR and DPF systems under China VI and BS VI norms. North America remains a key aftermarket market due to the high penetration of large-displacement heavy-duty diesel trucks operating under EPA emission standards. Rising average vehicle age and increasing miles driven in freight, mining, and construction applications are accelerating replacement cycles for DPF, SCR, DOC, sensors, and DEF-related components. Additionally, stricter in-use emission compliance programs, retrofit regulations, periodic inspection requirements, and fleet modernization initiatives across Europe, China, India, and California are increasing demand for certified aftermarket aftertreatment systems.

"Europe to be the second-largest market for exhaust aftertreatment systems in 2026"

Europe is expected to be the second-largest market for exhaust aftertreatment systems in 2026 due to its early adoption of advanced emission technologies and stringent Euro 6 and upcoming Euro 7 regulations. The region has a high penetration of diesel aftertreatment systems across premium passenger cars, multivans, LCVs, buses, and heavy-duty trucks, particularly from OEMs such as Mercedes-Benz, BMW, Volkswagen Group, Stellantis, and Renault. Diesel powertrains continue to dominate Europe's heavy commercial vehicle, bus, and large van segments, requiring advanced SCR, DPF, DOC, and ammonia slip catalyst systems for compliance with low NOX and real driving emission requirements. Premium SUVs, executive sedans, long-haul trucks, and multi-purpose vans still witness significant diesel adoption due to higher torque requirements, fuel efficiency, and long-distance operational advantages. Upcoming Euro 7 regulations are expected to further increase aftertreatment system complexity through stricter cold-start, low-temperature, brake dust, and real driving emission limits. This is accelerating OEM investments in integrated close-coupled exhaust architectures, dual-dosing SCR systems, advanced onboard diagnostics, and thermally efficient catalyst technologies. Additionally, Europe maintains one of the world's largest installed bases of Euro VI diesel vehicles, creating sustained demand for high-value aftertreatment systems across both OEM and replacement markets, particularly in long-haul freight transportation and commercial fleet applications.

The breakup of the profile of primary participants in the exhaust aftertreatment system market:

- By Company Type: Exhaust Aftertreatment System Manufacturers - 70% and Automotive OEMs - 30%

- By Designation: C-Level Executives - 60%, Director Level - 10%, and Others - 30%

- By Region: North America - 20%, Europe - 15%, Asia Pacific - 40%, and RoW - 25%

Tenneco Inc. (US), Forvia (France), Eberspacher (Germany), Friedrich Boysen GmbH & Co KG (Germany), and Futaba Industrial Co.Ltd. (Japan) are the leading providers of exhaust system aftertreatment in the global market.

Research Coverage:

This research report categorizes the exhaust aftertreatment system market size based on aftertreatment device, vehicle type, fuel type, sales channel, and region. The report comprehensively discusses key factors impacting the growth of the exhaust aftertreatment system market, including drivers, constraints, challenges, and opportunities. It provides detailed analyses of major industry players, offering insights into their business profiles, solutions, services, key strategies, contracts, partnerships, agreements, new product and service launches, mergers and acquisitions, recession impacts, and recent developments. Additionally, the report includes a competitive analysis of emerging startups within the exhaust aftertreatment system market ecosystem.

Reasons to buy this report:

This report offers comprehensive analyses of market share and supply chains and detailed information on component manufacturers. It is designed to aid market leaders and new entrants by providing precise revenue estimates for the overall exhaust aftertreatment system market. Additionally, the report helps stakeholders understand the market dynamics, highlighting key drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Rising GPF deployment in gasoline direct injection vehicles for particulate reduction, Increasing adoption of integrated SCR, DPF, and DOC systems in diesel trucks and buses), restraints (Reduction in long-term demand for aftertreatment systems amid rising EV popularity), opportunities (Mounting demand for GPF in GDI engines, Rising replacement demand for aftertreatment systems in aging commercial vehicles), and challenges (Fluctuating precious metal prices, Limited vehicle packaging space complicating multi device integration) fueling the demand of the exhaust systems

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the exhaust aftertreatment system market, such as the use of various kinds of metals in exhaust systems, including titanium, stainless steel, etc.

- Market Development: Comprehensive information about lucrative markets-the report analyses the exhaust aftertreatment system market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the exhaust aftertreatment system market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the exhaust aftertreatment system market, such as Tenneco Inc.(US), Forvia (France), Eberspacher (Germany), Friedrich Boysen GmbH & Co KG (Germany), and Futaba Industrial Co.Ltd. (Japan)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SNAPSHOT

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN EXHAUST AFTERTREATMENT SYSTEM MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN EXHAUST AFTERTREATMENT SYSTEM MARKET

- 3.2 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE

- 3.3 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY VEHICLE TYPE

- 3.4 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY FUEL TYPE

- 3.5 EXHAUST AFTERTREATMENT SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE

- 3.6 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising demand for heavy commercial vehicles

- 4.2.1.2 Growing demand for gasoline particulate filters (GPFs) in gasoline direct injection (GDI) engines

- 4.2.2 RESTRAINTS

- 4.2.2.1 Declining production of diesel passenger vehicles

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing demand for integrated multi-functional aftertreatment modules

- 4.2.4 CHALLENGES

- 4.2.4.1 Balancing diesel particulate filter (DPF) regeneration requirements with fuel-efficiency targets

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES IN EXHAUST AFTERTREATMENT SYSTEM MARKET

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 SUPPLIERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 GDP TRENDS AND FORECAST

- 5.1.2 TRENDS IN GLOBAL AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.2 ECOSYSTEM ANALYSIS

- 5.2.1 EXHAUST AFTERTREATMENT SYSTEM MANUFACTURERS

- 5.2.2 CATALYST AND SUBSTRATE SUPPLIERS

- 5.2.3 FILTER AND SCR COMPONENT PROVIDERS

- 5.2.4 EMISSION CONTROL TECHNOLOGY PROVIDERS

- 5.2.5 AUTOMOTIVE OEMS

- 5.2.6 AFTERMARKET AND DISTRIBUTION PLAYERS

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 PRICING ANALYSIS

- 5.4.1 ASIA PACIFIC: AFTERTREATMENT DEVICE AVERAGE SELLING PRICE, BY VEHICLE TYPE, 2025

- 5.4.2 EUROPE: AFTERTREATMENT DEVICE AVERAGE SELLING PRICE, BY VEHICLE TYPE, 2025

- 5.4.3 NORTH AMERICA: AFTERTREATMENT DEVICE AVERAGE SELLING PRICE, BY VEHICLE TYPE, 2025

- 5.5 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 842132)

- 5.7.2 EXPORT SCENARIO (HS CODE 842132)

- 5.8 CASE STUDY ANALYSIS

- 5.8.1 FORVIA IMPROVED LOW TEMPERATURE NOX REDUCTION FOR FUTURE EMISSION COMPLIANCE

- 5.8.2 TENNECO ADVANCED INTEGRATED AFTERTREATMENT FOR HEAVY-DUTY EMISSIONS CONTROL

- 5.8.3 CORNING ENHANCED PARTICULATE FILTRATION THROUGH ADVANCED CERAMIC SUBSTRATES

- 5.8.4 BOSCH STRENGTHENED REAL-TIME EMISSION CONTROL THROUGH ADVANCED SENSOR TECHNOLOGY

- 5.8.5 UMICORE IMPROVED CATALYST EFFICIENCY WHILE REDUCING PRECIOUS METAL DEPENDENCE

- 5.9 IMPACT OF EU-INDIA FTA ON AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.9.1 IMPACT ON EXHAUST AFTERTREATMENT SYSTEM MARKET

- 5.10 IMPACT OF ISRAEL-IRAN CONFLICT ON AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.10.1 IMPACT ON EXHAUST AFTERTREATMENT SYSTEM MARKET

- 5.10.2 SUPPLY CHAIN DISRUPTIONS

- 5.10.2.1 Global shipping and trade route disruptions

- 5.10.2.2 Manufacturing cost inflation

- 5.10.2.3 Supply risks for critical aftertreatment components

- 5.10.3 REGIONAL/COUNTRY-LEVEL IMPACT

- 5.10.3.1 Europe

- 5.10.3.2 India

- 5.10.3.3 Japan and South Korea

- 5.10.3.4 China

6 TECHNOLOGICAL ADVANCEMENTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 INTEGRATED SOFTWARE CONTROLLED EMISSIONS PLATFORMS

- 6.1.2 SCR ON FILTER (SCRF) TECHNOLOGY

- 6.1.3 ADVANCED AMMONIA DELIVERY AND UREA DOSING SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 CATALYST COATING AND WASHCOAT ENGINEERING

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 HYDROGEN INTERNAL COMBUSTION ENGINE PLATFORMS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM ROADMAP

- 6.4.2 MID-TERM ROADMAP

- 6.4.3 LONG-TERM ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 LIST OF PATENTS

- 6.6 FUTURE APPLICATIONS

- 6.7 OEM ANALYSIS

- 6.7.1 AFTERTREATMENT ARCHITECTURE BENCHMARKING

- 6.7.2 THERMAL MANAGEMENT & PACKAGING CAPABILITIES

- 6.7.3 SUBSTRATE & CATALYST TECHNOLOGY POSITIONING

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 OEM TECHNOLOGY ADOPTION & BENCHMARKING

- 7.2.1 EMISSION COMPLIANCE ROADMAP (EURO 7, BS7 READINESS)

- 7.2.2 PLATFORM-WISE EXHAUST INTEGRATION STRATEGIES

- 7.2.3 OEM TECHNOLOGY ADOPTION

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES

9 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE

- 9.1 INTRODUCTION

- 9.2 DIESEL OXIDATION CATALYST (DOC)

- 9.2.1 RISING PRODUCTION OF DIESEL-POWERED COMMERCIAL VEHICLES TO DRIVE MARKET

- 9.3 DIESEL PARTICULATE FILTER (DPF)

- 9.3.1 INTEGRATION OF HIGH-CAPACITY SOOT FILTRATION SYSTEMS IN HEAVY-DUTY DIESEL PLATFORMS TO DRIVE MARKET

- 9.4 LEAN NOX TRAP (LNT)

- 9.4.1 EXTENSIVE USE OF COMPACT DIESEL POWERTRAINS IN LIGHT COMMERCIAL VEHICLES TO DRIVE MARKET

- 9.5 SELECTIVE CATALYTIC REDUCTION (SCR)

- 9.5.1 GROWING PRODUCTION OF INDUSTRIAL VEHICLES TO DRIVE MARKET

- 9.6 GASOLINE PARTICULATE FILTER (GPF)

- 9.6.1 REGULATORY PUSH FOR GASOLINE VEHICLES TO REDUCE EMISSIONS TO DRIVE MARKET

- 9.7 INDUSTRY INSIGHTS

10 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY VEHICLE TYPE

- 10.1 INTRODUCTION

- 10.2 PASSENGER CAR

- 10.2.1 RISING PRODUCTION AND SALES VOLUME TO DRIVE MARKET

- 10.3 LIGHT COMMERCIAL VEHICLE (LCV)

- 10.3.1 CONTINUED EXPANSION OF URBAN DELIVERY FLEETS TO DRIVE MARKET

- 10.4 TRUCK

- 10.4.1 RAPID ADOPTION IN COMMERCIAL TRANSPORTATION TO DRIVE MARKET

- 10.5 BUS

- 10.5.1 INCREASING DEPLOYMENT OF INTERCITY AND PUBLIC TRANSIT FLEETS TO DRIVE MARKET

11 EXHAUST AFTERTREATMENT SYSTEM (OE) MARKET, BY FUEL TYPE

- 11.1 INTRODUCTION

- 11.2 DIESEL

- 11.2.1 HIGH AFTERTREATMENT CONTENT INTENSITY IN DIESEL POWERTRAINS TO DRIVE MARKET

- 11.3 GASOLINE

- 11.3.1 DOMINANCE OF GASOLINE-POWERED PASSENGER VEHICLE BASE AND SHIFT TOWARD ADVANCED ENGINE ARCHITECTURES TO DRIVE MARKET

- 11.4 INDUSTRY INSIGHTS

12 EXHAUST SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE

- 12.1 INTRODUCTION

- 12.2 DIESEL OXIDATION CATALYST (DOC)

- 12.2.1 AGING DIESEL VEHICLE PARC TO DRIVE AFTERMARKET

- 12.3 DIESEL PARTICULATE FILTER (DPF)

- 12.3.1 CLOGGING AND ASH BUILDUP TO DRIVE AFTERMARKET

- 12.4 SELECTIVE CATALYTIC REDUCTION (SCR)

- 12.4.1 HIGH DUTY CYCLE DIESEL OPERATIONS TO DRIVE AFTERMARKET

- 12.5 INDUSTRY INSIGHTS

13 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY SALES CHANNEL

- 13.1 INTRODUCTION

- 13.2 OE-FITTED

- 13.3 AFTERMARKET

14 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 ASIA PACIFIC

- 14.2.1 CHINA

- 14.2.1.1 Expansion of commercial vehicle and logistics fleets to drive market

- 14.2.2 INDIA

- 14.2.2.1 Growth in heavy-duty transportation and infrastructure activities to drive market

- 14.2.3 JAPAN

- 14.2.3.1 Export-oriented vehicle manufacturing to drive market

- 14.2.4 SOUTH KOREA

- 14.2.4.1 Increasing adoption of integrated emission control architectures to drive market

- 14.2.5 THAILAND

- 14.2.5.1 Expansion of pickup truck manufacturing to drive market

- 14.2.6 REST OF ASIA PACIFIC

- 14.2.1 CHINA

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Expansion of hybrid vehicle platforms to drive market

- 14.3.2 FRANCE

- 14.3.2.1 Growth of light commercial vehicle electrification transition phase to drive market

- 14.3.3 UK

- 14.3.3.1 Expansion of low-emission urban transport fleets to drive market

- 14.3.4 SPAIN

- 14.3.4.1 Growth of export-focused vehicle assembly operations to drive market

- 14.3.5 TURKEY

- 14.3.5.1 Growing demand for fuel-efficient vehicles to drive market

- 14.3.6 RUSSIA

- 14.3.6.1 Expansion of domestic vehicle platform localization to drive market

- 14.3.7 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 NORTH AMERICA

- 14.4.1 US

- 14.4.1.1 Fleet modernization and replacement cycle acceleration to drive market

- 14.4.2 MEXICO

- 14.4.2.1 Integration into North American supply chains to drive market

- 14.4.3 CANADA

- 14.4.3.1 Cold climate durability requirements to drive market

- 14.4.1 US

- 14.5 REST OF THE WORLD

- 14.5.1 BRAZIL

- 14.5.1.1 Multi-fuel vehicle ecosystem and gasoline particulate control adoption to drive market

- 14.5.2 ARGENTINA

- 14.5.2.1 Growth of regionally standardized vehicle imports to drive market

- 14.5.3 OTHERS

- 14.5.1 BRAZIL

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, JANUARY 2022-MAY 2026

- 15.3 MARKET SHARE ANALYSIS, 2025

- 15.4 REVENUE ANALYSIS, 2021-2025

- 15.5 COMPANY VALUATION AND FINANCIAL METRICS, 2026

- 15.6 BRAND/PRODUCT COMPARISON

- 15.7 COMPANY EVALUATION MATRIX: EXHAUST AFTERTREATMENT SYSTEM PROVIDERS, 2025

- 15.7.1 STARS

- 15.7.2 EMERGING LEADERS

- 15.7.3 PERVASIVE PLAYERS

- 15.7.4 PARTICIPANTS

- 15.7.5 COMPANY FOOTPRINT

- 15.7.5.1 Company footprint

- 15.7.5.2 Region footprint

- 15.7.5.3 Aftertreatment device footprint

- 15.7.5.4 Vehicle type footprint

- 15.8 COMPETITIVE SCENARIO

- 15.8.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 15.8.2 DEALS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 FORVIA

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Deals

- 16.1.1.3.2 Others

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 TENNECO INC.

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches/developments

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 EBERSPACHER

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches/developments

- 16.1.3.3.2 Deals

- 16.1.3.3.3 Expansions

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 FRIEDRICH BOYSEN GMBH & CO. KG

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 MnM view

- 16.1.4.3.1 Key strengths

- 16.1.4.3.2 Strategic choices

- 16.1.4.3.3 Weaknesses and competitive threats

- 16.1.5 FUTABA INDUSTRIAL CO., LTD.

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 MnM view

- 16.1.5.3.1 Key strengths

- 16.1.5.3.2 Strategic choices

- 16.1.5.3.3 Weaknesses and competitive threats

- 16.1.6 CUMMINS INC.

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product launches/developments

- 16.1.6.3.2 Deals

- 16.1.7 SANGO CO., LTD.

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.8 SEJONG INDUSTRIAL CO., LTD.

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.9 BOSAL

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.1 FORVIA

- 16.2 OTHER PLAYERS

- 16.2.1 MARELLI HOLDINGS CO., LTD.

- 16.2.2 BENTELER INTERNATIONAL AG

- 16.2.3 DINEX A/S

- 16.2.4 WALKER EXHAUST

- 16.2.5 TATA AUTOCOMP KATCON EXHAUST SYSTEMS

- 16.2.6 JOHNSON MATTHEY

- 16.2.7 BASF

- 16.2.8 UMICORE

- 16.2.9 CORNING

- 16.2.10 DENSO

- 16.2.11 BOSCH

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 List of key secondary sources

- 17.1.1.2 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 List of primary participants

- 17.1.3 SAMPLING TECHNIQUES AND DATA COLLECTION METHODS

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 TOP-DOWN APPROACH

- 17.3 DATA TRIANGULATION

- 17.4 RESEARCH LIMITATIONS

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RISK ASSESSMENT

18 APPENDIX

- 18.1 INSIGHTS FROM INDUSTRY EXPERTS

- 18.2 DISCUSSION GUIDE

- 18.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.4 CUSTOMIZATION OPTIONS

- 18.4.1 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY EMISSION STANDARD

- 18.4.1.1 EURO 6/7

- 18.4.1.2 CHINA 6/7

- 18.4.1.3 BHARAT STAGE VI

- 18.4.1.4 EPA 2027

- 18.4.2 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY SYSTEM ARCHITECTURE

- 18.4.2.1 Standalone aftertreatment systems

- 18.4.2.2 Integrated DOC + DPF + SCR systems

- 18.4.2.3 Close coupled aftertreatment systems

- 18.4.3 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY APPLICATION

- 18.4.3.1 On-highway vehicles

- 18.4.3.2 Off-highway equipment

- 18.4.4 TWO & THREE-WHEELER VEHICLE EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION

- 18.4.4.1 Asia Pacific

- 18.4.4.2 Europe

- 18.4.4.3 North America

- 18.4.4.4 Rest of the World

- 18.4.1 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY EMISSION STANDARD

- 18.5 RELATED REPORTS

- 18.6 AUTHOR DETAILS