|

시장보고서

상품코드

2070358

실내 위치 정보 시장 : 제공별, 기술별, 용도별, 업계별, 지역별 - 세계 예측(-2031년)Indoor Location Market by Solution (Asset & People Tracking, Indoor Location Analytics, Indoor Navigation, Database Management Systems), By Technology (BLE, UWB, Wi-Fi, RFID, Magnetic Positioning, Wirepas Mesh) - Global Forecast to 2031 |

||||||

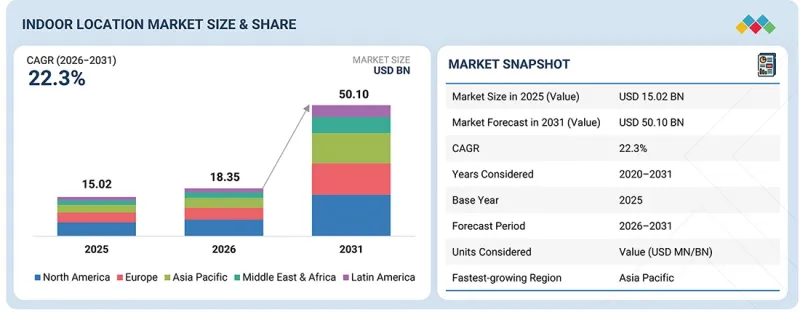

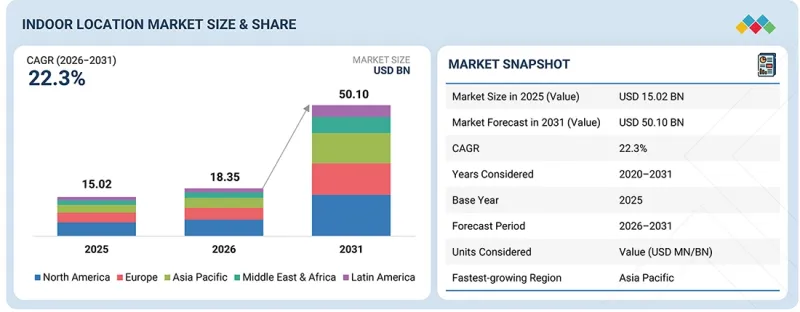

실내 위치 정보 시장 규모는 2026년에는 183억 5,000만 달러, 2031년까지 501억 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR은 22.3%를 기록할 전망입니다.

조직들이 건물 내 효율성, 안전성, 자동화 향상을 추구하는 가운데, 실내 위치 정보 기술은 전 세계적으로 큰 주목을 받고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(10억 달러) |

| 부문 | 제공별, 기술별, 용도별, 업계별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카 및 라틴아메리카 |

IoT 기기, 블루투스 저에너지(BLE), 초광대역(UWB), 무선 충실도(Wi-Fi)를 통한 위치 측정, 무선 주파수 식별(RFID), 그리고 AI를 활용한 분석 기술의 도입이 확대됨에 따라 자산, 인력, 업무 흐름을 실시간으로 정확하게 추적할 수 있게 되었습니다. 스마트 빌딩, 스마트 시티, 인더스트리 4.0 및 디지털 전환에 대한 투자 확대가 시장 성장을 더욱 가속화하고 있습니다. 이러한 솔루션은 업무 효율성 향상, 자원 활용 최적화, 고객 경험 개선, 보안 및 비상 대응 능력 강화, 그리고 데이터 기반 의사결정을 지원합니다. 이에 따라 실내 위치 측위는 전 세계 모든 산업 분야에서 지능적이고 연결성이 뛰어나며 생산성이 높은 실내 환경을 구현하기 위한 핵심 요소로 자리 잡고 있습니다.

“2026년부터 2031년까지 의료·제약 부문이 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 전망”

의료·제약 부문은 예측 기간 동안 실내 위치 정보 시장에서 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 예상됩니다. 이 부문의 성장은 병원 및 의료 시설 전반에 걸쳐 RTLS, 실내 위치 추적, 자산 추적 기술이 빠르게 도입된 데 기인합니다. 의료 서비스 제공자들은 의료기기, 환자, 직원을 실시간으로 추적하여 업무 효율성과 환자 안전을 향상시키기 위해 BLE, RFID, Wi-Fi, UWB 솔루션 도입을 점점 더 확대하고 있습니다. 영국의 NHS(국민보건서비스) 병원에서는 RTLS 도입으로 인해 중요한 의료기기의 위치를 파악하는 데 소요되는 시간이 대폭 단축되었다고 보고되고 있습니다. 스마트 병원, 디지털 의료 인프라, 워크플로우 자동화 및 직원 안전 대책 솔루션에 대한 막대한 투자가 도입을 더욱 가속화하고 있습니다. 그 효과로는 의료기기 분실 감소, 환자 동선 개선, 긴급 대응 신속화, 자원 활용 최적화, 그리고 의료 서비스의 질 향상을 들 수 있습니다.

“2026년에는 Wi-Fi 부문이 실내 위치 정보 시장에서 가장 큰 점유율을 차지할 것으로 전망”

Wi-Fi 부문은 기업, 병원, 공항, 소매점, 교육 기관 등에 이미 구축된 기존 무선 인프라를 활용할 수 있기 때문에 2026년에는 실내 위치 정보 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 조직은 대규모의 추가 하드웨어 투자 없이도 실내 위치 정보 시스템을 도입할 수 있으므로, 도입 비용과 복잡성을 줄일 수 있습니다. Wi-Fi 6 및 Wi-Fi 6E의 도입이 확대됨에 따라 위치 정보의 정확도, 네트워크 용량, 실시간 추적 기능이 향상되고 있습니다. 자산 추적, 인력 관리, 방문자 분석, 내비게이션 서비스에 대한 수요가 증가함에 따라, 이러한 서비스의 보급이 더욱 확대되고 있습니다. 그 효과로는 업무 효율 향상, 공간 활용 최적화, 고객 경험 향상, 데이터 기반 의사결정 강화 등을 들 수 있습니다. 지속적인 기업의 디지털화와 스마트 빌딩 추진이 여전히 주요 성장 요인으로 작용하고 있습니다.

“예측 기간 동안 아시아태평양이 가장 높은 성장률을 기록할 것으로 전망”

아시아태평양은 중국, 인도, 일본, 한국 및 동남아시아의 급속한 도시화, 대규모 스마트 시티 구상, 디지털 인프라 확충, 그리고 인더스트리 4.0 기술의 보급에 힘입어, 예측 기간 동안 실내 위치 정보 시장에서 가장 높은 성장률을 기록할 것으로 예상됩니다. 정부와 기업들은 스마트 공항, 병원, 공장, 물류 허브, 상업 빌딩에 대한 투자를 확대하고 있으며, 이로 인해 실내 내비게이션, 실시간 자산 추적, 위치 정보 분석 솔루션에 대한 수요가 크게 증가하고 있습니다. 5G, IoT, Wi-Fi, BLE, UWB 기술의 도입이 확대됨에 따라 실내 위치 파악의 정확도와 확장성이 향상되고 있습니다. 동시에, 업무 효율, 근로자 안전, 자동화, 공급망 가시성에 대한 요구가 높아짐에 따라 도입이 더욱 가속화되고 있습니다. 이러한 동향에 따라 다양한 산업 분야에서 생산성, 자원 활용도, 고객 경험의 향상이 기대되고 있습니다. 최근 동향으로는 2025년에 아세안(ASEAN) 전역의 스마트 병원, 제조 시설, 스마트 빌딩을 대상으로 한 UWB 기반 실내 추적 시스템에 관한 지역 이니셔티브가 출범할 예정이라는 점이 꼽히며, 이 지역에서 첨단 실내 위치 정보 솔루션에 대한 관심이 높아지고 있음을 여실히 보여주고 있습니다.

주요 응답자의 구성

실내 위치 정보 시장의 주요 기업으로는 Zebra Technologies(미국), Cisco(미국), HPE(미국), Esri(미국), Acuity Brands(미국), Inpixon(미국), HID Global(미국), CenTrak(미국), Sonitor(노르웨이), HERE Technologies(네덜란드), Ubisense(영국), Infsoft(독일), Polaris Wireless(미국), Quuppa(핀란드), Securitas Healthcare(미국), Navigine(미국), Pointr(영국), BlueIot(중국), 아이리스타(미국), InnerSpace(캐나다), Syook(인도), Oriient(이스라엘), Navenio(영국), Situm(스페인), Pozyx(벨기에), Azitek(포르투갈), Mapxus(홍콩), 및 Kontakt.io(미국)입니다.

조사 범위

본 시장 조사에서는 실내 위치 측정 시장의 각 부문별 시장 규모를 포괄적으로 다루고 있습니다. 본 조사는 제공 서비스, 기술, 용도, 업종, 지역 등 다양한 부문별 시장 규모와 성장 가능성을 추정하는 것을 목적으로 합니다. 또한, 주요 기업에 대한 상세한 경쟁 분석, 각 기업 개요, 제품 및 사업 제공과 관련된 주요 관찰 사항, 최근 동향, 그리고 시장 전략에 대해서도 다루고 있습니다.

본 보고서를 구매할 때의 주요 이점

본 보고서는 시장을 선도하는 기업 및 신규 진입 기업을 대상으로, 전 세계 실내 위치 정보 시장의 매출액 및 하위 부문에 대한 가장 정확한 추정치를 제공합니다. 본 보고서는 이해관계자들이 경쟁 구도를 이해하고, 자사의 비즈니스를 더 유리한 위치에 놓으며, 적절한 시장 진입 전략을 수립하는 데 필요한 추가적인 인사이트를 얻는 데 도움이 됩니다. 또한, 본 보고서는 이해관계자들이 시장 동향을 파악할 수 있도록 인사이트를 제공할 뿐만 아니라, 주요 시장 촉진요인, 억제요인, 과제 및 기회에 대한 정보도 제공합니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인(스마트 빌딩 및 캠퍼스 내 실내 내비게이션, 점유율 분석, 공간 최적화에 대한 수요 증가, 카메라, LED 조명, POS 단말기, 디지털 사이니지에 비콘 통합이 진행되고 있는 점)에 대한 분석, 제약요인(데이터 보안 및 개인정보 보호에 대한 우려, 신호 간섭 및 복잡한 실내 레이아웃으로 인한 위치 정보의 부정확성), 기회(공간 계획, 유지보수, 에너지 최적화, 시설 자동화를 지원하기 위한 디지털 트윈 통합이 진행되고 있는 점, 인더스트리 4.0, 스마트 시티, 스마트 제조에 대한 집중), 그리고 시장 성장에 영향을 미치는 과제(실내 위치 파악 기술에 대한 기술 및 인식 부족, 지도, 태그, 비콘, 센서의 유지 관리 문제)

- 제품 개발/혁신 : 실내 위치 정보 시장의 향후 기술, 연구개발 활동 및 신제품·서비스 출시에 관한 상세한 인사이트

- 시장 개발 : 수익성이 높은 시장에 대한 종합적인 정보 - 본 보고서에서는 각 지역의 실내 위치 추적 시장을 분석하고 있습니다.

- 시장의 다양화 : 실내 위치 측정 시장의 신제품·서비스, 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁사 분석 : Zebra Technologies(미국), Cisco(미국), HPE(미국), Esri(미국), Acuity Brands(미국), Inpixon(미국), HID Global(미국), CenTrak(미국), Sonitor(노르웨이), HERE Technologies(네덜란드), Ubisense(영국), Infsoft(독일), Polaris Wireless(미국), Quuppa(핀란드), Securitas Healthcare(미국), Navigine(미국), Pointr(영국), Blueiot(중국), AiRISTA(미국), InnerSpace(캐나다), Syook(인도), Oriient(이스라엘), Navenio(영국), Situm(스페인), Pozyx(벨기에), Azitek(포르투갈), Mapxus(홍콩), 및 Kontakt.io(미국)

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요와 업계 동향

제5장 업계 동향

제6장 전략적 파괴 : 디지털과 AI의 도입

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 실내 위치 정보 시장(제공별)

제10장 실내 위치 정보 시장(기술별)

제11장 실내 위치 정보 시장(용도별)

제12장 실내 위치 정보 시장(업계별)

제13장 실내 위치 정보 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSM 26.07.02The indoor location market size is projected to be USD 18.35 billion in 2026 and USD 50.10 billion by 2031, recording a CAGR of 22.3% during the forecast period. Indoor location technologies are gaining significant traction globally as organizations seek greater efficiency, safety, and automation within buildings.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) |

| Segments | By offering, technology, application, vertical, and region |

| Regions covered | North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America |

The increasing deployment of IoT devices, Bluetooth Low Energy (BLE), Ultra-Wideband (UWB), Wireless Fidelity (Wi-Fi) positioning, Radio Frequency Identification (RFID), and AI-powered analytics enables accurate tracking of assets, personnel, and workflows in real time. Increasing investments in smart buildings, smart cities, Industry 4.0, and digital transformation initiatives are further accelerating market growth. These solutions enhance operational efficiency, optimize resource utilization, improve customer experiences, strengthen security and emergency response capabilities, and support data-driven decision-making. This makes indoor location a critical enabler of intelligent, connected, and productive indoor environments across industries worldwide.

"Healthcare & pharmaceuticals segment to register the highest CAGR from 2026 to 2031"

The healthcare & pharmaceuticals segment is expected to register the highest CAGR in the indoor location market during the forecast period. The segmental growth is due to the rapid adoption of RTLS, indoor positioning, and asset-tracking technologies across hospitals and healthcare facilities. Healthcare providers are increasingly deploying BLE, RFID, Wi-Fi, and UWB solutions to track medical equipment, patients, and staff in real time, improving operational efficiency and patient safety. NHS hospitals in the UK have reported significant reductions in time spent locating critical equipment through RTLS deployments. High investments in smart hospitals, digital healthcare infrastructure, workflow automation, and staff safety solutions are further accelerating adoption. The impact includes reduced equipment loss, improved patient flow, faster emergency response, optimized resource utilization, and enhanced quality of care.

"Wi-Fi segment to account for the largest share of the indoor location market in 2026"

The Wi-Fi segment is anticipated to hold the largest share of the indoor location market in 2026 as it leverages existing wireless infrastructure deployed across enterprises, hospitals, airports, retail stores, and educational institutions. Organizations can implement indoor positioning without significant additional hardware investments, reducing deployment costs and complexity. The growing adoption of Wi-Fi 6 and Wi-Fi 6E enhances location accuracy, network capacity, and real-time tracking capabilities. Increasing demand for asset tracking, workforce management, visitor analytics, and navigation services is further driving adoption. The impact includes improved operational efficiency, better space utilization, enhanced customer experiences, and stronger data-driven decision-making. Continuous enterprise digitalization and smart-building initiatives remain key growth drivers.

"Asia Pacific to register the highest growth rate during the forecast period"

Asia Pacific is expected to witness the highest growth rate in the indoor location market during the forecast period, driven by the rapid urbanization, large-scale smart city initiatives, expanding digital infrastructure, and increasing adoption of Industry 4.0 technologies across China, India, Japan, South Korea, and Southeast Asia. Governments and enterprises are investing in smart airports, hospitals, factories, logistics hubs, and commercial buildings, creating strong demand for indoor navigation, real-time asset tracking, and location analytics solutions. The growing deployment of 5G, IoT, Wi-Fi, BLE, and UWB technologies is improving indoor positioning accuracy and scalability. At the same time, requirements for operational efficiency, worker safety, automation, and supply chain visibility continue to accelerate adoption. These trends are expected to enhance productivity, resource utilization, and customer experiences across multiple industries. Recent developments include the launch of a regional UWB-based Indoor Tracking System initiative for smart hospitals, manufacturing facilities, and smart buildings across ASEAN countries in 2025, highlighting the region's growing focus on advanced indoor location solutions.

Breakdown of primaries

The study contains insights from various industry experts, from solution vendors to Tier 1 companies. The break-up of the primaries is as follows:

- By Company Type: Tier 1 - 34%, Tier 2 - 43%, and Tier 3 - 23%

- By Designation: C-level Executives - 50%, D-level - 30%, and Managers - 20%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 30%, Middle East & Africa- 10%, and Latin America- 5%

Major players in the indoor location market are Zebra Technologies (US), Cisco (US), HPE (US), Esri (US), Acuity Brands (US), Inpixon (US), HID Global (US), CenTrak (US), Sonitor (Norway), HERE Technologies (Netherlands), Ubisense (UK), Infsoft (Germany), Polaris Wireless (US), Quuppa (Finland), Securitas Healthcare (US), Navigine (US), Pointr (UK), Blueiot (China), AiRISTA (US), InnerSpace (Canada), Syook (India), Oriient (Israel), Navenio (UK), Situm (Spain), Pozyx (Belgium), Azitek (Portugal), Mapxus (Hong Kong), and Kontakt.io (US).

Research Coverage

The market study covers the indoor location market size across different segments. It aims to estimate the market size and the growth potential across various segments, including offering, technology, application, vertical, and region. The study includes an in-depth competitive analysis of the leading market players, their company profiles, key observations related to product and business offerings, recent developments, and market strategies.

Key Benefits of Buying the Report

The report will help the market leaders/new entrants with information on the closest approximations of the global indoor location market's revenue numbers and sub-segments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. Moreover, the report will provide insights for stakeholders to understand the market's pulse and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Mounting demand for indoor navigation, occupancy analytics, and space optimization in smart buildings and campuses, Rising integration of beacons into cameras, LED lighting, PoS devices, and digital signage), restraints (Concerns related to data security and privacy, Location inaccuracy due to signal interference and complex indoor layouts), opportunities (Increasing digital twin integration to support space planning, maintenance, energy optimization, and facility automation, Focus on Industry 4.0 smart cities and smart manufacturing), and challenges (Lack of skills and awareness about indoor location technologies, issues in maintaining maps, tags, beacons, and sensors) influencing the market growth

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product and service launches in the indoor location market

- Market Development: Comprehensive information about lucrative markets-the report analyses various regions' indoor location markets

- Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the indoor location market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Zebra Technologies (US), Cisco (US), HPE (US), Esri (US), Acuity Brands (US), Inpixon (US), HID Global (US), CenTrak (US), Sonitor (Norway), HERE Technologies (Netherlands), Ubisense (UK), Infsoft (Germany), Polaris Wireless (US), Quuppa (Finland), Securitas Healthcare (US), Navigine (US), Pointr (UK), Blueiot (China), AiRISTA (US), InnerSpace (Canada), Syook (India), Oriient (Israel), Navenio (UK), Situm (Spain), Pozyx (Belgium), Azitek (Portugal), Mapxus (Hong Kong), and Kontakt.io (US)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN INDOOR LOCATION MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INDOOR LOCATION MARKET

- 3.2 INDOOR LOCATION MARKET, BY SERVICE AND REGION

- 3.3 INDOOR LOCATION MARKET, BY SERVICE

- 3.4 INDOOR LOCATION MARKET, BY OFFERING

- 3.5 INDOOR LOCATION MARKET, BY TECHNOLOGY

- 3.6 INDOOR LOCATION MARKET, BY VERTICAL

4 MARKET OVERVIEW AND INDUSTRY TRENDS

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Proliferation of Smartphones, Connected Devices, and Location-based Applications

- 4.2.1.2 Advancement and Effectiveness of Indoor Positioning with SLAM

- 4.2.1.3 Increasing Number of Applications Powered by Beacons and BLE Tags

- 4.2.1.4 Smart Buildings and Campuses Driving Indoor Navigation and Space Optimization

- 4.2.1.5 Growing Integration of Beacons in Cameras, LED Lighting, PoS Devices, and Digital Signage

- 4.2.2 RESTRAINTS

- 4.2.2.1 Concerns Related to Data Security and Privacy

- 4.2.2.2 Stringent Government Regulations

- 4.2.2.3 High Installation and Maintenance Costs

- 4.2.2.4 Signal Interference and Complex Indoor Layouts Can Reduce Location Accuracy

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing Demand for RFID Tags Across the Retail Industry

- 4.2.3.2 Growing Use of 5G for Location-based Services

- 4.2.3.3 Digital Twin Integration for Space Planning, Maintenance, Energy Optimization, and Facility Automation

- 4.2.3.4 Focus on Industry 4.0, Smart Cities, and Smart Manufacturing

- 4.2.4 CHALLENGES

- 4.2.4.1 Lack of Skills and Awareness About Indoor Location Technologies

- 4.2.4.2 Maintaining Maps, Tags, Beacons, and Sensors Can Increase Operational Complexity

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.3.1 SMART BUILDINGS AND FACILITY MANAGEMENT

- 4.3.2 HEALTHCARE ASSET TRACKING AND PATIENT FLOW MANAGEMENT

- 4.3.3 RETAIL, CUSTOMER EXPERIENCE, AND FOOTFALL ANALYTICS

- 4.3.4 WAREHOUSING, LOGISTICS, AND INDUSTRIAL OPERATIONS

- 4.3.5 AIRPORTS, TRANSPORT HUBS, AND PUBLIC VENUES

- 4.3.6 MANUFACTURING, WORKER SAFETY, AND INDUSTRY 4.0

- 4.3.7 EDUCATION CAMPUSES AND ENTERPRISE WORKPLACE EXPERIENCE

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN INDOOR LOCATION INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING MODEL ANALYSIS

- 5.5.1 INDICATIVE PRICING ANALYSIS OF INDOOR LOCATION SOLUTIONS, 2025

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 DEPLOYING INPIXON RTLS & LOCATION-AWARE AGENTIC AI FOR MANUFACTURING WORKFLOW AUTOMATION (SIEMENS ENERGY)

- 5.9.2 DEPLOYING HID MOBILE ACCESS & SPACEFLOW TENANT EXPERIENCE PLATFORM TO UNLOCK TENANT SATISFACTION

- 5.9.3 DEPLOYING CENTRAK RTLS FOR ASSET TRACKING AND MANAGEMENT AT MISSION HOSPITAL

- 5.9.4 DEPLOYING SONITOR RTLS FOR WORKFLOW OPTIMIZATION AT MEDSTAR HARBOR HOSPITAL

- 5.9.5 DEPLOYING INFSOFT RTLS AND E-INK TECHNOLOGY FOR DIGITAL TRANSPARENCY IN WAFER MANUFACTURING

- 5.9.6 DEPLOYING AZITEK WAREHOUSE DIGITAL TWIN FOR REAL-TIME ASSET VISIBILITY AND PROCESS AUTOMATION

- 5.10 IMPACT OF 2025 US TARIFF - INDOOR LOCATION MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.3.1 Strategic shifts and emerging trends

- 5.10.4 IMPACT ON COUNTRIES/REGIONS

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON END-USER INDUSTRIES

- 5.10.5.1 Healthcare

- 5.10.5.2 Logistics & Warehousing

- 5.10.5.3 Manufacturing

- 5.10.5.4 Smart Buildings & Commercial Real Estate

- 5.10.5.5 Energy & Utilities

6 STRATEGIC DISRUPTIONS: DIGITAL AND AI ADOPTION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 WI-FI

- 6.1.2 ULTRA-WIDE BAND (UWB)

- 6.1.3 RADIO FREQUENCY IDENTIFICATION

- 6.2 ADJACENT TECHNOLOGIES

- 6.2.1 INTERNET OF THINGS

- 6.2.2 MACHINE LEARNING

- 6.2.3 BLOCKCHAIN

- 6.2.4 5G

- 6.3 COMPLEMENTARY TECHNOLOGIES

- 6.3.1 DIGITAL TWIN

- 6.3.2 BLUETOOTH LOW ENERGY BEACONS

- 6.3.3 INERTIAL MEASUREMENT UNITS

- 6.3.4 INDOOR MAPPING AND 3D MODELING

- 6.4 TECHNOLOGY/PRODUCT ROADMAP FOR INDOOR LOCATION MARKET

- 6.4.1 SHORT-TERM ROADMAP (2023-2025)

- 6.4.2 MID-TERM ROADMAP (2026-2028)

- 6.4.3 LONG-TERM ROADMAP (2029-2030)

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI/GEN AI ON INDOOR LOCATION MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN INDOOR LOCATION PROCESS

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN INDOOR LOCATION MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN INDOOR LOCATION

7 REGULATORY LANDSCAPE

- 7.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE & BUYING BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

9 INDOOR LOCATION MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.1.1 OFFERING: MARKET DRIVERS

- 9.2 HARDWARE

- 9.2.1 BEACONS

- 9.2.2 TAGS

- 9.2.3 SENSORS

- 9.2.4 FIXED RFID READERS

- 9.2.5 OTHER HARDWARE

- 9.3 SOLUTIONS

- 9.3.1 INDOOR TRACKING

- 9.3.1.1 Asset & People Tracking

- 9.3.1.2 Indoor Location Analytics

- 9.3.2 INDOOR NAVIGATION

- 9.3.3 DATABASE MANAGEMENT SYSTEM

- 9.3.1 INDOOR TRACKING

- 9.4 SERVICES

- 9.4.1 PROFESSIONAL SERVICES

- 9.4.1.1 TRAINING & CONSULTING

- 9.4.1.2 SUPPORT & MAINTENANCE

- 9.4.1.3 SYSTEM INTEGRATION & IMPLEMENTATION

- 9.4.2 MANAGED SERVICES

- 9.4.1 PROFESSIONAL SERVICES

10 INDOOR LOCATION MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.1.1 TECHNOLOGY: MARKET DRIVERS

- 10.2 BLE

- 10.3 UWB

- 10.4 WI-FI

- 10.5 RFID

- 10.6 MAGNETIC POSITIONING

- 10.7 WIREPAS MESH

- 10.8 OTHER TECHNOLOGIES

11 INDOOR LOCATION MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.1.1 APPLICATION: MARKET DRIVERS

- 11.2 SALES & MARKETING

- 11.3 INVENTORY MANAGEMENT

- 11.4 REMOTE MONITORING

- 11.5 PREDICTIVE ASSET MANAGEMENT

- 11.6 EMERGENCY RESPONSE MANAGEMENT

- 11.7 SUPPLY CHAIN MANAGEMENT

- 11.8 OTHER APPLICATIONS

12 INDOOR LOCATION MARKET, BY VERTICAL

- 12.1 INTRODUCTION

- 12.1.1 VERTICAL: MARKET DRIVERS

- 12.2 TRANSPORTATION & LOGISTICS

- 12.3 TRAVEL & HOSPITALITY

- 12.4 MEDIA & ENTERTAINMENT

- 12.5 RETAIL

- 12.6 MANUFACTURING

- 12.7 HEALTHCARE & PHARMACEUTICALS

- 12.8 GOVERNMENT & PUBLIC SECTOR

- 12.9 MINING

- 12.10 OTHER VERTICALS

13 INDOOR LOCATION MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 NORTH AMERICA: INDOOR LOCATION MARKET DRIVERS

- 13.2.2 US

- 13.2.2.1 Healthcare digitalization and smart infrastructure investments to accelerate indoor location adoption

- 13.2.3 CANADA

- 13.2.3.1 Smart building adoption and healthcare modernization to drive indoor location deployments

- 13.3 EUROPE

- 13.3.1 EUROPE: INDOOR LOCATION MARKET DRIVERS

- 13.3.2 UK

- 13.3.2.1 Smart infrastructure modernization and workplace digitalization to fuel market growth

- 13.3.3 GERMANY

- 13.3.3.1 Industry 4.0 initiatives and smart factory investments to strengthen indoor location demand

- 13.3.4 FRANCE

- 13.3.4.1 Smart mobility initiatives and public infrastructure modernization to encourage adoption

- 13.3.5 SPAIN

- 13.3.5.1 Airport modernization and smart tourism investments to accelerate market development

- 13.3.6 ITALY

- 13.3.6.1 Digital infrastructure expansion and logistics modernization to support adoption

- 13.3.7 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 ASIA PACIFIC: INDOOR LOCATION MARKET DRIVERS

- 13.4.2 CHINA

- 13.4.2.1 Smart city development and industrial digitalization to strengthen market adoption

- 13.4.3 INDIA

- 13.4.3.1 Smart infrastructure investments and urban digitalization to create significant opportunities

- 13.4.4 JAPAN

- 13.4.4.1 Advanced transportation infrastructure and automation initiatives to drive growth

- 13.4.5 AUSTRALIA & NEW ZEALAND

- 13.4.5.1 Smart building adoption and digital workplace transformation to support market expansion

- 13.4.6 REST OF ASIA PACIFIC

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 MIDDLE EAST & AFRICA: INDOOR LOCATION MARKET DRIVERS

- 13.5.2 UAE

- 13.5.2.1 Smart city initiatives and world-class transportation infrastructure to accelerate adoption

- 13.5.3 KSA

- 13.5.3.1 Vision 2030 projects and smart infrastructure investments to strengthen demand

- 13.5.4 SOUTH AFRICA

- 13.5.4.1 Enterprise digitalization and infrastructure modernization to support market development

- 13.5.5 REST OF MIDDLE EAST & AFRICA

- 13.6 LATIN AMERICA

- 13.6.1 LATIN AMERICA: INDOOR LOCATION MARKET DRIVERS

- 13.6.2 BRAZIL

- 13.6.2.1 Transportation modernization and retail digitalization to strengthen market demand

- 13.6.3 MEXICO

- 13.6.3.1 Manufacturing expansion and logistics modernization to support market growth

- 13.6.4 REST OF LATIN AMERICA

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2026

- 14.3 MARKET SHARE ANALYSIS, 2025

- 14.4 REVENUE ANALYSIS OF LEADING PLAYERS, 2021-2025

- 14.5 BRAND/PRODUCT COMPARISON

- 14.6 COMPANY VALUATION AND FINANCIAL METRICS

- 14.7 COMPANY EVALUATION MATRIX, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Product footprint

- 14.7.5.4 Application footprint

- 14.7.5.5 Technology footprint

- 14.7.5.6 Vertical footprint

- 14.8 STARTUP/SME EVALUATION MATRIX

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

15 COMPANY PROFILES

- 15.1 MAJOR PLAYERS

- 15.1.1 ZEBRA TECHNOLOGIES

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 CISCO

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 HPE

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 ESRI

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Expansions

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 ACUITY BRANDS

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 INPIXON

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches

- 15.1.6.3.2 Deals

- 15.1.7 HERE TECHNOLOGIES

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Deals

- 15.1.8 HID GLOBAL

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.9 CENTRAK

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product launches

- 15.1.9.3.2 Deals

- 15.1.10 SONITOR TECHNOLOGIES

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches

- 15.1.10.3.2 Deals

- 15.1.1 ZEBRA TECHNOLOGIES

- 15.2 OTHER PLAYERS

- 15.2.1 UBISENSE

- 15.2.2 INFSOFT

- 15.2.3 POLARIS WIRELESS

- 15.2.4 QUUPPA

- 15.2.5 SECURITAS HEALTHCARE

- 15.2.6 NAVIGINE

- 15.3 SMES/STARTUPS

- 15.3.1 BLUEIOT

- 15.3.2 KONTAKT.IO

- 15.3.3 AIRISTA

- 15.3.4 INNERSPACE

- 15.3.5 SYOOK

- 15.3.6 ORIIENT

- 15.3.7 NAVENIO

- 15.3.8 SITUM

- 15.3.9 POZYX

- 15.3.10 AZITEK

- 15.3.11 MAPXUS

- 15.3.12 POINTR

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Breakdown of primary profiles

- 16.1.2.2 Key data from primary sources

- 16.1.2.3 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 MARKET BREAKUP AND DATA TRIANGULATION

- 16.3 MARKET SIZE ESTIMATION

- 16.3.1 TOP-DOWN APPROACH

- 16.3.2 BOTTOM-UP APPROACH

- 16.3.3 INDOOR LOCATION MARKET ESTIMATION: DEMAND-SIDE ANALYSIS

- 16.4 MARKET FORECAST

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 LIMITATIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS