|

시장보고서

상품코드

2072264

의약품 검사 장비 시장(-2031년) : 컴포넌트(비전 검사, X선 검사, 중량 선별기, 금속 감지기, 소프트웨어), 유형(수동, 자동), 포장 유형(주사기, 블리스터, 보틀), 제제(비경구, 경구)Pharmaceutical Inspection Machines Market by Component (Vision Inspection, X-Ray, Checkweigher, Metal Detector, Software), Type (Manual, Automatic), Packaging Type (Syringe, Blister, Bottle), and Formulation (Parenteral, Oral) - Global Forecast to 2031 |

||||||

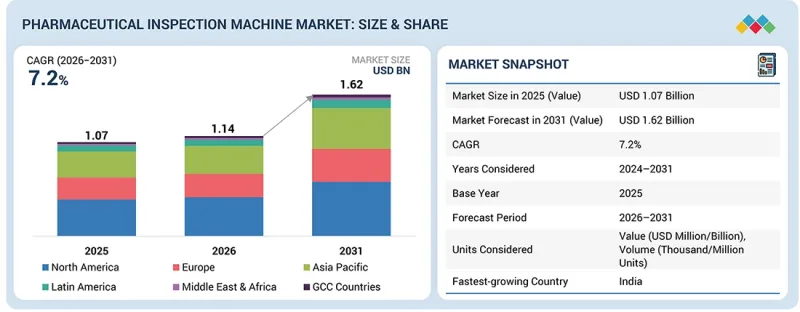

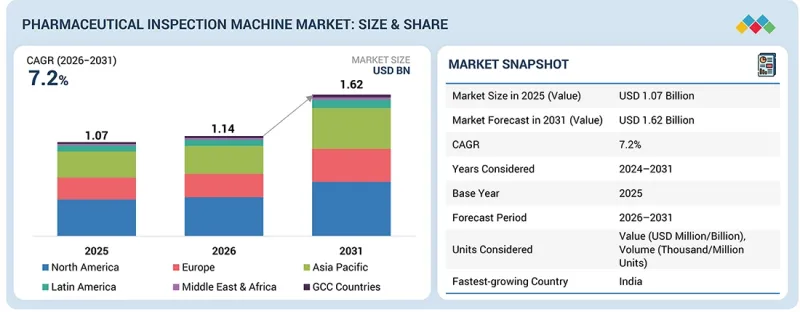

의약품 검사 장비 시장 규모는 2026년 11억 4,000만 달러에서 2031년에는 16억 2,000만 달러에 이를 것으로 예측되며, CAGR은 7.2%를 기록할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 컴포넌트, 유형, 포장 유형, 제형, 최종사용자별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가 |

앰플 및 바이알 부문의 급속한 성장은 엄격한 품질 관리 및 검사 기준이 요구되는 주사제, 생물학적 제제, 백신, 무균 의약품의 생산 증가에 힘입어 이루어지고 있습니다. 이러한 포장 유형은 매우 민감하기 때문에 입자 오염, 외관상의 결함, 충전량의 불균일, 균열, 밀봉 상태의 문제 등을 감지할 수 있는 첨단 검사 기술이 요구됩니다. 머신 비전 및 고해상도 이미지 기술과 통합된 AI 기반 검사 시스템은 정확한 실시간 분석을 제공하여 결함 감지 능력을 향상시킵니다. 비경구 제제에 대한 수요가 증가하는 데 더해, 규제 요건의 강화와 의약품 제조 자동화의 진전에 따라 앰플 및 바이알용 첨단 검사 시스템의 도입이 가속화되고 있습니다. 또한, 제조업체들은 업무 효율 향상, 리콜 최소화, 제품 안전성 확보를 위해 고속 검사 솔루션에 대한 투자를 점점 더 늘리고 있습니다.

구성 요소별:

소프트웨어 및 비전 시스템 부문의 성장을 이끄는 주요 요인 중 하나는 첨단 머신 비전, AI, 센서 기술의 도입 확대입니다. 검사 시스템은 카메라, 센서, 로봇, 컨베이어, 소프트웨어 플랫폼, 데이터 분석 도구 등의 구성 요소로 이루어져 있으며, 이들이 유기적으로 연동되어 정확한 검출과 품질 보증을 실현합니다. 고성능 이미징 시스템과 AI 지원 소프트웨어를 통해 미세 입자 오염, 외관상의 결함, 충전량의 편차, 포장 불일치 등을 식별하는 정확도가 향상되고 있습니다. 또한, 첨단 소프트웨어 솔루션은 오판으로 인한 불량품 배출률을 낮추고, 실시간 모니터링 및 공정 최적화를 지원합니다. 제약사들이 자동화 및 품질 규정 준수에 대한 투자를 지속함에 따라, 지능형 검사 구성 요소에 대한 수요가 증가하고 있으며, 현대 제약 제조 환경에서 이러한 구성 요소의 역할은 점점 더 중요해지고 있습니다.

제형별: 주사제 및 무균 제형 부문이 주도적인 위치를 차지하는 주요 요인 중 하나는 엄격한 품질 관리와 환자 안전에 대한 매우 중요한 요구 사항입니다. 의약품 검사 장비는 주사제, 생물학적 제제, 정제, 캡슐, 안과용 제품, 액제 등의 제제에서 결함, 입자 오염, 충전량의 불균일, 포장 오류를 검출하기 위해 널리 사용되고 있습니다. 주사제나 무균 제품은 엄격한 규제 요건과 오염으로 인한 높은 위험성 때문에 매우 정밀한 검사가 필요합니다. 또한, 생물학적 제제, 프리필드 주사기, 복잡한 제제의 생산이 증가함에 따라 첨단 검사 시스템에 대한 수요가 높아지고 있습니다. 제약사들이 제품의 무결성과 규정 준수를 지속적으로 최우선으로 삼고 있는 가운데, 다양한 제품 유형에 걸친 검사 요건이 시장의 지속적인 성장을 이끌고 있습니다.

북미의 확립된 의약품 제조 생태계는 의약품 검사 장비 도입을 추진하는 데 있어 매우 중요한 역할을 하고 있습니다. 이 지역에는 주요 제약 및 생명공학 기업, 수탁 제조 기관(CMO), 엄격한 품질 관리와 규제 준수가 요구되는 첨단 생산 시설이 다수 위치해 있습니다. 미국과 캐나다의 제약사들은 업무 효율을 높이고 제품의 안전성을 확보하기 위해 자동 검사 기술, 머신 비전 시스템, AI를 활용한 품질 보증 솔루션에 대한 투자를 확대되고 있습니다. 또한, 엄격한 규제 체계와 품질 기준에 따라 생산 라인 전반에 걸쳐 첨단 검사 시스템의 도입이 촉진되고 있습니다. 강력한 연구개발 역량, 높은 의료비 지출, 제조 공정의 현대화를 위한 지속적인 투자 역시 시장 성장을 더욱 뒷받침하고 있습니다. 이러한 견고한 제약 생태계 덕분에 지역 전체에서 의약품 검사 장비에 대한 지속적인 수요와 광범위한 도입이 보장되고 있습니다.

본 보고서에서는 전 세계 의약품 검사 장비 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 현황, 주요 기업 프로파일 등을 정리했습니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 현황과 구매 행동

제9장 의약품 검사기 시장 : 컴포넌트별

제10장 의약품 검사기 시장 : 유형별

제11장 의약품 검사기 시장 : 포장 유형별

제12장 의약품 검사기 시장 : 제제별

제13장 의약품 검사기 시장 : 최종사용자별

제14장 의약품 검사기 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

LSHThe pharmaceutical inspection machines market is projected to reach USD 1.62 billion by 2031 from USD 1.14 billion in 2026, growing at a CAGR of 7.2%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | By Component, Type, Packakging type, Formulation and End users |

| Regions covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa, and GCC Countries |

The rapid growth of the ampoules and vials segment is driven by increasing production of injectable drugs, biologics, vaccines, and sterile pharmaceutical products that require stringent quality control and inspection standards. These packaging formats are highly sensitive and demand advanced inspection technologies capable of detecting particulate contamination, cosmetic defects, fill-level inconsistencies, cracks, and seal integrity issues. AI-enabled inspection systems integrated with machine vision and high-resolution imaging technologies provide accurate real-time analysis and improve defect detection capabilities. Rising demand for parenteral formulations, coupled with stricter regulatory requirements and increasing adoption of automated pharmaceutical manufacturing, is accelerating the deployment of advanced inspection systems for ampoules and vials. Additionally, manufacturers are increasingly investing in high-speed inspection solutions to enhance operational efficiency, minimize recalls, and ensure product safety.

Based on Component:

One of the key factors driving the growth of the software and vision system segment in the Pharmaceutical Inspection Machine market is the increasing adoption of advanced machine vision, AI, and sensor technologies. Inspection systems comprise components such as cameras, sensors, robotics, conveyors, software platforms, and data analytics tools that work together to ensure accurate detection and quality assurance. High-performance imaging systems and AI-enabled software improve the identification of particulate contamination, cosmetic defects, fill-level variations, and packaging inconsistencies with greater precision. In addition, advanced software solutions reduce false rejection rates and support real-time monitoring and process optimization. As pharmaceutical manufacturers continue investing in automation and quality compliance, demand for intelligent inspection components is increasing, strengthening their role in modern pharmaceutical manufacturing environments.

Based on Formulation: One of the major factors driving the dominance of injectable and sterile formulation segments in the Pharmaceutical Inspection Machine market is the critical need for stringent quality control and patient safety. Pharmaceutical inspection machines are extensively used for formulations such as injectables, biologics, tablets, capsules, ophthalmic products, and liquid formulations to detect defects, particulate contamination, fill-level inconsistencies, and packaging errors. Injectable and sterile products require highly precise inspection due to strict regulatory requirements and the high risk associated with contamination. In addition, the growing production of biologics, prefilled syringes, and complex drug formulations has increased demand for advanced inspection systems. As pharmaceutical manufacturers continue to prioritize product integrity and compliance, inspection requirements across diverse formulation types are driving sustained market growth.

North America's well-established pharmaceutical manufacturing ecosystem plays a crucial role in driving the adoption of pharmaceutical inspection machines. The region has a strong presence of leading pharmaceutical and biotechnology companies, contract manufacturing organizations (CMOs), and advanced production facilities that require stringent quality control and regulatory compliance. Pharmaceutical manufacturers in the U.S. and Canada increasingly invest in automated inspection technologies, machine vision systems, and AI-enabled quality assurance solutions to enhance operational efficiency and ensure product safety. Additionally, strict regulatory frameworks and quality standards encourage the deployment of advanced inspection systems across production lines. The presence of strong R&D capabilities, high healthcare expenditure, and continuous investments in manufacturing modernization further support market growth. This robust pharmaceutical ecosystem ensures sustained demand and widespread adoption of pharmaceutical inspection machines across the region.

A breakdown of the primary participants (supply-side) for the pharmaceutical inspection machine market referred to in this report is provided below:

- By Company Type: Tier 1:34%, Tier 2: 38%, and Tier 3: 28%

- By Designation: C-level: 26%, Director Level: 35%, and Others: 39%

- By Region: North America: 17%, Europe: 39%, Asia Pacific: 28%, Latin America: 8%, Middle East & Africa: 3%, GCC Countries: 5%

Prominent players in the pharmaceutical inspection machine market are market Korber AG (Germany), Mettler Toledo (US), Omron Corporation (Japan), Cognex Corporation (US), Stevanato Group (Italy), Antares Vision S.p.A. (Italy), Optel Group (Canada), Syntegon Technology GmbH (Germany), Jekson Vision (India), ACG (India), Brevetti CEA S.p.A. (Italy), Roquette Freres (France), Toflon Life Science (China), Prodieco (Ireland), WIPOTEC GmbH (Germany), CMP Pharma S.R.L. (Italy), Keyence Corporation (Japan), Cassel Messtechnik GmbH (Germany), Thermo Fisher Scientific Inc. (US), Loma Systems (UK), VITRONIC Dr.-Ing. Stein Bildverarbeitungssysteme GmbH (Germany), Minebea Intec GmbH (Germany), Marchesini Group S.p.A. (Italy), N.K.P. Pharma Pvt. Ltd. (India), and Span Systems (India).

Research Coverage

The report evaluates the pharmaceutical inspection machine market and estimates the market size and future growth potential of this market based on various segments, including by component, type, packaging type, formulation, end user, and region. The report also includes a competitive analysis of the major players in this market, along with company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will assist the market leader/new entrants in the market with data on the nearest approximations of the revenue numbers for the overall, the pharmaceutical inspection machine market, and the subsegments. The report will assist stakeholders in understanding the competitive landscape and gain further insights into better positioning their businesses and making appropriate go-to-market strategies. The report assists the stakeholders in understanding the market pulse and gives them data on influential drivers, hindrances, obstacles, and opportunities in the market.

This report provides insights into the following points:

- Analysis of key drivers (increasing adoption of AI- and machine vision-based inspection systems, rising pharmaceutical manufacturing output, growing emphasis on stringent regulatory compliance and quality assurance, rising demand for automated inspection solutions, increasing focus on patient safety and defect reduction), restraints (high implementation and maintenance costs of advanced inspection systems, complex integration with existing manufacturing infrastructure), opportunities (growing adoption of Industry 4.0 and smart manufacturing, rising demand for pharmaceutical inspection solutions in emerging markets), and challenges (shortage of skilled professionals for operating advanced systems, managing high inspection accuracy while minimizing false rejection rates)

- Product Enhancement/Innovation: Comprehensive details about product launches and anticipated trends in the global pharmaceutical inspection machines market

- Market Development: Thorough knowledge and analysis of the profitable rising markets by product, application, end user, and region.

- Market Diversification: Comprehensive information about newly launched products, expanding markets, current advancements, and investments in the global pharmaceutical inspection machines market

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings, and capacities of the major competitors in the global pharmaceutical inspection machines market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 SEGMENTS COVERED & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 LIMITATIONS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: INSIGHTS & DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET GROWTH

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 PHARMACEUTICAL INSPECTION MACHINES MARKET OVERVIEW

- 3.2 ASIA PACIFIC: PHARMACEUTICAL INSPECTION MACHINES MARKET, BY PRODUCT AND COUNTRY (2025)

- 3.3 PHARMACEUTICAL INSPECTION MACHINES MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.4 PHARMACEUTICAL INSPECTION MACHINES MARKET, BY REGION (2023-2030)

- 3.5 PHARMACEUTICAL INSPECTION MACHINES MARKET: DEVELOPED MARKETS VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing use of inspection machines by pharmaceutical and biotechnology companies

- 4.2.1.2 Rising number of inspection checkpoint mandates

- 4.2.1.3 Technological advancements and stringent regulatory mandates for high-quality products

- 4.2.2 RESTRAINTS

- 4.2.2.1 High initial capital expenditure and recurring maintenance costs

- 4.2.2.2 Increased data security and privacy concerns

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing outsourcing of manufacturing operations to emerging economies

- 4.2.3.2 Focus on production optimization and high R&D investments

- 4.2.4 CHALLENGES

- 4.2.4.1 Complexities in integrating pharmaceutical inspection machines

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS IN PHARMACEUTICAL INSPECTION MACHINES MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL PHARMACEUTICAL INDUSTRY

- 5.2.4 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.3.1 ROLE IN SUPPLY CHAIN

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 PHARMACEUTICAL INSPECTION MACHINE SUPPLIERS

- 5.5.2 END USERS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND FOR PHARMACEUTICAL INSPECTION MACHINES, BY PRODUCT

- 5.6.2 AVERAGE SELLING PRICE TREND FOR PHARMACEUTICAL INSPECTION MACHINES, BY REGION

- 5.6.3 AVERAGE SELLING PRICE TREND FOR PHARMACEUTICAL INSPECTION MACHINES, BY END-USE INDUSTRY

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA FOR INSTRUMENTS, APPLIANCES, AND MACHINES FOR MEASURING OR CHECKING (HS CODE: 903180)

- 5.7.2 EXPORT DATA FOR INSTRUMENTS, APPLIANCES, AND MACHINES FOR MEASURING OR CHECKING (HS CODE: 903180)

- 5.7.3 IMPORT DATA FOR PARTS AND ACCESSORIES FOR INSTRUMENTS, APPLIANCES, AND MACHINES FOR MEASURING AND CHECKING (HS CODE: 903190)

- 5.7.4 EXPORT DATA FOR PARTS AND ACCESSORIES FOR INSTRUMENTS, APPLIANCES, AND MACHINES FOR MEASURING AND CHECKING (HS CODE: 903190)

- 5.8 KEY CONFERENCES & EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.12 IMPACT OF 2025 US TARIFFS ON PHARMACEUTICAL INSPECTION MACHINES MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUTRY/REGION

- 5.12.5 IMPACT ON END USE INDUSTRIES

- 5.12.5.1 Pharmaceutical companies

- 5.12.5.2 Biotechnology companies

- 5.12.5.3 Contract research organizations (CROs) and contract development and manufacturing organizations (CDMOs)

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Machine vision technology

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Advanced sensors & imaging techniques

- 6.1.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 PATENT ANALYSIS

- 6.2.1 INSIGHTS ON PATENT PUBLICATION TRENDS, TOP APPLICANTS, AND JURISDICTION FOR PHARMACEUTICAL INSPECTION SYSTEMS, JANUARY 2015-APRIL 2026

- 6.2.2 LIST OF MAJOR PATENTS, 2023-2026

- 6.3 FUTURE APPLICATIONS

- 6.3.1 AI-POWERED VISUAL DEFECT DETECTION

- 6.3.2 ADVANCED HYPERSPECTRAL & MULTI-IMAGING INSPECTION

- 6.3.3 SMART SENSOR-INTEGRATED INSPECTION SYSTEMS

- 6.3.4 INTEGRATED MULTI-FUNCTION PHARMACEUTICAL INSPECTION PLATFORMS

- 6.4 IMPACT OF AI ON PHARMACEUTICAL INSPECTION MACHINES MARKET

- 6.4.1 TOP USE CASES & MARKET POTENTIAL

- 6.4.2 BEST PRACTICES IN PHARMACEUTICAL INSPECTION MACHINES MARKET

- 6.4.3 CASE STUDIES OF AI IMPLEMENTATION IN PHARMACEUTICAL INSPECTION MACHINES MARKET

- 6.4.4 INTERCONNECTED ADJACENT ECOSYSTEM & IMPACT ON MARKET PLAYERS

- 6.4.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN PHARMACEUTICAL INSPECTION MACHINES MARKET

7 SUSTAINABILITY & REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY ANALYSIS

- 7.1.1.1 North America

- 7.1.1.2 Europe

- 7.1.1.3 APAC

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.1 REGULATORY ANALYSIS

- 7.2 INDUSTRY STANDARDS

- 7.2.1 PHARMACEUTICAL INSPECTION MACHINE PRACTICE STANDARDS

- 7.2.2 ELECTRICAL AND MACHINERY SAFETY STANDARD - ISO 12100 & EN 60204-1

- 7.2.3 SOFTWARE LIFECYCLE STANDARD - GAMP 5 & FDA 21 CFR PART 11

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 PHARMACEUTICAL INSPECTION MACHINES MARKET, BY COMPONENT

- 9.1 INTRODUCTION

- 9.2 PHARMACEUTICAL INSPECTION SYSTEMS

- 9.2.1 VISION INSPECTION SYSTEMS

- 9.2.1.1 Multifunctional vision inspection systems

- 9.2.1.1.1 Versatility and improved production efficiency to drive segmental growth

- 9.2.1.2 Specialized vision inspection systems

- 9.2.1.2.1 Stringent quality standards and better patient well-being to propel segment growth

- 9.2.1.1 Multifunctional vision inspection systems

- 9.2.2 X-RAY INSPECTION SYSTEMS

- 9.2.2.1 Increasing demand for precise underfill and overfill inspection to aid market growth

- 9.2.3 LEAK DETECTION SYSTEMS

- 9.2.3.1 Rising adoption in pharmaceutical applications to drive market growth

- 9.2.4 METAL DETECTORS

- 9.2.4.1 Growing need for metal contaminant detection in food & beverage industry to boost demand

- 9.2.5 CHECKWEIGHERS

- 9.2.5.1 Increased focus on reducing waste in manufacturing process to aid market growth

- 9.2.6 COMBINATION SYSTEMS

- 9.2.6.1 Technological advancements for ensuring thorough quality assessment and regulatory compliance to drive market

- 9.2.7 OTHER PHARMACEUTICAL INSPECTION SYSTEMS

- 9.2.1 VISION INSPECTION SYSTEMS

- 9.3 PHARMACEUTICAL INSPECTION SOFTWARE

- 9.3.1 RISING NEED TO IMPROVE INSPECTION EFFICIENCY TO PROPEL ADOPTION

10 PHARMACEUTICAL INSPECTION MACHINES MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 FULLY AUTOMATED PHARMACEUTICAL INSPECTION MACHINES

- 10.2.1 SUPERIOR THROUGHPUT RATES AND DEFECT DETECTION ACCURACY IN HIGH-VISCOSITY SUSPENSIONS TO DRIVE MARKET

- 10.3 SEMI-AUTOMATED PHARMACEUTICAL INSPECTION MACHINES

- 10.3.1 SIMULTANEOUS INSPECTION CAPABILITIES WITH HIGH STANDARDS OF PHARMACEUTICAL QUALITY CONTROL TO AID MARKET GROWTH

- 10.4 MANUAL PHARMACEUTICAL INSPECTION MACHINES

- 10.4.1 COST-EFFECTIVENESS TO AUGMENT SEGMENT GROWTH

11 PHARMACEUTICAL INSPECTION MACHINES MARKET, BY PACKAGING TYPE

- 11.1 INTRODUCTION

- 11.2 AMPOULES & VIALS

- 11.2.1 INCREASING DEMAND FOR VACCINES AND BIOPHARMACEUTICALS TO FUEL MARKET GROWTH

- 11.3 SYRINGES

- 11.3.1 IMPROVED SAFETY AND INCREASED COMPLIANCE WITH CGMP STANDARDS TO SUPPORT MARKET GROWTH

- 11.4 BOTTLES

- 11.4.1 RISING DEMAND FOR LIQUID OR SOLID RESIDUE DETECTION TO AUGMENT MARKET GROWTH

- 11.5 BLISTERS

- 11.5.1 SUPERIOR PRODUCT PROTECTION AND ENHANCED PATIENT COMPLIANCE TO BOOST MARKET GROWTH

- 11.6 OTHER PACKAGING TYPES

12 PHARMACEUTICAL INSPECTION MACHINES MARKET, BY FORMULATION

- 12.1 INTRODUCTION

- 12.2 ORAL FORMULATIONS

- 12.2.1 TABLETS & CAPSULES

- 12.2.1.1 Increasing applications in pharmaceutical industry to drive segment

- 12.2.2 ORAL SOLUTIONS & SUSPENSIONS/SYRUPS

- 12.2.2.1 Focus on improved product quality and prevention of contamination to fuel segment growth

- 12.2.3 OTHER ORAL FORMULATIONS

- 12.2.1 TABLETS & CAPSULES

- 12.3 PARENTERAL FORMULATIONS

- 12.3.1 INCREASED PRODUCTION THROUGHPUT AND REDUCED HUMAN ERRORS TO BOOST SEGMENT GROWTH

- 12.4 OTHER FORMULATIONS

13 PHARMACEUTICAL INSPECTION MACHINES MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 PHARMACEUTICAL COMPANIES

- 13.2.1 HIGH PREVALENCE OF CHRONIC DISEASES TO SUPPORT MARKET GROWTH

- 13.3 BIOTECHNOLOGY COMPANIES

- 13.3.1 FOCUS ON REDUCING COUNTERFEIT DRUG PRODUCTION AND IMPROVING PRODUCT QUALITY TO SPUR MARKET GROWTH

- 13.4 CROS & CDMOS

- 13.4.1 LOW MANUFACTURING COSTS AND HIGH-QUALITY MAINTENANCE TO FUEL MARKET GROWTH

14 PHARMACEUTICAL INSPECTION MACHINES MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 US to dominate North American pharmaceutical inspection machines market during forecast period

- 14.2.2 CANADA

- 14.2.2.1 Focus on better healthcare quality and increased patient safety to support market growth

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 High healthcare spending and presence of key pharmaceutical manufacturers to aid market growth

- 14.3.2 UK

- 14.3.2.1 Rising demand for personalized medicines and increasing geriatric population to augment market growth

- 14.3.3 FRANCE

- 14.3.3.1 Growth in generic drug market and increased pharmaceutical exports to spur adoption

- 14.3.4 ITALY

- 14.3.4.1 Favorable government initiatives and increased private investments to drive market

- 14.3.5 SPAIN

- 14.3.5.1 Improved healthcare infrastructure and high prevalence of chronic diseases to boost market growth

- 14.3.6 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Increased investment in healthcare infrastructure to propel market growth

- 14.4.2 JAPAN

- 14.4.2.1 Well-developed pharmaceutical manufacturing industry and stringent healthcare regulations to drive market

- 14.4.3 INDIA

- 14.4.3.1 Growing focus on cost-effective branded drug production to fuel market growth

- 14.4.4 AUSTRALIA

- 14.4.4.1 High R&D expenditure and technological advancements to fuel market growth

- 14.4.5 SOUTH KOREA

- 14.4.5.1 Attractive medical tourism industry and favorable government policies to propel market growth

- 14.4.6 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 LATIN AMERICA

- 14.5.1 BRAZIL

- 14.5.1.1 Increasing geriatric population and rising per capita income to aid market growth

- 14.5.2 MEXICO

- 14.5.2.1 Improving healthcare infrastructure and burgeoning pharmaceutical industry to augment market growth

- 14.5.3 REST OF LATIN AMERICA

- 14.5.1 BRAZIL

- 14.6 MIDDLE EAST & AFRICA

- 14.6.1 GCC COUNTRIES

- 14.6.1.1 Robust economic growth and high public healthcare spending to support market growth

- 14.6.1 GCC COUNTRIES

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGY/RIGHT TO WIN

- 15.3 REVENUE ANALYSIS, 2023-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.5.5.1 Company footprint

- 15.5.5.2 Region footprint

- 15.5.5.3 Component footprint

- 15.5.5.4 Type footprint

- 15.5.5.5 Packaging type footprint

- 15.6 COMPETITIVE EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 RESPONSIVE COMPANIES

- 15.6.3 DYNAMIC COMPANIES

- 15.6.4 STARTING BLOCKS

- 15.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.6.5.1 Detailed list of key startups/SMEs

- 15.6.5.2 Competitive benchmarking of key startups/SMEs

- 15.7 COMPANY VALUATION & FINANCIAL METRICS

- 15.7.1 FINANCIAL METRICS

- 15.7.2 COMPANY VALUATION

- 15.8 BRAND/PRODUCT COMPARISON

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

- 15.9.4 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 KORBER AG

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses & competitive threats

- 16.1.2 METTLER-TOLEDO

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches

- 16.1.2.4 MnM view

- 16.1.2.4.1 Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses & competitive threats

- 16.1.3 OMRON CORPORATION

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches & upgrades

- 16.1.3.3.2 Deals

- 16.1.3.4 MnM view

- 16.1.3.4.1 Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses & competitive threats

- 16.1.4 STEVANATO GROUP

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches & upgrades

- 16.1.4.3.2 Deals

- 16.1.4.4 MnM view

- 16.1.4.4.1 Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses & competitive threats

- 16.1.5 COGNEX CORPORATION

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product launches

- 16.1.5.3.2 Deals

- 16.1.5.4 MnM view

- 16.1.5.4.1 Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses & competitive threats

- 16.1.6 ANTARES VISION GROUP

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product launches & upgrades

- 16.1.6.3.2 Deals

- 16.1.6.3.3 Expansion

- 16.1.6.3.4 Other developments

- 16.1.7 OPTEL GROUP

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.8 SYNTEGON TECHNOLOGY GMBH

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches

- 16.1.9 JEKSON VISION

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.10 ACG

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.11 BREVETTI CEA SPA

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Deals

- 16.1.12 ROQUETTE FRERES

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.13 TOFFLON LIFE SCIENCE

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.14 PRODITEC

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.15 WIPOTEC GMBH

- 16.1.15.1 Business overview

- 16.1.15.2 Products offered

- 16.1.16 CMP PHARMA S.R.L.

- 16.1.16.1 Business overview

- 16.1.16.2 Products offered

- 16.1.16.3 Recent developments

- 16.1.16.3.1 Expansions

- 16.1.1 KORBER AG

- 16.2 OTHER PLAYERS

- 16.2.1 KEYENCE CORPORATION

- 16.2.2 CASSEL MESSTECHNIK GMBH

- 16.2.3 THERMO FISHER SCIENTIFIC INC.

- 16.2.4 LOMA SYSTEMS

- 16.2.5 VITRONIC DR.-ING. STEIN BILDVERARBEITUNGSSYSTEME GMBH

- 16.2.6 MINEBEA INTEC GMBH

- 16.2.7 MARCHESINI GROUP S.P.A.

- 16.2.8 N.K.P. PHARMA PVT. LTD.

- 16.2.9 SPAN SYSTEMS

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 Key industry insights

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.3 MARKET BREAKDOWN & DATA TRIANGULATION

- 17.4 MARKET RANKING ANALYSIS

- 17.5 STUDY ASSUMPTIONS

- 17.6 RISK ASSESSMENT

- 17.7 LIMITATIONS

- 17.7.1 METHODOLOGY-RELATED LIMITATIONS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS