|

시장보고서

상품코드

2072265

방사선 탐지, 모니터링 및 안전 시장(-2031년) : 제품(개인 선량계, 모니터, 에어리어 프로세스, 환경, 재료, 소프트웨어), 구성(GM 카운터, 신틸레이터), 최종사용자(원자력발전소, 의료, 방위)Radiation Detection, Monitoring & Safety Market by Product (Personal Dosimeter; Monitor: Area Process, Environment, Material; Software), Composition (GM Counter, Scintillator), End User (Nuclear Plants, Healthcare, Defense) - Global Forecast to 2031 |

||||||

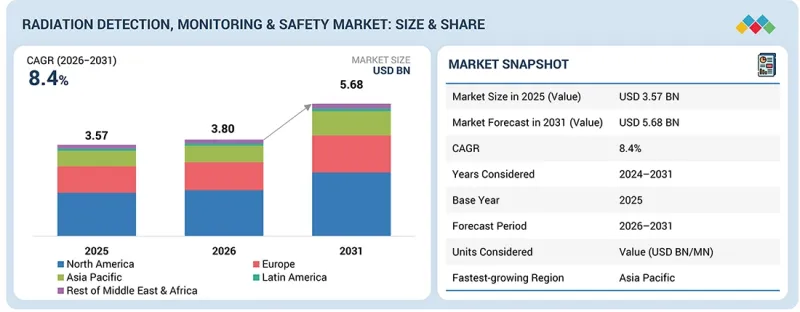

방사선 탐지, 모니터링 및 안전 시장은 2026년 380만 달러에서 2031년까지 56억 8,000만 달러에 이를 것으로 예측되며, CAGR은 8.4%를 기록할 전망입니다.

의료 분야에서의 방사선 활용 확대는 물론, 원자력 에너지 부문의 급속한 성장, 보안 대책 강화, 엄격한 규제 기준 등이 시장 성장을 뒷받침하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 제품, 구성, 용도 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

임상 진단 및 암 치료 분야에서 X선, 컴퓨터 단층촬영(CT), 양전자 방출 단층촬영(PET), 방사선 치료 등의 영상 진단법이 지속적으로 도입됨에 따라, 첨단 방사선 탐지 및 모니터링 시스템에 대한 수요가 더욱 크게 증가하고 있습니다. 이러한 기술은 환자와 의료진 모두의 안전과 보호를 보장하는 데 필수적입니다.

제품별로는 방사선 탐지 및 모니터링 제품이 2025년에 가장 큰 시장 점유율을 차지했습니다.

방사선 탐지 및 모니터링 제품 부문이 가장 큰 시장 점유율을 차지하고 있습니다. 국제원자력기구(IAEA), 미국 원자력규제위원회(NRC), 직업안전보건청(OSHA) 등의 규제 기관은 근로자의 방사선 피폭 및 환경 조건에 대한 지속적인 모니터링에 대해 엄격한 규제를 시행하고 있습니다. 원자력, 제조, 석유 및 가스, 광업 등의 업계에서는 천연 방사성 물질(NORM)을 자주 접하게 됩니다. 이는 법규를 준수하고 위험을 줄이기 위해 효과적인 방사선 탐지 및 모니터링 솔루션이 매우 중요함을 보여줍니다. 또한, 방사선 누출, 우발적 피폭, 오염 사고의 발생 빈도가 높아짐에 따라 첨단 실시간 모니터링 기능에 대한 수요가 증가하고 있으며, 이로 인해 첨단 방사선 검출 기기에 대한 전 세계적인 수요가 더욱 촉진되고 있습니다.

구성별로는 2025년에 검출기가 1위를 차지했습니다.

검출기 부문은 핵폐기물, 오염 지역, 광업 및 석유 및 가스 부문에서 흔히 발견되는 NORM에 의한 방사선 피폭에 대한 우려가 커짐에 힘입어 가장 큰 시장 점유율을 차지하고 있습니다. 이러한 환경적 요인으로 인해 첨단 방사선 검출기에 대한 수요가 확대되고 있습니다. 국제원자력기구(IAEA) 및 미국 환경보호청(EPA) 등의 기관이 수립한 규제 체계는 방사선 모니터링에 관한 엄격한 절차를 의무화하고 있으며, 첨단 감지 기술의 도입을 더욱 촉진하고 있습니다. 특히 고체 검출기 및 실시간 모니터링 시스템 분야의 소형화와 기술 발전이라는 지속적인 추세는 다양한 산업 분야에서 이러한 기술의 보다 광범위한 도입을 촉진하고 있습니다. 이러한 진화를 통해 최신 방사선 검출기는 필수적인 도구로서의 위상을 확립하고, 시장 상황에서의 우위를 공고히 하고 있습니다.

아시아태평양은 예측 기간 동안 상당한 성장률을 나타낼 것으로 전망됩니다.

아시아태평양에서는 급속한 산업화, 원자력 발전의 확대, 의료 분야에 대한 투자 확대, 방사선과 관련된 보안 우려의 고조 등을 배경으로 상당한 성장을 이룰 것으로 전망됩니다. 중국, 인도, 일본, 한국 등의 국가들은 증가하는 에너지 수요를 충족시키기 위해 원자력 에너지 인프라에 막대한 투자를 해왔습니다. 이러한 추세에 따라, 효과적인 방사선 모니터링 및 안전 대책 솔루션에 대한 꾸준한 수요가 지속적으로 발생하고 있습니다. 또한, 의료 분야의 확대, 특히 방사선을 이용한 영상 진단 기술(X선, CT, PET 스캔 등) 및 암 치료를 위한 방사선 요법의 이용 증가로 인해, 방사선 검출기 및 모니터링 기기에 대한 수요가 높아지고 있습니다. 또한, 해당 지역에서는 핵 테러나 방사성 물질의 불법 거래로 인한 위험도 높아지고 있습니다. 그 결과, 각국 정부는 국경, 교통 요충지, 방위 시설 등 주요 거점에서의 방사선 탐지 능력을 강화해야 합니다.

본 보고서에서는 전 세계 방사선 탐지 및 모니터링·안전 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 현황, 주요 기업 프로파일 등을 정리했습니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI 도입에 의한 전략적 파괴적 변화

제7장 규제 상황

제8장 고객 현황과 구매 행동

제9장 방사선 탐지, 모니터링 및 안전 시장 : 제품별

제10장 방사선 탐지, 모니터링 및 안전 시장 : 구성별

제11장 방사선 탐지, 모니터링 및 안전 시장 : 용도별

제12장 방사선 탐지, 모니터링 및 안전 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

LSHThe radiation detection, monitoring & safety market is projected to reach USD 5.68 billion by 2031, from USD 3.80 million in 2026, with a CAGR of 8.4%. The expanding application of radiation across healthcare, coupled with the booming nuclear energy sector, heightened security considerations, and rigorous regulatory standards, is propelling market growth.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product, Composition, Application |

| Regions covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

The continuous implementation of imaging modalities such as X-rays, computed tomography (CT), positron emission tomography (PET), and radiotherapy in clinical diagnostics and oncological treatment has further generated substantial demand for advanced radiation detection and monitoring systems. These technologies are essential for ensuring the safety and protection of both patients and healthcare personnel.

By product, radiation detection & monitoring products held the largest market share in 2025.

The radiation detection & monitoring products segment holds the largest market share. Regulatory bodies such as the International Atomic Energy Agency (IAEA), the Nuclear Regulatory Commission (NRC), and the Occupational Safety and Health Administration (OSHA) enforce stringent regulations for the continuous monitoring of radiation exposure among workers and environmental conditions. Industries such as nuclear power, manufacturing, oil & gas, and mining frequently encounter Naturally Occurring Radioactive Materials (NORM). This underscores the critical need for effective radiation detection and monitoring solutions to ensure compliance and mitigate risks. Moreover, the growing frequency of radiation leaks, accidental exposures, and contamination incidents has heightened the demand for advanced real-time monitoring capabilities, further driving the global need for sophisticated radiation detection instruments.

By composition, detectors secured the leading position in 2025.

The detectors segment represents the largest market share, driven by rising concerns over radiation exposure from nuclear waste, contaminated sites, and NORM commonly found in mining and oil & gas sectors. These environmental factors have escalated the demand for advanced radiation detectors. Regulatory frameworks established by agencies like the IAEA and the Environmental Protection Agency (EPA) enforce strict protocols for radiation monitoring, further incentivizing the adoption of sophisticated detection technologies. The ongoing trends of miniaturization and technological advancements, particularly in solid-state detectors and real-time monitoring systems, have facilitated broader implementation across various industries. This evolution has positioned modern radiation detectors as essential tools, consolidating their dominance within the market landscape.

Asia Pacific is expected to register a significant growth rate during the forecast period.

The Asia Pacific region is projected to experience significant growth in the market, driven by rapid industrialization, advancements in nuclear power initiatives, increased healthcare investments, and heightened security concerns related to radiation. Countries such as China, India, Japan, and South Korea have substantially invested in nuclear energy infrastructure to meet escalating energy demands. This trend has consistently created a robust need for effective radiation monitoring and safety solutions. Furthermore, the expansion of the healthcare sector, particularly the rising utilization of radiation-based diagnostic imaging techniques (such as X-rays, CT, and PET scans) and radiation therapies for cancer treatment, has intensified the demand for radiation detectors and monitoring instruments. The region also faces increased risks from nuclear terrorism and the illicit trafficking of radioactive materials. Consequently, governments must enhance their radiation detection capabilities at critical points, including borders, transportation hubs, and defense installations.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1-40%, Tier 2-30%, and Tier 3-30%

- By Designation: C-level-- 27%, Director-level-18%, and Other Designations-55%

- By Region: North America-50%, Europe-20%, Asia Pacific-15%, Latin America-10%, and Middle East & Africa-5%

Prominent players in this market are Fortive (US), Thermo Fisher Scientific Inc. (US), Mirion Technologies Inc. (US), Fuji Electric Co., Ltd. (Japan), Ludlum Measurements, Inc. (US), and Ametek, Inc.(US).

Research Coverage

The radiation detection, monitoring & safety market is segmented by product, composition, application, and region. Key factors influencing market growth include driving forces, restraints, opportunities, and challenges for stakeholders. The report also reviews the leading companies competing in the radiation detection, monitoring & safety market. A micro-level analysis can be conducted to examine trends, growth opportunities, and contributions to the market. Additionally, it highlights potential revenue growth opportunities across various market segments in five major regions.

Key Benefits of Buying this Report:

The report will be beneficial for the new entrants or market leaders and smaller firms in this market in evaluating their investments in the radiation detection, monitoring & safety sector through a thorough analysis of data as a solid basis for risk assessment and well-validated investment decisions. Get detailed market segmentation on the end-user and regional dimensions for customized reporting that can be used to target a specific segment. This report will also contain an exhaustive assessment covering key trends, challenges, growth catalysts, and prospects so that strategic decisions can be made with complete insight.

The report provides insights into the following pointers:

- Analysis of key drivers (Growing number of PET/CT scans, increasing usage of nuclear medicine and radiation therapy), restraints (Increasing use of alternatives for nuclear energy. Additionally, Shift in nuclear energy policies and increased nuclear phase-out), opportunities (Technological advancements in radiation detection), and challenges (High cost of lead for manufacturing radiation safety products) influencing the growth of the radiation detection, monitoring & safety market

- Product Development/Innovation: Detailed insights on upcoming technologies, R&D activities, and new product & service launches in the radiation detection, monitoring & safety market

- Market Diversification: Exhaustive information about untapped geographies, new products, recent developments, and investments in the radiation detection, monitoring & safety market

- Market Development: Comprehensive information about lucrative markets -the report analyzes the radiation detection, monitoring & safety market across varied regions

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Fortive (US), Thermo Fisher Scientific Inc. (US), Mirion Technologies Inc. (US), Fuji Electric Co., Ltd. (Japan), Ludlum Measurements Inc. (US), and Ametek Inc.(US), among others

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKETS COVERED

- 1.3.1 INCLUSIONS & EXCLUSIONS

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STUDY LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 DISRUPTIVE TRENDS IN RADIATION DETECTION, MONITORING, AND SAFETY MARKET

- 2.3 HIGH GROWTH SEGMENTS

- 2.4 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 RADIATION DETECTION, MONITORING, AND SAFETY MARKET OVERVIEW

- 3.2 NORTH AMERICA: RADIATION DETECTION, MONITORING, AND SAFETY MARKET, BY PRODUCT, 2025

- 3.3 GEOGRAPHIC SNAPSHOT OF RADIATION DETECTION, MONITORING, AND SAFETY MARKET

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing number of PET/CT scans

- 4.2.1.2 Increasing usage of nuclear medicine and radiation therapy

- 4.2.1.3 Rising military expenditure for homeland security

- 4.2.1.4 Increasing safety awareness among personnel working in radiation-prone environments

- 4.2.2 RESTRAINTS

- 4.2.2.1 Increasing use of alternatives for nuclear energy

- 4.2.2.2 Cybersecurity threats to networked radiation monitoring infrastructure

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Technological advancements in radiation detection

- 4.2.3.2 Rising focus on nuclear power in developing countries

- 4.2.4 CHALLENGES

- 4.2.4.1 High cost of lead for manufacturing radiation safety products

- 4.2.4.2 Shortage of workforce and skilled professionals in nuclear power industry

- 4.2.1 DRIVERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL RADIATION INDUSTRY

- 5.2.4 TRENDS IN GLOBAL RADIATION DETECTION, MONITORING, AND SAFETY INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL

- 5.3.2 MANUFACTURING

- 5.3.3 SALES & DISTRIBUTION

- 5.3.4 APPLICATIONS

- 5.4 VALUE CHAIN ANALYSIS

- 5.4.1 RESEARCH & DEVELOPMENT

- 5.4.2 RAW MATERIAL PROCUREMENT

- 5.4.3 MANUFACTURING

- 5.4.4 DISTRIBUTION

- 5.4.5 MARKETING & SALES

- 5.4.6 POST-SALE SERVICES

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE, BY KEY PLAYER

- 5.7 TRADE ANALYSIS

- 5.8 KEY CONFERENCES AND EVENTS (2026-2027)

- 5.9 TRENDS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.12 IMPACT OF 2025 US TARIFF

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 KEY TARIFF RATES

- 5.12.4 PRICE IMPACT ANALYSIS

- 5.12.5 IMPACT ON COUNTRY/REGION

- 5.12.5.1 US

- 5.12.5.2 Europe

- 5.12.5.3 Asia Pacific

- 5.12.6 IMPACT ON END USERS

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Gas detectors

- 6.1.1.2 X-ray radiation detectors

- 6.1.1.3 Scintillators

- 6.1.1.4 Cyclotrons

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Multi-sensor integration technology

- 6.1.2.2 Cloud computing

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Nanotechnology in radiation detection & protection

- 6.1.1 KEY TECHNOLOGIES

- 6.2 PATENT ANALYSIS

- 6.3 IMPACT OF AI ON RADIATION DETECTION, MONITORING, AND SAFETY MARKET

- 6.3.1 TOP USE CASES AND MARKET POTENTIAL

- 6.3.2 BEST PRACTICES IN RADIATION DETECTION, MONITORING, AND SAFETY MARKET

- 6.3.3 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.3.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN RADIATION DETECTION, MONITORING, AND SAFETY

- 6.4 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGULATORY ANALYSIS

- 7.1.1 REGULATORY LANDSCAPE

- 7.1.1.1 North America

- 7.1.1.1.1 US

- 7.1.1.1.2 Canada

- 7.1.1.2 Europe

- 7.1.1.3 Asia Pacific

- 7.1.1.3.1 China

- 7.1.1.3.2 Japan

- 7.1.1.3.3 India

- 7.1.1.4 Latin America

- 7.1.1.4.1 Brazil

- 7.1.1.4.2 Mexico

- 7.1.1.5 Middle East

- 7.1.1.6 Africa

- 7.1.1.1 North America

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.1 REGULATORY LANDSCAPE

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 8.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.5 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

9 RADIATION DETECTION, MONITORING, AND SAFETY MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 RADIATION DETECTION AND MONITORING PRODUCTS

- 9.2.1 PERSONAL DOSIMETERS

- 9.2.1.1 Increasing focus on worker radiation protection boosting market growth

- 9.2.1.2 Passive dosimeters

- 9.2.1.2.1 Increasing use of passive dosimeters driving market expansion

- 9.2.1.3 Active dosimeters

- 9.2.1.3.1 Growing demand for real-time radiation monitoring drives active dosimeter adoption

- 9.2.2 AREA MONITORS

- 9.2.2.1 Development of technologically advanced products at lower costs to propel market growth

- 9.2.3 ENVIRONMENTAL RADIATION MONITORS

- 9.2.3.1 Stringent government regulations regarding radiation exposure to propel market growth

- 9.2.4 SURFACE CONTAMINATION MONITORS

- 9.2.4.1 Development of user-friendly, accurate, and portable radiation contamination monitors to drive market growth

- 9.2.1 PERSONAL DOSIMETERS

- 9.3 MATERIAL MONITORS

- 9.3.1 RADIOACTIVE MATERIAL MONITORS

- 9.3.1.1 Increased use of radioisotopes in nuclear medicine to drive market growth

- 9.3.2 OTHER MATERIAL MONITORS

- 9.3.2.1 Development of user-friendly, accurate, and portable radiation contamination monitors to drive market growth

- 9.3.1 RADIOACTIVE MATERIAL MONITORS

- 9.4 RADIATION MONITORING SOFTWARE

- 9.4.1 ACCELERATED ADOPTION OF WEARABLE RADIATION DETECTORS TO STRENGTHEN FRONTLINE RADIOLOGICAL DEFENSE FOR FIRST RESPONDERS DRIVES SEGMENT

10 RADIATION DETECTION, MONITORING, AND SAFETY MARKET, BY COMPOSITION

- 10.1 INTRODUCTION

- 10.2 DETECTORS

- 10.2.1 GAS-FILLED DETECTORS

- 10.2.1.1 Expanding radiation safety requirements drive demand for gas-filled detectors

- 10.2.2 GEIGER-MULLER COUNTER

- 10.2.2.1 Increasing use of personnel monitoring programs driving market expansion

- 10.2.3 IONIZATION CHAMBERS

- 10.2.3.1 Growing demand for real-time radiation monitoring driving active dosimeter adoption

- 10.2.4 PROPORTIONAL COUNTERS

- 10.2.4.1 Growing environmental and reactor monitoring activities drive proportional counter demand

- 10.2.1 GAS-FILLED DETECTORS

- 10.3 SCINTILLATORS

- 10.3.1 STRINGENT RADIATION EXPOSURE REGULATIONS TO PROPEL MARKET GROWTH

- 10.3.2 INORGANIC SCINTILLATORS

- 10.3.2.1 Development of user-friendly, accurate, and portable radiation contamination monitors to drive market growth

- 10.3.3 ORGANIC SCINTILLATORS

- 10.3.3.1 Development of user-friendly, accurate, and portable radiation contamination monitors to drive market growth

- 10.4 SOLID-STATE DETECTORS

- 10.4.1 INCREASED USE OF RADIOISOTOPES IN NUCLEAR MEDICINE TO DRIVE MARKET GROWTH

- 10.4.2 SEMICONDUCTOR DETECTORS

- 10.4.2.1 Development of user-friendly, accurate, and portable radiation contamination monitors to drive market growth

- 10.4.3 DIAMOND DETECTORS

- 10.5 RADIATION PROTECTION PRODUCTS

- 10.5.1 FULL-BODY PROTECTION PRODUCTS

- 10.5.1.1 Growing volume of medical imaging procedures to increase demand

- 10.5.2 FACE PROTECTION PRODUCTS

- 10.5.2.1 Availability of lightweight eyewear for enhanced comfort to drive market

- 10.5.3 HAND SAFETY PRODUCTS

- 10.5.3.1 Lead-free and powder-free gloves to eliminate risk of allergies

- 10.5.4 LEAD APRONS & LEAD-FREE APRONS

- 10.5.4.1 Advanced safety with eco-friendly lead-free radiation aprons to boost segment

- 10.5.5 OTHER RADIATION PROTECTION PRODUCTS

- 10.5.1 FULL-BODY PROTECTION PRODUCTS

- 10.6 RADIATION SHIELDING PRODUCTS

- 10.6.1 LEAD-LINED RADIATION SHIELDING WALLS

- 10.6.1.1 Efficient properties and relatively low prices to drive adoption

- 10.6.2 OTHER RADIATION SHIELDING PRODUCTS

- 10.6.1 LEAD-LINED RADIATION SHIELDING WALLS

11 RADIATION DETECTION, MONITORING, AND SAFETY MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 INDUSTRY

- 11.2.1 NUCLEAR POWER PLANTS

- 11.2.1.1 Increasing focus on worker radiation protection boosts market growth

- 11.2.2 MANUFACTURING

- 11.2.2.1 Increasing use of personnel monitoring programs drives market expansion

- 11.2.3 RADIONUCLEOTIDE

- 11.2.3.1 Growing demand for real-time radiation monitoring drives active dosimeter adoption

- 11.2.1 NUCLEAR POWER PLANTS

- 11.3 SAFETY & SECURITY

- 11.3.1 ENVIRONMENTAL

- 11.3.1.1 Stringent government regulations regarding radiation exposure to propel market growth

- 11.3.2 HOMELAND SECURITY & DEFENSE

- 11.3.2.1 Development of user-friendly, accurate, and portable radiation contamination monitors to drive market growth

- 11.3.1 ENVIRONMENTAL

- 11.4 DIAGNOSTICS & THERAPY

- 11.4.1 RADIOTHERAPY

- 11.4.1.1 Increased use of radioisotopes in nuclear medicine to drive market growth

- 11.4.2 NUCLEAR MEDICINE

- 11.4.2.1 Development of user-friendly, accurate, and portable radiation contamination monitors to drive market growth

- 11.4.1 RADIOTHERAPY

- 11.5 OTHER APPLICATIONS

12 RADIATION DETECTION, MONITORING, AND SAFETY MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Growing applications of nuclear reactors expand market growth

- 12.2.2 CANADA

- 12.2.2.1 Increased awareness of radiation safety to propel market

- 12.2.1 US

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Growing geriatric population and increasing number of radiography procedures to drive market

- 12.3.2 UK

- 12.3.2.1 Enhanced radiation protection through innovation and surveillance to boost market

- 12.3.3 FRANCE

- 12.3.3.1 Integrate radiation protection and nuclear safety under a unified framework

- 12.3.4 ITALY

- 12.3.4.1 Well-established healthcare infrastructure to support market growth

- 12.3.5 SPAIN

- 12.3.5.1 Increasing awareness through conferences, driving market growth

- 12.3.6 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 ASIA PACIFIC

- 12.4.1 CHINA

- 12.4.1.1 Increase in prevalence of chronic diseases and healthcare expenditure

- 12.4.2 JAPAN

- 12.4.2.1 Rising awareness of radiation exposure to drive market

- 12.4.3 INDIA

- 12.4.3.1 Favorable government policies and healthcare infrastructure to support market growth

- 12.4.4 SOUTH KOREA

- 12.4.4.1 Favorable regulations drive market growth

- 12.4.5 AUSTRALIA

- 12.4.5.1 Government-led safety initiatives support market growth

- 12.4.6 REST OF ASIA PACIFIC

- 12.4.1 CHINA

- 12.5 LATIN AMERICA

- 12.5.1 NUCLEAR DEVELOPMENT AND EXPANDING PRIVATE HEALTHCARE SECTOR PROPEL MARKET GROWTH

- 12.5.2 BRAZIL

- 12.5.2.1 Innovation Through Research, Regulatory Modernization, and Nuclear Infrastructure Development

- 12.5.3 MEXICO

- 12.5.3.1 Increasing geriatric population and rising need for cancer treatment to propel market

- 12.5.4 REST OF LATIN AMERICA

- 12.5.4.1 Advancing Radiation Safety in Latin America Through training and Collaboration to drive market

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 GROWING HEALTHCARE INFRASTRUCTURE TO FUEL MARKET GROWTH

- 12.6.2 GCC COUNTRIES

- 12.6.2.1 Advancing Nuclear and Radiological Safety Capabilities in GCC

- 12.6.3 REST OF MIDDLE EAST & AFRICA

- 12.6.3.1 Increasing number of cancer patients to drive market

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER STRATEGY/RIGHT TO WIN

- 13.3 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS

- 13.4 REVENUE ANALYSIS, 2021-2025

- 13.5 MARKET SHARE ANALYSIS, 2025

- 13.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.6.1 STARS

- 13.6.2 EMERGING LEADERS

- 13.6.3 PERVASIVE PLAYERS

- 13.6.4 PARTICIPANTS

- 13.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.6.5.1 Company footprint

- 13.6.5.2 Region footprint

- 13.6.5.3 Product footprint

- 13.6.5.4 Composition footprint

- 13.6.5.5 Application footprint

- 13.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.7.1 PROGRESSIVE COMPANIES

- 13.7.2 RESPONSIVE COMPANIES

- 13.7.3 DYNAMIC COMPANIES

- 13.7.4 STARTING BLOCKS

- 13.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.7.5.1 Detailed list of key startups/SMEs

- 13.7.5.2 Competitive benchmarking of startup/SME players

- 13.8 COMPANY VALUATION & FINANCIAL METRICS

- 13.8.1 FINANCIAL METRICS

- 13.8.2 COMPANY VALUATION

- 13.9 BRAND/PRODUCT COMPARISON

- 13.10 COMPETITIVE SCENARIO

- 13.10.1 PRODUCT LAUNCHES

- 13.10.2 DEALS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 THERMO FISHER SCIENTIFIC INC.

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches & approvals

- 14.1.1.3.2 Other developments

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 MIRION TECHNOLOGIES INC.

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches & approvals

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Other developments

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 FORTIVE

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 MnM view

- 14.1.3.3.1 Right to win

- 14.1.3.3.2 Strategic choices

- 14.1.3.3.3 Weaknesses and competitive threats

- 14.1.4 AMETEK INC.

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches & approvals

- 14.1.4.3.2 Deals

- 14.1.4.4 MnM view

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 TELEDYNE FLIR

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.2.1 Other developments

- 14.1.6 FUJI ELECTRIC CO., LTD.

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 MnM view

- 14.1.6.3.1 Right to win

- 14.1.6.3.2 Strategic choices

- 14.1.6.3.3 Weaknesses and competitive threats

- 14.1.7 LUDLUM MEASUREMENTS INC.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.2.1 Other developments

- 14.1.8 ARKTIS RADIATION DETECTORS LTD.

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.9 POLIMASTER EUEOPE UAB

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.10 AMRAY

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.11 INFAB LLC

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Product launches & approvals

- 14.1.11.3.2 Deals

- 14.1.12 IBA WORLDWIDE

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.12.3 Recent developments

- 14.1.12.3.1 Deals

- 14.1.13 RADIATION DETECTION COMPANY (RDC)

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.13.3 Recent developments

- 14.1.13.3.1 Deals

- 14.1.13.3.2 Other developments

- 14.1.14 BERTIN TECHNOLOGIES

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.15 ATOMEX

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.1 THERMO FISHER SCIENTIFIC INC.

- 14.2 OTHER PLAYERS

- 14.2.1 ARROW-TECH, INC.

- 14.2.2 S.E. INTERNATIONAL, INC.

- 14.2.3 NUCLEONIX SYSTEMS

- 14.2.4 ALPHA SPECTRA, INC.

- 14.2.5 LND, INC.

- 14.2.6 RAY-BAR ENGINEERING CORP

- 14.2.7 TRIVITRON HEALTHCARE

- 14.2.8 MICRON SEMICONDUCTOR LTD.

- 14.2.9 SCIONIX HOLLAND B.V.

- 14.2.10 RADCOMM SYSTEMS

- 14.2.11 XENA SHIELD

- 14.2.12 SIMAD SRL

- 14.2.13 BURLINGTON MEDICAL

- 14.2.14 RADIATION PROTECTION PRODUCTS INC.

- 14.2.15 NUCLEAR SHIELDS

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key sources of secondary data

- 15.1.1.2 Objectives of secondary research

- 15.1.1.3 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key primary sources

- 15.1.2.2 Key objectives of primary research

- 15.1.2.3 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH (REVENUE SHARE ANALYSIS)

- 15.2.1.1 Company revenue estimation approach

- 15.2.1.2 Customer-based market estimation

- 15.2.2 TOP-DOWN APPROACH

- 15.2.1 BOTTOM-UP APPROACH (REVENUE SHARE ANALYSIS)

- 15.3 DATA TRIANGULATION

- 15.4 MARKET SHARE ASSESSMENT

- 15.5 STUDY ASSUMPTIONS

- 15.5.1 MARKET ASSUMPTIONS

- 15.5.2 GROWTH RATE ASSUMPTIONS

- 15.6 RESEARCH LIMITATIONS

- 15.7 RISK ANALYSIS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS