|

시장보고서

상품코드

2074463

전자전 시장 : 제공 제품별, 플랫폼별, 지출별, 능력별, 지역별 - 예측(-2031년)Electronic Warfare Market by Offering (Receivers, Jammers, Anti-Jam Systems, EW Suites, Software), Capability (Electronic Support, Attack, and Protection), Spending (RDT&E, Procurement), Platform, and Region - Global Forecast to 2031 |

||||||

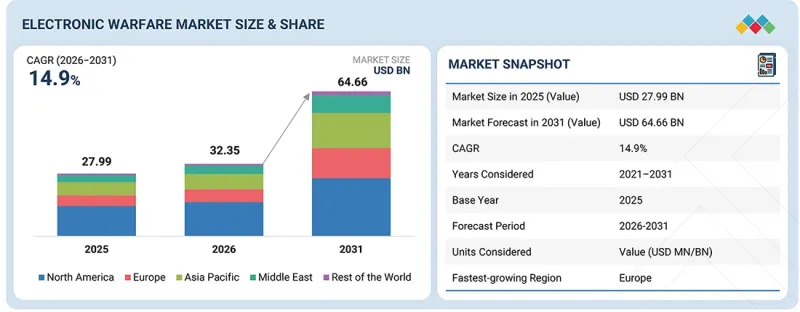

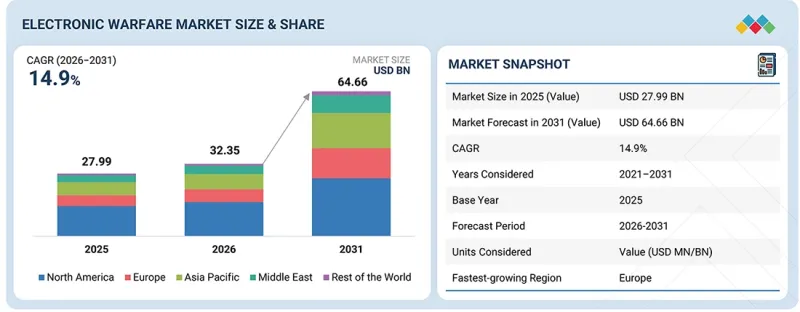

전자전(EW) 시장 규모는 2026년에 323억 5,000만 달러 라고 추계되고 있어 예측 기간 중에 CAGR 14.9%로 확대되어 2031년에는 646억 6,000만 달러에 이를 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(10억 달러) |

| 부문 | 제공 제품별, 플랫폼별, 지출별, 능력별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

운영상의 민첩성과 주파수 대역에 대한 상황 인식을 향상시키기 위한 소프트웨어 정의 시스템, 인공지능, 신호 처리, 적응형 방해 기술, 그리고 사이버·전자기 통합 분야의 지속적인 발전이 시장의 주요 성장 동력이 되고 있습니다.

예측 기간 동안, 플랫폼별로는 지상 부문이 전자전 시장을 주도할 것으로 전망됩니다.

차량 탑재형 유닛, 고정 설치형 시스템, 이동식 쉘터, 무인항공기(UAS) 대응 기술, 즉석 폭발 장치(IED) 대응 전자전, 그리고 보병용 시스템을 포함한 현대의 지상 전자전 시스템은 신호 감청, 전자·통신 정보, 교란 기술, 지상 감시, 무선 주파수(RF) 대책, 지휘통제(C2) 지원과 같은 고도의 기능을 점점 더 많이 활용하고 있습니다. 이러한 통합 시스템은 위협 감지, 전장 상황 인식, 안정적인 통신 유지, 그리고 전자전이 벌어지는 환경에서 작전 지속성을 확보하는 데 필수적입니다. 또한, 이러한 시스템은 인근 위협에 대한 인식을 제고하고, 전술 부대를 신호 차단으로부터 보호하며, 작전 임무 전반에 걸쳐 병사, 차량, 드론 및 C2 시스템 간의 협력을 촉진합니다.

예측 기간 동안 조달 분야가 지출의 대부분을 차지할 것으로 예측됩니다.

방위 기관은 표적형 조달 이니셔티브를 통해 중요한 전자 지원 조치, 교란 시스템, 신호 정보 수집 장비, 대드론 기술, 주파수 대역 관리 도구, 그리고 진화하는 전자기 위협에 대응하기 위해 맞춤화된 종합적인 전자전(EW) 솔루션을 확보하고 있습니다. 군에서 노후화된 시스템의 현대화, 여러 분야에 걸친 전자전 능력의 확대, 그리고 최첨단 전자전 기능을 신규 조달 장비와 기존 플랫폼 모두에 통합하기 위해 노력함에 따라, 이 부문의 중요성은 더욱 커지고 있습니다. 네트워크 중심의 전쟁, 다중 영역 작전, 그리고 능력의 신속한 전개가 점점 더 중요시되는 가운데, 각국 정부는 보다 기동적인 조달 전략을 채택하고 있습니다. 이러한 강화된 접근 방식을 통해 신속한 조달 절차, 원활한 시스템 통합, 그리고 향후 확장성이 뛰어난 업그레이드가 가능해지며, 군이 새로운 과제에 직면하더라도 경쟁 우위를 유지할 수 있게 됩니다.

예측 기간 동안 전자전 시장에서 유럽이 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다.

유럽은 전자전 시장에서 가장 빠르게 성장하고 있는 지역이며, 그 주된 요인은 국방비 증가, 진행 중인 군사 현대화 프로그램, 그리고 국방 역량에 대한 중요성이 커지고 있기 때문입니다. 유럽 각국은 작전 준비 태세 강화, 전파 스펙트럼 지배력 향상, 그리고 다영역 군사 작전 실현을 목적으로 첨단 전자전 시스템에 대한 투자를 확대되고 있습니다. 전자 공격, 전자 방어 및 전자 지원 기능에 중점을 둔 차세대 방위 기술에 대한 자금 지원이 급증하고 있습니다. 육상, 항공, 해상, 무인 등 다양한 플랫폼에 걸친 전자전 시스템의 통합이 진행되고 있는 것이 시장 확대를 크게 견인하고 있습니다. 또한, 지역 안보 강화와 동맹군 간의 군사적 상호운용성 향상에 대한 관심이 높아지고 있는 점도 이러한 추세를 이끄는 중요한 요인입니다.

조사 범위:

본 시장 조사는 전자전 시장의 다양한 부문 및 하위 부문을 대상으로 합니다. 본 조사는 각 지역별 해당 시장 규모와 성장 가능성을 추정하는 것을 목적으로 합니다. 또한, 시장 내 주요 기업에 대한 상세한 경쟁 분석, 기업 프로파일, 제품 및 사업 제공과 관련된 주요 관찰 사항, 최근 동향, 그리고 각 기업이 채택한 주요 시장 전략에 대해서도 다루고 있습니다.

이 보고서를 구매해야 하는 이유:

본 보고서는 시장을 선도하는 기업 및 신규 진출기업을 대상으로, 전자전 시장 전체의 매출액에 관한 가장 정확한 추정치를 제공합니다. 또한, 이해관계자들이 경쟁 구도를 이해하고, 자사의 비즈니스를 더 나은 위치로 이끌며, 적절한 시장 진출 전략을 수립하는 데 필요한 추가적인 인사이트를 얻는 데 도움이 됩니다. 또한, 본 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움이 되며, 주요 시장 성장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다.

- 시장 성장 촉진요인(전자기 스펙트럼의 제어 및 보호, 국방력의 현대화, 전자전 플랫폼의 업그레이드에 중점을 두고 있음), 억제요인(높은 개발·통합 비용, 조달 및 인증까지의 긴 기간), 기회(소프트웨어 정의형 및 AI 탑재 전자전 시스템, 휴대형 및 전술적 대드론 전자전 시스템), 과제(급변하는 신호 및 위협 환경, 사이버 보안 및 전자전 네트워크 보호)

- 시장 침투도 : 시장을 선도하는 주요 기업들이 제공하는 전자전 시스템 및 솔루션에 대한 종합적인 정보

- 제품 개발 및 혁신 : 전자전 시장의 향후 기술, 연구개발 활동 및 제품 출시에 관한 상세한 인사이트

- 시장 개발: 다양한 지역의 수익성이 높은 시장에 대한 종합적인 정보

- 시장의 다양화: 전자전 시장의 신제품, 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁사 분석 : 전자전 시장에서 주요 기업의 시장 점유율, 성장 전략, 제품 및 생산 능력에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황

제8장 고객 현황과 구매 행동

제9장 전자전 시장(제공 제품별)

제10장 전자전 시장(플랫폼별)

제11장 전자전 시장(지출 별)

제12장 전자전 시장(능력별)

제13장 전자전 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

LSH 26.07.07The electronic warfare (EW) market is estimated at USD 32.35 billion in 2026 and is projected to reach USD 64.66 billion by 2031 at a CAGR of 14.9% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) |

| Segments | By Offering, Capability and Region |

| Regions covered | North America, Europe, APAC, RoW |

Ongoing advancements in software-defined systems, artificial intelligence, signal processing, adaptive jamming technologies, and cyber-electromagnetic integration to enhance operational agility and spectrum situational awareness are among the key drivers of the market.

The land segment is projected to lead the electronic warfare market by platform during the forecast period.

Modern land EW systems, encompassing vehicle-mounted units, fixed-installation setups, mobile shelters, counter-unmanned aerial system (UAS) technologies, counter-improvised explosive device (IED) EW, and dismounted soldier systems, are increasingly leveraging advanced capabilities such as signal interception, electronic and communication intelligence, jamming techniques, ground surveillance, radio frequency (RF) countermeasures, and command-and-control (C2) support. These integrated systems are essential for threat detection, situational awareness on the battlefield, maintaining robust communications, and ensuring operational continuity in environments contested by electronic warfare. Moreover, they enhance awareness of proximate threats, safeguard tactical units against signal interruptions, and facilitate improved coordination among soldiers, vehicles, drones, and C2 systems throughout operational missions.

Procurement is projected to be the dominant spending segment during the forecast period.

Through targeted procurement initiatives, defense organizations acquire critical electronic support measures, jamming systems, signal intelligence equipment, counter-drone technologies, spectrum management tools, and holistic EW suites tailored to counteract evolving electromagnetic threats. The importance of this segment is amplified as military forces strive to modernize aging systems, expand EW capabilities across multiple domains, and integrate state-of-the-art EW functionality into both new acquisitions and legacy platforms. The increasing emphasis on network-centric warfare, multi-domain operations, and expedited capability deployment is prompting governments to adopt more agile procurement strategies. These enhanced approaches facilitate rapid acquisition processes, seamless system integration, and scalable future upgrades, ensuring that military forces maintain a competitive edge in the face of emerging challenges.

Europe is projected to register the highest CAGR in the electronic warfare market during the forecast period.

Europe is the fastest-growing electronic warfare market, mostly driven by increased defense spending, ongoing military modernization programs, and a growing emphasis on defense capabilities. European countries are increasingly investing in advanced EW systems to bolster operational readiness, enhance spectrum dominance, and enable multi-domain military operations. There is a surge in funding for next-generation defense technologies focused on electronic attack, electronic protection, and electronic support functions. The enhanced integration of EW systems across diverse platforms-land, airborne, naval, and unmanned-is significantly driving market expansion. In addition, the growing emphasis on fortifying regional security and enhancing military interoperability among allied forces is a critical driver of this trend.

The breakdown of profiles for primary participants in the electronic warfare market is provided below:

- By Company Type: Tier 1 - 30%, Tier 2 - 45%, and Tier 3 - 25%

- By Designation: C-Level - 20%, Director-Level - 10%, and Others -70%

- By Region: North America - 40%, Europe - 20%, Asia Pacific - 20%, Middle East - 10%, and Rest of the World - 10%

Research Coverage:

This market study covers the electronic warfare market across various segments and subsegments. It aims to estimate the size and growth potential of this market across different regions. This study also includes an in-depth competitive analysis of the key players in the market, their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies they adopted.

Reasons to Buy This Report:

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall electronic warfare market. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report will also help stakeholders understand the market pulse and will provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Market drivers (focus on electromagnetic spectrum control and protection, defense modernization and EW platform upgrades), restraints (high development and integration costs, long procurement and certification timelines), opportunities (software-defined and AI-enabled EW systems, portable and tactical counter-drone EW systems), challenges (fast-changing signal and threat environments, Cybersecurity and protection of EW networks)

- Market Penetration: Comprehensive information on electronic warfare systems and solutions offered by the top players in the market

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the electronic warfare market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the electronic warfare market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the electronic warfare market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 HIGH-GROWTH SEGMENTS

- 2.4 DISRUPTIVE TRENDS SHAPING MARKET

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ELECTRONIC WARFARE MARKET

- 3.2 ELECTRONIC WARFARE MARKET, BY OFFERING

- 3.3 ELECTRONIC WARFARE MARKET, BY SPENDING

- 3.4 ELECTRONIC WARFARE MARKET, BY PLATFORM

- 3.5 ELECTRONIC WARFARE MARKET, BY CAPABILITY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Focus on electromagnetic spectrum control and protection

- 4.2.1.2 Defense modernization and EW platform upgrades

- 4.2.1.3 Rising drone and unmanned system threats

- 4.2.2 RESTRAINTS

- 4.2.2.1 High development and integration costs

- 4.2.2.2 Long procurement and certification timelines

- 4.2.2.3 Export control and technology transfer restrictions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Software-defined and AI-enabled EW systems

- 4.2.3.2 Portable and tactical counter-drone EW systems

- 4.2.3.3 Integration of EW into multi-domain operations

- 4.2.4 CHALLENGES

- 4.2.4.1 Fast-changing signal and threat environments

- 4.2.4.2 Cybersecurity and protection of EW networks

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 ADAPTIVE AND RAPIDLY UPDATABLE EW CAPABILITIES

- 4.3.2 INTEROPERABILITY AND MULTI-DOMAIN EW INTEGRATION

- 4.3.3 MINIATURIZED AND SCALABLE EW FOR DISTRIBUTED OPERATIONS

- 4.3.4 SECURE, RESILIENT, AND AFFORDABLE EW DEPLOYMENT

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 MILITARY COMMUNICATION MARKET

- 4.4.2 RADAR SYSTEM MARKET

- 4.4.3 CYBER WARFARE AND CYBERSECURITY MARKET

- 4.4.4 SIGNALS INTELLIGENCE MARKET

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 ECOSYSTEM ANALYSIS

- 5.1.1 PROMINENT COMPANIES

- 5.1.2 PRIVATE AND SMALL ENTERPRISES

- 5.1.3 END USERS

- 5.2 VALUE CHAIN ANALYSIS

- 5.3 TRADE ANALYSIS

- 5.3.1 IMPORT SCENARIO (HS CODE 8526)

- 5.3.2 EXPORT SCENARIO (HS CODE 8526)

- 5.4 CASE STUDY ANALYSIS

- 5.4.1 ELECTRONIC ATTACK OPERATIONS USING EA-18 G GROWLER AGAINST INTEGRATED AIR DEFENSE SYSTEMS

- 5.4.2 EA-37B COMPASS CALL FOR LONG-RANGE ELECTROMAGNETIC DISRUPTION

- 5.4.3 STAND-IN JAMMING UAVS FOR CLOSE-RANGE RADAR DISRUPTION

- 5.4.4 KALAETRON ATTACK STAND-IN JAMMER FOR TACTICAL ELECTRONIC ATTACK

- 5.4.5 AN/ASQ-239 EW SUITE FOR F-35 OPERATIONS IN CONTESTED ENVIRONMENTS

- 5.4.6 SELF-PROTECTION POD FOR MISSILE THREAT DETECTION AND COUNTERMEASURES

- 5.4.7 JOINT COUNTER RADIO-CONTROLLED IMPROVISED EXPLOSIVE DEVICE EW FOR FORCE PROTECTION

- 5.4.8 EGON FLX GROUND EW FOR FIELD FORCE PROTECTION OPERATIONS

- 5.4.9 MALD-J DECOY FOR JAMMING AND DECEPTION IN CONTESTED AIRSPACE

- 5.4.10 SPEAR-EW FOR IMPROVED EW REACH DURING SUPPRESSION MISSIONS

- 5.5 KEY CONFERENCES AND EVENTS, 2026

- 5.6 INVESTMENT AND FUNDING SCENARIO

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 MACROECONOMIC OUTLOOK

- 5.8.1 GDP TRENDS AND FORECAST

- 5.8.2 TRENDS IN GLOBAL EW INDUSTRY

- 5.8.3 TRENDS IN GLOBAL DEFENSE INDUSTRY

- 5.9 PRICING ANALYSIS

- 5.9.1 INDICATIVE PRICING ANALYSIS, BY OFFERING, 2025

- 5.9.2 INDICATIVE PRICING ANALYSIS, BY PLATFORM, 2025

- 5.10 BILL OF MATERIALS

- 5.11 TOTAL COST OF OWNERSHIP

- 5.12 BUSINESS MODELS

- 5.12.1 PROGRAM-BASED CONTRACTING MODEL

- 5.12.2 PLATFORM INTEGRATION MODEL

- 5.12.3 LIFECYCLE SUPPORT AND SUSTAINMENT MODEL

- 5.12.4 UPGRADE AND MODERNIZATION MODEL

- 5.12.5 PRODUCT AND SUBSYSTEM SUPPLIER MODEL

- 5.12.6 MISSION SERVICES, TRAINING, AND TEST SUPPORT MODEL

- 5.12.7 MODULAR/OPEN ARCHITECTURE MODEL

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 RF SENSING AND RECEIVER TECHNOLOGIES

- 6.1.2 ELECTRONIC ATTACK AND COUNTERMEASURE TECHNOLOGIES

- 6.1.3 ELECTRONIC PROTECTION AND SPECTRUM RESILIENCE TECHNOLOGIES

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ARTIFICIAL INTELLIGENCE AND MACHINE LEARNING

- 6.2.2 ADVANCED ANTENNA AND BEAM-STEERING TECHNOLOGIES

- 6.2.3 HIGH-PERFORMANCE COMPUTING AND DIGITAL PROCESSING TECHNOLOGIES

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 CYBER-ELECTROMAGNETIC TECHNOLOGIES

- 6.3.2 AUTONOMOUS AND UNMANNED SYSTEMS TECHNOLOGIES

- 6.4 TECHNOLOGY ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI/GEN AI

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 CASE STUDIES OF AI IMPLEMENTATION

- 6.6.3 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.4 CLIENTS' READINESS TO ADOPT AI/GEN AI

- 6.6.5 FUTURE APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF END-USE PLATFORMS

9 ELECTRONIC WARFARE MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.2 CLASSIFICATION OF EW OFFERINGS BASED ON TECHNOLOGY ENABLERS: TOP USE CASES

- 9.2.1 RF & MICROWAVE TECHNOLOGIES

- 9.2.1.1 Teledyne Technologies' Integrated Microwave Assemblies (IMAs) Support RF Functions in EW Systems

- 9.2.1.2 Amphenol RF Connectors and Interconnect Solutions Support Reliable EW Communications

- 9.2.2 EO/IR COUNTERMEASURE TECHNOLOGIES

- 9.2.2.1 Northrop Grumman's CIRCM and IRCM Systems Improve Aircraft Survivability

- 9.2.2.2 BAE Systems AN/AAR-57 CMWS Enhances Missile Warning and Countermeasure Response

- 9.2.3 DIGITAL SIGNAL PROCESSING AND SOFTWARE-DEFINED EW

- 9.2.3.1 Tektronix RSA7100B Enables Real-Time RF Signal Capture for EW Applications

- 9.2.3.2 Curtiss-Wright's SDR and Electronic Warfare System Enable Software-Defined EW Operations

- 9.2.4 AI-ENABLED AND COGNITIVE EW

- 9.2.4.1 BAE Systems Anti-Threat System (BATS) Enhances AI-Based Counter-Drone Threat Detection

- 9.2.4.2 HII's Cognitive Electronic Warfare Solution Improves AI-Driven RF Threat Detection and Analysis

- 9.2.5 CYBER-ELECTROMAGNETIC ACTIVITIES INTEGRATION

- 9.2.5.1 BAE Systems Cyber and Electromagnetic Activities (CEMA) Solution Integrates Cyber and EW Operations

- 9.2.5.2 Leonardo's CEMA Capabilities Support Protection Against Evolving Wireless Threats

- 9.2.6 EW MODELING, SIMULATION, & DIGITAL TESTING

- 9.2.6.1 SRC's NEWEG and DGEN Systems Support EW Threat Modeling and Simulation

- 9.2.6.2 BAE Systems Electronic Warfare Modeling Capability Supports Virtual Assessment of EW Systems

- 9.2.1 RF & MICROWAVE TECHNOLOGIES

- 9.3 RECEIVERS & SENSING SYSTEMS

- 9.3.1 PASSIVE THREAT DETECTION AND ELECTROMAGNETIC AWARENESS TO DRIVE MARKET

- 9.3.2 RADAR WARNING RECEIVERS

- 9.3.3 ELECTRONIC SUPPORT MEASURES SYSTEMS

- 9.3.4 ELECTRONIC INTELLIGENCE SYSTEMS

- 9.3.5 DIRECTION-FINDING & GEOLOCATION SYSTEMS

- 9.3.6 SPECTRUM MONITORING & EMS SENSING SYSTEMS

- 9.3.7 MULTI-THREAT WARNING SENSOR SYSTEMS

- 9.4 JAMMERS

- 9.4.1 SHIFT TOWARD WIDER SPECTRUM CONTROL AND COUNTER-DRONE CAPABILITY TO DRIVE MARKET

- 9.4.2 RADAR JAMMERS

- 9.4.2.1 Electronic jammers

- 9.4.2.2 Mechanical jammers

- 9.4.3 COMMUNICATION & SATCOM JAMMERS

- 9.4.4 RCIED JAMMERS

- 9.4.5 GNSS/PNT JAMMERS & SPOOFERS

- 9.4.6 DATALINK & DRONE-LINK JAMMERS

- 9.5 SELF-PROTECTION & COUNTERMEASURE SYSTEMS

- 9.5.1 GROWING REQUIREMENT TO IMPROVE PLATFORM SURVIVABILITY TO DRIVE MARKET

- 9.5.2 COUNTERMEASURE DISPENSING SYSTEMS

- 9.5.2.1 Chaff dispensing systems

- 9.5.2.2 Flare dispensing systems

- 9.5.2.3 Combined chaff/flare dispensing systems

- 9.5.3 TOWED DECOYS

- 9.5.3.1 Expendable RF towed decoys

- 9.5.3.2 Fiber-optic/Controlled RF towed decoys

- 9.5.4 DIRECTED INFRARED COUNTERMEASURE SYSTEMS

- 9.5.5 INTEGRATED SELF-PROTECTION SUITES

- 9.5.6 NAVAL SELF-PROTECTION SUITES

- 9.6 ANTI-JAM & SPECTRUM RESILIENCE SYSTEMS

- 9.6.1 SMOOTH FUNCTIONING OF COMMUNICATION AND NAVIGATION DURING ELECTRONIC ATTACKS TO DRIVE MARKET

- 9.6.2 ANTI-JAM GNSS/PNT SYSTEMS

- 9.6.3 PROTECTED COMMUNICATION SYSTEMS

- 9.6.4 RESILIENT TACTICAL DATALINKS

- 9.6.5 FREQUENCY-AGILE & SPREAD-SPECTRUM WAVEFORM SYSTEMS

- 9.6.6 ELECTRONIC COUNTER-COUNTERMEASURE & INTERFERENCE MITIGATION SYSTEMS

- 9.6.7 EMISSION CONTROL SYSTEMS

- 9.7 EW PODS, PAYLOADS, & MISSION SUITES

- 9.7.1 SURGE IN DEMAND FOR FLEXIBLE AND MISSION-SPECIFIC ELECTRONIC WARFARE CAPABILITY TO DRIVE MARKET

- 9.7.2 AIRBORNE EW PODS

- 9.7.3 UAV EW PAYLOADS

- 9.7.4 SHIPBORNE EW MISSION SUITES

- 9.7.5 VEHICLE-MOUNTED EW KITS

- 9.7.6 MODULAR EW MISSION PACKAGES

- 9.7.7 MULTI-FUNCTION EW SUITES

- 9.8 SOFTWARE

- 9.8.1 GROWING NEED FOR FASTER DECISION-MAKING AND BETTER THREAT UNDERSTANDING TO DRIVE MARKET

- 9.8.2 SIGNAL PROCESSING & EMITTER IDENTIFICATION SOFTWARE

- 9.8.3 COGNITIVE & ADAPTIVE EW SOFTWARE

- 9.8.4 EW MISSION PLANNING SOFTWARE

- 9.8.5 EMSO BATTLE MANAGEMENT SOFTWARE

- 9.8.6 EW MODELING, SIMULATION, & TEST SOFTWARE

- 9.9 SERVICES

- 9.9.1 FOCUS ON MAINTAINING READINESS AND SYSTEM PERFORMANCE TO DRIVE MARKET

- 9.9.2 INTEGRATION & INSTALLATION

- 9.9.3 TESTING, CALIBRATION, & CERTIFICATION

- 9.9.4 MAINTENANCE, REPAIR, & OVERHAUL

- 9.9.5 MISSION DATA REPROGRAMMING & THREAT LIBRARY SUPPORT

- 9.9.6 TRAINING, SIMULATION, & RANGE SUPPORT

10 ELECTRONIC WARFARE MARKET, BY PLATFORM

- 10.1 INTRODUCTION

- 10.2 CLASSIFICATION OF EW PLATFORMS BASED ON MISSION USE: TOP USE CASES

- 10.2.1 PLATFORM SELF-PROTECTION

- 10.2.1.1 Leonardo's Miysis DIRCM Protects Aircraft Against Infrared-Guided Missile Threats

- 10.2.1.2 Leonardo-Led Praetorian DASS Enhances Eurofighter Typhoon Self-Protection Capabilities

- 10.2.2 THREAT DETECTION & SPECTRUM AWARENESS

- 10.2.2.1 BAE Systems AN/AAR-57 CMWS Improves Aircraft Missile Warning and Survivability

- 10.2.2.2 HENSOLDT's SkyLark-N ESM System Strengthens Maritime Threat Detection and Spectrum Awareness

- 10.2.3 COMMUNICATIONS & RADAR DENIAL

- 10.2.3.1 Leonardo's CoDeSS Enables Communication Denial and Electronic Attack Operations

- 10.2.3.2 Shoghi's Communication and GPS Jammers Support Tactical Spectrum Denial Missions

- 10.2.4 SEAD/DEAD SUPPORT

- 10.2.4.1 Northrop Grumman's AARGM-ER Supports Long-Range Suppression of Enemy Air Defenses

- 10.2.4.2 HAVA SOJ Extends Stand-Off Electronic Attack Against Air-Defense Networks

- 10.2.5 CYBER-ELECTROMAGNETIC ACTIVITIES

- 10.2.5.1 BAE Systems CEMA Integration Framework Synchronizes Cyber and EW Operations

- 10.2.5.2 Thales CEMA Solution Integrates Cyber and Electromagnetic Operations

- 10.2.6 NAVIGATION & COMMUNICATIONS RESILIENCE

- 10.2.6.1 Safran's Skydel NAVWAR Strengthens Navigation Warfare and PNT Protection

- 10.2.6.2 STM's EW-Resilient Communication Solution Sustains UAV Connectivity in Contested Environments

- 10.2.1 PLATFORM SELF-PROTECTION

- 10.3 AIRBORNE

- 10.3.1 LONGER STAND-OFF MISSIONS AND OPERATIONS NEAR ADVANCED AIR DEFENSE SYSTEMS TO DRIVE MARKET

- 10.3.2 COMBAT AIRCRAFT

- 10.3.3 TRANSPORT & UTILITY AIRCRAFT

- 10.3.4 SPECIAL MISSION AIRCRAFT

- 10.3.5 MILITARY HELICOPTERS

- 10.4 LAND

- 10.4.1 IMPROVED BATTLEFIELD AWARENESS AND FORCE PROTECTION TO DRIVE MARKET

- 10.4.2 VEHICLE-MOUNTED

- 10.4.2.1 Infantry fighting vehicles

- 10.4.2.2 Armored personnel carriers

- 10.4.2.3 Main battle tanks

- 10.4.3 DISMOUNTED SOLDIER SYSTEMS

- 10.4.4 FIXED-SITE/BASE PROTECTION

- 10.4.5 MOBILE GROUND STATIONS & TACTICAL EW SHELTERS

- 10.4.6 COUNTER-IED EW

- 10.4.7 COUNTER-UAS

- 10.5 NAVAL

- 10.5.1 INCREASING INVESTMENTS IN NAVAL FLEET READINESS TO DRIVE MARKET

- 10.5.2 SURFACE VESSELS

- 10.5.2.1 Surface combatants

- 10.5.2.2 Offshore patrol vessels

- 10.5.2.3 Aircraft carriers

- 10.5.3 SUBMARINES

- 10.6 SPACE

- 10.6.1 EMPHASIS ON SPACE-BASED ELECTRONIC PROTECTION AND OPERATIONAL CONTROL TO DRIVE MARKET

- 10.7 UNMANNED/AUTONOMOUS

- 10.7.1 RISE OF AUTONOMOUS OPERATIONS TO DRIVE MARKET

- 10.7.2 UNMANNED AERIAL VEHICLES

- 10.7.3 UNMANNED GROUND VEHICLES

- 10.7.4 UNMANNED MARINE VEHICLES

- 10.7.4.1 Unmanned surface vehicles

- 10.7.4.2 Unmanned underwater vehicles

- 10.8 MULTI-DOMAIN

- 10.8.1 SHIFT TOWARD NETWORKED WARFARE AND DISTRIBUTED OPERATIONS TO DRIVE MARKET

- 10.8.2 JOINT ELECTROMAGNETIC SPECTRUM

- 10.8.3 INTEGRATED AIR-LAND

- 10.8.4 INTEGRATED AIR-SEA

- 10.8.5 INTEGRATED EW-CYBER

11 ELECTRONIC WARFARE MARKET, BY SPENDING

- 11.1 INTRODUCTION

- 11.2 RDT&E

- 11.2.1 CONTINUOUS MODERNIZATION OF ELECTROMAGNETIC CAPABILITIES TO DRIVE MARKET

- 11.3 PROCUREMENT

- 11.3.1 EXPANSION OF ELECTRONIC WARFARE CAPABILITIES ACROSS DEFENSE FORCES TO DRIVE MARKET

- 11.3.2 OEMS

- 11.3.3 UPGRADES

12 ELECTRONIC WARFARE MARKET, BY CAPABILITY

- 12.1 INTRODUCTION

- 12.2 ELECTRONIC SUPPORT

- 12.2.1 HEIGHTENED DEMAND FOR SPECTRUM AWARENESS TO DRIVE MARKET

- 12.2.2 SIGNALS INTELLIGENCE

- 12.2.2.1 Electronic intelligence

- 12.2.2.2 Communication intelligence

- 12.3 ELECTRONIC ATTACK

- 12.3.1 INCREASED DEPENDENCE ON ELECTRONIC SYSTEMS TO DRIVE MARKET

- 12.3.2 ACTIVE ELECTRONIC ATTACK

- 12.3.3 PASSIVE ELECTRONIC ATTACK

- 12.4 ELECTRONIC PROTECTION

- 12.4.1 NEED TO MAINTAIN RELIABLE OPERATIONS UNDER ELECTRONIC THREATS TO DRIVE MARKET

- 12.4.2 ANTI-ACTIVE ELECTRONIC PROTECTION

- 12.4.3 ANTI-PASSIVE ELECTRONIC PROTECTION

13 ELECTRONIC WARFARE MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Modernization and military platform upgrades to drive market

- 13.2.2 CANADA

- 13.2.2.1 Arctic surveillance and allied defense coordination to drive market

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 FRANCE

- 13.3.1.1 Combat aircraft capability expansion and domestic defense systems to drive market

- 13.3.2 GERMANY

- 13.3.2.1 NATO defense preparedness and tactical force readiness to drive market

- 13.3.3 UK

- 13.3.3.1 Threat response and air mission protection to drive market

- 13.3.4 ITALY

- 13.3.4.1 Maritime defense preparedness and naval platform upgrades to drive market

- 13.3.5 SPAIN

- 13.3.5.1 Defense surveillance improvements and multi-service mission support to drive market

- 13.3.6 POLAND

- 13.3.6.1 Border defense readiness and ground force modernization to drive market

- 13.3.7 REST OF EUROPE

- 13.3.1 FRANCE

- 13.4 ASIA PACIFIC

- 13.4.1 SOUTH KOREA

- 13.4.1.1 Border monitoring and local defense programs to drive market

- 13.4.2 JAPAN

- 13.4.2.1 Airspace monitoring and maritime security to drive market

- 13.4.3 AUSTRALIA

- 13.4.3.1 Long-range surveillance and defense coordination to drive market

- 13.4.4 INDIA

- 13.4.4.1 Border security improvements and domestic defense programs to drive market

- 13.4.5 REST OF ASIA PACIFIC

- 13.4.1 SOUTH KOREA

- 13.5 MIDDLE EAST

- 13.5.1 GCC COUNTRIES

- 13.5.1.1 Saudi Arabia

- 13.5.1.1.1 Defense modernization and air defense programs to drive market

- 13.5.1.2 UAE

- 13.5.1.2.1 Military technology upgrades and integrated defense systems to drive market

- 13.5.1.1 Saudi Arabia

- 13.5.2 ISRAEL

- 13.5.2.1 Real-time threat response and defense technology development to drive market

- 13.5.3 REST OF MIDDLE EAST

- 13.5.1 GCC COUNTRIES

- 13.6 REST OF THE WORLD

- 13.6.1 LATIN AMERICA

- 13.6.1.1 Border monitoring and defense communication improvements to drive market

- 13.6.2 AFRICA

- 13.6.2.1 Border security and military modernization to drive market

- 13.6.1 LATIN AMERICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 14.3 REVENUE ANALYSIS, 2021-2025

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 BRAND/PRODUCT COMPARISON

- 14.6 COMPANY VALUATION AND FINANCIAL METRICS

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Offering footprint

- 14.7.5.4 Platform footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING

- 14.8.5.1 List of startups/SMEs

- 14.8.5.2 Competitive benchmarking of startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 14.9.2 DEALS

- 14.9.3 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 BAE SYSTEMS

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches/developments

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Other developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 RTX

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches/developments

- 15.1.2.3.2 Deals

- 15.1.2.3.3 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 L3HARRIS TECHNOLOGIES, INC.

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.3.2 Other developments

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 THALES

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches/developments

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Other developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 NORTHROP GRUMMAN

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.3.2 Other developments

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 LOCKHEED MARTIN CORPORATION

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Other developments

- 15.1.7 BHARAT ELECTRONICS LIMITED

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.7.3.2 Other developments

- 15.1.8 GENERAL DYNAMICS CORPORATION

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Other developments

- 15.1.9 SAAB AB

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product launches/developments

- 15.1.9.3.2 Deals

- 15.1.9.3.3 Other developments

- 15.1.10 ELBIT SYSTEMS LTD.

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Other developments

- 15.1.11 LEONARDO S.P.A.

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.11.3.2 Other developments

- 15.1.12 ISRAEL AEROSPACE INDUSTRIES

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Deals

- 15.1.12.3.2 Other developments

- 15.1.13 ASELSAN

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product launches/developments

- 15.1.13.3.2 Other developments

- 15.1.14 RAFAEL ADVANCED DEFENSE SYSTEMS LTD.

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Deals

- 15.1.14.3.2 Other developments

- 15.1.15 HENSOLDT AG

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Product launches/developments

- 15.1.15.3.2 Other developments

- 15.1.1 BAE SYSTEMS

- 15.2 OTHER PLAYERS

- 15.2.1 ROHDE & SCHWARZ

- 15.2.2 ELETTRONICA S.P.A.

- 15.2.3 SIERRA NEVADA CORPORATION

- 15.2.4 ANDURIL INDUSTRIES

- 15.2.5 SRC, INC.

- 15.2.6 TERMA

- 15.2.7 DZYNE

- 15.2.8 NETLINE COMMUNICATIONS TECHNOLOGIES

- 15.2.9 EPIRUS INC.

- 15.2.10 PLATH GMBH & CO. KG

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Primary sources

- 16.1.2.2 Key data from primary sources

- 16.1.2.3 Breakdown of primary interviews

- 16.1.1 SECONDARY DATA

- 16.2 FACTOR ANALYSIS

- 16.2.1 DEMAND-SIDE INDICATORS

- 16.2.2 SUPPLY-SIDE INDICATORS

- 16.3 MARKET SIZE ESTIMATION

- 16.3.1 BOTTOM-UP APPROACH

- 16.3.1.1 Market size estimation methodology (demand side)

- 16.3.2 TOP-DOWN APPROACH

- 16.3.1 BOTTOM-UP APPROACH

- 16.4 DATA TRIANGULATION

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 RESEARCH LIMITATIONS

- 16.7 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS