|

시장보고서

상품코드

2076881

방사선 치료 시장 : 기술별, 치료법별, 암 유형별, 최종사용자별 - 세계 예측(-2031년)Radiotherapy Market by Technology, Procedure, Cancer, End User - Global Forecast to 2031 |

||||||

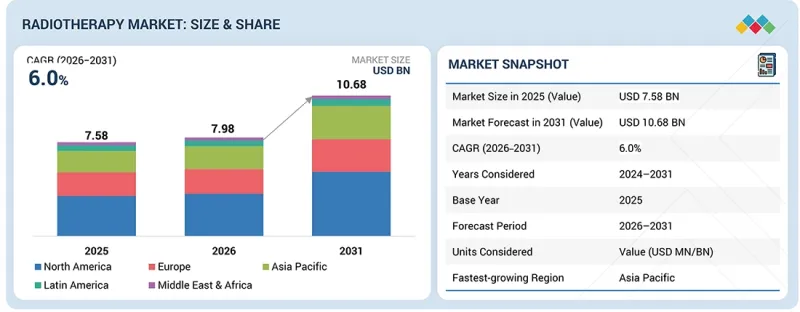

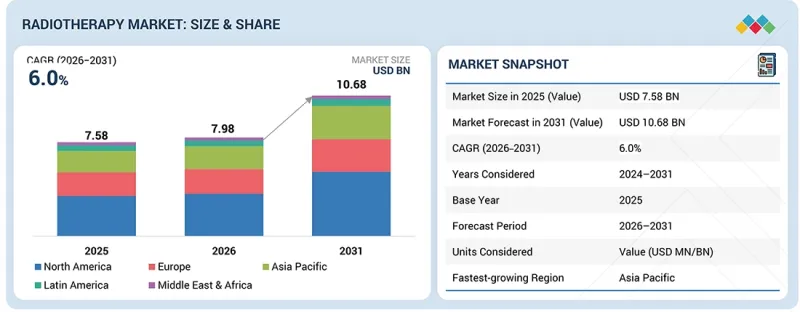

세계의 방사선 치료 시장 규모는 2026년 79억 8,000만 달러에서 2031년에는 106억 8,000만 달러로 확대되어 예측 기간 동안 CAGR은 6.0%에 달할 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 제공, 기술, 용도, 시술, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

방사선 치료 기술의 발전에 힘입어, 향후 몇 년 동안 시장 성장이 크게 가속화될 것으로 예상됩니다. 한편, 방사선 치료 제품은 비용이 높아 시장 확대를 저해할 가능성이 있습니다.

"2025년에는 외부 조사 요법 부문이 시장에서 가장 큰 점유율을 차지했습니다."

기술별로는 외부 조사 요법 부문이 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 이는 주변의 정상 조직에 미치는 방사선 노출을 최소화하면서 종양을 정확하게 표적으로 삼을 수 있기 때문입니다. 이 부문의 성장은 첨단 치료법의 도입 확대와 정밀 의학에 대한 수요 증가에 힘입어 이루어지고 있습니다.

"2025년에는 외부 조사 요법 부문이 시장에서 가장 큰 점유율을 차지할 것으로 전망됩니다."

처치 유형별로 보면 외부 조사 요법 부문이 예측 기간 동안 시장을 주도할 것으로 예상됩니다. 이는 종양을 정확하게 표적으로 삼으면서도 정상 조직에 대한 방사선 피폭을 최소화할 수 있는 높은 정밀도 덕분입니다. 또한, 외부 방사선 치료는 암 치료에 널리 사용되고 있습니다. 영상 유도 방사선 치료 및 강도 변조 방사선 치료 시스템의 기술 혁신이 이 부문의 성장을 더욱 촉진하고 있습니다.

"2025년에는 병원 부문이 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다."

최종사용자별로는 병원 부문이 향후 몇 년간 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 이러한 성장은 환자 수의 증가, 첨단 방사선 치료 기기의 보급, 병원 내 종합 암 치료 시설에 대한 수요 증가 등 여러 요인에 기인한 것으로 보입니다. 또한, 개발도상국에서의 병원 확충, 의료 인프라에 대한 투자, 숙련된 종양 전문의 확보가 이 부문의 성장을 더욱 촉진할 것입니다.

"아시아태평양 시장은 예측 기간 동안 가장 높은 성장률을 기록할 것으로 예상됩니다."

미국은 확립된 의료 인프라, 첨단 방사선 치료 장비, 유리한 보험 환급 정책, 주요 기업의 존재 덕분에 세계 방사선 치료 시장에서 중요한 역할을 하고 있습니다. 한편, 예측 기간 동안 아시아태평양이 가장 높은 성장률을 보일 것으로 예상됩니다. 이러한 성장은 암 발병률의 증가, 의료 분야에 대한 투자 확대, 암 치료 자금 지원 확충, 중국, 인도, 일본 등 국가들의 의료 인프라 구축 진전 등에 의해 주도되고 있으며, 이 모든 요인이 방사선 치료의 보급 확대로 이어지고 있습니다.

본 보고서에서는 전 세계 방사선 치료 시장을 조사하여, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추정 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 현황, 주요 기업 개요 등을 정리하고 있습니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 방사선 치료 시장 : 시스템, 소프트웨어 및 서비스별

제10장 방사선 치료 시장 : 용도별

제11장 방사선 치료 시장 : 시술별

제12장 방사선 치료 시장 : 기술별

제13장 방사선 치료 시장 : 최종사용자별

제14장 방사선 치료 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSMThe global radiotherapy market is expected to grow from USD 7.98 billion in 2026 to USD 10.68 billion by 2031, registering a CAGR of 6.0% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Offering, Technology, Application, Procedure, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

The advancements in radiotherapy technology are expected to significantly boost market growth in the coming years. However, the high costs of radiotherapy products may hinder market expansion.

"The external beam radiotherapy segment held the largest share of the market in 2025."

By technology, the radiotherapy market is categorized into external beam radiotherapy and internal beam radiotherapy/brachytherapy. During the forecast period, the external beam radiotherapy segment is expected to hold the largest market share. This is due to its ability to accurately target tumors while minimizing exposure to surrounding healthy tissue. The growth of this segment is driven by the increasing adoption of advanced procedures and a rising demand for precision medicine.

"The external beam radiotherapy procedures segment is expected to hold the largest share of the market in 2025."

By procedure, the radiotherapy market can be categorized into external beam radiotherapy and internal beam radiotherapy/brachytherapy procedures. The external beam radiotherapy procedures segment is expected to dominate the market during the forecast period. This is due to their accuracy, which allows for precise targeting of tumors while minimizing radiation exposure to healthy tissues. Additionally, external beam radiotherapy is commonly used to treat cancer. Innovations in image-guided and intensity-modulated radiotherapy systems are further driving the growth of this segment.

"The hospital segment is expected to hold the largest share of the market in 2025."

By end user, the radiotherapy market is categorized into hospitals and standalone radiotherapy centers. In the coming years, the hospitals segment is expected to capture the largest share of the global radiotherapy market. This growth can be attributed to several factors, including a high patient volume, the availability of advanced radiotherapy equipment, and the increasing demand for comprehensive cancer treatment facilities within hospitals. Additionally, the expansion of hospitals in developing countries, investments in healthcare infrastructure, and the availability of trained oncologists will further support the growth of this segment.

"The market in the APAC region is expected to register the highest growth rate during the forecast period."

The radiotherapy market is divided into five key regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America plays a significant role in the global radiotherapy market due to its established healthcare infrastructure, advanced radiotherapy equipment, favorable reimbursement policies, and the presence of key market players. However, the Asia Pacific region is expected to experience the highest growth rate during the forecast period. This growth is driven by the rising incidence of cancer, increased investment in healthcare, enhanced funding for oncology treatments, and advancements in healthcare infrastructure in countries such as China, India, and Japan, all of which have led to greater adoption of radiotherapy.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1 (40%), Tier 2 (30%), and Tier 3 (30%)

- By Designation: Directors (18%), C-level Executives (27%), and Other Designations (55%)

- By Region: North America (50%), Europe (20%), Asia Pacific (10%), Latin America (10%), and the Middle East & Africa (10%)

The prominent players in the radiotherapy market are Siemens Healthineers GmbH (Germany), Elekta (Sweden), Accuray Incorporated (US), IBA WORLDWIDE (Belgium), ViewRay Technologies, Inc (US), Perspective Therapeutics, Inc. (US), Hitachi High Tech Corporation (Japan), Sumitomo Heavy Industries Ltd. (Japan), Carl Zeiss Meditec AG (Germany), and Koninklijke Philips N.V. (Netherlands), among others.

Research Coverage

This report studies the radiotherapy market based on offering, technology, application, procedure, end user, and region. It also covers the factors affecting market growth, analyzes the opportunities and challenges in the market, and provides details on the competitive landscape among market leaders. Furthermore, the report analyzes micromarkets by their individual growth trends and forecasts revenue for market segments across five main regions (and the countries within these regions).

Reasons to Buy the Report

The report will enable established firms, as well as entrants/smaller firms, to gauge the pulse of the market, which, in turn, will help them garner a larger market share. Firms purchasing the report could use one or a combination of the following strategies to strengthen their market presence.

This report provides insights into the following pointers:

- Analysis of key drivers (advancements in radiotherapy treatment technology, growing patient population, increasing initiatives to promote radiotherapy awareness, and growing use of particle therapy for cancer treatment), restraints (high cost of advanced lab consumables and environmental sustainability concerns), opportunities (lack of adequate healthcare infrastructure, high capital cost of radiotherapy, and complexity of radiotherapy), and challenges (dearth of skilled personnel, difficulties in visualizing tumors during radiotherapy, and risk of Radiation Exposure) influencing the growth of the radiotherapy market.

- Market Penetration: Comprehensive information on the product portfolios offered by the top players in the radiotherapy market.

- Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product developments in the radiotherapy market.

- Market Development: Comprehensive information on lucrative emerging regions.

- Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the radiotherapy market.

- Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN RADIOTHERAPY MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 RADIOTHERAPY MARKET OVERVIEW

- 3.2 RADIOTHERAPY MARKET, BY REGION

- 3.3 NORTH AMERICA: RADIOTHERAPY MARKET, BY TECHNOLOGY AND COUNTRY

- 3.4 GEOGRAPHIC SNAPSHOT OF RADIOTHERAPY MARKET

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Advancements in radiotherapy treatment

- 4.2.1.2 AI and automation in treatment planning

- 4.2.1.3 Increasing government investments and awareness initiatives for cancer care

- 4.2.2 RESTRAINTS

- 4.2.2.1 High costs associated with radiotherapy systems such as proton therapy and advanced linear accelerators

- 4.2.2.2 Limited access to advanced radiotherapy infrastructure and skilled workforce in low- and middle-income countries

- 4.2.2.3 Shortage of skilled radiation oncologists, medical physicists, and trained technicians

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Emerging markets offer significant growth potential for radiotherapy technologies

- 4.2.3.2 Integration of radiotherapy with immunotherapy and systemic therapies

- 4.2.3.3 Growing adoption of outpatient radiotherapy and hypofractionated treatment regimens

- 4.2.4 CHALLENGES

- 4.2.4.1 Increasing cybersecurity and data protection challenges in digital radiotherapy ecosystems

- 4.2.4.2 Patient safety concerns and radiation exposure risks

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 THREAT OF NEW ENTRANTS

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 GDP TRENDS AND FORECAST

- 5.2.2 TRENDS IN GLOBAL RADIOTHERAPY INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RESEARCH & DEVELOPMENT

- 5.3.2 PROCUREMENT & MANUFACTURING

- 5.3.3 MARKETING, SALES, AND DISTRIBUTION

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT DATA (HS CODE 902214)

- 5.6.2 EXPORT DATA (HS CODE 902214)

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 SBRT'S ROLE IN MINIMIZING RADIATION RISK IN ELDERLY PATIENTS

- 5.10.2 RADIOTHERAPY FOR BREAST CANCER IN PATIENTS WITH HEREDITARY COPROPORPHYRIA

- 5.10.3 RADIATION THERAPY TREATMENT FOR TRANSITIONAL CELL CARCINOMA OF DISTAL URETHRA

- 5.11 IMPACT OF 2025 US TARIFF - RADIOTHERAPY MARKET

- 5.11.1 KEY TARIFF RATES

- 5.11.2 PRICE IMPACT ANALYSIS

- 5.11.3 IMPACT ON COUNTRIES/REGIONS

- 5.11.4 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 MR-GUIDED ADAPTIVE RADIOTHERAPY

- 6.1.2 ARTIFICIAL INTELLIGENCE-DRIVEN TREATMENT PLANNING

- 6.1.3 PROTON AND PARTICLE THERAPY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ADVANCED TREATMENT PLANNING SYSTEMS AND AI-ENABLED DECISION SUPPORT

- 6.2.2 CLOUD-BASED AND REMOTE RADIOTHERAPY PLATFORMS

- 6.3 PATENT ANALYSIS

- 6.3.1 INNOVATIONS AND PATENT REGISTRATIONS

- 6.4 FUTURE APPLICATIONS

- 6.5 IMPACT OF AI/GEN AI ON RADIOTHERAPY MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS IN RADIOTHERAPY MARKET

- 6.5.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN RADIOTHERAPY MARKET

- 6.5.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENT'S READINESS TO ADOPT GENERATIVE AI IN RADIOTHERAPY MARKET

- 6.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.2.1 North America

- 7.1.2.1.1 US

- 7.1.2.1.2 Canada

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.3.1 China

- 7.1.2.3.2 Japan

- 7.1.2.3.3 India

- 7.1.2.1 North America

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM END-USERS

9 RADIOTHERAPY MARKET, BY SYSTEM AND SOFTWARE & SERVICE

- 9.1 INTRODUCTION

- 9.2 SYSTEMS

- 9.2.1 INCREASING ADOPTION OF AI-ENABLED AND IMAGE-GUIDED RADIOTHERAPY SYSTEMS TO DRIVE GROWTH

- 9.3 SOFTWARE & SERVICES

- 9.3.1 INCREASING ADOPTION OF INTEGRATED ONCOLOGY SOFTWARE PLATFORMS TO SUPPORT MARKET GROWTH

10 RADIOTHERAPY MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 EXTERNAL BEAM RADIOTHERAPY

- 10.2.1 PROSTATE CANCER

- 10.2.1.1 High incidence rate and efficiency of EBRT in prostate cancer treatment to support growth

- 10.2.2 BREAST CANCER

- 10.2.2.1 Therapeutic benefits of EBRT to drive market

- 10.2.3 LUNG CANCER

- 10.2.3.1 High prevalence of lung cancer and efficiency of EBRT to drive market

- 10.2.4 HEAD & NECK CANCER

- 10.2.4.1 Increasing preference for noninvasive treatment of head & neck cancers to drive market

- 10.2.5 COLORECTAL CANCER

- 10.2.5.1 High incidence of colorectal cancer to support market growth

- 10.2.6 OTHER EBRT APPLICATIONS

- 10.2.1 PROSTATE CANCER

- 10.3 INTERNAL BEAM RADIOTHERAPY/BRACHYTHERAPY

- 10.3.1 PROSTATE CANCER

- 10.3.1.1 Precision of brachytherapy to drive market

- 10.3.2 GYNECOLOGICAL CANCER

- 10.3.2.1 Availability of alternatives to hinder adoption of brachytherapy

- 10.3.3 BREAST CANCER

- 10.3.3.1 Growing adoption of accelerated partial breast irradiation drives breast brachytherapy utilization

- 10.3.4 CERVICAL CANCER

- 10.3.4.1 MRI-guided adaptive brachytherapy and AI-enabled planning drive advances in cervical cancer treatment

- 10.3.5 PENILE CANCER

- 10.3.5.1 Increasing awareness of organ-preservation strategies to drive market

- 10.3.6 OTHER IBRT APPLICATIONS

- 10.3.1 PROSTATE CANCER

11 RADIOTHERAPY MARKET, BY PROCEDURE

- 11.1 INTRODUCTION

- 11.2 EXTERNAL BEAM RADIOTHERAPY

- 11.2.1 IMAGE-GUIDED RADIOTHERAPY

- 11.2.1.1 Growing adoption of real-time imaging and adaptive workflows to support market growth

- 11.2.2 INTENSITY-MODULATED RADIOTHERAPY

- 11.2.2.1 Growing adoption of hypofractionation and adaptive treatment planning to propel market

- 11.2.3 PARTICLE THERAPY

- 11.2.3.1 Advancements in treatment planning systems and expansion of proton therapy facilities to drive adoption

- 11.2.4 3D CONFORMAL RADIOTHERAPY

- 11.2.4.1 Continued utilization in resource-constrained settings to support adoption of 3D-CRT

- 11.2.5 STEREOTACTIC RADIOTHERAPY

- 11.2.5.1 Expanding clinical applications and hypofractionated treatment approaches to propel adoption

- 11.2.6 OTHER EBRT PROCEDURES

- 11.2.1 IMAGE-GUIDED RADIOTHERAPY

- 11.3 INTERNAL BEAM RADIOTHERAPY/BRACHYTHERAPY

- 11.3.1 LDR BRACHYTHERAPY

- 11.3.1.1 Low risk of radiation exposure to surrounding tissues to drive adoption

- 11.3.2 HDR BRACHYTHERAPY

- 11.3.2.1 Advancements in image-guided planning and dose optimization to drive growth

- 11.3.3 PDR BRACHYTHERAPY

- 11.3.3.1 Better radiation safety, easier prospective planning, and precise dose shaping to drive adoption

- 11.3.1 LDR BRACHYTHERAPY

12 RADIOTHERAPY MARKET, BY TECHNOLOGY

- 12.1 INTRODUCTION

- 12.2 EXTERNAL BEAM RADIOTHERAPY

- 12.2.1 LINACS

- 12.2.1.1 Conventional LINACs

- 12.2.1.1.1 Long treatment duration to limit adoption

- 12.2.1.2 Stereotactic advanced electron/cobalt-60 LINACs

- 12.2.1.2.1 CyberKnife

- 12.2.1.2.1.1 Precise radiation delivery with robotic correction capabilities to drive market

- 12.2.1.2.2 Gamma Knife

- 12.2.1.2.2.1 Advancements in precision intracranial radiosurgery to drive adoption

- 12.2.1.2.3 TomoTherapy

- 12.2.1.2.3.1 Accurate targeting of tumors and minimization of exposure to surrounding healthy tissues to drive adoption

- 12.2.1.2.1 CyberKnife

- 12.2.1.3 MRI LINACs

- 12.2.1.3.1 Real-time imaging advantage to propel growth

- 12.2.1.1 Conventional LINACs

- 12.2.2 PARTICLE THERAPY

- 12.2.2.1 Cyclotrons

- 12.2.2.1.1 Enhanced outcomes and other advantages to boost adoption

- 12.2.2.2 Synchrotrons

- 12.2.2.2.1 Increasing investments in synchrotron facilities to drive market

- 12.2.2.3 Synchrocyclotrons

- 12.2.2.3.1 Compact synchrocyclotron innovations support adoption despite infrastructure challenges

- 12.2.2.1 Cyclotrons

- 12.2.3 CONVENTIONAL COBALT-60 TELETHERAPY

- 12.2.3.1 Complex dose delivery planning and radiation exposure to limit market adoption

- 12.2.1 LINACS

- 12.3 INTERNAL BEAM RADIOTHERAPY/BRACHYTHERAPY

- 12.3.1 SEEDS

- 12.3.1.1 Adverse effects associated with brachytherapy seeds to limit adoption

- 12.3.2 AFTERLOADERS

- 12.3.2.1 Proper positioning and better control of isotopes in modern afterloaders to drive demand

- 12.3.3 IORT SYSTEMS

- 12.3.3.1 Growing clinical evidence supporting long-term efficacy to drive adoption

- 12.3.4 APPLICATORS

- 12.3.4.1 High risk of radiation exposure in manual applicators to limit growth

- 12.3.1 SEEDS

13 RADIOTHERAPY MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 HOSPITALS

- 13.2.1 INCREASING ADOPTION OF AI-ENABLED AND PRECISION RADIATION THERAPY SOLUTIONS TO DRIVE MARKET

- 13.3 INDEPENDENT RADIOTHERAPY CENTERS

- 13.3.1 EXPANSION OF RADIOTHERAPY INFRASTRUCTURE AND COMMUNITY-BASED CANCER CARE TO PROPEL MARKET

14 RADIOTHERAPY MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Favorable reimbursement scenario to drive growth

- 14.2.2 CANADA

- 14.2.2.1 Favorable initiatives from government and private organizations to boost market

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Availability of novel radiotherapy products to drive market

- 14.3.2 FRANCE

- 14.3.2.1 Presence of advanced healthcare systems to augment growth

- 14.3.3 UK

- 14.3.3.1 Growing adoption of advanced radiotherapy technologies and rising cancer burden to drive market

- 14.3.4 SPAIN

- 14.3.4.1 Adoption of advanced radiotherapy technologies to drive market

- 14.3.5 ITALY

- 14.3.5.1 Rising adoption of advanced radiotherapy technologies and strong research ecosystem to support market growth

- 14.3.6 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 JAPAN

- 14.4.1.1 Favorable reimbursement policies to propel market

- 14.4.2 CHINA

- 14.4.2.1 Precision oncology investments to drive market

- 14.4.3 INDIA

- 14.4.3.1 Growing cancer burden, infrastructure investments, and advanced technology adoption to drive market

- 14.4.4 SOUTH KOREA

- 14.4.4.1 Rising investments in heavy-ion therapy infrastructure to propel market

- 14.4.5 AUSTRALIA

- 14.4.5.1 Growing cancer cases to fuel market

- 14.4.6 REST OF ASIA PACIFIC

- 14.4.1 JAPAN

- 14.5 LATIN AMERICA

- 14.5.1 BRAZIL

- 14.5.1.1 Increasing prevalence of cancer to fuel market

- 14.5.2 MEXICO

- 14.5.2.1 Expanding oncology infrastructure and precision radiotherapy adoption to drive growth

- 14.5.3 REST OF LATIN AMERICA

- 14.5.1 BRAZIL

- 14.6 MIDDLE EAST & AFRICA

- 14.6.1 GCC COUNTRIES

- 14.6.1.1 Increasing investments in advanced oncology infrastructure to propel market

- 14.6.2 REST OF MIDDLE EAST & AFRICA

- 14.6.1 GCC COUNTRIES

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 15.2.1 KEY PLAYER COMPETITIVE STRATEGIES IN RADIOTHERAPY MARKET, JANUARY 2022-MAY 2026

- 15.3 REVENUE ANALYSIS, 2021-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.5.5.1 Company footprint

- 15.5.5.2 Region footprint

- 15.5.5.3 Technology footprint

- 15.5.5.4 Application footprint

- 15.5.5.5 End-user footprint

- 15.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 RESPONSIVE COMPANIES

- 15.6.3 DYNAMIC COMPANIES

- 15.6.4 STARTING BLOCKS

- 15.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.6.5.1 Detailed list of key startups/SMEs, 2025

- 15.6.5.2 Competitive benchmarking of key startups/SMEs, 2025

- 15.7 COMPANY VALUATION & FINANCIAL METRICS

- 15.8 BRAND COMPARISON

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES & APPROVALS

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 SIEMENS HEALTHINEERS AG

- 16.1.1.1 Business overview

- 16.1.1.2 Products/Solutions/Services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product approvals

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses & competitive threats

- 16.1.2 ELEKTA

- 16.1.2.1 Business overview

- 16.1.2.2 Products/Solutions/Services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches & approvals

- 16.1.2.3.2 Deals

- 16.1.2.3.3 Expansions

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses & competitive threats

- 16.1.3 ACCURAY INCORPORATED

- 16.1.3.1 Business overview

- 16.1.3.2 Products/Solutions/Services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches & approvals

- 16.1.3.3.2 Deals

- 16.1.3.3.3 Expansions

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses & competitive threats

- 16.1.4 IBA WORLDWIDE

- 16.1.4.1 Business overview

- 16.1.4.2 Products/Solutions/Services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Products launches

- 16.1.4.3.2 Deals

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses & competitive threats

- 16.1.5 VIEWRAY SYSTEMS, INC.

- 16.1.5.1 Business overview

- 16.1.5.2 Products/Solutions/Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product approvals

- 16.1.5.3.2 Deals

- 16.1.6 GT MEDICAL TECHNOLOGIES, INC.

- 16.1.6.1 Business overview

- 16.1.6.2 Products/Solutions/Services offered

- 16.1.7 HITACHI HIGH-TECH CORPORATION

- 16.1.7.1 Business overview

- 16.1.7.2 Products/Solutions/Services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Deals

- 16.1.8 SUMITOMO HEAVY INDUSTRIES, LTD.

- 16.1.8.1 Business overview

- 16.1.8.2 Products/Solutions/Services offered

- 16.1.9 ZEISS GROUP

- 16.1.9.1 Business overview

- 16.1.9.2 Products/solutions/services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Products launches

- 16.1.10 MIM SOFTWARE INC.

- 16.1.10.1 Business overview

- 16.1.10.2 Products/Solutions/Services offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Product launches & approvals

- 16.1.10.3.2 Deals

- 16.1.11 PANACEA MEDICAL TECHNOLOGIES PVT. LTD.

- 16.1.11.1 Business overview

- 16.1.11.2 Products/Solutions/Services offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Product launches

- 16.1.11.3.2 Deals

- 16.1.12 PROVISION HEALTHCARE

- 16.1.12.1 Business overview

- 16.1.12.2 Products/Solutions/Services offered

- 16.1.13 MEVION MEDICAL SYSTEMS

- 16.1.13.1 Business overview

- 16.1.13.2 Products/Solutions/Services offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Product launches & approvals

- 16.1.13.3.2 Deals

- 16.1.14 KONINKLIJKE PHILIPS N.V.

- 16.1.14.1 Business overview

- 16.1.14.2 Products/Solutions/Services offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Product launches

- 16.1.1 SIEMENS HEALTHINEERS AG

- 16.2 OTHER PLAYERS

- 16.2.1 SHINVA MEDICAL INSTRUMENT CO., LTD.

- 16.2.2 BRAINLAB AG

- 16.2.3 RAYSEARCH LABORATORIES

- 16.2.4 INTRAOP MEDICAL, INC.

- 16.2.5 OPTIVUS PROTON THERAPY, INC.

- 16.2.6 BEBIG MEDICAL

- 16.2.7 P-CURE

- 16.2.8 THERAGENICS CORPORATION

- 16.2.9 PROTOM INTERNATIONAL

- 16.2.10 DOSISOFT SA

- 16.2.11 ISOAID, LLC

- 16.2.12 MAGNETTX ONCOLOGY SOLUTIONS LTD.

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Objectives of secondary research

- 17.1.1.2 List of secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 Key industry insights

- 17.1.1 SECONDARY DATA

- 17.2 MARKET ESTIMATION METHODOLOGY

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 REVENUE MAPPING-BASED MARKET ESTIMATION

- 17.2.3 USAGE-BASED MARKET ESTIMATION

- 17.2.4 PRIMARY RESEARCH VALIDATION

- 17.2.5 TOP-DOWN APPROACH

- 17.3 DATA TRIANGULATION AND MARKET BREAKDOWN

- 17.4 MARKET SHARE ASSESSMENT

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RESEARCH LIMITATIONS

- 17.7 RISK ASSESSMENT

- 17.7.1 RISK ASSESSMENT ANALYSIS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS