|

시장보고서

상품코드

2076883

전기수술 시장 : 제품별, 수술 유형별, 최종사용자별 - 세계 예측(-2031년)Electrosurgery Market by Product, Surgery, End User : Global Forecast to 2031 |

||||||

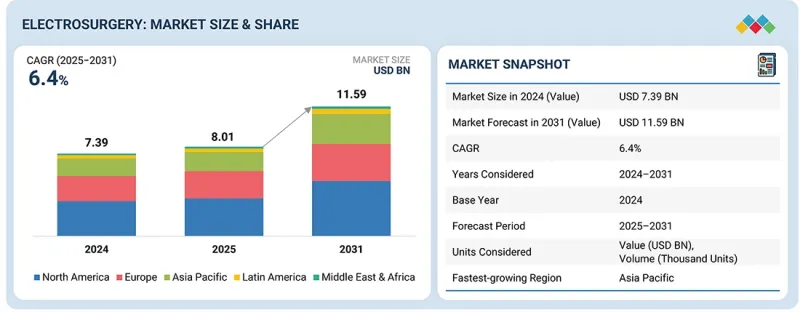

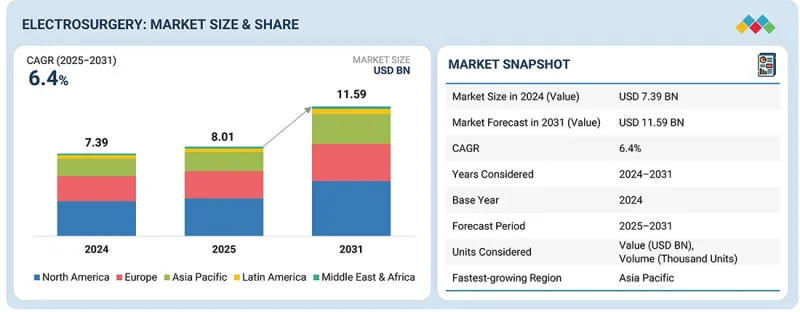

전기수술 시장 규모는 2025년 80억 1,000만 달러에서 2031년에는 115억 9,000만 달러로 성장하여 예측 기간 동안 CAGR은 6.4%에 달할 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 제품, 수술 유형, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

전기수술 업계는 수술 건수의 증가에 큰 영향을 받고 있으며, 그 배경에는 만성 질환의 유병률이 급속히 확대되고 있는 점이 있습니다. 또한, 최소침습 수술 및 외래 수술의 보급과 더불어, 에너지를 활용한 외과 수술 시스템의 지속적인 기술 발전이 시장 성장을 뒷받침하고 있습니다. 또한, 의료 인프라 확충과 정확하고 효율적이며 비용 대비 효과가 높은 외과적 솔루션에 대한 수요 증가도 시장 성장을 견인하고 있습니다. 한편, 시장은 화상, 수술 시 발생하는 연기의 흡입, 전자기 간섭 등 전기수술법과 관련된 위험이라는 큰 제약에 직면해 있습니다. 또한, 엄격한 규제 요건, 고가의 의료기기, 숙련된 외과 전문의의 부족으로 인해, 특히 의료 인프라가 미비한 지역이나 신흥국에서 도입률이 낮아지고 있으며, 이것이 시장 성장을 저해하고 있습니다.

"제품별로는 전기수술용 발전기 부문이 두 번째로 큰 점유율을 차지했습니다."

제품별로 보면 전기수술용 발전기가 2024년 시장에서 두 번째로 큰 점유율을 차지했습니다. 이는 임피던스가 다른 조직을 수술할 때 안정적인 출력을 제공하기 위해 전압과 전류를 자동으로 조정하는 폐루프 제어 시스템 등 기술 혁신이 진행되고 있기 때문입니다. 패드와 피부의 접촉 상태 및 전류 밀도를 모니터링하는 센서 등 통합된 안전 기능 덕분에 열 손상 위험이 줄어들고 시술의 안전성이 향상되고 있습니다. 또한, 수술 건수의 증가와 최소침습 수술에 대한 수요 증가를 배경으로, 병원 및 외래 수술 센터에서 첨단 에너지 플랫폼의 도입이 확대되고 있는 점도 이 부문의 시장 점유율을 더욱 강화하고 있습니다.

"최종사용자별로는 외래 수술 센터 부문이 두 번째로 큰 시장 점유율을 차지했습니다."

최종사용자별로는 외래 수술 센터 부문이 2024년 시장에서 두 번째로 큰 점유율을 차지했습니다. 이는 주로 외래 진료와 당일 수술을 선호하는 사람들이 점점 늘어나고 있기 때문입니다. 해당 최종사용자는 다양한 전문 분야에 걸쳐 빈도가 높고 효율적인 외과 수술 서비스를 제공하고 있습니다. 여기에는 일반외과, 정형외과, 산부인과, 피부과, 안과 등이 포함되며, 이러한 분야에서는 전기수술 기기가 주로 절개, 응고, 지혈에 사용됩니다. 외래 수술 센터(ASC)는 비용을 절감한 시술, 환자의 대기 시간 단축, 수술 후 조기 회복을 실현하고 있어, 환자뿐만 아니라 보험사에게도 매우 훌륭한 선택지가 되고 있습니다. 또한, ASC에는 첨단 전기수술 기기와 고도로 훈련된 의료 전문가들이 갖춰져 있어 안전하고 정확한 최소침습 수술이 가능할 뿐만 아니라, ASC의 보급과 시장 점유율 확대를 강력하게 뒷받침하고 있습니다.

"북미에서는 미국이 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 전망됩니다."

지역별로는 북미가 2024년에 시장을 독점했습니다. 북미의 전기수술 시장은 다시 미국과 캐나다로 나뉘며, 2024년에는 미국이 주요 시장 점유율을 차지했습니다. 이는 첨단 의료 인프라와 최종사용자의 혁신적인 의료 제품에 대한 신속한 도입 덕분입니다. 만성 질환의 부담이 증가함에 따라 외과적 개입의 필요성이 크게 높아질 것으로 예상되며, 이러한 수술은 전기수술 기기에 의해 뒷받침되고 있습니다. 또한, 의료비 증가, 병원 및 외래 수술 센터의 광범위한 보급, 주요 전기수술 기기 제조업체의 존재 역시 시장 성장의 강력한 기반이 되고 있습니다.

본 보고서에서는 전 세계 전기수술 시장을 조사하여, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추정 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 현황, 주요 기업 개요 등을 정리하고 있습니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 전기수술 시장 : 제품별

제10장 전기수술 시장 : 수술 유형별

제11장 전기수술 시장 : 최종사용자별

제12장 전기수술 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSMThe electrosurgery market is projected to grow from USD 8.01 billion in 2025 to USD 11.59 billion by 2031, at a CAGR of 6.4% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product, Surgery, End User, and Region |

| Regions covered | North America, Europe, APAC, LATAM, MEA |

The electrosurgery industry is largely influenced by the increasing number of surgical procedures, which, in turn, have been propelled by the rapidly growing prevalence of chronic diseases. In addition, the widespread acceptance of minimally invasive and outpatient surgeries, along with continuous technological advancements in energy-based surgical systems, is paving the way for market growth. Furthermore, expanding healthcare infrastructure and rising demand for precise, efficient, and cost-effective surgical solutions are driving market growth. The market faces a significant limitation in the form of risks associated with electrosurgical methods, such as heat burns, inhalation of surgical smoke, and electromagnetic interference, among others. In addition, tough regulatory requirements, expensive devices, and a lack of skilled surgical professionals are lowering the rate of adoption, especially in poor and emerging healthcare settings, which, in turn, is hampering the growth of the market.

"By product, the electrosurgical generators segment held the second-largest share in the electrosurgery market."

By product, the electrosurgery market comprises electrosurgical generators, electrosurgical instruments, electrosurgical accessories, and smoke evacuation systems. In 2024, electrosurgical generators held the second-largest share of the market. This is due to increasing technological innovations, such as closed-loop control systems that automatically regulate voltage and current to provide stable power output even when operating on tissues of varying impedance. Integrated safety features, such as sensors that monitor pad-to-skin contact and current density, reduce the risk of thermal injuries and enhance procedural safety. Moreover, the segment's market share is further strengthened by the growing adoption of advanced energy platforms in hospitals and ambulatory surgical centers, which is driven by rising surgical volumes and demand for minimally invasive procedures.

"By end user, the ambulatory surgical centers segment held the second-largest market share in the electrosurgery market."

By end user, the electrosurgery market is divided into hospitals, clinics, and ablation centers; ambulatory surgical centers; and research laboratories and academic institutes. In 2024, the ambulatory surgical centers segment held the second-largest share of the market. This is mainly because more and more people are preferring outpatient and day-care surgical procedures. The end users in question operate multi-specialty, high-volume, efficient surgical services. These include general surgery, orthopedics, gynecology, dermatology, and ophthalmology, where electrosurgical devices are mainly used for cutting, coagulation, and hemostasis. Ambulatory Surgery Centers (ASCs) provide less expensive procedures, shorter patient wait times, and quicker post-operative recovery, making them a very good option for patients as well as payers. Moreover, the presence of advanced electrosurgical products along with highly trained healthcare professionals in ASCs not only facilitates safe and accurate minimally invasive procedures but also strongly supports the adoption and market share of ASCs.

"US to grow at the highest CAGR in the North America electrosurgery market."

The global electrosurgery market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa (MEA). In 2024, North America dominated the global electrosurgery market. The North America electrosurgery market is further divided into the US and Canada. In 2024, the US held the major share in the North America electrosurgery market. This is due to its advanced healthcare infrastructure and rapid adoption of innovative medical products among end users. The increasing burden of chronic diseases will significantly raise the need for surgical interventions, which are supported by electrosurgical products. For example, the Population Reference Bureau has stated that the number of people aged 65 and above will increase from 58 million in 2022 to 82 million by 2050, thus greatly increasing the demand for surgeries. Additionally, the Centers for Disease Control and Prevention has revealed that the rate of obesity was above 25% in all the US states in 2024, whereas more than 90% of the adults aged 65 and above have at least one chronic condition. Furthermore, growth in healthcare expenditure, the wide presence of hospitals & ambulatory surgical centers, and the existence of leading electrosurgery manufacturers all provide a strong basis for market growth.

The US is anticipated to experience the fastest CAGR growth in the electrosurgery market in North America for several reasons

A breakdown of the primary participants (supply-side) in the electrosurgery referred to in this report is provided below:

- By Company Type: Tier 1-35%, Tier 2-40%, and Tier 3-25%

- By Designation: C-level-45%, Director Level-35%, and Others-20%

- By Region: North America-27%, Europe-25%, Asia Pacific-30%, Latin America- 8%, Middle East & Africa-10% .

Prominent players in the electrosurgery market include Medtronic (Ireland), Johnson & Johnson (US), Conmed Corporation (US), B Braun SE (Germany), Erbe Elektromedizin GmbH (Germany), Olympus Corporation (Japan), BOWA-electronic GmbH & Co. KG (Germany), Boston Scientific (US), and other players.

Research Coverage:

The report analyzes the electrosurgery market and estimates the market size and future growth potential across segments such as product, surgery, end user, and region. The report also includes a competitive analysis of the key players in this market, along with their company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will provide market leaders and new entrants with the closest available estimates of revenue for the overall electrosurgery market. It will help stakeholders understand the competitive landscape and gain insights to position their businesses more effectively and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides information on key market drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (growing prevalence of chronic diseases, increasing demand for minimally invasive surgeries, innovation and technological advancements in electrosurgical instruments, increasing number of hospitals coupled with rising surgical procedures, and shifting preference toward outpatient surgeries in developed regions), restraints (risks associated with electrosurgical procedures, stringent regulatory framework, and shortage of surgeons), opportunities (emerging markets, rising government funding to develop advanced medical treatments, and expected increase in cosmetic and bariatric procedures due to growing obesity prevalence), and challenges (concerns regarding toxic fumes produced during surgical procedures and electromagnetic-interference-related risks).

- Market Penetration: It includes extensive information on the products offered by the major players in the global electrosurgery market. The report covers product, surgery, end user, and region segments.

- Product Enhancement/Innovation: Comprehensive details about new product launches and anticipated trends in the global electrosurgery market

- Market Development: Thorough information and analysis of the profitable rising markets by product, surgery, end user, and region

- Market Diversification: Comprehensive information about newly launched products, expanding markets, current advancements, and investments in the global electrosurgery market

- Competitive Assessment: Thorough evaluation of the market share, growth plans, offerings of products, and capacities of the major competitors in the global electrosurgery market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED & REGIONAL SEGMENTATION

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND START DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ELECTROSURGERY MARKET OVERVIEW

- 3.2 NORTH AMERICA: ELECTROSURGERY MARKET, BY END USER

- 3.3 ELECTROSURGERY MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.4 ELECTROSURGERY MARKET: REGIONAL MIX

- 3.5 ELECTROSURGERY MARKET: DEVELOPED COUNTRIES VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing prevalence of chronic diseases

- 4.2.1.2 Increasing demand for minimally invasive surgeries

- 4.2.1.3 Shifting preference toward outpatient surgeries in developed regions

- 4.2.2 RESTRAINTS

- 4.2.2.1 Risks associated with electrosurgical procedures

- 4.2.2.2 Stringent regulatory framework

- 4.2.2.3 Shortage of surgeons

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising government funding to develop advanced medical treatments

- 4.2.4 CHALLENGES

- 4.2.4.1 Concerns regarding electromagnetic-interference-related risks

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN ELECTROSURGERY MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN MINIMALLY INVASIVE SURGERY

- 5.2.4 TRENDS IN SURGICAL ROBOTS

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS (2023-2025)

- 5.6.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS (2023-2025)

- 5.6.2 AVERAGE SELLING PRICE TREND, BY REGION (2023-2025)

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 9018)

- 5.7.2 EXPORT DATA (HS CODE 9018)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 IMPACT OF 2025 US TARIFF - ELECTROSURGERY MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON REGIONS

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 END-USE INDUSTRY IMPACT

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ROBOTIC-ASSISTED AND COMPUTER-ASSISTED SURGICAL SYSTEMS

- 6.1.2 AI-ENABLED SURGICAL SOFTWARE, ANALYTICS, AND SMART DEVICE INTEGRATION

- 6.1.3 COMPLEMENTARY TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.2.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.2.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.3 PATENT ANALYSIS

- 6.3.1 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 AI-ENABLED ROBOTIC AND COMPUTER-ASSISTED SURGERY

- 6.4.2 CONNECTED OPERATING-ROOM AND DIGITAL SUPPORT ECOSYSTEMS

- 6.5 IMPACT OF AI/GEN AI ON ELECTROSURGERY MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 CASE STUDIES OF AI IMPLEMENTATION IN THE ELECTROSURGERY MARKET

- 6.5.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ELECTROSURGERY MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF ELECTROSURGERY MARKET

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF ELECTROSURGERY MARKET

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

- 7.5 REIMBURSEMENT ANALYSIS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END USERS

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 ELECTROSURGERY MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 ELECTROSURGICAL INSTRUMENTS

- 9.2.1 BIPOLAR ELECTROSURGERY INSTRUMENTS

- 9.2.1.1 Advanced vessel sealing instruments

- 9.2.1.1.1 Enhanced procedural efficiency to boost segment

- 9.2.1.2 Bipolar forceps

- 9.2.1.2.1 Precision coagulation in delicate surgical procedures supports demand

- 9.2.1.1 Advanced vessel sealing instruments

- 9.2.2 MONOPOLAR ELECTROSURGERY INSTRUMENT

- 9.2.2.1 Electrosurgical pencils

- 9.2.2.1.1 Enhanced surgical control through precise energy activation and delivery

- 9.2.2.2 Electrosurgical electrodes

- 9.2.2.2.1 Controlled tissue effects through specialized energy delivery interfaces to boost demand

- 9.2.2.3 Suction coagulators

- 9.2.2.3.1 Combined fluid management and hemostasis to improve surgical efficiency - key driver

- 9.2.2.4 Monopolar forceps

- 9.2.2.4.1 Cost-effective tissue dissection and hemostasis across surgical procedures to drive market

- 9.2.2.1 Electrosurgical pencils

- 9.2.1 BIPOLAR ELECTROSURGERY INSTRUMENTS

- 9.3 ELECTROSURGICAL GENERATORS

- 9.3.1 SEGMENT DRIVEN BY ADVANCED ENERGY DELIVERY ACROSS ELECTROSURGICAL PROCEDURES

- 9.4 ELECTROSURGERY ACCESSORIES

- 9.4.1 PATIENT RETURN ELECTRODES OR DISPERSIVE ELECTRODES

- 9.4.1.1 Ensuring safe current return and reducing burn risk in monopolar electrosurgery - key functions

- 9.4.2 CORDS, CABLES, AND ADAPTERS

- 9.4.2.1 Maintaining system connectivity and supporting long-term utilization of electrosurgical platforms - key functions

- 9.4.3 OTHERS

- 9.4.1 PATIENT RETURN ELECTRODES OR DISPERSIVE ELECTRODES

10 ELECTROSURGERY MARKET, BY SURGERY TYPE

- 10.1 INTRODUCTION

- 10.2 GENERAL SURGERY

- 10.2.1 HIGH SURGICAL PROCEDURE VOLUMES AND GROWING ADOPTION OF MINIMALLY INVASIVE TECHNIQUES SUPPORT GROWTH

- 10.3 OBSTETRICS & GYNECOLOGY SURGERY

- 10.3.1 HIGH NUMBER OF CESAREAN DELIVERIES AND GROWING BURDEN OF BENIGN GYNECOLOGIC DISORDERS SUPPORT GROWTH

- 10.4 UROLOGIC SURGERY

- 10.4.1 RISING UROLOGICAL DISEASE BURDEN SUPPORTS SEGMENT DEMAND

- 10.5 ORTHOPEDIC SURGERY

- 10.5.1 RISING MUSCULOSKELETAL DISEASE BURDEN AND INCREASING JOINT RECONSTRUCTION PROCEDURES DRIVE SEGMENT GROWTH

- 10.6 CARDIOVASCULAR SURGERY

- 10.6.1 RISING CARDIOVASCULAR DISEASE BURDEN AND INCREASING CARDIAC INTERVENTION VOLUMES DRIVE SEGMENT GROWTH

- 10.7 COSMETIC SURGERY

- 10.7.1 GROWING PREFERENCE FOR MINIMALLY INVASIVE COSMETIC TREATMENTS DRIVE SEGMENT GROWTH

- 10.8 NEUROSURGERY

- 10.8.1 RISING BURDEN OF NEUROLOGICAL DISORDERS AND TRAUMATIC BRAIN INJURIES TO SUPPORT SEGMENT DEMAND

- 10.9 ONCOLOGY SURGERY

- 10.9.1 RISING CANCER INCIDENCE AND EXPANDING SURGICAL RESECTION VOLUMES SUPPORT SEGMENT GROWTH

- 10.10 OTHER SURGERIES

- 10.10.1 GROWING VOLUME OF ENT, OPHTHALMIC, DERMATOLOGIC, AND DENTAL PROCEDURES TO BOOST GROWTH

11 ELECTROSURGERY MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 HOSPITALS & CLINICS

- 11.2.1 HIGH SURGICAL PROCEDURE VOLUMES AND AVAILABILITY OF ADVANCED SURGICAL INFRASTRUCTURE SUPPORT THE DEMAND

- 11.3 AMBULATORY SURGICAL CENTERS

- 11.3.1 SHIFT TOWARD OUTPATIENT SURGERY AND EXPANSION OF MINIMALLY INVASIVE PROCEDURES DRIVE SEGMENT GROWTH

- 11.4 OTHER END USERS

12 ELECTROSURGERY MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 12.2.2 US

- 12.2.2.1 US to hold major share in North America electrosurgery market

- 12.2.3 CANADA

- 12.2.3.1 Growing chronic disease burden and aging population to support market growth

- 12.3 EUROPE

- 12.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 12.3.2 GERMANY

- 12.3.2.1 Aging population and investment in healthcare to drive market

- 12.3.3 UK

- 12.3.3.1 Rising chronic disease burden and aging population to support market growth

- 12.3.4 FRANCE

- 12.3.4.1 Growing cancer burden and aging population to support market growth

- 12.3.5 ITALY

- 12.3.5.1 Aging population and chronic disease burden to support market growth

- 12.3.6 SPAIN

- 12.3.6.1 High demand for surgical interventions to drive market growth

- 12.3.7 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 12.4.2 CHINA

- 12.4.2.1 High chronic disease burden to drive market

- 12.4.3 JAPAN

- 12.4.3.1 Rising aging population and growing cancer burden to support market growth

- 12.4.4 INDIA

- 12.4.4.1 Rising surgical oncology burden and expanding healthcare infrastructure to support growth

- 12.4.5 AUSTRALIA

- 12.4.5.1 High surgical procedure volumes to support market growth

- 12.4.6 SOUTH KOREA

- 12.4.6.1 Growing surgical demand and rapidly aging population to support market growth

- 12.4.7 REST OF ASIA PACIFIC

- 12.5 LATIN AMERICA

- 12.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 12.5.2 BRAZIL

- 12.5.2.1 Large aging patient pool to boost market

- 12.5.3 MEXICO

- 12.5.3.1 Rising chronic disease burden and surgical demand to support market growth

- 12.5.4 REST OF LATIN AMERICA

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 12.6.2 GCC COUNTRIES

- 12.6.2.1 Expanding healthcare infrastructure and surgical capacity to support market growth

- 12.6.3 REST OF MIDDLE EAST & AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN ELECTROSURGERY MARKET

- 13.3 REVENUE ANALYSIS, 2021-2025

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- 13.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.5.5.1 Company footprint

- 13.5.5.2 Region footprint

- 13.5.5.3 Product footprint

- 13.5.5.4 Surgery type footprint

- 13.5.5.5 End user footprint

- 13.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 RESPONSIVE COMPANIES

- 13.6.3 DYNAMIC COMPANIES

- 13.6.4 STARTING BLOCKS

- 13.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.6.5.1 Detailed list of key startups/SMEs

- 13.6.5.2 Competitive benchmarking of key startups/SMEs

- 13.7 COMPANY VALUATION & FINANCIAL METRICS

- 13.7.1 FINANCIAL METRICS

- 13.7.2 COMPANY VALUATION

- 13.8 BRAND/PRODUCT COMPARISON

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES & APPROVALS

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

14 COMPANY PROFILE

- 14.1 KEY PLAYERS

- 14.1.1 MEDTRONIC PLC

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches & approvals

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses & competitive threats

- 14.1.2 JOHNSON & JOHNSON (ETHICON)

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.3.4 Other developments

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses & competitive threats

- 14.1.3 OLYMPUS CORPORATION

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches

- 14.1.3.3.2 Expansions

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses & competitive threats

- 14.1.4 B. BRAUN

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Deals

- 14.1.4.3.2 Expansions

- 14.1.4.4 MnM view

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses & competitive threats

- 14.1.5 CONMED CORPORATION

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses & competitive threats

- 14.1.6 BOSTON SCIENTIFIC CORPORATION

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Deals

- 14.1.7 SMITH+NEPHEW

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches

- 14.1.7.3.2 Deals

- 14.1.7.3.3 Expansions

- 14.1.8 ERBE ELEKTROMEDIZIN GMBH

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches

- 14.1.8.3.2 Deals

- 14.1.8.3.3 Expansions

- 14.1.9 STRYKER CORPORATION

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.10 THE COOPER COMPANIES, INC.

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Deals

- 14.1.11 ZIMMER BIOMET

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Deals

- 14.1.12 UTAH MEDICAL PRODUCTS, INC.

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.13 INTEGRA LIFESCIENCES HOLDINGS CORPORATION

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.1 MEDTRONIC PLC

- 14.2 OTHER PLAYERS

- 14.2.1 BOWA-ELECTRONIC GMBH & CO. KG

- 14.2.2 KIRWAN SURGICAL PRODUCTS, LLC.

- 14.2.3 ENCISION INC.

- 14.2.4 KLS MARTIN GROUP

- 14.2.5 STILLE AB

- 14.2.6 I.C. MEDICAL, INC.

- 14.2.7 MEYER-HAAKE GMBH

- 14.2.8 APPLIED MEDICAL RESOURCES CORPORATION

- 14.2.9 ASPEN SURGICAL PRODUCTS, INC.

- 14.2.10 APYX MEDICAL

- 14.2.11 ECLIPSE PRISM MEDICAL DEVICES PVT. LTD

- 14.2.12 DIRECTA DENTAL GROUP

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.3 MARKET BREAKDOWN & DATA TRIANGULATION

- 15.4 MARKET RANKING ANALYSIS

- 15.5 STUDY ASSUMPTIONS

- 15.6 RESEARCH LIMITATIONS

- 15.6.1 METHODOLOGY-RELATED LIMITATIONS

- 15.6.2 SCOPE-RELATED LIMITATIONS

- 15.7 RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS