|

시장보고서

상품코드

2076885

소프트웨어 정의 차량(SDV) 시장 : SDV 유형별(SDV, 세미 SDV), E/E 아키텍처별(도메인 집중형, 존형), 차종별(승용차, 소형 상용차), 제공별(하드웨어, 소프트웨어), 용도별(ADAS, 텔레매틱스, 온디맨드 기능), 지역별 - 세계 예측(-2035년)Software Defined Vehicle Market by SDV Type (SDV, Semi-SDV), E/E Architecture (Domain Centralized, Zonal), Vehicle Type (PC, LCV), Offering (Hardware, Software), Application (ADAS, Telematics, Feature on Demand), and Region - Global Forecast to 2035 |

||||||

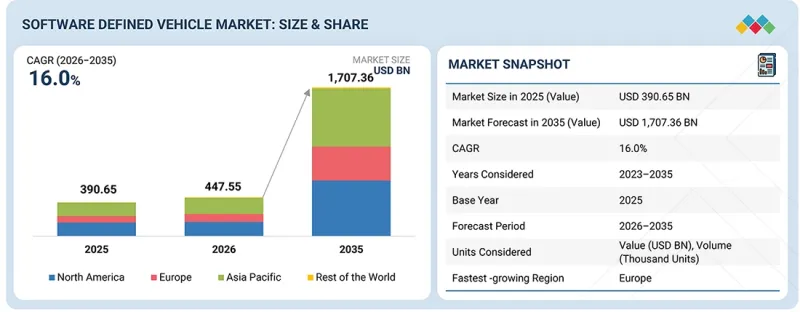

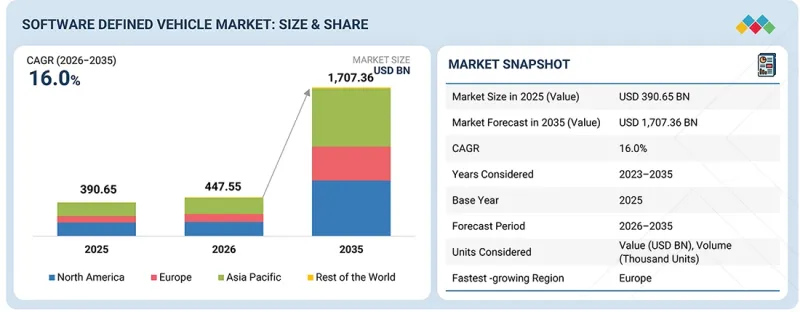

소프트웨어 정의 차량(SDV) 시장 규모는 2026년 4,475억 5,000만 달러에서 2035년에는 1조 7,073억 6,000만 달러로, CAGR 16.0%로 확대될 것으로 예측됩니다.

이 시장은 집중형 차량 컴퓨팅, 무선(OTA) 소프트웨어 업데이트, 커넥티드 서비스, AI 기반 기능의 도입 확대, 지속적인 소프트웨어 관리가 필요한 전기자동차(EV) 플랫폼으로의 전환에 힘입어 급속히 성장하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2033년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2033년 |

| 단위 | 달러 |

| 부문 | SDV 유형, E/E 아키텍처, 차종, 제공, 용도, 지역별 |

| 대상 지역 | 아시아태평양, 북미, 유럽, 기타 지역 |

자동차 제조사들은 차량을 업그레이드가 가능한 디지털 플랫폼으로 간주하는 경향을 점점 더 강화하고 있으며, 이를 통해 차량의 수명 주기 전반에 걸쳐 새로운 기능 추가, 성능 향상, 사이버 보안 업데이트, 구독형 서비스 제공이 가능해졌습니다. Tesla, Rivian, Stellantis, Xiaomi 등 주요 OEM 업체들은 SDV 아키텍처에 막대한 투자를 하고 있으며, Qualcomm과 Wayve와 같은 제휴도 AI 지원 차량 플랫폼 개발을 가속화하고 있습니다. 분산형 ECU에서 구역형 및 집중형 아키텍처로의 전환을 통해 확장성이 더욱 향상되고, 하드웨어의 복잡성이 줄어들며, 소프트웨어 정의 기능을 신속하게 배포할 수 있게 되었습니다.

"소프트웨어를 통한 기능의 수익화가 자동차 제조사들에게 새로운 지속적인 수익원을 창출하고 있습니다."

온디맨드 기능 구독 서비스는 SDV 시장의 주요 수익화 모델로 자리 잡고 있으며, 고객은 구매 후 소프트웨어를 통해 차량 기능을 활성화하거나, 업그레이드하거나, 개인화할 수 있게 됩니다. 이러한 성장을 주도하고 있는 요인은 무선 업데이트(OTA)의 보급 확대, 맞춤형 차량 내 경험에 대한 수요 증가, 중앙 집중형 컴퓨팅 아키텍처, 그리고 자동차 제조사들의 지속적인 수익 창출에 대한 집중입니다. 이러한 용도에는 프리미엄 인포테인먼트, 성능 업그레이드, 디지털 키 서비스, 주차 보조, 원격 차량 기능, 첨단 운전자 보조 기능 등이 포함됩니다.

BMW 그룹, 메르세데스-벤츠 그룹, 아우디 AG, 폭스바겐 그룹, 테슬라, NIO, XPENG 등 주요 OEM 업체들은 온디맨드 기능 제공을 적극적으로 확대하고 있습니다. 예를 들어, 2025년 6월, BMW 그룹은 업그레이드 가능한 소프트웨어 기반 기능을 갖춘 ‘Neue Klasse’ 생태계를 확대했습니다. 이는 업계가 지속적으로 업그레이드가 가능하고 수익을 창출하는 차량 플랫폼으로 전환되고 있음을 반영합니다.

"집중형 컴퓨팅이 하드웨어 도입을 가속화하고 있습니다."

SDV 시장에서 하드웨어 부문이 가장 큰 비중을 차지하는 이유는, 커넥티드카, 자율주행차, 소프트웨어 집약형 차량을 지원하기 위해 필요한 고성능 컴퓨팅 플랫폼, 첨단 센서, 자동차용 반도체, 존 컨트롤러, 중앙 집중형 차량 아키텍처의 도입이 증가하고 있기 때문입니다. ADAS, AI 주행 기능, 전기자동차, 실시간 데이터 처리의 도입 확대가 고성능 차량 컴퓨팅 인프라와 차세대 전자 시스템에 대한 수요를 견인하고 있습니다.

예를 들어, 2025년 1월, 혼다 모터는 미래의 SDV를 위해 설계된 중앙 집중형 컴퓨팅 아키텍처를 갖춘 ‘혼다 0 시리즈’ 플랫폼을 발표했습니다. 또한 2026년 3월에는 폭스바겐 그룹과 리비안이 중앙 집중형 컴퓨터와 구역 제어기를 통합한 차세대 차량 아키텍처를 검증했습니다. 이는 첨단 SDV 하드웨어 플랫폼에 대한 업계의 투자 확대를 보여줍니다.

"OEM을 통한 소프트웨어 투자 확대와 AI 지원 차량 플랫폼이 북미의 SDV 보급을 가속화하고 있습니다."

북미는 집중형 차량 컴퓨팅에 대한 투자 확대, 무선 업데이트(OTA)의 급속한 확산, AI를 활용한 ADAS 기능의 보급 확대, 자동차 제조사와 소프트웨어 기술 기업 간의 강력한 협력을 통해 SDV 시장에서 두각을 나타내고 있습니다. 이 지역은 SDV 분야를 선도하는 혁신 기업의 존재, 선진적인 클라우드 인프라, 지속적으로 업그레이드 가능한 차량 기능에 대한 소비자의 수요 증가라는 이점을 누리고 있습니다. 자동차 제조사들은 하드웨어 중심의 차량 개발에서 커넥티드 서비스, 기능의 수익화, 자율주행 기능을 지원하는 소프트웨어 주도형 아키텍처로 점점 더 전환하고 있습니다.

예를 들어, 2025년 8월, 포드 모터 컴퍼니(Ford Motor Company)는 OTA 업데이트와 핸즈프리 주행 기능을 지원하는 소프트웨어 정의형 전기자동차를 뒷받침하기 위해 설계된 유니버설 EV 플랫폼을 발표했습니다. 2025년 5월, 제너럴 모터스(General Motors)는 차세대 소프트웨어 플랫폼 전략을 발전시켜 차량 업데이트 기능을 개선하고, 전체 차량 라인업에 걸쳐 보다 폭넓은 소프트웨어 기반 서비스를 제공할 수 있게 되었습니다. 포드 모터 컴퍼니는 무선 업데이트 및 핸즈프리 주행 기능을 갖춘 소프트웨어 정의 전기자동차(SDEV)를 지원하도록 설계된 '범용 전기자동차 플랫폼'을 발표했습니다. 2025년 5월, 제너럴 모터스는 차량의 업데이트 기능을 개선하고 자사 차량 라인업 전반에 걸쳐 보다 폭넓은 소프트웨어 기반 서비스를 구현하기 위해 차세대 소프트웨어 플랫폼 전략을 추진했습니다.

본 보고서에서는 전 세계 소프트웨어 정의 차량(SDV) 시장을 조사하여, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추정 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등을 정리하고 있습니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 소프트웨어 정의 차량 아키텍처와 OEM의 경쟁 분석

제7장 소프트웨어 정의 차량 개발을 위한 OEM 생태계

제8장 기술의 진보, AI의 영향, 특허, 혁신, 향후 응용

제9장 규제 상황과 지속가능성에 대한 대처

제10장 고객 상황과 구매 행동

제11장 소프트웨어 정의 차량(SDV) 시장 : 유형별

제12장 소프트웨어 정의 차량(SDV) 시장 : 차종별

제13장 소프트웨어 정의 차량(SDV) 시장 : E/E 아키텍처별

제14장 소프트웨어 정의 차량(SDV) 시장 : 제공별

제15장 소프트웨어 정의 차량(SDV) 시장 : 용도별

제16장 소프트웨어 정의 차량(SDV) 시장 : 지역별

제17장 경쟁 구도

제18장 기업 개요

제19장 조사 방법

제20장 부록

KSMThe software defined vehicle (SDV) market is projected to grow from USD 447.55 billion in 2026 to USD 1,707.36 billion by 2035 at a CAGR of 16.0%. The market is growing rapidly due to increasing adoption of centralized vehicle computing, over-the-air (OTA) software updates, connected services, AI-driven features, and the shift toward electric vehicle platforms that require continuous software management.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | USD Billion |

| Segments | by SDV Type, E/E Architecture, Vehicle Type, Offering, Application, and Region |

| Regions covered | Asia Pacific, North America, Europe, and Rest of the World |

Automakers are increasingly treating vehicles as upgradable digital platforms, enabling new features, performance enhancements, cybersecurity updates, and subscription-based services throughout the vehicle lifecycle. Leading OEMs such as Tesla, Rivian, Stellantis, and Xiaomi are investing heavily in SDV architectures, while partnerships such as Qualcomm and Wayve are accelerating AI-enabled vehicle platforms. The transition from distributed ECUs to zonal and centralized architectures is further improving scalability, reducing hardware complexity, and enabling faster deployment of software-defined functionalities.

"Software-enabled feature monetization is creating new recurring revenue streams for automakers."

Feature-on-demand subscriptions are becoming a key monetization model in the SDV market, enabling customers to activate, upgrade, or personalize vehicle features via software after purchase. Growth is being driven by increasing adoption of over-the-air updates, rising demand for personalized vehicle experiences, centralized computing architectures, and automakers' focus on recurring revenue generation. Applications include premium infotainment, performance upgrades, digital key services, parking assistance, remote vehicle functions, and advanced driver assistance features. Major OEMs such as BMW Group, Mercedes-Benz Group, Audi AG, Volkswagen Group, Tesla, NIO, and XPENG are actively expanding feature on demand offerings. For instance, in June 2025, BMW Group expanded its Neue Klasse ecosystem with upgradeable software-based functionalities, reflecting the industry's shift toward continuously upgradeable and revenue-generating vehicle platforms.

"Centralized computing is accelerating hardware adoption."

The hardware segment is the largest offering in the software defined vehicle market due to increasing deployment of high-performance computing platforms, advanced sensors, automotive semiconductors, zonal controllers, and centralized vehicle architectures required to support connected, autonomous, and software-intensive vehicles. Growing adoption of ADAS, AI-driven functionalities, electric vehicles, and real-time data processing is driving demand for powerful vehicle computing infrastructure and next-generation electronic systems. For instance, in January 2025, Honda Motor Co., Ltd. unveiled its Honda 0 Series platform featuring centralized computing architecture designed for future SDVs, while in March 2026, Volkswagen Group and Rivian validated a next-generation vehicle architecture incorporating centralized computers and zonal controllers, highlighting growing industry investment in advanced SDV hardware platforms.

"Increasing OEM software investments and AI-enabled vehicle platforms are accelerating SDV adoption in North America"

North America is emerging in the software defined vehicle market due to increasing investments in centralized vehicle computing, rapid deployment of over-the-air updates, growing adoption of AI-enabled ADAS functions, and strong collaboration between automakers and software technology companies. The region is benefiting from the presence of leading SDV innovators, advanced cloud infrastructure, and rising consumer demand for continuously upgradable vehicle features. Automakers are increasingly transitioning from hardware-centric vehicle development toward software-driven architectures that support connected services, feature monetization, and autonomous driving capabilities. For instance, in August 2025, Ford Motor Company announced its Universal EV platform designed to support software-defined electric vehicles with over-the-air updates and hands-free driving capabilities. In May 2025, General Motors advanced its next-generation software platform strategy to improve vehicle update capabilities and enable a broader range of software-based services across its vehicle portfolio.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: Tier I - 20%, Tier II - 40%, OEMs - 40%

- By Designation: CXOs - 20%, Directors - 30%, Others - 50%

- By Country: Asia Pacific - 40%, North America - 20%, Europe - 30%, and Rest of the World - 10%

The software defined vehicle market is dominated by global players, such as Tesla (US), Li Auto Inc. (China), NIO (China), Rivian (US), and XPENG Inc. (China). These players have been adopting various strategies to sustain their positions in the market. Major strategies adopted are product launches, deals, and expansions. These strategies have been analyzed to understand the positions of these companies in the market. Manufacturers focus on maintaining their strategic position in the market by offering advanced software defined vehicle solutions to meet evolving regulatory and consumer demands.

Research Coverage:

The report covers the software defined vehicle market by SDV type (SDV, semi-SDV), E/E architecture (domain-centralized architecture, zonal architecture), vehicle type (passenger car, light commercial vehicle), offering (hardware, software), application ( ADAS, telematics, feature on demand), and region (Asia Pacific, Europe, North America, and Rest of the World). It covers the competitive landscape and company profiles of the major players in the software defined vehicle market ecosystem.

The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- This report will help market leaders/new entrants in this market with information on the closest approximations of revenue numbers for the software defined vehicle market ecosystem and its subsegments.

- The report will help market leaders/new entrants with software defined vehicle architecture & OEM competitive analysis and OEM ecosystem for E/E architecture development

- This report will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies.

- This report will also help stakeholders understand the market's pulse and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insight into the following pointers:

- Analysis of key drivers (reduced recall and manufacturing cost, paid ADAS and autonomous driving subscriptions, Increasing EV adoption requiring software driven vehicle control), restraints (ECU integration complexity from legacy to zonal architecture, slow OTA rollout due to safety validation requirements, OEM supplier divide in software led control), opportunities (feature-on-demand monetization, In vehicle app ecosystem development) and challenges (cybersecurity risks in connected vehicle systems, real-time AI processing constraints in vehicles)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the software defined vehicle market

- Market Development: Comprehensive information about lucrative markets (the report analyses the software defined vehicle market across varied regions)

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the software defined vehicle market

- Competitive Assessment: In-depth assessment of market ranking, growth strategies, and service offerings of leading players like Tesla (US), Li Auto Inc. (China), NIO (China), Rivian (US), and XPENG Inc. (China) in the software defined vehicle market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 DEFINITION BY GENERAL MOTORS

- 1.2.2 DEFINITION BY RENAULT

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SOFTWARE DEFINED VEHICLE MARKET

- 3.2 SOFTWARE DEFINED VEHICLE MARKET, BY TYPE

- 3.3 SOFTWARE DEFINED VEHICLE MARKET, BY VEHICLE TYPE

- 3.4 SOFTWARE DEFINED VEHICLE MARKET, BY OFFERING

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Reduced recall rate and development complexities

- 4.2.1.2 Rise of paid ADAS and autonomous driving subscriptions

- 4.2.1.3 Heightened EV adoption requiring software-driven vehicle control

- 4.2.2 RESTRAINTS

- 4.2.2.1 Complexity of transitioning from distributed ECU-based architecture to zonal architecture

- 4.2.2.2 Slow OTA rollout due to safety validation requirements

- 4.2.2.3 Interoperability constraint due to fragmented software ownership

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 New revenue streams from feature-on-demand models

- 4.2.3.2 Development of in-vehicle app ecosystems

- 4.2.4 CHALLENGES

- 4.2.4.1 Cybersecurity risks in connected vehicle systems

- 4.2.4.2 Real-time AI processing limitations

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 RELIABLE PERFORMANCE UNDER REAL-WORLD CONDITIONS

- 4.3.2 SIMPLIFIED ORCHESTRATION IN SOFTWARE-DEFINED INFRASTRUCTURE

- 4.3.3 LIMITED ECOSYSTEM INTEGRATION AND DATA USAGE IN SOFTWARE-DEFINED STACKS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 GDP TRENDS AND FORECAST

- 5.1.2 TRENDS IN CONNECTED VEHICLE MARKET

- 5.1.3 TRENDS IN GLOBAL AUTOMOTIVE AND TRANSPORTATION INDUSTRY

- 5.2 SUPPLY CHAIN ANALYSIS

- 5.3 ECOSYSTEM ANALYSIS

- 5.3.1 OEMS

- 5.3.2 TIER-1 HARDWARE PROVIDERS

- 5.3.3 TIER-2 PLAYERS

- 5.3.4 CHIP PROVIDERS

- 5.3.5 SOFTWARE PROVIDERS

- 5.3.6 CLOUD PROVIDERS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND, BY KEY PLAYER, 2023-2025

- 5.4.2 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025

- 5.5 TRADE ANALYSIS

- 5.5.1 IMPORT SCENARIO (HS CODE 8703)

- 5.5.2 EXPORT SCENARIO (HS CODE 8703)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 CUBIC TELECOM'S ROLE IN TRANSFORMING VEHICLE ARCHITECTURE

- 5.9.2 IMPLEMENTING VIRTUAL TESTING ENVIRONMENT WITH RED HAT

- 5.9.3 VOLKSWAGEN'S STRATEGIC FOCUS ON SOFTWARE INNOVATION

- 5.9.4 STANDARDIZING OTA UPDATES WITH ESYNC ALLIANCE

- 5.9.5 CONTINENTAL AUTOMOTIVE EDGE PLATFORM IN COLLABORATION WITH AWS

- 5.9.6 REVOLUTIONIZING AUTOMOTIVE SOFTWARE DEVELOPMENT WITH BLACKBERRY IVY AND AWS

- 5.9.7 AWS AND BLACKBERRY'S APPROACH TO MODERNIZING VEHICLE SOFTWARE

- 5.9.8 NVIDIA'S DRIVE PLATFORM POWERS VOLVO'S AUTONOMOUS VISION

- 5.9.9 TESLA'S JOURNEY INTO SOFTWARE DEFINED VEHICLES

- 5.9.10 BMW'S STRATEGIC SHIFT IN AUTOMOTIVE SOFTWARE

- 5.10 IMPACT OF ISRAEL-IRAN WAR

- 5.10.1 ENERGY MARKET DISRUPTION

- 5.10.2 OPERATING COST IMPACT

- 5.10.3 MARKET DEMAND SHIFT

- 5.10.4 SUPPLY CHAIN AND LOCALIZATION IMPACT

- 5.10.5 STRATEGIC MARKET OUTLOOK

- 5.11 IMPACT OF EU-INDIA FTA

- 5.11.1 EU TARIFFS

6 SOFTWARE DEFINED VEHICLE ARCHITECTURE AND OEM COMPETITIVE ANALYSIS

- 6.1 KEY TRENDS IN SOFTWARE DEFINED VEHICLES AND E/E ARCHITECTURE

- 6.1.1 TRENDS

- 6.1.2 RECENT INVESTMENTS

- 6.2 SOFTWARE DEFINED VEHICLE PROVIDER ANALYSIS

- 6.2.1 STRATEGIES FOLLOWED BY KEY LEGACY OEMS

- 6.2.2 COMPARISON OF TECH PLAYERS IN SOFTWARE DEFINED VEHICLE ECOSYSTEM

- 6.2.3 VEHICLE BODY PLATFORM COMPARISON

- 6.3 E/E ARCHITECTURE DEPLOYMENT

- 6.3.1 IN-HOUSE

- 6.3.2 OUTSOURCED

- 6.3.3 CO-DEVELOPMENT

- 6.4 OEM FEATURE OFFERING, BY SUBSCRIPRTION PRICING

- 6.5 LEVEL OF AUTONOMY SHIFT IMPACT ON SOFTWARE DEFINED VEHICLES

- 6.6 AI USE CASES

- 6.6.1 ADAS

- 6.6.2 DIGITAL COCKPIT

- 6.6.3 VEHICLE COMPUTE

- 6.6.4 OTHERS

7 OEM ECOSYSTEM FOR SOFTWARE DEFINED VEHICLE DEVELOPMENT

- 7.1 NORTH AMERICAN OEMS

- 7.1.1 TESLA

- 7.1.1.1 Tesla: Technology Roadmap

- 7.1.1.2 Tesla: Features Available on Demand and Pricing

- 7.1.2 FORD

- 7.1.2.1 FORD: Technology Roadmap

- 7.1.2.2 FORD: Technology Shift

- 7.1.2.3 FORD: Features Available on Demand and Pricing

- 7.1.3 RIVIAN

- 7.1.3.1 Rivian: Technology Roadmap

- 7.1.3.2 Rivian: Technology Shift

- 7.1.3.3 Rivian: Features Available on Demand and Pricing

- 7.1.4 LUCID MOTORS

- 7.1.4.1 Lucid Motors: Technology Roadmap

- 7.1.4.2 Lucid Motors: Features Available on Demand and Pricing

- 7.1.5 POLESTAR

- 7.1.5.1 Polestar: Technology Roadmap

- 7.1.5.2 Polestar: Features Available on Demand and Pricing

- 7.1.6 GENERAL MOTORS

- 7.1.6.1 General Motors: Technology Roadmap

- 7.1.6.2 General Motors: Technology Shift

- 7.1.6.3 General Motors: Features Available on Demand and Pricing

- 7.1.1 TESLA

- 7.2 EUROPEAN OEMS

- 7.2.1 STELLANTIS

- 7.2.1.1 Stellantis: Technology Roadmap

- 7.2.1.2 Stellantis: Technology Shift

- 7.2.1.3 Stellantis: Features Available on Demand and Pricing

- 7.2.2 VOLKSWAGEN

- 7.2.2.1 Volkswagen: Technology Roadmap

- 7.2.2.2 Volkswagen: Technology Shift

- 7.2.2.3 Volkswagen: Features Available on Demand and Pricing

- 7.2.3 BMW

- 7.2.3.1 BMW: Technology Roadmap

- 7.2.3.2 BMW: Technology Shift

- 7.2.3.3 BMW: Features Available on Demand and Pricing

- 7.2.4 MERCEDES-BENZ

- 7.2.4.1 Mercedes-Benz: Technology Roadmap

- 7.2.4.2 Mercedes-Benz: Technology Shift

- 7.2.4.3 Mercedes-Benz: Features Available on Demand and Pricing

- 7.2.5 JAGUAR LAND ROVER

- 7.2.5.1 Jaguar Land Rover: Technology Roadmap

- 7.2.5.2 Jaguar Land Rover: Technology Shift

- 7.2.5.3 Jaguar Land Rover: Features Available on Demand and Pricing

- 7.2.6 RENAULT

- 7.2.6.1 Renault: Technology Roadmap

- 7.2.6.2 Renault: Technology Shift

- 7.2.6.3 Renault: Features Available on Demand and Pricing

- 7.2.7 NISSAN

- 7.2.7.1 Nissan: Technology Roadmap

- 7.2.7.2 Nissan: Technology Shift

- 7.2.7.3 Nissan: Features Available on Demand and Pricing

- 7.2.8 VOLVO

- 7.2.8.1 Volvo: Technology Roadmap

- 7.2.8.2 Volvo: Technology Shift

- 7.2.8.3 Volvo: Features Available on Demand and Pricing

- 7.2.1 STELLANTIS

- 7.3 ASIAN OEMS

- 7.3.1 BYD

- 7.3.1.1 BYD: Technology Roadmap

- 7.3.1.2 BYD: Technology Shift

- 7.3.1.3 BYD: Features Available on Demand and Pricing

- 7.3.2 NIO

- 7.3.2.1 NIO: Technology Roadmap

- 7.3.2.2 NIO: Features Available on Demand and Pricing

- 7.3.3 XIAOMI

- 7.3.3.1 Xiaomi: Technology Roadmap

- 7.3.3.2 Xiaomi: Features Available on Demand and Pricing

- 7.3.4 LI AUTO

- 7.3.4.1 Li Auto: Technology Roadmap

- 7.3.4.2 Li Auto: Features Available on Demand and Pricing

- 7.3.5 ZEEKR

- 7.3.5.1 Zeekr: Technology Roadmap

- 7.3.5.2 Zeekr: Features Available on Demand and Pricing

- 7.3.6 GEELY

- 7.3.6.1 Geely: Technology Roadmap

- 7.3.6.2 Geely: Technology Shift

- 7.3.6.3 Geely: Features Available on Demand and Pricing

- 7.3.7 HYUNDAI-KIA-GENESIS

- 7.3.7.1 Hyundai-Kia Genesis: Technology Roadmap

- 7.3.7.2 Hyundai-Kia Genesis: Technology Shift

- 7.3.7.3 Hyundai-Kia Genesis: Features Available on Demand and Pricing

- 7.3.8 IM MOTORS

- 7.3.8.1 IM Motors: Technology Roadmap

- 7.3.8.2 IM Motors: Technology Shift

- 7.3.8.3 IM Motors: Features Available on Demand and Pricing

- 7.3.9 CHANGAN

- 7.3.9.1 Changan: Technology Roadmap

- 7.3.9.2 Changan: Technology Shift

- 7.3.9.3 Changan: Features Available on Demand and Pricing

- 7.3.10 CHERY

- 7.3.10.1 Chery: Technology Roadmap

- 7.3.10.2 Chery: Technology Shift

- 7.3.10.3 Chery: Features Available on Demand and Pricing

- 7.3.11 TOYOTA

- 7.3.11.1 Toyota: Technology Roadmap

- 7.3.11.2 Toyota: Technology Shift

- 7.3.11.3 Toyota: Features Available on Demand and Pricing

- 7.3.12 MAHINDRA & MAHINDRA

- 7.3.12.1 Mahindra & Mahindra: Technology Roadmap

- 7.3.12.2 Mahindra & Mahindra: Technology Shift

- 7.3.12.3 Mahindra & Mahindra: Features Available on Demand and Pricing

- 7.3.13 GWM

- 7.3.13.1 GWM: Technology Roadmap

- 7.3.13.2 GWM: Technology Shift

- 7.3.13.3 GWM: Features Available on Demand and Pricing

- 7.3.1 BYD

8 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 8.1 KEY TECHNOLOGIES

- 8.1.1 CENTRAL HPC

- 8.1.2 ZONAL CONTROLLERS

- 8.1.3 OTA UPDATES

- 8.2 COMPLEMENTARY TECHNOLOGIES

- 8.2.1 VEHICLE TO EVERYTHING (V2X) COMMUNICATION

- 8.2.2 VEHICLE CLOUD PLATFORMS

- 8.2.3 AUTONOMOUS DRIVING SOFTWARE STACKS

- 8.3 TECHNOLOGY/PRODUCT ROADMAP

- 8.4 SOFTWARE MONETIZATION & DIGITAL REVENUE MODELS

- 8.5 SDV ECOSYSTEM & STRATEGIC PARTNERSHIPS

- 8.6 AI, CYBERSECURITY & AUTONOMOUS INTELLIGENCE INTEGRATION

- 8.7 IMPACT OF AI/GEN AI

- 8.7.1 TOP USE CASES AND MARKET POTENTIAL

- 8.7.2 BEST PRACTICES

- 8.7.3 CASE STUDIES RELATED TO AI IMPLEMENTATION

- 8.7.3.1 TESLA'S FLEET LEARNING AI PLATFORM

- 8.7.3.2 MERCEDES-BENZ'S AI-POWERED MBUX VIRTUAL ASSISTANT

- 8.7.3.3 BMW'S AI-DRIVEN PERSONALIZATION PLATFORM

- 8.7.3.4 NIO'S NOMI AI COMPANION ECOSYSTEM

- 8.7.3.5 XPENG'S XNGP AI AUTONOMOUS DRIVING SYSTEM

- 8.7.4 CLIENTS' READINESS TO ADOPT AI

- 8.8 PATENT ANALYSIS

- 8.9 FUTURE APPLICATIONS

- 8.9.1 AI-DRIVEN VEHICLE PERSONALIZATION AND DIGITAL COMPANIONS

- 8.9.2 ON-DEMAND FEATURE ACTIVATION AND SOFTWARE MONETIZATION

- 8.9.3 IN-CABIN INTELLIGENCE AND USER INTERACTION

9 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 9.1 REGIONAL REGULATIONS AND COMPLIANCE

- 9.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 9.1.2 INDUSTRY STANDARDS

- 9.2 SUSTAINABILITY INITIATIVES

- 9.2.1 CARBON IMPACT AND ECO-APPLICATIONS

- 9.2.2 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

10 CUSTOMER LANDSCAPE AND BUYING BEHAVIOR

- 10.1 DECISION-MAKING PROCESS

- 10.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 10.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 10.2.2 BUYING CRITERIA

- 10.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 10.4 UNMEET NEEDS OF END USERS

11 SOFTWARE DEFINED VEHICLE MARKET, BY TYPE

- 11.1 INTRODUCTION

- 11.2 SDV

- 11.2.1 INCREASING FLEXIBILITY AND AGILITY THROUGH OTA UPDATES TO DRIVE MARKET

- 11.3 SEMI-SDV

- 11.3.1 KEY ROLE AS TRANSITIONAL PHASE TOWARD ADVANCED ZONAL CONTROL ARCHITECTURE TO DRIVE MARKET

- 11.4 PRIMARY INSIGHTS

12 SOFTWARE DEFINED VEHICLE MARKET, BY VEHICLE TYPE

- 12.1 INTRODUCTION

- 12.2 PASSENGER CAR

- 12.2.1 CONSUMER EXPECTATIONS FOR SEAMLESS, TECH-DRIVEN EXPERIENCES TO DRIVE MARKET

- 12.3 LIGHT COMMERCIAL VEHICLE

- 12.3.1 MOVE TOWARD ELECTRIFICATION AND STRICTER EMISSIONS AND SAFETY REGULATIONS TO DRIVE MARKET

- 12.4 PRIMARY INSIGHTS

13 SOFTWARE DEFINED VEHICLE MARKET, BY E/E ARCHITECTURE

- 13.1 INTRODUCTION

- 13.2 DOMAIN-CENTRALIZED ARCHITECTURE

- 13.3 ZONAL CONTROL ARCHITECTURE

14 SOFTWARE DEFINED VEHICLE MARKET, BY OFFERING

- 14.1 INTRODUCTION

- 14.2 SOFTWARE

- 14.2.1 GROWING DEMAND FOR CONNECTED VEHICLE SERVICES TO DRIVE MARKET

- 14.3 HARDWARE

- 14.3.1 SURGE IN COMPUTING DEMAND TO DRIVE MARKET

- 14.4 PRIMARY INSIGHTS

15 SOFTWARE DEFINED VEHICLE MARKET, BY APPLICATION

- 15.1 INTRODUCTION

- 15.2 ADAS

- 15.2.1 OEM SHIFT FROM LEVELS L0 TO L3

- 15.3 TELEMATICS

- 15.4 FEATURE-ON-DEMAND

16 SOFTWARE DEFINED VEHICLE MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 ASIA PACIFIC

- 16.2.1 CHINA

- 16.2.1.1 Stiff OEM competition and state support for intelligent connected vehicles to drive market

- 16.2.2 INDIA

- 16.2.2.1 Mass market digitalization and substantial investments in connected EV platforms to drive market

- 16.2.3 JAPAN

- 16.2.3.1 Emphasis on long-term software integration and platform-level investments to drive market

- 16.2.4 SOUTH KOREA

- 16.2.4.1 Global leadership in consumer electronics, semiconductor manufacturing, and 5G connectivity to drive market

- 16.2.1 CHINA

- 16.3 EUROPE

- 16.3.1 GERMANY

- 16.3.1.1 Concentration of global automotive OEMs and Tier-1 suppliers and large-scale investments in high-performance vehicle computing to drive market

- 16.3.2 FRANCE

- 16.3.2.1 National software ecosystem development and EV digitalization to drive market

- 16.3.3 ITALY

- 16.3.3.1 Significant presence of premium automotive manufacturers to drive market

- 16.3.4 SPAIN

- 16.3.4.1 EV manufacturing expansion and automotive digital transformation to drive market

- 16.3.5 UK

- 16.3.5.1 Strong automotive engineering capabilities and advanced connected mobility ecosystem to drive market

- 16.3.1 GERMANY

- 16.4 NORTH AMERICA

- 16.4.1 US

- 16.4.1.1 Leadership in automotive software development and strong presence of technology companies to drive market

- 16.4.2 CANADA

- 16.4.2.1 Expansion of automotive software engineering and connected mobility investments to drive market

- 16.4.1 US

- 16.5 REST OF THE WORLD

- 16.5.1 BRAZIL

- 16.5.1.1 Connected vehicle production and OEM investments to drive market

- 16.5.2 SOUTH AFRICA

- 16.5.2.1 Robust automotive manufacturing capabilities and growing adoption of connected vehicle technologies to drive market

- 16.5.1 BRAZIL

17 COMPETITIVE LANDSCAPE

- 17.1 OVERVIEW

- 17.2 KEY PLAYERS STRATEGIES/RIGHT TO WIN, 2023-2026

- 17.3 MARKET SHARE ANALYSIS, 2025

- 17.4 REVENUE ANALYSIS, 2021-2025

- 17.5 COMPANY VALUATION AND FINANCIAL METRICS

- 17.6 BRAND/PRODUCT COMPARISON

- 17.7 COMPANY EVALUATION MATRIX: OEMS, 2025

- 17.7.1 STARS

- 17.7.2 EMERGING LEADERS

- 17.7.3 PERVASIVE PLAYERS

- 17.7.4 PARTICIPANTS

- 17.7.5 COMPANY FOOTPRINT

- 17.7.5.1 Company footprint

- 17.7.5.2 Region footprint

- 17.7.5.3 Vehicle type footprint

- 17.7.5.4 E/E architecture footprint

- 17.8 COMPANY EVALUATION MATRIX: TECHNOLOGY PROVIDERS, 2025

- 17.8.1 PROGRESSIVE COMPANIES

- 17.8.2 RESPONSIVE COMPANIES

- 17.8.3 DYNAMIC COMPANIES

- 17.8.4 STARTING BLOCKS

- 17.9 COMPETITIVE SCENARIO

- 17.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 17.9.2 DEALS

- 17.9.3 EXPANSIONS

- 17.9.4 OTHERS

18 COMPANY PROFILES

- 18.1 KEY OEMS

- 18.1.1 TESLA

- 18.1.1.1 Business overview

- 18.1.1.2 Products offered

- 18.1.1.3 Recent developments

- 18.1.1.3.1 Product launches/developments

- 18.1.1.3.2 Deals

- 18.1.1.4 MnM view

- 18.1.1.4.1 Key strengths

- 18.1.1.4.2 Strategic choices

- 18.1.1.4.3 Weaknesses and competitive threats

- 18.1.2 LI AUTO INC.

- 18.1.2.1 Business overview

- 18.1.2.2 Products offered

- 18.1.2.3 Recent developments

- 18.1.2.3.1 Product launches/developments

- 18.1.2.3.2 Deals

- 18.1.2.3.3 Others

- 18.1.2.4 MnM view

- 18.1.2.4.1 Key strengths

- 18.1.2.4.2 Strategic choices

- 18.1.2.4.3 Weaknesses and competitive threats

- 18.1.3 XIAOMI

- 18.1.3.1 Business overview

- 18.1.3.2 Products offered

- 18.1.3.3 Recent developments

- 18.1.3.3.1 Product launches/developments

- 18.1.3.3.2 Deals

- 18.1.3.3.3 Others

- 18.1.3.4 MnM view

- 18.1.3.4.1 Key strengths

- 18.1.3.4.2 Strategic choices

- 18.1.3.4.3 Weaknesses and competitive threats

- 18.1.4 ZEEKR

- 18.1.4.1 Business overview

- 18.1.4.2 Products offered

- 18.1.4.3 Recent developments

- 18.1.4.3.1 Product launches/developments

- 18.1.4.3.2 Deals

- 18.1.4.3.3 Expansions

- 18.1.4.3.4 Others

- 18.1.4.4 MnM view

- 18.1.4.4.1 Key strengths

- 18.1.4.4.2 Strategic choices

- 18.1.4.4.3 Weaknesses and competitive threats

- 18.1.5 XPENG INC.

- 18.1.5.1 Business overview

- 18.1.5.2 Products offered

- 18.1.5.3 Recent developments

- 18.1.5.3.1 Product launches/developments

- 18.1.5.3.2 Deals

- 18.1.5.3.3 Others

- 18.1.5.4 MnM view

- 18.1.5.4.1 Key strengths

- 18.1.5.4.2 Strategic choices

- 18.1.5.4.3 Weaknesses and competitive threats

- 18.1.6 NIO

- 18.1.6.1 Business overview

- 18.1.6.2 Products offered

- 18.1.6.3 Recent developments

- 18.1.6.3.1 Product launches/developments

- 18.1.6.3.2 Deals

- 18.1.6.3.3 Expansions

- 18.1.6.3.4 Others

- 18.1.7 RIVIAN

- 18.1.7.1 Business overview

- 18.1.7.2 Products offered

- 18.1.7.3 Recent developments

- 18.1.7.3.1 Product launches/developments

- 18.1.7.3.2 Deals

- 18.1.7.4 MnM view

- 18.1.7.4.1 Key strengths

- 18.1.7.4.2 Strategic choices

- 18.1.7.4.3 Weaknesses and competitive threats

- 18.1.8 POLESTAR

- 18.1.8.1 Business overview

- 18.1.8.2 Products offered

- 18.1.8.3 Recent developments

- 18.1.8.3.1 Product launches/developments

- 18.1.8.3.2 Deals

- 18.1.9 SAIC

- 18.1.9.1 Business overview

- 18.1.9.2 Products offered

- 18.1.9.3 Recent developments

- 18.1.9.3.1 Product launches/developments

- 18.1.9.3.2 Deals

- 18.1.9.3.3 Others

- 18.1.10 VOLKSWAGEN

- 18.1.10.1 Business overview

- 18.1.10.2 Products offered

- 18.1.10.3 Recent developments

- 18.1.10.3.1 Product launches/developments

- 18.1.10.3.2 Deals

- 18.1.10.3.3 Expansions

- 18.1.11 HYUNDAI MOTOR COMPANY

- 18.1.11.1 Business overview

- 18.1.11.2 Products offered

- 18.1.11.3 Recent developments

- 18.1.11.3.1 Product launches/developments

- 18.1.11.3.2 Deals

- 18.1.11.3.3 Expansions

- 18.1.12 FORD MOTOR COMPANY

- 18.1.12.1 Business overview

- 18.1.12.2 Products offered

- 18.1.12.3 Recent developments

- 18.1.12.3.1 Product launches/developments

- 18.1.12.3.2 Deals

- 18.1.12.3.3 Expansions

- 18.1.12.3.4 Others

- 18.1.13 GENERAL MOTORS

- 18.1.13.1 Business overview

- 18.1.13.2 Products offered

- 18.1.13.3 Recent developments

- 18.1.13.3.1 Product launches/developments

- 18.1.13.3.2 Deals

- 18.1.13.3.3 Expansions

- 18.1.14 RENAULT GROUP

- 18.1.14.1 Business overview

- 18.1.14.2 Products offered

- 18.1.14.3 Recent developments

- 18.1.14.3.1 Product launches/developments

- 18.1.14.3.2 Deals

- 18.1.14.3.3 Expansions

- 18.1.15 TOYOTA MOTOR CORPORATION

- 18.1.15.1 Business overview

- 18.1.15.2 Products offered

- 18.1.15.3 Recent developments

- 18.1.15.3.1 Product launches/developments

- 18.1.15.3.2 Deals

- 18.1.15.3.3 Expansions

- 18.1.16 STELLANTIS N.V.

- 18.1.16.1 Business overview

- 18.1.16.2 Products offered

- 18.1.16.3 Recent developments

- 18.1.16.3.1 Product launches/developments

- 18.1.16.3.2 Deals

- 18.1.16.3.3 Expansions

- 18.1.17 MERCEDES-BENZ GROUP AG

- 18.1.17.1 Business overview

- 18.1.17.2 Products offered

- 18.1.17.3 Recent developments

- 18.1.17.3.1 Product launches/developments

- 18.1.17.3.2 Deals

- 18.1.17.3.3 Expansions

- 18.1.18 BYD

- 18.1.18.1 Business overview

- 18.1.18.2 Products offered

- 18.1.18.3 Recent developments

- 18.1.18.3.1 Product launches/developments

- 18.1.18.3.2 Deals

- 18.1.19 BMW GROUP

- 18.1.19.1 Business overview

- 18.1.19.2 Products offered

- 18.1.19.3 Recent developments

- 18.1.19.3.1 Product launches/developments

- 18.1.19.3.2 Deals

- 18.1.19.3.3 Expansions

- 18.1.1 TESLA

- 18.2 KEY TECHNOLOGY PROVIDERS

- 18.2.1 NVIDIA CORPORATION

- 18.2.2 QUALCOMM TECHNOLOGIES

- 18.2.3 BLACKBERRY LIMITED

- 18.2.4 VECTOR INFORMATIK GMBH

- 18.2.5 GOOGLE

- 18.2.6 AMAZON WEB SERVICES

- 18.2.7 MICROSOFT

- 18.2.8 APEX.AI

- 18.2.9 MOBILEYE

- 18.2.10 TENCENT

- 18.2.11 ALIBABA

- 18.2.12 HORIZON ROBOTICS

- 18.2.13 TATA TECHNOLOGIES

- 18.2.14 KPIT TECHNOLOGIES

19 RESEARCH METHODOLOGY

- 19.1 RESEARCH DATA

- 19.1.1 SECONDARY DATA

- 19.1.1.1 List of secondary sources

- 19.1.1.2 Key data from secondary sources

- 19.1.2 PRIMARY DATA

- 19.1.2.1 Primary interview participants

- 19.1.2.2 Breakdown of primary interviews

- 19.1.2.3 List of primary sources

- 19.1.1 SECONDARY DATA

- 19.2 MARKET SIZE ESTIMATION

- 19.2.1 BOTTOM-UP APPROACH

- 19.3 DATA TRIANGULATION

- 19.4 FACTOR ANALYSIS

- 19.5 RESEARCH ASSUMPTIONS

- 19.6 RISK ANALYSIS

- 19.7 RESEARCH LIMITATIONS

20 APPENDIX

- 20.1 INSIGHTS FROM INDUSTRY EXPERTS

- 20.2 DISCUSSION GUIDE

- 20.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.4 CUSTOMIZATION OPTIONS

- 20.4.1 FURTHER BREAKDOWN OF SOFTWARE DEFINED VEHICLE MARKET, BY VEHICLE TYPE, AT COUNTRY LEVEL (FOR COUNTRIES PRESENT IN REPORT)

- 20.4.2 ADDITIONAL COUNTRIES (APART FROM THOSE ALREADY CONSIDERED IN REPORT)

- 20.4.3 COMPANY INFORMATION

- 20.5 RELATED REPORTS

- 20.6 AUTHOR DETAILS