|

시장보고서

상품코드

2081119

치과용 골이식 대체재 시장 예측(-2031년) : 유형(이종 골이식재, 동종 골이식재, 합성 골이식재, 인공뼈), 용도(상악동 거상술, 치조골 증대술, 소켓 보존), 제품 유형(BioOss, Osteograf, Grafton), 최종사용자, 지역별Dental Bone Graft Substitutes Market by Type (Xenograft, Allograft, Synthetic Bone Grafts, Alloplast), Application (Sinus Lift, Ridge Augmentation, Socket Preservation), Product (BioOss, Osteograf, Grafton), End User, Region - Global Forecast to 2031 |

||||||

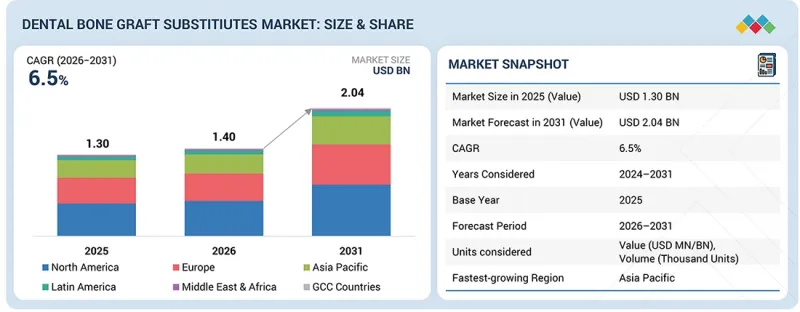

치과용 골이식 대체재 시장 규모는 2026년 14억 달러에서 2031년에는 20억 4,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간 중 CAGR은 6.5%에 달할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 제품, 제품 유형, 메커니즘, 용도, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

치과용 골이식 대체재 시장은 주로 치아 상실, 치주염, 악안면 결손 등의 치과 질환 유병률 증가에 힘입어 성장하고 있습니다. 이러한 증가에 따라 효과적인 골 재생 솔루션에 대한 수요가 높아지고 있습니다. 또한 치과 임플란트와 첨단 수복 재료의 인기가 높아짐에 따라 고품질 이식 재료에 대한 수요도 크게 증가하고 있습니다.

이종 이식재, 동종 이식재, 합성 대체재 등 이식 대체재 분야의 혁신을 통해 임상 성과 향상, 예측 가능성 개선, 편의성 증대가 실현되어, 치과의사들에게 바람직한 선택지가 되고 있습니다. 또한 환자와 임상의들 사이에서 구강 건강에 대한 인식이 높아지고 있는 데다, 치과 시설과 전문적인 외과 서비스의 확대도 시장 성장에 긍정적인 영향을 미치고 있습니다.

임상적 필요성, 기술의 발전, 환자 의식의 고취가 복합적으로 작용하여 전 세계에서 치과용 골이식 대체재에 대한 수요를 견인하고 있습니다.

'용도별로는 소켓 보존이 시장에서 가장 큰 시장 점유율을 차지할 것으로 예상된다''

치과용 골이식 대체재 시장에서는 소켓 보존 부문이 가장 큰 점유율을 차지하고 있습니다. 이는 발치 후 회복 기간에 자주 사용되며, 치조골의 양을 유지하는 데 중요한 역할을 하기 때문입니다. 발치 후에는 급속한 골흡수가 발생할 가능성이 있으며, 결국 치과 임플란트 식립이 필요해질 수 있습니다. 따라서 소켓 보존술은 치과용 골이식 대체재 시장에서 유력한 대안으로 자리 잡고 있습니다.

치과용 골이식 대체재는 일반적으로 발치 직후에 이식되어 발치 부위를 안정시키고 골 형성을 촉진합니다. 충치, 치주질환, 외상 등 다양한 이유로 전 세계에서 발치 시술이 이루어지고 있는 만큼, 소켓 보존 시장의 중요성이 부각되고 있습니다. 이 부문은 적용이 용이하고 예측 가능한 결과를 얻을 수 있다는 점에서 업계 내에서 널리 인정받고 있으며, 전문 분야에 관계없이 치과의사들 사이에서 선호되는 선택지로 자리 잡고 있습니다.

'최종사용자별로는 병원이 가장 큰 비중을 차지할 것으로 예상된다'

이는 주로 확립된 임상 환경과, 다양한 복잡한 치과 및 구강외과수술을 수행하면서 다수의 환자를 치료할 수 있는 능력 덕분입니다. 예를 들어 병원에는 골이식 대체재를 이용한 치과 및 턱 재건 수술이 필요한 환자를 치료할 수 있는 시설이 갖춰져 있습니다. 이러한 사례에는 치과 임플란트 수술, 치주병 치료, 턱 재건 수술 등이 포함됩니다. 이러한 시술에는 첨단 기술적·임상적 요건이 요구되므로, 골이식 대체재는 모든 치과 및 턱 수술에 필수적입니다. 또한 병원의 치과·악외과 부서는 충분히 정비되어 효율적으로 운영되고 있으며, 이러한 대체 재료를 효과적으로 활용할 수 있는 능력이 향상되고 있습니다. 그 결과, 병원은 치과용 골이식 대체재의 주요 최종사용자 시설로 간주되고 있습니다.

'예측 기간 중 북미 치과용 골이식 대체재 시장에서 미국은 가장 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 예상된다'

북미 치과용 골이식 대체재 시장에서 미국은 몇 가지 주요 요인의 지원을 받아 가장 높은 성장률을 보일 것으로 예상됩니다. 고령화의 진행과 치아 상실, 치주질환 등 노화에 따른 치과 질환의 유병률 증가가 해당 국가에서 치과용 골이식 대체재의 수요를 견인하고 있습니다. 또한 잘 갖춰진 치과 의료 인프라와 혁신적인 치과 기술에 대한 수용도가 높아진 점도 미국내 치과용 골이식 대체재 시장의 성장에 기여하고 있습니다. 또한 치과 임플란트 등 치과 치료의 보급이 확대되고 있는 점과, 치과 외과 의사 및 건강에 관심이 많은 소비자들 사이에서 치과 및 치주 건강에 대한 인식이 높아지고 있는 점도 이 시장의 성장을 지원하고 있습니다. 이러한 요인들이 복합적으로 작용하여, 미국은 북미 지역의 치과용 골이식 대체재 시장에서 주도적인 위치를 확립하고 있습니다.

이 보고서에서는 전 세계 치과용 골이식 대체재 시장을 조사하여, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 현황, 주요 기업 개요 등을 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 치과용 골이식 대체재 시장 : 유형별

제10장 치과용 골이식 대체재 시장 : 용도별

제11장 치과용 골이식 대체재 시장 : 메커니즘별

제12장 치과용 골이식 대체재 시장 : 최종사용자별

제13장 치과용 골이식 대체재 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

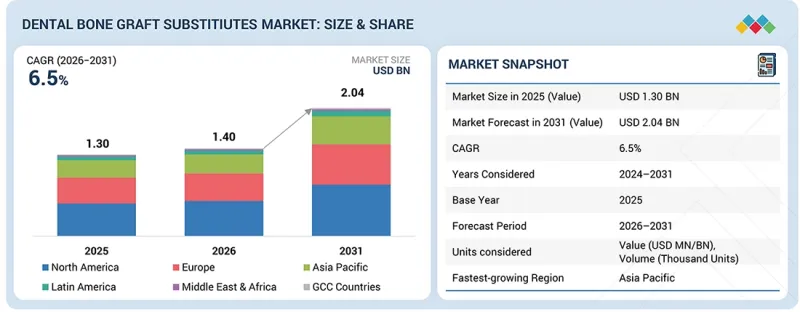

KSA 26.07.14The dental bone graft substitutes market is projected to reach USD 2.04 billion by 2031 from USD 1.40 billion in 2026, at a CAGR of 6.5% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product, Type, Mechanism, Application, End User, and Region |

| Regions covered | North America, Europe, APAC, LATAM, MEA |

The dental bone graft substitutes industry is largely driven by a rising prevalence of dental diseases, such as tooth loss, periodontitis, and maxillofacial defects. This surge has increased the demand for effective bone regeneration solutions. Additionally, the growing popularity of dental implants and advanced restorative materials has significantly increased demand for high-quality graft materials.

Innovations in graft substitutes, such as xenografts, allografts, and synthetic alternatives, have led to better clinical outcomes, greater predictability, and greater convenience, making them the preferred choice among dental practitioners. Furthermore, the growing awareness of oral health among patients and clinicians, along with the expansion of dental facilities and specialized surgical services, has positively impacted market growth.

The combination of clinical needs, technological advancements, and heightened patient awareness is driving the global demand for dental bone graft substitutes.

"By application, resins are expected to hold the largest market share in the dental bone graft substitutes market."

In the dental bone graft substitutes market, the socket preservation segment holds the largest share. This is due to its frequent use during the postoperative period following tooth extractions and its crucial role in preserving alveolar bone stock. After a tooth extraction, rapid bone resorption may eventually necessitate the placement of dental implants. As a result, socket preservation is a viable option within the dental bone graft substitutes market. Dental bone graft substitutes are typically placed immediately after an extraction to stabilize the socket and promote bone formation. Tooth extractions are quite common worldwide for various reasons, including dental caries, periodontal disease, and trauma, underscoring the importance of the socket preservation market. This segment is widely appreciated in the industry for its ease of application and predictable outcomes, making it a favored choice among dentists across specialties.

"By end user, hospitals are expected to hold the largest share in the dental bone graft substitutes market."

In the dental bone graft substitutes market, hospitals hold a significant market share. This is largely due to their established clinical settings and ability to treat a large number of patients while performing various complex dental and oral surgeries. For example, hospitals are equipped to handle cases requiring dental and jaw reconstruction procedures that involve bone grafting substitutes. These cases include dental implant procedures, periodontal treatments, and jaw rebuilding or reconstruction surgeries. Bone graft substitutes are essential for all dental and jaw surgeries, given the high technical and clinical demands of these procedures. Additionally, dental and jaw departments in hospitals are well-established and efficiently managed, thereby enhancing their capacity to use these substitutes effectively. Consequently, hospitals are considered the primary end-user facilities for dental bone substitutes.

"The US is expected to grow at the highest CAGR in the North American dental bone graft substitutes market during the forecast period."

The dental bone graft substitutes market in North America is expected to grow at the highest rate in the US, driven by several key factors. A growing aging population and an increasing prevalence of age-related dental issues, such as tooth loss and periodontitis, are driving the demand for dental substitutes in the country. Additionally, the presence of a favorable dental care infrastructure and a greater acceptance of innovative dental technologies are contributing to the growth of dental bone graft substitutes in America. Furthermore, the rising use of dental procedures like dental implantology, along with increasing awareness of dental and periodontal health among dental surgeons and conscientious consumers, is also supporting the expansion of this market. Collectively, these factors have positioned the US as the leading market for dental bone graft substitutes in North America.

A breakdown of the primary participants (on the supply side) for the dental bone graft substitutes market referenced in this report is provided below:

- By Company Type: Tier 1 (35%), Tier 2 (40%), and Tier 3 (25%)

- By Designation: C-level Executives (45%), Directors (35%), and Others (20%)

- By Region: North America (27%), Europe (25%), Asia Pacific (30%), Latin America (8%), and the Middle East & Africa (10%)

The prominent players in the dental bone graft substitutes market are Dentsply Sirona (US), Envista (US), Johnson & Johnson (US), Institut Straumann AG (Switzerland), Medtronic (Ireland), Zimvie Inc. (US), Henry Schein Inc. (US), RTI Surgical (US), and LifeNet Health (US).

Research Coverage:

The report provides an analysis of the dental bone graft substitutes market, focusing on estimating its size and future growth potential across segments such as product, application, type, mechanism, end user, and region. Additionally, the report features a competitive analysis of key players in the market, including their company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report provides valuable insights for both market leaders and new entrants in the dental bone graft substitutes market, offering the most accurate revenue estimates. It helps stakeholders understand the competitive landscape, enabling them to better position their businesses and develop effective go-to-market strategies. Additionally, the report highlights key market drivers, restraints, challenges, and opportunities, giving stakeholders a comprehensive understanding of current market trends.

This report provides insights into the following pointers:

- Analysis of key drivers (growing market for dental tourism in emerging countries, increasing disposable income in developing counties, rising cases of dental caries and subsequent increase in tooth repair procedures, and changing demographics), restraints (lack of proper reimbursement scenario, stringent regulations pertaining to medical devices used in dentistry, and dearth of trained dental practitioners), opportunities (increasing demand from customers and rising inclination towards cosmetic dentistry, low penetration rates for dental bone graft substitutes, consolidation of dental practices and rising DSO activity, and growing demand for bone graft substitutes from emerging markets), and challenges (pricing pressure faced by prominent market players).

- Market Penetration: It includes extensive information on the products offered by the major players in the global dental bone graft substitutes market. The report includes various segments, such as products, applications, types, mechanisms, end users, and regions.

- Product Enhancement/Innovation: Comprehensive details about new product launches and anticipated trends in the global dental bone graft substitutes market.

- Market Development: Thorough knowledge and analysis of the profitable rising markets by product, type, mechanism, application, end user, and region.

- Market Diversification: Comprehensive information about newly launched products, expanding markets, current advancements, and investments in the global dental bone graft substitutes market.

- Competitive Assessment: A comprehensive assessment of market shares, growth strategies, product offerings, and capabilities of key competitors in the global dental bone graft substitutes market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 KEY STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND MARKET DEVELOPMENTS

- 2.2 DISRUPTIVE TRENDS SHAPING MARKET

- 2.3 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.4 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 DENTAL BONE GRAFT SUBSTITUTES MARKET OVERVIEW

- 3.2 ASIA PACIFIC: DENTAL BONE GRAFT SUBSTITUTES MARKET, BY TYPE AND COUNTRY, (2025)

- 3.3 DENTAL BONE GRAFT SUBSTITUTES MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.4 DENTAL BONE GRAFT SUBSTITUTES MARKET, REGIONAL MIX, 2024-2031

- 3.5 DENTAL BONE GRAFT SUBSTITUTES MARKET: EMERGING VS. DEVELOPED MARKETS

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growth of dental tourism in emerging countries

- 4.2.1.2 Increasing disposable income in developing countries

- 4.2.1.3 Rising cases of dental caries and subsequent increase in tooth repair procedures

- 4.2.1.4 Changing demographics

- 4.2.2 RESTRAINTS

- 4.2.2.1 Lack of proper reimbursement scenario

- 4.2.2.2 Stringent regulations pertaining to medical devices used in dentistry

- 4.2.2.3 Dearth of trained dental practitioners

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing demand from customers and rising inclination toward cosmetic dentistry

- 4.2.3.2 Consolidation of dental practices and rising DSO activity

- 4.2.3.3 Growing demand for bone graft substitutes from emerging markets

- 4.2.4 CHALLENGES

- 4.2.4.1 Pricing pressure faced by prominent market players

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER- 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN DENTAL BONE GRAFT SUBSTITUTES MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND, BY KEY PLAYER, 2023-2025

- 5.6.2 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA FOR HS CODE 3006

- 5.7.2 EXPORT DATA FOR HS CODE 3006

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 CASE STUDY 1: SINUS FLOOR ELEVATION AND RIDGE AUGMENTATION USING GEISTLICH BIO-OSS

- 5.9.2 CASE STUDY 2: RIDGE PRESERVATION AND BONE REGENERATION USING NOVABONE DENTAL PUTTY

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 IMPACT OF US TARIFFS-DENTAL BONE GRAFT SUBSTITUTES MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USER INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 GROWTH FACTOR-ENHANCED BONE GRAFTS

- 6.1.2 SYNTHETIC BIOMIMETIC BONE GRAFT MATERIALS

- 6.1.3 GUIDED BONE REGENERATION TECHNOLOGY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 BARRIER MEMBRANE TECHNOLOGY

- 6.2.2 TITANIUM MESH TECHNOLOGY

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 COMPUTER-GUIDED IMPLANT PLANNING SOFTWARE

- 6.3.2 CONE-BEAM COMPUTED TOMOGRAPHY

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM | RECENT TECHNOLOGIES| FOUNDATION & EARLY COMMERCIALIZATION

- 6.4.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.4.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.5 PATENT ANALYSIS

- 6.5.1 PATENT PUBLICATION TRENDS

- 6.5.2 JURISDICTION ANALYSIS

- 6.6 IMPACT OF AI/GEN AI ON DENTAL BONE GRAFT SUBSTITUTES MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.6.3 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN DENTAL BONE GRAFT SUBSTITUTES MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 INSTITUT STRAUMANN/BOTISS: CAD/CAM CUSTOMIZED BONE BLOCK FOR RIDGE AUGMENTATION

- 6.7.2 DENTSPLY SIRONA: AI-POWERED DIGITAL WORKFLOW WITH SYMBIOS REGENERATIVE PORTFOLIO

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.2.1 North America

- 7.1.2.1.1 US

- 7.1.2.1.2 Canada

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.3.1 China

- 7.1.2.3.2 Japan

- 7.1.2.4 Latin America

- 7.1.2.4.1 Brazil

- 7.1.2.4.2 Mexico

- 7.1.2.5 Middle East

- 7.1.2.6 Africa

- 7.1.2.1 North America

- 7.2 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

9 DENTAL BONE GRAFT SUBSTITUTES MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 SYNTHETIC BONE GRAFTS

- 9.2.1 INCREASING TECHNOLOGICAL ADVANCEMENTS TO DRIVE ADOPTION OF SYNTHETIC BONE GRAFTS

- 9.3 XENOGRAFTS

- 9.3.1 RISING ADOPTION OF ADVANCED XENOGRAFT MATERIALS SUPPORTED BY TECHNOLOGICAL IMPROVEMENTS TO DRIVE MARKET

- 9.4 ALLOGRAFTS

- 9.4.1 GROWING PREFERENCE FOR ALLOGRAFTS DUE TO REDUCED SURGICAL BURDEN

- 9.4.2 DEMINERALIZED BONE MATRIX

- 9.4.2.1 Demineralized bone possesses more osteoinductive properties

- 9.4.3 OTHER ALLOGRAFTS

- 9.5 OTHER DENTAL BONE GRAFT SUBSTITUTES

10 DENTAL BONE GRAFT SUBSTITUTES MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 SOCKET PRESERVATION

- 10.2.1 SOCKET PRESERVATION REDUCES BONE LOSS AFTER TOOTH EXTRACTION

- 10.3 RIDGE AUGMENTATION

- 10.3.1 RIDGE AUGMENTATION RECREATES NATURAL CONTOUR OF GUMS AND JAW

- 10.4 PERIODONTAL DEFECT REGENERATION

- 10.4.1 CHANGES IN LIFESTYLE AND EATING HABITS TO LEAD TO USE OF DENTAL BONE GRAFT SUBSTITUTES FOR PERIODONTAL DEFECT REGENERATION

- 10.5 IMPLANT BONE REGENERATION

- 10.5.1 UTILIZATION OF GUIDED BONE REGENERATION MEMBRANES FACILITATES HEALING OF GRAFTED MATERIAL

- 10.6 SINUS LIFT

- 10.6.1 SINUS AUGMENTATION RAISES SINUS FLOOR AND DEVELOPS BONE FOR PLACEMENT OF DENTAL IMPLANTS

11 DENTAL BONE GRAFT SUBSTITUTES MARKET, BY MECHANISM

- 11.1 INTRODUCTION

- 11.2 OSTEOCONDUCTION

- 11.2.1 OSTEOCONDUCTION SERVES AS A SCAFFOLD FOR BONE CELLS TO ATTACH, MIGRATE, GROW, AND DIVIDE

- 11.3 OSTEOINDUCTION

- 11.3.1 OSTEOINDUCTION FACILITATES BONE HEALING PROCESS

- 11.4 OSTEOPROMOTION

- 11.4.1 OSTEOPROMOTION INVOLVES ENHANCEMENT OF OSTEOINDUCTION WITHOUT POSSESSION OF OSTEOINDUCTIVE PROPERTIES

- 11.5 OSTEOGENESIS

- 11.5.1 OSTEOGENESIS PLAYS CRUCIAL ROLE IN FACILITATING SUCCESSFUL BONE REGENERATION AND REPAIR

12 DENTAL BONE GRAFT SUBSTITUTES MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 DENTAL HOSPITALS

- 12.2.1 INCREASING NUMBER OF COSMETIC DENTISTRY PROCEDURES ACROSS DENTAL HOSPITALS TO DRIVE MARKET GROWTH

- 12.3 DENTAL CLINICS

- 12.3.1 EASY ACCESS AND AVAILABILITY OF HIGH-QUALITY SERVICES TO DRIVE MARKET GROWTH

- 12.4 OTHER END USERS

13 DENTAL BONE GRAFT SUBSTITUTES MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 13.2.2 US

- 13.2.2.1 Increasing patient awareness about advantages of dental bone graft substitutes over traditional treatments to boost growth

- 13.2.3 CANADA

- 13.2.3.1 Rising geriatric population to propel market expansion

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 13.3.2 GERMANY

- 13.3.2.1 Country's robust health insurance system to drive popularity of dental bone graft substitutes

- 13.3.3 UK

- 13.3.3.1 Preference for costly procedures due to the availability of reimbursement facilities to lead to potential growth

- 13.3.4 FRANCE

- 13.3.4.1 Rising awareness among people regarding benefits of dental bone graft substitutes and presence of major players to drive growth

- 13.3.5 ITALY

- 13.3.5.1 Intensive R&D and use of sophisticated materials to manufacture advanced products to propel market

- 13.3.6 SPAIN

- 13.3.6.1 Government initiatives to provide dental cover to people to boost market

- 13.3.7 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 13.4.2 JAPAN

- 13.4.2.1 Increasing awareness, availability of reimbursement, and growing income levels to offer growth opportunities for market players

- 13.4.3 CHINA

- 13.4.3.1 Growing geriatric population, economic boom, and increasing per capita income to propel growth

- 13.4.4 INDIA

- 13.4.4.1 Diverse, lucrative opportunities offered to dental product and service providers to ensure adequate market progress

- 13.4.5 AUSTRALIA

- 13.4.5.1 Popularity of xenograft and allograft to open new opportunities for growth of market players

- 13.4.6 SOUTH KOREA

- 13.4.6.1 Rising geriatric population and medical tourism to drive market

- 13.4.7 REST OF ASIA PACIFIC

- 13.5 LATIN AMERICA

- 13.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 13.5.2 BRAZIL

- 13.5.2.1 Improving healthcare infrastructure and rising investments by leading players to spur demand

- 13.5.3 MEXICO

- 13.5.3.1 Rising medical tourism to support market growth

- 13.5.4 ARGENTINA

- 13.5.4.1 Growing demand for personalized dentistry to spur market demand

- 13.5.5 REST OF LATIN AMERICA

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 GROWING INVESTMENTS IN DIGITAL HEALTHCARE INDUSTRY TO BOOST DEMAND FOR DENTAL BONE GRAFT SUBSTITUTES

- 13.6.2 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 13.7 GCC COUNTRIES

- 13.7.1 INCREASING DEMAND FOR HEALTH SERVICES DUE TO POPULATION GROWTH TO DRIVE MARKET FOR DENTAL BONE GRAFT SUBSTITUTES

- 13.7.2 MACROECONOMIC OUTLOOK FOR GCC COUNTRIES

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN DENTAL BONE GRAFT SUBSTITUTES MARKET

- 14.3 REVENUE ANALYSIS

- 14.4 MARKET SHARE ANALYSIS (2025)

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.5.1 COMPANY VALUATION

- 14.5.2 FINANCIAL METRICS

- 14.6 BRAND/PRODUCT COMPARISON

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT (KEY PLAYERS), 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Type footprint

- 14.7.5.4 APPLICATION Footprint

- 14.7.5.5 Mechanism Footprint

- 14.7.5.6 End-user footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES (2025)

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of startups/SMEs

- 14.9 R&D EXPENDITURE OF KEY PLAYERS (DENTAL BONE GRAFT SUBSTITUTES MARKET)

- 14.10 COMPETITIVE SCENARIO

- 14.10.1 PRODUCT LAUNCHES AND APPROVALS

- 14.10.2 DEALS

- 14.10.3 EXPANSIONS

- 14.10.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 DENTSPLY SIRONA INC.

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches and approvals

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 ENVISTA

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.3.2 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 INSTITUT STRAUMANN AG

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.3.2 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 ADVANCED MEDICAL SOLUTIONS GROUP PLC

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Deals

- 15.1.5 ZIMVIE INC.

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches and approvals

- 15.1.5.3.2 Deals

- 15.1.6 HENRY SCHEIN, INC.

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.6.3.2 Expansions

- 15.1.6.4 MnM view

- 15.1.6.4.1 Right to win

- 15.1.6.4.2 Strategic choices

- 15.1.6.4.3 Weaknesses and competitive threats

- 15.1.7 EVERGEN (FORMERLY RTI SURGICAL)

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.7.3.2 Other developments

- 15.1.8 LIFENET HEALTH

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches and approvals

- 15.1.8.3.2 Deals

- 15.1.9 NOVABONE

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product launches and approvals

- 15.1.9.3.2 Deals

- 15.1.10 GEISTLICH PHARMA AG

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.3.2 Other developments

- 15.1.1 DENTSPLY SIRONA INC.

- 15.2 OTHER PLAYERS

- 15.2.1 BOTISS BIOMATERIALS GMBH

- 15.2.2 REGENITY

- 15.2.3 OSTEOGENIC BIOMEDICAL

- 15.2.4 HANNOX INTERNATIONAL CORP

- 15.2.5 KEYSTONE DENTAL GROUP

- 15.2.6 YOUNG INNOVATIONS INC

- 15.2.7 BEGO GMBH &CO.KG

- 15.2.8 TISSUE REGENIX GROUP

- 15.2.9 DENTIUM CO., LTD

- 15.2.10 MEDBONE

- 15.2.11 PURGO BIOLOGICS INC

- 15.2.12 REGEDENT AG

- 15.2.13 TECNOSS DENTAL SRL

- 15.2.14 SIGMAGRAFT BIOMATERIALS

- 15.2.15 CITAGENIX

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 16.4 MARKET SHARE ESTIMATION

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 RESEARCH LIMITATIONS

- 16.6.1 SCOPE-RELATED LIMITATIONS

- 16.6.2 METHODOLOGY-RELATED LIMITATIONS

- 16.7 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS