|

시장보고서

상품코드

2082817

데이터센터 솔루션 시장 : 컴포넌트별, 워크로드 유형별, Tier 유형별, 데이터센터 규모별, 데이터센터 유형별, 지역별 - 예측(-2031년)Data Center Solutions Market by Infrastructure, Software (DCIM, BMS) - Forecast to 2031 |

||||||

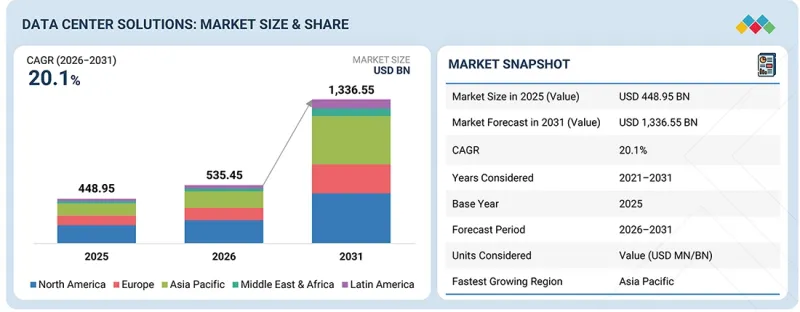

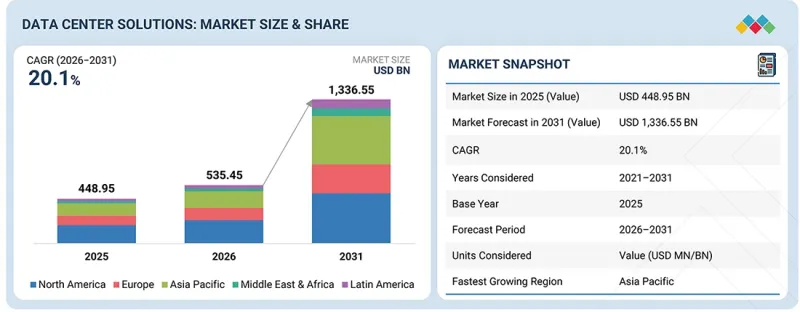

세계의 데이터센터 솔루션 시장 규모는 인공지능(AI), 클라우드 컴퓨팅 및 고성능 컴퓨팅(HPC) 인프라에 대한 투자 확대를 배경으로, 강력한 성장을 이루고 있습니다.

해당 시장은 2026년 535억 4,500만 달러에서 2031년까지 1조 3,365억 5,000만 달러로 확대될 것으로 예상되며, 예측 기간 동안 연평균 성장률(CAGR)은 20.1%를 기록할 것으로 전망됩니다. AI 훈련 및 추론 워크로드의 도입이 확대됨에 따라, 고밀도 컴퓨팅 환경, 첨단 스토리지 시스템, 고속 네트워크 및 차세대 냉각 기술에 대한 수요가 가속화되고 있습니다. 이러한 성장은 클라우드 제공업체와 디지털 플랫폼 기업들이 증가하는 컴퓨팅 및 데이터 처리 요구 사항에 대응하기 위해 데이터센터용량을 지속적으로 확대하고 있는 데 따라, 하이퍼스케일 투자 주기에 의해 더욱 가속화되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(100만/10억 달러) |

| 부문 | 컴포넌트별, 워크로드 유형별, Tier 유형별, 데이터센터 규모별, 데이터센터 유형별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

동시에, 지속가능성 관련 노력과 규제 체계의 발전에 따라 사업자들은 에너지 효율이 높은 설계, 액체 냉각 기술, 그리고 지능형 인프라 관리 솔루션을 통해 전력 및 냉각 인프라의 현대화를 추진하도록 장려받고 있습니다. 그러나 시장에서는 여전히 주요 전기·기계 설비의 긴 리드타임, 공급망 제약, 주요 데이터센터 허브의 전력 공급 안정성에 대한 우려가 커지고 있는 등의 과제에 직면해 있습니다. 또한, 인허가 절차의 복잡성, 부지 확보 문제, 송전망 연결 지연 등이 프로젝트 일정에 영향을 미칠 가능성이 있습니다. 이러한 요인들이 복합적으로 작용하여 전 세계 데이터센터 솔루션 시장 전반에 걸친 투자 우선순위, 기술 도입 및 인프라 개발의 방향성을 결정짓고 있습니다.

'예측 기간 동안 액체 냉각이 가장 높은 성장률을 나타낼 것으로 전망됩니다.'

액체 냉각 부문은 기존 엔터프라이즈 용도보다 훨씬 더 높은 열 부하를 발생시키는 AI, 머신러닝 및 고성능 컴퓨팅(HPC) 워크로드가 급속히 확대되고 있는 만큼, 데이터센터 솔루션 시장에서 가장 높은 연평균 성장률(CAGR)을 보일 것으로 예측됩니다. 랙의 전력 밀도가 30 kW를 점점 더 상회하고, 많은 AI 도입 사례에서 랙당 60-100 kW를 초과함에 따라 기존 공랭식 시스템의 효율은 떨어지고 에너지 소비량도 증가하고 있습니다. 직접 투 칩(Direct-to-Chip), 리어 도어 방식 열교환기, 침지 냉각 시스템 등의 액체 냉각 기술은 뛰어난 방열 성능을 제공하여, 사업자가 더 높은 연산 밀도를 지원하면서도 최적의 성능을 유지할 수 있도록 합니다. 하이퍼스케일 클라우드 제공업체, 코로케이션 사업자 및 기업들의 GPU 기반 AI 클러스터 도입 확대가 이 기술의 채택을 뒷받침하는 주요 요인이 되고 있습니다. 또한, 액체 냉각은 냉각 인프라와 관련된 에너지 소비를 줄이는 데에도 기여하여, 전력 사용 효율(PUE)을 높이고 지속가능성 목표 달성을 지원합니다. 또한, 기존 시설 내에서 데이터센터의 용량을 극대화해야 한다는 압박이 커지고 있는 만큼, 사업자들은 대개 액체 냉각이 필요한 고밀도 인프라 도입을 추진하고 있습니다. 기업들이 AI에 대응할 수 있고 에너지 효율이 높은 데이터센터에 투자함에 따라, 예측 기간 동안 첨단 액체 냉각 솔루션에 대한 수요는 기존 냉각 기술보다 더 빠르게 증가할 것으로 예측됩니다.

'예측 기간 동안 Tier 3 유형이 가장 큰 시장 점유율을 차지할 것으로 전망됩니다.'

Tier 3 데이터센터는 고가용성, 운영 신뢰성 및 비용 효율성 간의 균형을 모두 달성할 수 있기 때문에 데이터센터 솔루션 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 이러한 시설은 전원, 냉각, 네트워크 시스템 등 주요 인프라 구성 요소 전반에 걸쳐 N+1 중복성을 갖추도록 설계되어 있어, 운영을 중단하지 않고도 유지보수 작업을 수행할 수 있습니다. 이러한 수준의 내결함성 덕분에 Tier 3 시설은 미션 크리티컬 용도의 지속적인 가동이 필요한 기업, 클라우드 서비스 제공업체, 금융 기관, 코로케이션 사업자에게 최적의 선택지가 되고 있습니다. 클라우드 컴퓨팅, AI 워크로드, 디지털 서비스, 하이브리드 IT 환경의 도입이 확대됨에 따라, 예측 가능한 성능과 운영 연속성을 제공하는 인프라에 대한 수요가 증가하고 있습니다.

Tier 3 시설에는 일반적으로 이중화된 UPS 시스템, 예비 발전기, 첨단 냉각 솔루션, 지능형 전력 배전 시스템 및 데이터센터 인프라 관리(DCIM) 플랫폼이 도입되어 있어 효율성과 신뢰성을 최적화하고 있습니다. 또한, 높은 가용성을 유지하면서 확장 가능한 확장에 대응할 수 있다는 점은 현대 기업 및 클라우드 도입의 요구 사항에 부합합니다. 조직들이 내결함성이 높고 비용 대비 효과가 뛰어난 디지털 인프라에 대한 투자를 지속함에 따라, Tier 3 시설은 계속해서 선호되는 도입 모델로 자리매김할 것이며, 예측 기간 동안 시장에서 주도적인 위치를 유지할 것으로 예측됩니다.

'북미는 선진적인 디지털 인프라, 기업들의 적극적인 도입, 그리고 전 세계 기술 공급업체들의 집적 덕분에 데이터센터 솔루션 시장을 선도하고 있습니다. 아시아태평양은 급속한 디지털 전환, 클라우드 및 AI 도입 확대, 그리고 현대적인 데이터센터 인프라에 대한 정부 주도의 대규모 투자에 힘입어 가장 빠르게 성장하고 있는 지역입니다.'

북미는 성숙한 디지털 인프라 생태계, 클라우드의 적극적인 도입, 대규모 하이퍼스케일 투자, 그리고 주요 기술 기업 및 코로케이션 제공업체의 존재에 힘입어 데이터센터 솔루션 시장을 주도하고 있습니다. 이 지역에서는 확대되는 AI, 클라우드 및 고성능 컴퓨팅 워크로드를 처리하기 위해 대규모 데이터센터 개발에 대한 막대한 투자가 계속 이루어지고 있습니다. 예를 들어, 2026년 6월, 디지털 리얼티(Digital Realty)는 캔자스주에 600 MW 규모의 하이퍼스케일 데이터센터 단지를 건설할 계획을 발표했습니다. 장기적인 확장 잠재력은 2GW에 달할 것으로 예상되며, 이는 미국 내 대규모 디지털 인프라에 대한 지속적인 수요를 반영하고 있습니다. 버지니아주 북부, 텍사스주, 피닉스, 캔자스주 등 주요 시장에서 데이터센터의 수용 능력, 전력 인프라, 냉각 기술 및 연결 솔루션에 대한 지속적인 투자가 북미의 선도적 입지를 공고히 하고 있습니다.

아시아태평양은 급속한 디지털 전환, 클라우드 도입 확대, AI 도입 확대, 그리고 디지털 인프라 개발에 대한 정부의 강력한 지원에 힘입어, 예측 기간 동안 가장 빠른 성장세를 보일 것으로 예측됩니다. 중국, 인도, 일본, 싱가포르, 호주 등의 국가들은 클라우드 서비스, 디지털 용도 및 데이터 집약적 워크로드에 대한 수요 증가에 대응하기 위해 데이터센터용량 확대에 막대한 투자를 하고 있습니다. 또한, 해당 지역에서는 기업의 디지털화 진전, 5G 보급, 재생에너지를 활용한 데이터센터에 대한 투자도 긍정적인 요인으로 작용하고 있습니다. 이러한 요인들로 인해 서버, 스토리지 시스템, 네트워크 인프라, 전력 관리, 냉각 기술, 자동화 플랫폼 등 해당 지역 전체에 걸친 첨단 데이터센터 솔루션에 대한 수요가 가속화되고 있습니다.

본 보고서에는 데이터센터 솔루션 시장의 주요 기업에 대한 조사 결과가 포함되어 있습니다. 데이터센터 솔루션 시장의 주요 공급업체를 소개합니다. 주요 시장 진출기업으로는 Dell Technologies(미국), Broadcom(미국), Nvidia(미국), HPE(미국), Supermicro Computer Inc.(미국), Lenovo(중국), 슈나이더 일렉트릭(프랑스), 화웨이(중국), IBM(미국), 시스코(미국), 버티브(미국), VMware(미국), 이튼(아일랜드), 웨스턴 디지털(미국), 지멘스(독일), DDC 솔루션스(미국), Palo Alto Networks(미국), ABB(스위스), Arista(미국), Nutanix(미국), Pure Storage(미국), 다이킨(일본), Rittal(독일), 3M(미국), Coolit Systems(캐나다), 그리고 Delta Electronics(대만) 등이 있습니다.

조사 범위

본 조사 보고서에서는 데이터센터 솔루션 시장을 구성 요소(인프라(데이터센터 전력 인프라, 데이터센터 기계·냉각 인프라, 데이터센터 IT·네트워크 인프라, 데이터센터 물리적 인프라)), 소프트웨어(DCIM 소프트웨어, 건물/시설 관리 소프트웨어, 가상화·오케스트레이션 소프트웨어, 규정 준수·보안 소프트웨어, 애널리틱스·AIOps 소프트웨어))), 워크로드 유형(HPC·AI, 범용 IT), 티어 유형(Tier 1, Tier 2, Tier 3, Tier 4), 데이터센터 규모(소규모 데이터센터, 중규모 데이터센터, 대규모 데이터센터), 데이터센터 유형(하이퍼스케일 데이터센터, 코로케이션 데이터센터, 엔터프라이즈 데이터센터), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카)에 따라 분류하고 있습니다. 본 보고서의 조사 범위에는 데이터센터 솔루션 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 제약 요인, 과제, 기회 등)에 대한 상세 정보가 포함되어 있습니다. 주요 업계 진출 기업에 대한 상세한 분석을 통해 각 기업의 사업 개요, 솔루션 및 서비스, 주요 전략, 계약·제휴·합의, 신제품 및 서비스 출시, 합병·인수, 그리고 데이터센터 솔루션 시장의 최근 동향에 대한 인사이트를 제공합니다. 또한, 본 보고서에서는 데이터센터 솔루션 시장 생태계에서 두각을 나타내고 있는 스타트업 기업에 대한 경쟁 분석도 다루고 있습니다.

이 보고서를 구매해야 하는 이유

본 보고서는 이 시장의 선도 기업 및 신규 진출기업을 대상으로, 데이터센터 솔루션 시장 전체 및 그 하위 부문의 매출액에 관한 가장 정확한 추정치를 제공합니다. 이를 통해 이해관계자들은 경쟁 구도를 파악하고, 자사의 비즈니스를 더 유리한 위치로 이끌며, 적절한 시장 진출 전략을 수립하기 위한 추가적인 인사이트를 얻을 수 있습니다. 또한, 이해관계자들이 시장 동향을 파악하고, 주요 시장 성장 촉진요인, 억제요인, 과제 및 기회에 관한 정보를 얻는 데 도움이 됩니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다.

- 주요 촉진요인 분석(AI 및 고성능 컴퓨팅(HPC) 인프라 도입 확대가 첨단 데이터센터 솔루션 수요를 견인하고 있음; 하이퍼스케일 AI 데이터센터에 대한 투자 확대가 데이터센터 솔루션 수요를 견인하고 있음; 지속가능성 관련 규제가 에너지 효율이 높은 데이터센터 솔루션에 대한 투자를 촉진하고 있음), 제약 요인(송전망 인프라의 제약 및 지연되는 상호 연결 일정이 데이터센터 확장을 제한하고 있음; 고조되는 환경 문제에 대한 우려와 지역 사회의 반발이 데이터센터 개발을 지연시키고 있음), 기회(AI 대응을 위한 개조 수요 증가가 데이터센터 인프라 및 서비스 전반에 기회를 창출하고 있음; 지속가능성에 대한 투자 확대가 에너지 효율이 높은 데이터센터 솔루션에 대한 수요를 견인하고 있음; 액체 냉각 기술 채택 확대가 AI 데이터센터 인프라에 기회를 창출하고 있음), 과제(숙련된 인력 부족이 데이터센터의 확장 및 운영에 과제를 야기하고 있음; AI 워크로드 밀도 증가가 전력 및 인프라 관리상의 과제를 야기하고 있음)

- 제품 개발/혁신 : 데이터센터 솔루션 시장의 향후 기술, 연구 개발 활동 및 신제품 및 서비스 출시에 관한 상세한 인사이트

- 시장 개발: 수익성이 높은 시장에 대한 종합적인 정보 - 본 보고서에서는 다양한 지역에 걸친 데이터센터 솔루션 시장을 분석했습니다.

- 시장의 다양화: 데이터센터 솔루션 시장의 신제품 및 서비스, 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁사 분석 : Dell Technologies(미국), HPE(미국), Broadcom(미국), NVIDIA(미국), Super Micro Computer, Inc.(미국), IBM(미국), Lenovo(홍콩), Schneider Electric(프랑스), Cisco(미국), Huawei(중국), DDC Solutions(미국), Western Digital(미국), Vertiv(미국), Arista Networks(미국), NetApp(미국), Pure Storage(미국), Eaton(아일랜드), Rittal(독일), Cummins(미국), Caterpillar(미국), GE Vernova(미국), ABB(스위스), Delta Electronics(대만), Siemens(독일), Fujitsu(일본), Sunbird Software(미국), Legrand(프랑스), Modine(미국), Stulz(독일), Chatsworth Products(미국), Device42(미국), CoolIT Systems(캐나다), Submer(스페인), Active Power(미국), Green Revolution Cooling(미국), Riello UPS(이탈리아). 또한, 본 보고서는 이해관계자들이 데이터센터 솔루션 시장 동향을 파악하는 데 도움이 되며, 주요 시장 성장 촉진요인, 제약 요인, 과제 및 기회에 대한 정보를 제공합니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 테크놀러지, 특허, 디지털 기술, AI 도입에 의한 전략적 파괴

제7장 규제 상황

제8장 고객 현황과 구매 행동

제9장 데이터센터 솔루션 시장(컴포넌트별)

제10장 데이터센터 솔루션 시장(워크로드 유형별)

제11장 데이터센터 솔루션 시장(Tier 유형별)

제12장 데이터센터 솔루션 시장(데이터센터 규모별)

제13장 데이터센터 솔루션 시장(데이터센터 유형별)

제14장 데이터센터 솔루션 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

LSH 26.07.14The global data center solutions market is experiencing strong growth, driven by rising investments in artificial intelligence (AI), cloud computing, and high-performance computing (HPC) infrastructure. The market is projected to grow from USD 535.45 billion in 2026 to USD 1,336.55 billion by 2031, registering a CAGR of 20.1% during the forecast period. Increasing deployment of AI training and inference workloads is accelerating demand for high-density compute environments, advanced storage systems, high-speed networking, and next-generation cooling technologies. This growth is further supported by a hyperscale investment cycle, as cloud providers and digital platform companies continue expanding data center capacity to meet rising compute and data processing requirements.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Component, Workload Type, Tier Type, Data Center Size, Data Center Type |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

At the same time, sustainability initiatives and evolving regulatory frameworks are encouraging operators to modernize power and cooling infrastructure through energy-efficient designs, liquid cooling technologies, and intelligent infrastructure management solutions. However, the market continues to face challenges related to long lead times for critical electrical and mechanical equipment, supply chain constraints, and growing concerns about power availability in major data center hubs. In addition, permitting complexities, land acquisition challenges, and grid connection delays can affect project timelines. Together, these factors are shaping investment priorities, technology adoption, and infrastructure development across the global data center solutions market.

"Liquid cooling to account for the fastest growth rate during the forecast period"

The liquid cooling segment is expected to register the fastest CAGR in the data center solutions market due to the rapid growth of AI, machine learning, and high-performance computing (HPC) workloads, which generate significantly higher heat loads than traditional enterprise applications. As rack power densities increasingly exceed 30 kW and, in many AI deployments, surpass 60-100 kW per rack, conventional air-cooling systems are becoming less effective and more energy-intensive. Liquid cooling technologies, including direct-to-chip, rear-door heat exchangers, and immersion cooling systems, provide superior heat dissipation, enabling operators to maintain optimal performance while supporting higher compute densities. The increasing deployment of GPU-based AI clusters by hyperscale cloud providers, colocation operators, and enterprises is a major factor driving adoption. Liquid cooling also helps reduce energy consumption associated with cooling infrastructure, improving Power Usage Effectiveness (PUE) and supporting sustainability objectives. In addition, growing pressure to maximize data center capacity within existing facilities is encouraging operators to deploy high-density infrastructure that often requires liquid cooling. As organizations invest in AI-ready, energy-efficient data centers, demand for advanced liquid cooling solutions is expected to grow faster than for traditional cooling technologies throughout the forecast period.

"Tier 3 type to hold the largest market share during the forecast period"

Tier 3 data centers are expected to account for the largest share of the data center solutions market due to their ability to provide a balance between high availability, operational reliability, and cost efficiency. These facilities are designed with N+1 redundancy across critical infrastructure components, including power, cooling, and network systems, enabling maintenance activities without disrupting operations. This level of resilience makes Tier 3 facilities the preferred choice for enterprises, cloud service providers, financial institutions, and colocation operators that require continuous uptime for mission-critical applications. The growing adoption of cloud computing, AI workloads, digital services, and hybrid IT environments is increasing demand for infrastructure that delivers predictable performance and operational continuity.

Tier 3 facilities typically incorporate redundant UPS systems, backup generators, advanced cooling solutions, intelligent power distribution systems, and data center infrastructure management (DCIM) platforms to optimize efficiency and reliability. In addition, their ability to support scalable expansion while maintaining high availability aligns with the requirements of modern enterprise and cloud deployments. As organizations continue investing in resilient and cost-effective digital infrastructure, Tier 3 facilities are expected to remain the preferred deployment model, supporting their leading market position throughout the forecast period.

"North America leads the data center solutions market with advanced digital infrastructure, strong enterprise adoption, and a concentration of global technology providers. Asia Pacific is the fastest-growing region, fueled by rapid digital transformation, expanding cloud and AI deployments, and significant government-led investment in modern data center infrastructure."

North America leads the data center solutions market, supported by a mature digital infrastructure ecosystem, strong cloud adoption, extensive hyperscale investments, and the presence of major technology companies and colocation providers. The region continues to witness significant investments in large-scale data center developments to support growing AI, cloud, and high-performance computing workloads. For example, in June 2026, Digital Realty announced plans for a 600 MW hyperscale data center campus in Kansas, with long-term expansion potential reaching 2 GW, reflecting continued demand for large-scale digital infrastructure across the US. Ongoing investments in data center capacity, power infrastructure, cooling technologies, and connectivity solutions across key markets such as Northern Virginia, Texas, Phoenix, and Kansas are reinforcing North America's leadership position.

Asia Pacific is expected to register the fastest growth during the forecast period, driven by rapid digital transformation, increasing cloud adoption, expanding AI deployments, and strong government support for digital infrastructure development. Countries such as China, India, Japan, Singapore, and Australia are investing heavily in data center capacity expansion to support growing demand for cloud services, digital applications, and data-intensive workloads. The region is also benefiting from increasing enterprise digitization, 5G deployment, and investments in renewable energy-powered data centers. These factors are accelerating demand for advanced data center solutions across the region, including servers, storage systems, networking infrastructure, power management, cooling technologies, and automation platforms.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the data center solutions market.

- By Company: Tier I - 30%, Tier II - 45%, and Tier III - 25%

- By Designation: C-Level Executives - 50%, D-Level Executives -35%, and others - 15%

- By Region: North America - 50%, Europe - 30%, Asia Pacific - 15%, and Rest of the world - 5%

The report includes a study of key players in the data center solutions market. It profiles major vendors in the data center solutions market. The major market players include Dell Technologies (US), Broadcom (US), Nvidia (US), HPE (US), Supermicro Computer Inc. (US), Lenovo (China), Schneider Electric (France), Huawei (China), IBM (US), Cisco (US), Vertiv (US), VMware (US), Eaton (Ireland), Western Digital (US), Siemens (Germany), DDC Solutions (US), Palo Alto Network (US), ABB (Switzerland), Arista (US), Nutanix (US), Pure Storage (US), Daikin (Japan), Rittal (Germany), 3M (US), Coolit Systems (Canada), and Delta Electronics (Taiwan).

Research Coverage

This research report categorizes the data center solutions market based on Component (Infrastructure (Data Center Power Infrastructure, Data Center Mechanical & Cooling Infrastructure, Data Center IT & Networking Infrastructure, Data Center Physical Infrastructure), Software (DCIM Software, Building/Facility Management Software, Virtualization & Orchestration Software, Compliance & Security Software, Analytics & AIOps Software)), Workload Type (HPC & AI, General Purpose IT), Tier Type (Tier 1, Tier 2, Tier 3, Tier 4), Data Center Size (Small Data Centers, Medium-Sized Data Centers, Large Data Centers), Data Center Type (Hyperscale Data Center, Colocation Data Center, Enterprise Data Center), and Region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the data center solutions market. A detailed analysis of the key industry players was conducted to provide insights into their business overviews, solutions and services; key strategies; contracts, partnerships, agreements, new product & service launches, and mergers and acquisitions; and recent developments in the data center solutions market. Competitive analysis of upcoming startups in the data center solutions market ecosystem was also covered in this report.

Reason to buy this Report

The report would provide the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall data center solutions market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Increasing deployment of AI and high-performance computing (HPC) infrastructure driving demand for advanced data center solutions; Growing hyperscale AI data center investments driving demand for data center solutions; Sustainability regulations driving investments in energy-efficient data center solutions), restraints (Grid infrastructure constraints and long interconnection timelines limiting data center expansion; Rising environmental concerns and community resistance slowing data center development), opportunities (Rising demand for AI-ready retrofits creating opportunities across data center infrastructure and services; Growing sustainability investments driving demand for energy-efficient data center solutions; Increasing adoption of liquid cooling technologies creating opportunities in AI data center infrastructure), and challenges (Shortage of skilled workforce creating challenges for data center expansion and operations; Increasing AI workload density creating power and infrastructure management challenges)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the data center solutions market

- Market Development: Comprehensive information about lucrative markets - the report analyses the data center solutions market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the data center solutions market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players such Dell Technologies (US), HPE (US), Broadcom (US), NVIDIA (US), Super Micro Computer, Inc. (US), IBM (US), Lenovo (Hong Kong), Schneider Electric (France), Cisco (US), Huawei (China), DDC Solutions (US), Western Digital (US), Vertiv (US), Arista Networks (US), NetApp (US), Pure Storage (US), Eaton (Ireland), Rittal (Germany), Cummins (US), Caterpillar (US), GE Vernova (US), ABB (Switzerland), Delta Electronics (Taiwan), Siemens (Germany), Fujitsu (Japan), Sunbird Software (US), Legrand (France), Modine (US), Stulz (Germany), Chatsworth Products (US), Device42 (US), CoolIT Systems (Canada), Submer (Spain), Active Power (US), Green Revolution Cooling (US), and Riello UPS (Italy). The report also helps stakeholders understand the pulse of the data center solutions market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN DATA CENTER SOLUTIONS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DATA CENTER SOLUTIONS MARKET

- 3.2 DATA CENTER SOLUTIONS MARKET, BY COMPONENT

- 3.3 DATA CENTER SOLUTIONS MARKET, BY INFRASTRUCTURE

- 3.4 DATA CENTER SOLUTIONS MARKET, BY SOFTWARE

- 3.5 DATA CENTER SOLUTIONS MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing Deployment of AI and High-performance Computing (HPC) Infrastructure Driving Demand for Advanced Data Center Solutions

- 4.2.1.2 Growing Hyperscale AI Data Center Investments Driving Demand for Data Center Solutions

- 4.2.1.3 Sustainability Regulations Driving Investments in Energy-efficient Data Center Solutions

- 4.2.2 RESTRAINTS

- 4.2.2.1 Grid Infrastructure Constraints and Long Interconnection Timelines Limiting Data Center Expansion

- 4.2.2.2 Rising Environmental Concerns and Community Resistance Slowing Data Center Development

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising Demand for AI-ready Retrofits Creates Opportunities Across Data Center Infrastructure and Services

- 4.2.3.2 Growing Sustainability Investments Driving Demand for Energy-efficient Data Center Solutions

- 4.2.3.3 Growing Adoption of Liquid Cooling Technologies Creating Opportunities in AI Data Center Infrastructure

- 4.2.4 CHALLENGES

- 4.2.4.1 Shortage of Skilled Workforce Creating Challenges for Data Center Expansion and Operations

- 4.2.4.2 Increasing AI Workload Density Creating Power and Infrastructure Management Challenges

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN DATA CENTER SOLUTIONS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.1.1 Data center solutions business models

- 4.5.2 ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECASTS

- 5.2.3 TRENDS IN GLOBAL DATA CENTER POWER INDUSTRY

- 5.2.4 TRENDS IN GLOBAL DATA CENTER COOLING INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 IDENTIFIED STAKEHOLDERS FOR THE SUPPLY CHAIN OF DATA CENTER SOLUTIONS MARKET COMPRISE THE FOLLOWING:

- 5.4.1 COMPONENT & TECHNOLOGY PROVIDERS

- 5.4.2 INFRASTRUCTURE EQUIPMENT & SOFTWARE VENDORS

- 5.4.3 SYSTEM INTEGRATORS, EPCS & MANAGED SERVICE PROVIDERS

- 5.4.4 DATA CENTER OPERATORS & SERVICE PROVIDERS

- 5.4.5 END USERS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE (ASP) TREND OF DATA CENTER UPS, BY REGION, 2025

- 5.6.1.1 AVERAGE SELLING PRICE OF DATA-CENTER UPS FOR HYPERSCALE DEPLOYMENTS, 2025

- 5.6.1 AVERAGE SELLING PRICE (ASP) TREND OF DATA CENTER UPS, BY REGION, 2025

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 CASE STUDY 1: OXIGEN INTEGRATES VERTIV'S FREE COOLING AND ENERGY-SAVING TECHNOLOGY INTO ITS NEW HIGH-PERFORMANCE DATA CENTER

- 5.10.2 CASE STUDY 2: EATON ENHANCES POWER RESILIENCE AND IT UPTIME FOR UNIVERSITY OF WINCHESTER

- 5.10.3 CASE STUDY 3: ED NETZE DEPLOYS NEXT-GEN SUBSTATION WITH PURE AIR MV SWITCHGEAR

- 5.10.4 CASE STUDY 4: CAT POWER SYSTEMS DRIVE LONG-TERM UPTIME FOR SCOTT DATA CENTER

- 5.10.5 CASE STUDY 5: STULZ DELIVERS REDUNDANT, ENERGY-EFFICIENT COOLING FOR DEUTSCHE BAHN'S BATTERY TRAIN CHARGING SUBSTATION

- 5.11 IMPACT OF 2025 US TARIFF - DATA CENTER SOLUTIONS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON VERTICALS

- 5.11.5.1 Hyperscale Data Centers

- 5.11.5.2 Colocation Data Centers

- 5.11.5.3 Enterprise Data Centers

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Direct-to-chip (D2C) Liquid Cooling

- 6.1.1.2 Immersion Cooling

- 6.1.1.3 AIOps & Digital Twins

- 6.1.1.4 High-density GPU infrastructure

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Lithium-ion and Next-generation Battery Energy Storage Systems (BESS)

- 6.1.2.2 Software-defined Networking (SDN)

- 6.1.2.3 Hyper-converged Infrastructure (HCI)

- 6.1.2.4 Modular Power Infrastructure

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Small Modular Reactors (SMRs)

- 6.1.3.2 Direct Air Capture (DAC) and Carbon Removal Co-Location

- 6.1.3.3 Private 5G/6G and Edge Connectivity

- 6.1.3.4 Grid-interactive Data Centers

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 SHORT-TERM (2026-2028) | AI-READY INFRASTRUCTURE & OPERATIONAL EFFICIENCY

- 6.2.2 MID-TERM (2028-2031) | AUTONOMOUS OPERATIONS & ENERGY OPTIMIZATION

- 6.2.3 LONG-TERM (2031-2036+) | AUTONOMOUS, SUSTAINABLE & DISTRIBUTED DIGITAL INFRASTRUCTURE

- 6.3 PATENT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 AUTONOMOUS AI-DRIVEN DATA CENTER OPERATIONS & PREDICTIVE MANAGEMENT

- 6.4.2 CARBON-AWARE AND SELF-OPTIMIZING DATA CENTERS

- 6.4.3 GRID-INTERACTIVE AND ENERGY-ORCHESTRATED DATA CENTERS

- 6.4.4 DISTRIBUTED EDGE-TO-CORE AI INFRASTRUCTURE

- 6.4.5 DIGITAL TWIN-POWERED AUTONOMOUS INFRASTRUCTURE MANAGEMENT

- 6.5 IMPACT OF AI/GENERATIVE AI ON DATA CENTER SOLUTIONS MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES IN DATA CENTER SOLUTIONS

- 6.5.3 CASE STUDY OF AI IMPLEMENTATION IN DATA CENTER GENERATOR MARKET

- 6.5.3.1 Schneider Electric Improves Asset Performance Through AI-driven Monitoring and Predictive Maintenance

- 6.5.3.2 GE VERNOVA & CRUSOE ADVANCE AI DATA CENTER POWER INFRASTRUCTURE WITH AERODERIVATIVE GAS TURBINES

- 6.5.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENT READINESS TO ADOPT GENERATIVE AI IN THE DATA CENTER SOLUTIONS MARKET

- 6.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.6.1 CATERPILLAR: AI-OPTIMIZED ONSITE POWER INFRASTRUCTURE

7 REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS, BY REGION

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Middle East & Africa

- 7.1.2.5 Latin America

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USER INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 DATA CENTER SOLUTIONS MARKET, BY COMPONENT

- 9.1 INTRODUCTION

- 9.1.1 COMPONENT: DATA CENTER SOLUTIONS MARKET DRIVERS

- 9.2 INFRASTRUCTURE

- 9.2.1 GROWTH DRIVEN BY AI WORKLOADS, HIGH-DENSITY COMPUTING, AND DEMAND FOR SCALABLE, ENERGY-EFFICIENT DATA CENTERS

- 9.2.2 DATA CENTER IT & NETWORKING INFRASTRUCTURE

- 9.2.2.1 Servers

- 9.2.2.1.1 Blade Servers

- 9.2.2.1.2 Rackmount Servers

- 9.2.2.1.3 Tower Servers

- 9.2.2.1.4 GPU Servers

- 9.2.2.1.5 Others

- 9.2.2.2 Storage

- 9.2.2.2.1 Direct-attached Storage (DAS)

- 9.2.2.2.2 Network-attached Storage (NAS)

- 9.2.2.2.3 Storage Area Networks (SAN)

- 9.2.2.3 Networking

- 9.2.2.3.1 Switches

- 9.2.2.3.2 Routers

- 9.2.2.3.3 Network Interface Cards (NICs), Data Processing Units (DPUs), and Infrastructure Processing Units (IPUs)

- 9.2.2.3.4 AI & HPC Networking

- 9.2.2.4 Chips

- 9.2.2.4.1 Processors

- 9.2.2.4.2 Power management controllers

- 9.2.2.1 Servers

- 9.2.3 DATA CENTER POWER INFRASTRUCTURE

- 9.2.3.1 Critical Power

- 9.2.3.1.1 Uninterruptible Power Supply (UPS)

- 9.2.3.1.2 Flywheel Energy Storage Systems

- 9.2.3.1.3 Behind-the-Meter (BTM) BESS (Lithium-ion, Advanced Lead-acid, Flow Batteries, Others)

- 9.2.3.1.4 Battery Backup Units (VRLA, Li-ion, NiCd, Others)

- 9.2.3.2 Power Backup

- 9.2.3.2.1 Generators

- 9.2.3.2.2 Gas Turbines

- 9.2.3.2.3 Fuel Cells (Solid Oxide Fuel Cells (SOFC), Proton Exchange Membrane (PEM) Fuel Cells, Other Types)

- 9.2.3.3 Power Distribution

- 9.2.3.3.1 Switchboards

- 9.2.3.3.2 Busways

- 9.2.3.3.3 Power Distribution Units (PDUs)

- 9.2.3.3.4 Power Switching

- 9.2.3.3.5 Remote Power Panels (RPPs) (Wall-mounted, Floor Standing)

- 9.2.3.3.6 Transformers (Oil Immersed, Dry-type)

- 9.2.3.4 Switchgears

- 9.2.3.1 Critical Power

- 9.2.4 DATA CENTER MECHANICAL & COOLING INFRASTRUCTURE

- 9.2.4.1 Air Cooling

- 9.2.4.1.1 Air Conditioning System

- 9.2.4.1.2 Chiller Units

- 9.2.4.1.3 Cooling Towers

- 9.2.4.2 Liquid Cooling

- 9.2.4.2.1 Liquid Cooling Component

- 9.2.4.2.2 Coolant Distribution Units (CDUs)

- 9.2.4.2.3 Heat Exchangers

- 9.2.4.2.4 Data Center Fan Coil Units (FCUs)

- 9.2.4.2.5 Others

- 9.2.4.3 Other Mechanical & Cooling

- 9.2.4.3.1 Economizer systems

- 9.2.4.3.2 Heat Pumps

- 9.2.4.3.3 Insulation Materials

- 9.2.4.3.4 Containment Systems

- 9.2.4.1 Air Cooling

- 9.2.5 DATA CENTER PHYSICAL INFRASTRUCTURE

- 9.2.5.1 Racks

- 9.2.5.1.1 Open Frame Racks

- 9.2.5.1.2 Enclosed Racks

- 9.2.5.1.3 Others

- 9.2.5.2 Cabling

- 9.2.5.2.1 Cables

- 9.2.5.2.2 Power Connectors

- 9.2.5.1 Racks

- 9.3 SOFTWARE

- 9.3.1 DRIVING AUTONOMOUS, RESILIENT, AND DATA-DRIVEN DATA CENTER OPERATIONS THROUGH INTELLIGENT SOFTWARE PLATFORMS

- 9.3.2 DCIM SOFTWARE

- 9.3.2.1 Real-time Monitoring & Asset Tracking

- 9.3.2.2 Capacity Planning & Power Software

- 9.3.2.3 Rack-level Visualization & Environmental Mapping

- 9.3.2.4 Integration with BMS/EPMS Platforms

- 9.3.2.5 Event & Alarm Management

- 9.3.3 BUILDING/FACILITY MANAGEMENT SOFTWARE

- 9.3.3.1 Building Automation Systems (BAS)

- 9.3.3.2 HVAC Control & Optimization Platforms

- 9.3.3.3 Smart Lighting & Energy Efficiency Software

- 9.3.3.4 Maintenance Scheduling & Workflow Tools

- 9.3.3.5 Fire Safety & Emergency Response Management

- 9.3.4 VIRTUALIZATION & ORCHESTRATION SOFTWARE

- 9.3.4.1 Hypervisors (VMware ESXi, KVM, Hyper-V)

- 9.3.4.2 Container Orchestration Platforms (Kubernetes, OpenShift)

- 9.3.4.3 Bare-metal Orchestration Tools

- 9.3.4.4 Hybrid Infrastructure Management (Cloud + On-prem)

- 9.3.4.5 INFRASTRUCTURE AUTOMATION & PROVISIONING PLATFORMS

- 9.3.5 COMPLIANCE & SECURITY SOFTWARE

- 9.3.5.1 Access Control & Identity Management (IAM)

- 9.3.5.2 Data Encryption & Key Management

- 9.3.5.3 Threat Detection & Vulnerability Scanning

- 9.3.5.4 Compliance Monitoring (SOC 2, ISO 27001, GDPR)

- 9.3.5.5 Network Segmentation & Firewall Management

- 9.3.6 ANALYTICS & AIOPS SOFTWARE

- 9.3.6.1 Infrastructure Performance Analytics

- 9.3.6.2 Predictive Maintenance & Anomaly Detection

- 9.3.6.3 Energy Usage Analytics (PUE, DCiE)

- 9.3.6.4 AI-based Workload Forecasting & Resource Allocation

- 9.3.6.5 Thermal Optimization Analytics

10 DATA CENTER SOLUTIONS MARKET, BY WORKLOAD TYPE

- 10.1 INTRODUCTION

- 10.1.1 WORKLOAD TYPE: DATA CENTER SOLUTIONS MARKET DRIVERS

- 10.2 HPC & AI

- 10.2.1 SCALING DATA CENTER INFRASTRUCTURE TO SUPPORT AI MODEL TRAINING, HIGH-DENSITY GPU RACKS, AND LIQUID COOLING NEEDS

- 10.3 GENERAL PURPOSE IT

- 10.3.1 OPTIMIZING MODULAR INFRASTRUCTURE AND ORCHESTRATION TOOLS TO SUPPORT DISTRIBUTED, COST-EFFICIENT GENERAL PURPOSE IT WORKLOADS

11 DATA CENTER SOLUTIONS MARKET, BY TIER TYPE

- 11.1 INTRODUCTION

- 11.1.1 TIER TYPE: DATA CENTER SOLUTIONS MARKET DRIVERS

- 11.2 TIER 1

- 11.2.1 SUPPORTING ENTRY-LEVEL DIGITAL INFRASTRUCTURE WITH ESSENTIAL DATA CENTER SOLUTIONS

- 11.3 TIER 2

- 11.3.1 ENHANCING OPERATIONAL RESILIENCE THROUGH REDUNDANT INFRASTRUCTURE

- 11.4 TIER 3

- 11.4.1 OPTIMIZING HIGH-AVAILABILITY OPERATIONS WITH SCALABLE INFRASTRUCTURE

- 11.5 TIER 4

- 11.5.1 DELIVERING MAXIMUM RESILIENCE FOR MISSION-CRITICAL DIGITAL OPERATIONS

12 DATA CENTER SOLUTIONS MARKET, BY DATA CENTER SIZE

- 12.1 INTRODUCTION

- 12.1.1 DATA CENTER SIZE: DATA CENTER SOLUTIONS MARKET DRIVERS

- 12.2 SMALL DATA CENTERS

- 12.2.1 ENABLING LOCALIZED DIGITAL SERVICES WITH COMPACT INFRASTRUCTURE

- 12.3 MEDIUM DATA CENTERS

- 12.3.1 DRIVING SCALABLE ENTERPRISE GROWTH THROUGH BALANCED INFRASTRUCTURE

- 12.4 LARGE DATA CENTERS

- 12.4.1 POWERING HYPERSCALE AND AI ECOSYSTEMS WITH HIGH-DENSITY INFRASTRUCTURE

13 DATA CENTER SOLUTIONS MARKET, BY DATA CENTER TYPE

- 13.1 INTRODUCTION

- 13.1.1 DATA CENTER TYPE: DATA CENTER SOLUTIONS MARKET DRIVERS

- 13.2 HYPERSCALE DATA CENTERS

- 13.2.1 ENABLING NEXT-GENERATION AI AND CLOUD INFRASTRUCTURE WITH SCALABLE, SOFTWARE-DEFINED, AND ENERGY-EFFICIENT DATA CENTER SOLUTIONS

- 13.3 COLOCATION DATA CENTERS

- 13.3.1 ENABLING FLEXIBLE MULTI-TENANT DIGITAL INFRASTRUCTURE WITH INTELLIGENT, SCALABLE, AND SUSTAINABLE DATA CENTER SOLUTIONS

- 13.4 ENTERPRISE DATA CENTERS

- 13.4.1 MODERNIZING BUSINESS-CRITICAL IT ENVIRONMENTS THROUGH SOFTWARE-DEFINED AND HYBRID CLOUD INFRASTRUCTURE

- 13.5 EDGE DATA CENTERS

- 13.5.1 ENABLING LOW-LATENCY DIGITAL SERVICES THROUGH DISTRIBUTED, COMPACT, AND AUTONOMOUS INFRASTRUCTURE

14 DATA CENTER SOLUTIONS MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Rising AI Infrastructure Investments Accelerate US Data Center Solutions Market

- 14.2.2 CANADA

- 14.2.2.1 Power-integrated Data Center Developments Strengthen Canada's AI Infrastructure

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 UK

- 14.3.1.1 Energy-integrated Infrastructure Advances the UK's Data Center Solutions Market

- 14.3.2 GERMANY

- 14.3.2.1 Sustainable Digital Infrastructure Accelerates Germany's Data Center Solutions Market

- 14.3.3 FRANCE

- 14.3.3.1 Distributed Edge Infrastructure Strengthens France's Data Center Solutions Market

- 14.3.4 ITALY

- 14.3.4.1 Sovereign Digital Infrastructure Investments Accelerate Italy's Data Center Solutions Market

- 14.3.5 REST OF EUROPE

- 14.3.1 UK

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 AI-driven Capacity Expansion Accelerates China's Data Center Solutions Market

- 14.4.2 JAPAN

- 14.4.2.1 Japan Accelerates AI-ready Cloud Infrastructure and Renewable-powered Data Center Development

- 14.4.3 INDIA

- 14.4.3.1 Hyperscale AI Infrastructure Investments Accelerate India's Data Center Solutions Market

- 14.4.4 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 MIDDLE EAST & AFRICA

- 14.5.1 GCC COUNTRIES

- 14.5.1.1 Saudi Arabia

- 14.5.1.1.1 Carrier-neutral AI Infrastructure Investments Accelerate Saudi Arabia's Data Center Solutions Market

- 14.5.1.2 UAE

- 14.5.1.2.1 Sovereign AI Infrastructure Accelerates Data Center Solutions Adoption in UAE

- 14.5.1.3 Other GCC countries

- 14.5.1.1 Saudi Arabia

- 14.5.2 SOUTH AFRICA

- 14.5.2.1 South Africa Strengthens Carrier-neutral Connectivity to Support AI and Cloud Infrastructure Growth

- 14.5.3 REST OF MIDDLE EAST & AFRICA

- 14.5.1 GCC COUNTRIES

- 14.6 LATIN AMERICA

- 14.6.1 BRAZIL

- 14.6.1.1 AI and Cloud Infrastructure Investments Accelerate Data Center Solutions in Brazil

- 14.6.2 MEXICO

- 14.6.2.1 Cloud Region Expansion and Nearshoring Trends Accelerate Demand for Resilient Power Infrastructure

- 14.6.3 REST OF LATIN AMERICA

- 14.6.1 BRAZIL

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 15.3 REVENUE ANALYSIS

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 BRAND/PRODUCT COMPARISON

- 15.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025 (IT INFRASTRUCTURE)

- 15.6.1 STARS

- 15.6.2 EMERGING LEADERS

- 15.6.3 PERVASIVE PLAYERS

- 15.6.4 PARTICIPANTS

- 15.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.6.5.1 Company footprint

- 15.6.5.2 Region footprint

- 15.6.5.3 Component footprint

- 15.6.5.4 Infrastructure footprint

- 15.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.7.1 PROGRESSIVE COMPANIES

- 15.7.2 RESPONSIVE COMPANIES

- 15.7.3 DYNAMIC COMPANIES

- 15.7.4 STARTING BLOCKS

- 15.7.5 COMPETITIVE BENCHMARKING: STARTUP/SMES, 2025

- 15.7.5.1 Detailed list of key startups/SMEs

- 15.7.5.2 Competitive benchmarking of startups/SMEs

- 15.8 COMPANY VALUATION AND FINANCIAL METRICS OF KEY VENDORS

- 15.8.1 COMPANY VALUATION OF KEY VENDORS

- 15.8.2 FINANCIAL METRICS OF KEY VENDORS

- 15.9 COMPETITIVE SCENARIO AND TRENDS

- 15.9.1 PRODUCT LAUNCHES

- 15.9.2 DEALS

16 COMPANY PROFILES

- 16.1 INTRODUCTION

- 16.2 MAJOR PLAYERS

- 16.2.1 DELL TECHNOLOGIES

- 16.2.1.1 Business overview

- 16.2.1.2 Products/Solutions/Services offered

- 16.2.1.3 Recent developments

- 16.2.1.3.1 Product launches

- 16.2.1.3.2 Deals

- 16.2.1.4 MnM view

- 16.2.1.4.1 Right to win

- 16.2.1.4.2 Strategic choices

- 16.2.1.4.3 Weaknesses and competitive threats

- 16.2.2 HPE

- 16.2.2.1 Business overview

- 16.2.2.2 Products/Solutions/Services offered

- 16.2.2.3 Recent developments

- 16.2.2.3.1 Product Launches

- 16.2.2.3.2 Deals

- 16.2.2.4 MnM view

- 16.2.2.4.1 Right to win

- 16.2.2.4.2 Strategic choices

- 16.2.2.4.3 Weaknesses and competitive threats

- 16.2.3 BROADCOM

- 16.2.3.1 Business overview

- 16.2.3.2 Products/Solutions/Services offered

- 16.2.3.3 Recent developments

- 16.2.3.3.1 Product Launches

- 16.2.3.3.2 Deals

- 16.2.3.4 MnM view

- 16.2.3.4.1 Right to win

- 16.2.3.4.2 Strategic choices

- 16.2.3.4.3 Weaknesses and competitive threats

- 16.2.4 NVIDIA

- 16.2.4.1 Business overview

- 16.2.4.2 Products/Solutions/Services offered

- 16.2.4.3 Recent developments

- 16.2.4.3.1 Product Launches

- 16.2.4.3.2 Deals

- 16.2.4.4 MnM view

- 16.2.4.4.1 Right to win

- 16.2.4.4.2 Strategic choices

- 16.2.4.4.3 Weaknesses and competitive threats

- 16.2.5 SUPERMICRO COMPUTER INC.

- 16.2.5.1 Business overview

- 16.2.5.2 Products/Solutions/Services offered

- 16.2.5.3 Recent developments

- 16.2.5.3.1 Product Launches

- 16.2.5.3.2 Deals

- 16.2.5.4 MnM view

- 16.2.5.4.1 Right to win

- 16.2.5.4.2 Strategic choices

- 16.2.5.4.3 Weaknesses and competitive threats

- 16.2.6 IBM

- 16.2.6.1 Business overview

- 16.2.6.2 Products/Solutions/Services offered

- 16.2.6.3 Recent developments

- 16.2.6.3.1 Product Launches

- 16.2.6.3.2 Deals

- 16.2.6.3.3 Expansions

- 16.2.7 LENOVO

- 16.2.7.1 Business overview

- 16.2.7.2 Products/Solutions/Services offered

- 16.2.7.3 Recent developments

- 16.2.7.3.1 Product Launches

- 16.2.7.3.2 Deals

- 16.2.7.3.3 Expansions

- 16.2.8 SCHNEIDER ELECTRIC

- 16.2.8.1 Business overview

- 16.2.8.2 Products/Solutions/Services offered

- 16.2.8.3 Recent developments

- 16.2.8.3.1 Product Launches

- 16.2.8.3.2 Deals

- 16.2.8.3.3 Expansions

- 16.2.9 CISCO

- 16.2.9.1 Business overview

- 16.2.9.2 Products/Solutions/Services offered

- 16.2.9.3 Recent developments

- 16.2.9.3.1 Product Launches

- 16.2.9.3.2 Deals

- 16.2.10 HUAWEI

- 16.2.10.1 Business overview

- 16.2.10.2 Products/Solutions/Services offered

- 16.2.10.3 Recent developments

- 16.2.10.3.1 Product Launches

- 16.2.10.3.2 Deals

- 16.2.1 DELL TECHNOLOGIES

- 16.3 OTHER PLAYERS

- 16.3.1 WESTERN DIGITAL CORPORATIONS

- 16.3.2 VERTIV

- 16.3.3 ARISTA NETWORK

- 16.3.4 NETAPP

- 16.3.5 EVEPURE (PURE STORAGE)

- 16.3.6 EATON

- 16.3.7 RITTAL

- 16.3.8 CUMMINS

- 16.3.9 CATERPILLAR

- 16.3.10 GE VERNOVA

- 16.3.11 ABB

- 16.3.12 DELTA ELECTRONICS

- 16.3.13 SIEMENS

- 16.3.14 FUJITSU

- 16.3.15 SUNBIRD

- 16.3.16 LEGRAND

- 16.3.17 MODINE

- 16.3.18 STULZ

- 16.3.19 DDC SOLUTIONS

- 16.3.20 CHATSWORTH PRODUCTS

- 16.3.21 DEVICE42

- 16.3.22 COOLIT SYSTEMS

- 16.3.23 SUBMER

- 16.3.24 ACTIVE POWER

- 16.3.25 GREEN REVOLUTION COOLING

- 16.3.26 REILLO UPS

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Data & List of Key Secondary Sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Breakdown of primary interviews

- 17.1.3 MARKET SIZE ESTIMATION

- 17.1.4 DATA TRIANGULATION

- 17.1.5 FACTOR ANALYSIS

- 17.1.6 RESEARCH ASSUMPTIONS

- 17.1.1 SECONDARY DATA

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS