|

시장보고서

상품코드

2082818

심혈관 중재시술 기기 시장(-2031년) : 유형, 최종사용자별Interventional Cardiology Devices Market by Type, End User - Global Forecast to 2031 |

||||||

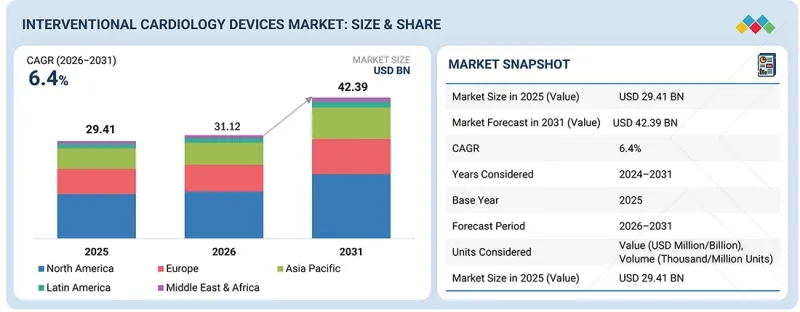

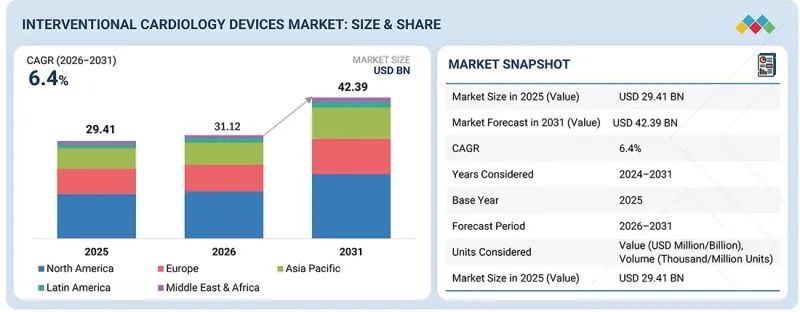

세계의 심혈관 중재시술 기기 시장 규모는 2026년 311억 2,000만 달러에서 2031년에는 423억 9,000만 달러에 이를 것으로 예측되며, 예측 기간에는 CAGR 6.4%를 기록할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 유형, 최종사용자, 지역 |

| 대상 지역 | 아시아태평양, 북미, 유럽, 라틴아메리카, 중동 및 아프리카 |

세계 심혈관 중재시술 기기 시장은 심혈관 질환 발병률 증가, 최소 침습적 치료법에 대한 선호, 세계 인구의 고령화 등의 요인을 주된 이유로 성장하고 있습니다. 또한, 약물 방출형 스텐트, 생체 흡수성 스캐폴드, 카테터를 활용한 영상 진단 기술의 발전과 같은 의료 기술의 혁신을 통해 치료의 안전성과 성공률이 향상되고 있습니다. 또한, 개발도상국의 의료시설 확충, 선진 지역에서의 치료를 촉진하는 보험 환급 정책의 도입, 심장 질환 검진 및 치료에 대한 소비자의 인식 제고 역시 시장 성장에 기여하고 있습니다.

'혈관성형술의 풍선 유형별로 보면, 기존/표준형 풍선 부문이 가장 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 예측됩니다.'

혈관성형술용 풍선의 경우, 저렴한 비용과 임상 현장에서의 폭넓은 수용성, 특히 개발도상국이나 비용 효율을 중시하는 의료 환경에서 일상적으로 시행되는 경피적 관상동맥 중재술(PCI) 및 1차 치료법에서의 높은 사용률 덕분에, 기존/표준형 부문이 지속적인 성장을 이어가고 있습니다. 스텐트 삽입을 위한 병변 준비나, 합병증이 없는 관상동맥 및 말초혈관 시술에 빈번하게 사용되고 있으며, 이러한 점이 수요 유지에 기여하고 있습니다. 또한, 입증된 안전성, 사용 편의성, 폭넓은 사이즈 라인업 덕분에 사례가 많은 병원에서 선호되는 선택지로 자리 잡고 있으며, 특수 풍선 기술 개발이 진행되고 있음에도 불구하고 시장의 지속적인 성장에 기여하고 있습니다.

'혈역학 및 혈류 조절 기기 부문에서는 색전 방지 기기 부문이 가장 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 예측됩니다.'

심혈관 및 신경혈관 중재술, 특히 경카테터 대동맥판막 치환술(TAVR), 경동맥 스텐트 삽입술, 말초혈관 시술이 혈류역학 변화 기기 시장에서 색전 방지 기기의 매출 증가를 이끄는 주요 동력이 되고 있습니다. 이러한 기기들은 시술의 부작용으로 발생할 수 있는 뇌졸중이나 말초 허혈을 예방함으로써, 더 많은 환자를 치료하고 임상 결과를 개선하는 데 기여하고 있습니다. 이 시장의 성장은 더 우수한 필터, 더 효율적인 포집, 더 용이한 투여를 가능하게 하는 기술적 진보뿐만 아니라, 긍정적인 임상 증거와 고령층을 대상으로 한 최소 침습 시술의 인기가 높아짐에 힘입어 뒷받침되고 있습니다.

'최종 사용자별로 보면, 병원 부문이 가장 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 예측됩니다.'

혈관성형술, 스텐트 삽입술, 구조적 심장질환 중재술 등 대부분의 심혈관 중재술은 양질의 환자 치료를 뒷받침하는 전문 시설과 첨단 영상 진단 기술을 갖춘 병원에서 시행되고 있습니다. 병원에는 간단한 것부터 복잡한 것까지 모든 처치에 대응할 수 있는 시설이 갖춰져 있습니다. 이러한 환경 덕분에 순환기 전문의는 약물 방출형 스텐트, 회전식 아테렉토미, 혈관 내 초음파 검사 등의 최신 기술을 활용하여 환자에게 최고의 정확성과 안전성을 보장할 수 있습니다.

본 보고서에서는 전 세계 심혈관 중재시술 기기 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 현황, 주요 기업 프로파일 등을 정리했습니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 현황과 구매 행동

제9장 혈관성형술용 스텐트 시장 : 유형별

제10장 구조적 심질환용 기기 시장 : 유형별

제11장 카테터 시장 : 유형별

제12장 혈관성형술용 풍선 시장 : 유형별

제13장 플라크 수식 기기 시장 : 유형별

제14장 혈행 동태 및 혈류 변경 기기 시장 : 유형별

제15장 기타 심혈관 중재시술 기기 시장 : 유형별

제16장 심혈관 중재시술 기기 시장 : 최종사용자별

제17장 심혈관 중재시술 기기 시장 : 지역별

제18장 경쟁 구도

제19장 기업 개요

제20장 조사 방법

제21장 부록

LSH 26.07.14The global interventional cardiology devices market is projected to reach USD 42.39 billion by 2031, from USD 31.12 billion in 2026, growing at a CAGR of 6.4% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Type, End User, and Region |

| Regions covered | Asia Pacific, North America, Europe, Latin America, and the Middle East and Africa. |

The worldwide interventional cardiology devices market is growing mainly because of factors such as a higher incidence of cardiovascular diseases, a preference for less invasive procedures, and an aging global population. In addition, innovations in medical technology, such as drug-eluting stents, bioresorbable scaffolds, and enhanced imaging with catheter-based techniques, are making procedures safer and more successful. Furthermore, the spread of better healthcare facilities in developing countries, the introduction of reimbursement policies that encourage treatment in developed regions, and higher consumer awareness of heart disease detection and treatment are also contributing to market growth.

"Based on the angioplasty balloon type, the old/normal balloons segment is expected to grow by the highest CAGR in the interventional cardiology devices market."

The old or normal (plain) angioplasty balloons segment of the angioplasty balloons market is growing due to low cost, general acceptance in clinical practice, and high usage in routine and first-line percutaneous coronary interventions, especially in developing and cost-sensitive healthcare settings. They are frequently used to prepare the lesion for stent placement and in uncomplicated coronary and peripheral procedures, which helps maintain demand. Moreover, their established safety record, user-friendliness, and the wide range of available sizes make them the preferred option in high-volume hospitals, thereby contributing to the continuous growth of the market, even though there have been developments in the technologies for specialty balloons.

"The embolic protection devices segment in the hemodynamic flow alteration devices segment is expected to grow with the highest CAGR in the interventional cardiology devices market."

Cardiovascular and neurovascular interventions, especially transcatheter aortic valve replacement (TAVR), carotid artery stenting, and peripheral vascular procedures, are the main drivers of increased sales of embolic protection devices in the hemodynamic flow alteration device market. These devices, which prevent strokes and distal ischemia that may occur as a side effect of the procedure, have led to more patients being treated and better clinical outcomes. Market growth is supported by technological advancements that yield better filters, more efficient capture, and easier deliverability, as well as by positive clinical evidence and the rising popularity of minimally invasive procedures among the elderly.

"The guidewires segment in the other devices segment is expected to grow with the highest CAGR in the interventional cardiology devices market."

Growth in the interventional cardiology devices market's guidewires segment is primarily driven by the rising incidence of surgical interventions involving percutaneous coronary angioplasty, a direct result of the global rise in cardiovascular diseases. Guidewires are among the most essential items for interventional procedures, creating steady demand in hospitals and catheterization labs. Emerging technologies, such as improved torque control, greater flexibility, hydrophilic coatings, and enhanced lesion-crossing ability, have expanded their use in complex and chronic total occlusion procedures. In addition, the growing preference for minimally invasive treatments, expanding healthcare infrastructure in developing countries, and the large number of procedures performed in both diagnostic and therapeutic interventions continue to support the market growth.

"Based on the end user, the hospital segment is expected to grow by the highest CAGR in the interventional cardiology devices market.

Most interventional cardiology procedures, such as angioplasties, stent placements, and structural heart interventions, are performed in hospitals because they offer specialized facilities and sophisticated imaging technologies that support high-quality patient care. Hospitals are well-equipped for both simple and complex procedures. These settings enable cardiologists to apply the latest technologies, including drug-eluting stents, rotational atherectomy, and intravascular ultrasound, to ensure utmost precision and safety for patients.

"The Asia Pacific is expected to grow with the highest CAGR in the interventional cardiology devices market during the forecast period."

The rise in cardiovascular diseases and the growing number of catheter-based heart surgeries performed in hospital settings have been the main drivers of growth in the interventional cardiology devices market. Hospitals are major end users, where complex and high-risk interventions are carried out because of their advanced infrastructure, the presence of skilled interventional cardiologists, and access to hybrid operating rooms and cath labs. The increasing use of minimally invasive techniques, favorable reimbursement for inpatient and outpatient cardiac interventions, and hospitals' ongoing investment in advanced interventional technologies also support their dominance and contribute to market growth.

The breakup of the profile of primary participants in the interventional cardiology devices market:

- By Company Type: Tier 1- 35%, Tier 2- 45%, and Tier 3-20%

- By Designation: C-level Executives- 35%, Directors- 25% , and Others- 40%.

- By Region: North America - 40%, Europe - 30%, APAC -20%, Latin America - 5%,Middle East & Africa-5%

Key players in the interventional cardiology devices market

Some of the prominent players operating in the interventional cardiology devices market include Boston Scientific Corporation (US), Medtronic (US), Abbott (US), B. Braun SE (Germany), Terumo Corporation (Japan), Edwards Lifesciences Corporation (US), Koninklijke Philips N.V. (Netherlands), Integer Holdings Corporation (US), Teleflex Incorporated (US), Penumbra, Inc. (US), Cook (US), Cordis (US), iVascular S.L.U (Spain), Biosensors International Group, Ltd (Singapore), BIOTRONIK SE & Co. KG (Germany), AMG International (Germany), ENDOCOR GmbH (Germany), InSitu Technologies, Inc. (US), Meril Life Sciences (India), Alvimedica (Istanbul), Cardionovum GmBH (Germany), Medinol Ltd (Turkey), Wellinq (Netherlands), Balton SP (Poland), Translumina (India).

Research Coverage:

The report analyzes the interventional cardiology devices market and aims to estimate the market size and future growth potential across segments such as angioplasty stents, structural heart devices, catheters, angioplasty balloons, plaque modification devices, hemodynamic flow alteration devices, other devices, and end users. The report also includes a product portfolio matrix of the interventional cardiology technologies available in the market. The report also provides a competitive analysis of the key players in this market, along with their company profiles, product offerings, and key market strategies.

Reasons to Buy the Report

The report will provide market leaders and new entrants in this market with the closest available estimates of revenue for the overall interventional cardiology devices market and its subsegments. It will help stakeholders understand the competitive landscape and gain insights to position their businesses more effectively and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides information on key market drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (Growing prevalence of cardiovascular diseases, Technological Advancements in interventional cardiology procedures, Increased prevalence of diabetes), restraints (Availability of alternative treatments, Recall of Products by Industry Participants to Limit the Uptake of Interventional Cardiology Equipment), opportunities (Growing Coronary Stent Demand in Developing Countries, Growing Product Launches by Leading Players in Developing Countries) challenges (Stringent regulatory requirements delaying the approval of cardiac devices)

- Product Enhancement/Innovation: Comprehensive details about new product launches and anticipated trends in the global interventional cardiology devices market.

- Product Development/Innovation: Detailed insights on upcoming trends, research & development activities, and new product launches in the global interventional cardiology devices market

- Market Development: Comprehensive information on the lucrative emerging markets by angioplasty stents, structural heart devices, catheters, angioplasty balloons, plaque modification devices, hemodynamic flow alteration devices, other devices, and end users.

- Market Diversification: Exhaustive information about new products and services or product and service enhancements, growing geographies, recent developments, and investments in the global interventional cardiology devices market.

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings of products and services, and capacities of the major competitors in the global interventional cardiology devices market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 MARKET STAKEHOLDERS

- 1.5 LIMITATIONS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN INTERVENTIONAL CARDIOLOGY DEVICES MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 INTERVENTIONAL CARDIOLOGY DEVICES MARKET OVERVIEW

- 3.2 ASIA PACIFIC: INTERVENTIONAL CARDIOLOGY DEVICES MARKET, BY END USER AND COUNTRY (2025)

- 3.3 INTERVENTIONAL CARDIOLOGY MARKET: REGION (2026-2031)

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising global burden of cardiovascular diseases

- 4.2.1.2 Technological advancements and innovations in interventional cardiology devices

- 4.2.1.3 Increasing prevalence of diabetes

- 4.2.1.4 Growing adoption of minimally invasive cardiac procedures

- 4.2.1.5 Reimbursement coverage for interventional cardiology procedures

- 4.2.2 RESTRAINTS

- 4.2.2.1 Risk of procedure-related complications

- 4.2.2.2 Product recalls and safety concerns

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 High growth potential in emerging markets

- 4.2.3.2 Increasing adoption of structural heart therapies

- 4.2.4 CHALLENGES

- 4.2.4.1 Stringent regulatory requirements for product approvals

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS IN INTERVENTIONAL CARDIOLOGY DEVICES MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES IN INTERVENTIONAL CARDIOLOGY DEVICES MARKET

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL MEDICAL DEVICE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 MANUFACTURERS

- 5.5.2 END USERS

- 5.5.3 REGULATORY BODIES

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF INTERVENTIONAL CARDIOLOGY DEVICES, BY TYPE, 2023-2025

- 5.6.2 AVERAGE SELLING PRICE TREND OF INTERVENTIONAL CARDIOLOGY DEVICES, BY REGION, 2023-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA (HS CODE 9018)

- 5.7.2 EXPORT DATA FOR (HS CODE 9018)

- 5.7.3 IMPORT DATA (HS CODE 9021)

- 5.7.4 EXPORT DATA FOR (HS CODE 9021)

- 5.8 REIMBURSEMENT SCENARIO

- 5.9 KEY CONFERENCES & EVENTS, 2026-2027

- 5.10 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.11 INVESTMENT & FUNDING SCENARIO

- 5.12 CASE STUDY ANALYSIS

- 5.13 IMPACT OF 2025 US TARIFFS ON INTERVENTIONAL CARDIOLOGY DEVICES MARKET

- 5.13.1 INTRODUCTION

- 5.13.2 KEY TARIFF RATES

- 5.13.3 PRICE IMPACT ANALYSIS

- 5.13.4 IMPACT ON COUNTRY/REGION

- 5.13.5 IMPACT ON END-USE SEGMENTS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Advanced imaging & AI-assisted guidance systems

- 6.1.1.2 Robotics & precision navigation technologies

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Advanced intravascular imaging modalities

- 6.1.2.2 Intravascular imaging (IVUS/OCT)

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Wearables & remote monitoring integrated with interventional care

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 NEAR TERM (2025-2027)

- 6.2.2 MID TERM (2028-2030)

- 6.2.3 LONG TERM (2030+)

- 6.3 PATENT ANALYSIS

- 6.3.1 JURISDICTION & TOP APPLICANT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 AI-ENABLED & DATA-DRIVEN PROCEDURE OPTIMIZATION

- 6.4.2 PERSONALIZED CARDIOVASCULAR INTERVENTIONS

- 6.4.3 CONNECTED CARDIOVASCULAR WORKFLOWS & DIGITAL INTEGRATION

- 6.5 IMPACT OF AI/GEN AI ON INTERVENTIONAL CARDIOLOGY DEVICES

- 6.5.1 INTRODUCTION

- 6.5.2 MARKET POTENTIAL OF AI IN INTERVENTIONAL CARDIOLOGY DEVICES

- 6.5.3 AI USE CASES

- 6.5.4 KEY COMPANIES IMPLEMENTING AI

7 SUSTAINABILITY & REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY FRAMEWORK

- 7.1.1.1 North America

- 7.1.1.2 Europe

- 7.1.1.3 Asia Pacific

- 7.1.1.4 Latin America

- 7.1.1.5 Middle East & Africa

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.1.1 REGULATORY FRAMEWORK

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 REDUCING SINGLE-USE MEDICAL DEVICE WASTE

- 7.2.2 USE OF LOWER-IMPACT MATERIALS AND PACKAGING

- 7.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 KEY STAKEHOLDERS & BUYING CRITERIA

- 8.1.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.1.2 BUYING CRITERIA

- 8.2 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.2.1 DECISION-MAKING PROCESS

- 8.2.2 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.2.3 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.2.4 MARKET PROFITABILITY

9 ANGIOPLASTY STENTS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.1.1 DRUG-ELUTING STENTS

- 9.1.1.1 Superior clinical outcomes and ongoing product innovations to support market growth

- 9.1.1.2 Global volume analysis of drug-eluting stents, 2024-2031 (Thousand units)

- 9.1.2 BARE-METAL STENTS

- 9.1.2.1 Cost advantages and continued adoption in resource-constrained healthcare settings to support demand

- 9.1.2.2 Global volume analysis of bare-metal stents, 2024-2031 (Thousand units)

- 9.1.3 BIOABSORBABLE STENTS

- 9.1.3.1 Advancements in resorbable scaffold technologies to boost segmental growth

- 9.1.3.2 Global volume analysis of bioabsorbable stents, 2024-2031 (Thousand units)

- 9.1.1 DRUG-ELUTING STENTS

10 STRUCTURAL HEART DEVICES MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.1.1 AORTIC VALVE THERAPY DEVICES

- 10.1.1.1 Rising burden of aortic stenosis and expanding adoption of TAVI procedures to fuel growth

- 10.1.1.2 Global volume analysis of aortic valve therapy devices, 2024-2031 (Thousand units)

- 10.1.2 OTHER THERAPY DEVICES

- 10.1.2.1 Global volume analysis of other therapy devices, 2024-2031 (Thousand units)

- 10.1.1 AORTIC VALVE THERAPY DEVICES

11 CATHETERS MARKET, BY TYPE

- 11.1 INTRODUCTION

- 11.1.1 ANGIOGRAPHY CATHETERS

- 11.1.1.1 Growing cardiovascular disease burden and advancements in catheter technologies to support market growth

- 11.1.1.2 Global volume analysis of angiography catheters market, 2024-2031 (Thousand units)

- 11.1.2 GUIDING CATHETERS

- 11.1.2.1 Growing adoption of complex coronary interventions to drive market growth

- 11.1.2.2 Global volume analysis of guiding catheters market, 2024-2031 (Thousand units)

- 11.1.3 IVUS/OCT CATHETERS

- 11.1.3.1 Increasing adoption of intravascular imaging technologies to drive demand

- 11.1.3.2 Global volume analysis of IVUS/OCT catheters market, 2024-2031 (Thousand units)

- 11.1.1 ANGIOGRAPHY CATHETERS

12 ANGIOPLASTY BALLOONS MARKET, BY TYPE

- 12.1 INTRODUCTION

- 12.1.1 OLD/NORMAL BALLOONS

- 12.1.1.1 Low treatment costs associated with old/normal balloons to drive growth

- 12.1.1.2 Global volume analysis of old/normal balloons market, 2024-2031 (Thousand units)

- 12.1.2 DRUG-ELUTING BALLOONS

- 12.1.2.1 Increasing regulatory approvals and expanding clinical adoption to contribute to market growth

- 12.1.2.2 Global volume analysis of drug eluting balloons market, 2024-2031 (Thousand units)

- 12.1.3 CUTTING/SCORING BALLOONS

- 12.1.3.1 Increasing use in complex and calcified lesion treatment to support segmental growth

- 12.1.3.2 Global volume analysis of cutting/scoring balloons market, 2024-2031 (Thousand units)

- 12.1.1 OLD/NORMAL BALLOONS

13 PLAQUE MODIFICATION DEVICES MARKET, BY TYPE

- 13.1 INTRODUCTION

- 13.1.1 THROMBECTOMY DEVICES

- 13.1.1.1 Ability to remove blood clots in STEMI and NSTEMI patients to propel market

- 13.1.1.2 Global volume analysis of thrombectomy devices market, 2024-2031 (Thousand units)

- 13.1.2 ATHERECTOMY DEVICES

- 13.1.2.1 Growing burden of calcified coronary lesions to drive market growth

- 13.1.2.2 Global volume analysis of atherectomy devices market, 2024-2031 (thousand units)

- 13.1.1 THROMBECTOMY DEVICES

14 HEMODYNAMIC FLOW ALTERATION DEVICES MARKET, BY TYPE

- 14.1 INTRODUCTION

- 14.1.1 EMBOLIC PROTECTION DEVICES

- 14.1.1.1 Expanding use of high-risk cardiovascular interventions to propel market growth

- 14.1.1.2 Global volume analysis of embolic protection devices market, 2024-2031 (Thousand units)

- 14.1.2 CHRONIC TOTAL OCCLUSION DEVICES

- 14.1.2.1 Rising complexity of coronary lesions to fuel market growth

- 14.1.2.2 Global volume analysis of chronic total occlusion devices market, 2024-2031 (Thousand units)

- 14.1.1 EMBOLIC PROTECTION DEVICES

15 OTHER INTERVENTIONAL CARDIOLOGY DEVICES MARKET, BY TYPE

- 15.1 INTRODUCTION

- 15.1.1 GUIDEWIRES

- 15.1.1.1 Increasing adoption in complex coronary interventions to support market growth

- 15.1.1.2 Global volume analysis of guidewires market, 2024-2031 (Thousand units)

- 15.1.2 VASCULAR CLOSURE DEVICES

- 15.1.2.1 Increasing focus on faster hemostasis and reduced access-site complications to aid market growth

- 15.1.2.2 Global volume analysis of vascular closure devices market, 2024-2031 (Thousand units)

- 15.1.3 INTRODUCER SHEATHS

- 15.1.3.1 Increasing demand for safe and reliable vascular access to support market growth

- 15.1.3.2 Global volume analysis of introducer sheaths market, 2024-2031 (Thousand units)

- 15.1.4 BALLOON INFLATION DEVICES

- 15.1.4.1 Rising adoption of balloon-based interventions in minimally invasive procedures to boost market growth

- 15.1.4.2 Global volume analysis of balloon inflation devices market, 2024-2031 (Thousand units)

- 15.1.5 HEMOSTASIS HEART VALVES

- 15.1.5.1 Increasing focus on procedural precision and controlled hemostasis to support market growth

- 15.1.5.2 Global volume analysis of hemostasis heart valves market, 2024-2031 (Thousand units)

- 15.1.1 GUIDEWIRES

16 INTERVENTIONAL CARDIOLOGY DEVICES MARKET, BY END USER

- 16.1 INTRODUCTION

- 16.2 HOSPITALS

- 16.2.1 AVAILABILITY OF ADVANCED INFRASTRUCTURE AND SPECIALIZED EQUIPMENT TO DRIVE MARKET

- 16.3 AMBULATORY SURGERY CENTERS

- 16.3.1 SHIFT TOWARD COST-EFFICIENT AND OUTPATIENT-BASED CARE MODELS TO SUPPORT MARKET GROWTH

- 16.4 CARDIAC CARE CENTERS

- 16.4.1 GROWING IMPORTANCE OF CARDIAC CARE CENTERS IN DELIVERING SPECIALIZED CARDIOVASCULAR INTERVENTIONS TO FUEL GROWTH

- 16.5 OTHER END USERS

17 INTERVENTIONAL CARDIOLOGY DEVICES MARKET, BY REGION

- 17.1 INTRODUCTION

- 17.2 NORTH AMERICA

- 17.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 17.2.2 NORTH AMERICA: VOLUME ANALYSIS OF INTERVENTIONAL CARDIOLOGY DEVICES, BY TYPE, 2024-2031 (THOUSAND UNITS)

- 17.2.3 US

- 17.2.3.1 Favorable reimbursement coverage and growing cardiovascular disease burden to support market growth

- 17.2.4 CANADA

- 17.2.4.1 Rising cardiovascular disease burden and advancements in cardiac care to drive market growth

- 17.3 EUROPE

- 17.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 17.3.2 EUROPE: VOLUME ANALYSIS OF INTERVENTIONAL CARDIOLOGY DEVICES, BY TYPE, 2024-2031 (THOUSAND UNITS)

- 17.3.3 GERMANY

- 17.3.3.1 Key hub for advanced interventional cardiology technologies to boost market

- 17.3.4 FRANCE

- 17.3.4.1 Government support for cardiovascular care and technological innovation to drive market growth in France

- 17.3.5 UK

- 17.3.5.1 Increasing adoption of advanced and personalized cardiovascular therapies to support market growth

- 17.3.6 ITALY

- 17.3.6.1 Rising prevalence of cardiovascular risk factors to drive demand for interventional cardiology devices

- 17.3.7 SPAIN

- 17.3.7.1 Aging population and increasing cardiovascular disease burden to support market growth

- 17.3.8 REST OF EUROPE

- 17.4 ASIA PACIFIC

- 17.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 17.4.2 ASIA PACIFIC: VOLUME ANALYSIS OF INTERVENTIONAL CARDIOLOGY DEVICES, BY TYPE, 2024-2031 (THOUSAND UNITS)

- 17.4.3 CHINA

- 17.4.3.1 High tobacco consumption and rising cardiovascular disease burden driving market growth

- 17.4.4 JAPAN

- 17.4.4.1 Aging population and growing demand for minimally invasive cardiac procedures to drive market growth

- 17.4.5 INDIA

- 17.4.5.1 Rising cardiovascular disease burden and expanding healthcare access to drive market growth

- 17.4.6 AUSTRALIA

- 17.4.6.1 Rising prevalence of lifestyle-related cardiovascular diseases to drive market growth

- 17.4.7 SOUTH KOREA

- 17.4.7.1 Advancements in medical technology and cardiovascular care to support market growth

- 17.4.8 REST OF ASIA PACIFIC

- 17.5 LATIN AMERICA

- 17.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 17.5.2 LATIN AMERICA: VOLUME ANALYSIS OF INTERVENTIONAL CARDIOLOGY DEVICES, BY TYPE, 2024-2031 (THOUSAND UNITS)

- 17.5.3 BRAZIL

- 17.5.3.1 Rising cardiovascular disease burden and healthcare infrastructure investments to drive market growth

- 17.5.4 MEXICO

- 17.5.4.1 Rising diabetes and cardiovascular disease burden to drive market growth

- 17.5.5 REST OF LATIN AMERICA

- 17.6 MIDDLE EAST & AFRICA

- 17.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 17.6.2 MIDDLE EAST & AFRICA: VOLUME ANALYSIS OF INTERVENTIONAL CARDIOLOGY DEVICES, BY TYPE, 2024-2031 (THOUSAND UNITS)

- 17.6.3 GCC COUNTRIES

- 17.6.3.1 Rising diabetes and cardiovascular disease burden to drive market growth

- 17.6.4 KINGDOM OF SAUDI ARABIA (KSA)

- 17.6.4.1 Expanding cardiovascular care infrastructure and healthcare investments to support market growth in Saudi Arabia

- 17.6.5 UNITED ARAB EMIRATES (UAE)

- 17.6.5.1 Healthcare modernization and advanced cardiovascular care to support market growth in the UAE

- 17.6.6 OTHER GCC COUNTRIES

- 17.6.7 REST OF MIDDLE EAST & AFRICA

18 COMPETITIVE LANDSCAPE

- 18.1 OVERVIEW

- 18.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 18.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN INTERVENTIONAL CARDIOLOGY DEVICES MARKET

- 18.3 REVENUE ANALYSIS, 2023-2025

- 18.4 MARKET SHARE ANALYSIS, 2025

- 18.4.1 ANGIOPLASTY STENTS MARKET SHARE ANALYSIS, 2025

- 18.4.2 STRUCTURAL HEART DEVICES MARKET SHARE ANALYSIS, 2025

- 18.4.3 CATHETERS MARKET SHARE ANALYSIS, 2025

- 18.4.4 ANGIOPLASTY BALLOONS MARKET SHARE ANALYSIS, 2025

- 18.4.5 PLAQUE MODIFICATION DEVICES MARKET SHARE ANALYSIS, 2025

- 18.4.6 HEMODYNAMIC FLOW ALTERATION DEVICES MARKET SHARE ANALYSIS, 2025

- 18.4.7 OTHER INTERVENTIONAL CARDIOLOGY DEVICES MARKET SHARE ANALYSIS, 2025

- 18.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 18.5.1 STARS

- 18.5.2 EMERGING LEADERS

- 18.5.3 PERVASIVE PLAYERS

- 18.5.4 PARTICIPANTS

- 18.6 COMPANY FOOTPRINT

- 18.6.1 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 18.6.1.1 Company footprint

- 18.6.1.2 Region footprint

- 18.6.1.3 Product footprint

- 18.6.1.4 Angioplasty stents footprint

- 18.6.1.5 Structural heart devices footprint

- 18.6.1.6 Catheters footprint

- 18.6.1.7 Angioplasty balloons footprint

- 18.6.1.8 Plaque modification devices footprint

- 18.6.1.9 Hemodynamic flow alteration devices footprint

- 18.6.1.10 Other interventional cardiology devices footprint

- 18.6.1.11 End-user footprint

- 18.6.1 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 18.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 18.7.1 PROGRESSIVE COMPANIES

- 18.7.2 RESPONSIVE COMPANIES

- 18.7.3 DYNAMIC COMPANIES

- 18.7.4 STARTING BLOCKS

- 18.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 18.8 COMPANY VALUATION & FINANCIAL METRICS

- 18.8.1 FINANCIAL METRICS

- 18.8.2 COMPANY VALUATION

- 18.9 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 18.10 COMPETITIVE SCENARIO

- 18.10.1 PRODUCT LAUNCHES & APPROVALS

- 18.10.2 DEALS

- 18.10.3 EXPANSIONS

19 COMPANY PROFILES

- 19.1 KEY PLAYERS

- 19.1.1 EDWARDS LIFESCIENCES CORPORATION

- 19.1.1.1 Business overview

- 19.1.1.2 Products offered

- 19.1.1.3 Recent developments

- 19.1.1.3.1 Product launches & approvals

- 19.1.1.3.2 Deals

- 19.1.1.4 MnM View

- 19.1.1.4.1 Key Strengths

- 19.1.1.4.2 Strategic Choices

- 19.1.1.4.3 Weaknesses & Competitive Threats

- 19.1.2 ABBOTT

- 19.1.2.1 Business overview

- 19.1.2.2 Products offered

- 19.1.2.3 Recent developments

- 19.1.2.3.1 Product launches & approvals

- 19.1.2.3.2 Deals

- 19.1.2.4 MnM view

- 19.1.2.4.1 Key strengths

- 19.1.2.4.2 Strategic choices

- 19.1.2.4.3 Weaknesses & competitive threats

- 19.1.3 MEDTRONIC

- 19.1.3.1 Business overview

- 19.1.3.2 Products offered

- 19.1.3.3 Recent developments

- 19.1.3.3.1 Product launches & approvals

- 19.1.3.3.2 Deals

- 19.1.3.4 MnM view

- 19.1.3.4.1 Key strengths

- 19.1.3.4.2 Strategic choices

- 19.1.3.4.3 Weaknesses & competitive threats

- 19.1.4 BOSTON SCIENTIFIC CORPORATION

- 19.1.4.1 Business overview

- 19.1.4.2 Products offered

- 19.1.4.3 Recent developments

- 19.1.4.3.1 Product launches & approvals

- 19.1.4.3.2 Deals

- 19.1.4.4 MnM view

- 19.1.4.4.1 Key strengths

- 19.1.4.4.2 Strategic choices

- 19.1.4.4.3 Weaknesses & competitive threats

- 19.1.5 TERUMO CORPORATION

- 19.1.5.1 Business overview

- 19.1.5.2 Products offered

- 19.1.5.3 Recent developments

- 19.1.5.3.1 Product launches

- 19.1.5.3.2 Deals

- 19.1.5.3.3 Expansions

- 19.1.5.3.4 Others

- 19.1.5.4 MnM view

- 19.1.5.4.1 Key strengths

- 19.1.5.4.2 Strategic choices

- 19.1.5.4.3 Weaknesses & competitive threats

- 19.1.6 KONINKLIJKE PHILIPS N.V.

- 19.1.6.1 Business overview

- 19.1.6.2 Products offered

- 19.1.6.3 Recent developments

- 19.1.6.3.1 Product launches & approvals

- 19.1.6.3.2 Deals

- 19.1.6.4 MnM view

- 19.1.6.4.1 Key strengths

- 19.1.6.4.2 Strategic choices

- 19.1.6.4.3 Weaknesses & competitive threats

- 19.1.7 CORDIS

- 19.1.7.1 Business overview

- 19.1.7.2 Products offered

- 19.1.7.3 Recent developments

- 19.1.7.3.1 Product launches & approvals

- 19.1.7.3.2 Deals

- 19.1.8 TELEFLEX INCORPORATED

- 19.1.8.1 Business overview

- 19.1.8.2 Products offered

- 19.1.8.3 Recent developments

- 19.1.8.3.1 Product approvals

- 19.1.8.3.2 Deals

- 19.1.9 ASAHI INTECC CO., LTD.

- 19.1.9.1 Business overview

- 19.1.9.2 Products offered

- 19.1.9.3 Recent developments

- 19.1.9.3.1 Deals

- 19.1.9.3.2 Expansions

- 19.1.10 COOK

- 19.1.10.1 Business overview

- 19.1.10.2 Products offered

- 19.1.10.3 Recent developments

- 19.1.10.3.1 Deals

- 19.1.11 B. BRAUN SE

- 19.1.11.1 Business overview

- 19.1.11.2 Products offered

- 19.1.11.3 Recent developments

- 19.1.11.3.1 Product launches & approvals

- 19.1.11.3.2 Deals

- 19.1.12 INTEGER HOLDINGS CORPORATION

- 19.1.12.1 Business overview

- 19.1.12.2 Products offered

- 19.1.12.3 Recent developments

- 19.1.12.3.1 Deals

- 19.1.12.3.2 Expansions

- 19.1.13 LEPU MEDICAL TECHNOLOGY (BEIJING) CO., LTD.

- 19.1.13.1 Business overview

- 19.1.13.2 Products offered

- 19.1.14 IVASCULAR S.L.U.

- 19.1.14.1 Business overview

- 19.1.14.2 Products offered

- 19.1.15 BIOSENSORS INTERNATIONAL GROUP, LTD.

- 19.1.15.1 Business overview

- 19.1.15.2 Products offered

- 19.1.1 EDWARDS LIFESCIENCES CORPORATION

- 19.2 OTHER PLAYERS

- 19.2.1 ENDOCOR GMBH & CO. KG

- 19.2.2 INSITU TECHNOLOGIES, INC.

- 19.2.3 MERIL LIFE SCIENCES PVT. LTD

- 19.2.4 ALVIMEDICA

- 19.2.5 CARDIONOVUM GMBH

- 19.2.6 MEDINOL

- 19.2.7 BALTON SP.

- 19.2.8 TRANSLUMINA

- 19.2.9 SINO MEDICAL SCIENCES TECHNOLOGY INC.

- 19.2.10 SMT

20 RESEARCH METHODOLOGY

- 20.1 RESEARCH DATA

- 20.1.1 SECONDARY DATA

- 20.1.1.1 Key secondary sources

- 20.1.2 PRIMARY DATA

- 20.1.2.1 Primary sources

- 20.1.2.2 Key data from primary sources

- 20.1.2.3 Key industry insights

- 20.1.2.4 Breakdown of primaries

- 20.1.1 SECONDARY DATA

- 20.2 MARKET SIZE ESTIMATION

- 20.2.1 APPROACH 1: COMPANY REVENUE ANALYSIS APPROACH

- 20.2.2 APPROACH 2: CUSTOMER-BASED MARKET ESTIMATION

- 20.2.3 APPROACH 3: TOP-DOWN APPROACH

- 20.2.4 APPROACH 4: BOTTOM-UP APPROACH

- 20.2.5 APPROACH 4: PRIMARY INTERVIEWS

- 20.2.6 APPROACH 5: DEMAND-SIDE APPROACH

- 20.2.7 APPROACH 6: VOLUME DATA ANALYSIS

- 20.3 DATA TRIANGULATION AND MARKET BREAKDOWN

- 20.4 MARKET SHARE ASSESSMENT

- 20.5 RESEARCH ASSUMPTIONS

- 20.5.1 STUDY ASSUMPTIONS

- 20.5.2 GROWTH RATE ASSUMPTIONS

- 20.6 RISK ASSESSMENT

- 20.6.1 RESEARCH LIMITATIONS

21 APPENDIX

- 21.1 DISCUSSION GUIDE

- 21.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 21.3 CUSTOMIZATION OPTIONS

- 21.4 RELATED REPORTS

- 21.5 AUTHOR DETAILS