|

시장보고서

상품코드

2084067

철도용 배터리 시장 예측(-2033년) : 배터리 유형 및 배터리 기술별, 용도 및 배터리 유형별, 엔진/헤드별, 용도별, 첨단형 철도 유형별, 차량별, 지역별Train Battery Market by Technology (Lead-acid Tubular, VRLA, Conventional; Ni-Cd Sinter, Fiber, Pocket, & Li-ion; LFP, LTO), Advanced Train (Battery-operated, and Hybrid), Rolling Stock Type, Application, Aftermarket, Region - Global Forecast to 2033 |

||||||

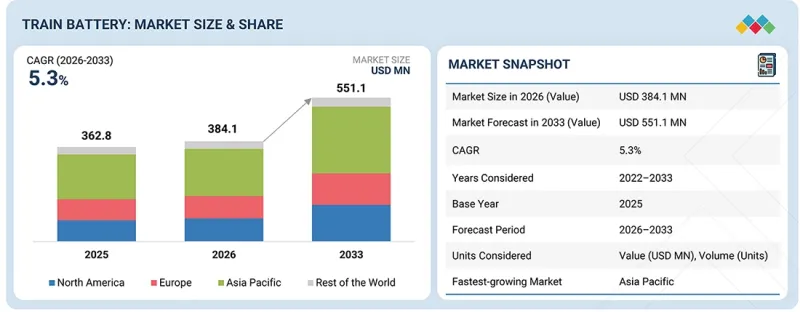

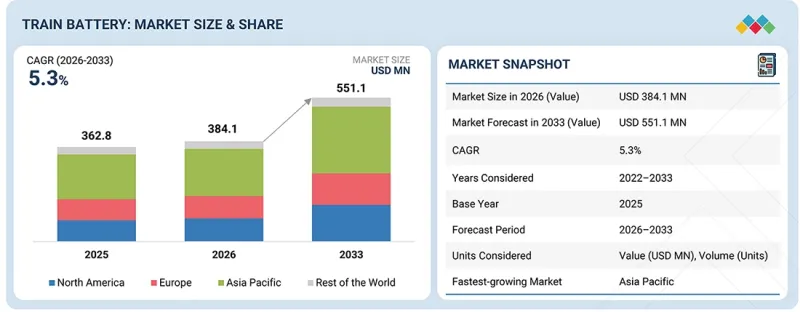

철도용 배터리 시장 규모는 2026년 3억 8,410만 달러에서 2033년에는 5억 5,110만 달러로 성장할 것으로 예측되고 있으며, CAGR은 5.3%에 달합니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2033년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2033년 |

| 산정 단위 | 100만 달러 |

| 부문 | 배터리 유형 및 배터리 기술별, 용도 및 배터리 유형별, 엔진/헤드별, 용도별, 첨단형 철도 유형별, 차량별, 지역별 |

| 대상 지역 | 아시아태평양, 유럽, 북미 및 기타 지역 |

부분적으로 전기화된 철도 노선에서 디젤 운행을 줄이고, 철도의 탈탄소화 목표를 지원하기 위해 배터리 기술이 활용됨에 따라 철도용 배터리 시장은 확대되고 있습니다. 2025년 1월, 리투아니아, 라트비아, 에스토니아 전역의 철도 전철화를 추진하기 위해 201억 3,000만 달러 규모의 ‘레일 발티카(Rail Baltica)’ 전철화 계약이 체결되었습니다. 2030년까지 완공을 목표로 하고 있으며, 이를 통해 배터리 탑재 차량 및 보조 전원 시스템에 대한 장기적인 수요가 창출될 것으로 전망됩니다. 영국에서는 2025년 내내 활발하게 개발이 진행된 HS2 고속철도 프로젝트가, 보조 전원과 백업 전원으로 첨단 차량용 배터리 시스템이 필요한 최첨단 차량의 조달을 계속해서 주도하고 있습니다. 한편, 2025년 7월 유럽집행위원회는 최신 ‘철도 시장 모니터링 보고서’를 통해 빠르고 지속가능한 철도 운송 확대를 위한 노력을 재확인하고, 프랑스, 독일, 이탈리아 및 기타 주요 시장에서 철도 현대화를 위한 추가 투자를 장려했습니다. 이러한 추세는 첨단 철도용 배터리 기술의 도입을 가속화하여, 보다 친환경적이고 효율적인 철도 운송으로의 전환을 지원하는 배터리 공급업체들에게 새로운 기회를 창출하고 있습니다.

'예측 기간 중, 용도별로는 보조 배터리가 가장 빠르게 성장하는 부문이 될 것입니다. '

보조 배터리는 열차 배터리 시장에서 가장 빠르게 성장할 것으로 예상되는 부문입니다. 이는 조명, 공조(HVAC), 통신, 승객 정보 표시, 문 조작, 제어 전자기기, CCTV, 비상 백업 시스템 등 차내의 중요한 시스템에 전력을 공급하여, 정전 시에도 열차 운행이 중단 없이 이루어지도록 하는 역할을 담당하고 있기 때문입니다. 최신 전기식 열차(EMU), 지하철, 고속열차, 여객 객차에는 디지털 기능과 승객의 편의성을 높이는 기능이 점점 더 많이 탑재됨에 따라 신뢰성이 높은 보조 전원에 대한 수요는 계속해서 증가하고 있습니다. 또한 유럽, 일본, 북미 지역의 신형 차량에는 전용 사이버 보안 게이트웨이, 차량용 서버, 예측 유지보수 시스템 및 지속적인 데이터 로깅 기능이 점점 더 많이 탑재되고 있으며, 이러한 기능에는 중단 없는 저전압 전원이 필요합니다. 그 결과, 보조 배터리 시스템의 대형화와 열차 1량당 배터리 용량 증가로 이어지고 있습니다. 이러한 추세는 기술 전환도 촉진하고 있으며, 철도 차량 제조사들은 기존의 납축전지나 경우에 따라 니켈카드뮴(Ni-Cd) 배터리를 보조 전원 용도로 경량이며, 충방전 속도가 빠르고, 뛰어난 성능을 발휘하는 첨단 인산철리튬(LFP) 배터리나 티탄산염 리튬(LTO) 배터리로 대체하는 움직임을 강화하고 있습니다.

보조 배터리의 중요성이 커지고 있는 점을 반영하여, 철도용 배터리 업계의 각 OEM 기업은 보조 용도로 사용될 첨단 리튬이온 배터리 및 니켈카드뮴 배터리의 개발에 주력하고 있습니다. 예를 들어 2024년 5월, 사프트(Saft)사는 카이로 지하철 4호선의 차량 92량에 MRX 니켈계 배터리를 공급하여, 통신, 문 조작, 공조 등 안전에 필수적인 기능에 대한 백업 전원을 제공했습니다. 철도 사업자들이 신뢰성, 승객의 편의성, 디지털 연결성, 사이버 보안 및 수명 주기 비용 절감을 지속적으로 우선시함에 따라 첨단 보조 배터리 시스템에 대한 수요는 신차 시장과 애프터마켓 교체용 시장 모두에서 확대될 것으로 예상됩니다.

'여객 차량이 철도용 배터리 업계의 미래를 이끌어 갈 것입니다. ' '

여객 차량은 방대한 보유 대수뿐만 아니라 조명, 공조(HVAC), 자동문, 승객 정보 표시, Wi-Fi, USB 충전 포트, CCTV, 진단 시스템, 통신, 비상 조명, 안전 시스템 등 배터리 구동 방식의 차량용 시스템 활용이 확대되고 있으며, 철도용 배터리 시장을 촉진할 것으로 예상됩니다. 승객의 편의에 대한 기대가 높아지고, 디지털화가 진행되며, 커넥티드 철도 여행이 발전함에 따라 보조 전원에 대한 수요가 증가하고 있습니다. 유럽 및 북미에서는 니켈-카드뮴(Ni-Cd) 배터리가 입증된 신뢰성, 긴 수명, 극한 온도 및 진동에 대한 내성, 그리고 기존 대형 철도 차량과의 호환성 덕분에 여객차의 보조 전원 용도로 여전히 주류를 차지하고 있습니다. 반면 중국, 인도, 동남아시아에서는 경량성, 높은 에너지 밀도, 낮은 유지보수 요구 사항 덕분에 신형 여객 차량, 지하철 및 전기 다단 열차(EMU)에 리튬이온 배터리의 채택이 확대되고 있습니다. 일반적인 보조 배터리 시스템은 24V, 72V 또는 110V로 작동하며, 용량은 100Ah에서 500Ah 이상까지 다양합니다. 수요는 전 세계적인 차량 현대화 프로그램에 힘입어 더욱 증가하고 있습니다. 여기에는 2025년 3월 독일 알스톰사에 수주요 6억 5,000만 달러 규모의 여객 철도 차량 계약, 유럽 전역에서 진행 중인 객차 개조 프로그램, 650억 달러를 초과하는 영국의 HS2에 대한 투자, 그리고 북미 메트로폴리탄 교통국(MTA)의 지속적인 차량 업그레이드 등이 포함됩니다.

애프터마켓의 관점에서 볼 때, 보조 배터리는 지속적인 수입원이 됩니다. 유럽 및 북미에서 대량으로 보급된 니켈-카드뮴(Ni-Cd) 배터리는 일반적으로 12-15년마다 교체해야 하지만, 아시아태평양의 일부에서는 10-12년마다 Ni-Cd 배터리를 교체하고 있습니다. 중국 및 동남아시아의 일부 시장에서는 여객 열차, 지하철, 전기식 단위 열차(EMU)에 리튬이온 배터리의 도입이 확대되고 있으며, 운용 조건에 따라 다르지만 교체 주기는 일반적으로 8-15년입니다. 이러한 투자 및 교체 수요로 인해 차량 1대당 배터리 탑재량이 증가하면서, OEM 탑재용 및 교체용 배터리 모두에 대한 지속적인 수요가 발생하고 있습니다. 이로 인해 여객 차량은 전 세계 철도용 배터리 시장에서 주도적인 위치를 유지하고 있습니다.

'파이버/PNE(FNC) 니켈-카드뮴 배터리 부문은 납축전지 기술 분야에서 가장 빠르게 성장할 것으로 전망됩니다. '

Fiber/PNE(FNC) 니켈-카드뮴 배터리는 높은 출력 밀도, 뛰어난 충전 수용성, 과방전에 대한 우수한 내성, 낮은 유지보수 요구 사항을 갖추고 있으며, 가혹한 철도 환경에서도 15-20년을 넘는 수명을 실현합니다. 기존의 납축 배터리와 비교했을 때, FNC 배터리는 수명이 길고, 빈번한 충방전 사이클에서도 뛰어난 성능을 발휘하며, 심방전 후 회복 속도가 빠르고, 진동 및 전기적 스트레스에 대한 내성도 높기 때문에 철도 차량의 보조 전원이나 백업 전원 용도로 특히 적합합니다. 많은 주요 기업이 FNC 기술에 적극적으로 투자하고 있으며, 이 기술은 전 세계 철도 분야에서 널리 채택되고 있습니다. 2025년 시점에 HOPPECKE사는 전 세계 철도 고객사에 250만개 이상의 FNC 셀을 납품했으며, 북미 지역만 해도 28만 5,000개 이상의 FNC 셀을 납품했다고 보고하고 있는데, 이는 지방 철도, 지하철, 기관차, 고속철도, 경전철 차량 등 폭넓은 분야에서 널리 채택되고 있음을 보여줍니다. 또한 이 회사는 자사의 FNC 배터리가 35년 이상 철도 분야에서 가동되어 왔으며, 교체 주기를 연장하고 수명 주기 비용을 절감하고자 하는 사업자들을 지원하고 있다는 점을 강조하고 있습니다. 철도 사업자들이 배터리 초기 비용 최소화보다 차량 가동률 극대화와 장기적인 유지보수 비용 절감에 점점 더 주력하고 있는 가운데, 파이버/PNE 니켈카드뮴(Ni-Cd) 배터리는 신규 차량 및 배터리 교체 프로그램 모두에서 채택이 확대되고 있습니다.

'아시아태평양은 가장 큰 지역 시장이 될 것으로 전망됩니다. '

아시아태평양은 광범위한 철도망의 확장, 막대한 차량 보유 대수, 그리고 중국, 인도, 일본, 한국 등 주요 국가들의 지하철, 고속철도, 지방철도 인프라가 잘 갖춰져 있다는 점을 배경으로, 세계 철도용 배터리 시장에서 가장 큰 점유율을 차지하고 있습니다. 또한 이 지역은 세계에서 가장 많은 여객 철도 이용 횟수를 기록하고 있으며, 시장의 40% 이상을 차지하고 있는데, 이는 기관차, 객차, 전기 다단 열차(EMU), 디젤 다단 열차(DMU), 지하철, 고속철도 등에서 사용되는 배터리에 대한 활발한 수요를 직접 견인하고 있습니다. 이러한 우위는 정부 주도의 적극적인 철도 전기화 및 탈탄소화 프로그램을 통해 더욱 강화되고 있으며, 이러한 노력 덕분에 전기식, 하이브리드식 및 배터리 구동 차량의 도입이 가속화되고 있습니다. 예를 들어 중국의 철도망은 2025년에 16만 2,000km를 넘어섰으며, 그중 고속철도는 4만 8,000km 이상에 달했습니다. 한편, 인도에서는 2030년까지 철도 운영에서 탄소 중립 목표를 달성하기 위한 조치의 일환으로, 2025년까지 광궤 철도망의 99% 이상을 전철화했습니다. 일본에서도 각 철도 사업자들은 비전철화 노선에서 BEC819 'DENCHA'나 EV-E301 등의 배터리식 열차 도입을 확대하고 있으며, 해당 지역의 저탄소 철도 모빌리티로의 전환을 지원하고 있습니다.

이러한 대규모 네트워크 확장에 따라 신뢰성이 높은 보조 전원 및 시동 전원 시스템에 대한 수요가 증가하고 있으며, 특히 인도, 중국, 동남아시아에서는 기관차 용도로 리튬이온 배터리가 가장 널리 채택되고 있는 기술입니다. 이러한 우위는 긴 수명, 극한의 온도 및 진동 조건에서도 뛰어난 신뢰성, 그리고 미션 크리티컬한 철도 운행에서 보여주는 안정적인 성능에서 비롯됩니다. 이에 반해, 니켈-카드뮴(Ni-Cd) 배터리는 보통 12-20년마다, 납축 배터리는 4-8년마다 교체가 필요하므로 초기 비용은 비싸지만 수명 주기 전체를 고려하면 Ni-Cd 배터리가 비용 효율 면에서 더 우수한 선택지가 됩니다. 또한 아시아태평양에는 GS 유아사, 아마라 라자 에너지 앤 모빌리티, HBL 엔지니어링, 에나시스, 사프트와 같은 주요 배터리 제조사들이 강력하게 진출해 있으며, 현지 생산, 기술 도입의 신속화, 효율적인 공급망이 확보되어 있습니다. 이를 통해 철도용 배터리 시장에서 해당 지역의 선도적 입지가 더욱 공고해지고 있습니다.

철도용 배터리 시장에는 Saft(프랑스), Enersys(미국), Exide Industries(인도), GS 유아사 주식회사(일본), Amara Raja Batteries Ltd(인도), Hoppecke Batterien GmbH & Co. KG(독일), SEC Batteries(중국), First National Batteries(남아프리카), Power & Industrial Battery Systems GmbH(독일), 그리고 Exide Technologies(미국)와 같은 글로벌 기업이 시장을 독점하고 있습니다. 이 기업은 시장내 입지를 강화하기 위해 제품 개발, 파트너십 구축 및 기타 조치와 같은 전략을 채택했습니다.

조사 범위:

본 조사에서는 철도용 배터리 시장을 세분화하여, 용도 및 배터리 유형(시동용 배터리 및 보조용 배터리)별, 용도 및 배터리 기술(납축전지, 니켈카드뮴 전지, 리튬이온 전지)별, 엔진/차종(디젤 기관차, 디젤 다중 단위 차량, 전기 다중 단위 차량, 전기 기관차)별, 용도별(지하철, 고속 열차, 경전철/노면전차, 여객 객차); 첨단 열차 유형별(하이브리드 열차, 완전 배터리 구동 열차, 자율주행 열차); 차량별 애프터마켓(기관차, 다단 편성, 여객 객차); 배터리 유형별 애프터마켓(납축전지, 니켈카드뮴 배터리); 용도별 애프터마켓(시동용 배터리, 보조용 배터리); 지역별 애프터마켓(아시아태평양, 유럽, 북미); 및 지역별(아시아태평양, 유럽, 북미, 기타 지역). 또한 철도용 배터리 제조사 시장 생태계내 주요 기업의 경쟁 현황과 기업 개요에 대해서도 포괄적으로 다루고 있습니다.

이 보고서의 주요 장점

이 보고서는 시장을 선도하는 기업 및 신규 진입 기업을 대상으로, 철도용 배터리 시장 및 그 하위 부문의 매출에 대해 가장 정확한 추정치를 제공합니다. 또한 공급업체별 철도용 배터리 판매 동향을 분석하고 있으며, 부품 공급업체가 전략을 수립하는 데 도움이 됩니다. 이 보고서는 이해관계자들이 경쟁 구도를 이해하고, 자사의 비즈니스를 보다 효과적으로 포지셔닝하기 위한 인사이트를 얻어, 적절한 시장 진입 전략을 수립하는 데 도움이 됩니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움이 되며, 주요 시장 촉진요인, 시장 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

이 보고서에서는 다음 사항에 대한 인사이트를 제공합니다. :

- 주요 촉진요인(자율주행 철도 및 고속철도 도입 확대, 전력망의 탈탄소화 및 재생에너지 활용 전략), 제약 요인(높은 수명 주기 비용 및 운영상의 신뢰성), 기회(차세대 에너지 저장 시스템의 통합, 스마트 철도 에너지 관리 및 디젤 전기 열차의 개조), 그리고 과제(대형·장거리 철도 운행시 배터리 성능의 한계, 인프라 통합 및 표준화의 복잡성)에 대해 철도용 배터리 시장의 성장에 영향을 미치는 요인을 분석하고 있습니다.

- 제품 개발/혁신: 철도용 배터리 시장의 향후 기술, 연구개발 활동 및 신제품 출시에 대한 심층적인 인사이트

- 시장 개발: 수익성이 높은 시장에 대한 포괄적인 정보 - 이 보고서에서는 다양한 지역의 철도용 배터리 시장을 분석하고 있습니다.

- 시장의 다양화: 철도용 배터리 시장의 신제품, 미개발 지역, 최근 동향 및 투자에 관한 포괄적인 정보

- 경쟁사 평가: 시장 점유율, 성장 전략, 스타트업/중소기업 대상 시장 사분면, 그리고 Saft(프랑스), Enersys(미국), Exide Industries(인도), GS 유아사 주식회사(일본), Amara Raja Batteries Ltd(인도), Hoppecke Batterien GmbH & Co. KG(독일), SEC Batteries(중국), First National Batteries(남아프리카공화국), Power &Industrial Battery Systems GmbH(독일), Exide Technologies(미국) 등, 철도용 배터리 제조사 시장의 주요 기업별 시장 점유율, 성장 전략, 스타트업/중소기업 대상 시장 쿼드런트 및 서비스 제공에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 철도용 배터리 시장(배터리 유형별 및 배터리 기술별)

제10장 철도용 배터리 시장(용도별 및 배터리 유형별)

제11장 철도용 배터리 시장(엔진/헤드별)

제12장 철도용 배터리 시장(용도별)

제13장 철도용 배터리 시장(첨단형 철도 유형별)

제14장 배터리 애프터마켓(차량별)

제15장 철도용 배터리 애프터마켓(배터리 유형별)

제16장 철도용 배터리 애프터마켓(용도별)

제17장 철도용 배터리 시장(지역별)

제18장 철도용 배터리 애프터마켓(지역별)

제19장 경쟁 구도

제20장 기업 개요

제21장 조사 방법

제22장 부록

KSAThe train battery market is projected to grow from USD 384.1 million in 2026 to USD 551.1 million in 2033, reflecting a CAGR of 5.3%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | USD million |

| Segments | by Technology, Advanced Train, Rolling Stock Type, Application, Aftermarket, Region |

| Regions covered | Asia Pacific, Europe, North America, and Rest of the World |

The train battery market is growing as battery technology is used to reduce diesel operations on partially electrified rail routes and support rail decarbonization goals. In January 2025, the USD 20.13 billion Rail Baltica electrification contract was awarded to advance railway electrification across Lithuania, Latvia, and Estonia, with completion targeted by 2030, creating long-term demand for battery-equipped rolling stock and auxiliary power systems. In the UK, the HS2 high-speed rail project, which remained under active development throughout 2025, continues to drive procurement of modern rolling stock that requires advanced onboard battery systems for auxiliary and backup power. Meanwhile, in July 2025, the European Commission reaffirmed its commitment to expanding high-speed and sustainable rail transport through its latest Rail Market Monitoring Report, encouraging further investment in rail modernization across France, Germany, Italy, and other major markets. These developments are accelerating the adoption of advanced train battery technologies and creating new opportunities for battery suppliers supporting the transition toward cleaner and more efficient rail transportation.

"Auxiliary batteries will be the fastest-growing segment by application during the forecast period"

Auxiliary batteries will be the fastest-growing segment in the train battery market because they power critical onboard systems, including lighting, HVAC, communications, passenger information displays, door operation, control electronics, CCTV, and emergency backup systems, ensuring uninterrupted train operation even during power disruptions. As modern EMUs, metros, high-speed trains, and passenger coaches incorporate more digital and passenger-comfort features, demand for reliable auxiliary power continues to rise. In addition, new rolling stock in Europe, Japan, and North America increasingly includes dedicated cybersecurity gateways, onboard servers, predictive maintenance systems, and continuous data-logging capabilities that require uninterrupted low-voltage power, leading to larger auxiliary battery systems and higher battery capacity per train. This trend is also driving a technology shift, with train manufacturers increasingly replacing traditional lead-acid and, in some cases, Ni-Cd batteries with advanced Lithium Iron Phosphate (LFP) and Lithium Titanate Oxide (LTO) batteries, which offer lower weight, higher charge-discharge rates, and superior performance for auxiliary power applications.

Reflecting the growing importance of auxiliary batteries, OEMs in the train battery industry are focusing on developing advanced lithium-ion and nickel-cadmium batteries for auxiliary applications. For instance, in May 2024, Saft supplied MRX nickel-based batteries for 92 Cairo Metro Line 4 trains, providing backup power for safety-critical functions such as communications, door operation, and air conditioning. As rail operators continue to prioritize reliability, passenger comfort, digital connectivity, cybersecurity, and lower lifecycle costs, demand for advanced auxiliary battery systems is expected to grow across both new train production and aftermarket replacement markets.

"Passenger coaches will lead the future of the train battery industry."

Passenger coaches are expected to lead the train battery market because of their large installed fleet and the growing use of battery-powered onboard systems, including lighting, HVAC, automatic doors, passenger information displays, Wi-Fi, USB charging ports, CCTV, diagnostics, communications, emergency lighting, and safety systems. Rising passenger comfort expectations, digitalization, and connected rail travel are increasing auxiliary power requirements. In Europe and North America, Ni-Cd batteries continue to dominate auxiliary coach applications because of their proven reliability, long service life, resistance to extreme temperatures and vibration, and compatibility with large existing rail fleets. In contrast, China, India, and Southeast Asia are increasingly adopting Li-ion batteries in new passenger coaches, metros, and EMUs because of their lighter weight, higher energy density, and lower maintenance requirements. Typical auxiliary battery systems operate at 24V, 72V, or 110V, with capacities ranging from 100 Ah to over 500 Ah. Demand is further supported by fleet modernization programs worldwide, including a USD 650 million passenger rail vehicle contract awarded to Alstom in Germany in March 2025, ongoing coach refurbishment programs across Europe, the UK's HS2 investment exceeding USD 65 billion, and continued fleet upgrades by the Metropolitan Transportation Authority in North America.

From an aftermarket perspective, auxiliary batteries generate recurring revenue. Europe and North America's large installed base of Ni-Cd batteries typically requires replacement every 12-15 years, while parts of Asia Pacific replace Ni-Cd batteries every 10-12 years. In China and several Southeast Asian markets, where Li-ion batteries are increasingly deployed in passenger coaches, metros, and EMUs, replacement cycles generally range from 8-15 years, depending on operating conditions. These investments and replacement requirements are increasing battery content per coach and generating sustained demand for both OEM-installed and replacement batteries, helping passenger coaches maintain a leading position in the global train battery market.

"The fiber/PNE (FNC) Ni-Cd battery segment is likely to be the fastest-growing in lead acid battery technology."

Fiber/PNE (FNC) nickel-cadmium batteries offer high power density, excellent charge acceptance, superior resistance to deep discharge, low maintenance requirements, and a service life that can exceed 15-20 years in demanding railway environments. Compared with conventional lead-acid batteries, FNC batteries provide higher cycle life, better performance under frequent charge-discharge cycles, faster recovery after deep discharge, and greater tolerance to vibration and electrical stress, making them particularly suitable for auxiliary and backup power applications in rolling stock. Many key players are actively investing in FNC technology, which is widely used in railway applications worldwide. As of 2025, HOPPECKE reported deliveries of more than 2.5 million FNC cells to railway customers globally and over 285,000 FNC cells in North America alone, demonstrating strong adoption across regional trains, metros, locomotives, high-speed trains, and light rail vehicles. The company also highlights that its FNC batteries have been operating in railway applications for more than 35 years, supporting operators seeking longer replacement intervals and lower lifecycle costs. As rail operators increasingly focus on maximizing fleet availability and reducing long-term maintenance costs rather than minimizing upfront battery expenditure, Fiber/PNE Ni-Cd batteries are seeing growing adoption in both new rolling stock and replacement battery programs.

"Asia Pacific region is projected to be the largest regional market."

The Asia Pacific region holds the largest share of the global train battery market, supported by extensive railway network expansion, a large rolling stock base, and a strong presence of metro, high-speed rail, and regional rail infrastructure across key countries such as China, India, Japan, and South Korea. The region also records the highest number of passenger rail journeys globally and accounts for more than 40% of the market, directly driving strong demand for batteries used across locomotives, passenger coaches, EMUs, DMUs, metros, and high-speed trains. This dominance is further strengthened by aggressive government-led rail electrification and decarbonization programs, which are accelerating the adoption of electric, hybrid, and battery-powered rolling stock. For instance, China's railway network exceeded 162,000 km in 2025, including over 48,000 km of high-speed rail, while India had electrified more than 99% of its broad-gauge network by 2025 as part of its net-zero railway operations target by 2030. In Japan, operators are also expanding battery train deployments, such as the BEC819 "DENCHA" and EV-E301, on non-electrified routes, reinforcing the region's transition toward low-carbon rail mobility.

This large-scale network growth is supported by strong demand for reliable auxiliary and starting power systems, with Li-ion batteries the most widely used technology in locomotive applications, particularly in India, China, and Southeast Asia. Their dominance stems from long service life, high reliability under extreme temperatures and vibration, and stable performance in mission-critical railway operations. By comparison, Ni-Cd batteries typically require replacement every 12-20 years, while lead-acid batteries need replacement every 4-8 years, making Ni-Cd a more cost-efficient choice over the lifecycle despite higher upfront costs. Additionally, the Asia Pacific region benefits from the strong presence of key battery manufacturers such as GS Yuasa, Amara Raja Energy & Mobility, HBL Engineering, EnerSys, and Saft, which ensures localized production, faster technology adoption, and efficient supply chains, further reinforcing the region's leadership in the train battery market.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: OEMs - 20%, Battery Supplier Company - 80%

- By Designation: C Levels - 20%, Directors- 30%, Others- 50%

- By Region: North America- 30%, Europe - 30%, Asia Pacific- 40%

The train battery market is dominated by global players such as Saft (France), Enersys (US), Exide Industries (India), GS Yuasa Corporation (Japan), Amara Raja Batteries Ltd (India), Hoppecke Batterien Gmbh & Co. Kg (Germany), SEC Batteries (China), First National Batteries (South Africa), Power & Industrial Battery Systems Gmbh (Germany), and Exide Technologies (US). These companies adopted strategies such as product development, partnerships, and other measures to gain traction in the market.

Research Coverage:

The study segments the train battery market and forecasts market size by application and battery type (starter batteries and auxiliary batteries); by application and battery technology (lead-acid batteries, nickel-cadmium batteries, and lithium-ion batteries); by engine/head (diesel locomotives, diesel multiple units, electric multiple units, and electric locomotives); by application (metro, high-speed trains, light rails/trams, and passenger coaches); by advanced train type (hybrid trains, fully battery-operated trains, and autonomous trains); aftermarket by rolling stock (locomotives, multiple units, and passenger coaches); aftermarket by battery type (lead-acid batteries and nickel-cadmium batteries); aftermarket by application (starter batteries and auxiliary batteries); aftermarket by region (Asia Pacific, Europe, and North America); and by region (Asia Pacific, Europe, North America, and Rest of the World). It also covers the competitive landscape and company profiles of the major players in the train battery manufacturers market ecosystem.

Key Benefits of the Report

The report will provide market leaders and new entrants with the closest approximations of revenue figures for the tarin battery market and its subsegments. It also examines tarin battery sales trends by supplier, enabling component suppliers to plan their strategies. This report will help stakeholders understand the competitive landscape, gain insights into positioning their businesses more effectively, and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (increasing adoption of autonomous and high speed railways, grid decarbonization & regenerative energy utilization strategies), restraints (high lifecycle cost and operational reliability), opportunities (next-generation energy storage integration and smart rail energy management and retrofitting of diesel-electric trains), and challenges (battery performance limitations in heavy-duty and long-range rail operations and infrastructure integration and standardization complexity) influencing the growth of the train battery market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the train battery market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the train battery market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the train battery market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, market quadrant for startup/SMEs and service offerings of leading players such as Saft (France), Enersys (US), Exide Industries (India), GS Yuasa Corporation (Japan), Amara Raja Batteries Ltd (India), Hoppecke Batterien Gmbh & Co. Kg (Germany), SEC Batteries (China), First National Batteries (South Africa), Power & Industrial Battery Systems Gmbh (Germany), and Exide Technologies (US), among others in the train battery manufacturers market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 REGIONS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 SUMMARY OF CHANGES

- 1.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 REPORT SUMMARY

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES IN TRAIN BATTERY MARKET

- 3.2 TRAIN BATTERY MARKET, BY BATTERY TYPE

- 3.3 TRAIN BATTERY MARKET, BY ROLLING STOCK

- 3.4 TRAIN BATTERY MARKET, BY APPLICATION

- 3.5 TRAIN BATTERY MARKET, BY ADVANCED TRAIN TYPE

- 3.6 TRAIN BATTERY AFTERMARKET, BY APPLICATION

- 3.7 TRAIN BATTERY AFTERMARKET, BY BATTERY TYPE

- 3.8 TRAIN BATTERY MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Shift toward battery-assisted and hybrid rail architecture

- 4.2.1.2 Grid decarbonization & regenerative energy utilization strategies

- 4.2.2 RESTRAINTS

- 4.2.2.1 High lifecycle cost and operational reliability

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Next-generation energy storage integration and smart rail energy management

- 4.2.3.2 Retrofitting of diesel-electric trains

- 4.2.4 CHALLENGES

- 4.2.4.1 Battery performance limitation in heavy-duty and long-range rail operation

- 4.2.4.2 High cost of charging infrastructure and replacement

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.3 TRENDS IN GLOBAL TRAIN BATTERY INDUSTRY

- 5.1.3.1 Regional GDP dynamics

- 5.1.3.1.1 Developed markets (Asia Pacific, Europe, North America, and Rest of the World)

- 5.1.3.1.2 Emerging markets

- 5.1.3.1.2.1 China

- 5.1.3.1.2.2 India

- 5.1.3.1.2.3 Brazil

- 5.1.3.1.2.4 Indonesia

- 5.1.3.1.2.5 Thailand

- 5.1.3.2 Investment environment

- 5.1.3.1 Regional GDP dynamics

- 5.2 SUPPLY CHAIN ANALYSIS

- 5.3 TRAIN BATTERY MARKET ECOSYSTEM

- 5.4 MARKET ECOSYSTEM

- 5.5 PRICING ANALYSIS

- 5.5.1 TRAIN BATTERY, AVERAGE SELLING PRICE, BY REGION

- 5.5.2 TRAIN BATTERY, AVERAGE SELLING PRICE TREND, BY BATTERY HEAD

- 5.6 KEY CONFERENCES & EVENTS, 2026 - 2027

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 860120)

- 5.7.2 EXPORT SCENARIO (HS CODE 843210)

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 SEPTA CARRIED OUT A PROJECT WITH VIRIDITY ENERGY TO INCREASE OPERATIONAL EFFICIENCY WITH LESS ENERGY CONSUMPTION

- 5.10.2 SAFT PROVIDES RELIABLE AUTONOMOUS BATTERY SOLUTIONS FOR HARSH WEATHER TO VR GROUP

- 5.10.3 DEVELOPMENT OF HYBRID TRAIN FOR NON-ELECTRIFIED SUBSECTIONS OF LINE

- 5.10.4 HITACHI PARTNERS WITH TURNTIDE TECHNOLOGIES TO PROVIDE MORE SUSTAINABLE RAIL JOURNEYS IN UK

- 5.11 BILL OF MATERIALS

- 5.12 TOTAL COST OF OWNERSHIP

- 5.13 OEM ANALYSIS

- 5.13.1 BATTERY MANUFACTURERS VS BATTERY VOLTAGE

- 5.13.2 BATTERY MANUFACTURERS VS BATTERY VOLTAGE

- 5.13.3 OEM VS BATTERY SUPPLIERS

- 5.14 FUTURE INVESTMENT AND DEALS FOR ELECTRIC TRAINS

- 5.15 FUTURE TRAIN ROUTE INVESTMENT AND PROJECTS FOR HIGH-SPEED TRAINS AND METROS

- 5.16 ROADMAP FOR RAILWAY DECARBONIZATION IN KEY COUNTRIES

- 5.17 EVOLUTION OF AUXILIARY BATTERIES IN RAILWAY

6 TECHNOLOGICAL ADVANCEMENTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 BATTERY MANAGEMENT SYSTEMS

- 6.1.2 FAST-CHARGING TECHNOLOGY

- 6.1.3 SMART MONITORING SYSTEMS

- 6.1.4 THERMAL MANAGEMENT SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ONBOARD ENERGY STORAGE SYSTEMS

- 6.2.2 PREDICTIVE MAINTENANCE SYSTEMS

- 6.2.3 DC-DC CONVERTERS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 HYDROGEN FUEL CELL TECHNOLOGIES

- 6.3.2 MICROGRID TECHNOLOGIES

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE AND BUYING BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY BUYER STAKEHOLDERS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 TRAIN BATTERY MARKET, BY BATTERY TYPE & BATTERY TECHNOLOGY

- 9.1 INTRODUCTION

- 9.2 LEAD-ACID BATTERIES

- 9.2.1 CONVENTIONAL LEAD-ACID BATTERIES

- 9.2.1.1 Growing popularity of VRLA batteries to impact demand for conventional lead-acid batteries

- 9.2.2 VALVE-REGULATED LEAD-ACID BATTERIES

- 9.2.2.1 High reliability and low cost of ownership to drive market

- 9.2.3 GEL TUBULAR LEAD-ACID BATTERIES

- 9.2.3.1 High current applications to increase demand

- 9.2.1 CONVENTIONAL LEAD-ACID BATTERIES

- 9.3 NICKEL-CADMIUM BATTERIES

- 9.3.1 SINTER/PNE NICKEL-CADMIUM BATTERIES

- 9.3.1.1 Good chargeability and longer life cycle to drive demand

- 9.3.2 POCKET PLATE NICKEL-CADMIUM BATTERIES

- 9.3.2.1 Lower energy density capacity and short lifetime to impact demand

- 9.3.3 FIBER/PNE NICKEL-CADMIUM BATTERIES

- 9.3.3.1 Reduction in shortcomings of second-generation nickel-cadmium battery technology to drive demand

- 9.3.1 SINTER/PNE NICKEL-CADMIUM BATTERIES

- 9.4 LITHIUM-ION BATTERIES

- 9.4.1 LITHIUM IRON PHOSPHATE BATTERIES

- 9.4.1.1 Good chargeability and longer life cycle to drive demand

- 9.4.2 LITHIUM TITANATE OXIDE BATTERIES

- 9.4.2.1 Fast charging capability to drive demand

- 9.4.3 OTHERS

- 9.4.4 INDUSTRY INSIGHTS

- 9.4.1 LITHIUM IRON PHOSPHATE BATTERIES

10 TRAIN BATTERY MARKET, BY APPLICATION & BATTERY TYPE

- 10.1 INTRODUCTION

- 10.2 STARTER BATTERIES

- 10.2.1 LEAD-ACID BATTERIES

- 10.2.1.1 Easy transportation and value for cost to increase demand in the rail sector

- 10.2.2 NICKEL-CADMIUM BATTERIES

- 10.2.2.1 Uninterruptible power supply and high current supply for diesel starting motors to drive demand

- 10.2.1 LEAD-ACID BATTERIES

- 10.3 AUXILIARY BATTERIES

- 10.3.1 LEAD-ACID BATTERIES

- 10.3.1.1 Cost competitiveness and durability to increase demand in the rail sector

- 10.3.2 NICKEL-CADMIUM BATTERIES

- 10.3.2.1 High energy density, longer lifespan, and ability to deliver high currents to increase market penetration

- 10.3.3 LITHIUM-ION BATTERIES

- 10.3.3.1 Fast charging time, longer lifespan, and high energy density to drive adoption in rolling stock

- 10.3.4 INDUSTRY INSIGHTS

- 10.3.1 LEAD-ACID BATTERIES

11 TRAIN BATTERY MARKET, BY ENGINE/HEAD

- 11.1 INTRODUCTION

- 11.2 DIESEL LOCOMOTIVES

- 11.2.1 DEVELOPMENT OF FREIGHT TRAINS AND RAIL NETWORKS IN EMERGING ECONOMIES TO DRIVE MARKET

- 11.3 DIESEL MULTIPLE UNITS

- 11.3.1 EXPANSION OF INTERCITY RAIL NETWORKS TO DRIVE MARKET

- 11.4 ELECTRIC LOCOMOTIVES

- 11.4.1 LOW MAINTENANCE COST AND HIGHER OPERATIONAL EFFICIENCY TO DRIVE MARKET

- 11.5 ELECTRIC MULTIPLE UNITS

- 11.5.1 ADVANCEMENTS IN LIGHTING SOLUTIONS, SAFETY DOORS, AND HVACS TO DRIVE MARKET

- 11.5.2 INDUSTRY INSIGHTS

12 TRAIN BATTERY MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 METROS

- 12.2.1 EXPANSION OF URBAN RAIL NETWORK TO DRIVE DEMAND

- 12.3 HIGH-SPEED TRAINS

- 12.3.1 INFRASTRUCTURE DEVELOPMENT AND NEED FOR CHEAPER AND FASTER TRANSPORTATION MODES TO DRIVE DEMAND

- 12.4 LIGHT RAILS/TRAMS/MONORAILS

- 12.4.1 RAPID URBANIZATION AND AESTHETIC VALUE TO DRIVE DEMAND

- 12.5 PASSENGER COACHES

- 12.5.1 RAIL EXPANSION PROJECTS AND AN INCREASING NUMBER OF PASSENGERS TO DRIVE DEMAND

- 12.5.2 INDUSTRY INSIGHTS

13 TRAIN BATTERY MARKET, BY ADVANCED TRAIN TYPE

- 13.1 INTRODUCTION

- 13.2 HYBRID TRAINS

- 13.2.1 REDUCTION IN ENERGY CONSUMPTION AND REDUCED LIFECYCLE COST TO DRIVE DEMAND

- 13.3 FULLY BATTERY-OPERATED TRAINS

- 13.3.1 EXPANSION OF RAIL NETWORK AND HIGHER COST OF ELECTRIFICATION TO DRIVE DEMAND

- 13.4 AUTONOMOUS TRAINS

- 13.4.1 CONTINUOUS DEVELOPMENTS, LOW COST OF OPERATION, AND LOW ENERGY CONSUMPTION TO DRIVE DEMAND

- 13.4.2 INDUSTRY INSIGHTS

14 TRAIN BATTERY AFTERMARKET, BY ROLLING STOCK

- 14.1 INTRODUCTION

- 14.2 LOCOMOTIVES

- 14.2.1 IMPROVED LIFE CYCLE OF LOCOMOTIVES TO DRIVE DEMAND FOR TRAIN BATTERIES

- 14.3 MULTIPLE UNITS

- 14.3.1 ADVANCED FEATURES IN URBAN TRANSIT SYSTEMS TO INCREASE TRAIN BATTERY ADOPTION IN MULTIPLE UNITS

- 14.4 PASSENGER COACHES

- 14.4.1 REFURBISHMENT PROJECTS TO EXTEND THE OPERATIONAL LIFE OF PASSENGER COACHES TO BOOST DEMAND

- 14.4.2 INDUSTRY INSIGHTS

15 TRAIN BATTERY AFTERMARKET, BY BATTERY TYPE

- 15.1 INTRODUCTION

- 15.2 LEAD-ACID BATTERIES

- 15.2.1 FREQUENT REPLACEMENT RATE AND LOW CYCLE LIFE TO DRIVE DEMAND

- 15.3 NICKEL-CADMIUM BATTERIES

- 15.3.1 LONGER LIFE AND EASY MAINTENANCE TO BOOST MARKET SHARE

- 15.3.2 INDUSTRY INSIGHTS

16 TRAIN BATTERY AFTERMARKET, BY APPLICATION

- 16.1 INTRODUCTION

- 16.2 STARTER BATTERIES

- 16.2.1 REQUIREMENT FOR REPLACEMENT BATTERIES IN DMUS AND DIESEL LOCOMOTIVES TO DRIVE DEMAND

- 16.3 AUXILIARY BATTERIES

- 16.3.1 GROWING POWER REQUIREMENT FOR ONBOARD ELECTRIC SYSTEMS TO RAISE DEMAND

- 16.3.2 INDUSTRY INSIGHTS

17 TRAIN BATTERY MARKET, BY REGION

- 17.1 INTRODUCTION

- 17.2 ASIA PACIFIC

- 17.2.1 CHINA

- 17.2.1.1 Rail expansion projects to drive the market

- 17.2.2 INDIA

- 17.2.2.1 Electrification of rail routes to drive market

- 17.2.3 JAPAN

- 17.2.3.1 Development of high-speed EMUs to drive market

- 17.2.4 SOUTH KOREA

- 17.2.4.1 Strong urban rail network and development of high-speed rail service to drive market

- 17.2.1 CHINA

- 17.3 EUROPE

- 17.3.1 GERMANY

- 17.3.1.1 Replacement of diesel locomotives with battery-operated trains to drive market

- 17.3.2 FRANCE

- 17.3.2.1 Stringent emission norms for locomotives to boost demand for train batteries

- 17.3.3 ITALY

- 17.3.3.1 Increasing demand for batteries for EMUs and light rails to drive market

- 17.3.4 UK

- 17.3.4.1 Urban rail developments to drive market

- 17.3.5 SPAIN

- 17.3.5.1 Investment in high-speed rail networks to drive market

- 17.3.6 SWITZERLAND

- 17.3.6.1 Growing development of passenger trains to drive demand for batteries

- 17.3.7 POLAND

- 17.3.7.1 Development of intercity trains to drive demand for batteries

- 17.3.8 SWEDEN

- 17.3.8.1 Rising demand for regional trains to drive market

- 17.3.1 GERMANY

- 17.4 NORTH AMERICA

- 17.4.1 US

- 17.4.1.1 Rising diesel prices to drive market

- 17.4.2 CANADA

- 17.4.2.1 Development of commuter trains like metros and passenger rails to drive demand for batteries

- 17.4.3 MEXICO

- 17.4.3.1 Growing development of catenary-free rail tracks to drive market

- 17.4.1 US

- 17.5 REST OF THE WORLD

- 17.5.1 BRAZIL

- 17.5.1.1 Growing demand for auxiliary function batteries to drive market

- 17.5.2 RUSSIA

- 17.5.2.1 Increasing demand for wide temperature range rail batteries to drive market

- 17.5.3 INDUSTRY INSIGHTS

- 17.5.1 BRAZIL

18 TRAIN BATTERY AFTERMARKET, BY REGION

- 18.1 INTRODUCTION

- 18.2 ASIA PACIFIC

- 18.2.1 HIGH NUMBER OF ROLLING STOCKS TO DRIVE REPLACEMENT DEMAND

- 18.3 EUROPE

- 18.3.1 EXPANSION OF INTERCITY RAIL NETWORKS TO DRIVE DEMAND

- 18.4 NORTH AMERICA

- 18.4.1 GROWING DIESEL LOCOMOTIVE RETROFITTING AND REFURBISHMENT TO DRIVE DEMAND

- 18.4.2 INDUSTRY INSIGHTS

19 COMPETITIVE LANDSCAPE

- 19.1 OVERVIEW

- 19.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 19.3 REVENUE ANALYSIS OF TOP LISTED/PUBLIC PLAYERS

- 19.4 MARKET SHARE ANALYSIS, 2025

- 19.5 BRAND COMPARISON

- 19.6 COMPANY EVALUATION MATRIX: KEY TRAIN BATTERY MANUFACTURERS, 2025

- 19.6.1 STARS

- 19.6.2 EMERGING LEADERS

- 19.6.3 PERVASIVE PLAYERS

- 19.6.4 PARTICIPANTS

- 19.6.5 COMPANY FOOTPRINT: KEY TRAIN BATTERY MANUFACTURERS, 2025

- 19.6.5.1 Company footprint

- 19.6.5.2 Region footprint

- 19.6.5.3 Application footprint

- 19.7 COMPETITIVE EVALUATION MATRIX: KEY BATTERY-POWERED TRAIN MANUFACTURERS, 2025

- 19.7.1 STARS

- 19.7.2 EMERGING LEADERS

- 19.7.3 PERVASIVE PLAYERS

- 19.7.4 PARTICIPANTS

- 19.7.5 COMPANY FOOTPRINT: KEY BATTERY-POWERED TRAIN MANUFACTURERS, 2025

- 19.7.5.1 Company footprint

- 19.7.5.2 Application footprint

- 19.7.5.3 Rolling stock footprint

- 19.8 COMPANY VALUATION

- 19.9 COMPANY FINANCIAL METRICS

- 19.10 COMPETITIVE SCENARIO

- 19.10.1 PRODUCT LAUNCHES

- 19.10.2 DEALS

- 19.10.3 EXPANSIONS

- 19.10.4 OTHER DEVELOPMENTS

20 COMPANY PROFILES

- 20.1 KEY PLAYERS

- 20.1.1 ENERSYS

- 20.1.1.1 Business overview

- 20.1.1.2 Products offered

- 20.1.1.3 Recent developments

- 20.1.1.3.1 Product launches

- 20.1.1.4 MnM view

- 20.1.1.4.1 Key strengths

- 20.1.1.4.2 Strategic choices

- 20.1.1.4.3 Weaknesses and competitive threats

- 20.1.2 SAFT

- 20.1.2.1 Business overview

- 20.1.2.2 Products offered

- 20.1.2.3 Recent developments

- 20.1.2.3.1 Deals

- 20.1.2.3.2 Expansions

- 20.1.2.4 MnM view

- 20.1.2.4.1 Key strengths

- 20.1.2.4.2 Strategic choices

- 20.1.2.4.3 Weaknesses and competitive threats

- 20.1.3 GS YUASA INTERNATIONAL LTD.

- 20.1.3.1 Business overview

- 20.1.3.2 Products offered

- 20.1.3.3 Recent developments

- 20.1.3.3.1 Product launches

- 20.1.3.3.2 Expansions

- 20.1.3.4 MnM view

- 20.1.3.4.1 Key strengths

- 20.1.3.4.2 Strategic choices

- 20.1.3.4.3 Weaknesses and competitive threats

- 20.1.4 EXIDE INDUSTRIES LTD.

- 20.1.4.1 Business overview

- 20.1.4.2 Products offered

- 20.1.4.3 Recent developments

- 20.1.4.3.1 Deals

- 20.1.4.3.2 Expansions

- 20.1.4.4 MnM view

- 20.1.4.4.1 Key strengths

- 20.1.4.4.2 Strategic choices

- 20.1.4.4.3 Weaknesses and competitive threats

- 20.1.5 AMARA RAJA BATTERIES LIMITED

- 20.1.5.1 Business overview

- 20.1.5.2 Products offered

- 20.1.5.3 Recent developments

- 20.1.5.3.1 Deals

- 20.1.5.3.2 Expansions

- 20.1.5.3.3 Other developments

- 20.1.5.4 MnM view

- 20.1.5.4.1 Key strengths

- 20.1.5.4.2 Strategic choices

- 20.1.5.4.3 Weaknesses and competitive threats

- 20.1.6 HOPPECKE BATTERIEN GMBH & CO. KG

- 20.1.6.1 Business overview

- 20.1.6.2 Products offered

- 20.1.6.3 Recent developments

- 20.1.6.3.1 DEALS

- 20.1.7 TOSHIBA CORPORATION

- 20.1.7.1 Business overview

- 20.1.7.2 Products offered

- 20.1.7.3 Recent developments

- 20.1.7.3.1 Product launches

- 20.1.7.3.2 Deals

- 20.1.8 SEC BATTERY

- 20.1.8.1 Business overview

- 20.1.8.2 Products offered

- 20.1.9 POWER & INDUSTRIAL BATTERY SYSTEMS GMBH

- 20.1.9.1 Business overview

- 20.1.9.2 Products offered

- 20.1.10 EXIDE TECHNOLOGIES

- 20.1.10.1 Business overview

- 20.1.10.2 Products offered

- 20.1.1 ENERSYS

- 20.2 OTHER PLAYERS

- 20.2.1 EAST PENN MANUFACTURING COMPANY

- 20.2.2 MICROTEX ENERGY PRIVATE LIMITED

- 20.2.3 AEG POWER SOLUTIONS

- 20.2.4 THE FURUKAWA BATTERY CO., LTD.

- 20.2.5 HUNAN FENGRI POWER & ELECTRIC CO., LTD.

- 20.2.6 SHUANGDENG GROUP CO., LTD.

- 20.2.7 COSLIGHT INDIA

- 20.2.8 SHIELD BATTERIES LIMITED

- 20.2.9 AKASOL AG

- 20.2.10 DMS TECHNOLOGIES

- 20.2.11 NATIONAL RAILWAY SUPPLY

- 20.2.12 LECLANCHE SA

- 20.2.13 ECOBAT

- 20.2.14 HBL BATTERIES

- 20.2.15 STAR BATTERY LTD.

- 20.2.16 HITACHI, LTD.

21 RESEARCH METHODOLOGY

- 21.1 RESEARCH DATA

- 21.1.1 SECONDARY DATA

- 21.1.2 LIST OF KEY SECONDARY SOURCES TO ESTIMATE BASE NUMBERS AND MARKET SIZING (LOCOMOTIVE & ROLLING STOCK)

- 21.1.2.1 Key data from secondary sources

- 21.1.3 PRIMARY DATA

- 21.1.3.1 Sampling techniques and data collection methods

- 21.1.4 PRIMARY PARTICIPANTS

- 21.2 MARKET SIZE ESTIMATION

- 21.2.1 BOTTOM-UP APPROACH: TRAIN BATTERY MARKET, BY BATTERY TYPE AND ROLLING STOCK

- 21.2.2 TOP-DOWN APPROACH: TRAIN BATTERY MARKET, BY BATTERY TECHNOLOGY

- 21.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 21.4 RESEARCH LIMITATIONS

- 21.5 RISKS AND ASSUMPTIONS

- 21.5.1 MARKET ASSUMPTIONS

22 APPENDIX

- 22.1 INSIGHTS FROM INDUSTRY EXPERTS

- 22.2 DISCUSSION GUIDE

- 22.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 22.4 CUSTOMIZATION OPTIONS

- 22.4.1 TRAIN BATTERY MARKET, BY APPLICATION AND ROLLING STOCK

- 22.4.2 TRAIN BATTERY MARKET, BY ROLLING STOCK AND BY BATTERY TYPE

- 22.4.3 US TRAIN BATTERY AFTERMARKET, BY ROLLING STOCK

- 22.5 RELATED REPORTS

- 22.6 AUTHOR DETAILS