|

시장보고서

상품코드

1445519

황산 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Sulfuric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

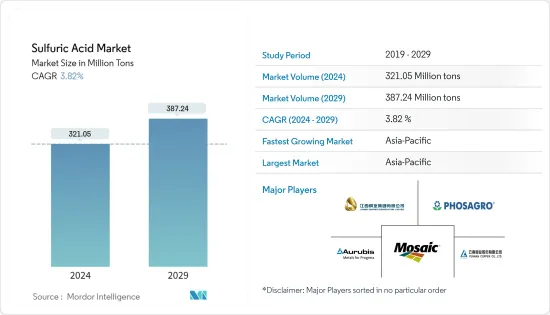

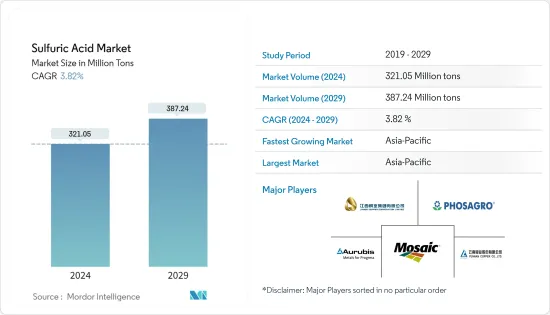

황산 시장 규모는 2024년 3억 2,105만 톤으로 추정되며, 2029년까지 3억 8,724만 톤에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 3.82%의 CAGR로 성장할 것으로 예상됩니다.

COVID-19는 2020년 황산 시장에 적당한 영향을 미쳤습니다. 여러 국가의 봉쇄 발동과 공급 중단은 화학 부문에 영향을 미쳤습니다. 그러나 황산은 화학 부문에서 사용되는 주요 화학제품 중 하나이기 때문에 예측 기간 동안 높은 수요가 예상됩니다.

주요 하이라이트

- 단기적으로 인산염 기반 비료의 황산에 대한 높은 수요와 전 세계 화학 산업 및 제약 산업의 수요 증가로 인해 시장 조사가 추진되고 있습니다.

- 한편, 원자재 가격 변동으로 인해 향후 몇 년 동안 황산 시장의 성장이 둔화 될 수 있습니다.

- 의료 및 기타 산업에서 발연 황산 사용의 증가는 시장에 큰 기회로 간주 될 수 있습니다.

- 아시아태평양은 세계 황산 시장을 독점하고 있으며 중국, 인도, 일본 등 국가가 가장 많이 소비하고 있습니다.

황산 시장 동향

비료 부문의 소비 확대

- 황산은 황, 수소, 산소로 구성된 강력한 광산입니다. 강한 냄새가 나고 매우 부식성이 강한 기름진 투명한 액체입니다. 희석된 상태에서도 항상 조심스럽게 취급해야 합니다. 물로 희석하면 세라믹의 배기 반응으로 열을 방출합니다. 비료 생산 공정에 사용되는 중요한 산업용 화학제품입니다.

- 전 세계 황산 공급량의 약 절반은 농업과 농업, 특히 비료로 사용됩니다. 황산은 석회 과인산 염 및 황산 암모늄과 같은 인산 비료의 제조에 사용됩니다. 황산은 농작물 수확량을 증가시키고 영양가가 높은 작물을 생산하여 농부들이 더 많은 수익을 올릴 수 있도록 도와줍니다.

- 비료는 작물이 토양에서 제거한 영양분을 보충합니다. 비료가 없으면 작물 수확량과 농업 생산성이 크게 감소합니다. 이 때문에 미네랄 비료는 작물이 즉시 흡수하여 사용할 수 있는 미네랄로 토양의 영양분을 보충하기 위해 사용됩니다.

- 농업은 전 세계적으로 주요 생계수단입니다. 인도와 미국에서는 농업이 긍정적인 성장세를 보이고 있습니다. 따라서 향후 몇 년 동안 시장은 비료 수요에 의해 움직일 수 있습니다.

- 예를 들어, 식량농업기구에 따르면 2021년 세계 암모니아, 인산, 칼륨의 생산 능력은 315,973톤으로 2022년에는 318,652톤에 달할 것으로 예상되며, 이는 황산에 대한 시장 수요를 증가시킬 것으로 예상됩니다. 예측 기간.

- 2021년 농산물 및 관련 제품의 총 수출액은 412억 5,000만 달러에 달했습니다. 관개에 대한 투자 증가는 총 관개 면적을 확대하고 비료에 대한 수요를 창출하여 황산 시장을 자극했습니다.

- 라틴아메리카와 카리브해 지역의 농업 부문은 과거에 상당한 성장을 이루었습니다. 경제협력개발기구(OECD)와 유엔식량농업기구(FAO)에 따르면 2018년부터 2028년까지 농업 및 어업 생산량이 17% 증가할 것으로 예상됩니다. 이 성장의 약 53%는 작물 생산량 증가에 기인할 것으로 예상됩니다. 따라서 농업 산업의 성장으로 인해 비료에 대한 수요가 증가했습니다. 이는 황산 시장의 성장에 영향을 미칠 것으로 예상됩니다.

- 국제비료산업협회에 따르면 2021년 전 세계 농업용 비료(질소, 인, 칼륨(NPK)) 소비량은 199,884 킬로톤으로 집계됐습니다. 총 소비량 중 동아시아, 남아시아, 라틴아메리카, 카리브해 국가 및 북미는 2021년에 각각 6만 1,936kg, 3만 8,694kg, 2만 8,817kg, 2만 5,730kg, 2만 8,817kg, 2만 5,730kg을 소비했습니다.

- 따라서 향후 몇 년 동안 시장은 비료에서 황산 사용이 증가함에 따라 시장이 주도 할 수 있습니다.

아시아태평양이 시장을 독점

- 아시아태평양은 예측 기간 동안 황산 시장을 장악할 것으로 예상됩니다. 중국, 인도, 일본 등의 화학, 비료 및 기타 제조 부문의 높은 수요로 인해 황산 시장은 빠르게 성장하고 있습니다.

- 중국 국가 통계국에 따르면 2021년 중국의 황산 생산량은 9,383 만 톤으로 2020년 9,238 만 톤에 비해 1.5 % 이상 증가했습니다. 중국의 황산 생산량은 계속 증가하여 2022년 생산 능력은 1억 2,900 만 톤으로 전년 동기 대비 1.59 % 증가했습니다.

- 중국에서는 각 기업이 황산 생산능력을 연간 2,108만 톤으로 확대할 계획을 세우고 있습니다. 2022년부터 2024년까지 생산능력 증설 후 국내 황산 시장의 공급 패턴은 수출 증가, 수입 감소, 물량 흐름의 변화 등 큰 변화를 겪을 것으로 예상됩니다.

- 중국은 세계 최대의 비료 생산국입니다. 중국 국가통계국에 따르면 2021년 중국의 질소, 인산염, 칼륨 비료 생산량은 5,544만 톤으로 2020년 5,496만 톤에 비해 0.87% 증가했습니다.

- 인도에서는 2021년 7월 오리사 주 총리가 비료 협동조합 IFFCO의 파라딥 사업부 부지에 황산 생산 시설의 초석을 놓았습니다. 이 프로젝트의 비용은 약 4억 인도 루피(약 4,836만 달러)이며, 2023년까지 가동을 시작할 예정입니다. 이 새로운 생산 공장은 화학제품 수입 의존도를 줄일 수 있습니다. 이는 IFFCO의 세 번째 황산 생산 공장으로 하루 약 2,000톤(MT)의 생산 능력을 갖추고 있습니다.

- 또한 인도는 농업에 크게 의존하는 경제 국가 중 하나입니다. 농업은 여전히 인구의 55% 이상의 주요 생계 수단입니다. 인도 경제조사 2020-21 보고서에 따르면, 2020년도 국내 식용 곡물 총 생산량은 2억 9,665만 톤으로 19년도의 2억 8,521만 톤에 비해 1,144만 톤이 증가했습니다.

- 위의 모든 요인으로 인해 예측 기간 동안 아시아태평양의 황산 수요가 증가할 것으로 예상됩니다.

황산 산업 개요

세계 황산 시장은 매우 세분화되어 있습니다. 시장을 지배하는 상위 5개 기업은 Mosaic, PhosAgro Group of Companies, Jiangxi Copper Group, Yunnan Copper, Aurubis AG입니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사 가정

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 인산염 기반 비료의 황산의 높은 수요

- 화학 및 제약 업계로부터의 수요 확대

- 성장 억제요인

- 원재료 가격 변동성

- 업계의 밸류체인 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 구매자의 교섭력

- 신규 참여업체의 위협

- 대체 제품과 서비스의 위협

- 경쟁 정도

- 무역 분석

- 원료 분석

- 지역 생산능력

제5장 시장 세분화

- 원재료 종류

- 원소 유황

- 황철석

- 기타 원재료 종류

- 최종 이용 산업

- 비료

- 화학 및 의약품

- 자동차

- 정유

- 기타 최종 이용 산업(제지·펄프, 금속 가공)

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 상황

- 합병, 인수, 합작투자, 협업 및 계약

- 시장 점유율(%) 분석

- 유력 기업이 채용한 전략

- 기업 개요

- Aarti Industries Limited

- Aurubis AG

- Bodal Chemicals Ltd

- Boliden Group

- Hindustan Zinc

- Jiangxi Copper Group Co. Ltd

- KANTO KAGAKU

- Nouryon

- Panoli Intermediates India Private Limited

- PhosAgro Group of Companies

- PVS

- Mosaic

- WeylChem International GmbH

- Yunnan Copper Co. Ltd

제7장 시장 기회와 향후 동향

- 의료 및 기타 산업의 발연황산 사용 증가

The Sulfuric Acid Market size is estimated at 321.05 Million tons in 2024, and is expected to reach 387.24 Million tons by 2029, growing at a CAGR of 3.82% during the forecast period (2024-2029).

The COVID-19 pandemic moderately affected the sulfuric acid market in 2020. The imposition of lockdowns across various countries and disruptions in supply affected the chemical sector. However, since sulfuric acid is among the primary chemicals used in the chemical sector, high demand is anticipated in the forecast period.

Key Highlights

- In the short term, the market study is being driven by the high demand for sulfuric acid in phosphate-based fertilizers and the growing demand from the chemical and pharmaceutical industries around the world.

- On the other hand, changes in the prices of raw materials are likely to slow the growth of the sulfuric acid market in the coming years.

- The growing use of oleum in medical and other industries can be seen as a major opportunity for the market.

- The Asia-Pacific region dominated the sulfuric acid market globally, with the highest consumption coming from countries such as China, India, and Japan.

Sulfuric Acid Market Trends

Growing Consumption from Fertilizer Segment

- Sulfuric acid is a strong mineral acid made up of sulfur, hydrogen, and oxygen. It has a strong smell and is an extremely corrosive, oily, and clear liquid. It should always be handled with caution, even in its diluted form. When diluted with water, it releases heat in a ceramic exhaust reaction. It is an important industrial chemical used in fertilizer manufacturing processes.

- Around half of the global sulfuric acid supply is used in agriculture and farming, especially as fertilizer. Sulfuric acid is used to manufacture phosphate fertilizers, such as the superphosphate of lime and ammonium sulfate. Sulfuric acid increases crop yield, which helps farmers generate more revenue by producing highly nutritional crops.

- Fertilizers replace the nutrients that crops remove from the soil. Without fertilizers, crop yields and agricultural productivity would be significantly reduced. Due to this, mineral fertilizers are used to supplement the soil's nutrient stocks with minerals that may be quickly absorbed and used by crops.

- Agriculture is the major source of livelihood globally; India and the United States are witnessing positive growth in agriculture. So, the market is likely to be driven by the need for fertilizers over the next few years.

- For instance, according to the Food and Agriculture Organization, the global capacity for producing ammonia, phosphoric acid, and potash in 2021 was 315,973 metric tons, which is expected to reach 318,652 metric tons in 2022, thereby boosting the market demand for sulfuric acid in the forecast period.

- The total agricultural and allied products exports stood at USD 41.25 billion in 2021. The growing investments in irrigation enhanced the gross irrigated area, creating a demand for fertilizers and stimulating the sulfuric acid market.

- The agriculture sector in Latin America and the Caribbean has witnessed significant growth in the past. According to the Organization for Economic Co-operation and Development (OECD) and the Food and Agriculture Organization of the United Nations (FAO), agricultural and fisheries production is expected to grow by 17% during 2018-2028. Around 53% of this growth is expected to come from increased crop production. Hence, the growing agricultural industry boosted the demand for fertilizers. This is expected to impact the growth of the sulfuric acid market.

- According to the International Fertilizer Industry Association, the consumption of agricultural fertilizer (nitrogen, phosphorus, and potassium (NPK)) across the globe accounted for 199,884 kilotons in 2021. Out of the total consumption, East Asia, South Asia, Latin America and the Caribbean, and North America consumed 61,936 kilotons, 38,694 kilotons, 28,817 kilotons, and 25,730 kilotons, respectively, in 2021.

- So, the market is likely to be driven by the growing use of sulfuric acid in fertilizers over the next few years.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the sulfuric acid market during the forecast period. Due to the high demand from the chemical, fertilizer, and other manufacturing sectors in countries like China, India, and Japan, the sulfuric acid market has been rapidly increasing.

- In 2021, the sulfuric acid production in China was 93.83 million metric tons, compared to 92.38 million metric tons in 2020, registering a growth of over 1.5%, according to the National Bureau of Statistics of China. The sulfuric acid production output continued to rise in China, with a manufacturing capacity of 129 million tons in 2022, registering a growth of 1.59% from the same period in the previous year.

- In China, companies are planning to increase the manufacturing capacity of sulfuric acid to 21.08 million tons annually. After the capacity increase in 2022-2024, the supply pattern of the sulfuric acid market is expected to undergo significant changes in the country, including increasing exports, shrinking imports, and changes in goods flow.

- China is the largest fertilizer manufacturer in the world. According to the National Bureau of Statistics of China, the nitrogen, phosphate, and potash fertilizer production volume in China accounted for 55.44 million tons in 2021, compared to 54.96 million tons in 2020, registering a growth of 0.87%.

- In India, in July 2021, the Chief Minister of Odisha laid the foundation stone for a sulfuric acid manufacturing facility on the premises of the fertilizer cooperative IFFCO at its Paradip division. The project will cost around INR 400 crore (~USD 48.36 million), with operations estimated to start by 2023. This new production plant will reduce dependency on the import of chemicals. This is IFFCO's third sulfuric acid manufacturing plant, with a capacity of about 2,000 metric tons (MT) per day.

- Furthermore, India is one of the economies largely dependent on agriculture. Agriculture is still the primary source of livelihood for more than 55% of the population. According to The Economic Survey of India 2020-21 report, in FY20, the total food grain production in the country was recorded at 296.65 million tons, which increased by 11.44 million tons compared with 285.21 million tons in FY19.

- All the factors mentioned above are expected to boost the demand for sulfuric acid in the Asian-Pacific region over the forecast period.

Sulfuric Acid Industry Overview

The global sulfuric acid market is highly fragmented. The top five players dominating the market are Mosaic, PhosAgro Group of Companies, Jiangxi Copper Group Co. Ltd, Yunnan Copper Co. Ltd, and Aurubis AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 High Demand for Sulfuric Acid in Phosphate-based Fertilizers

- 4.1.2 Growing Demand from Chemical and Pharmaceutical Industries

- 4.2 Restraints

- 4.2.1 Volatility In Raw Material Pricing

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Trade Analysis

- 4.6 Feedstock Analysis

- 4.7 Regional Production Capacities

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Raw Material Type

- 5.1.1 Elemental Sulfur

- 5.1.2 Pyrite Ore

- 5.1.3 Other Raw Material Types

- 5.2 End-user Industry

- 5.2.1 Fertilizer

- 5.2.2 Chemical and Pharmaceutical

- 5.2.3 Automotive

- 5.2.4 Petroleum Refining

- 5.2.5 Other End-user Industries (Pulp and Paper, Metal Processing)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aarti Industries Limited

- 6.4.2 Aurubis AG

- 6.4.3 Bodal Chemicals Ltd

- 6.4.4 Boliden Group

- 6.4.5 Hindustan Zinc

- 6.4.6 Jiangxi Copper Group Co. Ltd

- 6.4.7 KANTO KAGAKU

- 6.4.8 Nouryon

- 6.4.9 Panoli Intermediates India Private Limited

- 6.4.10 PhosAgro Group of Companies

- 6.4.11 PVS

- 6.4.12 Mosaic

- 6.4.13 WeylChem International GmbH

- 6.4.14 Yunnan Copper Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Use of Oleum in Medical and Other Industries