|

시장보고서

상품코드

1639441

차세대 검색 엔진 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Next Generation Search Engines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

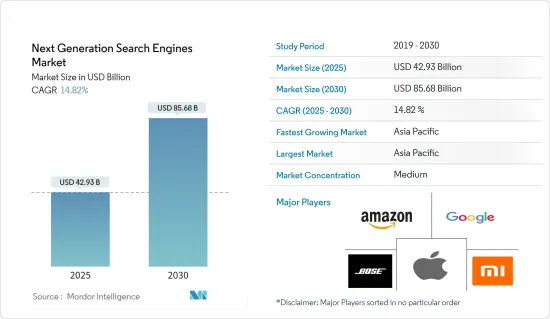

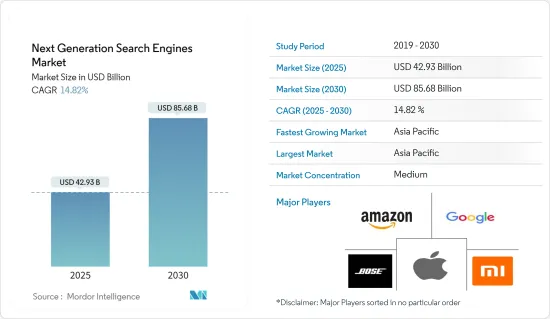

차세대 검색 엔진 시장 규모는 2025년에 429억 3,000만 달러로 추정됩니다. 예측기간(2025-2030년)의 CAGR은 14.82%로, 2030년에는 856억 8,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 차세대 검색 엔진은 사용 가능한 솔루션을 평가하고 소프트웨어 및 데이터 공급자와 상호 작용하기 위해 검색에 대한 실무 지식을 얻고자 하는 의사 결정자 및 과학자에게 고급 정보 검색 모델을 제공합니다. 최근 몇 년 동안 음성 검색의 수가 급격히 증가하고 있습니다. 또한 음성 검색은 참신함보다는 새로운 표준에 가까워지고 있습니다. 따라서 차세대 검색 엔진은 음성 기반 검색 엔진을 지향합니다.

- 딥 신경망과 머신러닝 등 AI 기술의 진보로 차세대 검색 엔진도 늘고 있습니다. 스마트 스피커와 같은 가상 어시스턴트는 소매, 은행/금융서비스/보험(BFSI), 의료 등 여러 최종 사용자 산업에 걸쳐 다양한 용도로 사용됩니다. 소비자를 위한 주요 용도 중 하나는 개인 어시스턴트입니다. 이렇게하면 소비자가 여러 작업을 수행하는 데 도움이 됩니다. 예를 들어, Apple의 Siri는 커넥티드 홈과 자동차에 직관적인 인터페이스를 제공합니다.

- 셀프서비스 옵션에 대한 수요 증가는 보다 놀라운 속도와 편의성을 요구하는 소비자 수요가 급속히 증가하고 있음을 보여줍니다. NICE의 2022 Digital First Customer Experience Report에 따르면 소비자의 81%가 더 많은 셀프 서비스 옵션을 원한다고 답했습니다. 그러나 제공된 툴에 높은 만족도를 보인 소비자는 불과 15%에 그쳤습니다. 이 동향은 차세대 검색 엔진 시장 수요를 견인하고 있습니다.

- 전문 서비스의 고객 경험 향상에 주목 증가가 시장을 견인합니다. 고객 경험의 향상은 풍부한 보상을 제공합니다. 업종에 관계없이 만족도가 높은 고객은 소비액이 늘어나고 장기간에 걸쳐 로열티가 유지됩니다. 고객에게 공감을 나타내고 문제 해결을 지원함으로써 이러한 기업은 엄청난 가치의 원천을 활용하고, 새로운 비즈니스 기회를 찾아 장기적으로 비즈니스 모델을 전환할 수 있습니다.

- 라이브 퍼슨 인터랙션에 대한 선호도 증가는 시장을 억제할 수 있습니다. Liveperson Inc.가 실시한 조사에 따르면 세계 소비자의 87%가 음성 및 메시징을 통한 상호작용에 유연하게 대응하는 기업을 선호하고 있습니다. 이러한 선호도는 상황과 시간대에 따라 변하기 때문에 소비자가 원하는 때에 원하는 곳에서 원하는 조건에서 사용할 수 있도록 하는 것이 중요합니다.

차세대 검색 엔진 시장 동향

가장 높은 성장을 이루는 셀프서비스와 퍼스널 부문

- 개인용 최종 사용자용 스마트 스피커가 점유율의 대부분을 차지할 것으로 예상됩니다. 현재 스마트 스피커에 기대되는 기능으로는 음악 재생과 모든 질문에 답하는 음성 어시스턴트로 구성된 스마트 홈 기기의 제어 등이 있습니다.

- 소비자용 애플리케이션 개발의 기술적 강화는 스마트 홈 또는 커넥티드 홈의 통합을 가져왔습니다. 스마트 홈 개발로 최종 사용자는 모바일 인터넷과 고속 광대역 연결을 시장 전 가구에 도입하게 되었습니다.

- 음성 시작 스피커는 사람들의 일과의 일부가 되었습니다. 음성 스피커는 멀티태스킹을 수행하면서 기술을 사용하는 능력을 설명합니다. 맞춤형 답변은 음성 검색의 유명한 이용 사례 중 하나이며, Google은 사용자가 다음에 묻는 질문을 알고 추측할 수 있기 때문에 상당한 정도까지 도달했습니다. 반면 Alexa는 Google처럼 컨텍스트를 이해할 수 없습니다. Alexa는 맞춤 제작 기술과 프로토콜에 의존하는 반면 Google Assistant는 특정 사용자의 요청을 이해하고 개인화된 답변을 제공할 수 있습니다.

- 음성 사용자는 제품 조사, 가격 비교, 장바구니에 추가 등 구매 과정을 따라 많은 작업을 수행하기 위해 도우미를 사용합니다. Adobe의 조사에 따르면 소비자는 쇼핑 과정에서 음성을 사용하고 있습니다. 상위 3가지 활동은 상품 조사/리서치(47%), 쇼핑 목록 작성(43%), 가격 비교(32%)였습니다.

- 스마트 스피커로 가장 유명한 것은 Amazon Echo와 Google Nest 시리즈이지만 알렉사와 Google 어시스턴트를 모두 내장한 Sonos One과 같은 타사 스피커도 많이 있습니다.

- 미국은 여전히 개인용 부문, 특히 음성 어시스턴트의 보급에 중요한 시장입니다. eMarketer에 따르면 음성 어시스턴트의 수는 지난 5년간 1억 300만 대에서 1억 2,300만 대로 증가했습니다. NPR의 최신 스마트 오디오 보고서에 따르면, 18세 이상의 미국인의 24%가 적어도 하나의 스마트 스피커를 소유하고 있습니다. 평균 소유자는 여러 개 있습니다. 미국인의 과반수가 알렉사를 소유하고 있습니다. 아마존이 처음으로 에코를 발표한 이래 미국에서 인기를 얻고 있으며, 톱 클래스의 경쟁사에 계속 도전하고 있습니다.

아시아태평양이 가장 큰 시장 점유율을 차지

- 아시아태평양은 현재 조사 대상 시장에서 가장 큰 시장 점유율을 차지하고 있습니다. 신흥국을 중심으로 한 이 지역의 제품에 대한 수요는 앞으로도 높은 수준에 이를 것으로 예상됩니다. 주요 기업은 주로 이 지역에 주력하고 젊은이를 대상으로 예상됩니다.

- 중국, 인도, 일본, 한국, 싱가포르 등 소비자 제품 기반 수요가 있는 인구 대국은 이들 국가에서의 제품 수요가 계속 시장을 견인하기 때문에 계속 대상 시장이 될 것으로 예상됩니다.

- 게다가 중국과 인도와 같은 국가에서는 전자상거래가 세계에서 성장하고 있으며 스마트 기기를 판매하는 온라인 유통 채널을 홍보할 것으로 예상됩니다. 예를 들어 IBEF에 따르면 인도의 전자상거래 시장은 2026년까지 2,000억 달러로 성장할 것으로 예상됩니다. 이 산업의 개발은 인터넷과 스마트폰의 보급률 증가가 원동력이 되고 있습니다.

- 최신 마케팅 동향은 기업이 음성 SEO를 구현하고 인바운드의 가능한 트래픽을 유치하는 것입니다. 예를 들어, 중국의 iFlytek은 98%의 정확도를 가진 음성 인식 시스템을 가지고 있습니다. 이 시스템은 영어에서 베이징어, 베이징어에서 영어, 한국어, 일본어, 22개의 다른 중국어 방언을 정확하게 번역합니다. 이 회사의 팀은 3년 이내에 99%의 정확성을 달성할 것으로 예측됩니다.

- 또한 이 지역의 주요 공급업체는 다양한 가격 부문 제품을 제공함으로써 가격에 민감한 소비자 그룹을 대상으로할 것으로 예상됩니다. 따라서 저렴한 가격으로 제품을 제공하는 공급업체에게는 기회가 됩니다. 비싼 제품을 가진 공급업체는 노트북 및 태블릿 단말기와 같은 다른 전자 제품과 협력하여 포장으로 제품을 제공함으로써 다른 고객층을 대상으로 할 수 있습니다.

차세대 검색 엔진 산업 개요

이 시장은 주로 기술 혁신을 중요한 성장 요인으로 격렬한 경쟁에 직면하고 있습니다. Amazon, Google, Apple 등 산업 리더를 중심으로 적당한 집중도를 유지하고 있습니다.

2023년 5월 Google은 AI를 통합한 검색엔진 결과 페이지 계획을 발표했습니다. 이 혁신적인 검색 엔진은 현재 테스트 단계에 있으며 AI가 생성한 주제 요약이 기존 검색 결과 위에 표시됩니다. 또한 사용자의 검색 의도에 따라 색상이 동적으로 조정되는 강조된 배경 섹션도 포함됩니다.

2022년 9월, Gen Z는 TikTok과 전략적 제휴를 맺고 새로운 검색 엔진을 도입했습니다. 이 제휴는 TikTok의 강력한 알고리즘을 활용하여 청소년 사용자의 취향에 효과적으로 맞춘 것입니다. 주목해야할 것은 이 검색 엔진은 익명의 웹사이트가 아니고, 플랫폼상의 실제 개인이 합성하고 제공하는 컨텐츠로 차별화를 도모하고 있는 점입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력 - Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

- COVID-19가 차세대 검색 엔진 시장에 미치는 영향

제5장 시장 역학

- 시장 역학의 채용

- 시장 성장 촉진요인

- 전문 서비스의 고객 경험 향상에 대한 집중도 증가

- 가장 높은 성장을 이루는 셀프서비스와 퍼스널 부문

- 시장 성장 억제요인

- 실시간 대화에 대한 선호도 증가

제6장 시장 세분화

- 유통 채널별

- 온라인

- 오프라인

- 최종 사용자별

- 개인

- 업무

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- Amazon.com Inc.

- Google LLC(Alphabet Inc.)

- Alibaba Group

- Sonos Inc.

- Harman-Kardon Inc./JBL

- Apple Inc.

- Bose Corporation

- Xiaomi Inc.

- Baidu Inc.

제8장 투자 분석

제9장 시장 기회와 앞으로의 동향

KTH 25.02.07The Next Generation Search Engines Market size is estimated at USD 42.93 billion in 2025, and is expected to reach USD 85.68 billion by 2030, at a CAGR of 14.82% during the forecast period (2025-2030).

Key Highlights

- The next-generation search engine provides an advanced information retrieval model for decision-makers and scientists who wish to gain working knowledge about the search to evaluate available solutions and dialogue with software and data providers. Over the last few years, the number of voice searches has increased exponentially. Also, it is becoming less of a novelty and more like a new standard. Therefore, the next-generation search engines are more oriented toward voice-based search engines.

- Next-generation search engines are also increasing because of deep neural networks, machine learning, and other advancements in AI technologies. Virtual assistants, such as smart speakers, are used for various applications across several end-user industries, such as retail, BFSI, and healthcare. One primary consumer-facing application is a personal assistant. It helps consumers accomplish multiple tasks. For instance, Apple's Siri offers an intuitive interface for connected homes or cars.

- Growing demand for Self-service options indicates rapid growth in consumer demand for more incredible speed and convenience. According to NICE's 2022 Digital First Customer Experience Report, 81% of consumers say they want more self-service options. Yet, only 15% of consumers expressed high satisfaction with the tools provided to them. This trend drives the demand for Next next-generation search engine market.

- Increasing focus on improving Customer Experience across professional services drives the market. Enhancing the customer experience can bring rich rewards. Across industries, satisfied customers spend more and stay more loyal over time. By showing empathy with customers and helping to fix their problems, companies like these can tap into a source of tremendous value, find new business opportunities, and shift their operating model over time.

- Increasing Preference for Live Person Interaction could restrain the market. According to a survey conducted by Liveperson Inc., 87% of consumers worldwide prefer that the companies provide the flexibility to connect interactions across voice and messaging. Such preferences also shift based on different situations and times of the day, demonstrating the importance of allowing consumers to engage on their terms, when, and where they want.

Next Generation Search Engines Market Trends

Self Service and Personal Segment to Witness the Highest Growth

- Smart speakers in personal end-user verticals are expected to hold the majority share. The characteristics expected from a smart speaker nowadays include playing music and controlling smart home devices consisting of voice assistants ready to answer every question.

- The technological enhancements in the development of consumer applications resulted in the integration of smart homes or connected homes. Smart homes' development pushed end users to adopt mobile internet and fast broadband connections across households in the market.

- Voice-activated speakers have become part of people's routines. They provide the ability to use the technology while multi-tasking, as people speak more quickly than they can type (speed), and the increasingly "human" interfaces. Personalized responses are one of the famous use cases of voice search, which Google has attained to a large extent, as Google can know and guess the next question the users will most likely ask. On the other hand, Alexa cannot understand the context to the same extent as Google. Alexa relies on custom-built skills and protocols, whereas Google Assistant can understand specific user requests and further personalize the response.

- Voice users turn to their assistants to accomplish many tasks along their buying journeys, such as product research, price comparison, and adding to cart. A study from Adobe announced the consumer's usage of voice throughout their shopping journeys. The top three activities included product search/research (47%), creating shopping lists (43%), and price comparison (32%).

- The most well-known smart speakers are the Amazon Echo and Google Nest range of products, but there are plenty of third-party speakers, like the Sonos One, which comes with both Alexa and Google Assistant built-in.

- The United States remains a key market for the personal segment, especially voice assistant adoption. According to eMarketer, The number of voice assistants has risen from 103 million to 123 million over the last five years. According to the latest Smart Audio Report from NPR, 24% of Americans aged 18 years or above own at least one smart speaker. The average owner has more than one. A majority of Americans own Alexa. Since Amazon first introduced the Echo, it has become popular in the United States, and it continues to challenge top competitors.

Asia-Pacific Occupies the Largest Market Share

- The Asia-Pacific region currently holds the largest market share for the market studied. The demand for the products in the region, which is primarily from emerging economies, is expected to remain high. The major players are expected to focus chiefly on this region, with the youth as the target audience.

- China, India, Japan, South Korea, Singapore, and other populous nations with consumer product-based demand are expected to remain the target market as product demand in these countries continues to drive the market.

- Moreover, the growth of e-commerce across the world in countries like China and India is anticipated to drive the online distribution channels for selling smart devices. For instance, according to IBEF, the Indian e-commerce market is expected to grow to USD 200 billion by 2026. The development of the industry is driven by increasing internet and smartphone penetration.

- The latest marketing trend is companies implementing voice SEO to attract possible inbound traffic. For instance, China's iFlytek has a speech recognition system with an accuracy rate of 98%. The system accurately translates English to Mandarin and Mandarin to English, Korean, Japanese, and 22 different Chinese dialects. Its team predicts that it will achieve 99% accuracy within three years.

- Also, the major vendors in this region are expected to target the price-sensitive consumer group by offering products in different price segments. Therefore, they create an opportunity for vendors who offer products at a low price. Vendors with expensive products may target a different customer segment by offering products as a package in collaboration with other electronic products, such as notebooks and tablets.

Next Generation Search Engines Industry Overview

The market faces intense competition, primarily driven by technological innovation as a pivotal growth factor. It maintains a moderate level of concentration, featuring industry leaders such as Amazon, Google, and Apple. Several noteworthy developments have recently taken place:

In May 2023, Google Inc. unveiled plans for an AI-integrated search engine results page. This innovative search engine is currently in its testing phase and promises AI-generated topic summaries that will appear above the conventional search results. Additionally, it will include a highlighted background section, with its color dynamically adjusting according to the user's search intent.

In September 2022, Gen Z entered into a strategic partnership with TikTok to introduce a new search engine. This collaboration leverages TikTok's powerful algorithm, effectively tailored to the preferences of younger users. Notably, this search engine differentiates itself by offering content synthesized and delivered by real individuals on the platform rather than anonymous websites.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Next Generation Search Engine Market

5 MARKET DYNAMICS

- 5.1 Introduction to Market Dynamics

- 5.2 Market Drivers

- 5.2.1 Increasing Focus to Improve Customer Experience Across Professional Services

- 5.2.2 Self Service and Personal Segment to Witness the Highest Growth

- 5.3 Market Restraints

- 5.3.1 Increasing Preference for Live Person Interaction

6 MARKET SEGMENTATION

- 6.1 By Distribution Channel

- 6.1.1 Online

- 6.1.2 Offline

- 6.2 By End-user

- 6.2.1 Personal

- 6.2.2 Commercial

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amazon.com Inc.

- 7.1.2 Google LLC (Alphabet Inc.)

- 7.1.3 Alibaba Group

- 7.1.4 Sonos Inc.

- 7.1.5 Harman-Kardon Inc. /JBL

- 7.1.6 Apple Inc.

- 7.1.7 Bose Corporation

- 7.1.8 Xiaomi Inc.

- 7.1.9 Baidu Inc.