|

시장보고서

상품코드

1851734

카메라 모듈 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Camera Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

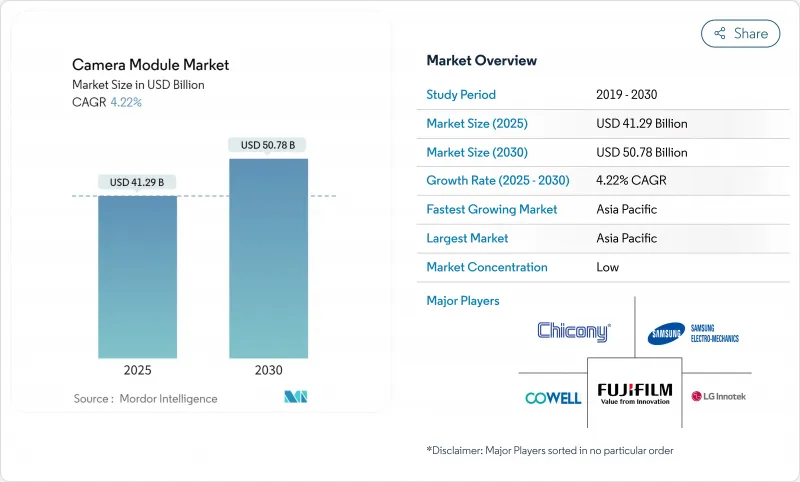

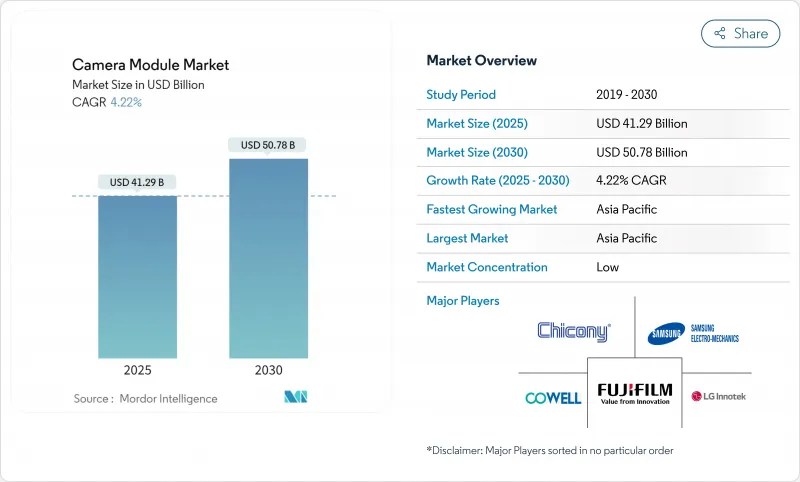

카메라 모듈 시장의 2025년 시장 규모는 412억 9,000만 달러로 평가되었고 2030년에는 507억 8,000만 달러에 이를 것으로 예측되며, 이 기간의 CAGR은 4.22%를 나타낼 전망입니다.

휴대폰 시장 포화로 제조업체들이 다중 카메라 어레이, 접이식 광학 줌, 기기 내 AI 처리 기술로 전환하면서 성장은 단순한 물량 확대에서 기능 중심의 혁신으로 전환되고 있습니다. 자동차 안전 규정, 엣지 분석 감시 시스템, 신흥 XR 기기 등이 전통적인 모바일 출하량을 넘어 수익원을 확대하고 있습니다. 2024년 대만 지진으로 음성 코일 모터(VCM) 조달의 취약점이 드러난 이후 부품 제조사들은 공급망 회복탄력성을 최우선 과제로 삼고 있으며, 인도 등 정부는 생산 연계 인센티브를 활용해 현지 조립을 촉진하고 신규 투자를 유치하고 있습니다. 한국, 일본, 중국 공급업체들이 언더디스플레이 카메라 및 페리스코프 모듈 같은 고부가가치 틈새 시장에서 지적 재산권 확보를 위해 경쟁하면서 경쟁 강도는 더욱 높아지고 있습니다.

세계의 카메라 모듈 시장 동향 및 인사이트

중국 플래그십 스마트폰, 3개 이상 렌즈 탑재하는 멀티 카메라 채택 확대

중국 핸드셋 브랜드들은 멀티 카메라 배열을 주류 사양으로 전환하며 2025년까지 평균 렌즈 수를 5개로 끌어올릴 전망입니다. 대형 센서, 전용 초광각 및 매크로 촬영기, 페리스코프 망원 모듈은 스마트폰을 주요 이미징 도구로 공고히 합니다. 컴퓨테이셔널 포토그래피와 결합된 이러한 배열은 포화 상태의 핸드셋 시장에서 기기 차별화를 가능케 하는 야간 모드, 인물 모드, 고배율 줌 기능을 구현합니다. 국내 공급망이 급속히 확장되며 기존 업체에 압박을 가하는 동시에, 카메라 모듈 시장은 브랜드 정체성과 소비자 업그레이드 의도를 결정하는 핵심 영역으로 부상했습니다. 화웨이의 200MP 잠망경 프로토타입은 광학 기술의 야망이 도약했음을 보여줍니다. AI 기반 컴퓨테이셔널 포토그래피는 작은 픽셀에서 더 넓은 다이나믹 레인지와 노이즈 제어를 이끌어내, 대형 센서 없이도 전문적인 수준의 화질을 마케팅할 수 있게 합니다.

후방 시야 및 ADAS 카메라 의무화(FMVSS 111, EU GSR)

미국과 유럽연합의 안전 규제로 인해 후방 카메라와 서라운드 뷰 카메라는 선택적 액세서리에서 필수 구성 요소로 변모했습니다. 자동차 제조사들은 사각지대 모니터링, 차선 유지 보조, 보행자 감지 요구사항을 충족하기 위해 다중 렌즈를 통합하며, 내구성과 내열성을 갖춘 모듈에 대한 지속적인 수요를 창출하고 있습니다. 미국 NCAP(National Highway Traffic Safety Administration)는 이제 사각지대 경고, 차선 유지 보조, 보행자 자동 긴급 제동 기능을 평가하여 차량당 기본 카메라 수를 높였습니다. 이에 자동차 제조사들은 규정 최소 기준을 초과하는 서라운드 뷰 시스템을 주문하며 센서 노드를 증설하고 카메라 모듈 시장을 촉진하고 있습니다.

2024년 대만 지진 후 VCM 액추에이터 공급 제약

2024년 지진으로 밀집된 VCM 생태계가 교란되며 전 세계 스마트폰 조립 라인에 파급된 공급 부족 사태가 발생했습니다. OEM 업체들은 이중 조달을 가속화하고 저전력 소비 및 빠른 응답 시간을 약속하는 압전 대체 기술을 모색했습니다. 부품 제조사들은 지리적 다각화에 착수하여 향후 재해 위험을 분산시키기 위해 동남아시아에 생산 능력을 구축했습니다. 이 사건은 프리미엄 카메라 출시 일정에 결정적 요소가 된 핵심 액추에이터 확보를 위해 한국과 중국의 주요 공급업체들 사이에서 수직 통합 전략을 촉진했습니다. 알프스 알파인은 조달 프리미엄으로 인한 이익 압박을 공개했으며, 이중 사이트 제조로 다각화하고 있습니다. 압전 대체재는 무소음, 저전력 구동과 틈새 시장인 코일 권선 업체에 대한 의존도 감소를 제공합니다.

부문 분석

VCM 액추에이터는 빠른 자동 포커스 및 광학식 손떨림 보정 기능을 뒷받침하여 사진 및 동영상 성능 차별화의 전략적 수단입니다. 핸드셋 브랜드들이 저조도 선명도와 영화 같은 모션 캡처를 강조함에 따라 해당 세그먼트의 7.2% CAGR은 전체 카메라 모듈 시장을 상회합니다. 지진으로 인한 공급 부족은 압전 및 MEMS 대체재 탐색을 촉진했으나, VCM은 여전히 비용 및 성숙도 우위를 유지합니다. 동시에 이미지 센서는 2024년 매출 점유율 48.8%를 기록했으며, 온센서 메모리를 통합한 적층 구조로 버스트 촬영 및 멀티프레임 HDR 기능을 구현했습니다. 후면 조명 기술 발전으로 노이즈 플로어가 감소하여 모바일 및 자동차 애플리케이션의 동적 범위가 확대되었습니다.

통합 트렌드는 VCM과 센서 내 위상차 감지 알고리즘을 연계하여 포커스 시스템이 하드웨어에서 소프트웨어 공생으로 전환되도록 합니다. 접힌 광학(folded-optics) 및 가변 조리개 설계가 확산되면서 렌즈 세트의 복잡성은 증가하고 있으며, 모듈 조립업체들은 마이크론 수준의 공차를 달성하기 위해 능동 정렬 로봇을 도입하고 있습니다. 이러한 변화는 스마트폰 성장세가 정체되는 가운데 카메라 모듈 시장이 단위당 고부가가치로 전환되는 추세를 강화합니다. 액추에이터 혁신과 센서-렌즈 공동 개발에 투자하는 공급업체들은 카메라 모듈 산업의 마진 곡선 상 프리미엄 영역에 포지셔닝하고 있습니다.

CMOS 기술은 출하량의 90.1%를 차지하며, 단일 칩 통합과 저전력 특성으로 CCD를 대체하고 있습니다. 후면 조명(BSI) 변형이 혁신을 주도하며 야간 모드 촬영과 자율주행 차량 비전을 위한 양자 효율을 높여 4.24%의 연평균 성장률(CAGR)로 확장 중입니다. 하이 다이내믹 레인지(HDR) CMOS 설계는 이제 측면 오버플로 커패시터를 활용하여 단일 노출로 극한의 휘도 범위를 포착함으로써 까다로운 자동차 안전 요구 사항을 충족합니다.

8-13MP 대역은 데이터 부하, 배터리 소모, 인지되는 이미지 선명도의 균형 덕분에 34.7%의 매출을 차지하며 업계의 주력 제품으로 남아 있습니다. 컴퓨테이셔널 포토그래피 기술은 파일 크기를 비례적으로 늘리지 않고 디테일을 업스케일하여 OEM이 더 큰 픽셀 수보다 소프트웨어 파이프라인을 우선시할 수 있게 합니다. 듀얼 게인 센서와 멀티프레임 퓨전은 중간 해상도 하드웨어에서 우수한 동적 범위를 추출하여 비용에 민감한 스마트폰과 IoT 비전 노드 전반에 걸쳐 이 세그먼트의 우위를 강화합니다.

반면 13MP 초과 해상도는 6.8% CAGR로 성장 중이며, 이는 세밀한 디테일이 필요한 플래그십 페리스코프 카메라, 의료 영상 프로브, 산업용 검사 시스템에 의해 주도됩니다. 쿼드-베이어 픽셀 비닝 기술은 이러한 고해상도 센서가 전력 예산을 지키면서 풀 해상도 주간 촬영과 저노이즈 야간 촬영 사이를 전환할 수 있게 합니다. 모듈 두께 제약이 지속되는 가운데, 마이크로 렌즈 설계와 딥 트렌치 절연 기술의 혁신은 양자 효율 유지에 기여하며, 카메라 모듈 시장 규모 확대를 프리미엄 등급에서 촉진하고 있습니다.

지역 분석

아시아태평양 지역은 2024년 전 세계 매출의 59.7%를 차지했으며, 이는 일본과 대만의 센서, 중국 본토의 렌즈 어셈블리, 베트남과 인도의 마무리 라인을 아우르는 밀집된 공급망에 힘입은 결과입니다. 인도 뉴델리의 생산 연계 인센티브 프로그램은 국내 모듈 조립에 대한 자본 지출을 환급하여 다국적 계약 제조업체들이 생산을 현지화하고 납기 시간을 단축하도록 유도합니다. 대만의 반도체 산업은 카메라 내 AI 코프로세서를 위한 최첨단 로직을 공급하여 해당 지역의 체계적 중요성을 강화합니다.

북미와 유럽은 프리미엄 핸드셋 수요와 엄격한 차량 안전 기준이 결합되어 고신뢰성 모듈에 대한 안정적인 수요를 뒷받침합니다. 미국 기반 XR 헤드셋 프로그램은 심도 감지 어레이에 대한 추가 수요를 창출하는 한편, 유럽연합의 EN 303645 사이버 보안 기준은 설계 주기를 연장하지만 강화되고 업그레이드 가능한 연결형 카메라를 생산합니다. 전기차 자율주행을 위한 보조금 제도는 카메라를 핵심 인식 입력 장치로 더욱 공고히 합니다.

중동 및 아프리카는 연평균 6.5% 성장률로 가장 빠르게 성장하는 지역으로, 걸프 지역의 스마트시티 구축이 교통 흐름 및 공공 안전 분석을 위한 엣지 AI 카메라를 도입하며 성장 동력이 되고 있습니다. 현지 통합업체들은 글로벌 하드웨어 벤더와 협력하여 FIPS 준수 감시망을 구축하며, 이로 인해 스토리지, 컴퓨팅, 네트워크 업그레이드에 대한 2차 수요가 촉진됩니다. 남미는 스마트폰 보급률이 상승하고 지역 자동차 안전 기준이 EU 및 미국 선례와 수렴함에 따라 장기적인 성장 잠재력을 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 및 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 중국 플래그십 스마트폰의 3개 이상 렌즈 탑재 확대

- 후방 시야 및 ADAS 카메라 의무화(FMVSS 111, EU GSR)

- 중동 스마트시티 프로젝트의 AI 기반 엣지 분석 감시 시스템 도입

- 잠망경/접이식 광학 기술 붐으로 인한 모듈당 렌즈 수 증가

- 인도 내 모듈 현지 조립을 촉진하는 생산연계인센티브(PLI) 제도

- 미국 및 한국의 XR 헤드셋용 3D/심도 센싱 수요

- 시장 성장 억제요인

- 2024년 대만 지진 이후 VCM 액추에이터 공급 제약

- 언더디스플레이 카메라 모듈의 웨이퍼 레벨 광학 수율 손실

- 적층형 CIS 아키텍처에 대한 특허 소송 증가

- EU 내 네트워크 모듈의 EN 303645 사이버 보안 규정 준수 지연

- 업계 생태계 분석

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 가격 분석

- 초소형 카메라 모듈의 다이나믹스

- 투자 분석(조립과 테스트 라인의 설비 투자)

제5장 시장 규모와 성장 예측

- 컴포넌트별

- 이미지 센서

- 렌즈 세트

- 카메라 모듈 조립

- 보이스 코일 모터(AF 및 OIS)

- 센서 유형별

- CMOS

- CCD

- 픽셀/해상도별

- 7MP 이하

- 8-13MP

- 13MP 이상

- 포커스 유형별

- 고정 포커스

- 오토 포커스

- 제조 공정별

- 칩 온보드(COB)

- 플립칩/웨이퍼 레벨 패키징

- 모듈 형식별

- 컴팩트/CCM

- MIPI 인터페이스 모듈(CSI/DSI)

- 용도별

- 모바일/스마트폰

- 소비자 가전(모바일 제외)

- 자동차

- 헬스케어와 의료 영상

- 보안 및 모니터링

- 산업 및 로봇 공학

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 동남아시아

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(M&A, JV, 설비투자)

- 시장 점유율 분석

- 기업 프로파일

- LG Innotek Co. Ltd

- Samsung Electro-Mechanics Co. Ltd

- Sunny Optical Technology(Gp) Co. Ltd

- O-Film Group Co. Ltd

- Hon Hai Precision/Foxconn(incl. Sharp)

- Chicony Electronics Co. Ltd

- LuxVisions Innovation Ltd(Lite-On)

- Cowell E Holdings Inc.

- Sony Group Corporation

- OmniVision Technologies Inc.

- STMicroelectronics NV

- AMS Osram AG

- ON Semiconductor Corp.

- Panasonic Corp.

- Largan Precision Co. Ltd

- MinebeaMitsumi(Mitsumi Electric)

- Canon Inc.

- Robert Bosch GmbH

- Continental AG

- Magna International Inc.

- Valeo SA

- e-con Systems Pvt Ltd

제7장 시장 기회와 장래의 전망

HBR 25.11.17The camera module market is valued at USD 41.29 billion in 2025 and is forecast to reach USD 50.78 billion by 2030, reflecting a 4.22% CAGR over the period.

Growth is shifting from pure volume expansion to feature-rich innovation, as handset saturation nudges manufacturers toward multi-camera arrays, folded-optics zoom, and on-device AI processing. Automotive safety mandates, edge-analytics surveillance, and emerging XR devices are broadening revenue streams beyond traditional mobile shipments. Component makers are prioritizing supply-chain resilience after the 2024 Taiwan earthquake exposed vulnerability in voice-coil motor (VCM) sourcing, while governments such as India are using production-linked incentives to localize assembly and attract fresh investment. Competitive intensity is rising as Korean, Japanese, and Chinese suppliers race to secure intellectual-property positions in high-value niches like under-display cameras and periscope modules.

Global Camera Module Market Trends and Insights

Multi-camera smartphone adoption exceeding three lenses in Chinese flagships

Chinese handset brands have turned multi-camera arrays into mainstream specifications, pushing the average lens count toward five by 2025. Larger sensor footprints, dedicated ultra-wide and macro shooters, and periscope telephoto modules reinforce smartphones as primary imaging tools. Combined with computational photography, these arrays enable night-mode, portrait, and high-zoom features that differentiate devices in a saturated handset field. Domestic supply chains scale rapidly, pressuring incumbents while elevating the camera module market as a critical arena for brand identity and consumer upgrade intent. Huawei's 200 MP periscope prototype illustrates the leap in optical ambition. AI-driven computational photography squeezes more dynamic range and noise control from small pixels, letting brands market professional-grade imagery without larger sensors.

Rear-visibility and ADAS camera mandates (FMVSS 111, EU GSR)

Safety regulations in the United States and European Union have transformed rear-view and surround-view cameras from optional accessories into compulsory components. Automakers integrate multiple lenses to satisfy blind-spot monitoring, lane-keeping, and pedestrian detection requirements, generating recurring demand for ruggedized, temperature-tolerant modules. The US NCAP now scores blind-spot warning, lane-keeping assist, and pedestrian automatic emergency braking, raising baseline camera count per vehicle. Automakers therefore order surround-view systems that exceed compliance minimums, multiplying sensor nodes and propelling the camera module market.

VCM actuator supply constraints post-2024 earthquake in Taiwan

he 2024 seismic event disrupted a tightly clustered VCM ecosystem, triggering shortages that rippled through smartphone assembly lines worldwide. OEMs accelerated dual-sourcing and pursued piezoelectric alternatives that promise lower power draw and faster response times. Component makers embarked on geographic diversification, erecting capacity in Southeast Asia to de-risk future disasters. The episode also fueled vertical-integration strategies among leading Korean and Chinese suppliers, as access to critical actuators became decisive for premium-camera launch schedule. Alps Alpine disclosed profit pressure from procurement premiums and is diversifying into dual-site manufacturing.Piezoelectric alternatives offer silent, low-power actuation and lower reliance on niche coil winders.

Other drivers and restraints analyzed in the detailed report include:

- AI-enabled edge-analytics surveillance roll-outs in Middle-East smart-city projects

- Periscope/folded-optics boom elevating lens count per module

- Wafer-level optics yield loss in under-display camera modules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

VCM actuators underpin rapid autofocus and optical image stabilization, making them strategic levers for differentiating photo and video performance. The segment's 7.2% CAGR surpasses the broader camera module market as handset brands spotlight low-light clarity and cinematic motion capture. Earthquake-induced shortages spurred exploration of piezoelectric and MEMS alternatives, yet VCMs retain cost and maturity advantages. Concurrently, image sensors held 48.8% revenue share in 2024, benefiting from stacked architectures that integrate on-sensor memory, enabling burst capture and multi-frame HDR. Advancements in back-side illumination have reduced noise floors, widening dynamic range for mobile and automotive applications.

Integration trends link VCMs with in-sensor phase-detection algorithms, allowing focus systems to swing from hardware to software symbiosis. Lens sets grow in complexity as folded-optics and variable-aperture designs proliferate, while module assemblers adopt active alignment robotics to hit micron-level tolerances. These changes reinforce the camera module market's shift toward higher value per unit even as smartphone growth plateaus. Suppliers investing in actuator innovation and sensor-lens co-development position themselves at the premium end of the camera module industry's margin curve.

CMOS technology owns 90.1% of shipments, its single-chip integration and low power making CCD largely obsolete. Back-side-illuminated (BSI) variants lead the innovation front, expanding at 4.24% CAGR as they boost quantum efficiency for night-mode photography and autonomous-vehicle vision. High-dynamic-range (HDR) CMOS designs now leverage lateral overflow capacitors to capture extreme luminance ranges in a single exposure, satisfying stringent automotive safety requirements.

Three-dimensional stacking pushes processing logic under the photodiode plane, trimming signal paths and opening doors to neuromorphic, event-based sensing that outputs only pixel-level changes. Such architectures reduce bandwidth and energy demand, critical for edge AI deployments. Continuous CMOS optimization ensures the camera module market remains driven by sensor advances that cascade into entire imaging subsystems.

The 8-13 MP band remains the industry's workhorse, controlling 34.7% revenue thanks to its balance of data load, battery drain, and perceived image clarity. Computational photography techniques upscale detail without proportionally larger files, letting OEMs prioritize software pipelines over larger pixel counts. Dual-gain sensors and multi-frame fusion extract superior dynamic range from mid-resolution hardware, reinforcing the segment's dominance across cost-sensitive smartphones and IoT vision nodes.

Conversely, resolutions above 13 MP are climbing at a 6.8% CAGR, driven by flagship periscope cameras, medical imaging probes, and industrial inspection systems that need granular detail. Quad-Bayer pixel-binning enables these high-res sensors to toggle between full-resolution daylight capture and low-noise night shots, guarding power budgets. As module thickness constraints persist, innovations in micro-lens design and deep-trench isolation help maintain quantum efficiency, anchoring the camera module market size gains in premium tiers.

The Camera Module Market Report is Segmented by Component (Image Sensor, Lens Set, and More), Sensor Type (CMOS, and CCD), Pixel/Resolution (Up To 7 MP, 8 - 13 MP, and More), Focus Type (Fixed-Focus, and Autofocus), Manufacturing Process (Chip-On-Board (COB), and More), Module Form-Factor (Compact/CCM, and More), Application (Mobile/Smartphones, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific controlled 59.7% of global revenue in 2024, propelled by dense supply chains spanning sensors in Japan and Taiwan, lens assemblies in mainland China, and finishing lines in Vietnam and India. New Delhi's Production Linked Incentive program reimburses capital expenditure for domestic module assembly, enticing multinational contract manufacturers to localize production and shorten delivery times. Taiwan's semiconductor depth supplies leading-edge logic for on-camera AI co-processors, reinforcing the region's systemic importance.

North America and Europe combine premium handset demand with stringent vehicle-safety standards, underpinning stable requirements for high-reliability modules. US-based XR headset programs add incremental pulls for depth-sensing arrays, while the European Union's EN 303645 cybersecurity baseline extends design cycles but yields hardened, upgradable connected cameras. Subsidy regimes for electric-vehicle autonomy further embed cameras as critical perception inputs.

Middle East & Africa, the fastest-growing region at 6.5% CAGR, banks on smart-city deployments in the Gulf that deploy edge AI cameras for traffic flow and public-safety analytics. Local integrators partner with global hardware vendors to roll out FIPS-compliant surveillance grids, catalyzing secondary demand for storage, compute, and network upgrades. South America offers longer-run upside as smartphone penetration rises and regional auto-safety standards converge with EU and US precedents.

- LG Innotek Co. Ltd

- Samsung Electro-Mechanics Co. Ltd

- Sunny Optical Technology (Gp) Co. Ltd

- O-Film Group Co. Ltd

- Hon Hai Precision/Foxconn (incl. Sharp)

- Chicony Electronics Co. Ltd

- LuxVisions Innovation Ltd (Lite-On)

- Cowell E Holdings Inc.

- Sony Group Corporation

- OmniVision Technologies Inc.

- STMicroelectronics N.V.

- AMS Osram AG

- ON Semiconductor Corp.

- Panasonic Corp.

- Largan Precision Co. Ltd

- MinebeaMitsumi (Mitsumi Electric)

- Canon Inc.

- Robert Bosch GmbH

- Continental AG

- Magna International Inc.

- Valeo SA

- e-con Systems Pvt Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Multi-camera Smartphone Adoption Exceeding 3 Lenses in Chinese Flagships

- 4.2.2 Rear-Visibility and ADAS Camera Mandates (FMVSS 111, EU GSR)

- 4.2.3 AI-Enabled Edge-Analytics Surveillance Roll-outs in Middle-East Smart-City Projects

- 4.2.4 Periscope/Folded-Optics Boom Elevating Lens Count per Module

- 4.2.5 PLI Scheme-Driven Local Assembly of Modules in India

- 4.2.6 3D/Depth Sensing Demand for XR Headsets in United States and Korea

- 4.3 Market Restraints

- 4.3.1 VCM Actuator Supply Constraints Post 2024 Earthquake in Taiwan

- 4.3.2 Wafer-Level Optics Yield Loss in Under-Display Camera Modules

- 4.3.3 Escalating Patent Litigation on Stacked CIS Architectures

- 4.3.4 EN 303645 Cyber-Security Compliance Delays for Networked Modules in EU

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Pricing Analysis

- 4.8 Ultra-miniature Camera Module Dynamics

- 4.9 Investment Analysis (CapEx in Assembly and Test Lines)

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Image Sensor

- 5.1.2 Lens Set

- 5.1.3 Camera Module Assembly

- 5.1.4 Voice-Coil Motor (AF and OIS)

- 5.2 By Sensor Type

- 5.2.1 CMOS

- 5.2.2 CCD

- 5.3 By Pixel/Resolution

- 5.3.1 Up to 7 MP

- 5.3.2 8 - 13 MP

- 5.3.3 Above 13 MP

- 5.4 By Focus Type

- 5.4.1 Fixed-Focus

- 5.4.2 Autofocus

- 5.5 By Manufacturing Process

- 5.5.1 Chip-on-Board (COB)

- 5.5.2 Flip-Chip/Wafer-Level Packaging

- 5.6 By Module Form-Factor

- 5.6.1 Compact/CCM

- 5.6.2 MIPI-Interface Modules (CSI/DSI)

- 5.7 By Application

- 5.7.1 Mobile/Smartphones

- 5.7.2 Consumer Electronics (ex-Mobile)

- 5.7.3 Automotive

- 5.7.4 Healthcare and Medical Imaging

- 5.7.5 Security and Surveillance

- 5.7.6 Industrial and Robotics

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 United Kingdom

- 5.8.2.3 France

- 5.8.2.4 Italy

- 5.8.2.5 Spain

- 5.8.2.6 Rest of Europe

- 5.8.3 Asia-Pacific

- 5.8.3.1 China

- 5.8.3.2 Japan

- 5.8.3.3 South Korea

- 5.8.3.4 India

- 5.8.3.5 South East Asia

- 5.8.3.6 Australia

- 5.8.3.7 Rest of Asia-Pacific

- 5.8.4 South America

- 5.8.4.1 Brazil

- 5.8.4.2 Rest of South America

- 5.8.5 Middle East and Africa

- 5.8.5.1 Middle East

- 5.8.5.1.1 United Arab Emirates

- 5.8.5.1.2 Saudi Arabia

- 5.8.5.1.3 Rest of Middle East

- 5.8.5.2 Africa

- 5.8.5.2.1 South Africa

- 5.8.5.2.2 Rest of Africa

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, CapEx)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 LG Innotek Co. Ltd

- 6.4.2 Samsung Electro-Mechanics Co. Ltd

- 6.4.3 Sunny Optical Technology (Gp) Co. Ltd

- 6.4.4 O-Film Group Co. Ltd

- 6.4.5 Hon Hai Precision/Foxconn (incl. Sharp)

- 6.4.6 Chicony Electronics Co. Ltd

- 6.4.7 LuxVisions Innovation Ltd (Lite-On)

- 6.4.8 Cowell E Holdings Inc.

- 6.4.9 Sony Group Corporation

- 6.4.10 OmniVision Technologies Inc.

- 6.4.11 STMicroelectronics N.V.

- 6.4.12 AMS Osram AG

- 6.4.13 ON Semiconductor Corp.

- 6.4.14 Panasonic Corp.

- 6.4.15 Largan Precision Co. Ltd

- 6.4.16 MinebeaMitsumi (Mitsumi Electric)

- 6.4.17 Canon Inc.

- 6.4.18 Robert Bosch GmbH

- 6.4.19 Continental AG

- 6.4.20 Magna International Inc.

- 6.4.21 Valeo SA

- 6.4.22 e-con Systems Pvt Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment