|

시장보고서

상품코드

1851842

항공기용 안테나 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Aircraft Antenna - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

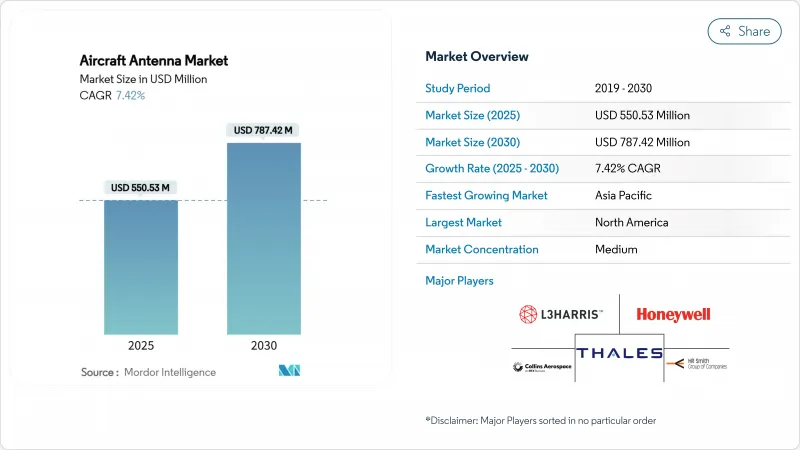

항공기용 안테나 시장 규모는 2025년에는 5억 5,053만 달러로, 2030년에는 7억 8,742만 달러에 이를 것으로 예상됩니다.

현재의 성장은 다중 궤도 연결에 대한 항공사의 헌신, 규제 당국이 주도하는 감시 시스템의 업그레이드, 시선외 작동을 위한 상시 연결 링크를 필요로 하는 무인 항공기 시스템 수요 증가에 기인하고 있습니다. 부문 리더는 현재 설계도 단계에서 디지털 비행 데크에 안테나를 설계하고 항공기 수명주기의 초기 단계에서 조달로 이동하고 있습니다. 이동통신사는 정지 궤도, 중간 궤도, 저궤도 및 새로운 5G 공대지 링크를 하나의 단말기에서 지원하는 장비를 선호하고 레거시 플릿 전체에서 교체를 촉진합니다. 갈륨과 특수 RF 기판에서 공급망의 혼란은 가격 설정에 영향을 미치고 있습니다. 이는 Tier One 공급업체 간의 수직 통합과 저중량 컨포멀 어레이의 Additive Manufacturing 채택을 촉진합니다.

세계의 항공기용 안테나 시장 동향과 인사이트

세계 항공기 납품 수 증가

보잉의 2024년 전망에서는 20년간 4만 3,975대의 신형 항공기 수요가 기록되었으며, 조종석과 승객의 연결에 중량 최적화 안테나를 사용하는 단통로 제트기가 대부분을 차지했습니다. 항공사는 초기 설계 재검토에서 멀티밴드, 소프트웨어 정의 어레이를 채택하는 경향이 있는데, 이는 안테나 선택이 후행이 아닌 30년에 걸친 전략적 결정으로 간주되기 때문입니다. 이러한 설계에서 완성까지의 전환은 공급업체에게는 수익 인식을 앞당기게 되고, 애프터마켓에서는 개수 사이클을 단축하게 됩니다. 연간 4.8%의 교통량 증가에 견인되는 아시아태평양의 높은 여객수 증가 예측은 퍼스트 피트 안테나의 수량과 정기적인 예비 수요에 직접 반영됩니다. 생산되는 각 기체의 베이스라인 주문을 확보해, 내용 연수 중반에 걸린 기체의 교환 요구를 가속시킴으로써, 임박한 납품 규모가 항공기용 안테나 시장을 밀어 올립니다.

차세대 위성 통신 및 5G 공중 연결 배포

다궤도 위성 별자리와 지상 5G 공대지 네트워크가 융합되어 안테나 벤더는 이종 스펙트럼을 원활하게 로밍하는 전자 제어 스티어러블 시스템의 개발을 강요받고 있습니다. 중국 텔레콤과 파트너 OEM은 타워와 LEO 링크 간의 네트워크 핸드오프를 입증하여 기존 GEO 전용 구성보다 높은 처리량과 낮은 지연을 입증했습니다. ViaSat-3의 출시와 2024년 최초의 상용 서비스 시작은 민첩한 평면 패널 개구부와 결합하여 GEO 공예가 여전히 제공할 수 있는 대역폭의 도약을 강조하고 있습니다. 항공사는 다중 궤도의 민첩성을 커버리지 갭에 대한 보험 및 실시간 분석의 기반으로 보고 있으며 안테나 업그레이드를 디지털 변혁 전략의 핵심으로 삼고 있습니다. 적극적인 롤아웃은 객실 및 운영 데이터 파이프의 프리미엄 서비스 수익을 이끌어 예측 CAGR에 2.1% 포인트를 추가합니다.

복합재 기체에서의 안테나·레이돔 통합의 복잡성

알루미늄에서 탄소섬유로의 기체 이동은 전도성 메쉬 층이 새로운 감쇠 경로를 도입하기 때문에 RF 전파를 복잡하게 만듭니다. ACASIAS 컨소시엄은 Ku 밴드 어레이를 1.2m x 3m 패널에 직접 통합하여 실현 가능성을 입증했지만 인증 및 결합 검증 단계에 시간이 걸린다고 강조했습니다. 구조적 무결성은 방사 효율과 쌍을 이루어야 하지만, 이를 위해서는 비용이 많이 드는 전자기 시뮬레이션, 프로토타입 쿠폰 및 파괴 시험이 필요합니다. 광대역 안테나 어댑터 플레이트의 부식에 관한 최근의 FAA 지침은 새로운 복합재는 물론, 금속 기체조차도 신뢰성 장애물이 계속되고 있음을 보여줍니다. 이러한 엔지니어링의 부담은 시장 투입까지의 시간을 늘리고, 사내에 재료 연구소가 없는 소규모공급자를 주저하기 때문에 인증된 설계 툴 체인이 성숙할 때까지 CAGR은 1.4% 감산됩니다.

부문 분석

민간 항공사는 표준화된 인증 패스웨이와 내로우 바디 제트의 대량 도입으로 2024년에는 항공기용 안테나 시장의 39.45%를 나타냈습니다. 항공사는 Wi-Fi 포털과 실시간 텔레메트리를 추가하는 객실 개조와 병행하여 멀티 궤도 및 5G 대응 안테나를 조달하여 예측 가능한 교환 사이클을 보장합니다. 비즈니스 항공 및 일반 항공 바이어는 전세 항공편 고객이 일관된 연결성을 요구하기 때문에 항공사 등급 광대역 회선으로 이동하기 시작했지만 캐빈 풋 프린트가 작기 때문에 다중 안테나 아키텍처에는 여전히 한계가 있습니다. 군용항공은 암호화, 안티잼, 전자전 사양 때문에 납품수는 적지만 높은 마진을 얻고 있습니다. F-16 Viper Shield 업그레이드와 같은 프로그램은 통합 광대역 조리개의 가치를 보여줍니다.

무인 항공기는 가장 급성장하는 분야이며 CAGR 9.09%를 나타낼 전망입니다. 과거에는 드론을 육안으로 볼 수 있는 범위로 제한하고 있던 규제도, 현재는 보다 긴 항로를 가능하게 하고, 짐 물류, 파이프라인 검사, 정밀 농업 등을 가능하게 하고 있습니다. NASA가 현장 시험한 경량 에어로겔 안테나는 Ka 밴드 링크를 유지하면서 시스템 질량을 줄여 전동 멀티콥터의 엄격한 크기, 무게, 전력 목표를 달성했습니다. 방어 분야의 구매자는 또한 협력 비행을 위한 위상 정렬 네트워크에 의존하는 군유 플랫폼의 규모를 확대하고 있습니다. 이러한 크로스오버를 통해 생산자는 소비자용 및 군용 채널에 걸쳐 R&D를 상각할 수 있으며, UAV의 기세는 항공기용 안테나 시장의 지속적인 성장 레버로 정착합니다.

ADS-B, 교통 충돌 회피 시스템, 우주 기반 레이더는 위치 데이터를 수집하기 위해 전용 개구부에 의존하기 때문에 모니터링 및 정찰은 2024년 수익의 41.25%를 차지했습니다. 상업용 및 비즈니스용 항공기에는 탑재가 의무화되어 있어 매년 안정된 교환이 이루어져 국경 경비기관에서는 고게인의 합성 개구 레이더 포드의 주문이 늘어납니다. 승객의 광대역 이용이 급증하고 항공사가 비즈니스 메시징을 IP 링크로 전환하고 있기 때문에 통신 용도는 후진을 받고 있습니다. 내비게이션 안테나는 스푸핑과 재밍에 대한 내성을 향상시키는 다중 별자리 업그레이드로 안정적인 수요를 누리고 있습니다.

전자전은 CAGR 8.43%로 가장 높은 상승률을 보이고 있습니다. 기존 전투기의 블록 업그레이드에는 활성 보호 제품군을 위한 송수신 요소가 내장된 모듈형 안테나 장치가 필요합니다. 전자전 항공기용 안테나 시장 규모는 프로그램이 실시간 빔포밍이 가능한 디지털 어레이로 이동하여 검색, 추적, 방해 기능을 동시에 실현할 수 있게 됨에 따라 상승합니다. 또한 민간 플랫폼은 진화하는 안보 지침을 준수하기 위해 위협 모니터링 하드웨어를 통합하여 상업 및 방어 지출 흐름을 융합합니다. 이러한 동향은 지역 제트기의 레이돔에서 드론의 철탑에 이르기까지 확장 가능한 공통 코어 칩셋의 구축을 공급자에게 촉구하여 비용 효율성을 높이고 있습니다.

지역 분석

북미는 보잉의 라인 핏 프로그램과 국방부의 지속적인 지출로 생산 라인이 바빠지고 2024년 세계 매출의 35.65%를 차지했습니다. 이 지역의 항공사는 지구 저궤도 콘스텔레이션의 조기 채용을 주도해, 여객 Wi-Fi와 비행 크리티컬 통신용으로 인정된 위상 어레이 패널을 지역 제트에 장비하기 시작했습니다. 유나이티드 항공은 300대 이상의 항공기에 스타링크 단말기를 개설할 계획으로 기술 혁신을 빠르게 진행할 의욕을 강조하고 있습니다. C5ISR 하드웨어를 위한 5억 6,800만 달러의 Viasat 프레임워크를 포함한 정부 계약은 볼륨을 추가하고 차세대 조리개 개념을 검증합니다. 캐나다에서는 우주 기반의 ADS-B가 의무화되어 비즈니스나 헬리콥터의 플릿 전체에 다이버시티 안테나가 설치되게 되어, 교체 수요가 높아집니다.

아시아태평양은 항공기의 구조적 성장과 기술적 야망 증가를 반영하여 CAGR 8.12%로 가장 빠르게 성장할 것으로 예측됩니다. 중국은 2043년까지 항공기 보유수를 2배 이상의 9,740대로 늘릴 것으로 예측되고 있으며, 조종석, 캐빈, 드론용 안테나에 수십억 달러의 파이프라인이 전망됩니다. 지역 공급업체는 국내 5G의 진보를 활용하여 타워와 위성의 하이브리드 아키텍처로 직접 도약하여 제품 사이클을 압축합니다. 2026년까지 애드혹 공중 통신 기지국을 시작하는 일본의 목표는 기존 위성을 넘어서는 공중 네트워크 계층에 대한 정책적 지지를 보여줍니다. 인도와 동남아시아도 급증하는 중산계급 여행에 대응하기 위해 새로운 내로우 바디 기체를 주문하고 있으며 표준화된 연결 키트 수요 기반을 확대하고 있습니다.

유럽은 에어버스 생산을 통해 대규모 설치 기반을 유지하고 있지만, 성장은 지속가능성과 도시 이동성으로 축족을 옮기고 있습니다. 탄소에 대한 영향에 관한 규제의 뒷받침도 있어, 공기 저항을 줄이는 경량의 플래시 마운트 안테나의 채용이 진행되고 있습니다. 유럽 위성 서비스 제공업체 컨소시엄은 우주 기반 교통 모니터링을 향해 움직이고 있으며, 궤도 및 지상 링크의 다양성 요구를 충족시키기 위해 새로운 2주파 어레이가 필요합니다. Lilium이 eVTOL 프로그램에서 단일 공급업체 전략을 선택한 것은 유럽이 통합 안테나 스킨에 중점을 두고 있음을 보여줍니다. 중동 및 아프리카는 현재는 아직 규모가 작지만 광대역 대응 여객 경험에 의존하는 주요 허브 공항의 확장을 받아들이고 있으며, 인프라의 성숙에 따라 안테나의 이용이 증가하는 입장에 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계 항공기 납품 수 증가

- 차세대 SATCOM과 5G 공중 접속의 전개

- 플릿 전체의 ADS-B/Mode-S 트랜스폰더 의무화

- BVLOS 미션 프로파일에 대한 UAV 수요의 급증

- eVTOL 플랫폼용 초경량 컨포멀 안테나

- SWaP를 저하시키는 적층 조형 프린트 안테나

- 시장 성장 억제요인

- 복합재 기체에 있어서 안테나와 레이돔의 통합의 복잡성

- L 밴드와 C 밴드의 스펙트럼 혼잡

- 항공우주 하드웨어의 긴 인증 사이클

- 특수 RF 재료공급 체인 부족

- 밸류체인 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 최종 사용자별

- 상업 항공

- 군용 항공

- 비즈니스 및 일반 항공

- 무인 항공기(UAV)

- 용도별

- 통신

- 내비게이션

- 감시 및 정찰

- 전자전

- 승객 연결성/기내 엔터테인먼트(IFE)

- 안테나 유형별

- VHF/UHF 통신

- 위성통신(SATCOM)

- 내비게이션(VOR/ILS/MB)

- 트랜스폰더 및 ADS-B

- GNSS/GPS 안테나

- 다중대역 컨포멀 안테나

- 5G 항공용

- 주파수 대역별

- HF

- VHF

- UHF

- L 밴드

- C 밴드

- X 밴드

- Ku/Ka 밴드

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- L3Harris Technologies, Inc.

- Honeywell International Inc.

- Collins Aerospace(RTX Corporation)

- CMC Electronics Inc.

- Thales Group

- RAMI(RA Miller Industries, Inc.)

- PIDSO GmbH(Riedel Communications GmbH)

- Hexagon AB

- Tallysman Wireless(Calian Ltd.)

- General Dynamics Mission Systems(General Dynamics Corporation)

- Viasat, Inc.

- HR Smith Group of Companies

- AeroVironment, Inc.

제7장 시장 기회와 향후 전망

KTH 25.11.17The aircraft antenna market size is valued at USD 550.53 million in 2025 and is forecasted to reach a USD 787.42 million aircraft antenna market size by 2030, advancing at a 7.42% CAGR.

Current growth stems from airline commitments to multi-orbit connectivity, regulator-driven surveillance upgrades, and rising unmanned aerial system demand that requires always-on links for beyond-visual-line-of-sight operations. Segment leaders now design antennas into digital flight decks at the blueprint stage, shifting procurement earlier in the aircraft life cycle. Operators prioritize equipment supporting geostationary, medium, low Earth orbit, and emerging 5G air-to-ground links in a single terminal, creating a replacement pull across legacy fleets. Supply-chain disruption in gallium and specialty RF substrates continues to influence pricing. It encourages vertical integration among tier-one suppliers and additive-manufacturing adoption for low-weight conformal arrays.

Global Aircraft Antenna Market Trends and Insights

Increasing Global Aircraft Deliveries

Boeing's 2024 outlook sets demand for 43,975 new airplanes over two decades, dominated by single-aisle jets that rely on weight-optimized antennas for cockpit and passenger connectivity. During initial design reviews, airlines are locking in multi-band, software-defined arrays because antenna choices are now seen as a thirty-year strategic decision rather than an afterthought. This design-finish migration pulls revenue recognition forward for suppliers and compresses retrofit cycles in the aftermarket. High passenger growth forecasts in Asia-Pacific, led by 4.8% annual traffic gains, translate directly into first-fit antenna volume and recurring spares demand. The scale of impending deliveries lifts the aircraft antenna market by securing baseline orders for each airframe produced and by accelerating replacement needs for fleets approaching midlife.

Next-gen SATCOM and 5G Airborne-Connectivity Roll-outs

Multi-orbit satellite constellations and terrestrial 5G air-to-ground networks converge, forcing antenna vendors to develop electronically steerable systems that roam seamlessly across disparate spectra. China Telecom and partner OEMs demonstrated network hand-off between tower and LEO links, proving higher throughput and lower latency than legacy GEO-only configurations; this benchmark is pushing North American carriers to field dual-mode arrays within the next fleet retrofit window. The ViaSat-3 launch and the first commercial service activation in 2024 underscore the bandwidth leap GEO craft can still deliver when paired with agile flat-panel apertures. Airlines view multi-orbit agility as an insurance policy against coverage gaps and a foundation for real-time analytics, making antenna upgrades core to digital transformation strategies. Aggressive roll-outs add 2.1 percentage points to forecast CAGR by unlocking premium service revenues across passenger cabins and operational data pipes.

Antenna-radome Integration Complexity in Composite Airframes

The shift from aluminum to carbon-fiber fuselages complicates RF propagation because conductive mesh layers introduce new attenuation paths. The ACASIAS consortium embedded Ku-band arrays directly into a 1.2 m X 3 m panel, proving feasibility yet highlighting lengthy qualification and bonding verification steps. Structural integrity must pair with radiation efficiency, which can demand costly electromagnetic simulations, prototype coupons, and destructive testing. Recent FAA directives on broadband antenna adapter plate corrosion illustrate continuing reliability hurdles even for metal airframes, let alone novel composites. These engineering burdens extend time-to-market and deter smaller suppliers without in-house materials labs, subtracting 1.4 percentage points from potential CAGR until certified design toolchains mature.

Other drivers and restraints analyzed in the detailed report include:

- Fleet-wide ADS-B/Mode-S Transponder Mandates

- Surging UAV Demand for BVLOS Mission Profiles

- Spectrum Congestion in L- and C-bands

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial aviation held 39.45% of the aircraft antenna market in 2024, thanks to standardized certification pathways and the sheer quantity of narrow-body jets entering fleets. Airlines procure multi-orbit and 5G-ready antennas parallel with cabin refits that add Wi-Fi portals and real-time telemetry, assuring predictable replacement cycles. Business and general aviation buyers have begun migrating toward airline-grade broadband links as charter clients demand consistent connectivity, but smaller cabin footprints still limit multi-antenna architectures. Military aviation delivers fewer units yet commands higher margins because of encryption, anti-jam, and electronic warfare specifications; programs like the F-16 Viper Shield upgrade illustrate the value of integrated broadband apertures.

Unmanned aerial vehicles represent the fastest-growing slice, advancing at a 9.09% CAGR. Regulations that once confined drones to visual line-of-sight now allow longer routes, enabling package logistics, pipeline inspection, and precision agriculture. Lightweight aerogel antennas field-tested by NASA cut system mass while sustaining Ka-band links, meeting the strict size, weight, and power targets for electric multicopters. Defense buyers also scale swarming platforms that rely on phase-aligned networks for cooperative flight. This crossover lets producers amortize R&D across civil and military channels, anchoring UAV momentum as a durable growth lever for the aircraft antenna market.

Surveillance and reconnaissance made up 41.25% of revenues in 2024 because ADS-B, traffic collision avoidance systems, and space-based radar rely on dedicated apertures to collect positional data. Mandatory carriage across commercial and business fleets ensures stable annual replacements, while border-security agencies add orders for high-gain synthetic aperture radar pods. Communication applications sit close behind as passenger broadband usage spikes and airlines shift operational messaging to IP links. Navigation antennas enjoy consistent demand through multi-constellation upgrades that improve resilience to spoofing and jamming.

Electronic warfare shows the highest upside at an 8.43% CAGR. Block upgrades to existing fighters require modular antenna units that house transmitter and receiver elements for active protection suites. The aircraft antenna market size for electronic warfare rises as programs migrate toward digital arrays capable of real-time beamforming, enabling simultaneous search, track, and jam functions. Civil platforms also integrate threat-monitoring hardware to comply with evolving security directives, blending commercial and defense spending streams. These trends induce suppliers to build common core chipsets that can be scaled from regional jet radomes to drone pylons, gaining cost efficiency.

The Aircraft Antenna Market Report is Segmented by End User (Commercial Aviation, Military Aviation, Business and General Aviation, and More), Application (Communication, Navigation, and More), Antenna Type (SATCOM, VHF/UHF Communication, Transponder and ADS-B, and More), Frequency Band (HF, VHF, X-Band, Ku/Ka-band, and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 35.65% of global revenue in 2024 as Boeing line-fit programs and sustained Pentagon outlays kept production lines busy. Airlines in the region have led the early adoption of low Earth orbit constellations and have begun equipping regional jets with phased-array panels certified for passenger Wi-Fi and flight-critical communications. United Airlines' plan to retrofit more than 300 aircraft with Starlink terminals underscores a willingness to fast-track innovation. Government contracts, including a USD 568 million Viasat framework for C5ISR hardware, add volume and validate next-generation aperture concepts. Canadian mandates for space-based ADS-B further boost diversity antenna installations across business and helicopter fleets, anchoring replacement sales.

Asia-Pacific is projected to grow the fastest at an 8.12% CAGR, reflecting structural fleet growth and escalating technology ambitions. China is forecasted to more than double its active aircraft to 9,740 by 2043, translating to a multibillion-dollar pipeline for cockpit, cabin, and drone antennas. Regional suppliers leverage domestic 5G advances to leapfrog directly to hybrid tower-satellite architectures, compressing the product cycle. Japan's target of launching ad-hoc airborne telecommunications base stations by 2026 shows policy support for aerial network layers beyond traditional satellite. India and Southeast Asia also order new narrow-body fleets to serve fast-rising middle-class travel, extending the demand base for standardized connectivity kits.

Europe retains a large installed base through Airbus production, but growth pivots toward sustainability and urban mobility. Regulatory pushes on carbon impact drive the adoption of lighter, flush-mounted antennas that reduce drag. The European Satellite Services Provider consortium's move toward space-based traffic surveillance requires new dual-frequency arrays to satisfy orbital and terrestrial link diversity needs. Lilium's selection of a single-supplier strategy for its eVTOL program magnifies European focus on integrated antenna skins. Middle East and Africa remain smaller today, yet host major hub expansions that rely on broadband-enabled passenger experience, positioned to increase antenna uptake as infrastructure matures.

- L3Harris Technologies, Inc.

- Honeywell International Inc.

- Collins Aerospace (RTX Corporation)

- CMC Electronics Inc.

- Thales Group

- RAMI (R.A. Miller Industries, Inc.)

- PIDSO GmbH (Riedel Communications GmbH)

- Hexagon AB

- Tallysman Wireless (Calian Ltd.)

- General Dynamics Mission Systems (General Dynamics Corporation)

- Viasat, Inc.

- HR Smith Group of Companies

- AeroVironment, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing global aircraft deliveries

- 4.2.2 Next-gen SATCOM and 5G airborne-connectivity roll-outs

- 4.2.3 Fleet-wide ADS-B/Mode-S transponder mandates

- 4.2.4 Surging UAV demand for BVLOS mission profiles

- 4.2.5 Ultra-light conformal antennas for eVTOL platforms

- 4.2.6 Additive-manufactured printed antennas lowering SWaP

- 4.3 Market Restraints

- 4.3.1 Antenna-radome integration complexity in composite airframes

- 4.3.2 Spectrum-congestion in L- and C-bands

- 4.3.3 Long qualification cycles for aerospace hardware

- 4.3.4 Supply-chain shortages of specialty RF materials

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By End User

- 5.1.1 Commercial Aviation

- 5.1.2 Military Aviation

- 5.1.3 Business and General Aviation

- 5.1.4 Unmanned Aerial Vehicles (UAVs)

- 5.2 By Application

- 5.2.1 Communication

- 5.2.2 Navigation

- 5.2.3 Surveillance and Reconnaissance

- 5.2.4 Electronic Warfare

- 5.2.5 Passenger Connectivity/IFE

- 5.3 By Antenna Type

- 5.3.1 VHF/UHF Communication

- 5.3.2 SATCOM

- 5.3.3 Navigation (VOR/ILS/MB)

- 5.3.4 Transponder and ADS-B

- 5.3.5 GNSS/GPS Antennas

- 5.3.6 Multiband Conformal

- 5.3.7 5G Airborne

- 5.4 By Frequency Band

- 5.4.1 HF

- 5.4.2 VHF

- 5.4.3 UHF

- 5.4.4 L-band

- 5.4.5 C-band

- 5.4.6 X-band

- 5.4.7 Ku/Ka-band

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Russia

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 UAE

- 5.5.5.1.3 Qatar

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 L3Harris Technologies, Inc.

- 6.4.2 Honeywell International Inc.

- 6.4.3 Collins Aerospace (RTX Corporation)

- 6.4.4 CMC Electronics Inc.

- 6.4.5 Thales Group

- 6.4.6 RAMI (R.A. Miller Industries, Inc.)

- 6.4.7 PIDSO GmbH (Riedel Communications GmbH)

- 6.4.8 Hexagon AB

- 6.4.9 Tallysman Wireless (Calian Ltd.)

- 6.4.10 General Dynamics Mission Systems (General Dynamics Corporation)

- 6.4.11 Viasat, Inc.

- 6.4.12 HR Smith Group of Companies

- 6.4.13 AeroVironment, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment