|

시장보고서

상품코드

1851184

수술대 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Surgical Tables - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

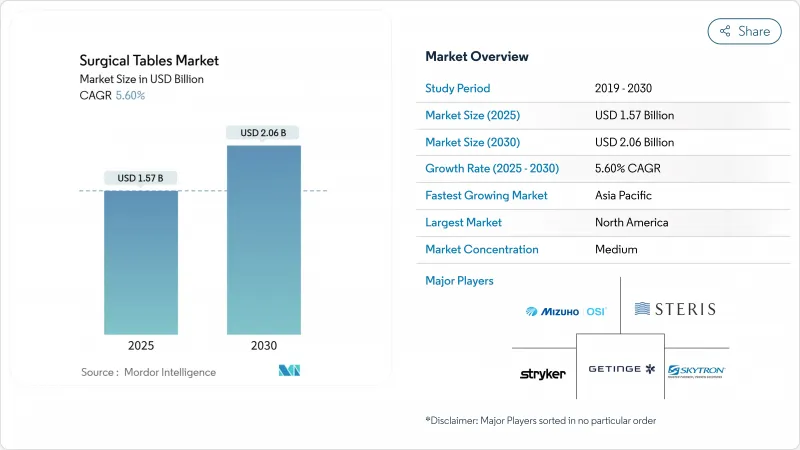

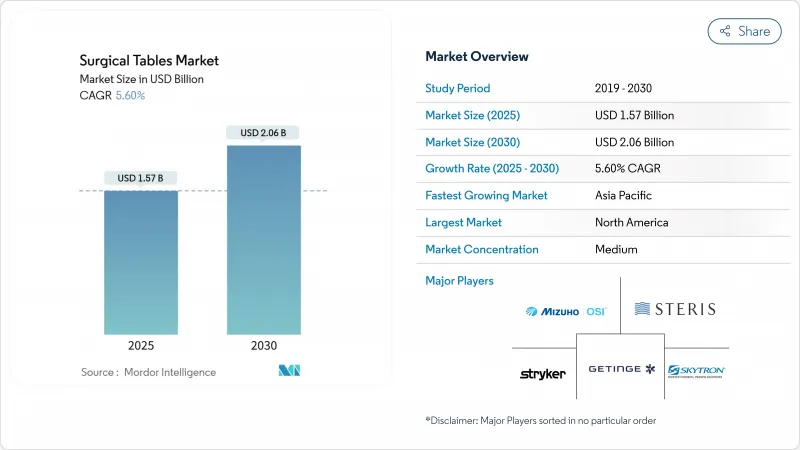

세계의 수술대 시장은 2025년 15억 7,000만 달러, 2030년까지 20억 6,000만 달러에 이르고, CAGR 5.6%로 성장할 전망입니다.

인구동태의 고령화에 의해 정형외과와 심혈관 수술의 증례 수가 증가하고, 외래환자의 치료가 외래수술센터(ASC)로 이행하고, 로봇 대응 수술실(OR)이 환자 위치결정 플랫폼의 기술 수준을 끌어올리고 있습니다. 병원은 실시간 이미징을 지원하기 위해 탄소섬유 방사선 투과성 상판으로 업그레이드하고 있지만, 서유럽의 지속가능성 의무화는 에너지 효율적인 모듈 설계를 평가했습니다. 경쟁 전략은 공급자가 조달과 통합을 간소화할 수 있도록 수술대를 이미지 처리, 조명, 로봇에 연결하는 번들 OR 에코시스템을 중심으로 전개되어 왔습니다. 프리미엄 부문 제조업체는 중견 병원의 자본 예산 제약을 완화하는 서비스 및 대출 프로그램을 시작하고 있습니다.

세계 수술대 시장 동향과 통찰

수술 건수 증가와 ASC 확대

미국의 외과 수술의 대부분은 외래에서 이루어지고 있으며, 정형외과 및 소화기 수술의 복잡한 사례는 병원 외래 부문보다 45-60% 낮은 비용으로 운영되며 평균 대기 시간이 20% 단축되기 때문에 계속 주목을 받고 있습니다. ASC가 성장함에 따라 공급업체는 발자국을 줄이고 사례간에 빠르게 회전하는 컴팩트한 다기능 테이블을 제공하게 되었습니다. 자본 지출을 줄이기 위해 제조업체는 현재 특수 상판에 해당하는 모듈식 기반을 판매하고 있으며 센터는 환자 수가 정당화 될 때까지 업그레이드를 연기할 수 있습니다. 그룹 구매 계약 및 장비 서비스로서의 자금 조달은 도입 장벽을 더욱 낮추고 있습니다.

고령화로 정형외과 및 심장 외과의 증례 수가 증가

인구의 고령화는 관절 재건, 골절 수리 및 정확한 위치 결정과 비만 체중 제한을 필요로 하는 인터벤셔널 심장 수술에 대한 수요를 높이고 있습니다. 미국의 정형외과 수술 건수는 연간 660만 건에 달할 것으로 예측되고 있으며, 고하중 리프트와 압박 상해 경감 센서의 필요성이 높아지고 있습니다. XSENSOR의 ForeSite OR과 같은 일체형 압력 매핑을 갖춘 비만 대응 테이블은 수술 환자의 최대 45%에 영향을 미치는 병원 내 압력 부상을 완화합니다.

중견 병원에서 프리미엄 가격과 설비투자 동결

운영 비용 상승과 인플레이션으로 소규모 병원은 장비 구매를 지연시키고 재생 장비와 다년간 임대를 선택합니다. 인공관절 전치환술의 증례 수가 증가하고 있음에도 불구하고, 메디케어로부터의 상환금이 감소하고 있기 때문에 마진이 압박되어, 하이엔드 영상 대응 테이블의 정당화가 어려워지고 있습니다. 공급업체는 시설에 베이스를 설치하고 나중에 연결 키트를 추가할 수 있는 단계적 업그레이드 경로와 유지보수, 재제조 컴플라이언스, 소프트웨어 업데이트를 번들한 서비스 계약 등으로 대응하고 있습니다.

부문 분석

2024년 수술대 시장 점유율은 일반 수술이 35.78%를 차지했습니다. 병원은 아침에 맹장, 오후에는 비만 사례에 해당하는 다목적 퀵 스위치 플랫폼을 선호합니다. 이 부문의 광범위한 절차 구성은 교체를 위한 스케일 이점을 지원하며, 워크플로우는 탈착식 암 보드 및 결석 제거 레그 지지대와 같은 표준화된 액세서리와 일치합니다. 한편, 로봇에 의한 담낭 적출술의 도입으로 많은 의료 제공업체들은 수동 유압식 베이스에서 속도와 일관성을 위해 풋스위치 메모리 프로파일을 특징으로 하는 전동 칼럼 시스템으로 대체를 진행하고 있습니다.

정형외과 및 외상 수술은 2030년까지 연평균 복합 성장률(CAGR)이 6.78%가 되어, 이 시장에서 가장 빠를 것으로 보입니다. Zimmer Biomet의 TMINI Miniature Robotic System과 같은 무릎과 고관절 로봇은 밀링 과정에서 mm 이하의 정확도를 유지하는 강성이 높은 저진동 표면에 의존합니다. 테이블 제조업체는 대퇴골 원위부를 재포지셔닝 없이 노출시켜 마취 시간과 X선 피폭을 단축하는 종방향 슬라이드와 틸트 레인지로 대응하고 있습니다. 뇌신경 수술과 심장혈관 전문 분야에서는 점유율이 작지만 카본 탑, 360 ° C 암 클리어런스, 내비게이션 시스템과 통합되는 머리 고정 인터페이스를 요구하기 때문에 가격이 비쌉니다. 병원이 분야를 횡단하는 하이브리드 룸을 추구함에 따라 수요는 동일한 섀시에서 척추, 혈관 및 두개골 워크 플로우를 지원하고 재고 및 서비스 오버 헤드를 줄이는 범용 플랫폼으로 이동하고 있습니다.

지역 분석

북미는 2024년 매출의 38.75%를 차지했으며 높은 수술 건수와 첨단 로봇의 조기 도입에 지지되고 있습니다. 미국의 ASC 시장만으로도 2028년까지 매출액이 590억 달러 가까이에 도달할 수 있어 비용 최적화된 회전이 빠른 테이블 주문에 박차를 가하고 있습니다. 메디케어에 의한 부위에 얽매이지 않는 상환의 추진은 병원에서 ASC로 기기 이행을 더욱 가속화해, Getinge와 STERIS의 지역 서비스 네트워크는 다운타임을 단축해, 브랜드에 대한 고집을 강화합니다.

유럽은 지속가능성과 규제의 엄격함이 구매를 형성하는 성숙한 교체 주도형 시장을 형성하고 있습니다. ASHRAE 189.3 가이드라인은 입찰 점수에 영향을 주며 에너지 효율적인 모터 드라이브와 재활용 가능한 포장을 구매자에게 촉구합니다. Getinge의 수술 워크플로우 부문은 2023년 4분기에 15.6% 증가를 달성했습니다. 녹색 공공조달 기준과 연관된 자본 보조금은 수술 건수의 성장이 평평함에도 불구하고 안정적인 수요를 유지할 가능성이 높습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 CAGR은 6.84%로 예측됩니다. 중국, 인도 및 ASEAN 국가에서는 의료 인프라 투자 및 의료 관광 확대가 하이브리드 룸 도입을 촉진하고 있습니다. 싱가포르의 Medtronic 로보틱스 체험 스튜디오는 교육 허브가 지역 전반에 걸쳐 첨단 수술실 기술의 보급을 가속화한다는 것을 보여줍니다. 벤처기업의 자금 조달은 지난 2년간 22% 감소했지만, 베트남과 한국의 국내 제조 이니셔티브는 수입 관세와 공급 병목 현상을 상쇄하고 현지화된 테이블 생산을 지원하는 데 도움이 되었습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 수술 건수 증가와 ASC의 확대

- 고령화에 의해 정형외과 및 심장외과의 증례 수가 증가

- 통합 OR 및 로봇 대응 테이블 업그레이드

- 수술 중 이미징을 가능하게 하는 탄소섬유제 방사선 투과성 상판

- 고도의 환자 포지셔닝 기능을 필요로 하는 저침습 수술과 로봇 수술의 급증

- 병원의 지속가능성 의무화에 의해 에너지 효율이 높은 모듈식 테이블 플랫폼을 선호

- 시장 성장 억제요인

- 중견 병원에서 프리미엄 가격과 설비투자의 동결

- 고급 테이블을 위한 숙련된 OR 기사의 부족

- 탄소섬유 공급망의 변동성

- 재처리와 규제 준수 엄격화에 의해 의료 제공업체의 평생 소유 비용이 상승

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 수술 유형별

- 일반 외과

- 정형외과 및 외상

- 순환기

- 뇌신경외과

- 기타

- 재료별

- 금속

- 탄소섬유 복합재료

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 전문 클리닉

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동

- GCC

- 남아프리카

- 기타 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Getinge AB

- Stryker Corporation

- Steris plc

- Trumpf Medical(Baxter/Hill-Rom)

- Mizuho OSI

- Skytron LLC

- Schaerer Medical AG

- Merivaara Corp.

- Alvo Medical

- LINET Group SE

- Mindray Medical Intl.

- Opt SurgiSystems Srl

- Eschmann Holdings Ltd

- Allengers Medical Systems

- Nuvo Inc.

- AGA Sanitatsartikel GmbH

- Meditek Canada

- Staan Bio-Med Engg. Pvt Ltd

제7장 시장 기회와 장래의 전망

JHS 25.11.21The surgical tables market stood at USD 1.57 billion in 2025 and is on track to reach USD 2.06 billion by 2030, growing at a 5.6% CAGR.

Demographic aging is lifting orthopedic and cardiovascular caseloads, outpatient care is shifting more procedures into ambulatory surgical centers (ASCs), and robotics-ready operating rooms (ORs) are raising the technical bar for patient-positioning platforms. Hospitals are upgrading to carbon-fiber radiolucent tops to support real-time imaging, while sustainability mandates in Europe and North America reward energy-efficient modular designs. Competitive strategies increasingly revolve around bundled OR ecosystems that tie surgical tables to imaging, lighting, and robotic offerings, helping providers simplify procurement and integration. Premium-segment manufacturers are also launching service and financing programs that mitigate capital-budget constraints for mid-tier hospitals.

Global Surgical Tables Market Trends and Insights

Rising surgical procedure volumes & ASC expansion

Outpatient sites perform the bulk of U.S. procedures and continue to attract complex orthopedic and gastroenterology cases because they operate at 45-60% lower costs than hospital outpatient departments and cut average wait times by 20% . ASC growth is encouraging vendors to deliver compact, multi-specialty tables that fit smaller footprints and rotate quickly between cases. To keep capital outlays down, manufacturers now market modular bases that accept specialty tops, letting centers defer upgrades until volumes justify them. Group-purchasing contracts and equipment-as-a-service financing further lower barriers to adoption.

Aging population driving higher orthopedic & cardiac caseload

Population aging elevates demand for joint reconstruction, fracture repair, and interventional cardiology procedures that require precise positioning and bariatric weight limits. U.S. orthopedic volumes are projected to reach 6.6 million procedures annually, reinforcing the need for heavy-load lifts and pressure-injury mitigation sensors. Bariatric-capable tables with integrated pressure mapping, such as XSENSOR's ForeSite OR, reduce hospital-acquired pressure injuries that affect up to 45% of surgical patients.

Premium pricing & capex freezes in mid-tier hospitals

Rising operating costs and inflation have caused smaller hospitals to delay capital purchases, selectively opting for refurbished equipment or multi-year leasing. Medicare reimbursement has slipped for total joint arthroplasty even as volumes climb, compressing margins and making high-end imaging-compatible tables harder to justify . Vendors are countering with staged upgrade paths that let facilities install a base and add connectivity kits later, plus service contracts that bundle maintenance, remanufacturing compliance, and software updates.

Other drivers and restraints analyzed in the detailed report include:

- Integrated-OR & robot-ready table upgrades

- Carbon-fiber radiolucent tops enabling intra-op imaging

- Surge in minimally invasive & robotic surgeries requiring advanced patient-positioning functionality

- Hospital sustainability mandates favoring energy-efficient, modular table platforms

- Shortage of skilled OR technologists for advanced tables

- Carbon-fiber supply chain volatility

- Stricter reprocessing and regulatory compliance raising lifetime ownership costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

General surgery held 35.78% of the surgical tables market share in 2024. Hospitals favor versatile, quick-switch platforms that serve appendectomies in the morning and bariatric cases in the afternoon. The segment's broad procedural mix supports economies of scale for replacement purchases, and its workflows align with standardized accessories such as removable armboards and lithotomy leg supports. Meanwhile, robotic cholecystectomy adoption is nudging many providers to replace manual hydraulic bases with motorized column systems featuring footswitch memory profiles for speed and consistency.

Orthopedic & trauma procedures are set to log a 6.78% CAGR to 2030, the fastest in the market. Knee and hip robotics like Zimmer Biomet's TMINI Miniature Robotic System depend on rigid, low-vibration surfaces that maintain sub-millimeter accuracy during milling. Table manufacturers respond with longitudinal slide and tilt ranges that expose distal femurs without repositioning, shortening anesthesia times and radiographic exposure. Neurosurgery and cardiovascular specialties occupy smaller shares but command premium pricing because they demand carbon tops, 360° C-arm clearance, and head fixation interfaces that integrate with navigation systems. As hospitals pursue cross-disciplinary hybrid rooms, demand is shifting toward universal platforms that support spinal, vascular, and cranial workflows on the same chassis, reducing inventory and service overhead.

The Surgical Tables Market Report is Segmented by Type of Surgery (General and Specialty), Material (Metal and Composite), End User (Hospitals, Ambulatory Surgical Centers, and Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Report Offers the Value (USD) for the Above Segments.

Geography Analysis

North America captured 38.75% of 2024 revenue, supported by high procedure volumes and early uptake of advanced robotics. The U.S. ASC market alone could reach nearly USD 59 billion in revenue by 2028, spurring orders for cost-optimized, quick-turnover tables. Medicare's push for site-neutral reimbursement further accelerates equipment migration from hospitals to ASCs, while regional service networks from Getinge and STERIS reduce downtime and reinforce brand stickiness.

Europe forms a mature, replacement-driven market where sustainability and regulatory rigor shape purchasing. ASHRAE 189.3 guidelines influence tender scores, nudging buyers toward energy-efficient motor drives and recyclable packaging. Getinge's Surgical Workflows segment posted 15.6% revenue growth in Q4 2023, helped by hospitals refreshing legacy fleets with integrated OR suites. Capital grants tied to green public-procurement criteria are likely to sustain steady demand despite flat procedural growth.

Asia-Pacific is the fastest-growing region, projected at a 6.84% CAGR. Healthcare infrastructure investment and widening medical-tourism flows drive adoption of hybrid rooms in China, India, and ASEAN states. Medtronic's Robotics Experience Studio in Singapore illustrates how training hubs accelerate diffusion of advanced OR technologies throughout the region. Venture funding dipped 22% over the past two years, yet domestic manufacturing initiatives in Vietnam and Korea help offset import tariffs and supply bottlenecks, supporting localized table production.

- Getinge

- Stryker

- Steris plc

- Trumpf Medical (Baxter/Hill-Rom)

- Mizuho

- Skytron

- Schaerer Medical AG

- Merivaara

- Alvo Medical

- LINET Group

- Mindray Medical Intl.

- Opt SurgiSystems Srl

- Eschmann Holdings

- Allengers Medical Systems

- Nuvo Inc.

- AGA Sanitatsartikel GmbH

- Meditek Canada

- Staan Bio-Med Engg. Pvt Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising surgical procedure volumes & ASC expansion

- 4.2.2 Aging population driving higher orthopedic & cardiac caseload

- 4.2.3 Integrated-OR & robot-ready table upgrades

- 4.2.4 Carbon-fiber radiolucent tops enabling intra-op imaging

- 4.2.5 Surge in minimally invasive & robotic surgeries requiring advanced patient-positioning functionality

- 4.2.6 Hospital sustainability mandates favoring energy-efficient, modular table platforms

- 4.3 Market Restraints

- 4.3.1 Premium pricing & capex freezes in mid-tier hospitals

- 4.3.2 Shortage of skilled OR technologists for advanced tables

- 4.3.3 Carbon-fiber supply chain volatility

- 4.3.4 Stricter reprocessing and regulatory compliance raising lifetime ownership costs for providers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type of Surgery

- 5.1.1 General Surgery

- 5.1.2 Orthopedic & Trauma

- 5.1.3 Cardiovascular

- 5.1.4 Neurosurgery

- 5.1.5 Others

- 5.2 By Material

- 5.2.1 Metal

- 5.2.2 Carbon-fiber Composite

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Clinics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Getinge AB

- 6.3.2 Stryker Corporation

- 6.3.3 Steris plc

- 6.3.4 Trumpf Medical (Baxter/Hill-Rom)

- 6.3.5 Mizuho OSI

- 6.3.6 Skytron LLC

- 6.3.7 Schaerer Medical AG

- 6.3.8 Merivaara Corp.

- 6.3.9 Alvo Medical

- 6.3.10 LINET Group SE

- 6.3.11 Mindray Medical Intl.

- 6.3.12 Opt SurgiSystems Srl

- 6.3.13 Eschmann Holdings Ltd

- 6.3.14 Allengers Medical Systems

- 6.3.15 Nuvo Inc.

- 6.3.16 AGA Sanitatsartikel GmbH

- 6.3.17 Meditek Canada

- 6.3.18 Staan Bio-Med Engg. Pvt Ltd