|

시장보고서

상품코드

1431021

세계 통증 관리 기기 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Global Pain Management Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

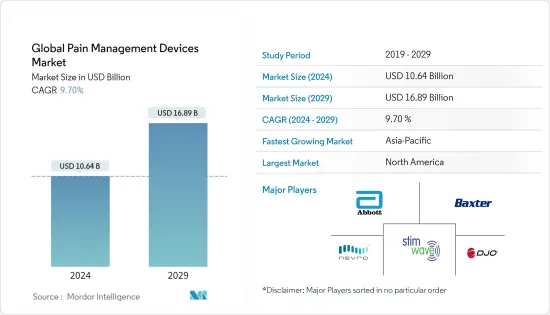

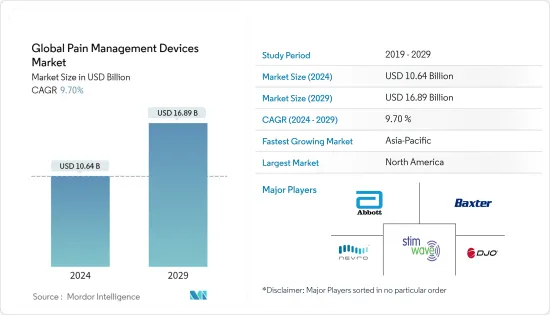

세계 통증 관리 기기 시장 규모는 2024년에 106억 4,000만 달러로 추정되며, 2029년까지는 168억 9,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2029년) CAGR 는 9.70%로 성장할 전망입니다.

COVID-19 팬데믹은 처음에는 통증 관리 기기 시장에 큰 영향을 미쳤습니다. 정부의 잠금과 엄격한 법률은 통증 관리 장비 시장의 성장에 영향을 미쳤습니다. 몇 가지 예기치 않은 이유로이 시장의 성장은 COVID-19의 초기 단계에서 크게 억제되었습니다. 그러나, 수액예약의 대폭적인 증가와 통증관리기기 시장을 세계적으로 확대시킨 어블레이션 처치에 의해 시장은 견인력을 얻었습니다. 또한, 통증관리기기의 대부분은 긴급성이 낮다고 판단되고, 또한 정부에 의한 엄격한 락다운으로 인해 외래환자와 개입조치가 모두 축소되었기 때문에 통증관리기기 시장은 큰 영향을 받았습니다.

COVID-19 사례의 급격한 증가는 간접적으로 세계에서 통증으로 고통받는 환자 수를 증가 시켰습니다. 근육통, 등통, 두통 등 COVID-19의 첫 증상은 통증으로 보고되었습니다. 예를 들어, Best Practice and Research in Clinical Anaesthesiology 2020년 7월호는 COVID-19 환자의 대부분이 근골격계, 등 통증, 두통을 증상으로 가지고 있었습니다고 보고하고 있습니다. 또한 Scientific Reports에 따르면 COVID 후 통증 점수는 10단계에서 6으로 증가했으며 COVID 이전에는 10단계에서 5였습니다고 합니다. COVID-19와 관련된 통증을 관리하고 극복하기 위해, 사람들은 의약품보다 통증 관리 기기를 선택하기 때문에 건강 관리 산업은 통증 관리 기기의 제조를 증가 시켰습니다. 견인하고 있습니다.

또한 암이나 심혈관질환 등 만성질환 증가도 통증관리기기의 보급을 뒷받침하고 통증관리기기 시장을 견인하고 있습니다. 예를 들어 세계보건기구가 발표한 데이터에 따르면 2020년에는 약 1,000만명이 암으로 사망했다고 보고되었습니다. 암의 이환율은 지난 수년간 극적으로 상승하고 있으며, 이 질병의 증상으로 관련 만성 통증도 증가하고 있기 때문에 통증 관리 기기 시장을 직접 견인하고 있습니다.

통증 관리 기기 중 하나 인 통증 제어 진통(PCA) 펌프는 척추 수술과 몇 가지 중요한 관절 수술과 관련된 통증을 극복하기 위해 수술 후 통증 관리에 사용됩니다. 예를 들어, 2021년 국립 척수 손상 통계 센터(NSCISC)의 데이터시트는 척수 손상의 연간 발생률을 100만 명당 60건으로 하고 있습니다. 이러한 증례가 증가하고 수술이 증가함에 따라 주입 펌프와 PCA 펌프 수요가 크게 증가하여 통증 관리 기기 시장을 견인하고 있습니다.

따라서 앞서 언급한 요인으로 인해 이 시장은 분석 기간 동안 성장할 것으로 예상됩니다. 그러나 낮은 인지도로 인해 통증 관리 기기보다 통증 관리 약물을 선호하는 환자는 여전히 적으며, 이는 통증 관리 기기 시장 성장 억제요인이 될 수 있습니다. 또한 이러한 장치는 통증을 극복하기 위해 두 번째 선택 치료를 치료하는 데 사용되며, 이는 또한이 시장의 과제가되었습니다.

통증 관리 기기 시장 동향

신경장애성 통증 관리 기기 분야는 세계 시장에서 가장 큰 점유율을 차지하고 현저한 성장을 이루

신경 병성 통증은 신경계가 손상되거나 정상적으로 작동하지 않을 때 발생합니다. 신경 장애 통증 관리 기기 분야는이 통증 관리 기기 시장에서 우위를 보여줍니다. 신경장애성 통증 관리 기기의 성장은 신경장애성 통증의 유병 인구 증가에 기인합니다. 예를 들어 질병관리센터(Centers for Disease Control and Center, 2021)는 성인의 약 5명 중 1명이 신경인성 통증으로 고통받고 있다고 보고하고 있습니다. 신경 인성 통증을 다루는 인구의 발생률 증가로 인한 것입니다.

COVID-19 증례 증가는 신경 병성 통증을 포함한 만성 통증의 증상 증가를 목격했습니다. 예를 들어, 학술지 'Pain Reports 2021'에 게재된 'COVID-19 유방병증 후 신경장애성 통증의 유병률 증가 가능성'이라는 제목의 논문에서 COVID-19는 신경장애성 통증의 말초 또는 중추 신경 합병증도 일으키는 것으로 언급됩니다. 특히 길란 밸리 증후군, 척수염, 뇌졸중을 포함한 COVID-19의 합병증 증가는 만성 신경 병성 통증의 잠재적 위험에 대해 검토되었습니다. COVID-19 후 만성 신경 병성 통증의 유병률 증가는 시장 성장을 뒷받침하는 또 다른 이유입니다.

기존의 통증 관리 요법에는 약물 요법이 있지만, 약물 요법에는 부작용이 수반되기 때문에 신경 병성 통증을 극복하기 위해 신경 자극 통증 관리 기기로 이동하고 있습니다. 이러한 이유로, 신경장애성 통증 관리 기기 분야는 이 통증 관리 기기 분야에서 가장 큰 점유율을 차지합니다.

북미가 통증관리기기 시장을 독점할 전망

북미는 통증 관리 기기 시장을 독점해 왔지만, 선진 기술의 존재, 주요 시장 기업, 외래 센터에서 통증 관리 기기의 대규모 도입으로 앞으로도 이 시장을 독점할 것으로 예상됩니다.

미국은 고통을 겪는 사람들의 수가 증가하고 있습니다. 예를 들어, Journal of Pain and Palliative Therapy, 2021에 따르면 미국 인구의 약 20.28%가 만성 통증으로 고통받고 있으며, 이 중 5%는 영향이 큰 만성 통증으로 고통받는 성인입니다. 따라서 미국에서는 만성 통증을 앓고 있는 인구가 증가하고 있으며 통증 관리 기기 시장을 빠르게 견인하고 있습니다. 또한 미국에서는 신경장애성 통증의 유병률이 높고 만성질환의 이환율이 높은 것으로 보고되어 있기 때문에 이 나라의 인구는 의약품보다 통증관리기기에 의존하고 있습니다. 예를 들어, Pain Medicine 기사에 따르면 미국 인구의 약 2%가 신경병증 통증으로 고통받고 있다고 합니다. 또한 2021년 International Journal of Environmental Health and Public Resource 잡지에 따르면 북미에서는 만성 질환의 유병률이 높기 때문에 미국인 전체의 약 45%(1억 3,300만 명)가 적어도 하나 만성 질환으로 고통받고 있습니다. 통증으로 고통받는 환자 증가는 시장 성장을 가속합니다.

높은 성장 가능성, 환자 기반 인구의 상당한 증가, 높은 가처분 소득으로 통증 관리 장비 시장 수요가 예측 기간 동안 증가할 것으로 예상됩니다.

통증 관리 장비 산업 개요

통증 관리 기기 시장은 세계 및 지역적으로 사업을 전개하는 다수의 기업이 존재하기 때문에 그 특성상 단편화되고 있습니다. 기존 주요 기업은 Abbott lab, AstraZeneca PLC, Baxter International Inc, DJO Global LLC, SPR Therapeutics, Stim Wave LLC, LivaNova, Nevro Corp, Innovis, ICU Medical Inc 등입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 혁신적이고 기술적으로 고도의 통증 관리 기기의 등장

- 통증 관리 기기의 채용 증가

- 고령자 인구 증가

- 시장 성장 억제요인

- 통증 관리를 위한 약제의 우선적 사용

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화(시장 규모 : 금액 기준)

- 제품 유형별

- 신경 자극 장치

- 주입 펌프

- 어블레이션 장치

- 용도별

- 근골격계

- 암성 통증

- 신경장애성 통증

- 안면통 및 편두통

- 기타

- 최종 사용자별

- 물리치료 센터

- 병원 및 클리닉

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Medtronic

- Boston Scientific Corporation

- Stryker

- Stim Wave LLC

- ICU Medical Inc

- Enovis

- Baxter

- LivaNova

- Abbott

- DJO Global LLC

- SPR Therapeutics

- Nevro Corp

제7장 시장 기회와 앞으로의 동향

JHS 24.03.04The Global Pain Management Devices Market size is estimated at USD 10.64 billion in 2024, and is expected to reach USD 16.89 billion by 2029, growing at a CAGR of 9.70% during the forecast period (2024-2029).

COVID-19 pandemic has had a substantial impact on the pain management devices market initially. The lockdown and strict laws imposed by the government impacted the growth of the pain management devices market.Due to some unforeseen reasons, the growth of this market was severely obstructed during the initial COVID-19 phase. However, the market gained traction due to the significant increase in infusion appointments, and ablation procedures which increased the market for pain management devices globally. Also, most of the pain management devices were deemed to be not so urgent, also all the outpatient and interventional procedures were reduced due to the strict lockdown imposed by the government, and thus the pain management device market was greatly impacted.

A significant increase in COVID-19 cases had also indirectly increased the number of patients suffering from pain worlwide. It was reported that pain was the first symptom of COVID-19, including myalgias, back pain, and headache. For instance, Best Practice and Research in Clinical Anaesthesiology, July 2020, reported that the majority of the COVID-19 patients had musculoskeletal, back pain, and headaches as a symptom. In another instance, the journal Scientific Reports, states that post-covid pain scores increased to 6 on a 10 scale as compared to pre-covid which was 5 on a 10. To manage and overcome the pain associated with COVID-19, people were more drifted towards pain management devices rather than medicines due to their less severe effects which subsequently led the healthcare industry to increase the manufacture of the pain management devices, which has driven this market.

The rise in cases of chronic diseases such as cancer and other cardiovascular diseases also boosted these devices to manage pain well, which has driven the pain management devices market. For instance, as per the data published by World Health Organization about 10 million deaths due to cancer were reported in 2020. The incidence of cancer is rising dramatically over the past few years and chronic pain associated as a symptom of this disease is also increasing, which is directly driving the pain management devices market.

One of the pain management device, pain controlled analgesia (PCA) pumps, are used to manage post-operative pain to overcome the pain associated with spine surgeries and some critical joint surgeries. For instance, National Spinal Cord Injury Statistical Center (NSCISC) 2021 datasheet has accounted the annual incidence of spinal cord injuries at 60 cases per million. With the increasing number of these cases, and a number of surgical procedures performed the demand for infusion and PCA pumps has significantly increased and thus has driven the pain management devices market.

Therefore, owing to the aforementioned factors the studied market is anticipated to witness growth over the analysis period. However, still few patients prefer pain management drugs over devices due to a lack of awareness which may cause hindrance to the management devices market. Also, these devices are used for the treatment of second-line of therapy to overcome pain, which is another challenge for this market.

Pain Management Devices Market Trends

The neuropathic pain management devices segment counted for the largest share of the global market and witness significant growth

Neuropathic pain can happen if the nervous system is damaged or not working correctly. The neuropathic pain management device segment has witnessed dominance in this pain management devices market. The growth of neuropathic pain management devices has increased attributed due to the increase in the prevalence population of neuropathic pain. For instance, the Centers for Disease Control and Center, 2021 reports that about one in five adults suffers from neuropathic pain. Due to an increase in the incidence rate of the population dealing with neuropathic pain

The increase in cases of COVID-19 had witnessed an increase in the symptoms of chronic pain including neuropathic pain. For instance, the article titled 'Potential for the increased prevalence of neuropathic pain after the COVID-19 pandemic' in the journal Pain Reports 2021, states that COVID-19 also causes peripheral or central neurological complications of neuropathic pain. Increased complications of COVID-19 including in particular Guillain-Barre syndrome, myelitis, and stroke are reviewed with regards to their potential risk of chronic neuropathic pain. This increase in the prevalence of chronic neuropathic pain after COVID-19 is another reason boosting the market growth.

Traditional therapy for pain management includes drugs and medicine, but due to the side effects associated with drugs, people are shifting towards neurostimulation pain management devices to overcome neuropathic pain. Thus because of the above-mentioned reasons neuropathic pain management devices segment is witnessing the largest share in this pain management devices segment.

North America is Expected to Dominate the Pain Management Devices Market

North America has dominated the pain management devices market and is expected to dominate this market due to the presence of advanced technology, key market players, and the large incorporation of pain management devices in ambulatory centers.

The United States accounts for the increasing number of individuals suffering from pain. For instance, the Journal of Pain and Palliative Therapy, 2021 accounts that approximately 20.28% of the United States population is suffering from chronic pain and 5% of this population comprises adults who are suffering from high-impact chronic pain. Therefore, with the increasing prevalence of the population suffering from chronic pain in the United States rapidly drives its market for pain management devices. Also due to the high prevalence of neuropathic pain and higher incidence of the chronic disease reported in the United States, the population there is more dependent on pain management devices rather than on medicines. For instance, according to an article in the journal Pain Medicine, about 2% of the United States population suffers from neuropathic pain. Additionally, as the article in journal International Journal of Environmental Health and Public Resource, 2021 mentioned that approximately 45%, (or 133 million) of all Americans suffer from at least one chronic disease thus due to the high prevalence of population in North America suffering from chronic diseases. The increase in patient population suffering from pain will in turn propel the market growth.

Due to high growth potential, a significant increase in the patient base population, and high disposable income the demand of the pain management devices market is expected to increase during the forecast period.

Pain Management Devices Industry Overview

The pain management devices market is fragmented in nature due to the presence of several companies operating globally as well as regionally. The existing key players in the market are Abbott lab, AstraZeneca PLC, Baxter International Inc, DJO Global LLC, SPR Therapeutics, Stim Wave LLC, LivaNova, Nevro Corp, Innovis, ICU Medical Inc, and other prominent players.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 The advent of Innovative and Technologically Advanced Pain Management Devices

- 4.2.2 Increase in Adoption of Pain Management Devices

- 4.2.3 Rise in Geriatric Population

- 4.3 Market Restraints

- 4.3.1 Preferable use of medications for pain management

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION( Market Size by Value)

- 5.1 By Product Type

- 5.1.1 Neurostimulation Devices

- 5.1.2 Infusion Pumps

- 5.1.3 Ablation Devices

- 5.2 By Application

- 5.2.1 Musculoskeletal

- 5.2.2 Cancer Pain

- 5.2.3 Neuropathic Pain

- 5.2.4 Facial Pain and Migraine

- 5.2.5 Other

- 5.3 By End-User

- 5.3.1 Physiotherapy Centers

- 5.3.2 Hospitals and Clinics

- 5.3.3 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Medtronic

- 6.1.2 Boston Scientific Corporation

- 6.1.3 Stryker

- 6.1.4 Stim Wave LLC

- 6.1.5 ICU Medical Inc

- 6.1.6 Enovis

- 6.1.7 Baxter

- 6.1.8 LivaNova

- 6.1.9 Abbott

- 6.1.10 DJO Global LLC

- 6.1.11 SPR Therapeutics

- 6.1.12 Nevro Corp