|

시장보고서

상품코드

1431448

세라믹 커패시터 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Ceramic Capacitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

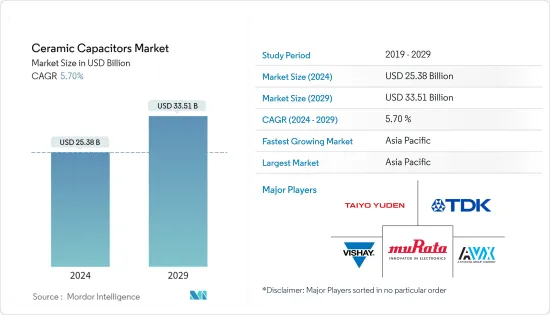

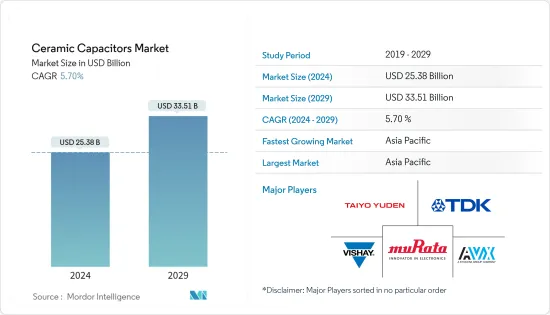

세계 세라믹 커패시터 시장 규모는 2024년 253억 8,000만 달러로 추정되며, 2029년에는 335억 1,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 연평균 5.70%의 성장률을 보일 것으로 예상됩니다.

세라믹 커패시터는 높은 신뢰성과 낮은 제조 비용으로 인해 대부분의 전기 장비에서 가장 일반적으로 사용됩니다. 이 커패시터는 여러 산업 분야에서 사용되며 주로 무극성 세라믹 또는 도자기 디스크로 구성되어 있습니다. 세라믹 소재는 전도성이 낮고 정전기장을 효율적으로 지원하기 때문에 우수한 유전체이기도 합니다.

주요 하이라이트

- 세 가지 주요 유형의 세라믹 커패시터가 있습니다. 스루홀 실장용 리드형 디스크 세라믹 커패시터, 수지 코팅된 표면 실장용 적층 세라믹 커패시터(MLCC), 그리고 주로 PCB의 슬롯에 장착하기 위한 특수한 유형의 전자 레인지용 베어 리드리스 디스크 세라믹 커패시터입니다.

- 그중에서도 MLCC는 많은 전자기기에 필수적인 부품으로 웨어러블 기기, 스마트폰(스마트폰에는 약 900-1,100개의 적층 세라믹 커패시터가 탑재되어 있음) 등에 널리 사용되고 있습니다.

- 또한 전자제품의 선호도가 가전제품에서 컴퓨팅으로 이동하고 있으며, AI, IoT, 클라우드, 디지털화의 출현으로 제조업체들은 이 분야에 집중하고 있습니다. 이러한 신기술은 소비재에 비해 수익성이 높고 생산량이 적기 때문에 제조업체의 생산 라인 관리도 가능합니다.

- 5G 스마트폰의 보급과 고기능화는 전자회로의 소형화 및 고밀도화에 대한 수요를 더욱 자극하고 있습니다. 예를 들어, 퀄컴과 미디어텍을 포함한 많은 기업들이 5G를 지원하는 칩셋을 출시했고, 많은 스마트폰 제조업체들이 이를 사용하고 있습니다. 이전에는 5G 지원은 플래그십 모바일에만 국한되어 있었지만, 이제는 중급형 스마트폰도 5G를 지원하여 더 저렴한 칩셋을 시장에 출시하고 있습니다. 이러한 노력으로 인해 세라믹 커패시터의 필요성이 증가하고 있습니다.

- 반면, 세라믹 커패시터 생산에는 몇 가지 도전과제가 있습니다. 가장 큰 과제 중 하나는 고용량 적층 세라믹 커패시터(MLCC)를 제조하는 것인데, 이를 위해서는 다수의 단층 커패시터를 하나의 패키지에 적층해야 합니다. 이러한 커패시터 제조에는 기계적 영향을 받기 쉽고, 회로 기판에 표면 실장 납땜 시 균열이 발생하기 쉬우며, 전체 층에서 높은 커패시턴스 균일성을 확보하기 어렵다는 문제점이 있습니다. 또 다른 문제는 커패시턴스의 온도 및 주파수 의존성인데, 이는 고성능 애플리케이션에서 문제를 일으킬 수 있습니다.

- COVID-19 팬데믹은 세라믹 커패시터 시장에 영향을 미쳤습니다. 전염병은 공급망과 제조 공정에 혼란을 일으켜 세라믹 커패시터의 수요와 공급에 변동을 일으켰습니다.

- 그러나 백신 접종 추진과 규제 완화로 상황이 정상화됨에 따라 시장이 회복될 것으로 예상했습니다. 한편, 세라믹 커패시터 부품은 전 세계적으로 재택근무가 증가함에 따라 노트북, PC 등 가전제품과 모바일 기기에 대한 수요가 증가함에 따라 다른 산업에서 수요가 증가할 것으로 예상됩니다. 또한, 팬데믹 기간 동안 온라인 게임 트렌드가 강화되면서 게임 및 홈시어터 전자제품에 대한 수요가 증가한 것도 큰 수요를 이끌었습니다.

세라믹 커패시터 시장 동향

자동차 부문이 시장 성장을 주도할 것으로 예상

- 세라믹 커패시터는 컴팩트한 크기, 높은 신뢰성, 고온과 진동을 견딜 수 있는 능력으로 인해 일반적으로 자동차 애플리케이션에 채택됩니다. 세라믹 커패시터는 엔진 제어 장치, 인포테인먼트 시스템, 조명 시스템 등 다양한 자동차 시스템의 전원 공급 장치에서 고주파 노이즈를 필터링합니다. 또한, 스위칭 회로의 전압 스파이크와 링잉을 억제하는 스내버 회로와 회로 간 고주파 신호를 통과시키는 커플링 회로에도 적용됩니다. 또한, 센서 및 액추에이터의 공진 회로, 각종 차량용 시스템의 클록 제너레이터 등 타이밍 회로 및 발진 회로에도 사용됩니다.

- 자율주행차 기술, 차량 간 통신, ADAS(첨단운전자보조시스템), 백업 카메라, 차선 이탈 감지기와 같은 안전 및 감지 시스템으로 인한 새로운 자동차 기능 및 특징이 자동차 전자부품에 대한 수요를 증가시키고 있습니다. 세라믹 커패시터와 같은 수동 부품은 안정성과 간섭 없는 설계를 보장하기 위해 필요합니다.

- 세계경제포럼(WEF)에 따르면, 2035년까지 완전 자율주행차는 연간 1,200만 대 이상 판매될 것으로 예상되며, 전 세계 자동차 시장의 25%를 차지할 것으로 예상됩니다. 또한 새로운 법은 이러한 차량은 "현재 승용차와 동일한 수준의 탑승자 보호를 계속 제공해야 한다"고 강조하고 있습니다. 교통부 장관의 말처럼, Pete Buttigieg의 새로운 규칙은 ADS 장착 차량에 대한 견고한 안전 기준을 확립하는 데 필수적입니다. 이러한 신흥국 시장 개척은 이 지역의 커넥티드카 시장 보급을 촉진하여 연구 시장의 성장을 지원할 것입니다. 이는 국내외 엣지 컴퓨팅 기업들이 시장 점유율을 확대할 수 있는 기회를 창출할 수 있습니다.

- 자율주행차, ADAS(첨단운전자보조시스템) 등 첨단 자동차로의 전환은 자동차 당 MLCC의 사용을 촉진하고 있습니다. 이에 따라 각 업체들은 이러한 추세에 대응하기 위해 세라믹 커패시터의 고용량화와 관련된 제품 혁신에 힘쓰고 있습니다. 예를 들어, 무라타제작소는 2021년 12월 MLCC 중 가장 높은 커패시턴스 22μF, 정격 전압 16V의 GCM31CC71C226ME36 MLCC를 개발했다고 발표했습니다. 이 MLCC는 차량용 애플리케이션과 안전 애플리케이션에 적합합니다. 또한, 이 커패시터는 박층 시트 성형 기술로 설계되어 더 높은 신뢰성과 효율을 실현했습니다.

- 마찬가지로 2022년 2월에는 3단자에서 4.3μF의 정전 용량을 제공하도록 설계된 NFM15HC435D0E3 MLCC를 출시했습니다. 이 커패시터는 ADAS(첨단운전자보조시스템), 자율주행 기능 등에 탑재되는 고성능 프로세서에 요구되는 노이즈 제거 및 우수한 디커플링 등의 효과를 발휘하는 차량용 애플리케이션을 위해 설계되었습니다. 이는 자동차 산업에서 세라믹 커패시터에 대한 수요가 확대되고 있음을 보여줍니다. 그러나 COVID-19의 상시적 유행으로 인해 공급망은 소규모의 혼란을 겪을 것으로 예상됩니다.

- 또한, 전기자동차의 MLCC 수요도 증가하고 있습니다. IEA에 따르면 2022년 전기차 판매량은 102만 대에 달할 것으로 예상되는데, 이는 운전 보조 기능, 완전 자율주행 시스템 등의 기능 증가로 인해 대부분의 전기차에 10-15,000개에 가까운 MLCC가 사용되기 때문입니다. 이러한 사례는 자동차 부문에서 MLCC의 수요가 확대되고 있음을 보여줍니다. 또한, EV의 높은 보급률과 각국 정부가 설정한 ICE 엔진의 완전한 단계적 폐지 시기는 자동차 부문에서 MLCC의 성장을 촉진할 것으로 보입니다.

아시아태평양은 높은 시장 성장 전망

- 아시아태평양은 세라믹 커패시터의 가장 중요한 시장 중 하나입니다. 중국에서는 자동차 산업이 확대되고 있으며 세계 자동차 시장에서 중요한 역할을 하고 있습니다. 중국 정부는 자동차 부품 부문을 포함한 자동차 산업을 국가의 주요 산업 중 하나로 간주하고 있습니다. 중국 정부는 2025년까지 중국의 자동차 생산량이 3,500만 대에 달할 것으로 예상하고 있습니다. 이는 커패시터 수요를 견인할 것으로 예상됩니다.

- EV의 인기가 높아지고 있으며, 중국은 전기자동차를 채택하는 주요 국가 중 하나로 간주되고 있습니다. 중국의 13차 5개년 계획은 교통 부문의 발전을 위해 하이브리드 및 전기차와 같은 친환경 교통 솔루션의 개발을 촉진하고 있습니다. 중국의 전기자동차는 수십 개의 경쟁업체들의 새로운 모델들이 신규 구매자를 끌어들이고 소유주들이 전기자동차로 전환하도록 유도하면서 중국 정부의 2025년 예측을 크게 상회하는 2022년 전국 보급률 20% 목표를 달성할 수 있는 기세를 보이고 있습니다.

- 또한 일본 정부는 2050년까지 일본에서 판매되는 모든 신차를 전기자동차든 하이브리드 자동차든 보급하는 것을 목표로 하고 있습니다. 또한 민간 기업의 전기차 배터리와 모터 개발을 가속화하기 위해 보조금을 지급할 계획도 있습니다. 일본은 10년 전 닛산 리프와 미쓰비시 i-MIEV가 출시되면서 전기차를 가장 먼저 도입한 국가 중 하나입니다.

- 세라믹 커패시터는 높은 커패시턴스, 높은 내전압, 저렴한 비용으로 인해 통신 산업에서 일반적으로 사용됩니다. 필터링, 디커플링, 전압 조정 등 다양한 용도로 사용됩니다. 특히 적층 세라믹 커패시터(MLCC)는 컴팩트 한 크기와 높은 커패시턴스 값으로 인해 통신 산업에서 인기가 높으며 MLCC는 스마트 폰, 기지국 및 기타 통신 장비와 같은 다양한 응용 분야에 사용됩니다.

- 교세라, KEMET 등 아시아태평양의 제조업체들은 통신용으로 설계된 세라믹 커패시터를 생산하고 있습니다. 이 지역의 통신 수요 증가는 이 지역의 세라믹 커패시터 수요를 증가시킬 것으로 예상됩니다. 예를 들어, 차이나텔레콤(China Telecom)에 따르면 2022년 매출은 약 4750억 위안으로 전년도 4400억 위안에서 크게 증가할 것으로 예상했습니다.

- 중국은 아시아태평양의 AGV 성장에 크게 기여하고 있습니다. 제조, 자동차, E-Commerce 등 모든 산업에서 AGV 제품에 대한 수요가 증가함에 따라 시장 성장에 긍정적인 영향을 미치고 있으며, AGV는 덤프 및 리프팅을위한 고출력 버스트와 스테이션 간 이동을 위해 지속적인 에너지가 필요합니다. 이러한 폭발적인 전력은 배터리 수명을 크게 단축시켜 제조업체는 배터리를 자주 교체해야 합니다. 또한 작업 교대 중에 배터리를 교체해야 합니다. 배터리와 달리 커패시터는 유지보수가 거의 필요하지 않으며 바닥 유도 충전을 사용하여 몇 초 만에 충전 할 수 있으므로 제조업체는 배터리 교체 및 교체에서 벗어날 수 있습니다. 아시아태평양의 공장 자동화는 예측 기간 동안 세라믹 커패시터 수요를 견인할 것으로 예상됩니다.

- 또한, 이 지역의 기업들은 다양한 고객 니즈에 대응하기 위해 다양한 제품을 제공하고 있습니다. 예를 들어, 무라타제작소는 자동차 파워트레인용 적층 세라믹 커패시터(MLCC), 고실효용량 칩 MLCC, 고리플 전류 칩 MLCC, 가전 및 산업기기용 안전 칩 MLCC 등 다양한 세라믹 커패시터를 공급하고 있습니다. 무라타제작소의 세라믹 커패시터는 작고 큰 정전용량 값으로 유명합니다. 또한, MLCC로는 세계 최초로 정전용량 1μF/25V의 GCM033D70E105ME36을 개발하여 양산을 개시하였습니다.

세라믹 커패시터 산업 개요

세라믹 커패시터 시장은 세계 시장 공급업체가 제한적이기 때문에 시장이 정체되어 있습니다. 주요 기업들은 시장 점유율을 높이고 시장 수익성을 높이기 위해 인수 및 파트너십과 같은 다양한 전략에 참여하고 있습니다. Murata Manufacturing Co., Ltd., TDK Corporation, Taiyo Yuden Co., Ltd., AVX Corporation, Vishay Intertechnology, Inc. 등의 대기업이 진출해 있습니다.

- 2023년 11월 교세라 AVX는 클래스 X1/Y2 표준을 준수하는 커패시터 KGK 시리즈와 클래스 X2 표준을 준수하는 커패시터 KGH 시리즈를 출시했습니다. 이 커패시터의 정격 전압은 250VAC이며 EN 60384-14, IEC 60384-14, UL 60384-14 표준의 요구 사항을 충족하도록 설계되었습니다. 서지 보호, 과도 보호, EMI 필터링 기능을 갖추고 있어 모뎀, 팩스 등 다양한 가전제품 및 산업 장비에 사용하기에 적합합니다.

- 2023년 9월 TDK 주식회사(사장: 가미카마 켄히로)는 적층 세라믹 커패시터(MLCC) CN 시리즈에 혁신적이고 특징적인 디자인을 채택한 강화 버전을 발표했습니다. 기존의 소프트 종단형 MLCC는 단자 전극 전체를 수지층으로 코팅했지만, 본 제품은 기판에 실장하는 한쪽 면에만 수지층을 형성했습니다. 또한, TDK는 대용량 MLCC에 대한 수요 증가에 대응하기 위해 CNA 시리즈(차량용) 및 CNC 시리즈(상업용)를 출시하여 제품 라인업을 확대했습니다.

기타 혜택:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 구매자의 교섭력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 관계

- 밸류체인 분석

- COVID-19 이후 분석을 포함한 거시경제 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 디지털화와 5G 기술 보급 확대

- 공장 자동화와 로보틱스 채용

- 시장 성장 억제요인

- 세라믹 커패시터 개발에 필요한 첨단 마이크로 레벨 기술력

제6장 시장 세분화

- 유형별

- MLCC

- 세라믹 디스크 커패시터

- 관통형 세라믹 커패시터

- 세라믹 파워 커패시터

- 최종사용자별

- 가전

- 자동차

- 통신

- 산업용

- 에너지·전력

- 기타 최종사용자

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 상황

- 기업 개요

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- Taiyo Yuden Co., Ltd.

- Vishay Intertechnology, Inc.

- AVX Corporation

- Johanson Dielectrics, Inc.

- AFM Microelectronics

- Kemet Corporation

- Walsin Technology Corporation

- TE Connectivity

제8장 투자 분석

제9장 시장 향후 전망

KSM 24.03.07The Ceramic Capacitors Market size is estimated at USD 25.38 billion in 2024, and is expected to reach USD 33.51 billion by 2029, growing at a CAGR of 5.70% during the forecast period (2024-2029).

Ceramic capacitors are one of the most commonly used in most electrical instruments, as they offer reliability and are cheaper to manufacture. These capacitors are used in multiple industries and primarily consist of ceramic or porcelain discs that exist in a non-polarized form. The ceramic material is also an excellent dielectric due to its poor conductivity and its efficient support of electrostatic fields.

Key Highlights

- Ceramic capacitors are mostly available in three types. However, other styles are also available: leaded disc ceramic capacitors for through-hole mounting, resin-coated surface mount multilayer ceramic capacitors (MLCC), and special type microwave bare lead-less disc ceramic capacitors, which are primarily intended to sit in a slot on the PCBs.

- Among the applications, MLCCs are essential components of many electronic devices and are widely used in such devices as wearable devices and smartphones (approximately 900 to 1100 multilayer ceramic capacitors are installed in a smartphone).

- Also, there has been a shift in preference in electronics from consumer electronics to computing. The emergence of AI, IoT, cloud, and digitalization has led manufacturers to concentrate on this segment. These new technologies have a high profit margin compared to consumer goods, and the units needed are also fewer, making it viable for manufacturers to manage their production lines.

- The widespread adoption of 5G smartphones and their increasing functionality are stoking demand for further miniaturization and higher electronic circuitry density. For instance, a number of companies, including Qualcomm and MediaTek, are releasing chipsets that support 5G, and numerous smartphone manufacturers are using them. Previously, 5G support was confined to only flagship mobiles; now, mid-level smartphones also support 5G to introduce cheaper chipsets in the market. Such initiatives are increasing the need for ceramic capacitors.

- On the flip side, the production of ceramic capacitors presents several challenges. One major challenge is manufacturing high-capacitance multilayer ceramic capacitors (MLCCs), which involves stacking many single-layer capacitors into a single package. The manufacture of these capacitors is fraught with problems, including mechanical susceptibility, cracking during surface-mount soldering to a circuit board, and difficulty achieving high uniformity of capacitance across the layers. Another challenge is capacitance's temperature and frequency dependence, which can cause issues in high-performance applications.

- The COVID-19 pandemic impacted the ceramic capacitor market. The pandemic caused disruptions in the supply chain and manufacturing processes, leading to fluctuations in the demand and supply of ceramic capacitors.

- However, the market was anticipated to recover as the situation normalized with the ongoing vaccination drives and relaxed regulations. Meanwhile, ceramic capacitor components were expected to witness a growing demand from other industries due to an increasing demand for consumer electronics and mobile devices, such as laptops and computers, due to the work-from-home scenario across the world. Also, significant demand was witnessed from the increasing trend of online gaming during the pandemic, which subsequently increased the demand for gaming and home theater electronics.

Ceramic Capacitors Market Trends

Automotive Segment is Expected to Drive the Market's Growth

- Ceramic capacitors are usually employed in automotive applications due to their compact size, high reliability, and ability to withstand high temperatures and vibrations. They filter out high-frequency noise from power supplies in various automotive systems, such as engine control units, infotainment systems, and lighting systems. They are also employed in snubber circuits to suppress voltage spikes and ringing in switching circuits and in coupling circuits to pass high-frequency signals between circuits. Further, they are used in timing and oscillation circuits, such as in resonant circuits for sensors and actuators, as well as in clock generators for various automotive systems.

- The new automotive features and functionality due to autonomous vehicle technologies, vehicle-to-vehicle communications, advanced driver-assistance systems, and other safety and sensing systems, like backup cameras and lane-departure detectors, are driving the demand for electronic components in automotive applications. Passive components, like ceramic capacitors, are required to ensure stability and interference-free designs.

- According to the World Economic Forum, over 12 million fully autonomous cars are expected to be sold annually by 2035, covering 25% of the global automotive market. Further, the new law emphasizes that such cars "must continue to offer the same high levels of occupant protection as current passenger vehicles." As the Transportation Secretary said, Pete Buttigieg's new rule is essential to establishing robust safety standards for ADS-equipped vehicles. Such developments aid the growth of the studied market by propelling the proliferation of the connected car market in the region. This may create opportunities for local and international edge computing players to expand their market share.

- The shift towards sophisticated vehicles, such as self-driving vehicles, ADAS (Advanced Driver Assistance Systems), is driving the use of MLCCs per vehicle. Therefore, to cater to such a trend, manufacturers are involved in product innovation related to higher capacitance for ceramic capacitors. For instance, in December 2021, Murata announced the development of a GCM31CC71C226ME36 MLCC that features the highest capacitance of 22 μF for MLCCs and has a voltage rating of 16V. The application of this MLCC is streamlined for automotive and safety applications. In addition, the capacitors are designed with thin-layer sheet forming technology to achieve greater reliability and efficiency.

- Similarly, in February 2022, the company launched the NFM15HC435D0E3 MLCC, designed with three terminals to provide a capacitance of 4.3 μF. The capacitors are designed for automotive applications to attain results on noise removal and superior decoupling that are required for high-performance processors employed in advanced driver assistance systems and autonomous driving functions. This indicates the growing demand for ceramic capacitors in the automotive industry. However, with the impact of the constant COVID-19 pandemic, the supply chain is expected to be disrupted on a small scale.

- Moreover, the demand for MLCC in electric vehicles is also increasing, as most of the EVs use close to 10-15,000 MLCC due to increased features like driver assistance functions and fully autonomous systems. The sales of EVs increased in 2022, according to the IEA, and accounted for 1.02 million electric vehicles. Such instances indicate the growing demand for MLCC in the automotive sector. Further, the high adoption of EVs and the complete phase-out dates of ICE engines set by various governments will drive the growth of MLCC in the automotive sector.

Asia-Pacific Region is Expected to Witness a High Market Growth

- The Asia-Pacific region is one of the most important markets for ceramic capacitors. The automotive industry is expanding in China, and the country plays an important role in the worldwide automotive market. The government sees its automotive industry, including the auto parts sector, as one of the country's primary industries. The government of China anticipates that China's automobile output is expected to reach 35 million units by 2025. This is expected to drive the capacitors' demand.

- The popularity of EVs is growing, and China is regarded as one of the dominant adopters of electric vehicles. The country's 13th Five-Year Plan promotes the development of green transportation solutions, such as hybrid and electric vehicles, for advancements in the country's transportation sector. China's electric cars were on track to reach the 20% nationwide penetration goal in 2022, well ahead of the Chinese government's 2025 forecast, due to new models by dozens of competitors attracting new buyers and encouraging owners to switch to electric vehicles.

- Further, the Japanese government aims to have all the new cars sold in Japan, whether electric or hybrid, by the year 2050. The country plans to also offer subsidies to accelerate the private sector's development of batteries and motors for electricity-powered vehicles. Japan is one of the countries that were early adopters of electric vehicles, with the launch of the Nissan LEAF and Mitsubishi i-MIEV more than a decade ago.

- Ceramic capacitors are commonly used in the telecommunications industry due to their high capacitance, high voltage tolerance, and low cost. They are employed in various applications, such as filtering, decoupling, and voltage regulation. In particular, multilayer ceramic capacitors (MLCCs) are popular in the telecommunications industry due to their compact size and high capacitance values. MLCCs are used in various applications, including smartphones, base stations, and other telecommunications equipment.

- Manufacturers in the Asia-Pacific region, such as Kyocera and KEMET, produce ceramic capacitors designed for telecommunications applications. The increasing telecom demand in the region is anticipated to boost the demand for ceramic capacitors in the region. For instance, according to China Telecom, in 2022, it generated revenue of approximately CNY 475 billion, a significant increase from CNY 440 billion in the previous year.

- China has been a significant contributor to the growth of the AGVs in the Asia-Pacific region. The growing demand for AGV products across industries, such as manufacturing, automotive, and e-commerce, among others, is boosting the market's growth positively. An AGV requires high power bursts for dumping or lifting, as well as continuous energy for traveling between stations. These bursts of power significantly reduce battery life, requiring manufacturers to replace batteries frequently. There is also the need to exchange batteries during working shifts. Unlike batteries, capacitors require little maintenance and can be charged in seconds using in-floor inductive charging, freeing manufacturers from constant battery swaps and replacements. The increasing factory automation in the Asia-Pacific region is anticipated to drive the demand for ceramic capacitors during the forecast period.

- Additionally, the players in the region are offering various products to cater to a wide range of customers' needs. For example, Murata Manufacturing Co., Ltd. offers various ceramic capacitors, including multilayer ceramic capacitors (MLCCs), high effective capacitance, and high ripple current chip MLCCs for automotive powertrains, and safety chip MLCCs for consumer electronics and industrial equipment. Murata's ceramic capacitors are renowned for their small size and large capacitance values. They have also developed and started mass production of the GCM033D70E105ME36, the world's first MLCC capacitance of 1 μF/25 V.

Ceramic Capacitors Industry Overview

The ceramic capacitor market is Semi-consolidated due to limited vendors in the global market. The key players are involved in various strategies, such as acquisitions and partnerships, to improve their market share and enhance their profitability in the market. Some of the leading players are there in the market are Murata Manufacturing Co., Ltd., TDK Corporation, Taiyo Yuden Co., Ltd., AVX Corporation, Vishay Intertechnology, Inc., and many others.

- November 2023: Kyocera AVX has introduced the KGK series of capacitors that comply with Class X1/Y2 standards and the KGH series of capacitors that comply with Class X2 standards. These capacitors, with a voltage rating of 250 VAC, are designed to meet the requirements set by EN 60384-14, IEC 60384-14, and UL 60384-14 standards. They offer surge and transient protection and EMI filtering, making them suitable for use in various consumer and industrial devices such as modems and fax machines.

- September 2023: TDK Corporation has introduced an enhanced version of its CN series of multilayer ceramic capacitors (MLCCs) that boasts an innovative and distinctive design. In contrast to conventional soft termination MLCCs, where the entire terminal electrodes are coated with resin layers, this new design incorporates resin layers only on one side that is mounted on a board. Moreover, TDK Corporation has also expanded its product range by introducing the CNA series (automotive grade) and CNC series (commercial grade) to cater to the growing demand for MLCCs with larger capacitances.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Value Chain Analysis

- 4.4 Macro-economic Assessment Including Post-COVID-19 Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Penetration of Digitalization and 5G technology

- 5.1.2 Adoption of Factory Automation and Robotics

- 5.2 Market Restraints

- 5.2.1 Requirement of Advanced Micro level Technical Competence for Developing Ceramic Capacitors

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 MLCC

- 6.1.2 Ceramic Disc Capacitor

- 6.1.3 Feedthrough Ceramic Capacitor

- 6.1.4 Ceramic Power Capacitor

- 6.2 By End-User

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 Telecommunication

- 6.2.4 Industrial

- 6.2.5 Energy & Power

- 6.2.6 Other End-Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Murata Manufacturing Co., Ltd.

- 7.1.2 TDK Corporation

- 7.1.3 Taiyo Yuden Co., Ltd.

- 7.1.4 Vishay Intertechnology, Inc.

- 7.1.5 AVX Corporation

- 7.1.6 Johanson Dielectrics, Inc.

- 7.1.7 AFM Microelectronics

- 7.1.8 Kemet Corporation

- 7.1.9 Walsin Technology Corporation

- 7.1.10 TE Connectivity