|

시장보고서

상품코드

1431615

세계 위성용 컴포넌트 시장 : 점유율 분석, 산업 동향, 성장 예측(2024-2029년)Satellite Component - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

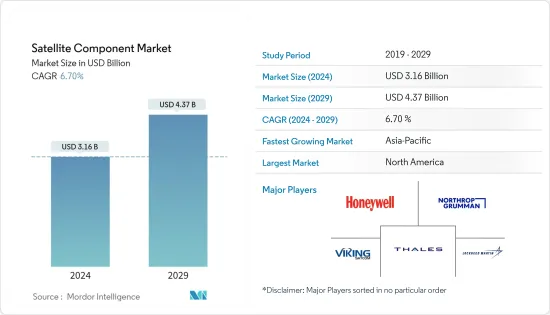

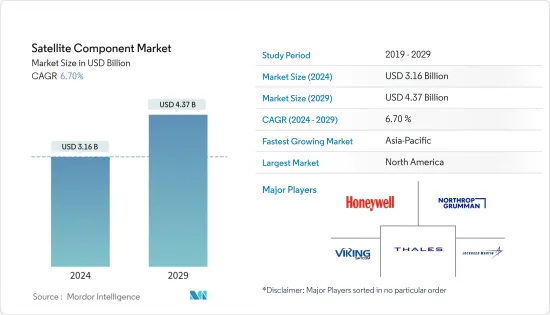

위성용 컴포넌트 시장 규모는 2024년에 31억 6,000만 달러로 추정되고, 2029년에는 43억 7,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2029년) CAGR은 6.70%로 성장할 전망입니다.

주요 하이라이트

- 세계 위성용 컴포넌트 시장은 COVID-19 팬데믹이 전례 없는 과제에 직면해 있습니다. 우주 분야는 원재료 부족, 위성 발사 계획 지연, 정부의 엄격한 규제에 의한 공급망의 혼란 등 과제를 목격했습니다. 유행 이후 시장은 강력한 회복을 보였습니다. 우주 분야에 대한 지출 증가와 소형 위성 발사 증가는 유행 이후 시장 성장을 이끌고 있습니다.

- 위성 구성 요소는 통신 시스템, 전원 시스템, 전원 시스템 등으로 구성됩니다. 통신 시스템은 신호를 수신하고 재전송하는 안테나와 중계기를 포함합니다. 추진 시스템은 위성을 추진하는 로켓으로 구성되며, 전력 시스템은 전력을 공급하는 태양전지판로 구성됩니다. 위성 발사 수 증가와 우주 분야에 대한 지출 증가가 시장 성장의 원동력이 되고 있습니다. 유엔 우주부(UNOOSA)의 지표에 따르면 2022년에는 8,261개의 위성이 지구를 주회하고 있으며, 2021년 4월에 비해 11.84% 증가하고 있습니다.

위성용 컴포넌트 시장 동향

안테나 부문은 예측 기간 동안 현저한 성장을 보일 것으로 예측

- 안테나 부문은 예측 기간 동안 현저한 성장을 나타낼 것으로 예측됩니다. 이러한 성장의 배경으로는 고급 통신 시스템에 대한 수요 증가, 위성 발사 수 증가, 우주 분야 지출 증가 등이 있습니다. 위성 안테나는 위성의 송신 전력을 지구상의 지정된 지리적 영역에 집중시키고 신호 전체의 품질을 저하시키는 원치 않는 신호로부터의 간섭을 피하기 위해 사용됩니다. 통신, 방송, 내비게이션, 일기 예보 등 다양한 최종 용도의 위성 발사 증가가 이 부문의 성장을 이끌고 있습니다.

- 미국 우주국(UNOOSA)은 2022년 11월에 155회의 궤도상 및 서브오비탈 발사가 이루어졌습니다고 발표했습니다. 또한 2022년 6월 위성산업협회(SIA)는 제25회 위성산업현황보고(SSIR)를 발표했습니다. 이 보고서에 따르면 2021년 상업위성 배치 수는 1,713대와 2020년 대비 40% 이상의 현저한 급증을 보였습니다. 이 위성 수요 증가는 위성 구성요소에 대한 대응 요구를 야기하고 예측 기간 동안 시장 성장을 가속합니다. 그 예로는 2022년 7월에 MDA Ltd.가 위성 제조업체 York Space Systems와 위성용 Ka 밴드 스티어러블 안테나의 건설 계약을 체결한 것을 들 수 있습니다.

예측기간 중 북미가 시장에서 상위를 차지

- 북미가 위성용 컴포넌트 시장을 독점하고 예측 기간 동안에도 그 지배는 계속됩니다. 미국 항공우주국(NASA)과 SpaceX에 의한 우주 연구 개발에 대한 지출 증가와 위성 발사 수 증가가 배경에 있습니다. 2022년 미국 정부는 우주 프로그램에 약 620억 달러를 지출해 세계에서 가장 우주 지출이 많은 나라가 되었습니다. 2022년에는 세계에서 180회의 로켓 발사가 성공해, 그 중 76회는 미국이 발사했습니다.

- 예를 들어, 2021년 9월 미국 위성 제조 회사인 Terran Orbital은 플로리다의 스페이스 코스트에 3억 달러를 투자하여 세계 최대 위성 제조 및 부품 시설을 개설한다고 발표했습니다. 게다가 2021년 12월, Redwire Corporation은 위성 제조 회사 Terran Orbital과 3년간공급업체 계약을 체결해, 위성 제조 및 서비스 제공에 사용되는 다양한 첨단 부품이나 솔루션을 제공하게 되었습니다.

위성용 컴포넌트 산업 개요

위성용 컴포넌트 시장은 소수의 기업이 큰 점유율을 차지하며 적당히 통합되어 있습니다. 유명한 시장 기업으로는 THALES, Viking Satcom, Lockheed Martin Corporation, Northrop Grumman Corporation, Honeywell International Inc. 등이 있습니다. 경쟁이 치열해짐에 따라 주요 상대방 상표 제품 제조업체(OEM)는 우주 용도의 고급 위성 구성 요소 및 시스템의 설계 및 개발에 주력하고 있습니다. 차세대 위성의 안테나, 중계기, 추진 시스템 등의 연구개발 및 설계개발에 대한 지출 증가는 향후 수년간 더 좋은 기회를 창출할 것으로 보입니다.

예를 들어, 2021년 10월, 유럽 우주 기관(ESA), 프랑스 우주 기관 CNES, 위성 제조업체인 Thales Alenia Space는 궤도에서 대형 위성의 온도를 유지하는 냉각 시스템을 공동 개발할 것이라고 발표했습니다. 대형 상업 통신 위성에 사용되는 최초의 기계식 펌프 루프입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자·소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 컴포넌트

- 안테나

- 전력 시스템

- 추진 시스템

- 트랜스폰더

- 기타 부품(센서, 열제어 시스템 등)

- 지역

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Lockheed Martin Corporation

- Viking Satcom

- Sat-lite Technologies

- Honeywell International Inc.

- THALES

- Northrop Grumman Corporation

- IHI Corporation

- BAE Systems plc

- Challenger Communications

- JONSA TECHNOLOGIES CO., LTD.

- Accion Systems

제7장 시장 기회와 앞으로의 동향

JHS 24.03.04The Satellite Component Market size is estimated at USD 3.16 billion in 2024, and is expected to reach USD 4.37 billion by 2029, growing at a CAGR of 6.70% during the forecast period (2024-2029).

Key Highlights

- The global satellite component market has faced unprecedented challenges due to the COVID-19 pandemic. The space sector witnessed challenges such as shortages of raw materials, delayed satellite launch programs, and supply chain disruptions due to strict regulations imposed by governments. The market showcased a strong recovery after the pandemic. An increase in expenditure on the space sector and rising small satellite launches drive the market growth post-covid.

- The satellite components consist of the communications system, power systems, power systems, and others. The communication system includes antennas and transponders that receive and retransmit signals. The propulsion system consists of rockets that propel the satellite, and the power system includes solar panels that provide power. An increasing number of satellite launches and growing expenditure on the space sector drive the market growth. According to the United Nations Office for Outer Space Affairs (UNOOSA) index, in 2022, there were 8,261 individual satellites orbiting the Earth, with an increase of 11.84% compared to April 2021.

Satellite Component Market Trends

The Antenna Segment is Expected to Show Remarkable Growth During the Forecast Period

- The antenna segment is projected to show significant growth during the forecast period. The growth is due to increasing demand for advanced communication systems, rising number of satellite launches, and rising spending on the space sector. Satellite antennas are used to concentrate the satellite's transmitting power to the designated geographical region on Earth and avoid interference from undesired signals that will deteriorate the overall quality of the signal. Increasing satellite launches for various end-use applications such as communications, broadcasting, navigation, weather forecasting, and others drive the growth of the segment.

- The United Nations Office for Outer Space Affairs (UNOOSA) stated that 155 orbital and suborbital launches took place in November 2022. Moreover, in June 2022, the Satellite Industry Association (SIA) unveiled the 25th annual State of the Satellite Industry Report (SSIR). The report indicated a remarkable deployment of 1,713 commercial satellites in 2021, reflecting a notable surge of over 40 percent compared to 2020. This escalating demand for satellites is set to trigger a corresponding need for satellite components, thereby propelling market growth in the projected period. As an illustration, a significant development took place in July 2022 when MDA Ltd. entered into a contract with York Space Systems, a satellite manufacturer, to construct Ka-Band steerable antennas for satellites.

North America Held Highest Shares in the Market During the Forecast Period

- North America dominated the satellite components market and continued its domination during the forecast period. An increase in spending on space research and development and a rising number of satellite launches from the National Aeronautics and Space Administration (NASA) and SpaceX. In 2022, the United States government spent approximately USD 62 billion on its space programs and making the country with the highest space expenditure in the world. There were 180 successful rocket launches worldwide in 2022, out of which 76 were launched by the United States.

- For instance, in September 2021, Terran Orbital, a satellite manufacturing company in the United States, announced that it would open the world's largest satellite manufacturing and component facility on Florida's Space Coast at a cost of USD 300 million. Furthermore, in December 2021, Redwire Corporation signed a three-year supplier agreement with Terran Orbital, a satellite manufacturer, to provide a range of advanced components and solutions used in satellite manufacturing and service offerings.

Satellite Component Industry Overview

The satellite component market is moderately consolidated in nature, with a handful of players holding significant shares in the market. Some prominent market players are THALES, Viking Satcom, Lockheed Martin Corporation, Northrop Grumman Corporation, and Honeywell International Inc. With the growing competition, major original equipment manufacturers (OEMs) are focusing on the design and development of advanced satellite components and systems for space applications. Growing expenditure on research and development and design and development of next-generation satellite antennas, transponders, propulsion systems, and others will create better opportunities in the coming years.

For instance, in October 2021, the European Space Agency (ESA), French space agency CNES and Thales Alenia Space, a satellite manufacturer, announced it would jointly develop a cooling system that will maintain the temperature of big satellites in orbit. It will be the first mechanically pumped loop to be used on large commercial telecommunications satellites.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Component

- 5.1.1 Antennas

- 5.1.2 Power Systems

- 5.1.3 Propulsion Systems

- 5.1.4 Transponders

- 5.1.5 Other Components (Sensors, Thermal Control Systems, etc)

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Lockheed Martin Corporation

- 6.1.2 Viking Satcom

- 6.1.3 Sat- lite Technologies

- 6.1.4 Honeywell International Inc.

- 6.1.5 THALES

- 6.1.6 Northrop Grumman Corporation

- 6.1.7 IHI Corporation

- 6.1.8 BAE Systems plc

- 6.1.9 Challenger Communications

- 6.1.10 JONSA TECHNOLOGIES CO., LTD.

- 6.1.11 Accion Systems