|

시장보고서

상품코드

1433795

특수 실리카 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Specialty Silica - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

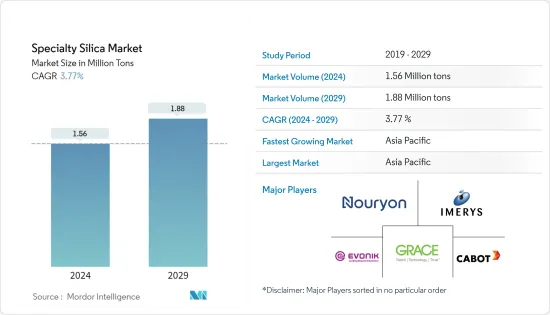

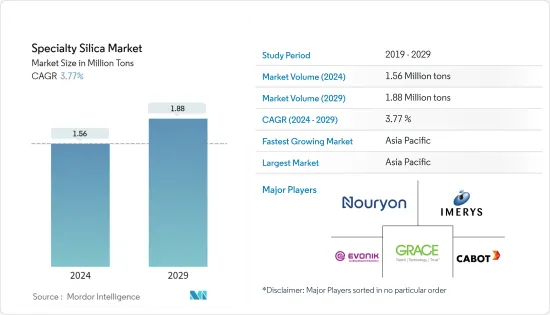

세계의 특수 실리카 시장 규모는 2024년에 156만 톤에 달하며, 2024-2029년의 예측 기간 중 CAGR 3.77%로 성장하며, 2029년에는 188만 톤 달할 것으로 예측됩니다.

COVID-19는 시장에 부정적인 영향을 미쳤습니다. 팬데믹 시나리오로 인해 전 세계 여러 정부가 바이러스 확산을 막기 위해 봉쇄 조치를 취했습니다. 수많은 기업과 공장이 폐쇄되어 세계 공급망이 혼란에 빠졌습니다. 그러나 시장은 COVID-19 팬데믹에서 회복되어 빠르게 성장하고 있습니다.

주요 하이라이트

- 고무 산업 수요 증가가 시장 성장을 주도하고 있습니다. 또한 퍼스널케어 제품에서 특수 실리카의 사용 확대도 시장 성장을 촉진하고 있습니다.

- 그러나 특수 실리카의 고가의 특성과 대체 제품의 가용성이 시장 성장에 걸림돌이 될 것으로 예상됩니다.

- 그럼에도 불구하고, 그린 타이어의 성장세는 향후 시장에 호재로 작용할 것으로 예상됩니다.

- 아시아태평양은 예측 기간 중 특수 실리카의 가장 크고 가장 빠르게 성장하는 시장이 될 것으로 예상됩니다.

특수 실리카 시장 동향

고무업계 수요 증가

- 특수 실리카는 일반적으로 액체 실리콘 고무(LSR) 및 고온 가황 고무(HTV)에 사용되며, 높은 기계적 강도와 우수한 전기 절연성이 요구됩니다.

- 산업용 고무 제품에서 특수 실리카는 컨베이어 벨트의 히스테리시스 손실을 줄이거나 유색 고무 입자 및 접촉성이 좋은 제품의 활성 필러로 사용됩니다.

- 미국 경제 분석국에 따르면 2022년 중 국가별 고무 제품(플라스틱 제품 포함)의 부가가치는 3,820억 달러 이상으로 전년도 부가가치를 약 11% 초과했습니다.

- 특수 실리카는 순도가 매우 높고 흡습성이 낮기 때문에 주로 타이어 제조용 고무에 사용됩니다. 고무 제품보다 전기적 특성이 우수합니다.

- 북미에서는 OICA(Organisation Internationale des Constructeurs d'Automobiles)에 따르면 2022년 자동차 생산량은 1,480만 대로 2021년 생산량 1,340만 대에 비해 9.88% 증가할 것으로 예상했습니다. 증가했습니다.

- 또한 OICA에 따르면 2022년 독일 자동차 생산량은 3억 7천만 대로 2021년 동기 3억 3천만 대에 비해 11% 증가했습니다.

- Modern Tire Dealer에 따르면 2022년 미국 타이어의 총 출하량은 약 3억 3,500만 개로, 2022년 출하된 타이어의 대부분은 교체용 승용차 타이어로 약 2억 2,200만 개에 달할 전망입니다. 타이어 산업 증가는 결국 고무 산업 수요를 증가시켜 특수 실리카 시장에 이익을 가져다 줄 것으로 보입니다.

- 따라서 앞서 언급한 모든 요인들이 예측 기간 중 세계 시장을 촉진할 것으로 예상됩니다.

아시아태평양이 시장을 독점

- 예측 기간 중 아시아태평양이 특수 실리카 시장을 주도할 것으로 예상됩니다. 중국, 인도, 일본 등의 국가에서 타이어 제조, 산업용 고무 제조, 페인트 및 코팅, 퍼스널케어 산업 등의 용도에서 수요가 증가하고 있기 때문입니다.

- 세계 도료 및 코팅 산업 협회에 따르면 2022년 아시아태평양의 도료 및 코팅 산업은 630억 달러 규모에 달할 것으로 추산됩니다. 중국이 이 지역 시장을 장악하고 있으며, CAGR 5.8%로 성장하고 있으며, 2022년 중국 시장은 5.7% 성장할 것으로 예상됩니다. 현재 추세에 따르면 중국의 페인트 및 코팅 총 매출액은 2022년에 450억 달러 이상에 달할 것으로 예상됩니다. 동아시아에서 중국 시장 점유율은 78%로 가장 큽니다.

- 인도는 2022년 기준 세계 4위의 고무 소비국입니다. 인도의 1인당 고무 사용량은 현재 1.2kg이며, 전 세계에서는 3.2kg입니다. 인도 고무 산업은 약 12,000 루피(약 14억 달러)의 매출을 창출하고 있습니다. 타이어 부문은 인도 고무 생산량의 대부분을 소비하고 있으며, 전체 생산량의 절반 이상을 차지합니다.

- 일본의 Yokohama Rubber Company는 인도 고무 산업의 성장에 따라 2023년 미화 8,200만 달러(약 679억 루피)를 투자하여 현지 시장 수요 증가에 대응하기 위해 인도 승용차 타이어 생산 능력을 확대할 것이라고 발표함. Visakhapatnam의 생산시설은 2024년 말까지 완공되어 가동을 시작할 예정입니다.

- 또한 중국은 가장 큰 자동차 생산국이자 소비국입니다. China Association of Automobile Manufacturers(CAAM)의 보고서에 따르면 2022년 중국의 자동차 생산량은 전년 대비 약 3.4% 증가하여 2021년자동차 생산량이 2,608 만 대였던 반면 2022년에는 약 2, 702 만 대가 생산 될 것으로 예상됩니다. 702만 대가 생산되었습니다. 이러한 증가는 타이어 수요 증가로 이어져 특수 실리카 시장에 영향을 미칠 것입니다.

- 인도에서는 고무의 약 12%가 신발 생산에 사용됩니다. 인도 신발 산업은 향후 수년간 4.5%의 성장을 이룰 것으로 추정됩니다. 운동화 카테고리에서 운동화가 가장 많이 소비되는 품목으로, 전년 대비 1.5배의 급격한 증가를 보였습니다. 말레이시아의 대표적인 신발 브랜드인 Bata는 2023년 말까지 500개의 프랜차이즈 매장을 오픈할 계획을 세우고 있습니다.

- Malaysian Rubber Board에 따르면 말레이시아의 타이어 제품 수출은 2022년 상반기 8억 3,280만 MYR(∼1억 8,890만 달러)에서 8억 8,320만 MYR(∼2억 3,039만 달러)로 6% 증가하여 성장의 여지가 있습니다. 성장의 여지가 있습니다. 협의회는 수출을 촉진하기 위해 새로운 투자, 기술 발전, 환경 친화적인 제품에 더욱 집중하여 수출을 촉진하고자 합니다.

- 따라서 이러한 모든 시장 동향은 예측 기간 중 이 지역의 특수 실리카 시장 수요를 촉진할 것으로 예상됩니다.

특수 실리카 산업 개요

특수 실리카 시장은 세분화되어 있습니다. 시장 점유율 측면에서 현재 소수의 대기업이 시장을 독점하고 있습니다. 특수 실리카 시장의 주요 기업으로는 W. R. Grace & Co., Cabot Corporation, Imerys, Evonik Industries AG, Nouryon 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 촉진요인

- 고무 업계로부터의 수요 확대

- 퍼스널케어 제품에서 특수 실리카의 이용 증가

- 기타 촉진요인

- 억제요인

- 특수 실리카의 고가의 성질

- 시장에서 대체품의 가용성

- 업계 밸류체인 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- 경쟁의 정도

제5장 시장 세분화 : 시장 규모(수량 기반)

- 유형

- 침전 실리카

- 실리카 겔

- 흄드 실리카(Fumed Silica)

- 콜로이달 실리카

- 용융 실리카

- 용도

- 고무

- 퍼스널케어

- 식품·사료

- 화학제품

- 플라스틱

- 페인트, 코팅제, 잉크

- 금속·내화물

- 기타 용도

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합병사업, 제휴, 협정

- 시장 점유율(%)**/순위 분석

- 주요 기업의 전략

- 기업 개요

- 3 M(Ceradyne Inc.)

- Cabot Corporation

- Clariant

- Denka Company Limited

- Evonik Industries AG

- Fuji Silysia Chemical

- Fuso Chemical Co. Ltd

- Glassven C.A.

- Imerys

- Merck KGaA

- Nouryon

- Orisil

- Tata Chemicals

- W. R. Grace & Co.

- Wacker Chemie AG

제7장 시장 기회와 향후 동향

- 그린 타이어의 부상

- 기타 기회

The Specialty Silica Market size is estimated at 1.56 Million tons in 2024, and is expected to reach 1.88 Million tons by 2029, growing at a CAGR of 3.77% during the forecast period (2024-2029).

COVID-19 had a negative influence on the market. Because of the pandemic scenario, various governments around the world established lockdowns to prevent the virus from spreading. Numerous companies and factory closures had disrupted global supply networks. However, the market has recovered from the COVID-19 outbreak and is growing rapidly.

Key Highlights

- The growing demand from the rubber industry is notably driving market growth. Moreover, the increasing utilization of specialty silica in personal care products is also pushing the market forward.

- However, the expensive nature of specialized silica and the availability of substitute products is expected to hinder market growth.

- Nevertheless, the growing emergence of green tires is projected to act as an opportunity for the market in the future.

- The Asia-Pacific region is expected to be the largest and fastest-growing market for specialty silica during the forecast period.

Specialty Silica Market Trends

Increasing Demand from the Rubber Industry

- Specialty silica is commonly used in Liquid Silicone Rubber (LSR) and High-Temperature Vulcanized (HTV) rubber, which requires high mechanical strength and good electrical insulation.

- In industrial rubber goods, specialty silica is used for reducing hysteresis loss in conveyor belts or as an active filler in colored rubber particles or in products with good contact.

- According to the United States Bureau of Economic Analysis, the value added by rubber products (plastic products included) in the country during 2022 was more than USD 382 billion, approximately 11% more than the value added during the previous year.

- Specialty Silica is mainly used in rubber for tire production due to its extremely high purity and low moisture absorption. It has superior electrical properties to rubber products.

- In North America, according to the Organisation Internationale des Constructeurs d'Automobiles (OICA), automotive production in 2022 accounted for 14.8 million units, an increase of 9.88% compared to the production in 2021, which was reported to be 13.4 million units.

- Further, OICA also stated that, in 2022, Germany produced 3.7 million vehicles which increased by 11% compared to 3.3 million vehicles in the same period in 2021, thereby indicating an increased demand for tires from the automotive industry.

- According to the Modern Tire Dealer, in 2022, overall shipments of United States tires amounted to around 335 million units. The majority of tire units shipped in 2022 were replacement passenger tires, with some 222 million units. The increasing tire industry would eventually enhance the demand from the rubber industry, thereby benefiting the specialty silica market.

- Therefore, all the aforementioned factors are expected to drive the global market during the forecast period.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is expected to dominate the market for specialty silica during the forecast period. In countries like China, India, and Japan, owing to the increasing demand from applications such as tire manufacturing, industrial rubber manufacturing, paints and coatings, and the personal care industry.

- In 2022, according to the World Paint & Coatings Industry Association, the Asia-Pacific paints and coatings industry was estimated to be worth USD 63 billion. China dominated the region's market, which is growing at a CAGR of 5.8%. In 2022, the Chinese market is expected to have grown by 5.7%. According to current trends, China's total sales of paints and coatings exceeded USD 45 billion in 2022. In East Asia, the country had the largest market share of 78%.

- India is the fourth-largest consumer of rubber in the world as of 2022. Rubber usage per capita in India is currently 1.2 kilograms, compared to 3.2 kilograms globally. The rubber industry in India generates revenue of approximately INR 12 thousand crores (~USD 1.4 billion). The tire sector consumes the majority of India's rubber production, accounting for over half of the country's total output.

- Owing to the growing rubber industry in the country, in 2023, Yokohama, the Indian arm of the Japanese Yokohama Rubber Company, announced that it would invest USD 82 million (~INR 679 crore) to expand its passenger car tire production capacity in India to meet the rising demands from the local market. The production facility at Visakhapatnam will be completed and start operations by the end of 2024.

- Moreover, China is the largest producer and consumer of automotive vehicles. The China Association of Automobile Manufacturers (CAAM) reported that, compared to the prior year, China's automobile production increased by about 3.4% in 2022. In comparison to the 26.08 million automobiles produced in the year 2021, around 27.02 million were produced in 2022. This increase would lead to growth in the demand for tires in the industry thereby impacting the specialty silica market.

- In India, about 12% of rubber is used to produce footwear. The Indian footwear industry is estimated to grow at 4.5% in the coming years. Under the sports footwear category, running shoes are the most consumed category, with a 1.5X spike compared to the previous year. Bata, one of the leading footwear brands in the country, has set out a plan to open 500 new franchise stores by the end of the year 2023.

- According to the Malaysian Rubber Board, Malaysia's exports have room for growth in terms of tire products as they registered a 6% increase from MYR 832.8 million (~USD 188.9 million) to MYR 883.2 million (~USD 200.39 million) during the first half of 2022. The council is trying to focus more on new investments, technological advances, and greener products to boost the country's exports.

- Hence, all such market trends are expected to drive the demand for the specialty silica market in the region during the forecast period.

Specialty Silica Industry Overview

The specialty silica market is fragmented in nature. In terms of market share, few of the major players currently dominate the market. Some of the key players in the specialty silica market include W. R. Grace & Co., Cabot Corporation, Imerys, Evonik Industries AG, and Nouryon, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Rubber Industry

- 4.1.2 Increasing Utilization of Specialty Silica in Personal Care Products

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Expensive Nature of Specialized Silica

- 4.2.2 Availability of Substitute Products in the Market

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Precipitated Silica

- 5.1.2 Silica Gel

- 5.1.3 Fumed Silica

- 5.1.4 Colloidal Silica

- 5.1.5 Fused Silica

- 5.2 Application

- 5.2.1 Rubber

- 5.2.2 Personal Care

- 5.2.3 Food and Feed

- 5.2.4 Chemicals

- 5.2.5 Plastics

- 5.2.6 Paints, Coatings and Inks

- 5.2.7 Metal and Refractories

- 5.2.8 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M (Ceradyne Inc.)

- 6.4.2 Cabot Corporation

- 6.4.3 Clariant

- 6.4.4 Denka Company Limited

- 6.4.5 Evonik Industries AG

- 6.4.6 Fuji Silysia Chemical

- 6.4.7 Fuso Chemical Co. Ltd

- 6.4.8 Glassven C.A.

- 6.4.9 Imerys

- 6.4.10 Merck KGaA

- 6.4.11 Nouryon

- 6.4.12 Orisil

- 6.4.13 Tata Chemicals

- 6.4.14 W. R. Grace & Co.

- 6.4.15 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Emergence of Green Tires

- 7.2 Other Opportunities