|

시장보고서

상품코드

1435922

폴리머 태양전지 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2024-2029년)Polymer Solar Cells - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

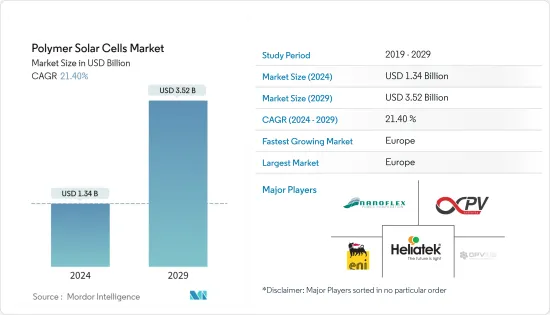

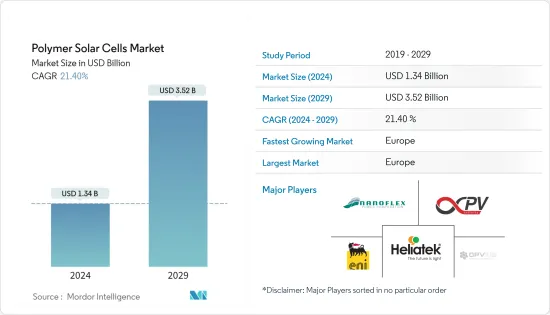

폴리머 태양전지 시장 규모는 2024년에 13억 4,000만 달러로 추정되고 2029년까지 35억 2,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간(2024-2029년) 중 21.40%의 CAGR로 성장합니다.

주요 하이라이트

- 장기적으로는 변환 효율을 높이기 위한 고분자 태양전지 기술의 기술 발전이 예측 기간 중 시장을 주도할 것으로 예상됩니다.

- 반대로 폴리머 태양전지는 실리콘 태양전지에 비해 효율이 낮기 때문에 예측 기간 중 시장 성장을 저해할 것으로 예상됩니다.

- 그럼에도 불구하고, 더 높은 변환 효율을 가진 새로운 폴리머 개발에 대한 연구개발은 예측 기간 중 시장에 중요한 성장 기회가 될 것으로 예상됩니다.

고분자 태양전지 시장 동향

시장을 주도하는 기술 발전

- 유기 광전지(OPV)라고도 불리는 고분자 태양전지는 유기 고분자 층을 사용하여 빛을 전기로 변환하는 3세대 태양광 전지입니다. 폴리머 태양전지는 가볍고 유연하며 사용자 정의가 가능하며 환경에 미치는 부정적인 영향이 적습니다.

- 2022년 세계 태양광발전 기술의 총 설치 용량은 약 1046.61GW로 2017년 390.87GW에 비해 167.7% 가까이 증가했습니다. 최근 수년간 PV 기술의 급속한 발전으로 폴리머 태양전지는 2022년에 18.42%의 효율을 달성했습니다. 실험실 상황. 효율성을 더욱 높이기 위해 분자 구조가 다른 다양한 조직에서 집중적인 연구를 수행하고 있으며 가까운 미래에 태양 광 시장에 침투할 것으로 예상됩니다.

- 폴리머 태양전지는 경량, 저비용, 투명성, 긴 수명(5000 시간 이상) 등 실리콘 태양전지에 비해 몇 가지 장점이 있지만 에너지 변환이 낮기 때문에 효율적인 상업적 용도가 매우 제한적입니다.

- Solarmer Energy Inc.에 따르면 현재 고분자 태양전지의 효율은 기술 개선을 통해 시간이 지남에 따라 개선될 것으로 추정되며, 이는 효율적인 고분자 분자 구조를 제공하여 고분자 태양전지가 실리콘 기반 태양전지에 비해 시장 경쟁력을 높일 수 있을 것으로 기대되고 있습니다. 그리고 기타 대체 태양전지 기술이 예측 기간 중 시장을 주도할 것으로 예상됩니다.

유럽이 시장을 독점할 가능성이 높음

- 유럽은 태양광발전 기술의 가장 큰 시장 중 하나이며, 2017년 109.98GW에서 2022년 기준 약 225.47GW의 태양광발전 설비가 설치될 것으로 예상됩니다. 기술의 발전과 함께 이 지역에서는 더 저렴하고 유연한 태양광 패널을 실현하기 위해 다양한 연구 프로젝트가 진행되고 있습니다. 여러 표면에 설치할 수 있습니다.

- Heliatek GmbH 및 OPVIUS GmbH와 같은 회사는 폴리머 태양전지를 개발하고 있으며, 이 지역에서 몇 가지 프로젝트를 시연하고 있습니다.

- 가장 큰 고분자 또는 유기 태양전지 프로젝트는 프랑스에서 진행되었습니다. 이를 BiOPV(Building Integrated Organic Photovoltaic)라고합니다. 이 프로젝트는 약 23.8MWh의 전력을 생산하는 약 500 평방미터의 지붕에 유기 태양 광 발전을 설치하는 것을 포함합니다.

- 2023년 현재 이 지역에는 몇 가지 다른 연구개발 프로젝트가 진행 중입니다. 2023년 10월, 프랑스와 스페인 연구팀은 고처리 사출성형을 통해 플라스틱 부품에 내장된 유기 태양광 모듈을 개발했습니다. 연구진은 열가소성 폴리우레탄을 모듈에 주입한 결과, 높은 유연성을 유지하면서 기계적 안정성이 향상된 것을 발견했습니다. 연구진은 먼저 P3HT:O-IDTBR로 알려진 광활성 블렌드를 사용하여 롤투롤 인쇄로 모듈을 제작했습니다. 이 블렌드는 이후 사출성형 공정과 관련된 형태학적 안정성과 열 안정성을 고려하여 선택되었습니다. 다양한 분야와 용도에서 연구개발이 완료됨에 따라 예측 기간 중이 지역 시장이 확대될 것으로 예상됩니다.

고분자 태양전지 산업 개요

고분자 태양전지 시장은 통합될 것입니다. 시장의 주요 기업으로는(무순서) Eni SpA, NanoFlex Power Corporation, Infinity PV, OPVIUS GmbH, Heliatek GmbH 등이 있습니다.

Eni의 조사는 통합형 태양광발전의 시야를 넓히는 기술을 개발했습니다. 페로브스카이트 전지는 유기 태양전지와 함께 재료비 및 생산 기술을 줄이고 반투명 박막으로 제작할 수 있으며, 건물 외벽에 매립하는 등 기존 태양전지로는 불가능했던 용도가 가능해졌습니다. 특히 이러한 용도는 최근 건물 에너지 효율 분야의 국제 지침 및 EU 지침에 의해 촉진되고 있습니다. 따라서 광범위한 응용이 기대됩니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 서론

- 2028년까지 시장 규모와 수요 예측

- 최근 동향과 발전

- 정부의 정책과 규제

- 시장 역학

- 촉진요인

- 억제요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 교섭력

- 신규 진출업체의 위협

- 대체품 및 서비스의 위협

- 경쟁 기업간 경쟁의 강도

제5장 시장 세분화

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 영국

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트

- 남아프리카공화국

- 북미

제6장 경쟁 구도

- 합병과 인수, 합병사업, 협업 및 계약

- 유력 기업이 채택한 전략

- 기업 개요

- Solarmer Energy Inc.

- NanoFlex Power Corporation

- Infinity PV

- OPVIUS GmbH

- Heliatek GmbH

- Eni SpA

제7장 시장 기회와 향후 동향

KSA 24.03.07The Polymer Solar Cells Market size is estimated at USD 1.34 billion in 2024, and is expected to reach USD 3.52 billion by 2029, growing at a CAGR of 21.40% during the forecast period (2024-2029).

Key Highlights

- Over the long term, technological advancements in polymer solar cell technology aimed at increasing conversion efficiency are expected to drive the market during the forecast period.

- On the flip side, the lower efficiency of polymer solar cells as compared to silicon solar cells is expected to hinder market growth during the forecasting period.

- Nevertheless, research and development into the development of new polymers with higher conversion efficiencies is expected to be a significant growth opportunity for the market beyond the forecast period.

Polymer Solar Cells Market Trends

Technological Advancements to Drive the Market

- Polymer solar cells, also called organic photovoltaic (OPV), are third-generation PV cells that use an organic polymer layer to convert light into electricity. Polymer solar cells are lightweight, flexible, customizable, and have a less adverse environmental impact.

- In 2022, global solar PV technology had a total installed capacity of around 1046.61 GW, growing by nearly 167.7% from 390.87 GW in 2017. With rapid improvements in PV technology in recent years, polymer solar cells achieved an efficiency of 18.42% in 2022 under lab conditions. In order to further increase efficiency, various organizations with different molecular structures are performing intensive research and are expected to penetrate the solar PV market in the near future.

- Polymer solar cells have a few advantages over silicon solar cells, like being lighter in weight, cheaper in cost, transparent, and having a longer lifetime (greater than 5000 hrs), but due to their low energy conversion, efficient commercial applications are very limited.

- As per Solarmer Energy Inc., the present efficiency of polymer solar cells is estimated to improve over time due to technological improvement, which is expected to provide efficient polymer molecular structure and make polymer solar cells more competitive in the market with silicon-based solar cells and other alternative solar cell technologies, driving the market during the forecast period.

Europe is Likely to Dominate the Market

- Europe was one of the largest markets for solar PV technology, with around 225.47 GW of solar PV installations as of 2022, up from 109.98 GW in 2017. With technological advancements, the region is doing various research projects to achieve cheaper and more flexible solar panels that can be installed on multiple surfaces.

- Companies like Heliatek GmbH and OPVIUS GmbH are developing polymer solar cells and have demonstrated a few projects in the region.

- The largest polymer or organic solar cell project was in France. It is called the BiOPV (Building Integrated Organic Photovoltaic). The project includes the installation of organic photovoltaics on the roof of around 500 square meters that generate nearly 23.8 MWh of electricity.

- As of 2023, a few other R&D projects were going on in the region. In October 2023, a French-Spanish research team developed organic photovoltaic modules embedded into plastic parts through high throughput injection molding. The researchers injected thermoplastic polyurethane into the modules and found it enhanced their mechanical stability while keeping a high flexibility. The researchers first created modules in roll-to-roll printing using a photoactive blend known as P3HT: O-IDTBR. This blend was chosen due to its morphological and thermal stability, which are relevant to the later injection molding process. The completion of R&D in various sectors and applications is expected to expand the market in the region during the forecast period.

Polymer Solar Cells Industry Overview

The polymer solar cells market is consolidated. Some of the key players in the market (in no particular order) include Eni SpA, NanoFlex Power Corporation, Infinity PV, OPVIUS GmbH, and Heliatek GmbH, among others.

Eni's research developed a technology that widens the horizons of integrated photovoltaics. Together with organic photovoltaic cells, perovskite cells can be made in semi-transparent thin film with reduced material costs and production techniques, enabling applications that have hitherto been impossible for conventional solar cells, such as embedding on building facades. Among other things, this application is promoted by recent international and EU directives in the area of energy efficiency for buildings. It is, therefore, destined to have an extensive range of uses.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecasts in USD million, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Geography

- 5.1.1 North America

- 5.1.1.1 United States

- 5.1.1.2 Canada

- 5.1.1.3 Mexico

- 5.1.2 Europe

- 5.1.2.1 Germany

- 5.1.2.2 France

- 5.1.2.3 United Kingdom

- 5.1.2.4 Rest of Europe

- 5.1.3 Asia-Pacific

- 5.1.3.1 China

- 5.1.3.2 India

- 5.1.3.3 Japan

- 5.1.3.4 South Korea

- 5.1.3.5 Rest of Asia-Pacific

- 5.1.4 South America

- 5.1.4.1 Brazil

- 5.1.4.2 Argentina

- 5.1.4.3 Rest of South America

- 5.1.5 Middle-East and Africa

- 5.1.5.1 Saudi Arabia

- 5.1.5.2 United Arab Emirates

- 5.1.5.3 South Africa

- 5.1.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Solarmer Energy Inc.

- 6.3.2 NanoFlex Power Corporation

- 6.3.3 Infinity PV

- 6.3.4 OPVIUS GmbH

- 6.3.5 Heliatek GmbH

- 6.3.6 Eni SpA