|

시장보고서

상품코드

1436025

차세대 임플란트 : 세계 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2024-2029년)Global Next-generation Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

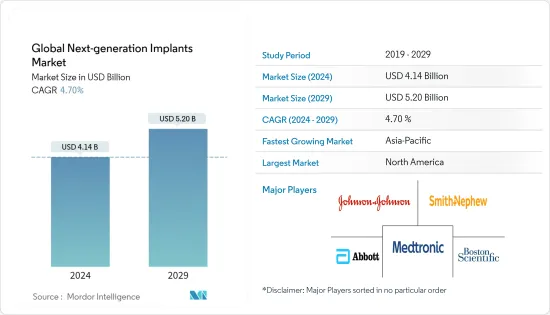

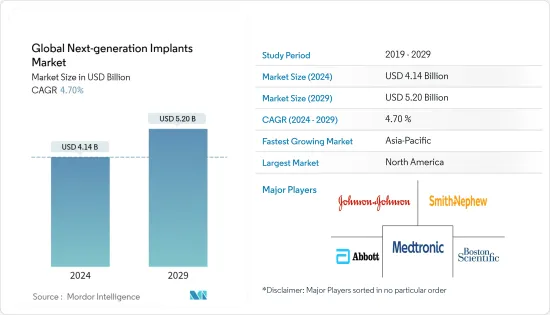

세계의 차세대 임플란트 시장 규모는 2024년 41억 4,000만 달러로 추정되고, 2029년까지 52억 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 4.70%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

COVID-19의 팬데믹에 의해, 감염자수가 증가하면서, 세계 대부분의 인구 이동 및 교통 시스템을 차단하였습니다. 대부분의 국가에서도 여행 제한이 실시되어 의료 서비스의 저하로 이어졌습니다. 대기 수술이 감소함에 따라 병원 및 진료소의 진찰 수가 줄어 차세대 의료용 임플란트 시장에 영향을 미쳤습니다. 임플란트 제조업체는 자원 부족, 수요 및 공급망 변화, 지난 수십년의 성장률에 비해 수익 감소 등 많은 과제에 직면해 있습니다. 차세대 임플란트 시장은 단기적으로 COVID-19의 팬데믹에 의해 방해되었습니다. 예를 들어, 2022년 8월에 게재된 「COVID-19 팬데믹 봉쇄중의 인공내이 수술-푸네의 KEM병원에서의 경험」이라고 하는 타이틀의 기사에 의하면, COVID-19의 팬데믹 중, 의료 자원을 COVID- 19로 돌아가기 위해 인공 내이와 같은 선택적 수술은 연기되었다고 합니다. 그러나 COVID-19의 중증도가 감소함에 따라 차세대 임플란트 시장은 COVID-19 팬데믹 이후 다시 높은 성장률을 보일 것으로 예상됩니다.

고령화 인구 증가, 평균 수명의 연장, 노화에 따른 질병 증가가 차세대 임플란트 시장의 성장에 기여하고 있습니다. 고령자는 심혈관 질환, 정형외과 질환, 치아 변성 질환에 걸리기 쉽기 때문에 차세대 임플란트 수요가 높아지고 있습니다. 2021년 10월에 발표된 세계보건기구(WHO)의 노화와 건강에 관한 보고서에 따르면 2015년부터 2050년 사이에 세계 인구에서 차지하는 60세 이상의 비율은 12%에서 22%로 거의 배증할 것으로 전망합니다. 이 보고서는 2020년에는 60세 이상의 인구가 5세 미만의 어린이 인구를 초과한다고 추정합니다. 또한 같은 정보원에 따르면 고령자 인구의 약 80%가 저중산계급에서 살게 될 것으로 예상되고 있습니다. 노인 인구가 증가함에 따라 혁신적인 치료법에 대한 수요가 더욱 증가할 것으로 예상되고 있으며, 이로 인해 세계 차세대 임플란트 시장의 성장이 가속될 것으로 예상됩니다. 게다가 세계 인구 고령화 2020년에 따르면, 가장 많이 증가하는 것은 동아시아와 동남아시아로, 2020년 2억 6,100만명에서 2050년에는 5억 7,300만명으로 증가할 것으로 예측되고 있습니다. 노인의 수가 가장 빠르게 증가하는 것은 북아프리카와 서아시아로, 2020년 2,900만 명에서 2050년에는 9,600만 명으로 증가할 것으로 예상됩니다.

또 다른 요인은 세계적으로 변성 질환의 만연과 만성 질환의 부담이 증가하고 있다는 것입니다. 2022년 6월에 발표된 신경퇴행성 질환에 관한 국립보건연구소의 논문에 따르면, 2022년에는 미국에서 620만명 이상의 성인이 알츠하이머병에 걸린 것으로 추정되며, 100만명 이상의 성인이 파킨슨 병에 걸린 것으로 추정됩니다. 황반 변성은 퇴행성 질환에 크게 기여합니다.

게다가, 기술의 진보는 이전 제품보다 단순화된 의료용 임플란트를 개발하고 소개합니다. 현재 다양한 기업들이 생체 흡수성 스텐트, 제세동기, 개인화된 인공관절 치환술, 리드레스페이스메이커 등 보다 고급 임플란트를 제공합니다. 이로 인해 조작성이 향상되고 배터리 수명이 연장되고 임베디드 후에도 환자가 정상적인 활동을 계속할 수 있습니다. 시장 관계자의 혁신은 시장 성장을 가속하는 주요 요인입니다. 예를 들어, 2021년 6월, 메드트로닉 PLC는 고성능 충전식 임베디드 신경 자극 장치인 Vanta에 대해 미국 식품의약국(FDA)의 인가를 취득했습니다. 신제품 출시로 예측 기간 동안 조사 대상 시장의 성장이 더욱 가속될 것으로 예상됩니다.

그러나 조사 대상 시장의 성장을 방해하는 주요 요인은 차세대 임플란트의 높은 비용 및 임플란트에 대한 엄격한 규제 정책입니다.

차세대 임플란트 시장 동향

정형외과용 임플란트 부문은 예측 기간 동안 시장의 상당한 점유율을 차지할 것으로 예상됩니다.

정형외과 임플란트는 누락되거나 손상된 뼈 또는 관절을 대체하거나 지원하도록 설계된 인공 뼈 또는 관절입니다. 이 임플란트는 이상을 수정하고 신체 자세를 개선하도록 설계되었습니다. 골다공증, 골관절염 및 기타 근골격계 문제의 위험을 증가시키는 노인 인구 증가는 이 부문 시장 성장의 주요 요인 중 하나입니다. 예를 들어 2022년 1월 'Climacteric' 잡지에 게재된 'Bone health 2022 : an update'라는 제목의 기사에 따르면, 골다공증은 전 세계적으로 연간 890만 건 이상의 골절을 일으키고 있으며, 3초마다 골다공증에 의한 골절이 발생하고 있다고 합니다. 이 기사는 세계 2억 명의 여성이 골다공증을 앓고 있음을 보여주었습니다. 또한, 2022년 5월에 발표된 2022년 골다공증 계발 월간에 관한 미국 생화학 및 분자 생물학 협회의 기사에 따르면, 골다공증은 300만건의 골절의 원인이 되어, 2025년 말까지 매년 253억 달러의 비용이 발생할 것으로 예상됩니다. 이러한 통계에 따르면 정형외과 수술의 수가 증가하고 향후 수년간 정형외과용 임플란트 수요가 증가할 것으로 예상됩니다.

또한 관절치환술의 진보와 정형외과용 임플란트의 연구개발 활동에 있어서 주요 시장 진입기업에 의한 투자 증가 등 여러 요인이 부문의 성장을 추진하고 있습니다. 예를 들어, 정형외과용 차세대 기술 플랫폼인 Intelligent Implants Ltd의 SmartFuse Implant 기술은 2021년 6월 미국 식품의약국(FDA)의 획기적인 장치 지정을 받았습니다. 정형외과용 임플란트 부문은 2021년 급속히 확대될 것으로 예상됩니다. 이는 혁신적인 치료법, 저침습 치료에 대한 수요 증가 및 정형외과 임플란트에 대한 환자 지식 증가로 분석 기간이 단축되었기 때문입니다.

따라서, 상기 요인들에 의해 정형외과용 임플란트 부문은 예측 기간 동안 상당한 성장이 예상됩니다.

예측기간 중 북미가 차세대 임플란트 시장을 독점할 것으로 예상됩니다.

현재 북미는 차세대 임플란트 시장을 독점하고 있으며 예측 기간 동안에도 비슷한 경향을 따를 것으로 예상됩니다. 노인 인구 증가 추세, 만성 질환 유병률 증가, 라이프스타일 변화, 고급 의료 시설 이용 가능성은 차세대 임플란트 시장의 성장을 가속할 것으로 예상됩니다. 2021년 10월에 갱신된 미국 질병 예방관리센터(CDC)의 관절염에 관한 기사에 따르면, 국내 약 5,850만 명이 의사의 진단에 의한 관절염을 앓고 있습니다. 같은 출처에 따르면 2040년까지 미국 7,840만 명 이상의 성인이 관절염을 앓게 됩니다. 또한, 2021년 9월에 갱신된 관절염의 팩트 및 수치에 관한 캐나다 관절염 협회의 기사에 따르면, 2021년에는 약 600만명의 캐나다인이 관절염을 앓고 있는 것으로 판명되었고, 2040년까지 900 만명 이상의 관절염 환자가 발생할 것으로 추정됩니다. 관절염 증가는 예측 기간 동안 이 지역 시장 성장을 가속할 것으로 예상됩니다.

마찬가지로 기술 발전과 제품 개량은 이 지역의 성장을 가속할 것으로 예상됩니다. 예를 들어, 치과 및 척추 시장의 생명 과학 솔루션 제공업체인 ZimVie Inc.는 2022년 6월에 FDA 승인을 받은 새로운 T3 PRO 테이퍼드 임플란트와 인코딩 에머전스 힐링 어버트먼트를 미국에서 출시했습니다. 이 지역에서 이러한 제품을 출시하면 차세대 임플란트 시장의 성장이 더욱 가속화될 수 있습니다.

따라서 위의 요인으로 인해 조사 대상인 북미 시장은 예측 기간 동안 성장을 추진할 것으로 예상됩니다.

차세대 임플란트 산업 개요

차세대 임플란트 시장은 많은 시장 관계자가 시장의 성장 기회를 활용하기 위해 보다 효율적이고 비용 효율적인 임플란트 장치를 제공하기 위한 기술의 발전에 초점을 맞추고 있으며, 대부분 세분화되었습니다. 주요 기업의 일부는 세계 시장에서의 지위를 강화하기 위해 정력적으로 제휴, 합병 및 인수를 실시했습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제 조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 고령화 인구 증가

- 변성질환의 유병률 증가

- 차세대 임플란트의 기술 진보

- 시장 성장 억제요인

- 차세대 임플란트의 고비용

- 엄격한 규제 개혁

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체 제품의 위협

- 경쟁 기업간 경쟁 관계의 격렬

제5장 시장 세분화(금액별 시장 규모)

- 용도별

- 정형외과용 임플란트

- 심장혈관용 임플란트

- 안과용 임플란트

- 치과용 임플란트

- 기타

- 재료별

- 금속 및 금속 합금

- 세라믹

- 폴리머

- 생물제제

- 기타

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 정형외과 클리닉

- 학술기관 및 연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 세계 기타 지역

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Abbott Laboratories

- Smith &Nephew PLC

- Johnson &Johnson

- Boston Scientific Corporation

- CR Bard Inc.

- Medtronic PLC

- Wright Medical Group NV

- Stryker Corporation

- Globus Medical Inc.

- DENTSPLY SIRONA Inc.

- Zimmer Biomet Holdings Inc.

제7장 시장 기회 및 미래 동향

AJY 24.03.08The Global Next-generation Implants Market size is estimated at USD 4.14 billion in 2024, and is expected to reach USD 5.20 billion by 2029, growing at a CAGR of 4.70% during the forecast period (2024-2029).

The COVID-19 pandemic shut down population movements and transport systems across large parts of the world due to the rising COVID-19 cases. Most countries also implemented travel restrictions, which led to a decline in medical services. The number of visits to hospitals and clinics decreased with the decline in elective surgical procedures which impacted the next-generation medical implants market. The implant manufacturers encountered many challenges, including scarcity of resources, shifts in the supply and demand chain, and revenue decline compared to the growth rate in the past decades. The next-generation implant market was hindered by the COVID-19 pandemic in the short term. For instance, according to an article titled 'Cochlear Implant Surgery During the Covid Pandemic Lockdown-The KEM Hospital, Pune Experience' published in August 2022, during the COVID-19 pandemic elective surgeries such as cochlear implantation were postponed to divert medical resources to COVID-19 management. However, with the reducing severity of the COVID-19 infection, the next-generation implants market is expected to resume a strong growth rate post-COVID-19 pandemic.

The growing aging population, higher life expectancy, and an increase in the number of age-related disorders are contributing to the growth of the next-generation implant market. The geriatric population is more prone to cardiovascular, orthopedic, and dental degenerative conditions, which increases the demand for next-generation implants. According to the World Health Organization (WHO) report on Ageing and Health published in October 2021, between 2015 and 2050, the proportion of the world's population over 60 years will nearly double from 12% to 22%. The report estimated that the population of people over 60 years would have outnumbered the population of children below the age of 5 years in 2020. Also, as per the same source, about 80% of the geriatric population will be living in low- and middle-income countries by 2050. The growing older population is expected to further increase the demand for innovative treatment procedures, thereby, accelerating the growth of the next-generation implants market all around the world.Moreover, according to the World Population Ageing 2020, the largest increase is projected to occur in Eastern and South-Eastern Asia, growing from 261 million in 2020 to 573 million in 2050. The fastest increase in the number of older persons is expected in Northern Africa and Western Asia, rising from 29 million in 2020 to 96 million in 2050.

Another factor is the growing prevalence of degenerative disease and the burden of chronic disease globally. According to the National Health Institute's article on neurodegenerative diseases published in June 2022, over 6.2 million in the United States were estimated to be affected by Alzheimer's disease and over a million adults were estimated to be affected by Parkinson's in the year 2022. Age-related macular degeneration makes a significant contribution to degenerative disorders.

Additionally, technological advancements have been resulting in the development and introduction of medical implants that are more simplified than earlier available products. Various companies are currently offering more advanced implants, such as bioabsorbable stents, cardioverter-defibrillators, personalized joint replacements, and leadless pacemakers, which offer improved operation and extended battery life and allow patients to continue normal activities after implantation. The innovation by the market players is a major factor adding to the growth of the market. For instance, in June 2021, Medtronic PLC gained the United States Food and Drug Administration (FDA) clearance for Vanta, a high-performance rechargeable implantable neurostimulator. The novel product launches are expected to add to the growth of the studied market over the forecast period.

However, major restraining factors for the growth of the studied market are the high cost of next-generation implants and stringent regulatory policies for implants.

Next-generation Implant Market Trends

The Orthopedic Implants Segment is Expected to Occupy a Significant Share of the Market During the Forecast Period

Orthopedic implants are artificial bones or joints designed to replace or support a missing or injured bone or joint. These implants are designed to correct abnormalities and improve body posture. The rise in the geriatric population, which raises the risk of osteoporosis, osteoarthritis, and other musculoskeletal problems, is one of the major factors for the growth of the segment market. For instance, according to an article titled 'Bone health 2022: an update' published in the journal of 'Climacteric' in January 2022, osteoporosis causes more than 8.9 million fractures annually all over the world, resulting in an osteoporotic fracture every 3 seconds. The article indicated that osteoporosis affects 200 million women worldwide. Also, as per an article by the American Society for Biochemistry and Molecular Biology on Osteoporosis Awareness Month 2022 published in May 2022, osteoporosis will be responsible for three million fractures resulting in USD 25.3 billion in costs every year by the end of the year 2025. According to these statistics, the number of orthopedic surgeries is expected to increase, driving the demand for orthopedic implants in the coming years.

Additionally, several factors drive the segmental growth, such as advances in joint replacements and increased investment by key market participants in orthopedic implant research and development activities. For instance, Intelligent Implants Ltd's SmartFuse Implant technology, a next-generation technological platform for orthopedics, gained the United States Food and Drug Administration (FDA)'s breakthrough device designation in June 2021. The orthopedic implants segment is expected to expand rapidly during the analysis period, owing to increased demand for innovative therapies, minimally invasive procedures, and increased patient knowledge of orthopedic implants.

Therefore, owing to the above-mentioned factors, the orthopedic implants segment is expected to have a significant growth during the forecast period.

North America is Expected to Dominate the Next-generation Implant Market During the Forecasts Period

North America currently dominates the next-generation implants market and is expected to follow the same trend over the forecast period. The rising trend in the geriatric population, the rising prevalence of chronic disease, changing lifestyles, and the availability of advanced medical facilities are anticipated to boost the growth of the next-generation implant market. According to the article on arthritis by the United States Centers for Disease Control and Prevention (CDC) updated in October 2021, around 58.5 million people in the country were affected by doctor-diagnosed arthritis. As per the same source, by the year 2040, over 78.4 million adults in the United States will be affected by arthritis. Also, as per the Arthritis Society Canada article on arthritis facts and figures updated in September 2021, around 6 million Canadians were found to be affected by arthritis in 2021, with an estimate of over 9 million arthritis cases by the year 2040. The rising cases of arthritis are expected to boost the market growth in the region over the forecast period.

Similarly, technological advancement and improvement in the products are expected to boost growth in the region. For instance, in June 2022, ZimVie Inc., a life sciences solutions provider in the dental and spine markets, launched the new, FDA-cleared T3 PRO Tapered Implant and Encode Emergence Healing Abutment in the United States. Such product launches in the region are likely to add to the growth of the next-generation implant market.

Thus, owing to the above-mentioned factors, the studied market in North America is expected to propel over the forecast period.

Next-generation Implant Industry Overview

The next-generation implants market is mostly fragmented with many market players focusing on advancement in the technology to deliver more efficient and cost-effective implant devices to leverage growth opportunities in the market. Some of the major players are vigorously making collaborations, mergers, and acquisitions to consolidate the market position across the world. The several players in the next-generation implants market are Abbott Laboratories, Smith & Nephew PLC, Johnson & Johnson, Boston Scientific Corporation, C.R. Bard Inc., Wright Medical Group NV, Stryker Corporation, Globus Medical Inc., DENTSPLY SIRONA Inc., and Zimmer Biomet Holdings Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Aging Population

- 4.2.2 Growing Prevalence of Degenerative Disease

- 4.2.3 Technological Advancement in Next-generation Implants

- 4.3 Market Restraints

- 4.3.1 High Cost of Next Generation Implants

- 4.3.2 Stringent Regulatory Reforms

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - in USD Millions)

- 5.1 By Application

- 5.1.1 Orthopedic Implants

- 5.1.2 Cardiovascular Implants

- 5.1.3 Ocular Implants

- 5.1.4 Dental Implants

- 5.1.5 Other Applications

- 5.2 By Material

- 5.2.1 Metals and Metal Alloys

- 5.2.2 Ceramics

- 5.2.3 Polymers

- 5.2.4 Biologics

- 5.2.5 Other Materials

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Orthopedic Clinics

- 5.3.4 Academic and Research Institutes

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Smith & Nephew PLC

- 6.1.3 Johnson & Johnson

- 6.1.4 Boston Scientific Corporation

- 6.1.5 C.R. Bard Inc.

- 6.1.6 Medtronic PLC

- 6.1.7 Wright Medical Group NV

- 6.1.8 Stryker Corporation

- 6.1.9 Globus Medical Inc.

- 6.1.10 DENTSPLY SIRONA Inc.

- 6.1.11 Zimmer Biomet Holdings Inc.