|

시장보고서

상품코드

1437598

세계 장갑 차량 네비게이션 시스템 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Armored Vehicle Navigation Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

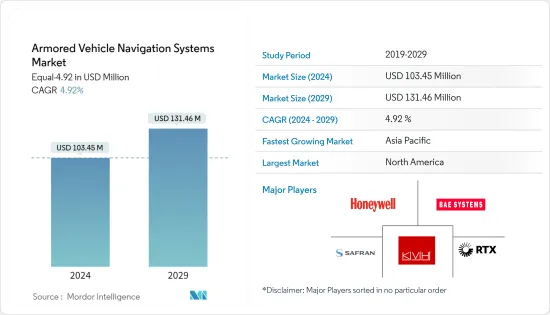

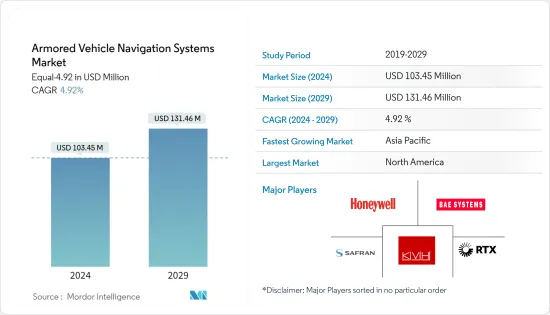

세계의 장갑차량 내비게이션 시스템 시장 규모는 2024년에 1억 345만 달러로 추정되며, 2029년에는 1억 3,146만 달러에 이르고, 예측기간 중(2024-2029년) CAGR 4.92%로 성장할 것으로 예상됩니다.

세계의 방위비 증가로 장갑차량 내비게이션 시스템 시장이 촉진되고 있습니다. 미국, 프랑스, 러시아 등 주요 국가와 인도, 중국 등 신흥국은 방위비를 급증시키고 있습니다. 이들 국가는 장갑차량의 개발과 조달에 많은 투자를 하고 있습니다. 또한, 함대의 전투 범위와 전투 효율을 향상시키기 위해, 장갑 차량 네비게이션 시스템의 분야에서 대폭적인 개발이 이루어지고 있습니다. 인공지능과 자율주행 차량 기술 등의 기술의 개발과 실장에 의해 장갑 차량 내비게이션 시스템 시장의 성장이 추진되고 있습니다.

장갑 차량 네비게이션 시스템 시장 동향

가장 높은 성장률을 나타내는 관성 내비게이션 시스템

세계 주요 군는 전장에서 전투 차량 부대의 상황 인식을 향상시키는 노력을 강화하고 있으며, 이것이 관성 내비게이션 시스템의 대폭적인 개선으로 이어지고 있습니다. 위성 포지셔닝 시스템과 관성 네비게이션 시스템의 통합은 세계 장갑 차량 네비게이션 시스템 시장 성장을 가속하고 있습니다. GPS가 거부된 영역에서도 정확하게 작동할 수 있는 기존 관성 내비게이션 기술을 개선하기 위해 투자가 이루어지고 있습니다. 관성 내비게이션 시스템은 방해나 스푸핑의 영향을 받기 쉬운 GPS 시스템과 달리 안전하고 정확합니다. 센서 기술의 개발은 관성 내비게이션 시스템 개발의 핵심입니다. 예를 들어, 2023년 11월 스웨덴에 본사를 둔 기업인 Kebni AB는 새로운 산업 협력의 일환으로 RV Connex로부터 Kebni SensAItion 관성 내비게이션 시스템(INS) 테스트 유닛을 수주했습니다. 이 주문은 고급 용도에서 내비게이션 지원을 평가하기 위한 테스트 유닛에 관한 것입니다.

센서의 사용이 증가함에 따라 장갑 차량 네비게이션 시스템의 무게와 공간을 줄이는 설계가 촉진되었습니다. 센서와 광섬유 자이로(FOG)는 관성 내비게이션 시스템의 불안정성을 줄이고 신뢰성을 높입니다. FOG 시스템은 자율주행차에 적용하여 예측기간 동안 높은 성장률을 보일 것으로 예상됩니다.

아시아태평양은 예측기간 동안 크게 성장할 것으로 예상

아시아태평양에는 일본, 중국, 인도, 한국 등의 군사대국이 있으며, 이들 국가들은 국경분쟁의 상승과 지역 테러에 의해 장갑차량과 장갑차량 내비게이션 시스템의 조달과 개발을 위한 국방지출을 대폭 로 증가하고 있습니다. 이 지역의 장갑 차량 조달은 내비게이션 시스템 수요를 돕고 있습니다. 예를 들어 2022년 12월 일본 방위성은 육상 자위대(JGSDF)의 장륜 장갑 병원 수송차(WAPC) 프로그램용으로 핀란드 기업 패트리아의 장갑 모듈러 차량(AMV)을 조달하는 5년 계획 개요를 발표했습니다. 이 나라는 29대, 1억 7,600만 달러 상당의 차량을 조달할 계획을 세우고 있습니다. 마찬가지로 2023년 9월 인도 국방부는 무한 궤도 플랫폼을 기반으로 170대의 장갑 회수 차량(ARV)을 조달하기 시작했습니다. 이러한 발전은 아시아태평양 시장을 지원할 것으로 기대됩니다.

장갑 차량 네비게이션 시스템 업계 개요

장갑 차량 내비게이션 시스템 시장은 반 통합 시장이며 Honeywell International Inc., KVH Industries Inc., Safran SA, RTX Corporation, BAE Systems PLC와 같은 대기업이 있습니다. 시장은 경쟁력 있는 저가로 제공할 수 있는 혁신과 정밀 기술 개발에 투자를 하고 있습니다. 수익 창출을 위해, 대기업은 각국 정부나 방위기관으로부터의 계약이나 거래를 획득하는 것을 목표로 하고 있습니다. 이 시장은 세계 주요 경제국의 방어 근대화와 업그레이드 노력으로 성장이 예상됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체 제품의 위협

- 경쟁 기업간 경쟁 관계의 격렬

제5장 시장 세분화

- 장갑 차량 유형

- 주력 탱크

- 보병 전투차

- 장갑 수송차

- 기타 장갑 차량 유형(전술 트럭, 버스, MRAP)

- 네비게이션 시스템

- 관성 내비게이션 시스템

- 위성 내비게이션 시스템

- 지역

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 라틴아메리카

- 멕시코

- 브라질

- 기타 라틴아메리카

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 이스라엘

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- Safran SA

- KVH Industries Inc.

- Hertz Systems

- Israel Aerospace Industries Ltd

- Bharat Electronics Limited(BEL)

- Advanced Navigation

- Honeywell International Inc.

- GEM elettronica

- BAE Systems PLC

- Northrop Grumman Corporation

- THALES

- RTX Corporation

제7장 시장 기회와 미래 동향

JHS 24.03.15The Armored Vehicle Navigation Systems Market size is estimated at USD 103.45 million in 2024, and is expected to reach USD 131.46 million by 2029, growing at a CAGR of 4.92% during the forecast period (2024-2029).

The increase in defense expenditure globally has propelled the armored vehicle navigation system market. The major economies, such as the United States, France, and Russia, and emerging economies, such as India and China, have surged their defense expenditures. These countries are heavily investing in the development and procurement of armored vehicles. Moreover, to give fleets increased battle ranges and combat effectiveness, substantial developments are being made in the field of armored vehicle navigation systems. Development and implementation of technologies, such as artificial intelligence and autonomous vehicle technology, are propelling the growth of the market for armored vehicle navigation systems.

Armored Vehicle Navigation Systems Market Trends

Inertial Navigation Systems to Exhibit the Highest Growth Rate

Major military forces across the world are increasing their efforts to improve the situational awareness of combat vehicle units on the battlefield, and this is leading to significant improvements in inertial navigation systems. The integration of satellite positioning systems with inertial navigation systems is propelling the growth of the global armored vehicle navigation systems market. Investments are being made to improve the existing inertial navigation technology that can work precisely in GPS-denied zones. Inertial navigation systems are safe and accurate, unlike GPS systems that are prone to jamming and spoofing. Development in sensor technology stands at the core of inertial navigation system development. For instance, in November 2023, Kebni AB, a Sweden-based firm, was awarded an order for a test unit of Kebni SensAItion inertial navigation systems (INS) from RV Connex as part of a new industrial cooperation. The order pertains to a test unit intended for the evaluation of navigational support in advanced applications.

The increasing use of sensors is fueling the weight- and space-reduction design of armored vehicle navigation systems. Sensors and Fiber Optic Gyros (FOG) reduce the instability of inertial navigation systems and make them more reliable. FOG systems are expected to witness a high growth rate during the forecast period, owing to their autonomous vehicle applications.

Asia-Pacific is Projected to Significant Growth During the Forecast Period

Asia-Pacific is home to major military powers, such as Japan, China, India, and South Korea, and these countries are significantly increasing their defense expenditures for the procurement and development of armored vehicles and armored vehicle navigation systems, owing to the rising border conflicts and terrorism in the region. The procurement of armored vehicles in the region has aided the demand for its navigation systems. For instance, in December 2022, the Japanese Ministry of Defense outlined a five-year plan for the procurement of Finnish company Patria's armored modular vehicles (AMVs) for the Japan Ground Self-Defense Force's (JGSDF's) wheeled armored personnel carrier (WAPC) program. The country has plans to procure 29 vehicles worth USD 176 million. Similarly, in September 2023, the Indian Ministry of Defense initiated the procurement of 170 armored recovery vehicles (ARVs) based on a tracked platform. These developments are expected to aid the market in the Asia-Pacific region.

Armored Vehicle Navigation Systems Industry Overview

The market for armored vehicle navigation systems is a semi-consolidated one, with a presence of major players, such as Honeywell International Inc., KVH Industries Inc., Safran SA, RTX Corporation, and BAE Systems PLC. The market is witnessing investments in innovations and the development of precise technology that can be offered at low, competitive rates. For revenue generation, major players aim to win contracts and deals from national governments and defense agencies. The market is expected to see growth, owing to the defense modernization and upgrade efforts by major economies around the world.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Armored Vehicle Type

- 5.1.1 Main Battle Tanks

- 5.1.2 Infantry Fighting Vehicle

- 5.1.3 Armored Personnel Carrier

- 5.1.4 Other Armored Vehicle Types (Tactical Truck, Bus, MRAP)

- 5.2 Navigation System

- 5.2.1 Inertial Navigation System

- 5.2.2 Satellite Navigation System

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Mexico

- 5.3.4.2 Brazil

- 5.3.4.3 Rest Of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Israel

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Safran SA

- 6.2.2 KVH Industries Inc.

- 6.2.3 Hertz Systems

- 6.2.4 Israel Aerospace Industries Ltd

- 6.2.5 Bharat Electronics Limited (BEL)

- 6.2.6 Advanced Navigation

- 6.2.7 Honeywell International Inc.

- 6.2.8 GEM elettronica

- 6.2.9 BAE Systems PLC

- 6.2.10 Northrop Grumman Corporation

- 6.2.11 THALES

- 6.2.12 RTX Corporation