|

시장보고서

상품코드

1437611

터보프롭 엔진 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2024-2029년)Turboprop Engine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

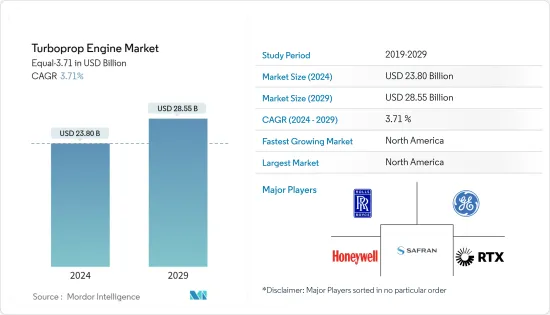

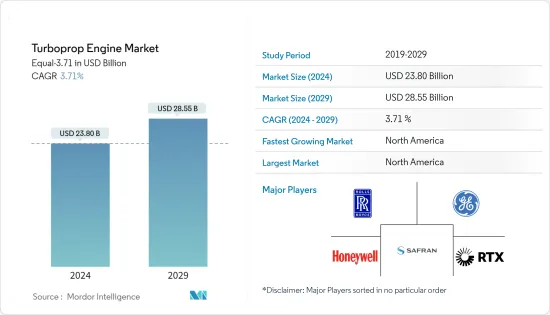

터보프롭 엔진 시장 규모는 2024년에 238억 달러로 추정되고 2029년까지 285억 5,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간(2024-2029년) 중 3.71%의 CAGR로 성장합니다.

새로운 지방 노선의 도입과 함께 민간 항공에서 터보프롭 엔진 탑재 항공기에 대한 관심이 높아지고 있습니다. 터보프롭 엔진은 단거리 및 저공비행에서 효율이 높아 민간 항공 분야의 성장에 기여하고 있습니다. 군용 및 일반 항공 분야에서 수요 증가는 주로 터보프롭 엔진을 장착한 새로운 항공기 모델의 도입에 기인합니다.

터보프롭 항공기 수요가 증가하고 있는 것은 새로 개발된 짧은 경로의 도입과 저고도 비행 능력, 그리고 비용 효율성 덕분입니다. 터보프롭 엔진 시장에서는 민간 항공 분야에서 인기가 높아지면서 하이브리드 유형이 우위를 점하고 있습니다. 또한 구형 항공기에 이러한 하이브리드 엔진이 개조되면서 터보프롭 엔진의 도입이 광범위하게 이루어지고 있습니다. 또한 새로운 항공기에는 이미 이 최신 터보프롭 엔진이 장착되어 있습니다.

터보프롭 엔진은 저공비행과 단거리 비행에서 효율성이 높고, 이륙과 착륙을 위해 최소한의 활주로 공간이 필요하며, 연료 효율을 향상시키는 것으로 입증되었습니다. 이러한 요소들은 개인에게 항공 여행을 보다 접근하기 쉽고 편리하게 만들어 터보프롭 엔진에 대한 시장 수요를 촉진하는 데 기여하고 있습니다.

터보프롭 엔진 시장 동향

일반 항공 부문은 예측 기간 중 큰 폭의 성장이 예상

최신 항공전자 및 성능면에서 기술적 진보를 갖춘 새로운 항공기 모델에 대한 수요가 증가함에 따라 여러 터보프롭 항공기 제조업체가 새로운 항공기를 개발하고 있습니다. 전 세계 부유층과 초부유층 인구 증가는 개인 여행에 대한 수요 증가의 촉매제 역할을하고 있으며, 이후 전 세계에서 터보프롭 항공기 조달을 촉진하고 있습니다. 예를 들어 2017-2022년 전 세계 부유층 인구는 83% 증가했습니다. 2022년 7월, Pratt & Whitney Canada는 PT6 E 시리즈 엔진 제품군의 새로운 엔진 모델을 발표했습니다. PT6E-66XT 엔진은 Daher의 최신 단발 터보프롭 비행기 TBM 960 전용으로 설계되었습니다.

2022년 1월, 캐나다의 프랫 앤 휘트니는 다이아몬드 에어크라프트가 신형 DART-750 항공기에 PT6A-25C 엔진을 선택했다고 발표했습니다. DART-750 항공기는 탄소섬유로 제작된 탠덤 터보프롭 연습기입니다. 따라서 특히 일반 항공 부문에서 신형 터보프롭 항공기에 대한 수요 증가는 터보프롭 엔진의 기술 혁신을 촉진할 것으로 예상되며, 예측 기간 중 시장 성장을 가속할 것으로 예상됩니다.

예측 기간 중 북미가 시장을 독점할 것으로 예상

북미는 2022년 터보프롭 엔진의 가장 큰 시장입니다. 또한 이 지역은 미국의 터보프롭 항공기에 대한 대규모 수요로 인해 예측 기간 중 가장 높은 CAGR로 성장할 것으로 예상됩니다. 일반 항공 분야에서는 북미가 2022년 터보프롭 항공기 인도량의 약 56%를 차지할 것으로 예상되며, 그 중 미국이 약 79%를 차지할 것으로 예상됩니다. 이 지역은 지역 항공기에 대한 수요 증가로 인해 민간 항공기 부문에서 새로운 터보프롭 항공기에 대한 수요를 창출하고 있습니다.

2039년까지 북미의 비즈니스 항공 및 민간 헬리콥터 부문은 79,000명의 조종사가 필요할 것으로 예상됩니다. 경제의 긍정적인 회복 추세와 비행 훈련 기관의 장비 확장 계획은 예측 기간 중 다른 카테고리의 성장을 가속할 것으로 예상됩니다. 북미에서는 2023-2028년까지 약 1,400대의 터보프롭 항공기가 인도될 것으로 예상됩니다.

2023년 11월, RTX의 프랫 앤 휘트니는 미국 국방부 물류청으로부터 B-52와 E-3에 동력을 공급하는 TF33 엔진에 대해 최대 8억 7,000만 달러 상당의 계약을 체결했습니다. 이러한 유형의 개발은 2023년 동안 터보프롭 엔진 시장 수요를 촉진할 것입니다. 북미 예측 기간.

터보프롭엔진 산업 개요

터보프롭 엔진 시장은 통합되어 있으며, 몇몇 터보프롭 엔진 OEM 업체가 시장 점유율의 대부분을 차지하고 있습니다. RTX Corporation, Rolls-Royce plc, Safran, General Electric Company, Honeywell International, Inc. 엔진 제조업체와 OEM은 제품과 서비스를 제공하기 위해 장기 계약을 체결하고 있습니다. 신규 시장 진출기업가 시장에 진입하고 유지하기가 어렵습니다. 적층 가공와 같은 첨단 기술 연구개발에 대한 막대한 투자와 엔진 생산 속도를 높이기 위한 자동화 및 AI 도입은 기업의 생산 능력 향상에 도움이 되어 예측 기간 중 성장을 가속할 것으로 예상됩니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 촉진요인

- 시장 억제요인

- Porter's Five Forces 분석

- 신규 진출업체의 위협

- 구매자의 교섭력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업간 경쟁의 강도

제5장 시장 세분화

- 응용

- 민간 항공기

- 군용기

- 일반 항공용 항공기

- 지역

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 기타 라틴아메리카

- 중동 및 아프리카

- 아랍에미리트

- 사우디아라비아

- 이스라엘

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 개요

- RTX Corporation

- Rolls-Royce plc

- Safran

- General Electric Company

- Honeywell International, Inc.

- MTU Aero Engines AG

- PBS AEROSPACE Inc.

- Motor Sich JSC

- TUSAS Engine Industries, Inc.

제7장 시장 기회와 향후 동향

KSA 24.03.07The Turboprop Engine Market size is estimated at USD 23.80 billion in 2024, and is expected to reach USD 28.55 billion by 2029, growing at a CAGR of 3.71% during the forecast period (2024-2029).

The preference for turboprop engine-powered aircraft in commercial aviation is growing with the introduction of new regional routes. The turboprop engines are highly efficient in short-distance and low-altitude flying, which is helping their growth in the commercial aviation sector. In the military and general aviation segments, the growth in demand is mainly due to the introduction of new aircraft models that are powered by turboprop engines.

The increrasing demand of turboprop aircraft are due to the introduction of newly developed shorter routes and the ability to fly at low altitudes, coupled with cost efficiency. Within the turboprop engine market, the hybrid variety holds dominance owing to its increasing popularity in the civil aviation sector. Furthermore, the deployment of turboprop engines is extensive as older aircraft are retrofitted with these hybrid engines. In addition, newer aircraft are already equipped with this modern turboprop engine.

The turboprop engines prove to be highly efficient in low altitude flying, short distance travel, requiring minimal airstrip space for take-off and landing, and enhancing fuel efficiency. These factors contribute to making air travel more accessible and convenient for individuals, thereby driving the market demand for turboprop engines.

Turboprop Engine Market Trends

General Aviation Segment is Expected Witness Significant Growth During the Forecast Period

With the growth in demand for newer aircraft models featuring the latest avionics and technological advancements in terms of performance, several turboprop aircraft manufacturers are developing new aircraft. Growth in the HNWI and UHNWI populations globally is acting as a catalyst for the increased demand for private travel, subsequently driving the procurement of turboprop aircraft globally. For instance, from 2017 to 2022, the HNWI population increased by 83% globally. In July 2022, Pratt & Whitney Canada announced a new engine model for its PT6 E-Series engine family. The PT6E-66XT engine is purpose-built for Daher's latest single-engine turboprop airplane, the TBM 960.

In January 2022, Pratt & Whitney Canada that Diamond Aircraft had selected the PT6A-25C engine for its new DART-750 aircraft. DART-750 aircraft is an all-carbon fiber tandem turboprop trainer aircraft. Thus, the growth in demand for newer turboprop aircraft, especially in the general aviation segment is expected to drive the innovations in turboprop engines which is expected to help the market growth during the forecast period.

North America Projected to Dominate the Market During the Forecast Period

North America is the largest market for Turboprop Engines in 2022. The region is also expected to grow with the highest CAGR during the forecast period, due to large-scale demand for turboprop aircraft from the United States. In the General Aviation segment, North America alone accounted for about 56% of the turboprop aircraft deliveries in 2022 in which the U.S. has having contribution of around 79%. The region is also generating demand for new turboprop aircraft in the commercial aircraft segment, with the growth in the demand for regional aircraft.

It is expected that by 2039 there will be a requirement of 79,000 pilots in the business aviation and civil helicopter sector in the North American region. The positive economic recovery trend along with the fleet expansion plans of flight training institutes is expected to aid the growth of other categories during the forecast period. It is expected around 1,400 turboprops will be delivered during 2023-2028 in North America.

In November 2023, RTX's Pratt & Whitney received a contract valued up to USD 870 million for TF33 engines powering B-52s, and E-3s by the Defense Logistics Agency of the U.S. Such kind of development will drive the demand for turboprop engine market during the forecast period in North America.

Turboprop Engine Industry Overview

The turboprop engine market is consolidated, with the presence of a few turboprop engine OEMs which occupy a majority of the market share. Some of the prominent players in the market are RTX Corporation, Rolls-Royce plc, Safran, General Electric Company, and Honeywell International, Inc. The engine manufacturers and OEMs enjoy long-term contracts, for providing products and their services, thereby, making it difficult for new players to enter and sustain in the market. Significant investment into R&D of advanced technologies like additive manufacturing and incorporation of automation and AI to increase the production rate of the engines are expected to help the players to ramp up their production capacity, thereby, helping their growth during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porters Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Commercial Aircraft

- 5.1.2 Military Aircraft

- 5.1.3 General Aviation Aircraft

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Israel

- 5.2.5.4 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 RTX Corporation

- 6.2.2 Rolls-Royce plc

- 6.2.3 Safran

- 6.2.4 General Electric Company

- 6.2.5 Honeywell International, Inc.

- 6.2.6 MTU Aero Engines AG

- 6.2.7 PBS AEROSPACE Inc.

- 6.2.8 Motor Sich JSC

- 6.2.9 TUSAS Engine Industries, Inc.