|

시장보고서

상품코드

1437951

세계 조영제 주입기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2024-2029년)Contrast Media Injectors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

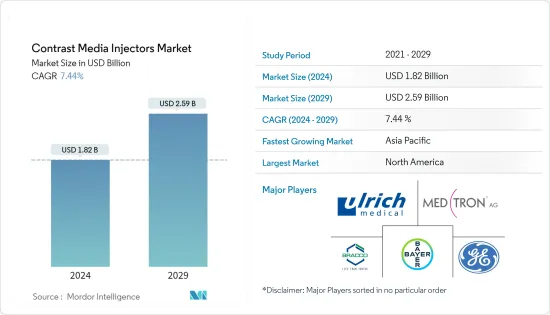

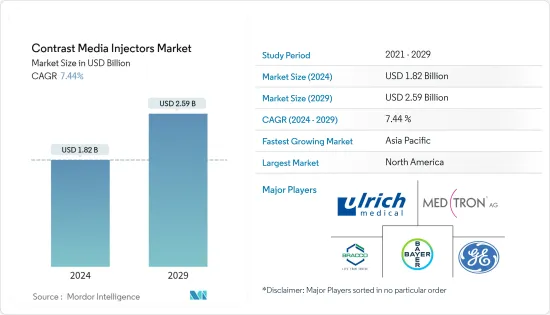

조영제 주입기 시장 규모는 2024년에 18억 2,000만 달러로 추정되며, 2029년까지 25억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 7.44%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

COVID-19 감염의 유행은 세계 인구의 건강에 치명적인 영향을 미치며 대부분의 국가에 중대한 경제적 영향을 미칩니다. 많은 방사선과에서의 영상 진단 건수는 극적으로 감소했습니다. 신형 코로나바이러스 감염(COVID-19)의 유행으로 환자는 구명 영상 진단을 기다려야 했고 건강 관리 시설에 대한 접근에 영향을 주었습니다. 유행은 환자가 이미지 검사를 받기까지의 대기 시간을 늘렸습니다. 2020년 4월에 북미가 발표한 기사에 따르면, 신형 코로나 바이러스 감염(COVID-19)의 유행은 미국의 방사선 의학 실천에 큰 영향을 미쳤습니다. 조영제 주입기 수요는 주로 이미징의 양과 설치된 CT 및 MRI 장치의 수에 의해 결정됩니다. 기준 완화와 백신 접종 프로그램의 시작으로 조영제 주입기 시장이 회복되었습니다.

조영제 주입기 시장 성장의 주요 요인은 낮은 침습 수술에 대한 수요 증가, 기술 진보 및 규제 당국의 승인 증가입니다. 조영제 주입기 기술은 조영제의 낭비를 줄이고 환자가 받은 복용량에 대한 데이터 수집을 자동화하기 위해 몇 가지 진전을 이루었습니다. 예를 들어, 자동 주입기 시스템은 사용된 조영제의 양을 정확하게 수집합니다. 공급업체는 EMR 또는 이미지 아카이브 통신 시스템(PACS)에서 얻은 정보를 사용하여 환자에게 맞는 복용량을 제공합니다. 조영제 낭비를 줄이기 위한 진전 중 하나는 주사기없는 주입기입니다.

2021년 7월 WHO의 최신 정보에 따르면, 심혈관 질환(CVD)은 세계 사망의 1위입니다. 매년 예상 1,790만 명이 심혈관 질환으로 고통받고 있습니다. 심혈관 질환으로 인한 사망의 5명 중 4명은 뇌졸중과 심장 발작으로 인한 것이며, 사망의 3분의 1은 70세 미만의 조기 사망입니다. 마찬가지로 WHO 2021 팩트 시트에 따르면 만성 질환으로도 알려진 비감염성 질환(NCD)은 매년 약 4,100만 명의 사망의 원인이 되며, 이는 전국적으로 기록된 총 사망자 수의 약 71%에 해당합니다. 세계. 같은 출처에 따르면 매년 세계 30세에서 69세까지 1,500만 명 이상이 NCD에 의해 사망합니다. 따라서 NCD에 의한 사망률이 높아 진단 절차 수요가 증가하고 있습니다. 낮은 침습 수술은 전통적인 수술에 비해 많은 장점이 있기 때문에 주목을 받고 있으므로 조영제 주입기 수요가 증가할 것으로 예상됩니다.

대부분의 기업은 조영제 낭비를 줄이고 경쟁 우위를 얻기 위해 혁신적인 제품을 개발하고 있습니다. Bracco는 시스템에 로드된 조영제를 한 방울 남기지 않고 사용하여 최대한의 경제성을 실현할 수 있는 스마트한 주사기 없는 주입기를 개발했습니다. 스마트 주입기는 주입량과 사용된 이미징 프로토콜을 기록하고 이 정보를 PACS로 전송합니다. 미디어 주입기 기술과는 대조적으로, 이러한 끊임없는 기술의 발전은 예측 기간 동안 시장을 밀어올릴 것으로 예상됩니다.

그러나 조영제 주입기의 높은 비용과 조영제의 부정적인 영향으로 예측 기간 동안 시장 성장이 급감할 것으로 예상됩니다.

조영제 주입기 시장 동향

CT 주입기 시스템 부문은 주입기 부문에서 높은 CAGR을 나타낼 것으로 예상

지난 몇 년동안 CT 시스템의 사용이 증가했기 때문에 CT 주입기는 긍정적인 성장이 예상됩니다. 이 CT 시스템은 이미징 중 첫 번째 및 후속 조영제 투여를 위해 두 개의 주사기가있는 듀얼 헤드 주입기를 사용합니다. 주요 학술 센터 및 제약 회사는 CT 사용자가 새로운 이미징 시스템의 고급 기능을 활용할 수 있도록 프로토콜을 개발하기 위해 지속적인 R&D 활동을 수행하고 있습니다.

주요 기업은 시장에서 경쟁력을 유지하기 위해 협력적인 노력과 같은 다양한 전략을 점진적으로 수행하고 있습니다. 예를 들어 Bayer Korea는 2022년 5월 컴퓨터 단층촬영(CT) 주입 의료기기 'MEDRAD Centargo' 판매를 시작해 1월에 식품의약품안전처 승인을 받았다고 발표했습니다. 마찬가지로 독일의 의료기술 기업인 Ulrich Medical은 2020년 5월 시카고에서 개최된 RSNA에서 미국 시장용으로 설계된 이 회사의 CT 모션 조영제 주입기 버전을 발표했습니다. 이 제품은 FDA에 의해 승인되었으며 GE Healthcare와 협력하여 판매되었습니다.

이러한 요인은 예측 기간 동안 시장 성장을 긍정적으로 끌어올릴 것으로 예상됩니다.

북미는 시장에서 중요한 점유율을 유지하고 예측 기간 동안 성장 추세를 지속할 것으로 예상

북미는 주로 낮은 침습 처치에 대한 선호도 증가와 라이프 스타일 변화로 인한 만성 질환의 유병률 증가로 인해 예측 기간 동안 전체 시장을 지배할 것으로 예상됩니다. 미국은 이 지역에서 가장 큰 시장 점유율을 차지합니다.

2021년 5월에 갱신된 CDC 데이터에 따르면, 심장병, 암, 당뇨병 등의 만성 질환이 미국에서 사망 및 장애의 주요 원인이 되고 있습니다. 또한 연간 3조 8,000억 달러의 헬스케어비에 기여하고 있습니다. 이 나라의 성인 10명 중 6명이 만성 질환을 앓고 있으며, 10명 중 4명이 2개 이상의 만성 질환을 앓고 있습니다.

또한, 심장병 및 뇌졸중 통계 사실 시트 2020에 따르면, 미국에서는 매년 적어도 40,000명의 유아가 선천성 심장 질환을 앓을 것으로 예상됩니다. 약 25%, 즉 2.4명(출생 1,000명당)이 생후 1년 이내에 치료가 필요합니다.

조영제 주입기 장비의 기술 진보, 주요 기업의 지출 증가, 규제 당국의 승인 증가도 북미 조영제 주입기 시장의 성장을 뒷받침하고 있습니다.

조영제 주입기 산업 개요

조영제 주입기 시장은 통합되고 경쟁적이며 소수의 주요 기업으로 구성됩니다. 시장 점유율 측면에서 현재 시장을 독점하는 대기업은 거의 없습니다. 기술의 진보, 질병의 확산, 낮은 침습 수술 증가에 따라 향후 몇 년동안 더 많은 기업이 시장에 진입할 것으로 예상됩니다. 시장의 주요 기업은 Bracco Group, GE Healthcare, Bayer Healthcare, Medtron AG 및 Ulrich GmbH & Co. KG입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 저침습 수술 수요 증가

- 기술의 진보와 규제 당국의 승인수 증가

- 시장 성장 억제요인

- 조영제 주입기의 높은 비용

- 조영제의 악영향

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체 제품의 위협

- 경쟁 기업간 경쟁 관계의 격렬

제5장 시장 세분화

- 제품별

- 주입기 시스템

- CT 주입기 시스템

- MRI 주입기 시스템

- 심장혈관/혈관조영용 주입기 시스템

- 소모품

- 튜브

- 주사기

- 기타 소모품

- 주입기 시스템

- 주입기 유형별

- 싱글 헤드 주입기

- 듀얼 헤드 주입기

- 시린지리스 주입기

- 용도별

- 방사선과

- 인터벤션 심장학

- 기타 용도

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 남은 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Bracco Group

- Guerbet Group

- Medtron AG

- Bayer HealthCare LLC

- ulrich GmbH & Co. KG

- Nemoto Kyorindo Co. Ltd

- GE Healthcare(GE Company)

- Hilin Life Products

- Sino Medical-Device Technology Co. Ltd

- APOLLO RT Co. Ltd

- Shenzen Seacrown Electromechanical Co. Ltd

- Shenzhen Anke High-tech Co. Ltd

제7장 시장 기회와 미래 동향

JHS 24.03.08The Contrast Media Injectors Market size is estimated at USD 1.82 billion in 2024, and is expected to reach USD 2.59 billion by 2029, growing at a CAGR of 7.44% during the forecast period (2024-2029).

The COVID-19 pandemic has had a devastating impact on the global population's health and a significant economic impact on most countries. The volume of imaging cases in many radiology departments dropped dramatically. The COVID-19 outbreak impacted patients' access to healthcare facilities as the pandemic forced them to wait for lifesaving imaging procedures. The pandemic also increased the waiting time for patients to have their imaging done. According to an article published by the Radiology Society of North America in April 2020, the COVID-19 pandemic profoundly impacted radiology practices across the country. The volume of diagnostic imaging and the number of CT and MRI machines installed will primarily determine the demand for contrast injectors. The easing of norms and the start of vaccination programs led to a recovery in the contrast media injectors market.

The major factors attributed to the growth of the contrast media injectors market are increasing demand for minimally invasive surgeries, technological advancements, and increasing regulatory approvals. Several advancements in contrast media injector technology have been made to reduce contrast media waste and automate data collection regarding the dose received by a patient. For example, the automated injector systems precisely collect the amount of contrast media used. Vendors offer personalized doses to patients, using the information pulled from EMR or picture archiving and communication systems (PACS). One such advancement in reducing contrast media waste is syringeless injectors.

According to the WHO updates from July 2021, cardiovascular diseases (CVDs) are the number one cause of death globally. An estimated 17.9 million each year suffer from cardiovascular diseases. Four out of five cardiovascular deaths are due to strokes and heart attacks, and one-third of deaths occur prematurely in people under 70 years. Similarly, according to the WHO 2021 fact sheet, non-communicable diseases (NCDs), also known as chronic diseases, are responsible for the death of about 41 million people each year, which was about 71% of the total deaths recorded all over the world. As per the same source, every year, over 15 million people aged between 30-69 years die due to NCDs across the world. Thus, due to the high burden of mortality due to NCDs, the demand for diagnostic procedures is increasing. As minimally invasive procedures have more advantages over traditional procedures, they are gaining traction, and thereby, the demand for contrast media injectors is expected to increase.

Most companies are developing innovative products to reduce contrast media waste and gain a competitive advantage. Bracco has developed smart syringeless injectors, which can use every drop of contrast loaded into the system for maximum economy. Smart injectors record the amount injected and the imaging protocol used and send the information to the PACS. These constant technological advancements in contrast to media injector technology are expected to boost the market during the forecast period.

However, the high cost of contrast media injectors and adverse effects of contrast agents are expected to plummet the growth of the market over the forecast period.

Contrast Media Injectors Market Trends

The CT Injector Systems Segment is Expected to Record a High CAGR in the Injectors Segment

CT injectors are expected to grow positively as the usage of CT systems has increased over the past few years. These CT systems use a dual-head injector with two syringes for initial and follow-up contrast doses during imaging. There has been constant R&D activity by major academic centers and pharmaceutical companies to develop protocols that help CT users with the advanced capabilities of newer imaging systems.

Major players are gradually implementing various strategies, such as collaborative initiatives, to remain competitive in the market. For example, In May 2022, Bayer Korea said it had started marketing MEDRAD Centargo, a computed tomography (CT) injection medical device, which received approval from the Ministry of Food and Drug Safety in January. Similarly, Ulrich Medical, a German medical technology company, presented a version of its CT motion contrast media injector designed for the American market at the RSNA in Chicago in May 2020. It was approved by the FDA and marketed in collaboration with GE Healthcare.

Such factors are expected to boost the market's growth over the forecast period positively.

North America is Expected to Hold a Significant Share in the Market and Continue the Growth Trend During the Forecast Period

North America is expected to dominate the overall market during the forecast period, primarily due to the increasing preference for minimally invasive procedures and the increasing prevalence of chronic diseases due to changing lifestyles. The United States holds the largest market share in the region.

According to the CDC data updated in May 2021, chronic diseases such as heart disease, cancer, and diabetes are the leading causes of death and disability in the United States. They also contribute to USD 3.8 trillion in annual healthcare costs. Six in 10 adults in the country have a chronic disease, and four in every 10 have two or more chronic diseases.

Additionally, according to Heart Disease & Stroke Statistical Fact Sheet 2020, a minimum of 40,000 infants are expected to be affected yearly by congenital heart defects in the United States. About 25% or 2.4 (per 1,000 live births) require treatment in the first year of an infant's life.

Technological advancements in contrast media injector devices, increasing expenditure by key players, and rising regulatory approvals are also boosting the growth of the contrast media injectors market in North America.

Contrast Media Injectors Industry Overview

The contrast media injectors market is consolidated, competitive, and consists of a few major players. In terms of market share, few major players currently dominate the market. With increasing technological advancements, the high prevalence of diseases, and the increasing usage of minimally invasive surgeries, more companies are expected to enter the market in the coming years. Major players in the market are Bracco Group, GE Healthcare, Bayer HealthCare, Medtron AG, and Ulrich GmbH & Co. KG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Minimally Invasive Surgeries

- 4.2.2 Technological Advancements and Increasing Number of Regulatory Approvals

- 4.3 Market Restraints

- 4.3.1 High Cost of Contrast Media Injectors

- 4.3.2 Adverse Effects of Contrast Agents

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Products

- 5.1.1 Injector Systems

- 5.1.1.1 CT Injector Systems

- 5.1.1.2 MRI Injector Systems

- 5.1.1.3 Cardiovascular/Angiography Injector Systems

- 5.1.2 Consumables

- 5.1.2.1 Tubing

- 5.1.2.2 Syringe

- 5.1.2.3 Other Consumables

- 5.1.1 Injector Systems

- 5.2 By Type of Injectors

- 5.2.1 Single-head Injectors

- 5.2.2 Dual-head Injectors

- 5.2.3 Syringeless Injectors

- 5.3 By Application

- 5.3.1 Radiology

- 5.3.2 Interventional Cardiology

- 5.3.3 Other Applications

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle-East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Bracco Group

- 6.1.2 Guerbet Group

- 6.1.3 Medtron AG

- 6.1.4 Bayer HealthCare LLC

- 6.1.5 ulrich GmbH & Co. KG

- 6.1.6 Nemoto Kyorindo Co. Ltd

- 6.1.7 GE Healthcare (GE Company)

- 6.1.8 Hilin Life Products

- 6.1.9 Sino Medical-Device Technology Co. Ltd

- 6.1.10 APOLLO RT Co. Ltd

- 6.1.11 Shenzen Seacrown Electromechanical Co. Ltd

- 6.1.12 Shenzhen Anke High-tech Co. Ltd